Viking

-

Posts

6,085 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

Fairfax has stated they hold the FFH-TRS as an investment. What do you think Fairfax is worth? Does it matter? My guess is Fairfax’s book value at June 30, 2026 is likely around $1,310/share. Excess of FV over CV is likely $3.9B, or about $140/share after tax. That puts economic book value at $1,450 per share at June 30. This is a conservative number because it materially undervalues a number of assets like BIAL. (Yes, it does value Eurobank at market value.) Fairfax’s stock is $1,665. That puts its P/BV at 1.15x That looks crazy cheap to me for a company that has delivered best-in-class performance the past five years, is best-in-class at capital allocation and is better positioned than at any time in its history (insurance, investments and capital allocation). There are other important reasons economic book value of $1,450/share is conservative. Interest rates have spiked over the past 6 months. This runs through Fairfax’s balance sheet (sizeable unrealized bond losses ($800 million?). Yes, there is an offset (shock absorber) with IFRS ($400 million?), but it only appears to offset about 50% of the impact of higher rates. At the end of Q2, Fairfax will have booked those losses and they will be reflected in BVPS. Two of Fairfax’s largest equity holdings are down significantly ($740 million) in 1H 2026: FFH-TRS and Orla Gold. Fairfax has absorbed that investment loss - it is reflected in BVPS. Fairfax looks cheap. And the froth has been taken out of Orla which is positive for future returns. Bottom line, Fairfax looks cheap to me. If management continues to hold the FFH-TRS I will be a happy camper. Having said that, if they choose to sell some I will also be ok with it. Fairfax has the best information. And given how they have performed over the past 5 years they have earned my trust.

-

I am preparing a preview of Q2 earnings for Fairfax. Part of the process is listening to the prior quarter conference call. The comment below from Wade Burton, President and Chief Investment Officer, from the Q1 2026 call caught my attention (again). It is stuffed full of important and useful information (this is becoming typical for Wade's comments on the calls). Public versus private (advantages of each) Criteria used (profitability, balance sheet, management) Value investing (price paid matters) Update on recent investments (Meadow, Peak and Sleep Country) The advantage of partnering with Fairfax The strong team that has been built over the past 10 to 15 years at Hamblin Watsa (mirroring what Andy Barnard has done with the insurance business). How the company is positioned today: "especially important now" Welcome to "new Fairfax." ----------- Wade Burton: Fairfax Q1 2026 conference call ... I thought it would be a good quarter to give a discussion about how we look at investments in publicly traded common stocks versus investing in private companies. The underlying process is the same. We work to uncover true economic profits and or profit capacity. We think about where those profits are going. We focus on balance sheet and balance sheet flexibility. We think about the price we pay for those profits. The same underlying process for both public and for private. In both cases, we know management is a key factor. As Buffett pointed out, a great manager can’t save a leaky boat, but what we have learned is that they make a huge difference paddling boats that do float. The advantages of buying public common stocks is: the ability to capitalize on the moods of the stock market and liquidity. The ability to enter and exit an investment quickly is a good thing. The advantages of making direct investments in private companies is we control the profits. That is, we can choose to reinvest the profits in the businesses we’ve invested in, or we can take the profits out and invest them elsewhere. In general, the flexibility to invest in either public or private companies is a huge advantage for us. It allows us to be opportunistic, agnostic, and truly seek the best possible investments. For example, today, with the Shiller PE at all-time highs, you would not expect we’d find a lot of fifty cent dollars in the stock market, and we aren’t. We have been able to make outstanding acquisitions on the private side, including Meadow Foods, Peak Achievement, and Sleep Country. We have the advantage of a history of being terrific long-term partners. 40 years of fair and friendly transactions with a long line of very happy partners, along with permanent no call capital, makes us an attractive home for many companies. To do all of this well takes a skilled and focused investment team, and I’m so proud of the team we’ve built over the last 10 or 15 years. Our people are decision-makers. They are analysts and value investors. We have skilled defensive players and skilled offensive players. All have experience in public and private investments. You know, having the independence to make decisions is so important, and they’re all doing it. We call them in where we need them on the bigger investments. With that, it is amazing to watch them come together as a group. Having this team in place is especially important now, given how big and globally spread out we are and how big we hope and plan to be in the next 50 years.

-

Share buybacks are clearly the dominant use of capital for Fairfax. At 0.9% yield, the dividend is small. But when combined with the buybacks, the total of $2.8 billion over nine months is significant. The interesting thing is this is not the only thing Fairfax is doing on the capital allocation front. Here are a few things from 2026: AGT Foods: converted sponsor notes to equity ($249M) + add to position ($146M) Under Armour: add to position ~$265M? Exit Occidental for proceeds of ~$303M? Foran was taken out by Eldorado Gold Sale of ~50% of Poseidon for proceeds of $1.9B Purchase of Kennedy Wilson for $1.6B Purchase of Peller Estates for $279M Pending: Orla Gold takeout by Equinox Gold: set to close in Q3? Sale of Eurolife's life insurance business: set to close Q3? Fairfax has also been very active with debt issuance (and some cancellation). Of note, the insurance business continues to grow modestly. Bottom line, there is a lot going on under the hood in addition to meaningful stock buybacks.

-

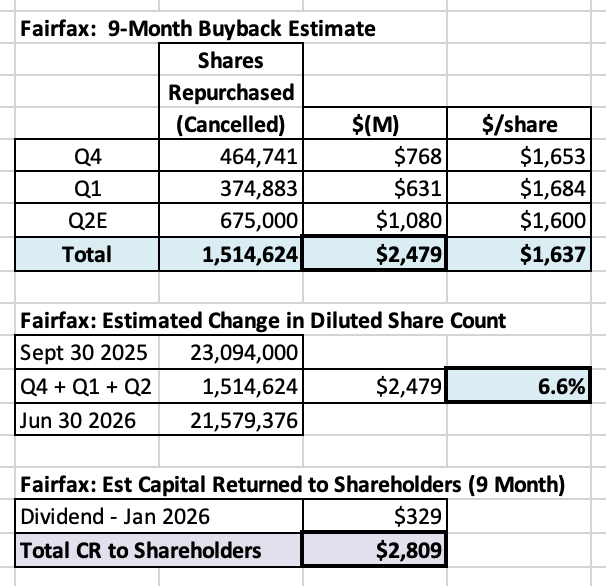

It appears Fairfax has been very busy on the share buyback front over the past 9 months (Q4-2025 + Q1 + EQ2-2026). We will get confirmation on Q2 amounts when Fairfax reports results. Shares repurchased: 1.5M, for $2.48B, or ~$1,637/share Diluted share count reduced: 6.6% Total capital returned to shareholders (including dividend): $2.81B Clearly, Fairfax feels their shares are trading at a very attractive valuation. And they are acting with conviction. ---------- Shareholder Friendly Management It is counterintuitive, but for long-term shareholders a low share price can actually be a gift — if the company is aggressively repurchasing shares. This is especially true when the discount persists for years. Buffett highlighted two major benefits. 1. Higher Per-Share Intrinsic Value This is straightforward arithmetic. When a company repurchases undervalued shares, the ownership stake of remaining shareholders increases. Intrinsic value per share rises immediately. 2. A Signal of Shareholder-Friendly Management This second benefit is more subtle — and often underappreciated. When management consistently repurchases stock below intrinsic value, it signals disciplined, shareholder-oriented capital allocation rather than empire building. Over time, investors reward this behavior with a higher valuation multiple. Buffett explained it this way in Berkshire Hathaway’s 1984 Annual Report: “The companies in which we have our largest investments have all engaged in significant stock repurchases at times when wide discrepancies existed between price and value. As shareholders, we find this encouraging and rewarding for two important reasons - one that is obvious, and one that is subtle and not always understood. The obvious point involves basic arithmetic: major repurchases at prices well below per-share intrinsic business value immediately increase, in a highly significant way, that value. When companies purchase their own stock, they often find it easy to get $2 of present value for $1. Corporate acquisition programs almost never do as well and, in a discouragingly large number of cases, fail to get anything close to $1 of value for each $1 expended. “The other benefit of repurchases is less subject to precise measurement but can be fully as important over time. By making repurchases when a company’s market value is well below its business value, management clearly demonstrates that it is given to actions that enhance the wealth of shareholders, rather than to actions that expand management’s domain but that do nothing for (or even harm) shareholders. Seeing this, shareholders and potential shareholders increase their estimates of future returns from the business. “This upward revision, in turn, produces market prices more in line with intrinsic business value. These prices are entirely rational. Investors should pay more for a business that is lodged in the hands of a manager with demonstrated pro-shareholder leanings than for one in the hands of a self-interested manager marching to a different drummer...” Warren Buffett – Berkshire Hathaway 1984AR

-

The short answer is I think your bracket of 1.2-1.5 looks pretty accurate these days (how the stock is actually trading). I think @Txvestor’s post above is spot on. Fairfax has been executing/performing exceptionally well for about 5 years now. IMHO, the current multiple range of 1.2-1.5x does not reflect that strong performance. As Fairfax continues to perform strongly - and their track record extends to 10 years - it makes sense to me the stock should trade at a higher valuation. But I really have no idea. My focus is fundamentals and capital allocation. Those topics… I have strong opinions.

-

@Maverick47, I find your comments very insightful and I learn a lot. Please keep them coming (it's like getting a peek behind the curtain). Thank you.

-

I am generally an idiot when it comes to understanding market multiple. I am looking forward to see what P/BV multiple (the range) Fairfax's stock trades at in the coming years. I think Fairfax's 2010-2020 multiple range was something 1.0x to 1.3x range. That looks much too low to use today, given the strong performance the company has delivered over the past 5 years and its strong prospects. But what is an appropriate multiple range to use today? Interestingly, what multiple will Mr. Market use? I am not optimistic. I think there is a good chance Fairfax stays cheap. For a whole bunch of reasons. If I am right, the silver lining is Fairfax will be able to buy back an enormous amount of stock at a low valuation. For long term shareholders that would an amazing outcome. Of interest, that is exactly what they have been doing for the past 6 years.

-

@wondering, I appreciate you taking the time to post your thoughts and questions. That is how we all learn. Here are some answers to your questions: "1. ...are you saying that the equity-accounted investments (20-50%) does not reflect the economic earnings of those." My post tried to weave together two different partnership models. The accounting treatment for each is very different (consolidated versus associate). Fairfax's share of earnings from the associate holdings (20 to 50%) showed up in the 'share of profit of associates' bucket. "2. When Gulf Insurance was equity-accounted, did Fairfax still have control in investing the float?" I don't know. My guess is Fairfax, as the minority partner, did not have control of the float. Kipco was the majority partner. "3. The head guy OMERS recently left the pension plan. Does anyone on the board be the know if this will materially effect the relationship with Fairfax. In the past OMERS seems to be the go-to guys for partnering on big investments? I guess it is a speculation question." I don't know. OMERS is a massive organization ($145 billion in assets under management?). The amount they have invested with Fairfax is pretty small (from their perspective) and they earned a solid return of the various investments over the years (collectively). It looks to me like Fairfax has been a very good and profitable partner for OMERS. I agree with your final point... I think Fairfax has a long list of companies they could partner with in the future. And given how strong the company's performance has been over the past 5 years, my guess is the list is getting longer...

-

My guess is Fairfax wants employees to write new business - if it hits Fairfax's underwriting hurdle rate. Incentives drive behaviour. Below are a couple of details. They provide some useful information. Underwriting profit: One part of the compensation program is the employee stock ownership plan. Part of it is linked to underwriting profit. Exhibit 1: Prem Watsa on Employee Stock Ownership Plan (2025 Annual Report) Fairfax also has an Employee Stock Ownership Plan that is available to essentially every employee in the company. The plan offers each employee the opportunity to take up to 10% of their salary annually in Fairfax shares. The company will automatically match 30% and then if certain targets are met (primarily underwriting profit), the company matches an additional 20%. The participation rates differ by company but generally for our large companies, we have a participation rate of approximately 60% and it has been increasing over time. (More on this plan in the Miscellaneous section at the end of the letter.) Long term timeframe: Another part of the compensation program is the annual bonus for senior executives. 50% is cash and 50% is Fairfax shares that vest over 5 years. Exhibit 2: Prem Watsa on Employee Ownership (2025 Annual Report) We continue to encourage all our employees to be shareholders of Fairfax. We think it will be a great investment for them over the long term and great for the company to have our employees as shareholders in the company. As part of that initiative, close to 10 years ago we decided to have a general principle that our annual bonuses to senior executives across the company would be awarded 50% in cash and 50% in Fairfax shares that vest in five years. As these bonus shares are awarded, the company buys the shares in the market (which comes out of shares outstanding) and they are recorded as treasury shares, as shown in the table below. As the shares are vested and or exercised, the shares are then reissued and come out of treasury shares and back into shares outstanding. You can see over the years our treasury shares have increased from 0.6 million to 1.8 million today. We think this is fantastic and hope they continue to grow over time.

-

For those who want more information, below is the full quote (lightly edited) from Fairfax's 2026 AGM that Article #6 above was based on. Question from Moderator Jeff Stacey Prem and Peter, our first question is about the current insurance environment. The question is as follows. Fairfax had record underwriting profits in 2025 of $1.8 billion and achieved its objective of $1.5 billion. You commented, however, in your shareholder letter that insurance pricing is beginning to soften. I would appreciate hearing any additional comments you might have about the current insurance underwriting environment. And specifically, do you think that Fairfax can still achieve its $1.5 billion underwriting profit target in a soft insurance market? V. Watsa - Founder, Chairman & CEO Thank you, Jeff. Peter will usually answer this. But we do have Andy Barnard, Brian Young, Lou Iglesias and Silvy Wright here. So, we'll ask them instead. As Andy makes his way up to speak, let me just say… yesterday I had people ask me: “What is the biggest -- best -- acquisition you've ever made?” The best one is Markel Insurance - the first one (1985) - because otherwise, you're not in the P/C insurance game. And the second best was a small company called Skandia America Re (1996). And why? Because I had to get someone to run Skandia. I went to New York three times to get Andy Bernard. The first time he said, "You got to be kidding me.” Over dinner he said, “I'm not going to leave Transatlantic to come and join Skandia." That's how it began. After a second and third attempt, ultimately, we were fortunate to get him 30 years ago. He's had a huge impact on Fairfax. In 2011, all of the insurance companies began reporting to him. After he started in his new role – 15 years ago (2011) – he said that he hoped that the insurance business will have the same reputation of being fantastic like the investment business that we had at the time. And the investment business did a little less well, and the insurance business has done fabulously well. Andy, over to you. Come on in. Andrew Barnard - Chairman of Fairfax Insurance Group Thank you very much, Prem, for all of that. I'm going to let Brian and the others talk about our position, the market and our prospects. As Prem mentioned, I've been in this role now for 15 years, and I thought I'd just give a little brief broad perspective on how I look back on that. I divide that 15 years, which started in 2011, into two periods. First, 2011 up to 2019. Looking back with the benefit of hindsight – this was a period of preparation. During that period, we added Allied World and Brit – two very powerful new platforms with capabilities that really build out our suite of products. We had Crum & Forrester, bolstering its capabilities. We had a few small acquisitions. Earlier on in that time Northbridge finished its integration, which really positioned it as a much stronger company. And of course, during this time, Odyssey and Zenith flourished. (Yes, Zenith had a few tough years at the beginning.) And we built out the international operation during the latter part of that first period. As Peter mentioned, it has become a significant business that we think will serve us well in the future. This was really a period of preparation that brought us to 2020. At Fairfax, across our companies, we now had in place excellent leaders, leaders that are fully aligned with Fairfax’s culture, that embody the trust, the transparency, the talent that without which our decentralized system could not function. That's all in place as we roll into 2020. Of course, the big thing at the start of the year was the pandemic. A lot of companies heading to the hills, a lot of uncertainty. Plus, we had a very attractive hard market that had already been underway – and I think the pandemic just accelerated it. So, we were at that time in just a unique position because of our structure, our capability, our leadership to thrive. And thrive, we did. Over the subsequent years, we go into the second period, 2020 up to 2025. From 2020, we virtually doubled our premium volume, and almost all of that was organic with the one exception of GIG. The vast majority of that growth was organic, driven by our companies by their leaderships, by their management teams. And more importantly than that, our underwriting profit over that period more than quadrupled. This is where we really came into our heyday. Today, to 2026, we're recognized as an underwriting powerhouse in the industry by the marketplace, by the rating agencies. We had huge increases in our ratings over the last 1.5 years. Looking back on it all over the past 15 years – with the benefit of hindsight – we just positioned ourselves so favorably to really take off when the market conditions were supportive of that strategy. I believe that what we built is built to last. It is built to withstand the pressures of the market cycle. Those who follow the industry know that we're in a softening cycle where things become more challenging. But we're very confident about our capabilities – about our management abilities – to navigate through some more challenging times and to sustain superior performance as we go into the future from here. I've been in this industry now for close to 50 years. I've been at Fairfax for 30 years. I'm not going anywhere quite yet. However, my good friend and partner of the last 36 years, Brian Young, is taking on a larger and larger share of the oversight responsibilities in Fairfax. Those of you who have followed Odyssey will know Brian took the helm in 2011. It's very clear that Brian is someone that knows how to make money in this business. And so, I think our future is very, very bright as we move forward from here. So let me turn the microphone over to my friend, Brian Young. Brian Young - President of Fairfax Insurance Group Thank you, Andy. I learned some big news a few minutes ago. Andy told me that he is going to be a grandfather for the third time. So big hand to Andy. I will cover the AI question (from earlier), the current market environment and our ability to generate an underwriting profit in the current environment. But first I want to highlight, as Peter mentioned, $1.82 billion of underwriting profit in 2025, fractionally higher than $1.79 billion in 2024. Combined ratio of 93%. Embedded in that was 4.8 points of CAT loss or the $1.2 billion, the biggest being the California wildfires in Q1. Within the 93%, we benefited from 2.9 points of favorable reserve development. And it's important to note that Fairfax has had 19 consecutive years of favorable reserve development for the last 2 decades. Our reserves have been a store of value. As you all know, all of our companies are really focused on disciplined underwriting and strong reserving. Prudent reserving is really foundational to disciplined underwriting. We have more than 30 operating companies. Nearly all of them equalled or exceeded expectations from an underwriting perspective in 2025. The small number that didn't – we weren't expecting them to make underwriting profits given the market circumstances that they faced. So, there were no negative surprises in any of our companies. I'd like to highlight a few standout performers, focused first on the big companies. Let's start with the most recent recipient of the Athappan Award, Allied World. Our largest insurance company generating record underwriting profit of $546 million – a fantastic result. Congratulations, Lou and to the team. I'm going to let Lou come up and tell us what the secret sauce is that's made Allied World so successful. The second company I'd like to highlight is last year's recipient of the Athappan Award, Northbridge. Silvy and team delivered the lowest combined ratio, at 88.3%, of all our big companies. In the last 4 out of 5 years, Northbridge has delivered a combined ratio below 90%. And Silvy will come up after Lou and give us an update on Northbridge. Turning to the international side. We generated $220 million of underwriting profit, more than double what we generated in 2024. The standout performers – Colonnade, Bryte and Singapore Re – all generated record underwriting profits. Singapore Re, headed by Philippe Mallier, had not only the lowest combined ratio on the international side, they had the lowest combined ratio of all of our companies at 77%. Well done, Philippe. Our premiums were $33.3 billion. It is slowing down. The market is getting more challenging, no doubt. And we have to exercise more discipline. We have to be more selective in the risks that we take. We have to focus on our line size deployment. But we still think there's opportunity out there in the market. The sectors of the business that are under the most pressure are the ones that have generated the most profit. So yes, the margins are shrinking, but we still think the margins are ok. When the margins are not there - when there is not that margin of safety we need to take on the volatility of insurance – then we're going to scale back. There's no pressure on any of our companies to write for top line growth. And I've experienced that at Odyssey working there for 28 years, leading it for 14 years, never did I or any of our people have any pressure to write for top line. On the question of AI, it's important in our decentralized structure, innovation comes from the ground. It can't be forced from the top down. And we've got 30-plus wonderful businesses. Everyone is focused. AI may well be very transformative. We're not at the cutting edge, and we don't really want to be at the cutting edge. We're where we think we need to be in the pack with the rest of the insurance industry. To understand and take advantage of the innovative things that we're doing at the company level, we formed an AI working group, across the Fairfax organization. We have more than 75 people participating in the working group. We have developed more than 100 use cases. We have a SharePoint site. If we develop a use case in a company in a certain part of the world, we can share that with the other companies through the forum, through the SharePoint site. In terms of the AI use cases, most of them have really been focused on improving process, doing things faster and smarter – trying to underwrite more business efficiently through the use of AI. Using AI to inform our underwriting decisions. Marc Adee (President of Crum and Forster) has used the phrase, and I think it's great, does AI bang the cash register, does it lower your loss ratio, does it lower your expense ratio? I would say right now we're not banging the cash register yet. With AI, we are able to underwrite more business using the tool than previously. Lowering the loss ratio, lowering the expense ratio in terms of the AI tools that we're using, that's really the focus. And I think lastly, it's really important to say, and Prem has emphasized it ad nauseam that AI will not cost us any jobs. We don't believe in laying off employees. Period. And that includes AI. If AI allows us to operate more efficiently then maybe the rate of growth in our employee count will slow down, which will help the expense ratio. But it won't come at the expense of people. Thank you. Now I would like to turn it over to Lou. Louis Iglesias - President of Allied World Thank you, Brian. Great to see everybody. It's good to see so many of you, I only get to see once a year and talk about our businesses here at Fairfax and at Allied. And it's also not every day that I feel like Allied World has won the Stanley Cup. So we're really proud of that as well. Brian mentioned our underwriting profit. We did have a record year last year on underwriting profit. We also had a high watermark on our net income. And I just want to recognize the investment group at Fairfax, who does a tremendous job on our portfolio. Having that type of net income really helps our cash flow and everything else. So, it's really, really good to see. We grew our company to $7.4 billion last year. And Brian talked about the market a bit. It is softening some. I would say it's getting a little bit more price competitive. But for those of you who've been with our industry for a long time, it's not a traditional soft market. We're not bottoming out. Terms and conditions are holding pretty well. Combined ratios don't have so much pressure on them, still manage the profitability. There are opportunities around the world to be able to get some growth. So we're not giving up on that because I think there are certainly some opportunities. What I wanted to talk about just for a couple of minutes is what are some of the things that we do to help us manage the cycle. We feel like we've built a company that could perform in all segments of the cycle. And in order for that to happen, we have to execute on many strategies every single day. The company has to be structured in a way to give us that ability. There are a couple of things in there. The first thing to talk about is the structure of having a very flat organization. You see that elsewhere in Fairfax. We have a very flat organization at Allied. We don't have many layers. So strategies and communication moves quickly. This gives us the opportunity to move fast in different marketplaces around the world. So as the markets change, we can change strategies. We can execute on those strategies. Our underwriters are at the desk since there's not lots of layers. They don't have to get multiple sign-offs to do their job to able to make a decision. We run with the mantra of hire really great people. And give them the authority and accountability to be able to get the job done. Additionally, we have product diversity – over 40 products. We are in 29 offices around the world – 11 countries and 4 continents. We're expanding our presence around the world geographically. So, the earnings stream is very diverse. And when we have that type of diverse earnings stream it really limits earnings volatility. So when the market starts to get a little bit tougher, it's really helpful to have different earnings streams because you may have to slow some down. If you're not getting the marketplace that you like in a certain product or a certain country, you're going to have to slow that down, but maybe there's an opportunity someplace else. So the diverse earnings stream is really very helpful. And I think you see that throughout Fairfax as well. The third thing that I would touch on is underwriting discipline. Underwriting discipline helps in every marketplace, whether it's a hard market, soft market in the middle. It's extremely important. It runs through every Fairfax company. It's part of the culture of Fairfax. Now what does that mean really? Our underwriters understand rate adequacy, they understand when they're negotiating a deal, where that rate crosses the line to not being enough for the exposure that they're taking on. When we run into that situation, we have the ability to say no. We say no a lot more than we say yes. But what we really prefer to do is to say, "No, we don't like the deal that way, but we do like it this other way. And we'll put a proposal out that works for us, and we hope works for the client. And we've been able to do business like that and sell deals like that fairly often, even in this marketplace when things are getting just a little bit softer. So that's been very helpful. Now nothing works without great people. And every year, I come up here, and I think I talk about how great the people are at Allied. We've had people with us for a very long period of time. They've seen all different cycles, so they understand how to manage in and through the different cycles. And we have a very low attrition rate at the company. So our people are really the key to making all the strategies work. And so for us, we're going to continue to do the things that we're good at. As the markets soften some, we're going to limit our mistakes so that when the market does get to a better place, we can do all the things that Andy talked about that we did a couple of years ago and not have any distractions. Thank you very much, everybody. Have a great day. Silvy Wright - President of Northbridge Financial Good morning, everyone. First, I'll start with a little confession to Lou. Northbridge employees wanted to do a Rory McIlroy (repeat as winners of the Athappan Cup), but we are happy that Allied World won this year. First a little perspective on Canada. Northbridge represents the Canadian insurance operations for Fairfax. With $3.4 billion in revenue, we're the third largest commercial insurer in Canada. We have a very good position - maybe a smaller fish at Fairfax but a bigger fish in this country. What are market conditions? What happened in '25, as Lou said, the price competition really started to ramp up. And we're starting to see competitors trying to buy business. And sorry, I apologize for being a broken record, but once again, we are not pressured to write premium at a loss. And so, in 2025, our employees did the right thing. They remained disciplined, not only in underwriting but claims and expense management. But equally important, we doubled down on really focusing on customer loyalty, customer service and customer safety. So not only be there when things go wrong, but we're trying to help our customers have safer operations. As a result, we did not grow in 2025. However, we did have a record year, as Brian noted. In 2026, it looks like the price competition continues and we will manage accordingly. Along with just being disciplined, we're also looking at building areas where we can grow when it's the right time to grow. For instance, increasing our lines on renewable energy in Canada. So just manage the market and then be ready to go when it's time. And one more comment. We talked about the culture many times and the beautiful word of being empowered not just at the president level, but throughout the company. I just wanted to share with you that our employees are like you, they're shareholders. Over 70% of our employees at Northbridge are shareholders. So not only are they empowered but they're owners in doing the right thing. Thank you. V. Watsa - Founder, Chairman & CEO Thank you very much Silvy. Peter, anything to add, final words, on the insurance industry? Peter Clarke - President & COO Sure. Just two quick things, Prem. And I mentioned in my remarks that we write $33 billion of premium across the world and that grew by 2.3% this year. It's interesting when you look at the international operations and how we benefit from diversification and scale. Bryte in South Africa grew 20% this year, Colonnade 18%, Asia was up 15% and Polish Re was up 15%. And so even though North America rates are coming down, we're maybe not growing as much, we have all these opportunities around the world. Secondly, I just have to comment that we have 2 cups in Fairfax. One is the Mr. Athappan Cup. And we also have a hockey game between the Fairfax head office and the Allied World Group, and unfortunately, now Allied owns both cups for this year and I have to say it did come into the evaluation process a bit, but we left that aside.

-

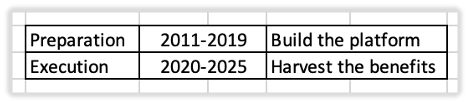

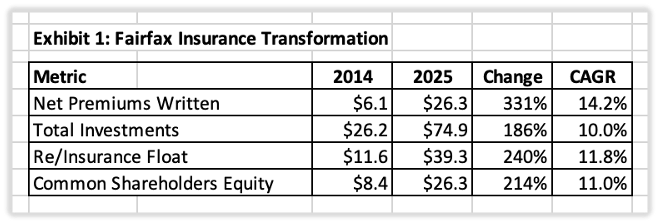

Article 6 - the final article in our 6-part series on Fairfax's insurance business. Why Fairfax's Insurance Platform Is Built to Last Insights from Fairfax's 2026 AGM In a previous article, we reviewed Fairfax's insurance transformation from 2014 to 2025. That story was told through financial results. Net premiums written increased from $6.1 billion to $26.3 billion. Float more than tripled. Most importantly, shareholders participated in that growth on a per-share basis. The increase in size is easy to see. It is evident in Fairfax's reported financial statements. What is less well understood is how much the quality of the insurance franchise has improved over the past fifteen years. Record underwriting profits are one visible sign of that improvement, but the real story lies beneath the numbers. The 2026 Annual General Meeting provided compelling evidence of that transformation. Rather than focusing on financial results, investors heard directly from the executives who built and now operate Fairfax's insurance business. Although each spoke from a different perspective, together they described the same underlying system: a decentralized organization built around exceptional people, disciplined underwriting, and long-term thinking. Understanding both changes—the growth in scale and the improvement in quality—is essential to understanding Fairfax today—and why the company's insurance business has never been better positioned for the future. Prem Watsa: It Starts with People Prem Watsa opened the discussion by talking about acquisitions. But he was not really talking about acquisitions. He described Markel (Canada) as Fairfax's most important acquisition because it established the company in the property and casualty insurance business. He then identified Skandia America Re as his second most important acquisition—not because of the business itself, but because it ultimately led to Andy Barnard joining Fairfax and building its global insurance operations. As Watsa explained: "The best one is Markel Insurance because otherwise you're not in the P/C insurance game. And the second best was a small company called Skandia America Re... because it brought Andy Barnard to Fairfax." It was a classic Prem Watsa answer. Fairfax's greatest asset is not its float, investment portfolio, or insurance subsidiaries. It is the people running them. That theme ran throughout the AGM and provided the foundation for everything that followed. Andy Barnard: Fifteen Years of Preparation Andy Barnard then provided perhaps the clearest framework for understanding Fairfax's recent success. Looking back on his fifteen years leading Fairfax's insurance operations, Barnard divided the period into two distinct phases. From 2011 to 2019, Fairfax prepared for future growth. The company acquired Brit and Allied World, expanded internationally, strengthened leadership teams, and built the organizational capabilities needed to compete on a global scale. The second phase began in 2020. With the platform in place, Fairfax was positioned to capitalize on a hardening insurance market. Premium volume nearly doubled, underwriting profits surged, and years of preparation translated into exceptional operating results. Barnard summarized the period this way: "The first period, from 2011 to 2019, was a period of preparation... The second period, from 2020 to 2025... we virtually doubled our premium volume, and our underwriting profit more than quadrupled." Exhibit 1: Andy Barnard's Framework Barnard's framework also helps investors better understand the insurance cycle. Hard markets create opportunities, but only companies that have spent years preparing are positioned to capitalize on them. Fairfax's insurance franchise was built before the hard market arrived. The hard market simply revealed its strength. Brian Young: The Message for Today If Barnard explained the past, Brian Young focused on the present. His message addressed investor concerns about a softening insurance market. Fairfax remains committed to underwriting discipline. There is no pressure on operating companies to write business simply to maintain premium growth. Growth matters, but profitability matters more. As Young stated: "There's no pressure on any of our companies to write for top line growth." This helps explain why growth has recently slowed across parts of Fairfax's insurance operations. Management is deliberately choosing underwriting profitability over market share. For long-term shareholders, that is exactly the right decision. Lou Iglesias: How Discipline Works Lou Iglesias of Allied World provided a clear illustration of Fairfax's decentralized operating structure. Authority is pushed down to experienced underwriters. Decisions are made close to the customer and close to the risk. Underwriters are trusted to exercise judgment—including walking away when pricing becomes inadequate. Iglesias summarized the philosophy simply: "Hire really great people and give them the authority and accountability to get the job done." Rather than relying on centralized oversight, Fairfax relies on capable people supported by clear accountability. It is the practical application of the philosophy Prem Watsa described at the beginning of the discussion. Silvy Wright: Discipline in Practice Silvy Wright showed how that philosophy works in practice. Northbridge did not pursue premium growth aggressively in 2025. Instead, management maintained underwriting standards while competing through customer service, claims management, relationships, and helping customers improve safety. Growth slowed. Results remained strong. As Wright explained: "We are not pressured to write premium at a loss." For investors, this illustrates an important principle. In insurance, slower premium growth is not necessarily a sign of weakness. It can be evidence of underwriting discipline. Peter Clarke: The Benefits of Scale Peter Clarke concluded the discussion by highlighting one of Fairfax's greatest competitive advantages: diversification. Today, Fairfax operates across numerous geographies, products, and markets. When pricing weakens in one area, capital can be redirected to more attractive opportunities elsewhere. As Clarke observed: "Even though North America rates are coming down, we have all these opportunities around the world." This flexibility is one of the lasting benefits of building a global insurance platform. What Investors Learned An earlier article documented Fairfax's insurance transformation through financial results. The 2026 AGM explained how those results were achieved. A consistent picture emerged. Fairfax's success was not simply the product of a favorable insurance market. It reflected years of preparation, disciplined capital allocation, decentralized decision-making, and an unwavering commitment to underwriting profitability. More importantly, the AGM demonstrated that Fairfax's insurance business has become better—not just bigger. Over the past fifteen years, the company has assembled an exceptional leadership team, strengthened its underwriting culture, expanded into attractive global markets, and built a decentralized operating model that empowers talented people to make disciplined decisions close to the customer. These improvements are structural rather than cyclical. Insurance pricing will inevitably fluctuate over time. Premium growth will accelerate during hard markets and slow during soft markets. Those cycles are outside management's control. The quality of Fairfax's people, its underwriting discipline, its decentralized operating model, and its global platform are different. Those are enduring competitive advantages that should persist through multiple insurance cycles. The financial statements tell investors that Fairfax has become much larger. The 2026 AGM explained why it has become much stronger. Understanding both changes is essential to understanding Fairfax today—and why the company's insurance business has never been better positioned for the future.

-

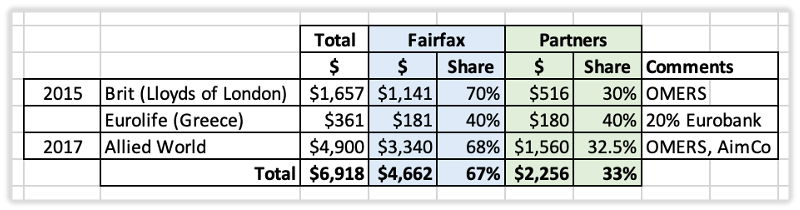

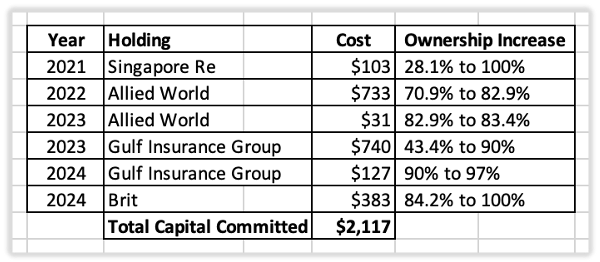

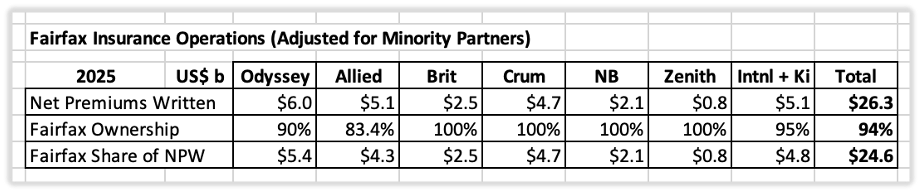

Article #5 in our 6 part series on Fairfax's insurance business. Let me know if I got the high-level description of the call option feature correct. Partnerships: An Underappreciated Growth Strategy Previous articles explained how Fairfax built one of the world's largest property and casualty insurance groups through disciplined acquisitions, strong underwriting, and organic growth. Another important contributor has received much less attention: partnerships. Over the past fifteen years, Fairfax repeatedly partnered with long-term investors to accelerate the expansion of its global insurance platform. Rather than funding every acquisition itself, management shared ownership of selected businesses, allowing Fairfax to acquire interests in more high-quality insurers than it could have using only its own capital. The strategy evolved over time. Partnerships initially maximized the size of Fairfax's insurance platform. As internally generated capital accumulated, Fairfax increasingly used that capital to increase its ownership of those same businesses. Together, the two phases illustrate one of Fairfax's more innovative capital allocation strategies. Phase One: Building the Insurance Platform By the early 2010s, Fairfax's acquisition strategy had evolved. Rather than focusing primarily on distressed insurers, management increasingly targeted higher-quality insurance businesses. These acquisitions required substantially more capital but also offered stronger long-term growth prospects. At the same time, Fairfax's equity hedging program reduced internally generated capital available for acquisitions. Partnerships helped solved that problem. By investing alongside long-term partners, Fairfax could pursue larger opportunities without relying solely on its own balance sheet. Fairfax generally used two partnership models. In some cases, it acquired control immediately. In others, it acquired a significant minority interest and patiently waited for the opportunity to obtain control. Although structured differently, both approaches pursued the same objective: long-term ownership of outstanding insurance businesses. Model 1: Controlling Partnerships In some transactions, Fairfax acquired control immediately while inviting partners to invest alongside it. Fairfax sourced the opportunity, negotiated the acquisition, and remained the controlling shareholder. Its partners—primarily Canadian pension funds—provided part of the required equity. Brit and Allied World are the best examples. Exhibit 1: Fairfax – Model 1: Controlling Partnerships The three largest transactions required almost US$6.9 billion of capital. Fairfax invested approximately US$4.7 billion, while partners contributed US$2.3 billion. As a result, Fairfax controlled almost US$7 billion of insurance acquisitions while providing only about two-thirds of the required capital. Accounting Implications Because Fairfax owned more than 50% of these businesses, it consolidated 100% of their premiums, assets, liabilities and operating results into its financial statements. Economically, however, Fairfax owned less than 100%. The partners' share of earnings was reported separately as non-controlling interests. Model 2: Strategic Minority Investments Not every opportunity required immediate control. Sometimes Fairfax acquired a significant minority interest while another shareholder remained in control. Rather than insisting on ownership from day one, management built a long-term relationship, learned the business and waited patiently for the opportunity to acquire control. Singapore Re and Gulf Insurance Group illustrate this approach. Fairfax was comfortable sitting in the passenger seat until the opportunity arose to move into the driver's seat. Exhibit 2: Fairfax – Model 2: Strategic Minority Investments Fairfax initially acquired a 28.1% interest in Singapore Re in 2009 and a 43.4% interest in Gulf Insurance Group in 2010. In both cases, Fairfax eventually acquired control years later. Accounting Implications Because Fairfax initially owned between 20% and 50%, these investments were accounted for using the equity method (share of profit of associates). As a result, their premiums, underwriting results and float did not appear in Fairfax's reported insurance operations until control was obtained. The different accounting treatments help explain why the economic impact of Fairfax's partnership strategy is not always obvious from the financial statements. Phase Two: Increasing Economic Ownership By 2021, Fairfax had entered a new phase. Years of disciplined underwriting, a strong insurance market, improving investment income, and substantial operating cash flow began transforming the company’s financial position. Fairfax was generating far more capital internally than it had a decade earlier. Rather than buying new insurers at significantly higher valuations, management began increasing its ownership of businesses it already owned. Between 2021 and 2024, Fairfax committed approximately US$2.1 billion to buy out partners in four existing insurance businesses. Singapore Re: increased ownership to 100% Brit: increased ownership to 100% Gulf Insurance Group: increased ownership from 43.4% to approximately 97% Allied World: increased ownership from 70.9% to 83.4% Exhibit 3: Fairfax – Insurance Partners Bought Out (2021–2024) The strategy had evolved. Initially, partnerships allowed Fairfax to build a larger insurance platform than it could otherwise have afforded. Now they allowed Fairfax to increase its ownership of the underwriting profits, investment income, float, and long-term value generated by that platform. Why Investors Miss the Economics The accounting creates an interesting paradox. During the first phase of the strategy, controlling partnerships immediately increased Fairfax's reported premiums, underwriting results, and float because those businesses were fully consolidated. During the second phase, buying out minority partners produced no change in those reported operating measures because the businesses had already been consolidated. Instead, the benefit flowed directly to Fairfax shareholders through increased ownership of the earnings those businesses generated. The insurance platform did not become larger. Fairfax simply owned more of it. That distinction is easy to overlook. Many investors focus on premium growth when evaluating insurers. Viewed through that lens, buying out minority partners appears to accomplish very little. Economically, however, Fairfax increased its ownership of businesses already producing substantial underwriting profits, investment income, and float. The growth shifted from the top line to the bottom line. For long-term shareholders, that is what ultimately matters. Controlling Partnerships: The Call Option Advantage The controlling partnership model contained another important feature: call options. When Fairfax negotiated these transactions, it secured the right to purchase its partners' interests in the future using valuation frameworks established at the time of the original investment. What is a call option? "A call option is a financial contract that gives the buyer the right, but not the obligation, to purchase a specific stock or asset at a predetermined price (the 'strike price') before a set expiration date. Buyers pay a fee, called a 'premium,' for this contract." — Investopedia What makes a call option valuable? "The primary benefit of holding a call option is the right, but not the obligation, to buy an asset at a set price before a specific date. This allows you to profit if the asset's market price rises, while strictly limiting your total potential loss to the initial cost paid." — Investopedia The same principle applies to Fairfax's controlling partnerships. The best time to acquire insurance businesses is typically during a soft insurance market, when underwriting results are weaker and valuations are generally lower. The most expensive time is often near the end of a hard market, when strong premium growth and improved underwriting profitability have increased earnings and driven valuations materially higher. Many of Fairfax's partnership agreements were negotiated during a soft insurance market. The call options established valuation frameworks at that time. Since then, one of the strongest hard insurance markets in decades has materially increased underwriting profits, earnings, and the value of high-quality insurance companies. The practical effect is significant. Fairfax can increase its ownership of certain businesses today while paying prices based on valuation frameworks negotiated during a soft market. In effect, management has the opportunity to acquire larger ownership interests in high-quality businesses at below-current market valuations. For shareholders, the call option feature transformed what initially appeared to be a financing arrangement into a long-term capital allocation advantage. What Remains? Fairfax is approximately half way through the process. Between 2021 and 2024, Fairfax increased its ownership of Singapore Re to 100%, Brit to 100%, Gulf Insurance Group to approximately 97%, and Allied World to 83.4%. By 2025, Fairfax economically owned approximately US$24.6 billion of its reported US$26.3 billion of net premiums written. Minority partners now account for only about US$1.7 billion, or roughly 6%, of reported premiums. Exhibit 4: Remaining Minority Interests (2025) The largest remaining minority interests are Allied World and Odyssey, where Fairfax owns approximately 83.4% and 90%, respectively. These businesses represent the largest remaining opportunity to increase Fairfax's ownership of an insurance platform it already controls. What Have We Learned? Fairfax's partnership strategy was much more than a financing tool. It was an innovative capital allocation strategy designed to exploit the insurance cycle. During the soft market, partnerships allowed Fairfax to acquire substantially more high-quality insurance businesses than it could have financed using only its own capital, when valuations were most attractive. As underwriting profits, investment income, and operating cash flow strengthened, management shifted to the second phase of the strategy—using internally generated capital to increase its ownership of those same businesses rather than acquiring new insurers at much higher valuations. The call option feature made the strategy even more powerful. By negotiating the right to purchase its partners' interests using valuation frameworks established years earlier, Fairfax positioned itself to increase ownership after one of the strongest hard insurance markets in decades while effectively paying soft-market prices. The accounting makes the economics easy to miss. Partnerships initially increased reported premiums because controlled businesses were fully consolidated. Later buyouts produced little change in reported premiums, but materially increased Fairfax's ownership of underwriting profits, investment income, float, and future earnings. Viewed across an entire insurance cycle, this is classic Fairfax: patient, creative, unconventional, and long term in its thinking. Management built flexibility into the original transactions, waited for the economics to become highly favourable, and then deployed internally generated capital when the opportunity was greatest. The result was a larger insurance franchise, greater economic ownership for common shareholders, and another meaningful contributor to long-term per-share value creation.

-

A general question for board members… Given how important float and investment leverage is to the business model of companies following in Buffett’s/Berkshire Hathaway’s footsteps is there a reason Markel doesn’t mention it? I have always found that peculiar.

-

@sholland and @patterson, thanks for the comments. I am rewriting the chapter on leverage (taking it from two to one). My plan is to include Buffett’s comments comparing float to equity there. Should be done in a couple of weeks.

-

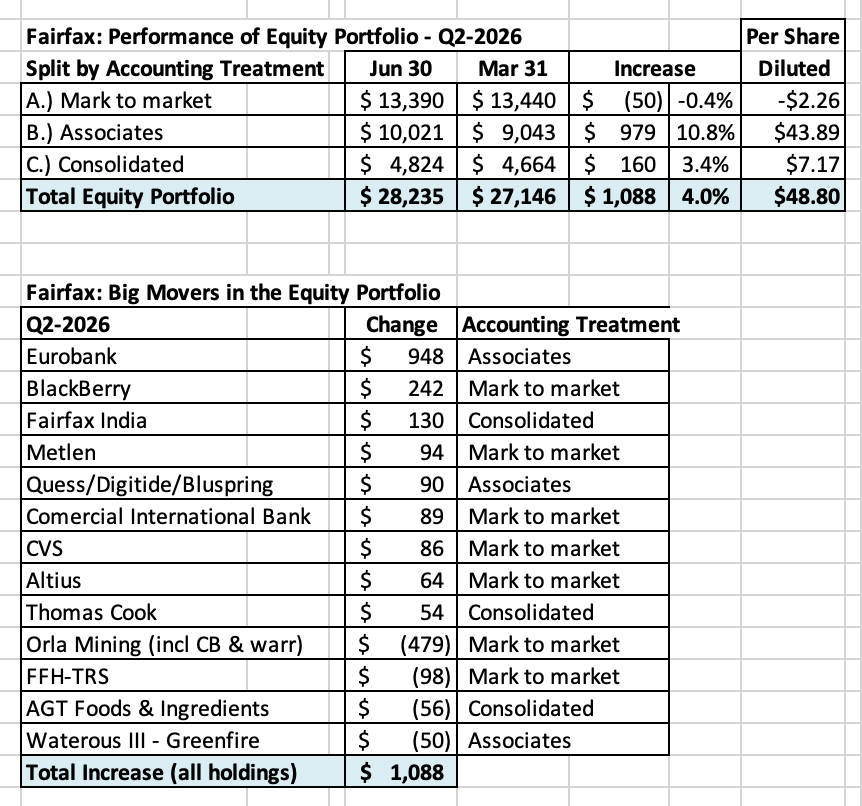

On balance, Fairfax's equity portfolio had another solid quarter, up ~$1.1 billion or ~$50 per diluted Fairfax share (pre-tax). The Greek Freak (Eurobank) continues to deliver MVP caliber performance. Strong US$ is taking gold out behind the woodshed - Orla was the big loser in the quarter. Lots of Fairfax's holdings are doing well - strength is broad based. Looks like the mark to market impact could be slightly negative. BlackBerry will be a wild card - Fairfax has been selling down its position in BB over the past year. If they continued to sell in the quarter the gain will not match what I have below (I used 25 million as my share count). Eurobank paid Fairfax a dividend of $95 million in mid-June. Given it is an associate holdings, it will not show up in income statement. On the balance sheet, cash will increase and carrying value for Eurobank will be reduced (by dividend amount). My spreadsheet does not capture what has been happening at a large number of holdings - like the non-insurance consolidated holdings. As a result, it is a conservative estimate. Of course the big news from an earnings perspective in Q2 is the sale of ~50% of Poseidon that will deliver a realized investment gain of $837 million. In Q3, when the sale of Eurolife's life insurance business to Eurobank closes in Q3 we will see another +$300 million realized investment gain. PS: I attached my Excel file if board members want more details (at bottom of post). Fairfax May 2026.xlsx

-

@dartmonkey, i appreciate the feedback. I will be making a few edits to my original based on your comments. Your second comment is bang on. When it comes to capital allocation, Fairfax bought low in 2015-2017. And from 2014 to 2025 they have also been selling high: First Capital, ICICI Lombard, pet Insurance and Ambridge. The sales realized significant proceeds and investment gains… that was in addition to the best in class growth in net premiums written per share they were able to deliver. Impressive. I have a coming article on how they have used partnerships as a strategy to grow their insurance business especially over the past 15 years. GIG is a good example of where Fairfax was the minority partner. Allied World isa good example of where they were the majority partner. What is so impressive about Fairfax is all the different levers they are pulling these days to drive per share value over the long term. Their capital allocation toolbox is full. And they have become very proficient with how they use each tool.

-

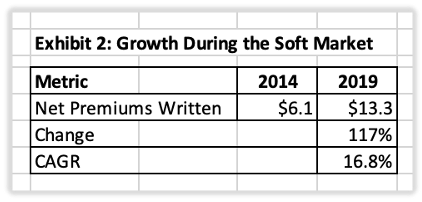

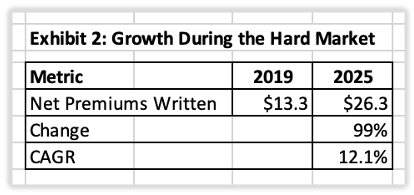

Article 4 into our deep dive into Fairfax's insurance business. What did they do in the last soft market? Fairfax's Insurance Transformation (2014–2025) One Insurance Cycle. One Management Team. One Remarkable Transformation. One of the best ways to evaluate management is to examine what it accomplishes over an entire business cycle. The eleven years from 2014 to 2025 provide an excellent test for Fairfax. During this period, the company navigated both a prolonged soft insurance market and one of the strongest hard markets in decades. The result was one of the most significant transformations in Fairfax's history. Several observations stand out. First, Fairfax dramatically expanded its insurance franchise. Net premiums written increased from $6.1 billion to $26.3 billion, while float grew from $11.6 billion to $39.3 billion. Second, shareholders ultimately participated in that growth on a per-share basis. This outcome was far from inevitable. Fairfax issued shares and partnered with outside investors to help finance several acquisitions. Over time, however, strong organic growth, improved underwriting profitability, rising investment income, share repurchases, and the purchase of minority interests largely offset that dilution. Finally, Fairfax created value under two very different insurance market conditions. During the soft market, management focused on expanding the business. During the hard market, it harvested the benefits of those earlier decisions. The transformation can be divided into two distinct phases. Setting the Stage In 2011, Andy Barnard was appointed Chief Operating Officer of Fairfax's insurance operations. His priority was not rapid growth. Instead, management concentrated on strengthening underwriting discipline, reinforcing Fairfax's decentralized operating model, recruiting talented leaders, and building a stronger insurance culture across the organization. These efforts attracted little attention from investors at the time. In hindsight, they laid the foundation for everything that followed. Phase One: Growing Through a Soft Market (2014–2019) “Someone’s sitting in the shade today because someone planted a tree a long time ago.” Warren Buffett Much of the period from 2014 to 2019 was characterized by a soft insurance market. Pricing was generally weak, competition was intense, and attractive underwriting opportunities were limited. Many insurers responded by chasing premium growth. Fairfax took a different approach. Rather than competing aggressively for underpriced business, management used the soft market to expand through acquisitions while maintaining underwriting discipline. Despite operating in a difficult insurance environment, Fairfax more than doubled net premiums written during the soft market. Premiums increased from $6.1 billion to $13.3 billion, representing compound annual growth of 16.8%. Most of that growth came from acquisitions rather than increasingly aggressive underwriting. Fairfax was deliberately expanding its insurance franchise while many competitors focused primarily on writing more business. The most significant acquisitions included: Brit (2015): $1.7B Various international insurance businesses (2015–2016): ~$1.0B Allied World (2017): $4.9B Between 2015 and 2017, Fairfax invested approximately $7.6 billion to acquire eleven insurance businesses. These acquisitions significantly expanded the company's geographic reach, product offerings, and underwriting capacity. The timing proved important. Late in a soft market, attractive underwriting opportunities are often scarce, but acquisition opportunities can be plentiful. Weak industry profitability frequently depresses valuations, allowing disciplined buyers to acquire high-quality insurance businesses at attractive prices. In effect, Fairfax was buying insurance assets when they were on sale. This strategy required significant capital. Fairfax issued shares and brought in minority partners to help finance several acquisitions, accepting short-term dilution in exchange for the opportunity to build a much larger insurance franchise. Whether that trade-off would create long-term value remained an open question. By the end of 2019, Fairfax had assembled a much larger and more diversified insurance business. Investors now had to wait for the next phase of the insurance cycle to see whether management's strategy would pay off. Phase Two: Growing Through a Hard Market (2019–2025) The insurance market began to harden at the end of 2019. Premium rates increased, underwriting conditions improved, and attractive growth opportunities emerged across much of the industry. Fairfax entered this environment with a significant competitive advantage. Years of acquisitions had created a much larger insurance franchise through which to deploy capital. Rather than pursuing additional acquisitions, management shifted its focus to organic growth. The results were exceptional. Between 2019 and 2025, net premiums written increased from $13.3 billion to $26.3 billion, representing compound annual growth of 12.1%. Unlike the previous phase, this growth was driven primarily by improved market conditions and disciplined underwriting rather than acquisitions. The hard market validated decisions that had been made years earlier during the soft market. Fairfax entered the cycle with a much larger insurance franchise and was well positioned to capitalize as pricing and underwriting conditions improved. The result was strong premium growth, improved underwriting profitability, and significantly higher float. Just as importantly, it answered the question investors had been asking since the acquisition program began. The larger insurance franchise was creating real shareholder value. By 2025, growth on a per-share basis closely matched the growth of the underlying business. Much of the dilution incurred while building the insurance franchise had been offset through organic growth, improved profitability, share repurchases, and the purchase of minority interests. What Was the Impact? Viewed as a whole, the results are striking. Between 2014 and 2025: Net premiums written increased from $6.1 billion to $26.3 billion. Total investments increased from $26.2 billion to $74.9 billion. Float increased from $11.6 billion to $39.3 billion. Book value per share increased from $395 to $1,260. Shareholders fully participated in the growth, with per-share results slightly exceeding the growth of the underlying business. More importantly, Fairfax successfully adapted its strategy as the insurance cycle evolved. During the soft market, management expanded the insurance franchise through acquisitions. During the hard market, it used that larger franchise to drive strong organic growth, improve underwriting profitability, and generate significantly more investment income. What Have We Learned? The transformation of Fairfax's insurance operations was not the product of a single acquisition or a favourable insurance market. It was the result of disciplined capital allocation across an entire insurance cycle. As the insurance industry begins to soften again, many investors assume growth opportunities will disappear. Fairfax's experience suggests otherwise. The opportunities change, but they do not disappear. Successful management teams adapt. They allocate capital differently as conditions evolve, but they remain focused on the same objective: creating long-term shareholder value. Over the past eleven years, Fairfax demonstrated exactly that.

-

Article 3 in our deep dive into Fairfax's insurance business. The Insurance Cycle: How Great Insurers Exploit Opportunity The P/C Insurance Cycle Understanding Hard Markets, Soft Markets, and Why They Matter Before investors can understand Fairfax's growth history, they first need to understand the property and casualty (P/C) insurance cycle. Unlike most industries, insurance pricing moves through long periods of expansion and contraction. These cycles influence growth, profitability, capital allocation, and ultimately shareholder returns. They also help explain many of Fairfax's most important strategic decisions over the past forty years. Understanding the insurance cycle is therefore essential to understanding Fairfax. What Is the Insurance Cycle? The property and casualty insurance industry moves through recurring periods of strong and weak pricing. These two phases are commonly known as hard markets and soft markets. Hard Markets Premium rates rise. Underwriting standards tighten. Capacity becomes scarce. Profitability improves. Soft Markets Premium rates fall. Competition intensifies. Capacity becomes abundant. Profitability deteriorates. These cycles often last for many years and can swing to extremes. Successful insurers therefore manage their businesses with a long-term perspective rather than reacting to short-term conditions. Understanding where the industry sits in the cycle is important because it affects an insurer's growth opportunities, profitability, and ability to create long-term shareholder value. Why Does the Cycle Exist? The insurance cycle exists for much the same reason financial markets experience booms and busts: human behavior. When profits are strong, insurers become increasingly willing to compete for business. New capital enters the market, underwriting standards loosen, and pricing gradually weakens. Eventually, profitability deteriorates. As returns decline, the process reverses. Capital leaves the industry, underwriting standards tighten, and pricing improves. The result is a repeating cycle driven by greed and fear. Like Benjamin Graham's Mr. Market, the insurance cycle provides investors with a useful mental model. Markets are not always rational, and neither are insurance companies. Reinsurance executive Paul Ingrey captured this process in his well-known Underwriting Cycle Clock, which illustrates how insurers repeatedly move through periods of discipline, optimism, overexpansion, deteriorating profitability, and recovery. The cycle persists because industry participants repeatedly make the same behavioral mistakes. Exhibit: Paul Ingrey's Insurance Underwriting Cycle Clock Reinsurance executive Paul Ingrey developed the "Underwriting Cycle Clock" to illustrate how strong underwriting profits attract capital and competition, eventually leading to weaker pricing and deteriorating underwriting results. As losses mount, capacity leaves the market, discipline returns, and the cycle begins again. The lesson is straightforward: the cycle is driven by human behavior. Companies that remain disciplined while competitors chase growth are often the long-term winners. Source: Arch Capital Group Limited Why the Cycle Matters The insurance cycle creates opportunities for disciplined insurers. During soft markets, the best companies focus on underwriting profitability and preserving capital. Growth becomes secondary to maintaining discipline. During hard markets, those same companies can deploy capital aggressively, write more business, and earn attractive returns. Many insurers struggle because they do the opposite. They pursue growth aggressively when pricing is weak and profitability is poor. By the time a hard market arrives, they often lack the capital needed to take full advantage of the opportunity. The most successful insurers are therefore not those that grow the fastest. They are the ones that remain disciplined throughout the cycle. For investors, the key lesson is simple: the insurance cycle itself is not the risk. The real risk is owning an insurer that cannot navigate it effectively. The Berkshire Hathaway Model No company has exploited the insurance cycle more successfully than Berkshire Hathaway. Warren Buffett understood that insurance companies possess a unique advantage. They collect premiums today while many claims are not paid until years later, creating float that can be invested until it is needed to pay future claims. Most insurers invest this float conservatively, primarily in bonds. Buffett combined disciplined underwriting with superior capital allocation. Because insurance cycles unfold over many years, Berkshire never felt compelled to chase premium growth simply to satisfy quarterly expectations. When pricing became unattractive, Buffett was willing to let business shrink and patiently wait for better opportunities. That flexibility became one of Berkshire's greatest competitive advantages. During hard markets, capital flowed into insurance. During soft markets, it could be allocated to stocks, wholly owned businesses, acquisitions, or share repurchases. A soft market therefore changed where Berkshire invested capital—not its ability to create value. Fairfax and the Insurance Cycle Fairfax has followed a remarkably similar approach. During the prolonged soft market from roughly 2014 through 2019, Fairfax expanded primarily through acquisitions. Purchases such as Brit and Allied World significantly increased the company's insurance platform while industry valuations remained depressed. Fairfax was effectively buying insurance assets when they were on sale. When the market turned in 2020, management shifted its emphasis toward organic growth. Strong pricing allowed Fairfax to expand premiums while maintaining underwriting discipline. As a result, Fairfax grew successfully during both phases of the cycle. Acquisitions drove growth during the soft market. Organic underwriting drove growth during the hard market. Equally important, the company improved the quality of its insurance operations throughout the process. Like Berkshire Hathaway, Fairfax is more than an insurance company. It is also an investment company and a capital allocator. Prem Watsa's significant ownership stake and voting control have allowed Fairfax to manage the business with a long-term perspective. That has helped the company remain disciplined through multiple insurance cycles while allocating capital wherever opportunities have been most attractive. When underwriting opportunities become less attractive, Fairfax can redirect capital toward acquisitions, public equities, private investments, debt reduction, or share repurchases. A soft market may slow premium growth, but it also creates opportunities elsewhere. What It Means for Investors As the insurance market begins to soften, investors often assume the industry's best years are over. For many insurers, that concern may be justified. But Fairfax is not a traditional insurance company. Like Berkshire Hathaway, Fairfax combines disciplined underwriting with investing and capital allocation. Changes in the insurance cycle influence where capital is deployed, but they do not determine whether value can be created. Poor insurers become victims of the cycle. Great insurers use the cycle to their advantage. Fairfax's forty-year record suggests it belongs in the latter group. Throughout multiple insurance cycles, management has followed a consistent approach: remain disciplined when opportunities are scarce, act decisively when opportunities are abundant, and allocate capital with a long-term perspective.

-

Fairfax’s insurance business is much larger. In recent years, its exposure to catastrophes has come down a little. More resilient: At the same time, the dramatic increase in Fairfax’s earnings (and sources) is important. Additionally, Fairfax has been building additional resilience into their business model: the significant increase in non-insurance consolidated holdings in recent years. I think looking to the ratings agencies (specifically AM Best) can provide another helpful take… they have increased Fairfax’s ratings twice in recent years. Lots of positive developments. It is encouraging.

-

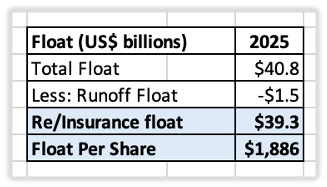

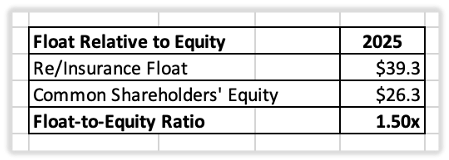

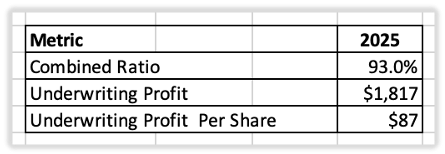

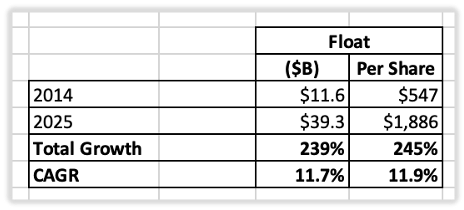

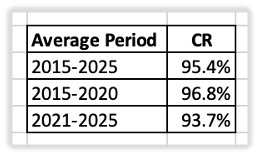

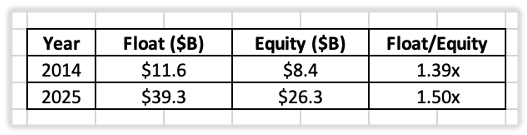

Article 2 in our series on Fairfax's insurance business Applying Buffett’s Float Framework to Fairfax In the previous article, Warren Buffett explained that investors should focus on three factors when evaluating an insurance company: The amount of float the company generates. The cost of that float. The long-term outlook for both. Let's apply Buffett's framework to Fairfax. Size: Fairfax Has Significant Float Warren Buffett's first test is simple: how much float does an insurer have? At December 31, 2025, Fairfax had total float of approximately $40.8 billion. For the purposes of this analysis, two adjustments have been made. First, runoff operations have been excluded. Runoff float has different economic characteristics than float generated by Fairfax's ongoing insurance and reinsurance businesses and is best analyzed separately. Second, Fairfax does not own 100% of certain subsidiaries, including Allied World and Odyssey. As a result, a portion of the float generated by those companies is attributable to minority shareholders rather than Fairfax shareholders. To keep the analysis simple and consistent with Fairfax's reported figures, no adjustment has been made for minority interests. After excluding runoff operations, Fairfax's insurance and reinsurance businesses generated approximately $39.3 billion of float, or about $1,882 per share. Exhibit 1: Insurance & Reinsurance Float Breakdown (2025) Fairfax has built a substantial float base. Before considering shareholders' equity, the company controls nearly $40 billion of investment capital generated by its insurance operations. Economic Significance: Float Exceeds Shareholders' Equity The size of float is important, but its significance becomes clearer when compared to shareholders' equity. At year-end 2025, Fairfax's common shareholders' equity was approximately $26.3 billion. Compared to insurance and reinsurance float of $39.3 billion, Fairfax's float-to-equity ratio was approximately 1.5x. Exhibit 2: Float Relative to Shareholders' Equity (2025) This means Fairfax had approximately $1.50 of float supporting every $1.00 of shareholder capital. Put differently, float was 50% larger than the equity supplied by shareholders. This is what makes float so valuable. When managed properly, it allows an insurer to control a substantially larger investment portfolio than shareholders' capital alone would support. Fairfax's investment portfolio is therefore funded not only by shareholders' equity, but also by a large pool of insurance float that has been built over decades of underwriting operations. Buffett's first test is therefore easily met. Fairfax has built a large and economically significant float base. Cost: Better Than Free Buffett's second test is the cost of float. Exhibit 3: Fairfax's Cost of Float (2025) In 2025, Fairfax reported a combined ratio of 93.0%. The company generated underwriting profits of approximately $1.8 billion while holding $39.3 billion of float. Viewed through Buffett's framework, Fairfax's float was better than free. Instead of paying to access this capital, Fairfax was paid to hold it. Trend: Growing Float Buffett believed the long-term trend was the most important factor of all. A large amount of float is valuable. A growing amount of float is even more valuable. Exhibit 4: Fairfax Insurance & Reinsurance Float Growth (2014–2025) From 2014 to 2025, Fairfax's float grew from approximately $11.6 billion to $39.3 billion. On a per-share basis, float increased from $547 to $1,886. This represents compound annual growth of approximately 12% over the past eleven years. Growth alone, however, is not enough. Buffett's third test also considers the long-term cost of float. Exhibit 5: Fairfax Combined Ratio (2015–2025) Fairfax delivered an average combined ratio of 95.4% from 2015 to 2025. The record includes years with elevated catastrophe losses. More importantly, underwriting performance has improved in recent years, with the average combined ratio declining from 97% in 2015–2020 to 94% in 2021–2025. Many insurers can grow float by sacrificing underwriting profitability. Others maintain underwriting discipline but struggle to grow. Fairfax accomplished both. Over the past eleven years, float increased by 245% while underwriting remained consistently profitable. Growing float is valuable. Growing float at a negative cost is even more valuable. A Fourth Question Buffett's three questions provide an excellent framework for evaluating an insurance company. I would add a fourth: How important is float to the business model? The answer depends on the relationship between float and shareholders' equity. The larger the float relative to equity, the greater its potential impact on shareholder returns. At year-end 2025, Fairfax's insurance and reinsurance float was approximately $39.3 billion compared to common shareholders' equity of $26.3 billion. Float was about 1.5 times larger than equity. Exhibit 6: Float Relative to Equity (2014 vs. 2025) What makes this particularly noteworthy is that the relationship has remained remarkably consistent over time. In 2014, float represented approximately 1.39 times shareholders' equity. By 2025, the ratio had increased modestly to 1.50 times. This means Fairfax has not only grown its float; it has preserved its importance within the business model. Despite substantial growth over the past decade, float remains larger than shareholders' equity and continues to provide meaningful leverage to shareholder capital. This distinguishes Fairfax from Berkshire Hathaway's evolution. As Berkshire grew into one of the world's largest companies, shareholders' equity expanded much faster than float, reducing float's relative importance over time. Fairfax has followed a different path. Insurance remains the foundation of the business, and float remains one of its most important competitive advantages. Buffett's Scorecard Viewed through Buffett's framework—and the additional question regarding the importance of float—Fairfax performs well across every measure. Float is large. Float has grown consistently over time. Float has been obtained at a negative cost. Float remains a significant contributor to shareholder returns. Individually, each characteristic is impressive. Together, they describe a valuable insurance franchise. Over the past eleven years, Fairfax has grown float from $11.6 billion to $39.3 billion, maintained profitable underwriting throughout that growth, and preserved the importance of float to its business model. Few insurers have accomplished all three simultaneously. Buffett's framework was designed to identify insurers with durable economics. By that standard, Fairfax appears to possess one of the strongest float franchises in the property and casualty insurance industry.

-