Viking

-

Posts

6,055 -

Joined

-

Last visited

-

Days Won

78

Viking's Achievements

")

-

Fairfax - A Deep Dive on Management and Culture

Viking replied to Viking's topic in Fairfax Financial

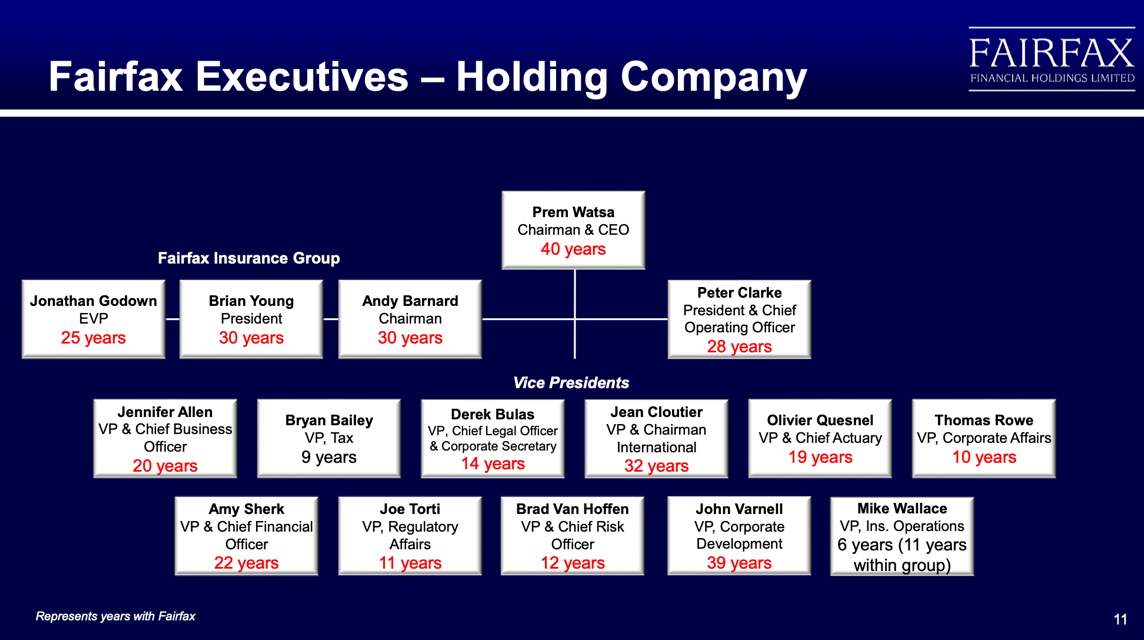

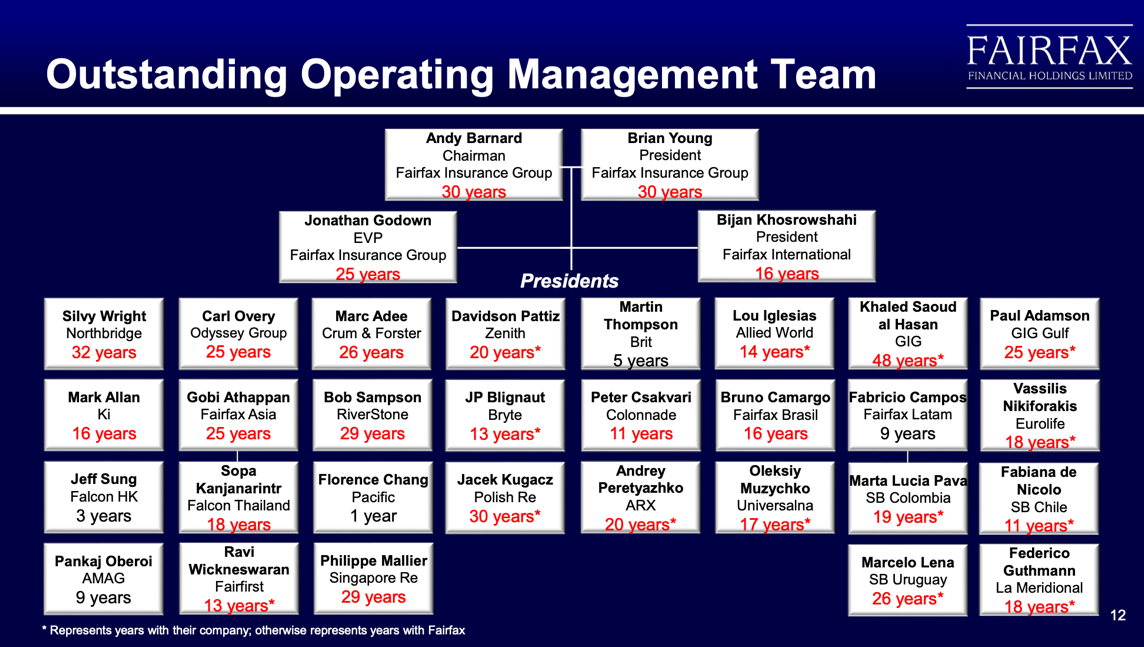

Article 4 in the series Corporate Culture: An Invisible Asset Investors spend enormous amounts of time analyzing financial statements, valuation multiples, earnings forecasts, and investment portfolios. Yet some of the most important drivers of long-term shareholder returns cannot be found in a spreadsheet. Corporate culture is one of them. Culture is often described as "how things get done around here." It encompasses an organization's values, incentives, decision-making processes, and behaviours. It influences how employees treat customers, how managers allocate capital, how risks are managed, and how organizations respond when conditions become difficult. Over time, culture can become a meaningful competitive advantage—or a significant liability. The challenge for investors is that culture is difficult to measure. Unlike revenue growth, profit margins, or return on equity, there is no widely accepted metric that captures its strength. For Fairfax investors, culture matters because it influences many of the factors that drive long-term shareholder returns: employee retention, underwriting discipline, acquisition integration, leadership development, and capital allocation. Culture Starts at the Top Corporate cultures are shaped by leadership. For nearly forty years, Prem Watsa has been Fairfax's chief steward of culture. He has consistently emphasized integrity, long-term thinking, decentralization, humility, and treating people fairly. More importantly, he has spent decades embedding those principles into Fairfax's organizational structure, incentive systems, and leadership selection. The company's decentralized structure requires trust. Its acquisition strategy depends on allowing acquired businesses to retain their identities and leadership teams. Its compensation programs encourage managers and employees to think like owners. Together, these practices reinforce the culture that Prem has spent decades building. As a result, Fairfax's culture is not simply a collection of stated values. It is embedded in the organization's structure and decision-making processes. Employee Retention as Evidence One of the clearest indicators of a strong culture is employee retention. Talented people have options. When leaders remain with an organization for decades, it often suggests they value the culture, opportunities, and working environment. Fairfax has an unusually strong record in this area. The company regularly publishes organizational charts for its holding company, operating businesses, and investment team. While these charts are intended to show reporting relationships, they also reveal something more important: extraordinary management continuity. Across all three groups, many senior leaders have spent decades with Fairfax or its operating companies. Examples include Prem Watsa (40 years), Roger Lace (40 years), Brian Bradstreet (39 years), John Varnell (39 years), Jean Cloutier (32 years), Silvy Wright (32 years), Brian Young (30 years), Andy Barnard (30 years), Peter Clarke (28 years), Carl Overy (25 years), and Paul Adamson (25 years). The significance is not that a handful of executives have remained for decades. Long tenure appears throughout the organization, suggesting Fairfax has built an environment that talented managers choose to remain part of for extended periods of time. This level of continuity is unusual among public companies and provides evidence of a culture built on trust, autonomy, and long-term thinking. A defining characteristic of Fairfax's culture is its willingness to partner with proven managers rather than replace them. Rather than imposing a centralized operating model, Fairfax typically leaves decision-making in the hands of local leaders and measures success over years and decades, not quarters. The result is an organization with remarkable management continuity—a characteristic that is difficult to replicate and one that may represent an important competitive advantage. Andy Barnard on Culture Perhaps the most credible assessment of Fairfax's culture comes from Andy Barnard. Barnard joined Fairfax in 1992 and spent more than three decades helping build Fairfax's global insurance operations. As President and Chief Operating Officer of Fairfax Insurance Group, he played a central role in developing Fairfax's decentralized structure and expanding the number of profit centres throughout the organization. Because of his long tenure and leadership role, Barnard is uniquely qualified to assess Fairfax's culture. At Fairfax's 2025 Annual General Meeting, he highlighted several characteristics that have defined the organization throughout its history: So of course, we had a fantastic year in 2024, $1.8 billion of underwriting profit. 7 of our companies achieved record underwriting profits during 2024, which we're very pleased and happy and proud to see. (W)hat I'd like to focus on… is the reasons that we've been able to achieve this success. And I'd like to go back to that slide that Prem shows every year… that shows the tenure of our CEOs across Fairfax because I really don't think there is any more important factor behind our success than what that slide reveals. Continuity of management is just so vitally important in our industry as it is in many businesses. (B)ut I think it's especially important in the insurance business. It allows us, over time, to build, to grow, to improve our operations. And we do so without the distractions and the disruptions that come from changes at the top. Now for those of you that might follow the trade press in our industry, you would see amongst many of our competitors, and I'm sort of referring to the global commercial, property and casualty market, which is really the main theatre that we operate in. But for so many of these companies, it's just a revolving door. And it's not just… the CEO. (B)ut it is also many of their key executives. And this creates circumstances that make it very hard for companies to have the stability that enables them to thrive and improve and build and grow over time. At Fairfax, our decentralized operating philosophy, whereby we keep our company separate and autonomous creates a much more favourable, much more rewarding environment for our CEOs and for their management teams. And it is that environment that allows them to continue to build and grow and improve their operations. And that's what you're seeing in the results that we've been able to achieve at Fairfax. And… we've said this many times. We may say it every one of these meetings, we are so blessed. And this gets better and better every year because of that continuity, but we are so blessed with the remarkable collection of CEOs and leaders that we have running our companies. And again, I don't think there is any more important explanation for the underwriting success that we've been able to achieve. Prem referred to our moat, the culture of Fairfax being our moat. This retention of employees is really something that is attributable to the unique culture that we've had at Fairfax: supportive, rewarding, empowering. And that's what's enabled us to have this remarkable duration. I would say if you compare us to any of the major companies in that global P&C world. I don't, think you would find anyone with close to the duration of tenure at the top. And not just at the top, at the very top, but also amongst their senior management teams that you find at Fairfax. Andy Barnard – Fairfax AGM – April 2025 Barnard's comments are noteworthy because they come from someone who spent more than three decades helping build Fairfax's insurance operations. While investors often think of competitive advantages in terms of brands, scale, patents, or cost structures, Fairfax's leaders increasingly point to culture as one of the company's most important moats. Prem Watsa has made this argument directly, and Barnard reinforced it when he noted that "the culture of Fairfax [is] our moat." The evidence supporting that claim can be seen in Fairfax's unusually strong management retention, decentralized operating structure, ability to attract entrepreneurial leaders, and success integrating acquisitions while preserving the people and cultures that made those businesses attractive in the first place. Several themes emerge from Barnard's comments. Fairfax places a high degree of trust in its people. Employees are encouraged to think independently and act like owners. The organization values humility, fairness, and long-term relationships. Most importantly, decentralization and culture reinforce one another. These traits may sound simple, but they are difficult to replicate. Competitors can copy products, strategies, and compensation systems. Culture develops gradually through thousands of decisions made over many years. What This Means for Shareholders Corporate culture is often described as an intangible asset. In Fairfax's case, it may be one of the company's most important assets. Over four decades, Fairfax has built a culture centred on integrity, trust, decentralization, accountability, and long-term thinking. These values have been reinforced through leadership actions, organizational design, compensation systems, and management selection. Culture alone does not guarantee success. Businesses must still compete effectively, allocate capital wisely, and execute well. But culture influences all of those activities. For investors evaluating Fairfax, culture should not be viewed as a soft or secondary consideration. It helps explain the company's ability to attract talented managers, retain leadership teams, and create an organization focused on long-term value creation. Like many competitive advantages, culture is difficult to quantify and easy to overlook. That may be precisely what makes it valuable.

-

Fairfax - A Deep Dive on Management and Culture

Viking replied to Viking's topic in Fairfax Financial

On share buybacks, Buffett definitely talked out of both sides of his mouth. He had one line of reasoning for buying back BRK stock... and a completely different line of reasoning when businesses he owned did it. That is not a criticism... it is complicated. -

Fairfax - A Deep Dive on Management and Culture

Viking replied to Viking's topic in Fairfax Financial

Article 3 in the series Decentralization at Fairfax – A Growing Competitive Advantage Most investors focus on financial statements, valuation metrics, and earnings forecasts. Few spend much time thinking about organizational structure. That is unfortunate because structure influences how decisions are made, how capital is allocated, how employees behave, and ultimately how businesses perform. Over long periods of time, organizational structure can have a meaningful impact on shareholder returns. One of Fairfax's defining characteristics since its founding in 1985 has been its commitment to decentralization. Rather than directing operations from head office, Fairfax pushes decision-making closer to customers and markets. Operating managers are given significant autonomy to run their businesses, while head office focuses on capital allocation, culture, and oversight. The benefits are substantial. Decentralization promotes accountability because authority and responsibility reside with the same people. It improves speed and flexibility because decisions are made by managers closest to the business. It also helps attract entrepreneurial leaders who value autonomy over bureaucracy and centralized control. The model can also be an advantage when making acquisitions. Many successful management teams are reluctant to sell to buyers who intend to integrate operations and impose centralized control. Fairfax offers a different proposition. Acquired businesses are generally allowed to continue operating independently, preserving both culture and leadership. Over time, decentralization can become a powerful competitive advantage. Entrepreneurial managers tend to produce better operating results. Better results generate more cash flow. Head office can then redeploy that capital to the most attractive opportunities across the organization. As Fairfax acquires and partners with additional high-quality operators, its competitive advantage deepens. This article examines Fairfax's decentralized structure from four perspectives. First, Prem Watsa explains the philosophy behind the model. Second, Silvy Wright illustrates how empowerment can drive organic growth throughout an organization. Third, Lou Iglesias explains how decentralization can become a competitive advantage in acquisitions. Finally, we examine how Fairfax continues to deepen the model through the expansion of profit centres and independent operating companies. Part 1: Prem Watsa — The Big Picture In his 2024 shareholder letter, Prem Watsa devoted unusual attention to Fairfax's decentralized operating structure. The reason was straightforward: succession. As Fairfax prepares for future generations of leadership, Prem wanted to clearly document why decentralization has been central to the company's success and why it must be preserved. His message was simple: Fairfax's long-term results are not the product of centralized decision-making. They are the product of empowering talented people, holding them accountable, and creating an environment where entrepreneurs can thrive. Since we began in 1985, 39 years ago, our book value per share has compounded at 18.7% per year (including dividends) while our common stock price has compounded at 19.2% (including dividends) annually. As I have mentioned previously, our success throughout our history and again in 2024, has come under a decentralized structure with outstanding management executing a disciplined approach to underwriting. Over the years, those who have followed Fairfax, read our letters and attended our annual meeting, are well aware that we are passionately devoted to the decentralized operating philosophy. This year, I want to spend more time on this subject. Aside from helping inform our shareholders about our thinking in the past and present, I have an ulterior motive that comes from an eye on the future. As Fairfax rolls into the future, your Chairman (gradually) passes leadership to the next generation, and they, in turn, to later generations; it is very important that we memorialize why decentralization is such a critical feature of Fairfax. I want and expect Fairfax to thrive over the next 100 years, and well beyond. To do so, I believe it is of paramount importance that we never abandon our decentralized approach! So, why are we so fervently attached to this model? At its foundation, decentralization places its faith in the many rather than the few. Embedded in the Guiding Principles, which we have published every year in this report, is our deep and abiding respect for the fact that we are all created equal before God. All of our offices display prominently The Golden Rule; treat others as you want to be treated yourself as depicted in all the religions of the world. All of our CEO’s have a plaque with the following quote Ronald Reagan loved so much and kept on his desk: “There is no limit to what a man can do or where he can go if he doesn’t care who gets the credit.” Decentralization is the best system for unleashing the power of the many, rather than being limited to the talents of the few. And it aligns so perfectly with the foundational values of Fairfax since its inception. Our optimism in what empowered people can accomplish is unbounded! What are the advantages of an empowering, decentralized operating system? Let me count the ways: 1.) Ownership and Accountability Each of our CEO’s is given full autonomy over all underwriting and operational functions within their company, other than investments. They set strategy and tactics. They are responsible for managing risk within the limits of their allocated capital. Accordingly, they are fully accountable for underwriting performance and its results. The decisions implemented in their companies are their own, not those passed down from above. 2.) Management Retention A direct benefit of this Ownership Culture is the exceptional continuity of management we enjoy at Fairfax. As I write this, our Presidents and Senior Executives at Fairfax average close to 20 years of service. We are big believers in the benefits that come from this continuity. Rather than shuttling in new leaders every four or five years, our companies are able to continually build on success, without undergoing the strategic U-turns that management turnover often brings. 3.) Flexibility and Nimbleness The autonomy our companies enjoy allows a degree of operating agility absent from large, centralized organizations. Our performance during the recent hard market years of 2020 to 2023 bear this out, as we advantageously expanded at an industry leading pace! We rely on the expertise and judgment at each of our companies, and we do not prescribe from the top. For example, when the cyber insurance market underwent radical change at the end of 2020, we had four of our major companies dramatically expand their activity, each pursuing a different strategy. Had we imposed a one-size-fits-all approach to this challenging class, the growth would have been a fraction of what it was. 4.) Reduced Leakage from Acquisitions We do not, as a general rule, look to integrate acquisitions into existing operations, which means we keep much more of the business and people we acquire. Our industry is replete with examples of acquisitions that have little to show after three or four years because people have left and portfolios have melted away! 5.) Financial Flexibility Maintaining independent, separately capitalized companies gives us a source of financial flexibility. While it will always be the case that none of our companies is for sale, there may be times it makes sense for us to sell a minority stake. Witness the sale of 10% of Odyssey a few years ago, enabling us to make a large share re-purchase at an opportune time. At Fairfax, for today and the future, we believe the best conditions for operating success depend on the Three Ts: 1.) Trust must be reciprocal between the holding and operating companies. Trust has to be earned and its strength increases over time. Decentralization cannot work without it. 2.) Transparency with clear and open communication is required at all times. 3.) Talent is necessary to operate successfully at a high level in a challenging industry. There are those who might look at Fairfax from the outside and lay out a plan that would, on paper, describe myriad benefits to be obtained by abandoning our approach. They would do so without being able to quantify the intangible benefits we enjoy. It is vitally important to me that the Fairfax approach does not change because I believe our long-term success depends on it!! Prem Watsa – Fairfax 2024 Annual Report Prem identifies five advantages of decentralization: ownership and accountability, management retention, flexibility, acquisition integration, and financial flexibility. The underlying principle is straightforward: Fairfax succeeds when talented people are trusted to run their businesses. Building an organization around trust, transparency, and talent has taken decades, but it has become one of Fairfax's defining characteristics. Part 2: Silvy Wright — Driving Organic Growth Northbridge provides a useful example of how decentralization works in practice. At Fairfax's 2025 AGM, Silvy Wright explained how the Canadian operations were transformed after four separate insurance companies were brought together operationally in 2011. Importantly, the objective was not centralization or cost-cutting. The objective was to create a stronger organization while preserving the entrepreneurial culture that had made the individual companies successful. (A)s you can appreciate, we've all had different journeys, and mine started in 1994. So I just want to take just a few moments to share an employee experience. And that's me. In 1994, I joined Markel. And Markel, as you all know, was the first company Prem bought. And in 1994, Markel was about $60 million in revenue (and) 60 people… I was not a president 30 years ago. Well, my parents would have been pretty proud if that happened. But I wasn't the president back then. (When) I joined, I was an accountant, but with a strong entrepreneurial drive. And it was very clear to me, when I joined Markel, that Prem's philosophy on decentralization really inspired that entrepreneurial spirit in Markel. There were 60 of us. And when I refer to entrepreneurial spirit, I'm thinking you feel like an owner of the company, so you work like an owner of the company. You've got the freedom to take risks or you have the freedom to challenge the status quo. And then you have a great sense of pride of what you do. And that spirit lived in all 60 people, from the collections manager who collected every dollar like her own, to the underwriting head who developed strong relationships with the customers. And within that environment, all the employees built the leading transportation insurer of Canada. Now of course, it didn't happen overnight, but over the years, that's what all the employees did. So flash forward, so I'm still here, 16 years later, I learned a lot at Markel, a lot of freedom, a lot of mistakes, learning along the way, and I was appointed the CEO of Northbridge Financial (in 2011). Northbridge Financial represented the Canadian insurance operations of four separate companies. And at that time -- I know you're not going to like this Prem. But at that time, we asked for the unthinkable. And that is to bring the 4 companies together from an operational perspective. And we asked for that because we really wanted to compete more effectively in the changing landscape in Canada. Not for layoffs -- we didn't have layoffs. But we knew that we could leverage the combined talents of the group. We can leverage the diverse portfolios that we had in the various companies so that we could be a stronger force with the broker distribution and then obviously to leverage scale to invest in that company. So that's what we did. But the top goal of that beginning was not that obvious. The obvious was, okay, you're going to make changes, you better make a profit. The top goal was not that. The top goal, having been with Fairfax already 16 years at that time, was to build the culture and the entrepreneurial spirit that I knew creates success in the long term. And so that's what we did. We empower -- we continuously fostered an employee empowerment. And empowerment does not work if it just sits at the top, right? Yes, presidents have freedom. But the success is when you cascade that empowerment throughout the organization. When people feel that they have the freedom to challenge the status quo, to come up to the president and share an idea, and that's what we've done. And we're not perfect, but we've unleashed a lot of talent, and it's all in the talent of those employees that we have established a very good record. And now we have a nice shiny silver cup. So, with that, thank you… Prem… the trust… we both took a risk, and it paid off. Silvy Wright – Fairfax AGM – April 2025 Silvy's comments highlight an important point: decentralization only works when empowerment extends throughout the organization. It cannot be limited to senior management. Employees must also be encouraged to think independently, challenge assumptions, and act on opportunities. Northbridge's long-term performance suggests that when this culture is successfully embedded, it can become a meaningful competitive advantage. Part 3: Lou Iglesias — Driving Growth Through Acquisitions Allied World demonstrates another benefit of decentralization: acquisitions. Many successful management teams are reluctant to sell their businesses to buyers that intend to integrate operations, replace leadership, or impose centralized control. Fairfax offers a different model. Operating companies retain substantial autonomy and continue executing their own strategies. At Fairfax's 2025 AGM, Lou Iglesias explained why this mattered when Allied World evaluated strategic alternatives in 2016 and 2017. It's good to see everybody. Obviously, one of the themes at the AGM this year is decentralization. So, I thought I would… talk about Allied World and decentralization and how it affects an operating company. And I'd like to start with a little story. I know some of my new friends that I met last night would like to hear a story about that. So going back to 2016, 2017 time-frame. At Allied, we were looking for a transaction, right? We were a midsized public company. We thought getting a bigger, better platform would help us continue our journey, build our company out. We felt that we still had the ability to create a lot of value. So we were talking to several suitors. And one, we got pretty far along with. We were working with them for over a year, and we're getting close to the finish line. And so now we're getting into the details. And we started to realize that this would be a merger and that it would be likely that Allied World would be broken up. And that didn't sit very well with us. It wasn't what we wanted as a company. So that transaction never happened. Shortly after that, we get a call from Fairfax. And at the time, we didn't know a lot about Fairfax. We were a little bit tired of working for over a year on a transaction that didn't work, and we were a little reluctant. But Prem said, wait a minute, Fairfax does things differently. You should hear us out. And we all know Prem could be very convincing. So we took the meeting, and we heard a lot about the Fairfax culture, which sounded very good to us. And we heard a lot about decentralization in the independent operating model, which sounded great to us because, again, we felt that we still had a great runway to build our company out. So, we finished a meeting. I went across the street to the restaurant with John Bender and Wes DuPont, who are sitting up there and a couple of others. And being the good underwriters that we are, we were kind of skeptical, a little bit. Prem loves to tell that story. We're a little skeptical, but we did our diligence, and we found out, yes, that is how they do it at Fairfax. And we did the transaction. And very quickly, since Fairfax exceeded most of our expectations, the skepticism went away, right? So very quickly, we got past that. But the point of this story is, number one, decentralization was so important to Allied World that it's likely that we may never have been part of Fairfax if it wasn't for it. And I think the second thing to take away is that I think Fairfax is going to have the #1 slot to talk to companies and acquire companies that still feel that they could do great things, right? Because that's the platform that you want to be able to move your company forward. So we had our own same management team, staff, strategies, no layoffs, right, and we move forward. So where does that bring us today? So, if you look at the full 6 years that we've been part of the Fairfax family we've posted over $1.6 billion of underwriting profit, over $3.6 billion of net income. Our combined ratio has improved for 6 years in a row every year. In 2024, just last year, we had $540 million of underwriting income, which is a record for Allied World and our third record year in a row. And we've more than doubled the size of the company at over $7.2 billion since we were acquired. So, a lot of things go into that. I credit our people, who I think are fantastic, and Andy talked about people. The ability to keep the best people certainly is a huge part of the results that I just talked about. That's one thing. We have great professionals at our company. But I'd also say, I could say with great confidence that in a centralized company or in a merged company, that level of performance I don't think would have been possible. And prior to Allied World, I was with a large centralized company for many years so I could see the differences pretty clearly. And they're stark, right? The ability to run your business, the ability to carry out your strategy seamlessly, to keep the best people, the lack of bureaucracy which is a really, really big benefit for all the Fairfax companies, is tremendous. And last thing I really want to touch on is trust because I don't believe that you could have a successful decentralized operation without trust, right? And we trust Fairfax explicitly. We believe they trust us as well. But trust equals transparency, right? So you could have decentralization. We have a tremendous amount of transparency without having to write thousands of reports, right? Andy and I, in a 1-hour call, will cover what would take me 7 hours of reports that I would have had to write, okay? Transparency is key. And I also think that Fairfax deserves a tremendous amount of credit. It's not easy to run a large decentralized company as successfully as they do, a large global company. It takes dedication, takes discipline, professionalism, and it takes a very unique skill set to be able to do it effectively. So great credit to Fairfax. And I think all the operating companies benefit tremendously. Lou Iglesias – Fairfax AGM – April 2025 Lou's comments highlight a competitive advantage that is difficult to quantify. Fairfax is often an attractive buyer for companies that believe their best years still lie ahead. For management teams seeking permanence, capital, and autonomy, Fairfax offers something few acquirers can match. This advantage may become increasingly important over time. The best businesses are often built by talented entrepreneurs who want to continue running their companies after a transaction closes. Fairfax's decentralized model makes it a natural home for these businesses and may improve both the quantity and quality of acquisition opportunities available to the company. Part 4: Walking the Talk — Expanding the Decentralized Model Decentralization has been a core part of Fairfax's culture for decades. What is interesting for investors today is not the philosophy itself, but the evidence that Fairfax continues to deepen and expand the model across the organization. One of the clearest indicators is the steady growth in the number of profit centres within Fairfax's insurance operations: 2022: approximately 200 profit centres 2023: more than 225 profit centres 2024: more than 250 profit centres 2025: more than 275 profit centres Much of this expansion can be traced to Andy Barnard and his team, who spent more than a decade systematically increasing the number of profit centres across Fairfax's insurance operations. The result has been greater accountability, transparency, and entrepreneurial decision-making throughout the organization. Each profit centre focuses on a specific geography, customer segment, or product line and is responsible for its own results. As the number of profit centres increases, decision-making moves closer to customers while accountability becomes more transparent. The trend extends beyond insurance. Fairfax increasingly appears to be applying the same philosophy across its non-insurance holdings. In 2025, Quess was separated into three independent public companies: Quess, Digitide, and Bluspring. The Keg was also spun out of Recipe Unlimited as a standalone private business. In both cases, Fairfax moved toward greater autonomy, accountability, and managerial ownership rather than increased centralization. As Prem Watsa noted in Fairfax's 2025 annual report: "We have over 275 profit centres across our group. Each profit centre is focused on a unique set of customers, geographies or products that benefit from market leadership, product knowledge and the ability to provide excellent customer service. These profit centres facilitate transparency, enabling Andy Barnard, Brian Young and Peter Clarke to effectively monitor the insurance operations. Empowerment thrives at Fairfax." For investors, the significance is straightforward. Fairfax is not merely talking about decentralization—it is actively building a more decentralized organization. Conclusion Decentralization is easy to describe but difficult to implement. It requires trust from head office, talented managers throughout the organization, and a culture that rewards accountability rather than bureaucracy. Building such a system takes years, often decades. The evidence suggests Fairfax has spent forty years building exactly that kind of organization. The result is an organization that appears unusually well positioned to attract entrepreneurial leaders, retain talented managers, integrate acquisitions, and adapt to changing markets. These advantages do not appear on a balance sheet and cannot be measured using a financial ratio. Nevertheless, they may prove to be one of Fairfax's most important long-term competitive advantages. -

Fairfax - A Deep Dive on Management and Culture

Viking replied to Viking's topic in Fairfax Financial

@RichardGibbons, you make a great point - it is complicated. Not just for Prem/Fairfax but for any company. It gets to the heart of what makes assessing management so difficult - it qualitative and comes down to judgement. As a result, two investors looking at the same information could come to very different conclusions. In my framework (right or wrong), much of my analysis is weighted to the past 5 years. Years 6 to 10 matter, but much less. More than 10 years is interesting but much less relevant (for me). It is important people understand that when they read my stuff. If I had completed the management chapter in late 2020 it would have had a very different tone. Fairfax is very active - buying and selling. They are involved in a number of transactions every year. Volume alone is going to put them in a tough spot every once in a while. Not that I am trying to make excuses for past behaviour. My view that Fairfax has moved up the quality ladder when making new purchases should help (if true). Taking companies private also helps. Buffett is an interesting comparison. He also had a few big stumbles over the years. Those are largely forgotten. Understanding Fairfax's long history pretty well, I am just so happy with where the company is at today. -

Fairfax - A Deep Dive on Management and Culture

Viking replied to Viking's topic in Fairfax Financial

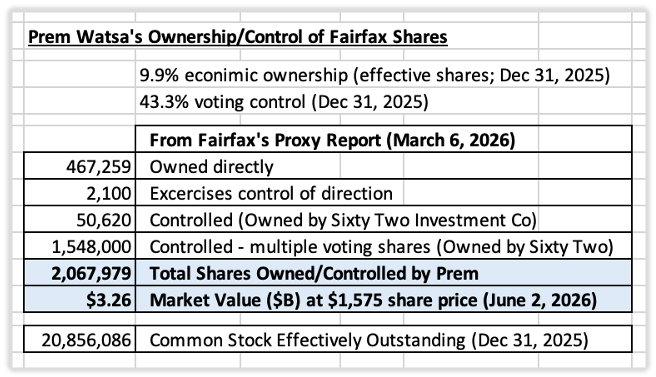

Article 2 in the series. Prem Watsa and Family Control Founder-led companies have historically been among the best long-term investments. When ownership, control, and management are concentrated in the hands of a capable founder, decisions are often made with a longer time horizon and a greater focus on value creation. Fairfax Financial is one such company. Prem Watsa founded Fairfax in 1985 and has led the company for nearly four decades. During that time, Fairfax has evolved from a small Canadian insurer into a global insurance, investment, and operating company with interests spanning dozens of countries and industries. For investors, understanding Prem's role is important because he remains Fairfax's largest individual shareholder, Chief Executive Officer, Chairman, and controlling voting shareholder. Fairfax's culture, capital allocation philosophy, and long-term orientation all reflect his influence. This article examines Prem's leadership record, ownership position, and family control structure—and what those factors mean for shareholders. Founder, Leader and Capital Allocator Prem Watsa founded Fairfax in 1985 and has led the company continuously ever since. Over that period, Fairfax's share price has compounded at approximately 19% annually, including dividends. This places Fairfax among the best long-term performing public companies in Canada and North America. But what makes Prem noteworthy is not simply what he achieved—it is how he achieved it. Warren Buffett has often said that he looks for three qualities in business leaders: Intelligence Initiative Integrity Of the three, Buffett considers integrity the most important because it forms the foundation of trust. Prem has demonstrated all three qualities throughout Fairfax's history. His intelligence is reflected in Fairfax's long-term record of capital allocation and value creation. His initiative is evident in the growth of Fairfax from a small Canadian insurer into a global organization. Most importantly, he has built a reputation for integrity that has earned the trust of shareholders, employees, customers, business partners, and communities. Two qualities have been especially important to Fairfax's success: temperament and an ability to attract talented people. Buffett has long argued that temperament is more important than intellect in investing. Throughout Fairfax's history, many of the company's most successful decisions required patience, conviction, and emotional discipline during periods of uncertainty. Throughout Fairfax's history, many of the company's most successful investments were made during periods of uncertainty and market stress. These decisions required patience, conviction, and emotional discipline. Prem has also demonstrated an uncommon ability to identify, recruit, develop, and retain talented managers. Fairfax's decentralized structure depends on capable leaders operating with significant autonomy. The depth and continuity of Fairfax's management team may ultimately prove to be one of Prem's most important accomplishments. As a result, Fairfax's success extends well beyond shareholder returns. Employees have built rewarding careers, customers have benefited from stable insurance partners, communities have received significant philanthropic support, and long-term shareholders have participated in one of the strongest compounding stories in modern Canadian business. Buffett on the importance of temperament – 1985 interview with Adam Smith: Adam Smith: What do you consider the most important quality for an investment manager? Warren Buffett: It's the temperament. You don't need tons of IQ in this business. I mean you have to have enough of IQ to get from here to downtown Omaha but you do not have to be able to play three-dimensional chess or being the top player in a bridge league. You need a stable personality and temperament that neither derives great pleasure from being with the crowd or against the crowd because this is not a business where you take polls; it's a business where you think. Ben Graham would say that you're not right or wrong because a thousand people agree with you and you're not right or wrong because a thousand people disagree with you. You're right because your facts and your reasoning are right. – Warren Buffett - Adam Smith’s Money World Interview 1985 Ownership, Compensation, and Alignment One of the most attractive features of Fairfax's governance structure is the alignment between management and shareholders. Prem's compensation package is unusually modest for a company of Fairfax's size and complexity. His annual salary is approximately C$600,000 and he receives no stock options or stock-based compensation. The more important consideration, however, is ownership. As of December 31, 2025, Prem owned or controlled approximately 2.1 million Fairfax shares, representing: 9.9% economic ownership 43.3% voting control At Fairfax's share price in mid-2026, that stake was worth more than $3 billion. As a result, the overwhelming majority of Prem's wealth remains tied to Fairfax's long-term success. Shareholders benefit from knowing that gains and losses are experienced alongside management. This alignment was demonstrated during the market turmoil of 2020. At a time when investor sentiment toward Fairfax was overwhelmingly negative, Prem personally purchased approximately US$150 million of Fairfax shares in the open market. He described Fairfax as trading at the largest discount to intrinsic value he had seen in the company's history. "At our AGM and on our first quarter earnings release call, I said that our shares are 'ridiculously cheap'. That statement reflected my recognition that in the 35 years since Fairfax began, I have never seen Fairfax shares sell at a bigger discount to their intrinsic value than they have recently. I have now backed up my strong words by purchasing close to US$150 million of Fairfax shares in the market over the last few days, as I believe that this will be an excellent long term investment." — Fairfax News Release, June 15, 2020 Actions often reveal more than words. Large insider purchases by already-wealthy founders are relatively uncommon and are generally viewed as one of the strongest indicators of management alignment. Family Control Fairfax is effectively a family-controlled company. While Prem owns ~10% of Fairfax's economic interest, his multiple-voting shares provide ~43% voting control. This gives the Watsa family substantial influence over Fairfax's strategic direction. For some investors, family control raises concerns. For others, it represents an important competitive advantage. The reality is that family-controlled structures can produce either excellent or poor outcomes depending on the quality of the controlling shareholder. When governance is strong, family control often promotes: Deep commitment to the business Long-term decision making Consistent capital allocation Preservation of corporate culture Stability during difficult periods Strong relationships with customers and employees Strong community focus and social purpose These characteristics can be especially valuable in insurance and investing, where the consequences of important decisions may take years to fully emerge. Fairfax's forty-year record suggests that family control has been a significant positive for shareholders. The structure has allowed management to think in decades rather than quarters, preserve Fairfax's culture, and maintain a consistent capital allocation philosophy through changing market environments. At the same time, investors should remain aware of the risks that accompany any founder-controlled organization. Potential concerns include succession planning, management entrenchment, and the possibility that future leaders may not possess the founder's abilities. No governance structure is perfect. Every structure involves trade-offs. What This Means for Shareholders Ownership structure matters because it influences incentives, decision making, and corporate culture. Fairfax remains a founder-led company with substantial insider ownership, significant voting control, and a leadership team whose financial interests are closely aligned with those of long-term shareholders. Prem's four-decade record of value creation, modest compensation, significant ownership position, and long-term orientation have all contributed to Fairfax's success. The historical evidence suggests that Fairfax's founder-led, family-controlled model has served shareholders exceptionally well. Fairfax's exceptional long-term performance, strong culture, and disciplined capital allocation are all closely tied to the leadership Prem has provided since 1985. The key question for investors is no longer whether this structure has worked under Prem Watsa. The historical record clearly answers that question. The more important question is whether Fairfax can preserve the culture, discipline, and capital allocation framework that Prem built once the next generation assumes greater responsibility. That question is examined later in this chapter when we turn to succession planning. Learn More About Prem Watsa Prem was inducted into the Canadian Business Hall of Fame in 2024. The six-minute biography prepared for his induction provides an excellent overview of his life, values, and the development of Fairfax. It is well worth watching for investors seeking a deeper understanding of the person who built Fairfax. To watch the 6-minute biography of Prem on YouTube, click the link below: - https://www.youtube.com/watch?v=SisxUC232t8

-

@LC, perhaps another way to ask the question is what cost base are you using when projecting future returns from the equity portfolio? Is it Fairfax’s carrying value? Or market value? The starting point matters. I use CV. Therefore, I think Fairfax will be able to outperform the broad market averages over the next 5 years. It really is an interesting thought exercise. The up-front assumptions matter a lot. I appreciate you taking the time to comment… this stuff really is complicated.

-

Fairfax - A Deep Dive on Management and Culture

Viking replied to Viking's topic in Fairfax Financial

Article 1 in the series. I look forward to hearing what other board members think... The Importance of Shareholder-Friendly Management In Berkshire Hathaway's 1977 Annual Report, Warren Buffett outlined four criteria for selecting investments: "We want the business to be: 1. One that we can understand, 2. With favorable long-term prospects, 3. Operated by honest and competent people, and 4. Available at a very attractive price." Notice that management is one of only four requirements. Buffett later explained why: “The certainty with which management can be evaluated, both as to its ability to realize the full potential of the business and to wisely employ its cash flows; The certainty with which management can be counted on to channel the rewards from the business to the shareholders rather than to itself.” Buffett's observation gets to the heart of shareholder-friendly management. Management's role extends beyond operating the business. It must also decide how the cash generated by the business is allocated. Over time, these capital allocation decisions can have an enormous impact on shareholder returns. Management therefore has two primary responsibilities. First, it must operate the business effectively. Second, it must allocate the resulting cash flows in a way that maximizes long-term shareholder value. For investors, evaluating management is not optional. It is a critical part of the investment process. Why Investors Often Ignore Management If management is so important, why do many investors spend relatively little time evaluating it? The answer is simple: management quality is largely a qualitative factor. Most investors naturally focus on quantitative measures such as earnings, profit margins, return on equity, and valuation ratios. These metrics are objective, easy to compare, and fit neatly into spreadsheets. Management quality is different. How do you measure integrity, judgment, capital allocation skill, long-term thinking, or shareholder alignment? There is no formula that can answer these questions. Evaluating management requires observation, experience, and judgment. Yet management often has a greater impact on long-term shareholder returns than many of the financial metrics investors spend their time analyzing. Management determines how capital is allocated, whether acquisitions are made, how much debt is assumed, whether shares are repurchased, and how corporate culture is developed. In The Outsiders, William Thorndike found that the CEOs who created the most value for shareholders distinguished themselves primarily through superior capital allocation. Over time, those decisions compound and can become a primary driver of shareholder returns. For this reason, qualitative analysis should not be viewed as a substitute for financial analysis. It is a necessary complement to it. A Framework for Evaluating Shareholder-Friendly Management Shareholders need to consider many factors when evaluating management. One of the most important is whether management consistently acts in the best interests of shareholders. Do executives think and act like owners? Do they allocate capital wisely? Do they communicate openly and honestly? While no framework can eliminate judgment, it can help investors ask the right questions. One useful approach is to evaluate management using seven criteria: Ownership Alignment – Do executives think and act like owners? Compensation – Are incentives tied to long-term value creation? Per-Share Value Creation – Does management focus on value per share rather than corporate size? Capital Allocation – Is capital deployed rationally and with discipline? Communication – Are shareholders treated as partners? Long-Term Orientation – Are decisions made with a multi-year perspective? Trust and Stewardship – Do actions consistently match words? No management team will score perfectly on every criterion. The goal is to identify management teams that consistently behave like owners and treat outside shareholders as partners. Evaluating Fairfax Through the Lens of Shareholder-Friendly Management Using this framework, Fairfax scores highly. Management owns a meaningful stake in the company, compensation is shareholder-friendly, capital allocation is a core competency, and the organization is managed with a distinctly long-term orientation. Most importantly, management has invested alongside shareholders and created substantial value over four decades. Ownership Alignment: A+ This is one of Fairfax's greatest strengths. Prem Watsa owns or controls approximately 10% of Fairfax's economic interest and more than 40% of the voting power. The vast majority of his net worth remains invested in Fairfax shares. Fairfax has also built an ownership culture throughout the organization. Senior executives receive 50% of their annual bonuses in Fairfax shares that vest over five years, while employees can participate in a stock ownership plan with meaningful company matching contributions. Management's alignment with shareholders was demonstrated again in 2020 when Prem purchased approximately $149 million of Fairfax shares in the open market during a period of extreme pessimism toward the company. Compensation: A+ Fairfax stands out relative to most public companies. For decades, Prem Watsa's annual salary has been C$600,000—remarkably modest given the size of the organization. Unlike many public-company CEOs, he has not relied on large stock option grants or aggressive incentive packages. His wealth has been created primarily through ownership, not compensation. Fairfax purchases in the open market the shares awarded under its compensation programs rather than issuing new shares. As a result, shareholders bear the economic cost of compensation but avoid the ongoing dilution that often accompanies stock-based compensation plans. This approach better aligns employee ownership with shareholder interests and helps protect per-share value. While Fairfax's compensation programs are shareholder-friendly in design, they still represent a meaningful economic cost that must ultimately be justified by improved performance, retention, and value creation. Focus on Per-Share Value Creation: A Fairfax has long emphasized growth in book value per share as its primary measure of success. Management's shareholder letters, annual meeting presentations, and public commentary consistently focus on per-share value creation, demonstrating a philosophy that prioritizes increasing shareholder value rather than simply increasing the size of the company. Just as importantly, management's actions have matched its words. Since 2020, Fairfax has repurchased a significant amount of its outstanding shares when they traded at meaningful discounts to intrinsic value. Rather than pursuing acquisitions or expanding the organization for the sake of growth, management chose to increase the ownership stake of existing shareholders. Capital Allocation: A+ William Thorndike argued that capital allocation is a CEO's most important responsibility because it has the greatest impact on long-term shareholder returns. By that standard, Fairfax's record is exceptional. Since 1985, Fairfax's share price has compounded at approximately 19% annually, including dividends. The record includes mistakes and periods of underperformance, but management has demonstrated an ability to learn, adapt, and continue creating value over four decades. Communication: B+ Fairfax provides more disclosure than most companies. Shareholder letters, annual meetings, and quarterly conference calls provide investors with substantial information about the business, investment portfolio, and culture. At the same time, Fairfax has never focused on promoting its story to Wall Street or cultivating media attention. Consistent with the philosophy described in The Outsiders, management appears to believe that operating the business and allocating capital are better uses of time than managing the short-term stock price. The result is a company that communicates extensively with shareholders, but on its own terms. Long-Term Orientation: A+ Long-term thinking has been a defining characteristic of Fairfax since its founding. Many of the company's most successful investments required years of patience before their value was recognized. Founder leadership and significant insider ownership reinforce this advantage by allowing management to focus on long-term value creation rather than quarterly expectations. Trust and Shareholder Stewardship: B+ Trust is earned through actions over long periods of time. Fairfax has built a reputation for integrity, fairness, and treating shareholders as partners. However, a balanced assessment should acknowledge that management's credibility was damaged during the difficult period from 2010 to 2020. The equity hedges persisted too long, several investments disappointed, and actual results often fell short of expectations. Importantly, the issue was not integrity. Rather, it was judgment and adaptability. Since 2020, Fairfax has rebuilt much of that credibility through actions rather than words. Strong operating performance, improved investment results, substantial share repurchases, and exceptional growth in book value and the share price have helped restore investor confidence. Overall Assessment Overall Grade: A Fairfax scores highly across all seven criteria. Management is strongly aligned with shareholders, compensation practices are disciplined, capital allocation has been exceptional, and long-term thinking is embedded throughout the organization. Most importantly, management has invested alongside shareholders and created substantial value over four decades. Viewed through the lens of shareholder friendliness, Fairfax compares favourably with almost any public company. On that measure, Fairfax earns an A. -

I decided to add a new chapter to my book on Fairfax: Management and Culture. I have six articles on the go. Rather than post them in the Fairfax 2026 thread I decided to post them in a separate thread. My articles are long and positing multiple articles really gums up the 2026 thread. My plan is to post the articles in this thread over the next week (perhaps one each day). Please keep comments in this thread focussed on management/culture. Keep general comments on the Fairfax 2026 thread. Let me know if you think this is a better way for me to post a series of articles. I look forward to hearing from board members on the content of the articles - that is how we all learn and improve (our understanding of Fairfax and as investors). To get started, here is the chapter overview: ------------ Chapter 7: Management and Culture Chapter Overview Most investors focus on financial statements, valuation metrics, and investment portfolios. Yet some of the most important drivers of long-term shareholder returns cannot be found in a spreadsheet. Management quality, organizational structure, incentives, and corporate culture often determine whether a good business becomes a great one. This is especially true at Fairfax. While investors often focus on underwriting results and investment performance, much of Fairfax's long-term success can be traced to its management philosophy, organizational structure, incentive systems, and culture. Understanding how Fairfax is led, how decisions are made, and how the organization is structured is essential to understanding the company itself. This chapter examines six aspects of Fairfax's management and culture: 1. What is shareholder-friendly management? We develop a framework for evaluating management quality and use it to assess Fairfax. 2. Who is Prem Watsa? We examine Fairfax's founder, largest shareholder, and chief architect, along with the implications of family control. 3. How is Fairfax organized? We explore Fairfax's decentralized operating model and why it may be one of the company's most important competitive advantages. 4. What is Fairfax's culture? We examine employee retention, management continuity, and the cultural traits that have shaped Fairfax's success. 5. How are incentives aligned? We review Fairfax's compensation and employee ownership programs to understand how the company encourages managers and employees to think like owners. 6. Can Fairfax succeed beyond Prem Watsa? We assess succession planning, leadership development, and the depth of Fairfax's management bench. The goal of this chapter is to determine whether Fairfax has built a management culture, organizational structure, and leadership pipeline capable of sustaining its success and compounding value for shareholders for decades to come. Keep reading for article 1.

-

Can you please define what you mean by equity portfolio? Are you talking stocks? Are you talking CDS/equity hedges (did well), equity hedges/shorts (did poorly) and TRS(did well)? What exactly are you trying to measure?

-

I think it is pretty much impossible to determine a rate of return on Fairfax’s equity book over the past 40 years. What do you include? CDS? Equity hedges? TRS? Some of these were risk management positions, others were investments? But we do know with certainty one thing: Fairfax’s share price compounded at 19% for the past 40 years (US$; dividends reinvested). That is elite performance. Clearly, Fairfax is doing a number of things exceptionally well. Fairfax has two businesses: Insurance Investments. We also know returns from the insurance business were weak pre-2010. As a result, I suspect investments have been an important driver of long term results. What did they return each year? No idea. And I don’t need to know… All I have to do is look at the stock price to know what I need to know. (Fairfax’s total performance has been elite.) I am a quickly becoming a Thordike desciple…. Capital allocation is the most important thing over the long term for a company like Fairfax. Capital allocation drives per share results over the long term more than anything. But assessing capital allocation is not easy - so most investors/analysts ignore it. Instead they focus on other things that are easier.

-

KW is an interesting company. I totally agree with you - retail shareholders in KW got taken out behind the woodshed owning the stock. But my read is Fairfax did ok. The stock they owned was table-stakes (as Jamie Dimon would say). It got Fairfax access to Kennedy Wilson’s deal flow. Real estate partnerships. Mortgage loans. ThePacWest deal was an absolute home run for Fairfax (still is). And in the end, it also allowed Fairfax to take KW out on the cheap (at least that is my initial uneducated read). Real estate is deeply out of favour - this is likely an ideal time to buy something like KW. Now having said all that… KW is a bit of a complex beast… so I could be completely off base in terms of how it works out for Fairfax. We will see. It reminds me a little of when Fairfax took Recipe private when Covid was still a thing here in Canada - Fairfax got it cheap (in terms of buying when there was a lot of pessimism).

-

Can you explain to me what the financials look like for each investment? What was the money Fairfax put in? (That is not the reported deal price.) What is the (likely) return they are going to generate off it in the coming years? Bottom line, I am being open minded with their new purchases. One reason is I haven’t spent a lot of time trying to understand them. I will get around to it. Another reason is Fairfax has been hitting the ball out of the park - as a result, I am giving them the benefit of the doubt. i don’t expect them to be perfect. Some investments will look like clunkers. Lynch said if you are right 6 times out of 10 you will do well in this business. I am not worried when it comes to Fairfax’s equity portfolio these days.

-

Is there a reason you use 15 years as the benchmark? Buffett has said that 5 years is a good timeframe to use to evaluate a management team. That is my preferred measure. Does year 6 to 10 performance matter? A little, but much less IMHO. What about year 11 to 15? Interesting… but too long ago to matter much IMHO. For instance… back in 2013, I did not use a 10 or 15 year timeframe to evaluate Fairfax’s management team at the time (their investment returns). That would have been pretty dumb, given the CDS and equity hedge positions (that worked fabulously well from 2007-2009) would have completely skewed results. The best way to evaluate Fairfax in 2013 was to look primarily at what they owned at the time, how the positions had performed recently (prior 5 years), and what their prospects were (next 5 years). (I did that and then sold all my shares in Fairfax.) Imagine using a 15 year timeframe to evaluate management at BlackBerry back in 2013? It would have told an investor to back up the truck… Really? One of the benefits of using 5 years is it makes calculating rate of return easier. Fairfax has a very concentrated portfolio: Eurobank FFH-TRS Poseidon Fairfax India - primarily BIAL Orla Mining Do I care today that Eurobank was a terrible business in 2014? Nope. What I care deeply about is what kind of business Eurobank is today - and it is a very good business. Could that change? Of course… that is why I listen to every quarterly call). Holdings get much smaller after the big 5. But there are a bunch of stars in there as well. Fairfax’s hit rate the past 5 years is nuts. To this, add the returns on the holdings they sold in the last 5 years: Resolute Forest Products Stelco Sigma Orla (part) Poseidon (part) All were massive home runs (5-year returns). And then, of course, we should also add the gains on the insurance businesses they IPO’d/sold in the last 5 years… this needs to get counted somewhere… Digit Pet insurance Ambridge Euolife’s life insurance business More massive gains… After all, at the end of the day, we are trying to evaluate a management team on their capital allocation skills. It should be fair and balanced and look at all the important pieces. How has Fairfax performed over the past 5 years? They have smoked - absolute and relative to the S&P500. Especially if you use the correct cost basis: FFH-TRS cost basis is not the starting value of Fairfax’s share price. It is much less. Interestingly, the last 5 years had two bear markets: 2022 and 2025 (I think just qualified). There was also a historic bear market in bonds. Yes, the starting point (Dec 31, 2020) was very favourable. But that is when you look at performance vs the S&P500. For the past 5 years, Fairfax’s capital allocation has been best-in-class and it is not close. The fact that people don’t get it is not surprising - this is Fairfax after all.

-

@djokovic1, thanks for the comment. Good luck with the pitch

-

Fairfax built their stake in Seaspan/Atlas over a number of years. And they made a number of different investments (the roll over of APR being one example). To keep the analysis simple (especially the time value of money part) I decided to take a FIFO approach. The key point: Seaspan has been one of Fairfax’s best-ever investments.