Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

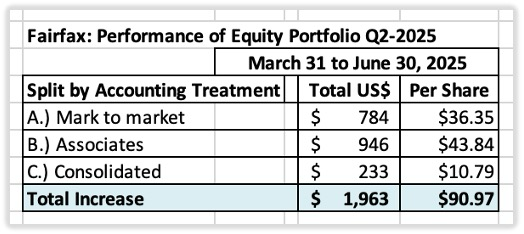

It is very interesting to read the updated analyst reports on Fairfax after results are released each quarter. With each report we learn as much (if not more) about the analyst/firm than we learn about Fairfax. The biggest single driver of economic results at Fairfax in Q2 was the significant increase in the value of Eurobank. This was captured in excess of FV over CV for associate the consolidated equity holdings, which increased $1 billion in Q2 to $2.4 billion. This was an increase in the quarter = $42/diluted share (pre-tax) or about $34/share (after tax). This puts 'economic EPS' in Q2 at about $96/diluted share ($62 + $34). What is interesting is some analysts don't even discuss the increase in 'excess of FV over CV' in their Q2 reports on Fairfax. Does that mean it didn't happen? Or that it is not important? What is interesting is if Fairfax owned less than 20% of Eurobank (they own 32%), the significant gain would have been reflected in Q2 earnings. What is puzzling is Fairfax's communication is very clear and transparent when it comes to 'excess of FV over CV.' So 'I didn't know' is not a good excuse. As updated Q2 reports come out we are learning which analysts/firms understand Fairfax’s business model. And which clearly do not.

-

@nwoodman +1

-

@charlieruane, a large special dividend just makes so much sense to me (something like 4% or even 5%). But I am not sure how this impacts the many families who each own hundreds of millions in stock (from a tax perspective). In recent years, Buffett really seemed to be prioritizing the needs of this group in how he was managing the company. At least that is what it looked like to an outside observer of the company.

-

@gfp and other BRK shareholders... I have a question. What do you think Abel will do with the cash pile at BRK in the next 2 or 3 years? Acquisitions? (including publicly traded stocks) Stock buybacks? Permanent dividend? Large one time dividend? Nothing? (let it keep building) IF Abel gets moderately more aggressive in redeploying the cash hoard we might have a catalyst for EPS. It really is a crazy set up when you think about it (how much cash that has built up on the balance sheet).

-

@Txvestor , my guess is Fairfax's decision to sell $1.1 billion in treasuries with maturities of 28 to 30 years in Q2 has little to do with where the Fed funds rate (very short term rates) might go in the next couple of months/year. Here is what we know: Trump is going to stack the Fed with a bunch of yes-men/women. The big move will be replacing Powell. When that happens, the Fed Funds rate will be coming down, likely fast and by a lot. How will financial markets respond? No idea. Trump is going to implement tariffs on all trading partners - the MINIMUM rate will likely be 15%. This is a slow moving process... it will take another 6 to 12 months to start to understand what this might do to inflation/the economy etc. The BBB locks in (and likely grows) massive deficit spending at the Federal level. Deficit spending usually juices the economy. It looks to me like the risks of higher inflation are going up. Note, I am thinking 'moderately' higher... not spiking. But here is the kicker. To state the obvious, Trump is a non-traditional thinker. How 'safe' are US treasuries today? The short answer is they aren't. Trump will not hesitate to run roughshod over Treasury bond holders if it furthers his aims. Long duration Treasuries are the most risky in this context. My question is why would anyone want to hold Treasuries with maturities from 28 to 30 years today? Especially if they don't have to (like Fairfax). As I said in my Q2 earnings recap, I don't think long duration Treasury holders are getting adequately compensated for the risks. Note, I am not 'pessimistic' in saying this. We could get a melt up in asset prices (and moderately higher inflation). The big move in gold over the past year might be telling us something important (or not). Bottom line, Bradstreet and the fixed income team at Fairfax have a brilliant 40 years track record. And their strength is navigating the exact environment we are in today. They know more in their pinkie finger than I will ever know in my lifetime about trying to invest in Treasuries and the fixed income market. I agree with @Santayana 'In Bradstreet (and team) we trust.'

-

Sky-high energy prices destroying European industry, warns metal giant https://ca.finance.yahoo.com/news/sky-high-energy-prices-destroying-080000103.html “Metlen’s core business is metal refining. It produces bauxite ore from its own mines in Greece where it also has a refinery and smelter. They annually produce 190,000 tonnes of aluminium and 860,000 tonnes of alumina, a vital ingredient in advanced ceramics. “From the same ore it is now also extracting gallium, a strategically vital metal where China has long dominated global markets. Metlen is also increasingly involved in metal recycling, melting down scrap and targeting valuable metals like zinc and lead. “The company has managed to avoid energy-induced shutdowns because its other key business is energy production: it owns around 14 wind farms, three solar farms and four hydroelectric plants, mostly in Greece, plus several gas-fired power stations. “It uses those generators to power its metal refining, giving it a near-unique level of immunity from the high energy prices that are wiping out energy-intensive industries across the UK and Europe.”

-

@nwoodman, thanks for posting these reports. They have help me a lot over the past 3 years to better understand what is happening at Eurobank (and there had been a ton of things going on).

-

@gfp and @mengan, I appreciate you both getting into the weeds regarding the accounting, and the differences in GAAP and IFRS. Very helpful for us non-accountant types.

-

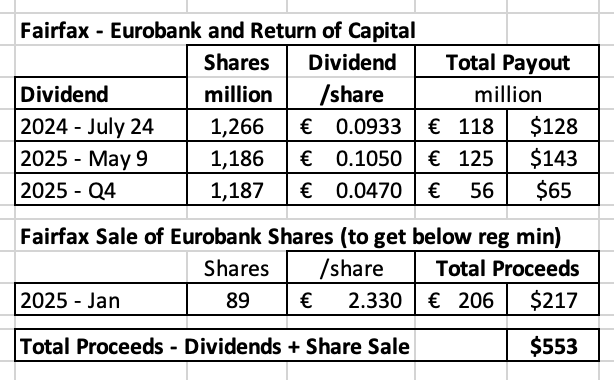

@nwoodman, thanks for the detailed update on Eurobank. And the detailed analysis. I think it's great to get different takes on topics. Below is a summary of my current take on the company followed by a summary of quotes from the Q2 earnings call transcript. --------- Eurobank is Fairfax’s largest equity holding (by far). With Q2 results, the company continues its exceptional performance. It continues to be positioned exceptionally well. Below is the link to all the material supplied by Eurobank (including the link to listen to the earnings call). https://www.eurobankholdings.gr/en/investor-relations/financial-results-pages/first-half-2025 Eurobank is an exceptionally well run bank. Why do I keep saying this? 1.) They underpromise and over deliver. Over and over. 2.) Their communication is very good. Their disclosures are detailed and transparent. Their answers on the Q&A actually answer the questions being asked - it is clear they understand their business inside out. 3.) Capital allocation is exceptionally rational (see points 4 and 5 below) 4.) They have a multi-year strategic plan and they are executing it superbly. Exiting Serbia in 2023. Aggessively growing in Cypress (banking and insurance) in 2023 and 2024. Aggressively growing the asset management business in 2024 and 2025 (fee income is spiking). Investing in technology/systems (yes, this has a short term cost... but it is necessary, especially in today's environment). 5.) They are extremely shareholder friendly. Small stock buyback was done in late 2023. Dividend was reinstated in 2024. Dividend and buybacks are being done in 2025. Second dividend will be paid in Q4. Payout ratio (dividend + Share buybacks) in 2025 will be more than 50% of earnings. 6.) The future is bright. Lots of opportunities to grow the top line and also bring down expenses. The integration of the Cypress businesses (Hellenic Bank, Eurobank and CNP) will get going in 2H. This should deliver significant cost savings. Bulgaria adopting the Euro will be a big tailwind for banks beginning in 2026 (boost to NII and the economy). The growth of the asset management business is likely still in its early days. More acquisitions are likely to happen in the coming years. ---------- The new dividend payment in Q4 will be about $65 million for Fairfax. Eurobank has been significant 'source of cash' for Fairfax in 2H 2024 and 2025. ----------- Below are some highlights from the Q2 conference call. My comments are underlined. What follows are comments that were made by either Fokion (CEO) or Harris (CFO). Summary Eurobank reported robust financial performance in the first half of 2025, achieving an adjusted net profit of EUR 711 million and a return on tangible book value of 16.6%. In more detail, net interest income rose 12% year-on-year as the quarter-on-quarter drop decelerated to less than 1%. Fees and commissions were up by 29% year-on-year, supported by a strong second quarter. As a result, corporate provision income was up by 7% year-on-year to over EUR 1 billion. The cost of risk ratio remained at 60 basis points, in line with our full year guidance. Asset quality remained resilient for another quarter with the NPE ratio decreasing to 2.8% and coverage exceeding 90%. As a result, core operating profit reached EUR 866 million. This is more than 6% higher year-on-year. In conclusion, the first half results were in line with our plan, notwithstanding a more rapid decline in ECB interest rates. Consequently, we anticipate that the return on tangible book value will exceed the initial annual target of 15%. The strong first half performance allows us to align with other European banks policy by introducing for the first time a 2025 interim cash dividend of EUR 170 million. This is EUR 0.047 per share to be distributed in the fourth quarter. An update on cost optimization (brining down expenses) Cost optimization efforts continued. Indicatively, in Bulgaria, staff decreased by more than 400 FTEs year-on-year and branch network reduced by 34 branches. This rationalization improved Bulgaria's cost-to-income ratio from 40% to 37.8% despite a declining interest rate environment. In Cyprus, the scheduled legal merger between Hellenic Bank and Eurobank Cyprus is set for September, expecting to accelerate cost synergies. An increase in lending is mitigating decline in NII (lower interest rates) Overall, in the second quarter, the group delivered accelerated performance, supported by robust lending expansion, increased deposit volumes and strong underlying core proitability indicators. The decline in net interest income was moderated as loan growth helped offset the adverse effect of decreasing rates. The consolidation of CNP Insurance had a positive impact of fee income, which remained solid overall, while strategic cost optimization initiatives continue to be implemented across all regions. Now expects to exceed 15% ROTBV target for 2025 Looking ahead, based on the first half performance, along with projected loan and bond volumes, anticipated lower MREL costs and solid fee income, the group expects to exceed its 15% return on tangible book value target for 2025. Net Interest Income (NII) For NII, we have run a top-down exercise some weeks ago. And based on that, we reaffirm our initial target of EUR 2.5 billion, even assuming the ECB terminal rate reaching 1.5%. That was the assumption when we run this top-down exercise. This implies that the expected average DFR for the year to be 35 basis points lower than our initial expectation, i.e., at 2.19% versus 2.53%. So the EUR 2.5 billion NII guidance is maintained as a result of higher loan deposits and bond volumes and better MREL management. Capital Allocation What is next? We have stated before that we are interesting not only for nonorganic growth in banking, but also in insurance and asset management in any of the 3 countries that we have a presence. So Bulgaria could be a possibility if there is the right opportunity. And again, the interest may be not only in banking, but also in insurance and asset management. At the moment, there is nothing that is advanced in terms of discussions. There is no specific target. But these opportunities may come at the time that we don't expect. For this reason, we would like to keep an amount of excess capital for potential inorganic growth opportunities. And based on these facts, so the fact of a strong loan growth and our desire to keep an amount of excess capital, we reiterate our commitment for a payout ratio of more than 50%. Initiates interim dividend and still has lots of firepower left in share buyback program Now our decision to initiate an interim dividend distribution of EUR 170 million or EUR 0.047 per share to our shareholders underscores also our commitment to shareholders' reward. And let me also remind everybody that our share buyback program, which is the largest as we speak, in the Athens Stock Exchange remains active. Out of the EUR 288 million of the program, so far, EUR 80 million have been used, which corresponds to an acquisition of 28 million shares, which is 0.77% of the share capital. And as we have stated in the past, any shares acquired through the program will be canceled out. Bulgaria Euro Adoption In Bulgaria, we expect about… EUR 1 billion of liquidity to be released because of the reserve requirements. So this is going to boost the NII 2026 onwards. The euro adoption is going to have definitely positive consequences for the economy overall. And this is good for the banking sector. The 4 largest banks control about -- and Eurobank is one of them, control about 75% of the banking sector. So there is still some room for further consolidation, which we monitor very closely. Change in Guidance for 2025 There are 3 items. In terms of (loan) volumes, we said we update our guidance from EUR 3.5 billion to EUR 4 billion for the full year 2025. In terms of fees, the guidance that we have provided before is the minimum that we should expect. There is upside potential there given the second quarter results in terms of fees that were quite encouraging. And overall, in terms of return on tangible book value, we said that they're going to be higher than the 15% initial target.

-

@Hoodlum, thanks for posting these updates. It is much appreciated. This will put a bow tie on a busy years for Recipe and Fairfax: Takeout of minority partner’s 16% stake - securing 100% of Recipe for Fairfax. Takeout of KRIF - securing 100% of the Keg banner for Recipe. Purchase of rights/restaurants of Olive Garden Canada. This does a couple of things for Recipe. Simplifies Recipe’s ownership structure. Gives Fairfax 100% control. Gives Recipe 100% control over all of its restaurant banners. Provides Recipe with some growth opportunities, like expanding Olive Garden in Canada (there are only 8 locations, all in Western Canada) and perhaps The Keg in the US. The Keg (KRIF) will provide a nice pickup in earnings for Recipe. Recipe will provide a nice pickup in earnings for Fairfax (16% will no longer be going to the minority partner). This also likely gives Fairfax the option to IPO Recipe (all or part) at some point down the road. I really like that flexibility this gives Fairfax with this asset moving forward. ————— Regarding KRIF, here is what the press release said for timing: “Subject to the satisfaction or waiver of all conditions to the Transaction, the Transaction is expected to be completed on or about August 13, 2025.”

-

@73 Reds, I call 'interest and dividend income' the most important for two reasons: It is the largest income stream. Depending on what you measure it against, it is about 40% to 45% of all income streams. It is also the one most revered by analysts/investors. Because it is considered stable and predictable = low volatility. I think Fairfax has come to appreciate this income stream over the past couple of years. Its size and consistency is generating an enormous amount of cash flow each year - that can opportunistically invested into the best available opportunities. But at its core, I think Fairfax is a total return investor (with a long term focus). But having said that, Fairfax has been aggressively adding to their 'non-insurance consolidated holdings.' The Recipe take-private in 2022 was very opportunistic - they got the business for a good (great?) price (they did not have to pay a premium to take it private - they bought it at the tail end of covid when full-serve restaurants in Canada were still on sale). Grivalia Hospitality and Peak were businesses they already owned - they just took out their partners. Meadow Foods and Sleep Country were the new purchases. Is the goal to become a conglomerate like Berkshire Hathaway? I am pretty confident the answer here is a hard no. I think Fairfax wants to continue to grow its P/C insurance business. I also think they like to have a variety of income streams (and assets) and some that are not correlated with P/C insurance. It provides some nice diversification for the company. Fairfax is focussed on growing per share value for long term shareholders. They want to do this primarily as a P/C insurance company. And when it comes to capital allocation they are very open minded - the range of proven capabilities they have is amazing. How Fairfax allocates capital is very different than Warren Buffett/Berkshire Hathaway. Sorry, not sure if I answered your question...

-

Fairfax Q2-2025 Earning Results - 7 High-Level Thoughts I thought this would be a good time to get out of the weeds. Instead, with our review of Q2 results at Fairfax, we are going to zoom out today and look at the big picture. What did we learn about Fairfax from their Q2, 2025 results? Let me know if you agree/disagree with my list. What did I miss? 1.) Fairfax has a very good P/C insurance business Combined ratio = 93.3% Underwriting profit = $427 million Net premiums written growth = 4.8% Yes, the hard market is slowing. Top line growth in insurance is slowing. Nice to see that Fairfax is being disciplined (although Mr. Market will probably not like it). However, Fairfax will be able to continue to grow their P/C insurance business at above average rates - in addition to growth of NPW - by taking out their minority partners (see comment 5 below). 2.) Fairfax’s most important income stream spiked higher in Q2 Interest and dividend income = $666 million (was $606.5 million in Q1) Increasing by 10% in one quarter is a big deal. This puts the annual number at about $2.6 billion. It increased because the total investment portfolio continues to grow in size. And Fairfax continues to invest it very well. Yield of fixed income portfolio = 5.1% (same as Q1) Average duration of fixed income portfolio = 2.4 years (down from 3.3 in Q1) Fairfax also reduced the average duration of its fixed income portfolio from 3.3 to 2.4 years. They sold U.S. treasury bonds with maturities principally between 28 to 30 years for net proceeds of $1,129.2. Why? Probably because investors are not being compensated appropriately for the inflation risk on long dated US Treasuries. This is prudent risk management on the part of Fairfax - protect the balance sheet. Will analysts hate this move - because it reduces ‘visibility’? Probably. But analysts are focussed on the short term. Fairfax is running the business for the long term - and shareholders should applaud that. 3.) A new income stream is breaking out for Fairfax Fairfax already has 4 large income streams: underwriting profit, interest and dividend income, share of profit of associates and investment gains. The fifth income stream is non-insurance consolidated equity holdings. In recent years Fairfax has been investing heavily in this bucket of equity holdings. Since 2022, it has added Recipe, Grivalia Hospitality, Sleep Country, Meadow Foods and Peak Achievements. To go with legacy holdings AGT Food Ingredients, Dexterra and Sporting Life. I have been (impatiently) waiting 2 years for this bucket of equities to start delivering bottom line results that are in line with its potential - and it appears we might be there. Q2 = $126 million This puts the annual number at about $500 million. This is an important emerging income stream for Fairfax. My guess is it will be Fairfax’s fastest growing income stream moving forward - especially with the hard market in insurance slowing (capital will go to where it earns the best return). And yes, results for this group will have some volatility. 4.) Fairfax (and the team at Hamblin Watsa) continues to invest exceptionally well We got two important updates on the conference call today regarding a couple of Fairfax’s largest investments in recent years. PacWest construction loan portfolio In June of 2023, Kennedy Wilson and Fairfax purchased a $4 billion construction loan portfolio from PacWest. PacWest was caught in the regional bank crisis and they were forced to sell their best assets at a discount. (Of note, Kennedy Wilson also got the loan platform from Pac West - the 40 people who were running the loan portfolio also moved over the Kennedy Wilson.) We got an update today on how this investment has been performing for Fairfax over the past three years. Wade Burton, CIO and VP of Hamblin Watsa on the Fairfax conference call today: “Within the fixed income portfolio, our mortgages continue to perform well. We have been repaid on $1.8 of mortgages from the Pacific Western Bank transaction, where we purchased approximately $4 billion in commitments at 95% of par in 2023. The IRR on the loans repaid thus far is 14.7%. Thanks to the outstanding work of Bill McMorrow, Matt Windisch and their team at Kennedy Wilson, these mortgages are proving to be a fantastic investment for Fairfax.” Blizzard Vacatia (Berkley Group) One of Fairfax’s largest investments in 2025 (January) was the purchase of the Berkley Group, one of the largest independent timeshare companies in the US. With this deal, Fairfax partnered with Caroline Shin and her team at Vacatia. The partnership is called Blizzard Vacatia. Fairfax invested $810 million in various fixed income instruments (with an average yield of 8.6%) and $25 million in equity (50% ownership position). We got an update today on how this investment has been performing for Fairfax YTD. Wade Burton, CIO and VP of Hamblin Watsa on the Fairfax conference call today: “It’s early days in the timeshare investment, Berkeley, run by Caroline Shin, but so far, it has exceeded expectations. Berkeley has approximately 125,000 available room nights per month. They started the year at virtually nil occupancy for overnight stays. In month one, Caroline brought that number to 10%, the next month 20%, and the third month 35%. I’m happy to report year to date operating income has already reached our full year expectations. Again, outstanding and capable partners doing an excellent job for Fairfax shareholders.” 5.) Fairfax telegraphed how it will continue to grow its P/C insurance business - even as the hard market slows Minority interests own stakes in Fairfax’s two largest P/C insurance companies: Allied World = 16.6% Odyssey Re = 9.9% As a result, not all of the earnings from these two companies are accruing to Fairfax common shareholders. Taking out the minority shareholders will be an easy way for Fairfax to grow its P/C insurance business - it will boost the total amount of earnings that accrue to its common shareholders. On the Q2 conference call Fairfax confirmed that it would like to take out its minority partners in its two insurance businesses. They will likely to this in two steps: Allied World later this year (my best guess) and Odyssey in 2026 (or perhaps 2027). The timing will likely be determined by the opportunity set that exists in financial markets in general. If a better capital allocation opportunity comes along, perhaps they will delay taking out minority partners. Because of the call option feature (put in place when the deals were initially struck), Fairfax is able to buy out the minority partners at a very favourable price. As a result, these transactions are high certainty, solid return uses of capital for Fairfax. Taking out minority partners will be a way for Fairfax to grow its bottom line (the part that accrues to its common shareholders) even if the hard market slows further in the coming years. Brilliant planning and execution on the part of Fairfax. 6.) Economic results are much better than accounting results Excess of fair value over carrying value for associate and consolidated holdings increased from $1.4 billion to $2.4 billion, or $111/FFH share (pre-tax). The increase in the quarter was $1 billion, or $46/share pre-tax. This amount is not captured in Fairfax’s reported results (EPS, BV or ROE). This puts the economic value created by Fairfax in Q2 at about $97 share (EPS of $62 plus excess of FV over CV of $35). 7.) Fairfax is exceptionally well positioned today With $3 billion in cash to the holding company, Fairfax is all cashed up. The insurance subs are also overcapitalized (by about $3 billion) - with the hard market slowing, this is another chunk of money that could be sent as a dividend to Fairfax to be redeployed elsewhere. Fairfax is also generating about $1 billion in earnings each quarter. Fairfax has built an earnings juggernaut. Importantly, it is just getting started. Compounding is just starting to kick in… This is resulting in exponential growth. This is very hard for investors to grasp (humans think linearly). This will likely cause investors to underestimate future earnings - and that is what we have seen in each of the past 4 years (like a dog chasing its tail, earnings estimates for Fairfax have consistently been too low and subsequently keep getting revised higher). Fairfax has spent the last 39 years building out its investment management business. It has an amazing range of internal capabilities. This will allow the company to be very nimble and opportunistic moving forward. At the same time, Fairfax has developed a large number of relationships with external capital allocators. Fairfax is viewed as being trustworthy and desirable partner. This is resulting in deal flow - Fairfax’s phone is ringing. Volatility is back. Interest rates have normalized. The macro environment is highly uncertain (tariffs being just one factor). Volatility is a wonderful thing for a value investor like Fairfax - it gives them the opportunity to deploy capital at very attractive rates of return. And Fairfax is on a ‘hot streak’ (a reference to Stanley Druckenmiller). For the past 5 years the team at Fairfax has been executing exceptionally well. ‘They are seeing the ball really well…’

-

Two quick things that jumped out to me: Interest and dividend income Came in at $666 million. Is that the new run rate? Or was there a big one time payment in Q2. It was $606 million in Q1. That is a very big change quarter over quarter. Operating Income from non-insurance consolidated companies (Recipe, Sleep Country, Peak Achievement, Meadow Foods, Dexterra, AGT etc) Came in at $126 million for the quarter. Is that a ‘normalized’ run rate? If so, that would put this income stream at $500 million on an annual basis. Is the wait finally over? For the past two years, when it comes to this bucket of earnings, it has felt like Charlie Brown continuously getting the football pulled away by Lucy…

-

When I worked for Kraft and Saputo I was always pretty good at forecasting. The key was understanding the big movers. The important thing wasn’t to get all the big movers exactly right (that is impossible). It was more important to be thoughtful about the build for each of the big movers (understanding the important puts and takes for each). Forecasts for some big movers will end up being too high. But others will end up being too low. Collectively the final number often comes in (at the end of the year) being pretty accurate. Of course, to do this you have to understand your business. (And of course, it also helps to be a little lucky )

-

Fairfax's Q2, 2025 earnings results are in... diluted EPS came in at $61.61/share. I would have to give the 'mob' at Corner of Berkshire and Fairfax a solid A- for their collective forecast (I am ignoring the +$100 votes because I think some of these included excess of FV over CV). Those who voted '$50 to $59' were super close. And those who voted '$60 to $69' hit the bulls-eye. Overall, it looks to me like this crowd is not mad... actually pretty rational. Well done! And thanks for participating and commenting.

-

Great quarter. Pretty much what we were expecting (I think). Like every quarter, yes, there were some puts and takes. Bottom line, great start to the year. Hopefully we get some good questions on the conference call in the morning.

-

Fairfax holds the FFH-TRS position as an investment. As such, my guess is they will hold the position as long as they continue to see it as a good investment. They still hold the position so I think we can conclude they think their stock remains undervalued at its current price. I think you have to answer the ‘what is Fairfax worth’ question first… to have a strong opinion on whether they should exit the position. If you think Fairfax is fairly valued today then I understand the desire to see them exit the position (i.e. they are not being compensated for the risk).

-

Below is a primer on a few of the things i will be watching for when Fairfax reports Q2 earnings. I think it will be a good quarter. The question is how good. We should also get an additional kicker to the growth in BV from the weak US$ (via comprehensive income). Anything missing from my list? 1.) P/C Insurance What is growth in net premiums written? (In Q1, 2025, GPW grew 5% and NPW grew 8.4%) What is CR? (93.9% in Q2 2024) What is level of net favourable PY reserve development? (Was 2.2% in Q2, 2024 and 3.4% in Q1, 2025) Commentary on hard market? Update on Ki? Growth? First year as stand alone company. What is the 6 month CR? (Was 93.7% in 2024) 2.) Interest and dividend income How does it compare to Q1? ($606.5 million in Q1, 2025) What is average yield of fixed income portfolio? (5.1% on Q1 call) What is average duration? (3.3 years on Q1 call) 3.) What is share of profit of associates? Eurobank? Poseidon? 4.) Non-insurance consolidated holdings? (Was -$41 million in Q1, 2025) $100 million in Q2? 5.) Investment gains (realized and unrealized)? Equities? (How close is my $784 million estimate?) My estimate does not include Digit (the piece that is mark to market) and IIFL Finance (a mark to market holding in Fairfax India), both pf which were up significantly in Q2 (Digit +20% and IIFL Finance +45%). Fixed income? (Bond yields were a little lower so there will likely be a small unrealized gain here.) Any changes to construction of bond portfolio? Rough estimate of change in value of equity portfolio in Q2 Q2 change in US Treasury rates 6.) IFRS 17 impact of change in interest rates How big is unrealized gain in bond portfolio How big is unrealized loss in insurance liabilities driven by IFRS 17? What is net impact? (My guess is a small gain). 7.) Tax rate? Guidance for year? (I am using 24% in my earnings model) 8.) Share buybacks (21.58 million at March 31, 2025) My guess is little in the way of buybacks in Q2. 9.) Diluted earnings per share? (My back of the napkin number is US$65/share) 10.) Book value per share? ($1,080.38 at March 31, 2025) What was impact of weak US$? 11.) Excess of FV over CV for associate and consolidated holdings? This was $1.4 billion at March 31, 2025 ($65/FFH share pre-tax). My estimate an increase of $1 billion ($46/share) to $2.4 billion. ($1.2 billion from above less adjustments for share of profit of associates and earnings of consolidated holdings and dividends paid to Fairfax.) Eurobank is the 800 pound gorilla. Does Fairfax have any plans to monetize the significant value that is building? Adding diluted EPS ($65) and change in excess of FV over CV ($35 after tax) and we could see economic value increasing by +$100/share in Q2. 12.) Miscellaneous items: Size of investment portfolio? ($65.2 billion at March 31, 2025) Any adverse reserve development in runoff? Any change to FFH-TRS position size? Any commentary on Praktiker sale? Size of investment gain to come in Q3? Any commentary on Recipe? (Takeout of minority partner in Q1, takeout of Keg Royalties Income Fund (pending) and purchase of Olive Garden Canada in Q3.) Big holding… lots going on. Capital allocation: Any change to priorities moving forward? Fairfax raised $900 million in debt in May. What was it used for? Update on buying back some of the outstanding minority interest at Allied World and Odyssey?

-

As we wait for Q2 results, here is @nwoodman’s excellent summary from the Q1 earnings call.

-

@bluedevil, great post. I think private companies are going to have a big advantage over public companies in navigating the disruption that is coming from AI. In this regard, I view Fairfax as a private company (given Prem has control). Fairfax is being run for the long term - so they should be all over AI (and focussed on doing whatever it takes to be one of the winners). What they are doing with Digit (they completely disrupted their P/C insurance business in India back in 2017) and more recent Ki (at Lloyds) are perhaps informative in this regard. Public companies that need to hit quarterly earnings are likely going to have a much harder time making the necessary investments - that likely will not pay off for years. Fairfax has also been aggressively growing out their non-insurance consolidated businesses in recent years (Recipe, Grivalia Hospitality, Sleep Country, Meadow Foods, Peak Achievement). My guess is the primary reason for this is because the hard market is slowing so capital is being shifted to investments. This is also has the effect of diversifying the company away from P/C insurance (diversifying its income streams). It will be interesting to see if this continues. Regardless, Fairfax has two businesses: P/C insurance and investment management. They can pivot more to investment management if P/C insurance gets nuts (i.e. shift capital). P/C competitors don't have this option. I also think the fact they are slowly transitioning to a younger leadership group will help (i.e. Peter Clarke, Wade Burton, Amy Sherk, Brian Young, Ben Watsa etc). And on the employee thing... keeping your stars is the name of the game for any company/industry. One of Fairfax's big strengths is employee retention. And you see it playing out in recent years with succession planning (the next generation is slowly getting more responsibility). AI may make this strength of Fairfax's even stronger (the result being they become even more of a magnet for those who want to build a career in the P/C industry). Super interesting topic!

-

@73 Reds, I think AI is going to be revolutionary. I think the next 20 years is going to be wild. Look at Microsoft... revenue growth high teens and employee count is shrinking. In another couple of years, that is going to be the story at many mid-size companies. I am very optimistic - society will be much better off. But there will be big winners and losers. Let's hope we learned something when all the manufacturing jobs went to Mexico, China and ROW (in terms of helping workers transition to new jobs).

-

@73 Reds, Sorry, I was not clear. I have held BRK at different times over the years as kind of a bond substitute. I like the stability of the company… and, to your point, I also like the much higher return (over time).

-

@Hamburg Investor, I agree AI is a big deal. It is going to boost margins for a lot of companies. This could lead to a stock market melt-up. And it is going to disrupt a lot of industries - so it will be important to monitor. I think it might really impact the generation just graduating (and younger). Lots of occupations are going to shrink in size (i.e. computer programmers). It is going to require lots of flexibility/toggling/retraining on the part of many younger people. I have started talking to my three kids about AI and the importance of embracing it at work (and home). It is going to be more important that ever that young people build a good sized emergency fund (to be able to absorb an unexpected job change/retraining). I was also going to wind down the kids group RESP when my youngest graduated… and have since decided to keep it open and to start grow its value again (so if they decide to go back to school they can pull $ out of the RESP and it is taxed in their hands - at a low level if they are not working full time). Interesting times - as usual!

-

I have always viewed BRK as kind of like a bond substitute.

-

@73 Reds, I have recently initiated a starter position in BRK, given the sell off with Buffett announcing his retirement. I think @Gregmal said recently that BRK might do better post Buffett (with Abel not constrained like Buffett was). I think that logic makes some sense. I also initiated a small position in Chubb. Channelling Shelby Davis and happy to own P/C insurers… (Of course, Fairfax continues to be a monster position for me). On BRK, I think one of the keys moving forward is for Abel to find a way to shrink the size of the company (over time). And to pay a dividend - if Buffett wasn’t able to find anything good and really big to invest in for years… well, Abel probably won’t either.