Leaderboard

Popular Content

Showing content with the highest reputation since 04/24/2021 in all areas

-

Updated June 1, 2026 An update of my book/collection of posts on Fairfax is attached below. New posts have been added. The book now has ~950 pages of material on Fairfax. My goal is not size - but I will continue to add material that I think adds value for those interested in learning more about Fairfax. I don't re-read the entire document when I post updated versions. If you see any big errors please let me know. Please note, not everything in the book has been brought up to date. That would have required a couple of months of work… and by the time it was done, much of it would be out of date again. My current plan is to keep updating parts of the document as time goes by. Bottom line, this document should be a much better resource for board members / investors than what existed before. I hope you find it useful. --------- For members who enjoy reading my posts on Fairfax I have attached at the bottom of this post two documents: Fairfax - The Emergence of a Wonderful Company: PDF file contains more than 100 of my best posts on Fairfax from over the past 2 years, organized into 20 chapters. Excel workbook: Companion document to the PDF file, contains 14 worksheets (see below for details). Sanjeev, thanks for everything you do running this board. For all the members on this investing forum, ‘thank you’ for breaking bread on a daily basis and sharing your thoughts on investing and life. Over the years, it has been a life changing experience for me and my family. What is contained in this document is the collective wisdom of this group. Let’s hope i have captured it reasonably well. A message from the legal department: Both documents are incomplete and contain errors. What is contained in the attached documents is not intended to be investing/financial advice. Its purpose is to educate and entertain. ----------- The Excel file contains 14 worksheets: FFH-24: lists and tracks many of Fairfax's equity holdings in real time Size: ranking of Fairfax's equity holdings by size Moves: detailed compilation of many on Fairfax's transactions going back to 2010 - organized by year Earnings Estimate: 2025 and 2026 Premiums: the build for 'underwriting profit' Interest: the build for 'interest and dividend income' Associate Equities: the build for 'share of profit of associates' Consolidated Equities: Non-insurance Consolidated Companies Investments: the build to calculate the return on the total investment portfolio Shares: reviews 'effective shares outstanding' Excess of Fair Value over Carrying Value: for the non-insurance associate and consolidated holdings Float: the build for float 13yr View: A 13 year view of many key metrics for Fairfax IFRS 17: Effects of discounting and risk adjustment - quarterly summary of historical numbers used in earnings forecast Fairfax May 2026 -compressed.pdf Fairfax May 2026.xlsx3 points

-

Every month I get with my wife to review our financial situation. This month the of Crip-Family net worth was not impressive, and when returns are compared against the S&P, it looks even worse. I gave her the low down, specifically, that Fairfax really killed our returns YTD and in May especially. She asked "What happened with Fairfax?"...response was "Not a damn thing, literally no bad news". This is instructive...company moves notably lower with, from what I can see, zero reason. Yes, it is frustrating to see the impact on the net worth, this is the kind of thing we live for...company getting better and price getting cheaper. We have been buying on the way down, but hindsight says we should have waited a little longer. -Crip2 points

-

We need to change the title to ‘Fairfax Stock - New 52-week Low’

2 points

2 points -

Thanks for the advice. I do have fond memories of camping with my Dad. I remember once while camping he wanted to listen to a soccer match and took out his Grundig short wave, looked at the specs in the manual and figured out that he needed a 20 foot antennae to get the game. He attached wire to the antennae and attached it to a couple of trees that my brother and I climbed up to get it high enough.

2 points

-

Check out my most recent article for the Globe and Mail about Fairfax. This is a gift article. https://www.theglobeandmail.com/gift/b04eb1bcd666173196423362ad31a8785d529ba1ad1cee14b25891c6ca2ccfbf/AKS47ZLUWZFSXEKQVGUNGOWYCU/2 points

-

Good question, @Viking…and the answer has to be that it is much better for Fairfax to buy out minority owners of the high quality insurers they already know and trust than to pay higher multiples for partial or total ownership of insurers that might be acquisition targets in external markets, but of whose management and reserving practices they are not as familiar with. Think back to when Buffett owned half of GEICO’s common stock, and had to pay a market price plus a premium to gain full ownership of the company whose reserving practices and operational and investment management were all known and trusted by him. Fairfax is in an even better position than Buffett was given the prices at which they are able to take out their trusted minority partners. And if for some reason Fairfax stock looks to be an even better investment than buying out minority partners, we can trust that Fairfax will find a way to balance their reinvestment opportunities as they did when they sold 10% of Odyssey to enable a Fairfax stock buyback. I think we can all agree that doing that was better for us as remaining shareholders than if they had borrowed funds externally (probably at an even higher cost?) and used it to take out some minority interests instead. Bottom line, I don’t need Fairfax to make the exact reinvestments that I, with my lack of direct knowledge of their opportunity set, think they should make. They have more than earned my trust that they will continue to treat me as a partner and that the reinvestment decisions they make in the future will be those that are likely to benefit us both.2 points

-

Met Ben Watsa at a Europe value investor conference. Asked him why Fairfax was short duration at high rates. Mostly comes down to protecting the downside as they see potential for an inflationary spike.2 points

-

Fairfax Q2-2025 Earning Results - 7 High-Level Thoughts I thought this would be a good time to get out of the weeds. Instead, with our review of Q2 results at Fairfax, we are going to zoom out today and look at the big picture. What did we learn about Fairfax from their Q2, 2025 results? Let me know if you agree/disagree with my list. What did I miss? 1.) Fairfax has a very good P/C insurance business Combined ratio = 93.3% Underwriting profit = $427 million Net premiums written growth = 4.8% Yes, the hard market is slowing. Top line growth in insurance is slowing. Nice to see that Fairfax is being disciplined (although Mr. Market will probably not like it). However, Fairfax will be able to continue to grow their P/C insurance business at above average rates - in addition to growth of NPW - by taking out their minority partners (see comment 5 below). 2.) Fairfax’s most important income stream spiked higher in Q2 Interest and dividend income = $666 million (was $606.5 million in Q1) Increasing by 10% in one quarter is a big deal. This puts the annual number at about $2.6 billion. It increased because the total investment portfolio continues to grow in size. And Fairfax continues to invest it very well. Yield of fixed income portfolio = 5.1% (same as Q1) Average duration of fixed income portfolio = 2.4 years (down from 3.3 in Q1) Fairfax also reduced the average duration of its fixed income portfolio from 3.3 to 2.4 years. They sold U.S. treasury bonds with maturities principally between 28 to 30 years for net proceeds of $1,129.2. Why? Probably because investors are not being compensated appropriately for the inflation risk on long dated US Treasuries. This is prudent risk management on the part of Fairfax - protect the balance sheet. Will analysts hate this move - because it reduces ‘visibility’? Probably. But analysts are focussed on the short term. Fairfax is running the business for the long term - and shareholders should applaud that. 3.) A new income stream is breaking out for Fairfax Fairfax already has 4 large income streams: underwriting profit, interest and dividend income, share of profit of associates and investment gains. The fifth income stream is non-insurance consolidated equity holdings. In recent years Fairfax has been investing heavily in this bucket of equity holdings. Since 2022, it has added Recipe, Grivalia Hospitality, Sleep Country, Meadow Foods and Peak Achievements. To go with legacy holdings AGT Food Ingredients, Dexterra and Sporting Life. I have been (impatiently) waiting 2 years for this bucket of equities to start delivering bottom line results that are in line with its potential - and it appears we might be there. Q2 = $126 million This puts the annual number at about $500 million. This is an important emerging income stream for Fairfax. My guess is it will be Fairfax’s fastest growing income stream moving forward - especially with the hard market in insurance slowing (capital will go to where it earns the best return). And yes, results for this group will have some volatility. 4.) Fairfax (and the team at Hamblin Watsa) continues to invest exceptionally well We got two important updates on the conference call today regarding a couple of Fairfax’s largest investments in recent years. PacWest construction loan portfolio In June of 2023, Kennedy Wilson and Fairfax purchased a $4 billion construction loan portfolio from PacWest. PacWest was caught in the regional bank crisis and they were forced to sell their best assets at a discount. (Of note, Kennedy Wilson also got the loan platform from Pac West - the 40 people who were running the loan portfolio also moved over the Kennedy Wilson.) We got an update today on how this investment has been performing for Fairfax over the past three years. Wade Burton, CIO and VP of Hamblin Watsa on the Fairfax conference call today: “Within the fixed income portfolio, our mortgages continue to perform well. We have been repaid on $1.8 of mortgages from the Pacific Western Bank transaction, where we purchased approximately $4 billion in commitments at 95% of par in 2023. The IRR on the loans repaid thus far is 14.7%. Thanks to the outstanding work of Bill McMorrow, Matt Windisch and their team at Kennedy Wilson, these mortgages are proving to be a fantastic investment for Fairfax.” Blizzard Vacatia (Berkley Group) One of Fairfax’s largest investments in 2025 (January) was the purchase of the Berkley Group, one of the largest independent timeshare companies in the US. With this deal, Fairfax partnered with Caroline Shin and her team at Vacatia. The partnership is called Blizzard Vacatia. Fairfax invested $810 million in various fixed income instruments (with an average yield of 8.6%) and $25 million in equity (50% ownership position). We got an update today on how this investment has been performing for Fairfax YTD. Wade Burton, CIO and VP of Hamblin Watsa on the Fairfax conference call today: “It’s early days in the timeshare investment, Berkeley, run by Caroline Shin, but so far, it has exceeded expectations. Berkeley has approximately 125,000 available room nights per month. They started the year at virtually nil occupancy for overnight stays. In month one, Caroline brought that number to 10%, the next month 20%, and the third month 35%. I’m happy to report year to date operating income has already reached our full year expectations. Again, outstanding and capable partners doing an excellent job for Fairfax shareholders.” 5.) Fairfax telegraphed how it will continue to grow its P/C insurance business - even as the hard market slows Minority interests own stakes in Fairfax’s two largest P/C insurance companies: Allied World = 16.6% Odyssey Re = 9.9% As a result, not all of the earnings from these two companies are accruing to Fairfax common shareholders. Taking out the minority shareholders will be an easy way for Fairfax to grow its P/C insurance business - it will boost the total amount of earnings that accrue to its common shareholders. On the Q2 conference call Fairfax confirmed that it would like to take out its minority partners in its two insurance businesses. They will likely to this in two steps: Allied World later this year (my best guess) and Odyssey in 2026 (or perhaps 2027). The timing will likely be determined by the opportunity set that exists in financial markets in general. If a better capital allocation opportunity comes along, perhaps they will delay taking out minority partners. Because of the call option feature (put in place when the deals were initially struck), Fairfax is able to buy out the minority partners at a very favourable price. As a result, these transactions are high certainty, solid return uses of capital for Fairfax. Taking out minority partners will be a way for Fairfax to grow its bottom line (the part that accrues to its common shareholders) even if the hard market slows further in the coming years. Brilliant planning and execution on the part of Fairfax. 6.) Economic results are much better than accounting results Excess of fair value over carrying value for associate and consolidated holdings increased from $1.4 billion to $2.4 billion, or $111/FFH share (pre-tax). The increase in the quarter was $1 billion, or $46/share pre-tax. This amount is not captured in Fairfax’s reported results (EPS, BV or ROE). This puts the economic value created by Fairfax in Q2 at about $97 share (EPS of $62 plus excess of FV over CV of $35). 7.) Fairfax is exceptionally well positioned today With $3 billion in cash to the holding company, Fairfax is all cashed up. The insurance subs are also overcapitalized (by about $3 billion) - with the hard market slowing, this is another chunk of money that could be sent as a dividend to Fairfax to be redeployed elsewhere. Fairfax is also generating about $1 billion in earnings each quarter. Fairfax has built an earnings juggernaut. Importantly, it is just getting started. Compounding is just starting to kick in… This is resulting in exponential growth. This is very hard for investors to grasp (humans think linearly). This will likely cause investors to underestimate future earnings - and that is what we have seen in each of the past 4 years (like a dog chasing its tail, earnings estimates for Fairfax have consistently been too low and subsequently keep getting revised higher). Fairfax has spent the last 39 years building out its investment management business. It has an amazing range of internal capabilities. This will allow the company to be very nimble and opportunistic moving forward. At the same time, Fairfax has developed a large number of relationships with external capital allocators. Fairfax is viewed as being trustworthy and desirable partner. This is resulting in deal flow - Fairfax’s phone is ringing. Volatility is back. Interest rates have normalized. The macro environment is highly uncertain (tariffs being just one factor). Volatility is a wonderful thing for a value investor like Fairfax - it gives them the opportunity to deploy capital at very attractive rates of return. And Fairfax is on a ‘hot streak’ (a reference to Stanley Druckenmiller). For the past 5 years the team at Fairfax has been executing exceptionally well. ‘They are seeing the ball really well…’2 points

-

I went on a podcast and spoke mostly about Fairfax. https://t.co/x7v5g2OvGf2 points

-

This is one of my favorite things to rant about so let me apologize in advance. This isn't a comment about Brett Horn in particular - I don't know him, and maybe he's great. But what I strongly recommend is to look to the broker analysts as a gauge of popular sentiment (if even that) or to understand how brokers drum up business. Nothing more. It is not a coincidence that companies reliant on capital raising tend to get the widest coverage and the best ratings. But since the ostensible separation of research from investment banking (and the removal of skin in the game - analysts ability to actually buy stocks in their coverage universe - in the name of removing conflicts of interest), the job is basically a glorified sales job for trading volumes. And many of them, if they do get a real nugget of information or have an actual insight, share it behind closed doors with whichever client trades the most through their bank. In other words... I wouldn't think that hard about it. The analyst incentive is to not stand out in a bad way and keep making ~$1-2mm/year to keep their kids in fancy schools. Even if one is actually bearish, he/she almost certainly won't stick his/her neck out and risk embarrassment and losing that cushy gig. Sorry, I've done that job as a bright eyed and bushy tailed junior analyst and unfortunately saw how the sausage is made, so maybe I'm too cynical now. Maybe the general takeaway is to keep your expectations low and allow yourself be pleasantly surprised, but the clear and simple fact is that @Viking and others with real insight and skin in the game do a 10x better job than any broker analyst. Maybe this wasn't the case in Lee Cooperman's days at GS (though it was probably even sketchier then) but it is now. At the bare minimum, the pay and prestige aren't what they used to be. The real talent is elsewhere. Expect the sell side estimates to keep climbing higher as Fairfax executes.2 points

-

I once saw a cheers-less post. Gregmal was being disciplined over in the Disney thread…2 points

-

@newtovalue you are welcome. Nice to hear that others find value in some of the posts. I use writing as a way to get my thoughts in order. And i love it when people take the other side as i spend a fair bit of time trying to figure out why i am wrong. I think my track record is pretty decent figuring out the earnings part of the equation. I am pretty terrible at figuring out the multiple expansion part of the equation (i tend to sell my big positions too early).2 points

-

FFH. Looks cheap. Anyone follow it?1 point

-

@mananainvesting , that is a great graphic description of what has been going on...1 point

-

Thank you very much; what a great idea! So at todays valuation and applying 2025 numbers, MKL ($1983) has a roughly 25% discount to IV and FFH ($1638) even a bit over 50% to IV (I used the $3348 from the pdf). So taking into account the IV numbers of the "orange and blue concept" of Tom Gayner - when would both be fully valued? If MKL would rise 33% tomorrow to a pb ratio of 1.8 (BVPS is $1476 end of 2025) it would be fully valued. FFH (BVPS $1260) could more than double tomorrow to a pb ratio of 2.7 for full valuation. Although I am much more happy with todays valuations, I think paying those prices at full value tomorrow an investor would still outperform the market (at least over the very long run) with both; and the chances are a bit better, when buying FFH. As Buffett said: "It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.” I think both are wonderful companies, while Fairfax seems even a bit more wonderful. But wait: Is the price of MKL and FFH fair? No - it's below IV. So we could change Buffetts cite a bit (and I hope he would agree ) "It's far better to buy a wonderful company at a wonderful price than buying the same wonderful company at a fair price." Imagine that: Paying double todays price for FFH and MKLs price rising a third, FFH would still be (much) cheaper than MKL. At least for everyone who thinks FFH IV to grow faster.1 point

-

1 point

-

BRK trades at a premium to its total investments so its possible but if FFH traded up to its investment value it would be close to 3x book. The key is, we’re still at a very big discount to that so margin of safety is high.1 point

-

It is interesting when we find some details regarding some of Fairfax's International Insurance companies. While small, AM Best provide some details regarding Southbridge in Chile and gives an idea of the growth potential of Fairfax's international subs. https://news.ambest.com/pr/PressContent.aspx?refnum=37004&altsrc=2 AM Best has assigned a Financial Strength Rating of A (Excellent) and a Long-Term Issuer Credit Rating of “a” (Excellent) to Southbridge Compañía de Seguros Generales S.A. (Southbridge) (Santiago, Chile). The outlook assigned to these Credit Ratings (ratings) is stable. Southbridge ranks sixth within the P/C segment in Chile, holding 5.9% of the market, based on gross written premiums. The company has improved its position during the past 10 years, moving up from 10th place in 2016. Southbridge’s operating performance is characterized by its profitability. The company consistently achieves premium sufficiency through strong risk selection and positive investment results. Southbridge has been able to improve its bottom-line results steadily since 2020, from USD 6.7 million to USD 25.1 million by year-end 2025, driven by prudent underwriting and a consistent focus on profitability. AM Best expects this positive trend to continue, as Southbridge implements its strategy and expands operations.1 point

-

I am starting to be a little wary of your postings. You've been on this message board for less than a month and have posted more than 30 times on FIH, most of which is highly critical of management and have not posted anything else on any other part of this board. Then, recently, the criticism seems to have turned into a combination of pessimism (see above) and rabble-rousing activism. Fully acknowledged and understood that criticism, in and of itself, is not necessarily a bad thing and I am not disagreeing with everything you are saying, but when I put everything together, it causes one to consider that the goal is to start grass-roots activism rather than constructive discussion of FIH. As stated above, I am less than happy with my results over the time I've owned this, and I do feel management can and should do more to realize shareholder value in terms of share price. It has not gotten to the point that I'm looking to exit the position, yet, but that's my plan if I find a better investment. Trust me, I am not one who has "twitter muscles" and see zero benefit of getting into a beef on a message board, especially this one which has had, over the years, very, very few of those. That's not my goal. It's that I'm feeling that there's an ultimate goal here that is beyond objective discussion of the merits of this investment. -Crip1 point

-

Fairfax didn’t increase their stake in Atlas. Their partners wanted to take it private.1 point

-

It's been discussed here in multiple occasions that Fairfax owes it's duty to its shareholders and not the retail investors who also hold its investments. There are many examples of Fairfax doing things that retail investors in underlying targets/controlled subs felt wasn't in their best interest, but ultimately suited Fairfax. There was even a court case about one of them. Simply be aware when you're buying into underlying holdings in Fairfax's portfolio - particularly if those names are underperforming1 point

-

Ben Graham's principles will never go out of fashion. There was no golden age of value investing...that's a myth. The GFC proved that...the Pandemic proved that...every time a stock falls to a third of its intrinsic value is proof of that! Half of the board has made a killing in a mis-priced Fairfax Financial over the last four years! Just look for ideas and then invest when you find a mispriced one. Cheers!1 point

-

E Verifying you are human. This may take a few seconds.1 point

-

Right, we discussed this a few days ago. Seems like the answer is, indefinitely! Fairfax made about $2.4b in net earnings APART from investment gains last year (underwriting, interest income, share of earnings of associates), so it is at about 13 times earnings even without its investment gains (or 9 times earnings if you include the investment gains. On the thesis that they will never pick good equity investments or make any money from them except by luck, they're still cheap, half of Intact's multiple. And Fairfax's might occasionally make a gain on investment too...1 point

-

Started nibbling around a year ago in the 1200s CAD when the short report from muddy waters was published.1 point

-

Lucky. Just like when they sold Resolute at the top of the lumber cycle. Just like when they sold pet insurance when there was a mania in cats and dogs. Just like when the average duration of their bond portfolio was 1.2 years and bond yields spiked. Just like when they did a dutch auction and bought 2 million Fairfax shares at $500/share. I could go on… Maybe they aren’t lucky… maybe its skill… And if it is skill, the question becomes: “is it reflected in the stock price?” My guess is no. As a result, it is like an investor today is getting a free call option on this aspect of Fairfax. ( @Hoodlum , FYI, my comment above is not directed at you )1 point

-

@mananainvesting , that is a great question. I will admit that ‘multiple’ is the most difficult part of the valuation process for me. Back in 2021 and probably 2022, I probably would have said i would be happy with a P/BV multiple of 1.3 x. But that would have been largely built off of Fairfax version 2010-2020. Much has changed regarding Fairfax over the past 4 years. As a result, my view today is a P/BV multiple of 1.3 x is too low. What is an appropriate valuation/multiple today? My short answer is higher than where we are at today. How high? I’m not sure. My guess is I will know it when we get there (ora least get closer to ‘it’).1 point

-

22% annualized over the last five years. Cheers!1 point

-

Sounds like a clear ethics violation. Most public companies have an anonymous number for that. As a regular employee, you can and generally will fired for much less than that. As for disclosure, I think the answer is <$10k or <$100k. Below that, it’s a matter of corporate policies which should apply to everyone, including CEO‘s.1 point

-

+1. I never understood the concept of "positioning". Why buy any position unless you know it as well as possible and have enough confidence to own it large? Imagine if a small business owner "positioned" his/her interest. Or a real estate owner. The objective is for it to grow. Generally diversification equates to mediocrity. Rather than diversifying, maintain sufficient cash or liquidity to ride out down cycles and also so you can take advantage of them. I fully realize that this is not the prevailing view (and would get me fired from most financial advisor jobs) but there are reasons why some folks achieve massive financial success and diversification is not one of them.1 point

-

Regardless of size of the positions or whatever profits might be realized, what puzzles (concerns) me is the lack of clarity about the investment philosophy/approach for Todd and Ted. Warren (and Charlie) over the years has talked (and written) many times about his view of stock purchases of companies such as American Express, Coca Cola, or Apple as partial ownership of companies. I realize it's unrealistic that every equity purchase initiated by Warren over the years squarely fell into this category. And not all of them worked out (e.g. airlines -- at least twice). But that's true for some of the wholly owned companies as well. But at least I understood what their "ideal" situation is and can understand and articulate their core philosophy and approach. I cannot do this for Todd and Tedd. For exaample, I've never understood purchases such as SNOW or PAYTM. Both felt so far outside of what Warren & Charlie would do or have explained to us as partial owners in the company with them. I've been wondering about drift for several years now. I am more than a bit wary of the idea of the two of them taking over investment decisions for Warren someday. I was relieved to hear earlier this month of Warren's confidence in Greg's ability to make capital allocation decisions. The way I heard Greg talk about capital allocation sounded just like Warren and Charlie. I left Omaha feeling better about Greg's role in the company.1 point

-

Depends on how short, but in general are a better inflation hedge than most other assets. The best immediate inflation hedge is oil. But oil is also exposed to idiosyncratic risks like cratering demand if the economy is also weakening (and politics!). So a basket that is heavily skewed to oil, some to gold, and some short-term fixed income should be a reasonably good hedge against inflation. Oil is immune to interest rates, but not immune to the economy. Gold/short term bonds are largely immune to the economy, but not real rates. As a basket, they should diversify the idiosyncratic risks of real rates, nominal rates, and the economy while hedging inflation. Future implications of deficit spending? More volatile inflation going forward.1 point

-

Impeccable timing @Luca. Well done1 point

-

I was leaning towards the return on your investment. It's very clear the message set by the CCP and these powerhouse Chinese companies that they do not care about their international shareholders. While I do think that Tencent's management is a step above the rest and these companies will weather the upcoming storm of headwinds it's very much apparent that institutional investors do not want to touch Chinese equities with a 10 foot pole and there's a chance these equities can stay very cheap and undervalued for a very long time. FYI - I own a decent amount of Baba and JD and a few microcaps as far as Chinese equities.1 point

-

Can't wait until Elizabeth Warren is running Tesla and SpaceX by fiat, that's when we'll see real progress in EVs and space!1 point

-

Well if someone would replace google search with something better on your iphone - would you miss it? maybe. Same with google maps - Apple maps has improved to the point where it is almost as good. So most tech moats don't have the longevity that people think they have. the above isn't a theoretical exercise either since google pays Apple dearly to be the default search engine and Apple maps already exists. So Apple could very well change their mind and attack the moat with their own search or replace with Google (AI enhanced) search for example. I don't think the tech moats have the longevity that people think they have. Lot's of tech moats have disintegrated lately -Paypal, Intel, Cisco are fairly recent examples. I believe with tech it's much more about having great and forward looking management in place then the tech moat itself. When you look at history, each tech moat is probably seriously challenged every 10 years or so and it depends on management if they keep the moat intact or even develop new moaty business or not.1 point

-

You know, it's all a derivative of punk rock. I grew up on The Clash, Sex Pistols, Dead Kennedys, etc. Metal, grunge, black metal, etc...all came from punk rock. Cheers!1 point

-

Agreed about the S&P, but it's small ($30m), I wonder if they acquired it somehow and haven't gotten rid of it yet. Seems contrary to everything they usually say and do. As for Occidental, at $354m it may be #1 in the 13-F, but it's really small potatoes compared to the huge bond portfolio, the big private companies they own, notably Eurobank and Atlas/Poseidon (each about $2b). Even Thomas Cook is bigger (about $400m), and Mytilineos is about the same size as the Occidental bet. And of course, the dreaded Blackberry is even smaller, fading into obscurity (thankfully!)1 point

-

Wirecard1 point

-

Some guy using the name "Ben Dover" sent me this angry message today: Fuck you and forcing people to pay $50 to sign up for a membership on a god damn internet forum After your hilariously failed career as an "investor", you clearly are down on your luck and have to resort to bilking people for $$ on an internet forum. Not only are you a shitty investor, you're completely oblivious of sound business practices and are all but ensuring the death of this website. Pathetic loser. May God have mercy on your dumbfuck soul. Genius used his Goldman email address: [email protected] And I'm the pathetic loser, eh! Cheers!1 point

-

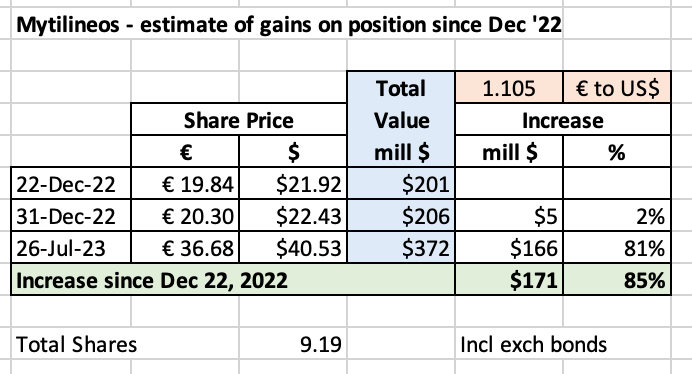

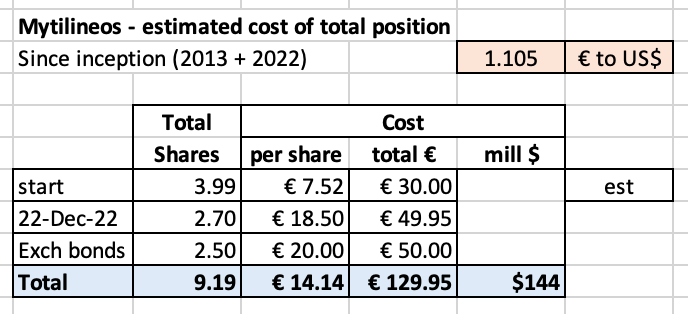

Mytilineos shares have been on a tear in 2023. Here is an short update of what it means for Fairfax. Who is Mytilineos? Ticker: MYTIL.AT (trades on the Athens stock exchange) Stock price: $36.68 (July 26, 2023) Market cap: €5.07 billion Dividend = €1.24 = 3.4% From the company’s web site: “MYTILINEOS Energy & Metals is a global industrial and energy company covering two business Sectors: Energy and Metallurgy. The Company is strategically positioned at the forefront of the energy transition as an integrated utility, while already established as a reference point for competitive green metallurgy at the European and global level. It has a consolidated turnover and EBITDA of €6.35 billion and €823 million, respectively, and employs more than 5,442 direct and indirect employees in Greece and abroad.” Corporate presentation Jun 2023: https://www.mytilineos.com/media/k5lj10q0/corporate_presentation_june_2023.pdf How much of Mytilineos does Fairfax own? Fairfax owns 9.19 million shares (including the exchangeable bonds) with a value of $372 million. This makes the company a top 15 holding in Fairfax’s equity portfolio. Fairfax made its first investment in Mytilineos in 2012 or 2013 (€30 million stake). In November of 2022, Fairfax owned 3.99 million shares. In December 2022, Fairfax more than doubled their stake: they purchased 2.7 million shares at €18.50. they purchased exchangeable bonds that gives them the right to buy another 2.5 million shares at €20. Fairfax is now the second largest shareholder. How has the investment performed since Fairfax added to their position in December, 2022? Fairfax’s position is up $171 million or 85% over the past 8 months. ————— October 21, 2013: Canada's Fairfax buys Mytilineos stake in second bet on Greece https://www.reuters.com/article/us-greece-fairfax/canadas-fairfax-buys-mytilineos-stake-in-second-bet-on-greece-idUSBRE99K05H20131021 December 13, 2022: Fairfax becomes the 2nd largest shareholder in MYTILINEOS https://www.mytilineos.com/news/company-news/fairfax-becomes-the-2nd-largest-shareholder-in-mytilineos ---------- Estimated cost to Fairfax of total position (very rough) My estimate below of €14.14 is likely high. It does not include dividends, which Mytilineos has paid since 2018. And my estimate of €7.52 for the initial 3.99 million shares is a guess. Given the large size of the position, Fairfax will likely give us the correct number in a future annual report.

1 point

-

You might want to ask a European if Russia’s invasion was a big deal (game changer) or not. My guess is many would disagree with your take. Energy supply to Europe has been changed forever. Cheap and abundant energy is the core building block of every society. Europe having the warmest winter on record was an important factor - an awesome development. The UK is an inflation shit show right now. High energy prices are now bleeding though to wage spiral. Finland is not part of NATO. The Ukraine war is not over. And we just learned how fragile (and messed up) Russia is. I’m not sure if your aware, but they have a few nuclear weapons… that is a fat tail risk (getting fatter). Not an issue until it is - i’m not sure but i have heard that nuclear weapons can really be a bitch when they are used. Now we can pretend that this risk does not exist… but this isn’t a Disney movie. Russia invading Ukraine has also ‘informed’ the rest of the world on China (multinational companies understand what is coming) and this is accelerating de-globalization. Totalitarian governments and liberal democracies are like dogs and cats… I think the US (and everyone else in the West) is looking to on-shore important stuff - like chip production (FYI, not the potato kind). Remember, prices cycle up. And down. And then back up… Perhaps we never see $100 oil again. Possible. I could go on. But Russia’s invasion of Ukraine did change the world - economically, politically and militarily. And it is still early days. It will take years (a decade or more?) to fully understand how much. Now i will agree that someone living in rural America or Canada is not being impacted all that much. To them it is probably looking like a big nothing burger. Please note, this is not a doom and gloom summary. I continue to be very optimistic. Change is inevitable and usually a good thing (over time). The West will continue to improve the standard of living for its people. That’s why so many people desperately want in.1 point

-

This reminds me of the optionality that Taleb always talks about. If you buy a lottery ticket (or go to a party where you don't know anyone), the downside is small and certain but the upside is huge and unlikely. If you skydive (or go in one of these), the upside is that you finish the day and you're still alive and not paralyzed, and your out a lot of money. The downside is small, but why put yourself in that position other than for bragging rights?1 point

-

I don't see why Xi has to figure out how the US does things in order to lead his country. Even so, I doubt Xi is dumb or otherwise incapable of understanding any complex topic, including "how the free markets operate".1 point

-

Warren Buffett seem to get an easy pass on his mistakes while we scrutinize Prem Watsa too much. Warren wailed and railed on how bad the airlines have been for investors and capitalism for ever. "Buffett's first investment foray into airlines began with USAir preferred stock in 1989. While Berkshire made money on the dividends, Buffett himself would lament the decision for decades, casting aspersions on the low-profit, expensive nature of the industry." https://finance.yahoo.com/news/how-warren-buffetts-airline-stocks-have-performed-since-berkshire-hathaway-sold-them-134849843.html Suddenly one day, we learn that Warren Buffett is putting billions into a bunch of airlines and just as suddenly airlines become a great investment because Warren Buffett is investing in them. "All in all, the four largest airlines in the US, which also happen to be four largest in the world, are in a good place. Which is why all four warrant the investment from the Oracle of Omaha." https://finance.yahoo.com/news/warren-buffetts-10-billion-airline-174600273.html He liked Delta so much that even his own 10% limit rule got broken and then communicated like this: "What I didn't realize was that that purchase had taken us over 10%. I was already in territory I didn't plan to get, so I just decided to buy a whole lot more stock." https://www.gurufocus.com/news/898907/warren-buffett-on-his-10-rule Then, just as suddenly, in the depths of the pandemic, AGM 2020, we learn that Warren Buffett sold all the airlines near their bottom which made those airlines stocks crash even further right after. A year later we learn that the sale of airlines was for the good of airlines themselves, a form of charity for airlines at the expense of shareholder value. A fine moment of Buffett communication? I wonder how much of our Warren Buffett mesmerizing is attributable to make-up team of Betty Quick. Not hating Buffett at all. He is a great teacher by the way, I learnt from him and still learning. However, I would be on guard being brainwashed about anyone or calling them a Prophet or an Oracle!1 point

-

@Luca Feels like a pet zoo.1 point

-

@SafetyinNumbers great point. My deep dive into the equity portfolio excluded (on purpose) the insurance holdings. The equity portfolio at Fairfax gets most of the attention. The real jewel at Fairfax is the insurance business. It has grown in size by 420% since the end of 2009 (organically and acquisitions). Net premiums written increased from $4.3 billion in 2009 to $22.3 billion in 2022. Fairfax has demonstrated they are excellent at seeding new insurance companies/management teams and then getting out of the way. They are also good at integrating acquisitions. Andy Barnard was put into his role in 2010 - managing the insurance side of Fairfax. He manages the business through 200 profit centres… which indicates just how decentralized the insurance operations are… separate insurance businesses all over the world that are quietly growing year after year - some for decades. Lots of the value that has been building in this group for decades is NOT captured in book value - for people who need convincing see the list below. Over the past 6 years Fairfax has opportunistically monetized a few of their insurance businesses and has booked significant pre-tax gains on these sales of more than $4 billion (see list below). Yes, Digit, seeded in 2017, has become a home run. Ki, seeded in 2020, is growing like crazy. Gulf Insurance Group, seeded in 2010, has quietly grown into a very large insurance company in the MENA region. So much is going on under the hood with the insurance business at Fairfax. As i have said numerous times before: Fairfax has three engines that drive results and all three are performing exceptionally well right now: insurance (hard market), fixed income (high interest rates) and equities (much improved portfolio of holdings). Importantly, the macro environment has also aligned (value investing, cyclicals, commodities, energy). Investors in Fairfax have never had this set-up before (with everything working together at the same time). We are seeing the early benefits of the flywheel effect at Fairfax. Except their transition has not been one from good to great; rather, their transition the past couple of years has been one from bad to great (yes, the cumulative losses from the equity hedges from 2010-2020 were bad). The company is generating record levels of free cash flow. In turn, that is driving record levels of spending on (good) investments. My tracking sheet for Fairfax says they invested a record $2.4 billion in 2022 across 20 different companies. I expect more of the same in 2023. And more again in 2024. Compounding is a beautiful thing - when it is done well. I think investors continue to underestimate the results Fairfax is going to deliver in the coming years. The stock is trading today at 1 x trailing BV (Dec 31, 2022) and at 0.95 x March 31 BV (est $690) and 5.5 x 2023E earnings (est $120/share). Despite the run up the past 18 months, the stock still looks crazy cheap to me. And that is because the business results keep getting better. And the story keeps getting better. So, despite the big run up in price, the stock stays cheap. Yes, i know… makes no sense. Peter Lynch loved these situations. ————— The flywheel effect: The Flywheel effect is a concept developed in the book Good to Great. No matter how dramatic the end result, good-to-great transformations never happen in one fell swoop. In building a great company or social sector enterprise, there is no single defining action, no grand program, no one killer innovation, no solitary lucky break, no miracle moment. Rather, the process resembles relentlessly pushing a giant, heavy flywheel, turn upon turn, building momentum until a point of breakthrough, and beyond. - https://www.jimcollins.com/concepts/the-flywheel.html ————— 1.) ICICI Lombard - India Seeded in 2001 Sold in 2017 (down to 10%) and remainder in 2019 for about a $950 million pre-tax gain Fairfax had to sell ICICI Lombard (down to 10%) to invest in Digit 2.) First Capital - Singapore Seeded in 2002 Sold in 2017 for $1.02 billion after-tax gain delivered a compound rate of return of 30% since 2002 3.) Riverstone Europe - runoff sold in 2020 & 2021 for proceeds of $1.3 billion (+$230 million contingent value instrument) 4.) Pet Insurance seeded with two purchases in 2013 and 2014 sold in 2022 for a $992 million after tax gain 5.) Ambridge Partners purchased by Brit in two transactions in 2015 and 2019 sold in 2023 for $275 million pre-tax gain (hasn’t closed yet)1 point

-

Why would a multibillion-dollar hedge fund manager buy fast food? For major profits. “We’ve been a big investor in the space,” Bill Ackman, founder and CEO of Pershing Square said of fast-food chains on Thursday. https://www.cnbc.com/id/466675681 point

-

Uncle dictator ate some chalk for a day.1 point

-

ChatGPT is terrible and its based on a type of "AI" that is a dead end that will never work for the vast majority of serious applications. To the first point, I'm a software engineer and i've seen code its generated, and its basically a templating engine. It is entirely useless for the work I do. Anyone who has used it for other tasks realizes it's "confidently wrong" in far too many use cases. To the second point, Benedict Evans said it best. :1 point

.jpg.e4162963b25898f493e79a7963ef728e.jpg)