SafetyinNumbers

-

Posts

2,895 -

Joined

-

Last visited

-

Days Won

41

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

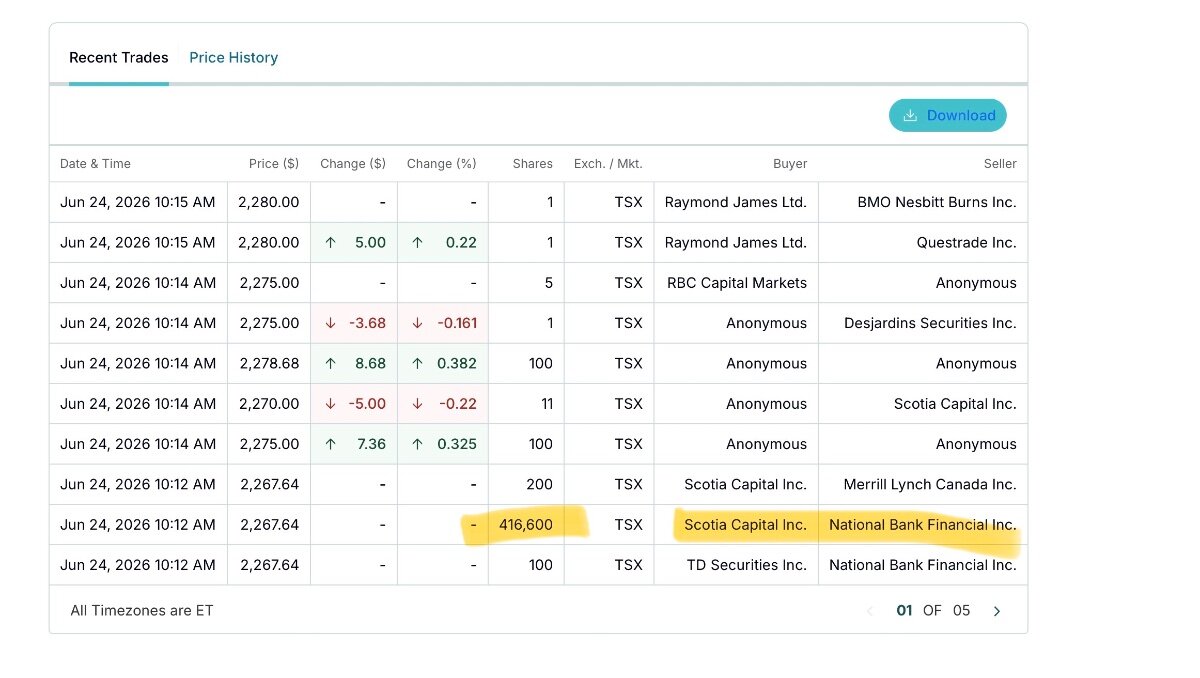

This could be the buyback. Scotia has the NCIB, no uptick, suggests it might be. The size might indicate it’s taking off TRS but I hope not.

-

Intrinsic value growth has been double digits since inception after fees. It not being reflected in the stock is the opportunity. Just like FFH, the conservatism and accounting policy make it so that book value growth lags intrinsic value growth. After 11 years, like FFH, the NAV can only be suppressed for so long.

-

Fairfax - A Deep Dive on Management and Culture

SafetyinNumbers replied to Viking's topic in Fairfax Financial

I think the real problem is the market structure. It’s the minority shareholders that determine what the equity is valued at by the market. Fairfax pays a big premium to that. The majority of the minority have to approve any transaction. They always go along because either they have better options for their capital or they don’t want to stomach a drawdown. I’m glad Fairfax is designed to take advantage of inefficient markets. It’s part of what makes me think a 10 year CAGR of 20-25% is more likely than <15%. -

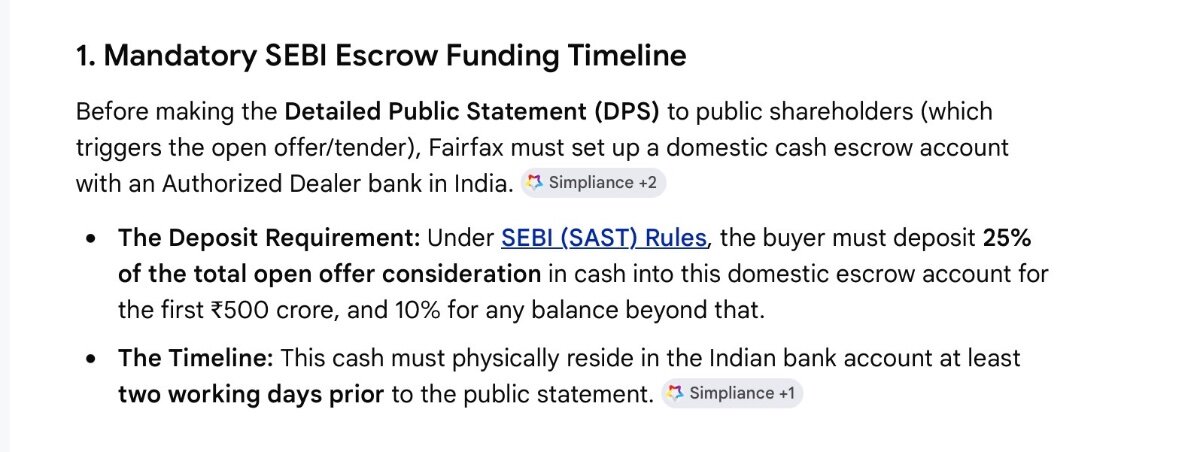

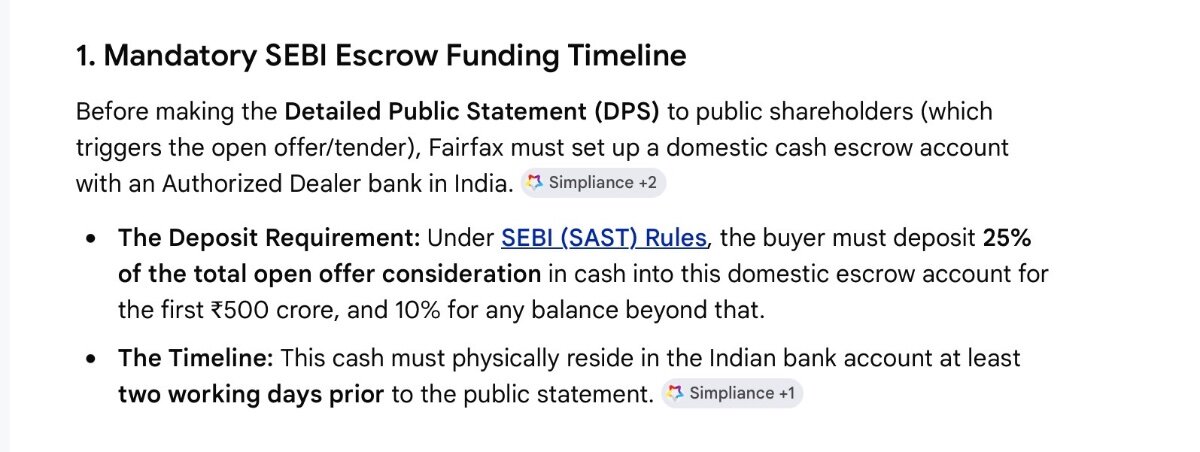

I think it was more to do with the escrow requirements but I’m an optimist.

-

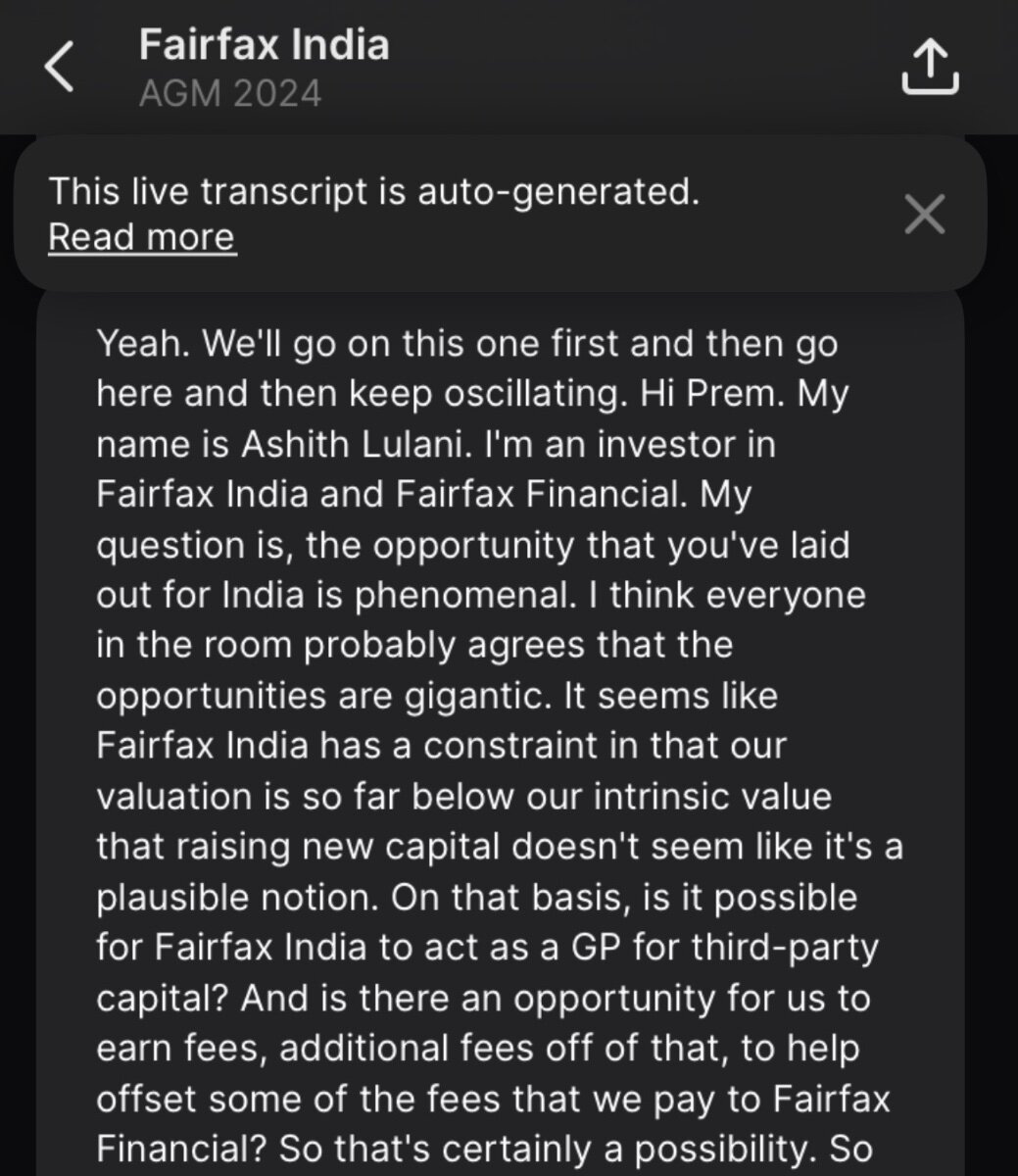

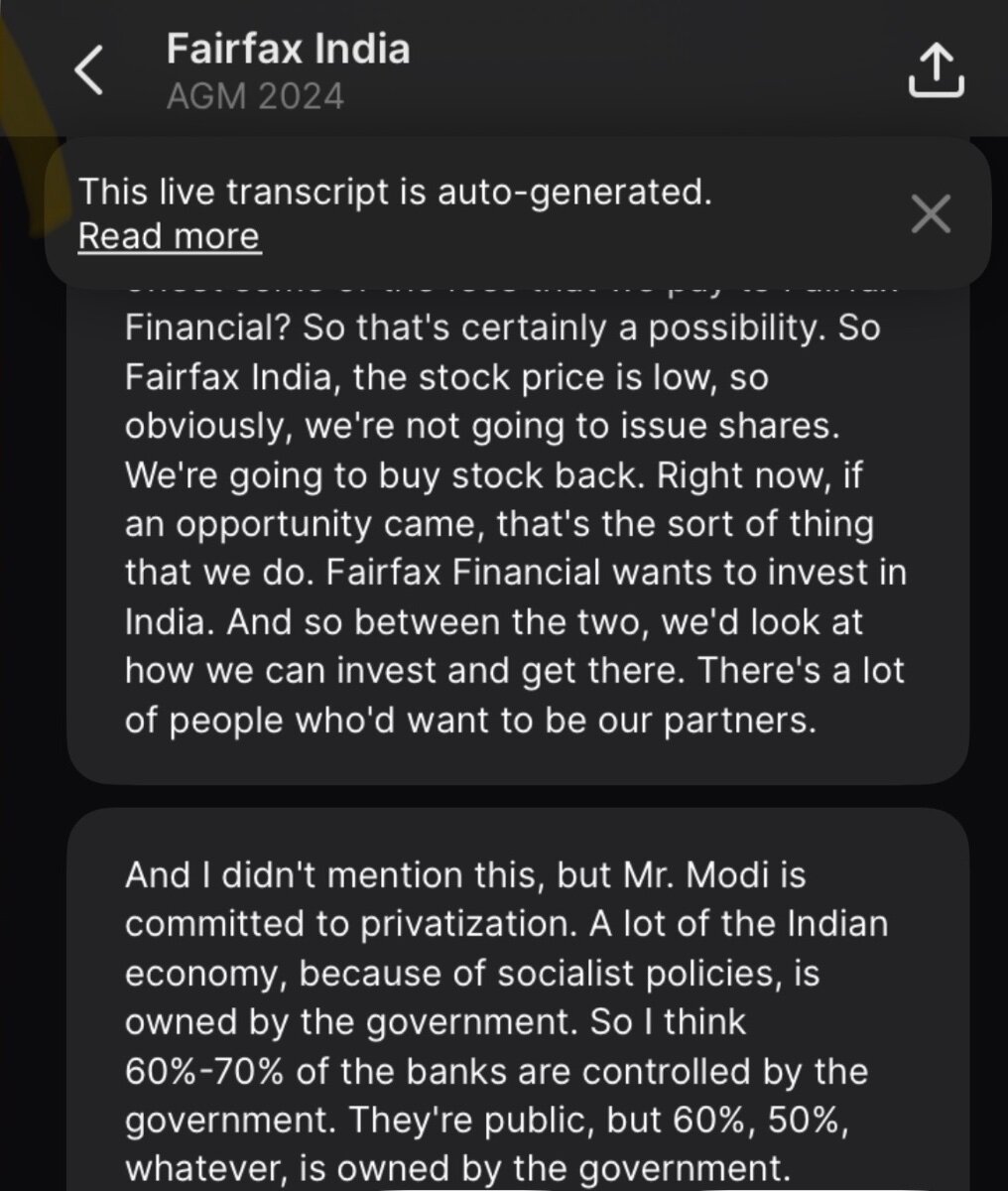

I’m Canadian. No clue on Mr. Lulani!

-

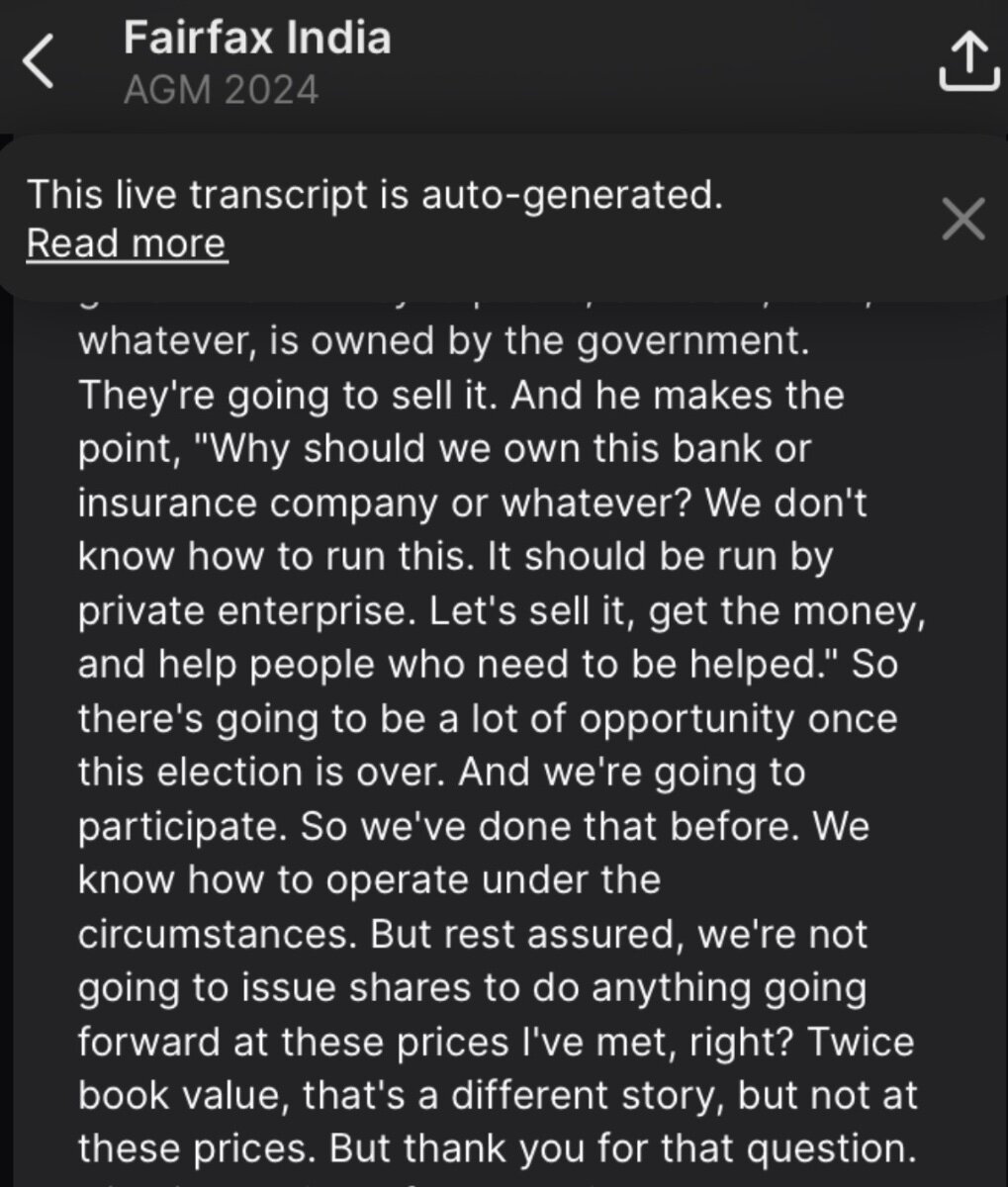

Zero chance new FIH shares are issued. I assume it will be a GP/LP structure with an FIH subsidiary as the GP and FFH along with other global investors as LPs. Ashith Lulani asked the question in the 2024 AGM and I think the answer is probably the same today.

-

Perhaps part of the GP/LP structure. I can see the regulator allowing them to defer announcement until it’s made public in India. Apparently there is a process to have funds onshore ahead of a tender announcement.

-

There shouldn’t be a link between the two but maybe it pushes the regulators along.

-

International is growing faster and parts of casualty are still strong. They also plan to use less reinsurance so they might grow net premiums by 5% not 3%. That needs a billion plus in capital. They do need capital to buy Allied World but, Eurolife is supposed to close next quarter and they raised the $750m in 30 year debt so have plenty of liquidity to scoop those up. Again, I don’t think the decision is acquisitions vs dividends at the subsidiary level. The constraints at the holdco seem to be maintaining the investment:equity leverage and debt:equity leverage.

-

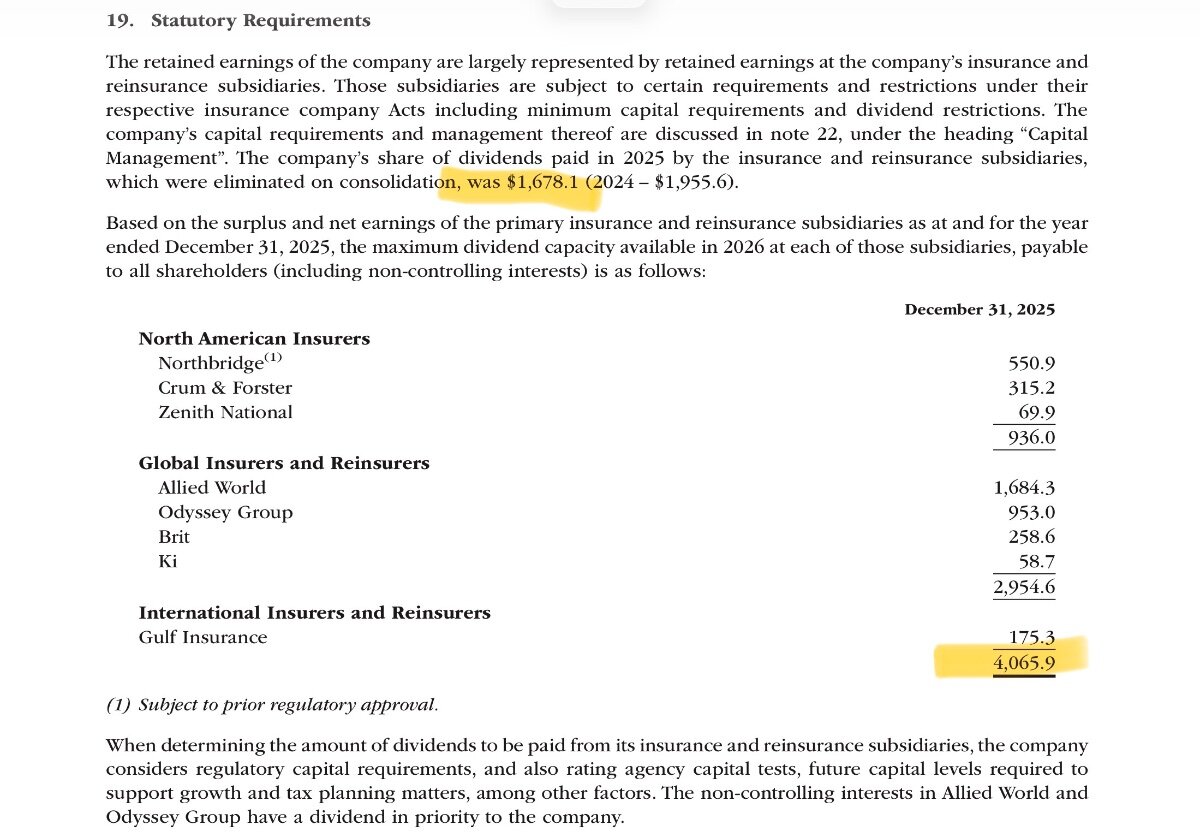

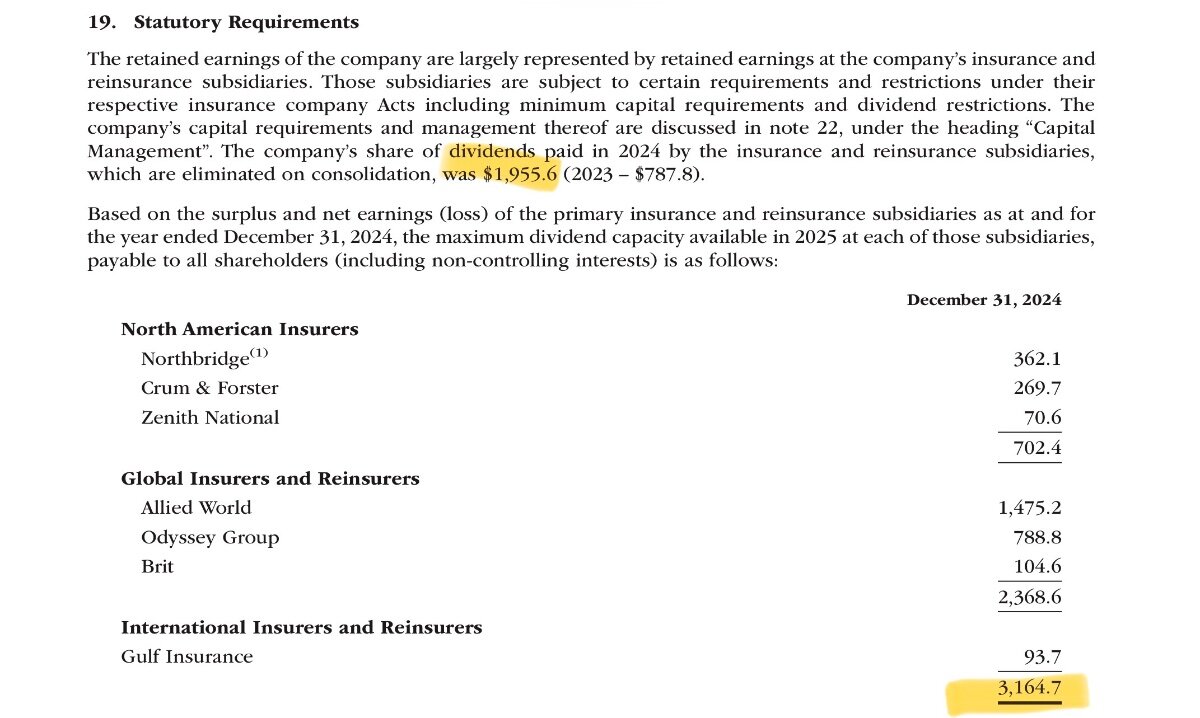

How do you define cash flow? Last year they spent a bit less than the dividends from the insurance subsidiaries on buybacks. I think that’s a good estimate for FCF. The insurance companies still need capital to grow and their portfolio turnover shouldn’t have much to do with buybacks except to the extent it creates excess capital. This year they are allowed to dividend up $4b. So far this year they are on pace for over $2b of buybacks.

-

I’m not sure the index return has much to do with what Fairfax’s portfolio does. Do you consider the difference between economic return and accounting returns in your analysis?

-

What’s middle of the pack numerically?

-

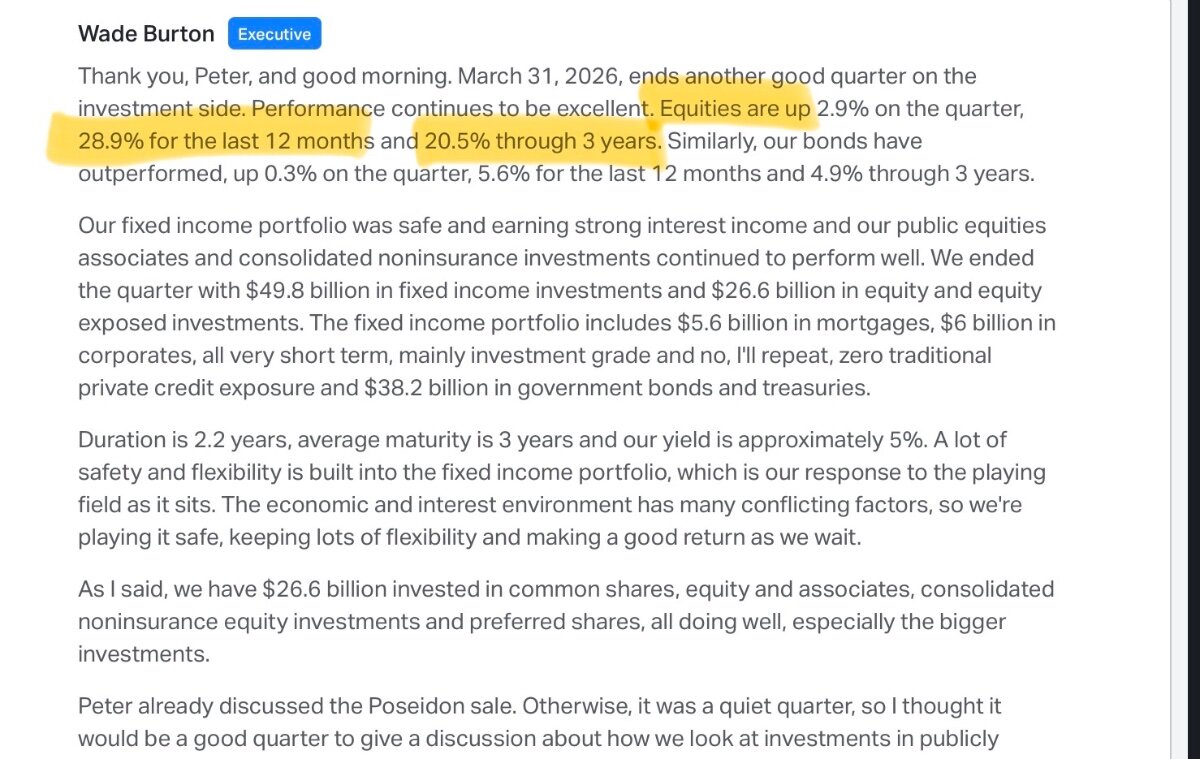

The equity returns were strong when underwriting was weak. Then the equity returns were weak when underwriting was strong. That generated 18%+ CAGR in BVPS. Now they are both strong. It will be interesting to see if returns are better than the <10% built in to the share price.

-

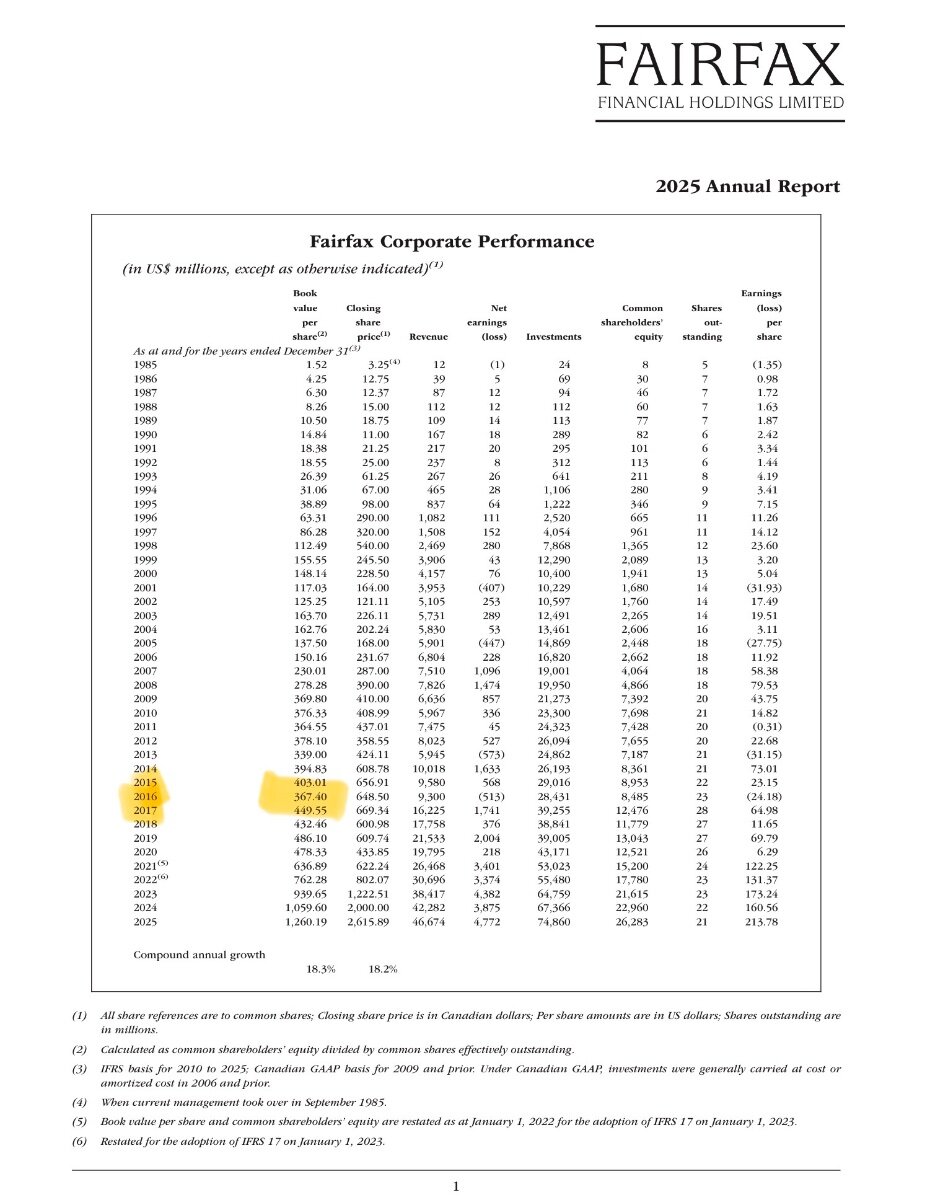

I think it was 19% over 39 years but I can’t find the reference. Last three years have been good as we know but most of it hasn’t shown up in accounting returns yet.

-

The market structure changed a lot during the period you are focused on. I think if you are uncomfortable with leverage you shouldn’t own Fairfax. I see the leverage as a feature not a bug. They did change their investment style by taking more control and significant influence positions (which hurts reported returns up front) but not their process of looking for margin of safety. Again beating the index is an outcome of the process not the goal. Most institutions since the GFC are focused on short term relative returns b/c they want to keep the AUM. Thankfully we don’t have to play that game.

-

How about 40 years?

-

The goal isn’t to outperform the S&P, it’s to generate absolute returns. Over time the process should outperform the S&P especially when the leverage is included. This most recent 15 year period the backdrop was particularly difficult for this investment style because of the change in market structure. Further, the decision by Fairfax to accumulate more significant influence and control positions ensures that the accounting returns lagged economic returns since 2012. While the lag continues, the gains are coming pretty regularly now as the strategy has matured.

-

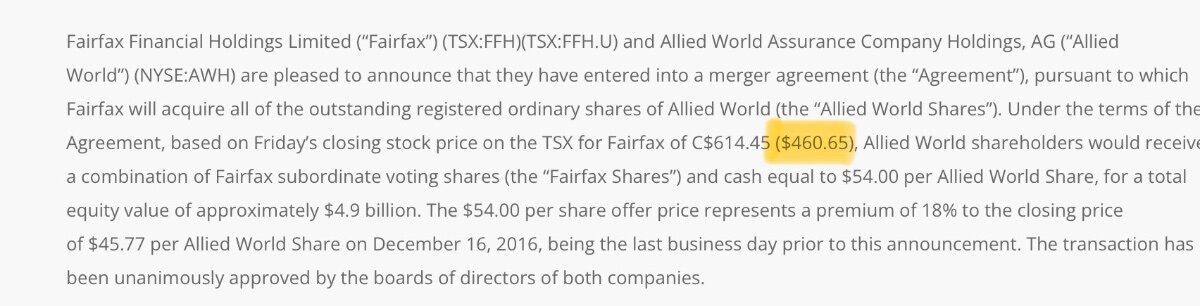

When they announced the deal in December 2016, the stock was trading closer to 1.3x BV. That’s when the Allied World BOD signed the definitive agreement. In March 2016, they also issued equity for closer to 1.4x BV. This was in a backdrop of low interest rates so ROE was structurally lower.

-

Probabilistic investing often looks like luck.

-

That’s what makes a market. I don’t expect them sell at these prices. I think they will ultimately sell the whole bank to a much larger European bank at a premium which will facilitate the exit.

-

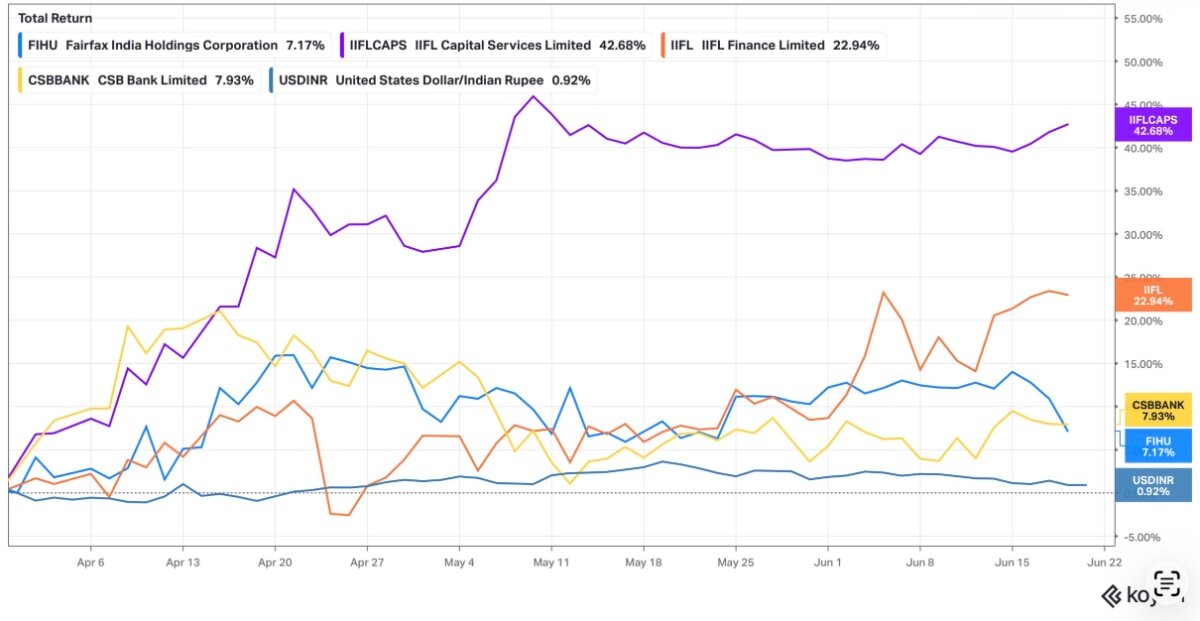

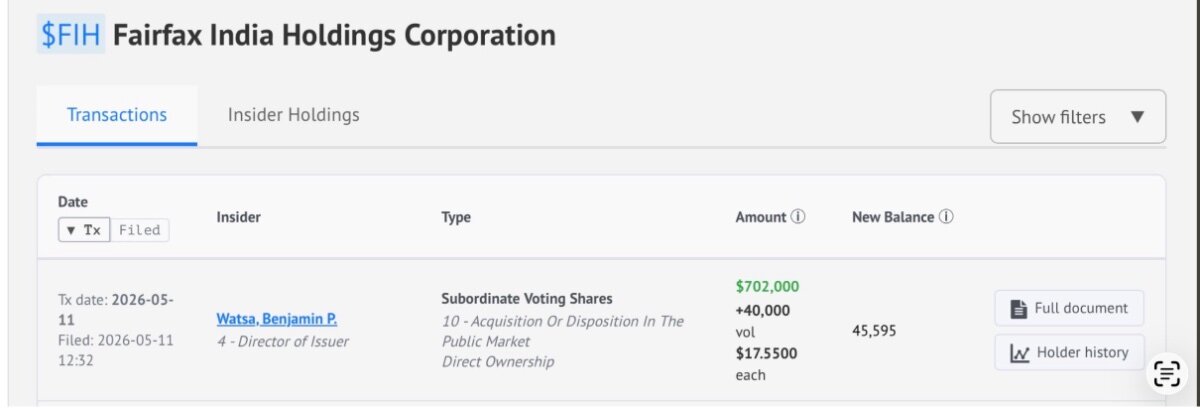

I think you mean highs. INR is down less than 1% this quarter to date. The big decline in the oil price is a big positive. Ben Watsa added 40k shares at $17.55 a few months ago before the war ended. Anchorage could IPO or IDBI could be bought. Both accelerate book value per share growth when they happen. Q2 as it stands now looks good as the listed companies are up a lot and the private companies will continue to accrete. The FX hit is also tiny compared to last quarter.

-

Me too! Big spread vs INDA today of ~5% underperformance. I think some investors worry about IDBI b/c they think it will be funded with newly issued equity. I can’t think of any other reasons for the weakness.

-

Is ~10x PE / 1.3x BV for Eurobank really fair value for a 15%+ ROE on TBV? I think FV is a lot higher. For accounting returns it’s contributing at over 20% given the earnings yield on carrying value. Plus with dividends and buybacks it’s returning a lot of cash. I pay attention to what they own of course but I know they will make mistakes. For the next few years at least, I don’t think we have to worry about the accounting returns which is what supports the stock.

-

I caution against using the stock price as a basis for value creation. I’m hopeful there is a lot of hidden value here since development properties don’t screen well.

-

I think so. I recall disclosure suggesting they recovered all of their capital back in that deal.