All Activity

- Today

-

I think I'm a tad confused. Can you elaborate on why this statement loses the author credibility? I'm curious because this a real problem and there are companies that rely on innovation here in agentic space (thinking Cloudflare and their L402 and x402 integration in the Workers platform).

-

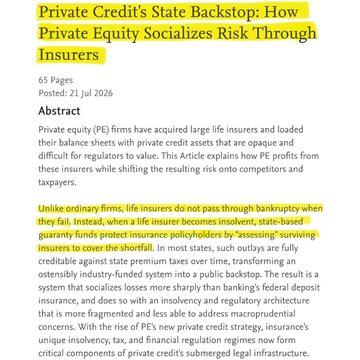

I have access to Burry's substack where the whole post is. The argument is again PE-owned life insurers. I.e. PE companies have a captive insurer, they ratchet up risk using offshore entities and lax regulations for overseas subsidiaries to leverage these these things up to juice returns on the fixed income side. And then they sell premium/policies/annuities as quickly as they can to collect the upfront cash/pay day on the insurance side. And as long as everything goes well, the PE company makes it rain cash from float and the investments. And when it goes south? The insurance sub fails and the state regulators and the surviving insurers carry the cost of the failure a la their social insurance. Privatize the gains. Socialize the losses. That's Burry's complaint. And he points to this being the mechanism that is funding much of the AI infrastructure build out.

-

I have access to Burry's substack where the whole post is. The argument is again PE-owned life insurers. I.e. PE companies have a captive insurer, they ratchet up risk using offshore entities and lax regulations for overseas subsidiaries to leverage these these things up to juice returns on the fixed income side. And then they sell premium as quickly as they can to collect the upfront cash/pay day on the insurance side. And as long as everything goes well, the PE company makes it rain cash. And when it goes south? State regulators and the surviving insurers bare the cost of the failure a la their social insurance. Privatize the gains. Socialize the losses.

-

Great companies which fail to create shareholder value

Dalal.Holdings replied to Cod Liver Oil's topic in General Discussion

We should also think about those “great” SaaS companies that have yet to earn a decent GAAP profit. Just machines that feed on common stock investors in order to churn out employee stock based comp. Many investors, including “value investors” were willing to pay huge multiples for these (valuing them off Price/Sales, of course) and got totally hosed. Stock based comp is, unfortunately, a real expense. And reality eventually always reasserts itself. Then there are software companies like Adobe, Intuit, even MSFT in some cases that have grown accustomed to abusing their customers with insane pricing and price rises year after year. Intuit lobbies regularly to keep the U.S. tax code complex so they stay in business. It’s actually great to see AI deliver a little karma… -

Excerpt from the article Libs posted: “Legacy credit card and banking infrastructures are unsuited for agentic micropayments due to their fee structures; a standard credit card transaction averages 2%-3% plus a flat fee of approximately US$0.30, versus AI agent payments that average US$0.001 to purchase a single second of compute or a data query.” Statements like this are like when someone claims they are a huge sports fan and says "I think LeBron is going to hit 50 homers for the Sixers next year". Credibility immediately goes out the window. Lolz.

-

It’s definitely cheap but no natural buyers so it makes sense to trade around it and you are helping provide liquidity to a fellow traveller. Win win I say. I was already at my core position so I didn’t sell any and got spoiled by that $3 price. I trade around FIH too but not FFH.

- Yesterday

-

Doubtful. I don't think even the Saudi deal for civilian nuclear power will work out. And I really doubt they will be enriching their own stuff. What is far more likely is more dependence on the U.S. to provide defense/weapons similar to Europe. And I think Ukraine will become a huge exporter of defense weapons/tools too thanks to their expertise in drones/air defenses/etc. In fact, Iran has just learned from this conflict that it doesn't even need a nuclear weapon. It can just threaten ships in the Strait/energy infrastructure in the Gulf. Iran now knows it possesses a very real source of leverage. Nukes are not necessary.

-

https://www.bloomberg.com/news/articles/2026-07-26/us-pauses-iran-strikes-for-second-night-as-red-sea-tensions-rise?srnd=homepage-americas Again, too many people want resolution of this for it to become a real problem. Obviously tail risks are that the crisis spirals out of control, but the base case is that the Strait reopens and does not stay shut long enough to cause too much damage because too many of the major players (USA, China, OECD, Gulf Nations, etc) want the Strait open.

-

Have they shown the burning tanker yet? It may be true, but I'm skeptical. This is all "according to Iran’s military-linked state media". Oil futures down 4-5% by the way. Maybe the market is smarter than the Western media lapping up Iranian propaganda.

-

Hah yea I’ve long held the opinion that there’s little better beer wise than one Guinness, and there little worse than two. Its not a beer you wanna binge. That said it’s been too long but by car bombs are unrivaled.

-

What are you listening to ? (Music thread)

whatstheofficerproblem replied to Spekulatius's topic in General Discussion

Frequent users of Apple Music might know just how dog shit Apple's "shuffle" is. It basically plays your music in the same damn order every time you hit shuffle. I hit radio instead and it threw up this song in my playlist that I haven't heard in a couple years. Nostalgia hit me like a truck. Been relating to this song way too much as of late. -

Yep. Took barely 30 mins at a CarMax. Carvana was low balling me. Sold at Carmax. Not much baggage, moving with just my clothes. Guinness overall sucks. Coffee every day is fine. Hell I drink it 3x a day. Thing is I don't drink "black coffee" which is literally just battery acid. I need dairy in my coffee.

-

Interesting. Maybe someone big trying to enter? I may regret selling. $2-ish is still pretty cheap, but was barely a 'watch' position that I had put on at the beginning of the year. So gave into the temptation to book a quick ~30% profit and see if I can't re-enter at the prices closer to where it's been trading most of the year.

-

Nice - you sell the car? I don't care for extra stout but I love Guiness draught. But I also drink black coffee every day of my life.

-

Pre-market it was very interesting. Was $3bid for 135k shares and they killed it before it could trade. I think it’s a strategy to get offers in the order book.

-

Friday was IPA day. Saturday I finished my golden drops of the Ardbeg 25 as a cheers to California. Today's day drinking session is a 6 pack Guinness extra stout. This is my second time drinking Guinness & I just don't get it. Why do you want to taste burnt barley? This thing tastes like black coffee i.e. battery acid. That said the extra stout is better at giving you a buzz vs draught. You folks have convinced me to get the Empress Gin. I will be setting up a bar in my studio in NY. Going to make my own mixers from scratch and will post recipes here from time to time if they're good. Have a first class one way ticket booked to NY on the 31st. Going there tail end of summer and if I can survive Iowa & Somaliland winters, I'll be just fine in NY.

-

Fairfax doesn’t have life insurance exposure in NA and is selling Eurolife. It doesn’t have exposure to private credit of this sort either.

-

I didn't equate Trump with Hitler. Re-read the post. I equated Trump with being the catalyst that created a Hitler...that Trump's antics on the global stage are going to give rise to something far worse than Trump...a consequence of his destabilization of the world order. Cheers!

-

John's perspective may get somewhat of a jolt if in a bit over 2 years if, that's if, we have an election where the far right loses the presidency. The new pres's influence should mean that the justice dept will likely have a full program of Trump family criminal and civil suits which could be just as exciting as Trump's pursuit of his perceived foes. I guess with your laissez-faire presentation of what presidential power can and should do Reds I guess you'll be equally as supportive of the next guy's agenda as you are Trump's...correct?

-

just found an X post where it was quoted this paper, highlighted by Mr Burry. Do you think FFH could be involved somehow?

-

I'm bullish on BTC as digital gold, but have always considered the rest of the crypto space garbage. This is making me re-think. If Agentic AI is indeed the future, and I think it will be huge, it can only run on the crypto rails. Eye - opening: https://www.franklintempleton.com/articles/2026/digital-assets/agentic-ai-the-killer-use-case-for-blockchain-and-crypto Courtesy of our controversial friend, Jordi Visser and his weekly video.

-

ok! I’m up north (although people tell me Virginia is still the south but it isn’t) and I got two bottles of dry Riesling from the finger lakes and I’m chilling them now so better late than never - thanks for the rec Spek

-

This was a great listen with a very smart investor.

-

If you didn't think crude prices were going up on Monday ... earlier today a tanker in the Strait of Homuz hit a naval mine. Taking its chances, navigating an Iranian non approved route, quite possibly with US 'assistance'; the Asian oil market opens today at 18:00 EST. Incredible weaponry, etc ... yet the US can't even adequately protect its own troops in their Gulf bases. Not going to go well for tanker rates, insurance, keeping ships crewed, etc, etc ..... and not going to change until an international coalition takes over shipping security. https://ca.video.search.yahoo.com/yhs/search?fr=yhs-fc-5918_3&hsimp=yhs-5918_3&hspart=fc¶m1=7¶m2=eJwtjstqwzAURH9FywQk%2BV7JkuVoFTfNB5SuKrRQHdURfmI7uPTri0OYzcCcgdOkm7P%2B44IAShXaUT8465UCcNTvk6O%2BdtaXZemoT5OzHk3OMddcoOQojKO%2BiaOzvg6O%2Bkdw1vfjX%2Bq6kCkO5LCl4TZuCxlWgsDBki0NOrfkV%2BdHEqapi1v8btOaKVlwqcmhva99R0mX2kiaWLfjkdT3eexjhgr4M2QJP2FOr8sutqSX7GOJ87O%2FyVypdwMMQFcM8YqsNFfJDF702Uiszrra%2BXqHBQjNQDAQn1iesDiB5sLA1z%2BSHFHt&p=Al+Jazeera+mine+strait+of+homuz&type=fc_A0DBACA6D59_s69_g_e_d_n5500_c999#id=1&vid=94d80a7b5a1b9390a65997f232346b2b&action=click SD

-

John, you tend to have much more perspective on these issues than most.