Leaderboard

Popular Content

Showing content with the highest reputation since 06/20/2026 in all areas

-

The only thing I’ll add on a personal note is that in over 30 years in the industry, with managing catastrophe exposure at the top of my responsibilities, there were at least three separate years in which inappropriate management of investments and poor management of the interest rate risk impact on fixed bond portfolios damaged the company I worked for more severely than the catastrophe risk that I was focused on ever did. Two of those events happened since 2000 — the Great Financial Crisis of 2008 and the increase in interest rates in 2022. The first resulted in the company I worked for being bought out by a larger competitor. The second resulted in sales of non core subsidiaries and employee layoffs in a successful effort to rebuild the capital base and reduce the expense levels going forward. I was fortunate enough to be a “casualty” in the second event. By virtue of severing my employment relationship a few years earlier than I would have chosen had I been left to my own devices, I received access to my retirement account years earlier than if I hadn’t been laid off. I rolled it over to a self directed retirement account and put the lion’s share into Fairfax and Berkshire, two companies I knew had not made the same mistakes my own employers had. The market value increase in Fairfax alone since then has been the equivalent of five years of my previous annual salary level. So I definitely do have a soft spot in my heart for the company and what it has meant to me personally.1 point

-

A very valid question and you are right to be skeptical. Background: I live and invest in India - I would rate 'IDBI Bank' as an 'above-average' investment opportunity which doesn't clear my local hurdle rate, but I still believe this is a great deal for Fairfax Financial. To provide better background - Fairfax Financial is 17% of the global fund I manage, IIFL Finance is 10% of fund (we own 1.7% of the firm), Fairfax India is 2% and IIFL Capital is 2% of the fund. All these have been long term holdings for us 5+ years and IIFL group has been in my personal portfolio for 15 years now. Why winning IDBI is great for Fairfax: 1.) IDBI is not a standalone deal, but it would boost all Indian financial investments of Fairfax My guess is that - Fairfax will form a bank holding firm which will hold IDBI Bank, IIFL Finance, IIFL Capital and Go Digit as their subsidiaries in 1 integrated group framework. In Indian context, a bank is the central core around which the highly valued capital light businesses can be built and scaled. In most verticals like asset management, insurance, institutional brokerage etc - the banking subsidiaries own the largest market share as they have the brand, balance sheet, customer relationship and distribution network. IIFL Group and Go Digit have been able to build large scale businesses despite not having a core banking shareholder. WIth a bank backing them and providing them with all its advantages, they can move to the next level in terms of growth and profitability. For example, the cost of funding for a bank backed firm will be 100+ bps lower (higher credit ratings) and can directly mean a 5% ROE improvement. Similarly, valuation multiple can go up 50% by being aligned with a bank for all these entities. The group will have good cross-sell synergies across - banking, broking, wealth management, asset management, life insurance, general insurance, reinsurance, investment banking and asset financing. I would expect a 1 billion USD uplift in valuation across their Indian financial investments with IDBI in the loop. Fairfax increasing its position in IIFL Capital to 51%, IIFL Finance moving a shareholder resolution to raise 1.3 billion USD of equity (July 24th vote) and taking a direct stake in Digit ealier this year are points to be noted. Indian central bank (RBI) has also been pushing banks to move their insurance (regulated by IRDAI), NBFC or asset management (regulated by SEBI) arms into seperately listed firms. Hence, my guess. 2.) IDBI is an A+ asset that has been run badly IDBI like several other public sector banks is mismanaged and not run to its true potential. IDBI has a phenomenal deposit franchise that is very difficult to replicate. The issues that you mention are all due to their lending ability that used to be mired in corruption and bad culture that comes along with having Government as your ultimate owner. They asset side has been cleaned up over the last several years and Fairfax gets a clean slate on the asset side that they can build upon. IDBI's cost of funds is like 4.7% (250 bps below G-Secs) with a 45% CASA ratio. Almost a 18 billion USD CASA book that is sticky and hasn't left them even in tough situtations. This is very valuable. In CSB bank turnaround, Fairfax quickly fixed the lending side and has been able to grow their asset book at 25% type CAGR, but they haven't been able to build their deposit book. That experience should have reinforced into them as to how valuable this sticky deposit franchise is. I would say, with the current bank licensing conditions, it would take 15 years for any small bank and new licensee to build a CASA or deposit book of this size. IIFL Finance is a co-lending partner of IDBI even now. This along with running CSB for 5+ years should give Fairfax the necessary knowledge to build up the asset side without taking excessive credit risks. IDBI bank currently earns 13% ROE purely from the deposit side advantages. Fairfax should be able to build a good credit book and move it to 16-18% ROE along with all the low hanging fruits that comes with an ownership and culture change. The large CASA base will allow them to build prime retail and corporate loans that compound value with minimal volatility. 3.) Large ticket size compounding for the next 20 years At a 5.7 billion USD cheque size, there are few opportunities of this scale for Fairfax. I (similar to the folks at Fairfax) believe that India is a secular growth story for the next 20 years and has the potential to be a 20+ trillion USD economy in that time frame. India currently has 4 large private banks and 3 large public sector banks. I believe that 5 of these large banks will continue to be the Top-5 even then. Indian large private sector banks have a 10 year average valuation of 3X book value. Fairfax is buying IDBI at 1.15X closing book value. If the turnaround doesn't materialize, they will still be able to exit the business at 1X book value on a conservative basis. On the upside, they can compound earnings at 16-18% CAGR for the next 10+ years and the valuation can double in that time-frame. The INR has gone through a large depreciation cycle over the last 2 years and well placed for lower hit in the coming decade. The absolute dollar returns/ money multiple from this deal can be super attractive even with decent execution. The overall set-up looks asymmetric to me with a juicy Risk-Reward for that ticket size.1 point

-

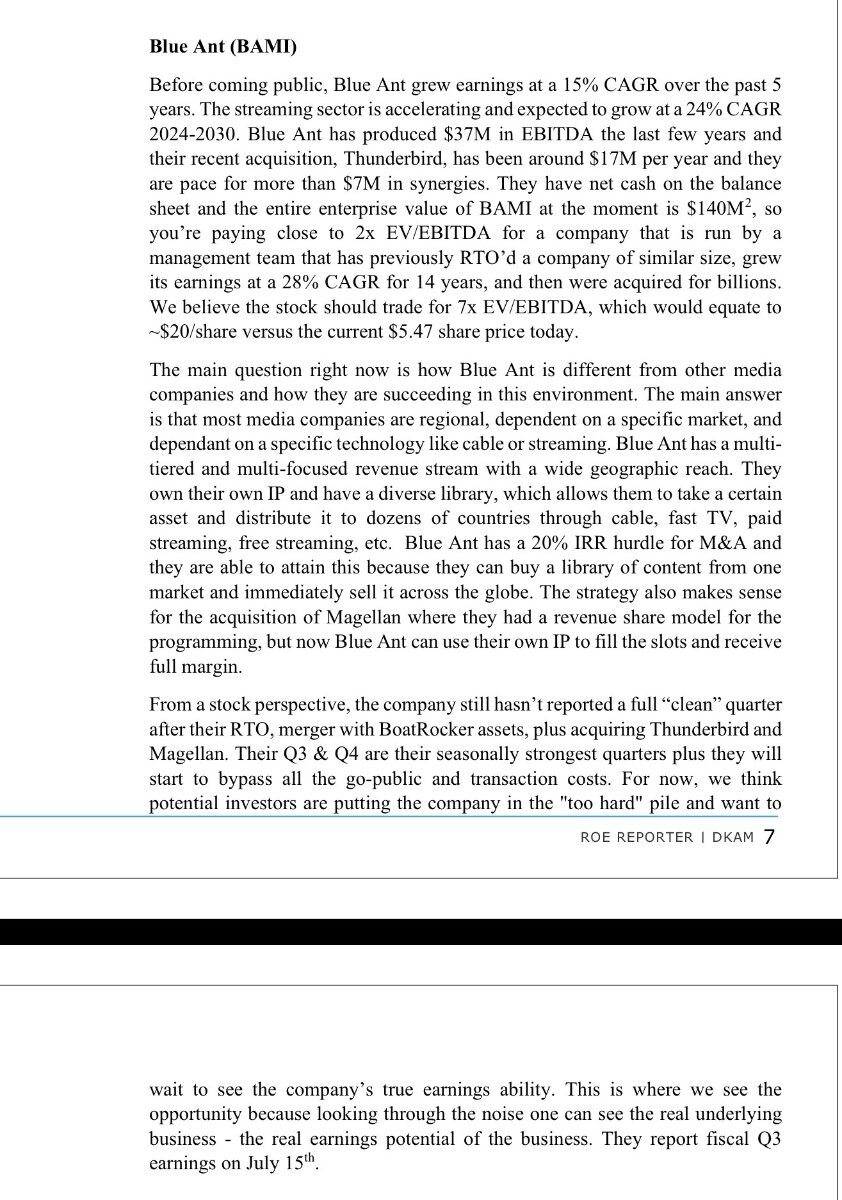

SCR has a new deck associated with its site visit: https://www.strathconaresources.com/wp-content/uploads/2026/07/Strathcona-2026-Lloyd-Thermal-Field-Tour_vF-WEB-Version.pdf They had a strong update with Meota getting to first steam under budget and ahead of schedule. Big value creating between the cost per barrel for production versus trading multiple. EQX and ORLA announced production for Q2 ahead of estimates. Microcap holding BAMI highlighted by DKAM.

1 point

1 point -

Here is the good news : Seaspan may be a beneficiary of Canada moving ahead on its submarine procurement program as they own the Seaspan Shipyard in the west coast. Here is the bad news: This is not the business that FFH co-owns with Washington family1 point

-

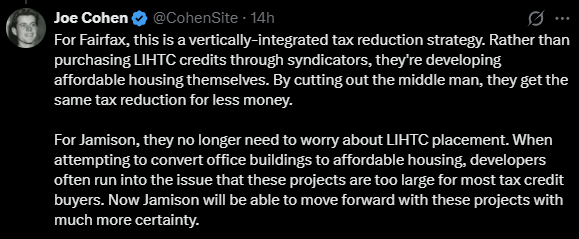

Kennedy Wilson likely delayed these announcements until after the acquisition by Management and Fairfax has closed. It will be interesting to see how Kennedy-Wilson grows over the coming years. Kennedy Wilson and Jamison Announce Joint Venture to Deliver 4,000 Affordable Housing Units Across the City of Los Angeles Kennedy Wilson acquires 421-unit multifamily community in Westchester County, NY for $237 Million Does anyone know if there is any truth to these statements.

1 point

-

"You can't take the same actions as everyone else and expect to outperform." Howard Marks is 100% right on that. To beat the market, your portfolio has to look different. David Swensen famously called this the "acceptance of uncomfortably idiosyncratic portfolios, which frequently appear downright imprudent in the eyes of conventional wisdom." Even on COBF, the herd mentality is real. Those are pretty bandwagon stocks to pick. It’s probably not a coincidence that the highest returns have been what only 1–2 people picked, not the ones where 5–6 people piled in. But six months is still too short to say if you are right or wrong. A half-year is a blink of an eye, and it is nowhere near enough time for a real structural value thesis to play out. At least you can hold yourself accountable after a year, although the biggest mouths on here seem to conveniently not hold themselves to account even then.1 point

-

I am using Interactive Brokers and Trade Republic for this one. Worked fine with IBKR; with Trade Republic, I had to file another acceptance instruction after the offer price increase. A colleague of mine did it through Deutsche Bank maxblue, and it was also sufficient to file the acceptance instruction only once. As settlement is generally T+2 in Germany, it should theoretically work until Wednesday, July 1. Usually, brokers have shorter acceptance periods, but you can sometimes extend those by contacting their customer service. I can generally recommend IBKR, as they seem to be the fastest when it comes to notifying you about the offer.1 point