Leaderboard

Popular Content

Showing content with the highest reputation since 07/19/2025 in all areas

-

Updated June 1, 2026 An update of my book/collection of posts on Fairfax is attached below. New posts have been added. The book now has ~950 pages of material on Fairfax. My goal is not size - but I will continue to add material that I think adds value for those interested in learning more about Fairfax. I don't re-read the entire document when I post updated versions. If you see any big errors please let me know. Please note, not everything in the book has been brought up to date. That would have required a couple of months of work… and by the time it was done, much of it would be out of date again. My current plan is to keep updating parts of the document as time goes by. Bottom line, this document should be a much better resource for board members / investors than what existed before. I hope you find it useful. --------- For members who enjoy reading my posts on Fairfax I have attached at the bottom of this post two documents: Fairfax - The Emergence of a Wonderful Company: PDF file contains more than 100 of my best posts on Fairfax from over the past 2 years, organized into 20 chapters. Excel workbook: Companion document to the PDF file, contains 14 worksheets (see below for details). Sanjeev, thanks for everything you do running this board. For all the members on this investing forum, ‘thank you’ for breaking bread on a daily basis and sharing your thoughts on investing and life. Over the years, it has been a life changing experience for me and my family. What is contained in this document is the collective wisdom of this group. Let’s hope i have captured it reasonably well. A message from the legal department: Both documents are incomplete and contain errors. What is contained in the attached documents is not intended to be investing/financial advice. Its purpose is to educate and entertain. ----------- The Excel file contains 14 worksheets: FFH-24: lists and tracks many of Fairfax's equity holdings in real time Size: ranking of Fairfax's equity holdings by size Moves: detailed compilation of many on Fairfax's transactions going back to 2010 - organized by year Earnings Estimate: 2025 and 2026 Premiums: the build for 'underwriting profit' Interest: the build for 'interest and dividend income' Associate Equities: the build for 'share of profit of associates' Consolidated Equities: Non-insurance Consolidated Companies Investments: the build to calculate the return on the total investment portfolio Shares: reviews 'effective shares outstanding' Excess of Fair Value over Carrying Value: for the non-insurance associate and consolidated holdings Float: the build for float 13yr View: A 13 year view of many key metrics for Fairfax IFRS 17: Effects of discounting and risk adjustment - quarterly summary of historical numbers used in earnings forecast Fairfax May 2026 -compressed.pdf Fairfax May 2026.xlsx2 points

-

Every month I get with my wife to review our financial situation. This month the of Crip-Family net worth was not impressive, and when returns are compared against the S&P, it looks even worse. I gave her the low down, specifically, that Fairfax really killed our returns YTD and in May especially. She asked "What happened with Fairfax?"...response was "Not a damn thing, literally no bad news". This is instructive...company moves notably lower with, from what I can see, zero reason. Yes, it is frustrating to see the impact on the net worth, this is the kind of thing we live for...company getting better and price getting cheaper. We have been buying on the way down, but hindsight says we should have waited a little longer. -Crip2 points

-

We need to change the title to ‘Fairfax Stock - New 52-week Low’

2 points

2 points -

Thanks for the advice. I do have fond memories of camping with my Dad. I remember once while camping he wanted to listen to a soccer match and took out his Grundig short wave, looked at the specs in the manual and figured out that he needed a 20 foot antennae to get the game. He attached wire to the antennae and attached it to a couple of trees that my brother and I climbed up to get it high enough.

2 points

-

Check out my most recent article for the Globe and Mail about Fairfax. This is a gift article. https://www.theglobeandmail.com/gift/b04eb1bcd666173196423362ad31a8785d529ba1ad1cee14b25891c6ca2ccfbf/AKS47ZLUWZFSXEKQVGUNGOWYCU/2 points

-

Good question, @Viking…and the answer has to be that it is much better for Fairfax to buy out minority owners of the high quality insurers they already know and trust than to pay higher multiples for partial or total ownership of insurers that might be acquisition targets in external markets, but of whose management and reserving practices they are not as familiar with. Think back to when Buffett owned half of GEICO’s common stock, and had to pay a market price plus a premium to gain full ownership of the company whose reserving practices and operational and investment management were all known and trusted by him. Fairfax is in an even better position than Buffett was given the prices at which they are able to take out their trusted minority partners. And if for some reason Fairfax stock looks to be an even better investment than buying out minority partners, we can trust that Fairfax will find a way to balance their reinvestment opportunities as they did when they sold 10% of Odyssey to enable a Fairfax stock buyback. I think we can all agree that doing that was better for us as remaining shareholders than if they had borrowed funds externally (probably at an even higher cost?) and used it to take out some minority interests instead. Bottom line, I don’t need Fairfax to make the exact reinvestments that I, with my lack of direct knowledge of their opportunity set, think they should make. They have more than earned my trust that they will continue to treat me as a partner and that the reinvestment decisions they make in the future will be those that are likely to benefit us both.2 points

-

Met Ben Watsa at a Europe value investor conference. Asked him why Fairfax was short duration at high rates. Mostly comes down to protecting the downside as they see potential for an inflationary spike.2 points

-

Fairfax Q2-2025 Earning Results - 7 High-Level Thoughts I thought this would be a good time to get out of the weeds. Instead, with our review of Q2 results at Fairfax, we are going to zoom out today and look at the big picture. What did we learn about Fairfax from their Q2, 2025 results? Let me know if you agree/disagree with my list. What did I miss? 1.) Fairfax has a very good P/C insurance business Combined ratio = 93.3% Underwriting profit = $427 million Net premiums written growth = 4.8% Yes, the hard market is slowing. Top line growth in insurance is slowing. Nice to see that Fairfax is being disciplined (although Mr. Market will probably not like it). However, Fairfax will be able to continue to grow their P/C insurance business at above average rates - in addition to growth of NPW - by taking out their minority partners (see comment 5 below). 2.) Fairfax’s most important income stream spiked higher in Q2 Interest and dividend income = $666 million (was $606.5 million in Q1) Increasing by 10% in one quarter is a big deal. This puts the annual number at about $2.6 billion. It increased because the total investment portfolio continues to grow in size. And Fairfax continues to invest it very well. Yield of fixed income portfolio = 5.1% (same as Q1) Average duration of fixed income portfolio = 2.4 years (down from 3.3 in Q1) Fairfax also reduced the average duration of its fixed income portfolio from 3.3 to 2.4 years. They sold U.S. treasury bonds with maturities principally between 28 to 30 years for net proceeds of $1,129.2. Why? Probably because investors are not being compensated appropriately for the inflation risk on long dated US Treasuries. This is prudent risk management on the part of Fairfax - protect the balance sheet. Will analysts hate this move - because it reduces ‘visibility’? Probably. But analysts are focussed on the short term. Fairfax is running the business for the long term - and shareholders should applaud that. 3.) A new income stream is breaking out for Fairfax Fairfax already has 4 large income streams: underwriting profit, interest and dividend income, share of profit of associates and investment gains. The fifth income stream is non-insurance consolidated equity holdings. In recent years Fairfax has been investing heavily in this bucket of equity holdings. Since 2022, it has added Recipe, Grivalia Hospitality, Sleep Country, Meadow Foods and Peak Achievements. To go with legacy holdings AGT Food Ingredients, Dexterra and Sporting Life. I have been (impatiently) waiting 2 years for this bucket of equities to start delivering bottom line results that are in line with its potential - and it appears we might be there. Q2 = $126 million This puts the annual number at about $500 million. This is an important emerging income stream for Fairfax. My guess is it will be Fairfax’s fastest growing income stream moving forward - especially with the hard market in insurance slowing (capital will go to where it earns the best return). And yes, results for this group will have some volatility. 4.) Fairfax (and the team at Hamblin Watsa) continues to invest exceptionally well We got two important updates on the conference call today regarding a couple of Fairfax’s largest investments in recent years. PacWest construction loan portfolio In June of 2023, Kennedy Wilson and Fairfax purchased a $4 billion construction loan portfolio from PacWest. PacWest was caught in the regional bank crisis and they were forced to sell their best assets at a discount. (Of note, Kennedy Wilson also got the loan platform from Pac West - the 40 people who were running the loan portfolio also moved over the Kennedy Wilson.) We got an update today on how this investment has been performing for Fairfax over the past three years. Wade Burton, CIO and VP of Hamblin Watsa on the Fairfax conference call today: “Within the fixed income portfolio, our mortgages continue to perform well. We have been repaid on $1.8 of mortgages from the Pacific Western Bank transaction, where we purchased approximately $4 billion in commitments at 95% of par in 2023. The IRR on the loans repaid thus far is 14.7%. Thanks to the outstanding work of Bill McMorrow, Matt Windisch and their team at Kennedy Wilson, these mortgages are proving to be a fantastic investment for Fairfax.” Blizzard Vacatia (Berkley Group) One of Fairfax’s largest investments in 2025 (January) was the purchase of the Berkley Group, one of the largest independent timeshare companies in the US. With this deal, Fairfax partnered with Caroline Shin and her team at Vacatia. The partnership is called Blizzard Vacatia. Fairfax invested $810 million in various fixed income instruments (with an average yield of 8.6%) and $25 million in equity (50% ownership position). We got an update today on how this investment has been performing for Fairfax YTD. Wade Burton, CIO and VP of Hamblin Watsa on the Fairfax conference call today: “It’s early days in the timeshare investment, Berkeley, run by Caroline Shin, but so far, it has exceeded expectations. Berkeley has approximately 125,000 available room nights per month. They started the year at virtually nil occupancy for overnight stays. In month one, Caroline brought that number to 10%, the next month 20%, and the third month 35%. I’m happy to report year to date operating income has already reached our full year expectations. Again, outstanding and capable partners doing an excellent job for Fairfax shareholders.” 5.) Fairfax telegraphed how it will continue to grow its P/C insurance business - even as the hard market slows Minority interests own stakes in Fairfax’s two largest P/C insurance companies: Allied World = 16.6% Odyssey Re = 9.9% As a result, not all of the earnings from these two companies are accruing to Fairfax common shareholders. Taking out the minority shareholders will be an easy way for Fairfax to grow its P/C insurance business - it will boost the total amount of earnings that accrue to its common shareholders. On the Q2 conference call Fairfax confirmed that it would like to take out its minority partners in its two insurance businesses. They will likely to this in two steps: Allied World later this year (my best guess) and Odyssey in 2026 (or perhaps 2027). The timing will likely be determined by the opportunity set that exists in financial markets in general. If a better capital allocation opportunity comes along, perhaps they will delay taking out minority partners. Because of the call option feature (put in place when the deals were initially struck), Fairfax is able to buy out the minority partners at a very favourable price. As a result, these transactions are high certainty, solid return uses of capital for Fairfax. Taking out minority partners will be a way for Fairfax to grow its bottom line (the part that accrues to its common shareholders) even if the hard market slows further in the coming years. Brilliant planning and execution on the part of Fairfax. 6.) Economic results are much better than accounting results Excess of fair value over carrying value for associate and consolidated holdings increased from $1.4 billion to $2.4 billion, or $111/FFH share (pre-tax). The increase in the quarter was $1 billion, or $46/share pre-tax. This amount is not captured in Fairfax’s reported results (EPS, BV or ROE). This puts the economic value created by Fairfax in Q2 at about $97 share (EPS of $62 plus excess of FV over CV of $35). 7.) Fairfax is exceptionally well positioned today With $3 billion in cash to the holding company, Fairfax is all cashed up. The insurance subs are also overcapitalized (by about $3 billion) - with the hard market slowing, this is another chunk of money that could be sent as a dividend to Fairfax to be redeployed elsewhere. Fairfax is also generating about $1 billion in earnings each quarter. Fairfax has built an earnings juggernaut. Importantly, it is just getting started. Compounding is just starting to kick in… This is resulting in exponential growth. This is very hard for investors to grasp (humans think linearly). This will likely cause investors to underestimate future earnings - and that is what we have seen in each of the past 4 years (like a dog chasing its tail, earnings estimates for Fairfax have consistently been too low and subsequently keep getting revised higher). Fairfax has spent the last 39 years building out its investment management business. It has an amazing range of internal capabilities. This will allow the company to be very nimble and opportunistic moving forward. At the same time, Fairfax has developed a large number of relationships with external capital allocators. Fairfax is viewed as being trustworthy and desirable partner. This is resulting in deal flow - Fairfax’s phone is ringing. Volatility is back. Interest rates have normalized. The macro environment is highly uncertain (tariffs being just one factor). Volatility is a wonderful thing for a value investor like Fairfax - it gives them the opportunity to deploy capital at very attractive rates of return. And Fairfax is on a ‘hot streak’ (a reference to Stanley Druckenmiller). For the past 5 years the team at Fairfax has been executing exceptionally well. ‘They are seeing the ball really well…’2 points

-

The only thing I’ll add on a personal note is that in over 30 years in the industry, with managing catastrophe exposure at the top of my responsibilities, there were at least three separate years in which inappropriate management of investments and poor management of the interest rate risk impact on fixed bond portfolios damaged the company I worked for more severely than the catastrophe risk that I was focused on ever did. Two of those events happened since 2000 — the Great Financial Crisis of 2008 and the increase in interest rates in 2022. The first resulted in the company I worked for being bought out by a larger competitor. The second resulted in sales of non core subsidiaries and employee layoffs in a successful effort to rebuild the capital base and reduce the expense levels going forward. I was fortunate enough to be a “casualty” in the second event. By virtue of severing my employment relationship a few years earlier than I would have chosen had I been left to my own devices, I received access to my retirement account years earlier than if I hadn’t been laid off. I rolled it over to a self directed retirement account and put the lion’s share into Fairfax and Berkshire, two companies I knew had not made the same mistakes my own employers had. The market value increase in Fairfax alone since then has been the equivalent of five years of my previous annual salary level. So I definitely do have a soft spot in my heart for the company and what it has meant to me personally.1 point

-

A very valid question and you are right to be skeptical. Background: I live and invest in India - I would rate 'IDBI Bank' as an 'above-average' investment opportunity which doesn't clear my local hurdle rate, but I still believe this is a great deal for Fairfax Financial. To provide better background - Fairfax Financial is 17% of the global fund I manage, IIFL Finance is 10% of fund (we own 1.7% of the firm), Fairfax India is 2% and IIFL Capital is 2% of the fund. All these have been long term holdings for us 5+ years and IIFL group has been in my personal portfolio for 15 years now. Why winning IDBI is great for Fairfax: 1.) IDBI is not a standalone deal, but it would boost all Indian financial investments of Fairfax My guess is that - Fairfax will form a bank holding firm which will hold IDBI Bank, IIFL Finance, IIFL Capital and Go Digit as their subsidiaries in 1 integrated group framework. In Indian context, a bank is the central core around which the highly valued capital light businesses can be built and scaled. In most verticals like asset management, insurance, institutional brokerage etc - the banking subsidiaries own the largest market share as they have the brand, balance sheet, customer relationship and distribution network. IIFL Group and Go Digit have been able to build large scale businesses despite not having a core banking shareholder. WIth a bank backing them and providing them with all its advantages, they can move to the next level in terms of growth and profitability. For example, the cost of funding for a bank backed firm will be 100+ bps lower (higher credit ratings) and can directly mean a 5% ROE improvement. Similarly, valuation multiple can go up 50% by being aligned with a bank for all these entities. The group will have good cross-sell synergies across - banking, broking, wealth management, asset management, life insurance, general insurance, reinsurance, investment banking and asset financing. I would expect a 1 billion USD uplift in valuation across their Indian financial investments with IDBI in the loop. Fairfax increasing its position in IIFL Capital to 51%, IIFL Finance moving a shareholder resolution to raise 1.3 billion USD of equity (July 24th vote) and taking a direct stake in Digit ealier this year are points to be noted. Indian central bank (RBI) has also been pushing banks to move their insurance (regulated by IRDAI), NBFC or asset management (regulated by SEBI) arms into seperately listed firms. Hence, my guess. 2.) IDBI is an A+ asset that has been run badly IDBI like several other public sector banks is mismanaged and not run to its true potential. IDBI has a phenomenal deposit franchise that is very difficult to replicate. The issues that you mention are all due to their lending ability that used to be mired in corruption and bad culture that comes along with having Government as your ultimate owner. They asset side has been cleaned up over the last several years and Fairfax gets a clean slate on the asset side that they can build upon. IDBI's cost of funds is like 4.7% (250 bps below G-Secs) with a 45% CASA ratio. Almost a 18 billion USD CASA book that is sticky and hasn't left them even in tough situtations. This is very valuable. In CSB bank turnaround, Fairfax quickly fixed the lending side and has been able to grow their asset book at 25% type CAGR, but they haven't been able to build their deposit book. That experience should have reinforced into them as to how valuable this sticky deposit franchise is. I would say, with the current bank licensing conditions, it would take 15 years for any small bank and new licensee to build a CASA or deposit book of this size. IIFL Finance is a co-lending partner of IDBI even now. This along with running CSB for 5+ years should give Fairfax the necessary knowledge to build up the asset side without taking excessive credit risks. IDBI bank currently earns 13% ROE purely from the deposit side advantages. Fairfax should be able to build a good credit book and move it to 16-18% ROE along with all the low hanging fruits that comes with an ownership and culture change. The large CASA base will allow them to build prime retail and corporate loans that compound value with minimal volatility. 3.) Large ticket size compounding for the next 20 years At a 5.7 billion USD cheque size, there are few opportunities of this scale for Fairfax. I (similar to the folks at Fairfax) believe that India is a secular growth story for the next 20 years and has the potential to be a 20+ trillion USD economy in that time frame. India currently has 4 large private banks and 3 large public sector banks. I believe that 5 of these large banks will continue to be the Top-5 even then. Indian large private sector banks have a 10 year average valuation of 3X book value. Fairfax is buying IDBI at 1.15X closing book value. If the turnaround doesn't materialize, they will still be able to exit the business at 1X book value on a conservative basis. On the upside, they can compound earnings at 16-18% CAGR for the next 10+ years and the valuation can double in that time-frame. The INR has gone through a large depreciation cycle over the last 2 years and well placed for lower hit in the coming decade. The absolute dollar returns/ money multiple from this deal can be super attractive even with decent execution. The overall set-up looks asymmetric to me with a juicy Risk-Reward for that ticket size.1 point

-

The fact that the principals are retaining their stake in the newly formed company, makes it more likely that that is the case. Because if they felt they were getting a great deal, they probably would've cashed out.

1 point

-

No, the purchaser is a new subsidiary that has been created to acquire the company.1 point

-

I like how the spread to the 30 year keeps tightening. Two years ago they issued at ~190bp spread, last year ~165bp and this year was ~135bp. I think Allied World is the logical place for this money. Extending the option would have been more expensive and buying Allied World minority boosts the borrowing base,1 point

-

If things continue to drag out in the Middle East, it is highly likely that stock prices will continue to be volatile. Using up the whole NCIB now is like using up your firepower all at once. They've been very good about buying back shares over the last six years...let's trust them to do the right thing over time on buybacks. Cheers!1 point

-

I was having a long conversation with an AI model about Fairfax's 10 year history of reserve redundancy / positive development of prior years reserves and how Fairfax has been very good at over-reserving up front, which has the effect of over-stating "float" and understating "shareholders equity" - since a fairly predictable chunk of "liabilities" is actually equity that just hasn't been released yet. This also has the effect of lowering the coveted leverage ratio (2.5-3x) we receive because equity is actually probably higher than stated. A similar lowering of the leverage ratio results from the under-marked assets we know are worth a few billion more than the accounting books say ("excess of fair value over carrying value"). Either way, Fairfax is working hard to shrink their equity through repurchases and maintain their leverage and they have a higher leverage ratio than Markel. Berkshire lost its leverage a while ago. Sad. The conversation moved into a discussion of the behavior of these prior years reserve releases (mostly in Q4s) in the 3-6 year period after a "hard market" and it became pretty clear that a whole lot of the past several years of hard market benefit has not actually been reflected yet on the books. A major counter-cyclical earnings buffer that makes those softer years a lot more enjoyable (another added bonus is growth slows, freeing up capital to be distributed down to the holdco). Because Fairfax grew so damn much during the hard market years, the annual contribution from reserve releases / positive development will likely be much higher than the $500m annual "typical" release and 2025's $751.5m. If you believe Fairfax has maintained the same over-reserved conservatism - and I don't know any reason to assume otherwise - then they already have a higher shareholders equity and lower liabilities than their accounting book indicates.

1 point

-

completely agree with this 100%. It’s based of my lived experience that most investors I know have studied or are invested in BRK/MKL but haven’t studied Fairfax or rejected it after a cursory look. Which explains to me why it trades at a big discount to peers. Nothing that time and continued execution won’t solve as long as we are right on management and their capital allocation. Bonus points: we get meaningful buybacks while we wait.1 point

-

Value it on normalized investment returns and combined ratio and with this amount of the best kind of leverage, a big structural advantage that somehow remains overlooked, it's easy to see how the long term CAGR could easily continue to be in the ~20% range, especially if Mr Market ever slides them into the "great capital allocator" / "compounder bro" bucket at some point in the future. We're talking about a ~10% earnings yield, almost all of which is distributable for buybacks at a discount. And those earnings should grow at double digit rates for a long time. How many opportunities like that exist in "big cap, outstanding track record, long runway" land nowadays? Sure, odds are the various drivers will have a down period at the same time at some point, but maybe our only edge as non-pod investors is the ability and duration to focus on the structural advantages because we can accept and live with that cyclicality and volatility - and maybe even take advantage of it because we don’t have risk managers or LPs looking over our shoulders every month (or day). Of course, that doesn’t mean there aren’t better ideas out there! I think I've got a few too!1 point

-

I'm not sure I agree with your first statement. Fairfax has done incredibly well since I invested in late '22, as insurance market strengthened bigtime and they have a ton of leverage to increasing rates given duration and size of bond portfolio. On top, their equity portfolio started doing much better, so all engines started firing just around the same time. On top, you had a very low price, so you got multiple expansion on top. That's a great investment! But it's not like Fairfax did anything particularly clever in my opinion. They just didn't do anything extremely dumb (reach for duration during ZIRP), and a lot of factors (largely outside of their control) fell in place. They weren't as dumb as they looked prior to '22, nor were they as smart as some make them out to me based on the period since. Most insurance companies have absolutely minted in recent years. I don't think it's Fairfax' investments that have been the main driver of returns, nor do I think it will be going forward. Given their size, I wouldn't expect any market-beating equity outperformance. We had a long stretch of underperformance prier to their recent hot streak, and as their capital base grows, outperformance will only get harder to come buy. If you compare Fairfax to well-run insurers like WRB and Beazley, which mostly holds T-bills as well, Fairfax is even struggling a bit to keep up. WRB gets a higher multiple, I suppose partly due to simplicity (which I think is fair, and I wouldn't expect it to change). I know I'm kicking a hornets' nest here, but I do think it's a bit of an echo chamber around Fairfax (and I guess that's no surprise given the name of the forum...). I recommend it to people who wants a low-maintenance, long-term holding, given quality of people/no agency risk. But I still think there are better insurance names around from a risk-reward perspective. It's not just whether Fairfax looks like a sound investment here. To me It's about opportunity cost. On a more tactical level (booo!), a lot of investors seem to have forgotten that insurance (and insurance brokering) is cyclical. And people hate when/if earnings start coming down/flatline.

1 point

-

US$1,605 - Could not help myself. - Added another 10% to my largest position. $70/share in earnings in Q2 looks to be a conservative estimate, so, that means $100/share in 1H of 2026 which puts them on pace for another year of EPS in excess of $200. Selling for just over $1,600... -Crip1 point

-

Does this mean the TRS income would be useful to offset head office and leverage costs at the holdco assuming there was no other income at the holdco?1 point

-

I think that is what ultimately will happen but the multiple it’s transacted at really doesn’t matter as they locked in the price when the swaps were put on. To that end, it makes sense to buy in shares via NCIB first as long as valuation stays low. If the multiple goes up they can unwind TRS instead. The most important thing for me is that I know excess capital has a high return home and that the share count is ultimately heading a lot lower.1 point

-

Fairfax has a lot going on right now (all expected to close in Q2): Sale of Eurolife's life insurance business Sale of half of Poseidon Take private of Kennedy Wilson My guess is they may surprise us with how aggressive they have been with share buybacks in Q1. If the stock stays low, 2026 could end up being a big year for share buybacks (more than the 1 million they bought back and retired last year).1 point

-

I just bought my ticket. I like supporting Crohn's and Colitis. I always meet great people. Fairfax has made me a boat load of money. But $450 bucks??!!!! Holy jumping!!!! I am value investor for a reason - I am cheapo. Next year, can we go to McDonalds?1 point

-

When I read this, it seems dismissive of the common sense probabilistic bets they made and continue to make, which may not be how you intended it. Most capital can’t make the same bet because the institutions are investing other people’s money. There aren’t many expected value / probabilistic investors around and most investors don’t respect us because we don’t invest like they do but it is a valid strategy. Worked for Buffett especially in the partnership days and Templeton etc… I have great respect for quality investors. I cosplay as one with small parts of my portfolio with mixed success (KNSL going badly right now but it’s a great business). The multiple expansion in quality compounders forced me to think long term and I think that’s really helped my returns since then. I never would have predicted would have such a concentrated position in anything ever even 5 years ago when I started buying FFH but the risk/reward seems that good. As an expected value investor I know I could be wrong but the odds that I’m wrong in a way where I don’t meet my 10% hurdle seem very low over the next 5 years. If I’m even remotely right though, I should handily beat my hurdle. I might beat it spectacularly. That’s a possibility when buying Fairfax but probably not when buying Costco. Quality investors follow Buffett’s rule #1, never lose money. Expected value investors expect to be wrong a third of the time. They also expect to underperform the market for long periods of time but if it’s a successful strategy they will also beat the market for long periods of time. Expected value investing is an absolute returns game. Quality investing has been hijacked by the relative returns crowd. Most self-described value investors are quality investors with a value filter on the buy decision. The ones that are out of business are the ones who used the value factor to inform, the sell decision. Never sell has all of the assets. It’s worked because growth and predictability factors have high correlation with stock prices. The value factor hasn’t had high correlation with stock prices for a long time. Most institutional capital is trying to beat the market in the short term. That’s how they keep the capital. That means keeping up with the quants. That’s why they are selling Fairfax despite the incredibly low valuation. They don’t even bother predicting expected return. Gross premiums are slowing. In every other sector this means the stock price is going down, so they sell. What’s surprising to me is how much they own. To keep the stock flat despite earnings beats every quarter means they owned a lot and might still. The big multiple expansion we saw from 2020-July 29, 2025 was due much more to institutions chasing the revenue growth than anything else. I think value investors were selling on the way up because the multiple was expanding from 0.6x to almost 1.7x BV. A lot of investors on this board contributed! Since June 2024, between index demand and buybacks over 2.1m shares have been spoken for. I was also buying on pullbacks. My position is up 68% since then and I used leverage to fund it. Channeling Buffett Partnership days. I think it’s a similar kind of market from what I have read. Now we are getting the big multiple contraction as momentum investors continue to unwind their positions. The beauty is the multiple can contract 20% and the stock might be flat. The share count will also be much smaller. We might have $2.4b to spend on buybacks between proceeds for Poseidon ($400m held at holdco) and dividends from the insurance subsidiaries. We are allowed to pay out $4b and the last few years they have been doing half and using it for buybacks.1 point

-

The thing is, if you have some sort of economic event, the stock could move down to Horne's price target (which should also be noted has moved up 10-12 times since his original target of like $730 CDN in Q1 2023 over 3 years ago). So that would be a qualified, but undeserved, win for Horne. Whereas if you based the results on actual analytical work and made investments on that work, Viking would not only be right over the same 3 years, but the stock price would be at Horne's current target and the investor still made a shitload of money! I think Horne should just find another line of work he is more qualified for...maybe a Starbucks barista! That being said, I'm particularly fond of my properly made Brown Sugar Oat Cortado and Horne is often wrong on things. If he messed up my Cortado, I would have to mess him up! Cheers!1 point

-

My mental model in the war in Iran is the US and the Israeli's are 'in control.' I am wondering if this is accurate today. Iran 'controls' the Straight of Hormuz. The longer they remain in control of the straight, the more their position improves. (Iran simply needs to not lose.) My assumption has been that Trump and Isreal will exit (declare victory) and the war will be over. But what if Iran keeps the Straight of Hormuz closed? It makes no sense to me that Iran would open the straight without a signed deal with the US/Israeli's (the fact that Trump is unreliable - putting it politely - is another fly in the ointment). The current leader of Iran had his father, wife and kid killed by US/Iranian strikes. He knows the US/Israeli's are now actively trying to take him out. How do you negotiate with someone who is actively trying to kill you? My guess is Iran is motivated to inflict pain on the US. How? Keep the straight closed for a couple of months. Oil at $150 (or even $200) will cause inflation expectations to ramp higher - this will cause interest rates to ramp higher. Obviously, the stock market expects this to be a big nothing burger (averages are near all time highs - which is almost always the right call). No idea how this plays out. The Straight of Hormuz has never been shut down before. We are in uncharted waters. What makes this conflict so interesting is the pain it is causing is highly disproportionate. It is barely (so far) impacting the US. It is having a big impact on oil importing countries (Europe, India, Japan etc). And it is having a massive impact on the economies of Gulf countries (who were not consulted before hand). This will likely become a much more important story the longer the straight remains closed. Trump is the master a pivoting when he needs to. I am starting to wonder if he has miscalculated this time. We will find out in the coming weeks and months. Crazy times. There is a reason no previous president has done what the US/Israeli's have just done - the risk of the Straight of Hormuz being closed for an extended period was too high (and the catastrophic impact this would have on the global economy). We are now in uncharted territory. Trump might be about to learn a very hard lesson: wars are very easy to start. And sometimes much more difficult to end. PS: Having said all of that, by base case is this ends up being a big nothing burger for financial markets. But it looks to me like the tail risks are getting larger the longer the straight remains closed.1 point

-

It’s not arbitrary. It’s based on the leverage on the balance sheet and reasonable return expectations for bonds and equities.1 point

-

Anecdotally, I have noticed the combined ratio of an acquisition goes up after Fairfax acquires them. I think this is because they are much more conservative on reserving so there is some padding required. The street seems to assume it means they did a bad deal but I think it’s classic Fairfax income deferral.1 point

-

@mananainvesting, great point. I know I do not fully understand the effect that compounding is having on Fairfax’s intrinsic value. This is going to be an increasingly important driver of future results (like it was for BRK back in the 1980’s and 1990’s). This is a topic I need to spend some time on.1 point

-

And then theres also the fact that they take volatility, something naturally inherent in pretty much anything, and point to its existence, as proof that their obvious biases are well founded and rational LOL......1 point

-

There's a thread on it where that is covered.1 point

-

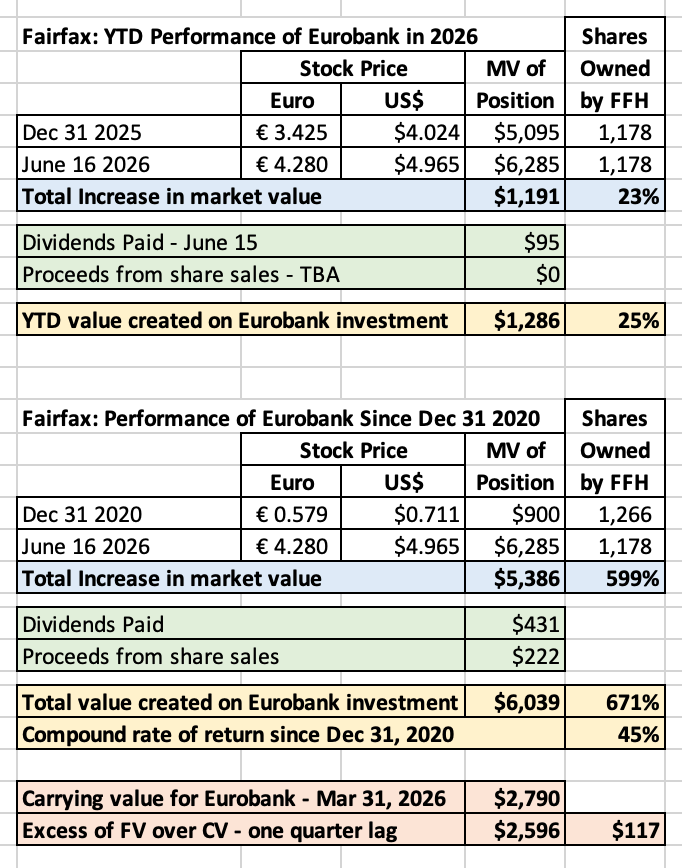

Fairfax invested 400 million euro in Eurobank in 2014 and took nearly a 100% loss on it in the restructuring. They then committed a few hundred million more AND purchased Eurolife. Ultimately, Fairfax's capital commitment/capital at risk on Eurobank was significantly more AND while it was a significantly smaller company. I don't think we need to sweat UA just yet. I think people underestimate the size of the repurchases because they're not including the impact of the repurchases of associates and maybe not the impact of the TRS (which comes through earnings instead of a balance sheet reducing of shares). Fairfax HAS repurchased substantial amounts over the last 5-years demonstrated by any measure - float/share, earnings/share, stocks & bonds/share, etc. I don't think they need to commit 100% of excess capital to repurchases oyf there are other opportunities with attractive returns that diversify future return streams. I must be a glutton for pain. Forgave Fairfax and loaded up in 2021/2022 Forgave Eurobank and loaded up in 2020 Currently forgiving and doubling down on JACK Doubled down on Fannie/Freddie in 2020 when Biden was elected. Have owned Exor since 2014/2015, been adding to it ever since, and here we are below my average cost-basis for that 10-year period and I'm still adding. Accumulated BTC at $14k and rode down to $3k in 2020, accumulated the whole way up to $40k and road down to $15k in 2022, and accumulated all the way up to $100k and road down to the current ~75-80k now. I regularly chase pain, I suppose. But long term it's worked out for most of those.1 point

-

Once again, I think there is confusion with capital allocation at the holding company vs the insurance subsidiaries. They can only pull so much capital out of the insurance subsidiaries while trying to maintain regulatory limits and credit ratings. That capital goes to pay interest expense, holding company costs (paying everyone at HWIC etc..) and buybacks for the most part. Investments like UA are happening at the insurance subsidiaries level and is not capital that could be used for buybacks.1 point

-

Solid results by WRB. BVPS grew 26.7% for the full year, combined ratio 90.7%, ROE > 20%.1 point

-

Fairfax bought Toys “R” Us to be in the toy business? My understanding is it was bought for the real estate. When you say “ultimately selling it at a 60% loss” does this include the real estate?1 point

-

Chat with Geminie to see how AI explain this pattern: The consistent appearance of 100-share "board lots" in the tape, especially during the pre-earnings reversals you noted, strongly suggests institutional algorithmic activity rather than retail sentiment. Why 100-Share Lots Point to Institutions Standard Unit of Trading: On the Toronto Stock Exchange (TSX), 100 shares is the standard "board lot". Algorithms are programmed to execute in these standard units to ensure the best possible execution and to remain "invisible" within the normal flow of the market. "Iceberg" Orders: Institutions often have millions of dollars to move. To avoid moving the price too much against themselves, they use algorithms to slice a massive order into hundreds of smaller 100-share "slices". This is why you see the same size (100 shares) hitting the tape repeatedly—it is likely one large institution slowly unloading or accumulating a position. Retail Capital Constraints: Very few retail traders have the capital or the risk tolerance to place $250,000 into a single trade, especially on a stock that, as you've observed, frequently reverses by 4-5% in a single day. Motives for Driving the Price Down (Without Options) Since there are no options, the motive for driving the price down pre-earnings is likely inventory management and liquidity hunting: Stop-Loss Hunting: By aggressively selling 100-share blocks, institutions can trigger technical sell-signals or "stop-loss" orders from smaller players. When those stops hit, it creates a "cascade" of selling, allowing the institution to buy back the shares they just sold (plus more) at a significantly lower price. Inventory De-risking: Ahead of an earnings report (which carries binary risk), some institutions may be required by their internal risk models to trim their positions. The "reversal" you see is the market absorbing these large sell programs. Accumulation before a "Beat": If an institution expects a strong earnings beat, they may use a "shakedown" strategy—driving the price lower to clear out weak hands so they can build a larger position at a lower cost-basis before the actual news breaks. In summary, the 100-share lot size at this price point is almost a "fingerprint" of institutional algorithms managing large-scale capital flows.1 point

-

According to AI a 4% to 8% sustainable price jump this week would be consistent with the price action of other recent additions to the TSX 60. I had a celebratory steak dinner last night because I like to count chickens before they hatch.1 point

-

People remember you being cheap. Sooner or later, that will impact deal flow in a negative way. Deal flow over the long term is much more important. So if there is any reason to be "fair and friendly" that is aligned with shareholder interest, that would be it.1 point

-

Here is a plug I posted on Twitter for David’s new book. Fairfax was founded in 1985. A $1,000 investment with Prem and team back then would now be worth more than $1 million. Yes, an amazing return = CAGR of 19% over 40 yrs. How did they it do it? In his book called ‘The Fairfax Way’, author David Thomas provides many of the answers. The narrative for Fairfax is upside down Fairfax is well known for a few of the big mistakes made that it has made. What is not well know are the many important things that the company got right. And given its outstanding performance over the past 40 years, it got way more right than it got wrong. What did it get right? The answers go way beyond the numbers. It includes the people, structure and culture - and a moat that has been slowly increasing in size around the company over the past 40 years: Prem Watsa (founder and CEO) - Driven, optimistic, risk taker, unconventional, ‘right’ temperament, able to attract and retain talent, nice and more… High quality management - Fairfax is stacked with quality people in all parts of the organization. We get to hear from many of them (past and present). A proven organizational structure. Decentralized operations - Run by entrepreneurs. Centralized capital allocation - Run by a best-in-class team. Long term focus. A strong culture - Its employee retention has been amazing. David’s book explores all of these topics and more. It is a treasure trove of information on the company. It is a great resource for investors. I really enjoyed and got great value from reading the book (I learned a lot). David, well done and thank you! ————— The 19% return over 40 years is in US$ and assumes all dividends were reinvested.1 point

-

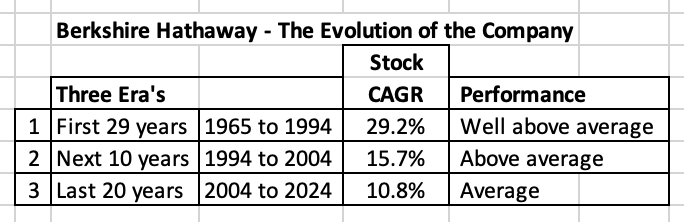

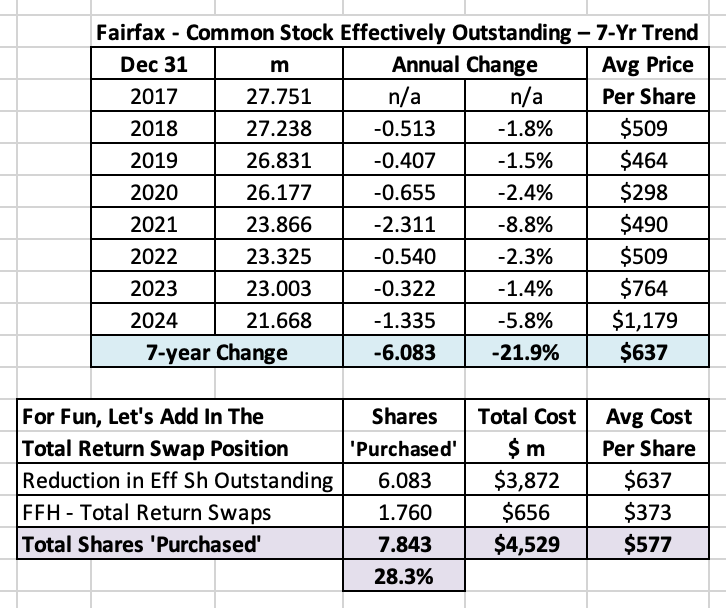

What is Berkshire Hathaway’s biggest problem today? ‘Only a fool learns from his own mistakes. The wise man learns from the mistakes of others.' Otto von Bismarck Berkshire Hathaway served as the inspiration for Fairfax’s creation way back in 1985 (when Hamblin Watsa purchased Markel’s insurance operations in Canada). Today, Berkshire Hathaway is at a much different life stage as a company than Fairfax. Being a much younger and smaller company, Fairfax has the opportunity to learn a great deal more from Berkshire Hathaway. Berkshire Hathaway is almost 60 years old as a company (in its present form). If Buffett could do it all over again, would he do anything differently? Of course he would. But let’s try and focus our discussion a little more. Today, we are going to ask a simple question: What is Berkshire Hathaway’s biggest problem today? Berkshire Hathaway’s biggest problem today is its size - it has grow into a massive company. Berkshire Hathaway has a market cap of over $1 trillion, making it the 9th largest publicly traded company in the US. I don’t think this is a controversial thing to say. And that is because Warren Buffett has been warning investors about this problem for decades. It has been getting worse every year. And it will continue to get worse every year moving forward. Why is size a problem? Berkshire Hathaway generates an enormous amount of excess capital every year. But because of its size, it now has a very limited opportunity set. This makes reinvestment of its excess capital very difficult. This lowers the rate of return the company is able to earn. As a result, the growing size of Berkshire Hathaway has been slowing the CAGR of the stock for decades. From a well above average rate of 29.2% for the first 30 years (1965 to 1994). To an above average rate of 15.7% for the next 10 years (1994 to 2004). To an average rate of 10.8% for the past 20 years (2004 to 2024). The rate of return being generated today is not a terrible thing. But clearly it is not what it once was. What is the root cause of the problem? The root cause of the problem is the power of compounding and time. As any investor knows (especially Buffett) compounding is an amazing and unstoppable force. Especially when given enough time. The result is magic. Decades ago, Berkshire Hathaway’s share price got to the exciting part of compounding curve (the hockey stick part). Ok… Yes, Buffett is the GOAT. Are we done? No, not so fast. Let’s ask another question: Was there anything Buffett could have done to stop the problem from happening? No, I don’t think there was anything Buffett could have done to stop Berkshire Hathaway from becoming such a large company. Ok. Dead end. Let’s reframe the question: Was there anything Buffett could have done to slow the problem from happening? Yes, I think there likely were some things Buffett could have done to slow Berkshire Hathaway from becoming such a large company. Like what? I can think of two things: Stock buybacks Buy and hold forever (steep aversion to selling anything) Both of these are big topics. Today, I am going to focus only on buybacks. How does buying back stock shrink the size of a company? Share buybacks are paid for using cash. This shrinks both assets and shareholders’ equity. Lower shareholders equity shrinks the size of the company. Stock Buybacks One of the reason’s Berkshire Hathaway got so big was Buffett refused to do any stock buybacks for many years. Even during extended periods when the company’s stock was cheap. Yes, Buffett had a good reason for not doing buybacks - he could usually earn a better return by allocating excess capital in other ways. This was clearly the right short term decision. And, with hindsight, arguably the wrong long term decision for the company and shareholders. Quality at a fair price “A great business at a fair price is superior to a fair business at a great price.” Charlie Munger Price/valuation might have been part of the problem. Perhaps Buffett was simply being too cheap - only wanting to buy back Berkshire Hathaway stock when it was wicked cheap (not just cheap). This would have severely restricted the opportunity for Buffett to buy back stock. This also makes no sense. Munger (supposedly) taught Buffett that it was preferable to buy “a great business at a fair price.” Why would this logic not apply to Berkshire Hathaway itself? Berkshire Hathaway was not just a great business… it was the best business in the world. And at many times in the past its shares were available at a fair price. A double standard? What is puzzling is Buffett loves it when companies he owns do big share buybacks (when their stock is trading at a low valuation). Apple is the best recent example. Buffett has been a big cheerleader of Apple’s buybacks for years. (Interestingly, massive buybacks have helped slow Apple’s own ‘too big’ size problem.) When it came to buybacks, Buffett seemed to have two standards - one for Berkshire Hathaway and another for the publicly traded stocks it owned. Buffett finally capitulates In 2011, Buffett finally relented and issued an official buyback policy for Berkshire Hathaway. But he set a buyback valuation threshold of 1.2 x BV. Really? That cheap? The result was Berkshire Hathaway repurchased few shares in the subsequent years. In 2018, Buffett ended the buyback valuation threshold of 1.2 x BV and gave management more discretion with when doing buybacks. As a result, the pace of buybacks increased quite a bit. But Buffett was decades too late - Berkshire Hathaway had already become a monster in size. The window of opportunity to use buybacks as a way to keep Berkshire Hathaway small was long gone. The Berkshire Hathaway multiverse Now imagine an alternate universe - imagine a past where Buffett was more open minded to share buybacks - actually did them in size at the appropriate times. Perhaps up to valuation threshold of 1.5 x BV - hardly a stretch for a company of Berkshire Hathaway’s quality. Would that have perhaps lowered past returns a little for investors? Probably a little. But it would have kept the size of the company smaller, perhaps much smaller. And this would have likely allowed the company to continue to compound at a much higher rate of return for a longer period of time - perhaps much longer. Summary Buffett has known for decades that Berkshire Hathaway was becoming too large of a company. After all, if anyone understands the power of compounding and time it is Buffett. I think it can be convincingly argued that Buffett did not do enough to manage that specific problem, especially 20 or even 30 years ago (when it was becoming apparent). Like being more open minded with stock buybacks (the concept and the price at which they made sense). Is this perhaps an example of where Buffett was not thinking long term enough? Yes, that question is a bit of a mind-bender. But it appears ‘long term’ to Buffett might have meant ‘during his lifetime’ (in terms of Berkshire Hathaway being an above average compounding machine). Of course, Berkshire Hathaway is a wonderful company. But it is no longer an above average compounding machine. And the risk for the company moving forward is it shifts from an ‘average’ to ‘below average’ rate of return for long term shareholders. Is there a lesson here for Fairfax? Yes, I think there is. An important one that is not on the radar today of long term investors. Buybacks are good because of all the usual reasons: When done at favourable prices (i.e. below intrinsic value), they deliver significant value. They increase the ownership stake of long term shareholders. They are a high certainty capital allocation activity. They are a sign management is rational and working in the best interests of long term shareholders. For compounding machines like Fairfax, we now have one more good reason to do buybacks. Especially when looking 10 or 20 years into the future. By meaningfully shrinking the size of the company (with aggressive buybacks over a long period of time), it allows compounding to continue at above average rates of return for a much longer period of time - it extends the runway of a compounding machine. Another important lesson: Don’t cheap out on the price you pay. As Charlie Munger taught investors, pay a fair price for a quality business - this will allow you to buy back many more shares than would otherwise be the case. What has Fairfax been doing? Fairfax has been aggressively buying back its stock since 2017. From 2017 to 2024, it has reduced effective shares outstanding by 6.1 million, or 21.9%, at an average cost of $637/share. The shares were repurchased at a crazy low price. And a significant number of shares have been repurchased. And if we include the FFH-total return swaps, Fairfax got exposure to 7.8 million of its shares, or 28.3%, at an average cost of $577/share. A very good news story is even better. In 2025, Fairfax has continued to buyback shares. YTD (to September 30, 2025), my guess is they have taken out around 400,000 more shares. In August and September, shares were likely repurchased at around $1,700/share. We will get details when Fairfax reports Q3 results on November 6, 2025. It appears Fairfax is comfortable paying ‘a fair price for a great business.’ This is another example of Fairfax moving up the quality ladder when deploying their excess capital. Bottom line, it looks like Fairfax has gotten the memo - they appear to understand Berkshire Hathaway’s size problem. And the management team at Fairfax appears to be doing something about it - in a pretty aggressive way. With buybacks it looks like Fairfax is thinking long term - the benefits of the buybacks being done today will flow to shareholders for decades into the future. This discussion leads us to another really important and related topic. Is having a chronically low share price (valuation) a good or a bad thing for Fairfax? Having a chronically low share price (valuation) has been a gift for Fairfax and its shareholders. It has allowed the company to buy back an enormous amount of stock over the past 7 years - to get exposure to 28.3% of its effective shares outstanding at a very low average price ($577/share). This was also a high certainty/low risk use of capital for Fairfax. The interesting thing is aggressive share buybacks have not impaired the company’s ability to grow its top line (the NPW of its P/C insurance business have increased in size by about 150% from 2017 to 2024). As a result, the per share value creation for long term Fairfax shareholders has been enormous. Bottom line, a low share price - especially if it persists for years - is a big benefit for long term Fairfax shareholders. Remember this when you look at Fairfax’s stock price each day.

1 point

-

Awesome! Thanks for sharing @Viking. I’ve pre-ordered it myself just now. By the way, anyone else notice who the publisher is? That’s what I call serendipity….1 point

-

A picture is worth 1,000 words. The best performing insurance company (over the past 5 years) is available at the cheapest valuation (compared to peers). What to do? Panic, of course. I love Mr. Market. (My guess is Fairfax does too.)

1 point

-

I did the same. I explain my thinking below. I manage my Fairfax investment in two ways: Core position Flex position The core position is the (relatively) new part for me. I have held a large core position in Fairfax since late October/early November 2020. At a little over 5 years, this is the longest time period I have ever owned a core position in Fairfax. (It is the longest period of time I have owned a core position in any stock.) Flexing my position size is something I have done with Fairfax on and off for +20 years. I sometimes buy more of the stock when it sells off/gets cheaper. And then I lighten up when the stock moves higher. With my flex position in Fairfax I am looking for a small gain (the exact amount will vary each time and will depend on the set-up). Normally, I find I get 2 or 3 nice opportunities each year to flex my position in Fairfax. Times when the stock sells off - where I like the short term risk/reward set up. Why did I ‘flex’ my position higher today? Stock closed today at $1,660/share. Three days ago it closed at $1,790/share. Decline was 7.3%. It looks to me like the stock has sold off over the past week for reasons that have nothing to do with Fairfax. (I.E. all financials are selling off.) Fairfax’s fundamentals continue to improve - I really like the sale of Fairfax’s 80% stake in Eurolife’s life insurance business for $944.7 million (expected to close in Q1-2026). Strong earnings - I expect Fairfax to deliver very good Q3 earnings report. My guess is BV will be comfortably over $1,200/share. This puts the P/BV at about 1.38 Hidden value - Excess of FV over CV for associate and consolidated holdings is likely $100/share (after tax). That puts ‘adjusted’ P/BV at about 1.28 ($1,660/$1,300) Hidden value part 2 - Of course, we know intrinsic value is much higher than ‘adjusted’ BV of $1,300. Let’s be conservative and add another $100/share (Eurolife sale will crystallize a nice investment gain in Q1-2026…). This puts Fairfax’s value (measured conservatively) at $1,400/share. This puts the. P/FV at 1.19 Today. Fairfax thinks its stock price is cheap - Fairfax was an aggressive buyer of its shares in Q2, paying about $1,700/share. Seasonality - As @SafetyinNumbers has pointed out many time before, Fairfax’s share price tends to underperform during hurricane season (which runs until about the end of October). A headwind will end soon. All cashed up - As I said earlier, I expect Fairfax to deliver strong Q3 earnings - they will be all cashed up in early November. What will they do? Well, being all cashed up, with shares trading below $1,700 and with hurricane season behind them… why not buy back a bunch of stock to year end? Added motivation - Fairfax still owns 1.76 million shares of FFH-TRS. Every $100 increase in Fairfax’s share price delivers an investment gain of $176 million to Fairfax. This makes buying back stock when it is undervalued (like it is today) an even better decision. A near term risk to my ‘flex’ trade: it appears the hard market in P/C insurance is coming to an end. Lots of P/C insurance companies will report in the next 2 weeks. It they disappoint in the top line (revenue) we could see a big sell off in P/C insurance stocks. Important: I flex my positions in stocks I am happy holding for the long term (with the increased position size). There is always a good chance the stock could get much cheaper from here (especially in the short term). Anyways, I do not post this as investment advice. My logic could turn out to be completely wrong. Please consult your investment advisor before making any investment decisions. My post above is intended to be for information/entertainment purposes1 point

-

It's been discussed here in multiple occasions that Fairfax owes it's duty to its shareholders and not the retail investors who also hold its investments. There are many examples of Fairfax doing things that retail investors in underlying targets/controlled subs felt wasn't in their best interest, but ultimately suited Fairfax. There was even a court case about one of them. Simply be aware when you're buying into underlying holdings in Fairfax's portfolio - particularly if those names are underperforming1 point

-

https://www.theglobeandmail.com/investing/markets/stocks/FFH-T/pressreleases/35502473/canadian-analyst-coverage-oct-16th-2025/ Raymond James raised its target to $3,050 from $2,900, maintaining an Outperform rating due to strong insurance underwriting performance and investment gains.1 point

-

Fairfax’s stock did terribly from 2010 to 2020 for one big reason: the equity hedges. The short positions were a second smaller factor. Everything after this pales in comparison - I.E. excluding these two factors, Fairfax’s performance would have likely been ok (including lower interest income from how defensive they were with the duration of their fixed income portfolio beginning at the end of 2016). Fairfax booked about $250 million in realized gains when they sold off their corporate bond portfolio in 2021 (at a yield of 1%). And in 2002/03, Fairfax avoided billions in losses in their fixed income portfolio because of how defensive they were positioned. And because they were so short duration, in 2022/23 the earn through from much higher rates (much higher interest income) was very quick. When you add up all the puts and takes, Fairfax likely did very well with the total return they earned on their fixed income portfolio from late 2016 to 2023.1 point

-

Ben Graham's principles will never go out of fashion. There was no golden age of value investing...that's a myth. The GFC proved that...the Pandemic proved that...every time a stock falls to a third of its intrinsic value is proof of that! Half of the board has made a killing in a mis-priced Fairfax Financial over the last four years! Just look for ideas and then invest when you find a mispriced one. Cheers!1 point

-

Still lots of our shareholders are happy to sell their shares at <10x earnings and have for the past 4 years. In part, maybe because the positions have become so big for some of them including some on this board but it is still interesting.1 point

-

I am of two minds on this. On one hand, I think the multi discipline approach to life is more appealing. But I think that’s just related to me being curious and willing to go pretty deep down rabbit holes of learning/practicing topics and ideas that on the surface don’t seem to be obviously beneficial from a business standpoint. I think this has helped me tremendously from the standpoint of getting good at “learning how to learn” about various topics. I stumbled into an academic decathlon type program in high school based on a teacher recommendation. It was really open ended, in terms of class time and study material, and pushed the students into learning foundational level content of a wide range of topics that weren’t covered in high school (like instead of just geometry or calculus, the math content was fractals and demographic statistics; there was a massive focus on theology and philosophy, the arts/music content was very nuanced compared to other classes, there was college level economic theory instead of just memorizing macro/micro definitions). The idea of this program was completely bananas to me at first and more than a little overwhelming, as my entire family was lower income working class - no discussion of school work at home, much less any talk of high brow ideas or philosophy or economics or anything. That experience was the single biggest advantage I had going into college and the workplace after college. Even though I had a cut and dried major (finance and accounting), that experience helped me in virtually every aspect of college and I got a lot more out of many of my classes because of it. Literally my entire life trajectory was probably altered substantially by that high school program. I wasn’t going to end up in jail or anything, but I think there’s a fairly decent chance that I would have dropped out of college due to being unprepared for the open-endedness and self study needed. Before that program, nothing in public school prepared me for the difficulty level, lack of hand holding, and relative ambiguity of university course work. So, when I read about Munger’s fascination with architecture and psychology, I can relate because I have several things that I’m very interested in and I feel are worthy of a lot of my time and brain power. And I think the concept of mental models/latticework is a great way to describe how I think. I have always struggled greatly with memorization and recalling facts. I need to “start at the beginning” with whatever I’m learning and then I can fairly quickly figure out how a system or business works. Munger’s obsession with incentives is a good example of what I’m talking about. Fully understanding an incentive structure (at the most basic level) can go along way in teaching me how a system works, what the economics of it are, and allows me to extrapolate knowledge about the system way way quicker than if I only read an analyst report or something. So, I’ve figured out that “mental models” (although the term is so overused now, I feel corny using it) are helpful for me in learning the things I want to learn. Learning how people in other fields analyze/problem solve, improves my learning ability - even though I almost never come close to gaining exert level knowledge in most of the topics I read about. On the other hand, there are people like Buffett and quite a few other top tier CEOs/money managers and business people that I’ve personally known, who are really almost myopically focused on the thing they do. Their minds don’t seem to wander all that far astray from the primary thing they practice. They have interests, like golf or fishing or hunting or wine or whatever, but those interests are all sort of recreational or to relax/decompress. Playing golf is not necessarily the same as Munger giving lectures about psychology or trying to corner a university into using his architectural design for windowless dormitories. So, I think either mind frame can work. And I think that, like every other character trait, people are just somewhere on the spectrum and people should just lean into whatever is most effective/enjoyable for them. Anecdotally, a couple of mentors of mine at the same company were good examples of both sides of the coin. Both high level executives, being number 3 and 4 behind CEO in the c-suite pecking order. Both loved what they did and were experts of the company from both in-the-weeds detail to high level capital allocation. But one of them would seem just as happy (if not happier) talking to you about books, military history, safari hunting, theology, etc. The other basically only thought/talked about work, with a sprinkling of conversation about college sports or his kids. Both were great at their jobs and a wealth of knowledge about the company. Just very different people.1 point

-

Fairfax is extracting quite a bit of cash between dividends and selling their proportionate share of the buybacks. It’s an exceptional seemingly reliable return especially when levered almost 3:1 in the investment portfolio. I think about Recipe that way too. They levered up in 2021, paid down the debt, levered up again in 2025 and perhaps in 2029, they will lever up again and pay Fairfax a big special dividend. IPO is an option but market likes growth and they don’t have to grow to provide great returns for Fairfax.1 point

.jpg.e4162963b25898f493e79a7963ef728e.jpg)