Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

@Hamburg Investor, I think the key to FHAPS is patience. (Patience is one of my weaknesses as an investor. I have to constantly beat back my impatient/impetuous inclinations with a big stick.) Unlike BRK, Fairfax actively looks to monetize assets. But they are opportunistic when they do this - it will happen at the right time. Eurobank is the 800lb gorilla. But it is poised to deliver mid to high teens ROTBV the next couple of years. It would be silly today to sell it down to below 20% ownership to be able to mark the position to current MV. Bottom line, the value that is building will get surfaced by Fairfax. There is a big benefit to Fairfax’s equity book being so skewed to associate and private holdings. For fun, let’s remove two items from the mark-to-market bucket: Private equity/parnership holdings like BDT and Shaw Kwei = $2.2 billion FFH TRS = $3.2 billion This reduces the mark-to-market bucket from $12.4 to $7 billion. At June 30, the value of Fairfax’s equity portfolio was about $25 billion. This means only about 28% of Fairfax’s total equity portfolio is driven by quarterly changes in equity markets (Mr. Market). This should make changes in MV much less volatile moving forward. As investors come to understand this, perhaps they reward Fairfax with a slightly higher multiple. ————— I think it is reasonable to remove the FFH-TRS from the calculation because Fairfax has some control over this - via stock buybacks. If we got a large drawdown in Fairfax’s share price (of 15 to 20%) I would expect Fairfax to count their lucky stars and be very aggressive with share buy backs. Today, a selloff in Fairfax’s share price would likely be a gift.

-

@SafetyinNumbers, I just finished listening to it. I learn something new every time I listen to you. I appreciate the deep dives - very insightful. Thanks for doing these! PS: Yes, Anthony is a very good host.

-

@Haryana, below is commentary on the tax rate from the Q3, 2024 Q&A on the confernece call. To your point, hopefully we get an update on the call on Friday of what average tax rate (range) to use moving forward. ---------- Fairfax’s tax rate has ticked higher in 2024. Where Fairfax’s new ‘normalized’ tax rate settles once all the dust has settled will be something to monitor moving forward. -------------- Comments from Fairfax’s Q3 2024 conference call: Question: Tom MacKinnon A question with respect to the tax rate - you know, it used to track kind of in the low 20s, maybe, and now it’s been sort of closer to 25%. How should we be thinking about that going forward? Answer: Peter Clarke Hey, thanks for the question, Tom. Yes, the tax rate is elevated in the quarter, and there’s a lot of things going on, as you might know, on the tax side; but why don’t I pass it to Jen, who can give us a little more detail? Answer: Jennifer Allen Yes, thanks Tom. As Peter indicated, there are a lot of moving parts within the global tax regime. As you indicated, our effective tax rate is sitting at 25.1%, elevated over 2023. A couple things driving that - in 2024, we now are under the global minimum tax, where there is a 15% mandated tax in certain jurisdictions that we didn’t have prior, primarily being in Bermuda, so on a YTD basis included in that number is about $107 million, about $30 million expense in the quarter. We also have a change in the tax rate legislation in India, where they changed their long-term capital gains rate - that also cost us another about $50 million in the quarter. There’s a couple of other things we’re still closely watching, which is the interest limitation tax rule that’s in place - currently no impact materially on our financials, but there could be, that’s where the 30% limitation rule could come into play at the holding company, and then we’re still tracking quite closely the capital gains rate, the inclusion rate change that’s coming in Canada as well, so as Peter indicated, a lot of moving parts on tax. I think trying to normalize what that effective tax rate would be is a little difficult, but I would say it is going to be elevated from prior year. If you kind of put in maybe a 22% to a 25%, you’re probably going to be in the ballpark where we’ll land.

-

@73 Reds, I always liked the FFH-TRS investment. I loved it when operating earnings began spiking in 2022. To your point, that is when Fairfax had the cash to be very aggressive with buybacks - that kind of put them in control of their share price (they could buy back aggressively on any weakness). That is why I am ok with the size of the position today. They know what the company is worth more than I do. If they like it as an investment that works for me.

-

I agree. In 2020 Fairfax was yelling from the rooftops that their shares were historically cheap. That was the year Prem backed up the truck and bought $150 million in shares at a little more than $300/share. They did repurchase 344,000 shares for cancellation at $293/share. They purchased another 458,000 shares for Treasury at $301/share. But they were short on cash. What to do? Get exposure to 1.96 million more shares at $373/share (late 2020 and early 2021). At the end of 2020 there were 26.2 million shares outstanding to this represented 7.5% of shares outstanding. It is easy today to look back and understand and appreciate what Fairfax has done with the FFH-TRS. But back when they announced it - well, analysts were gobsmacked. They didn’t know what to think about the position or Fairfax for putting it on. It was a complete shocker. And that was because what Fairfax had done was a first in P/C insurance - it had never been done before. And the size of the position was very audacious. I think the brilliance of this investment was the certainty factor. Buffett says certainty is the most important input to the investment decision. And Fairfax knew with 100% certainty that their business was being criminally undervalued - especially the insurance part of the business which had doubled in size (from acquisitions) and was a year into the hard market. They had much better information than everyone else (obviously). The FFH-TRS has increased in value by about $2.7 billion in 4.5 years (before carrying costs/dividends paid). What is the ROIC from this investment? Does anyone know how to calculate it? I don’t. Fairfax is in a league of their own when it comes to the FFH-TRS position. The investment and the size of the position was unique. It was the same thing with the positioning of the fixed income portfolio in late 2021 when they sold all their corporate bonds (at yields below 1%) and took the average duration to 1.2 years. This positioning saved the company +$3 billion (probably more) in what would have been unrealized losses (and would have severely hit book value). Buffett was the only other peer thinking the same way (fixed income was in a historical bubble). Both Buffett and Fairfax knew with a high level of certainty that the US 10 year trading at 0.70% was nuts. It was the same thing with the Dutch auction when Fairfax bought back 2 million shares at $500/share. When it was still short on cash (capital was going to the insurance subs to grow in the hard market). What to do? Get $900 million from the large Canadian pension funds. Back to the certainty thing. Fairfax saw that the hard market in insurance had legs. And they probably started to sniff out the beginnings of inflation. Back to that certainty thing… at $500, they knew Fairfax was still being significantly undervalued. No other P/C insurance company is doing these things. (If some are please let me know who and what it was they did/are doing.) The logic. The creativity. The size. The execution. The results.

-

How do you think about position size (for individual stocks)?

Viking replied to Viking's topic in General Discussion

-

How do you think about position size (for individual stocks)?

Viking replied to Viking's topic in General Discussion

@MMM20’s response to @gfp’s quote above -

@gfp, I have spent a great deal of time thinking about position size (for individual stocks) - especially the past 2 years. And it probably is topical for a lot of board members today, given the incredible run we are having with Fairfax. Position size is a multi-layered topic. Very situational.   I would love to hear from other board members. How are you thinking about position size (for individual stocks)? I have always been comfortable having a very concentrated stock portfolio. There have been times in the past where I have been 100% in one stock. Fortunately, I never blew myself up. Was that skill or luck? It certainly was some combination of the two - and of course, impossible to know. Bottom line, I am at a stage in my life today where I now have enough. And probably a little extra. As a result, I am now able to (thoughtfully) help out the next generation (and extended family members) - education/mentoring/permanent savings. Growing my wealth from here is probably not going to benefit me all that much… but it would certainly have an impact on the next generation (and that is a whole other discussion). The following quote really hit me hard about 2 years ago: “Never risk what you have and need for what we don’t have and don’t need.” Warren Buffett It has impacted my views on position size (of an individual stock). Of course, there is a lot of other factors at play (like my age, life situation etc). I’ll share more of my thinking in a future post. For now, I would love to hear from other board members.

-

I don’t think there is a price (where Prem would sell to BRK). 1.) When you already have more money than you (or your future generations) will ever need what does more money get you? Nothing. 2.) Control. Prem is an entrepreneur - control is EVERYTHING. And he certainly could not want to tie Ben’s hands in the future (by giving up control of the company). 3.) Where each company is in their life cycle. In important respects, it can be argued that Fairfax is just entering its prime. It is the perfect size (not too small amd certainly not too big). The next 10 years could be magic - in terms of compounding. Selling now would be idiotic. BRK, on the other hand, is an aging elephant (managed like a giant trust on behalf of the many families who have built fortunes being invested in BRK the past 60 years). 4.) Patriotism. Prem is a proud Canadian. He would not be interested in selling out to an American company - especially in today’s environment. Fairfax and BRK are vastly different companies today, at very different stages in their life cycles and on very different trajectories.

-

@Hamburg Investor, yes, I agree. My view is an enormous amount of economic value has been building in the equity holdings over the past 5 years that is not being captured in the accounting results. 1.) Excess of FV over CV is the obvious example. It was -$660 million at Dec 31, 2020. At March 31, 2025, it was $1.4 billion. My guess is it could increase $1 billion in Q2 to $2.4 billion ($110/share), or an increase of $3.06 billion in 4.5 years = an increase of $680 million per year. 2.) Fairfax India is captured at Fairfax India’s stock price. Trading at $20 this has increased quite a bit in recent years. This is still below book value. And book value is way low, IMHO. I think BIAL is worth much more than the value it is currently carried at in Fairfax India’s book value. 3.) The consolidated equity holdings have been ‘under earning’ for years. My guess is they are performing just fine… it is just being masked in the reported results (and carrying value). 4.) Ki Insurance, while not an equity, is another holding to watch. The really interesting thing is this is a bunch of value that has already been created. And it will recognized in the coming years - Fairfax has a long history of finding ways to surface/communicate hidden value. It is like Fairfax has an off balance sheet item with $3.5 or $4 billion sitting in it today. It is growing each year. We just don’t know when they will harvest the gains. When they do it will come as a surprise (to most observers). Who could have known? This will boost ROE as it gets harvested (analysts don’t generally build it into their estimates). Two good recent examples are Sigma (in Q1) and Prakiter (in July). With Sigma, Fairfax booked a $179 million gain. My guess is Praktiker might deliver a realized gain in the $100 million range in Q3… and I am not sure it was very profitable (from an accounting perspective) while Fairfax owed it. I think it was focussed on market position/growth not reported profits. But this is just a guess on my part (I don’t want to sound like I have gone off the deep end to the accountants on the board). Almost nobody was expecting these kinds of gains from Sigma and Praktiker - including me (although I suspect @glider3834 was on to Sigma). The 800 pound gorilla is Eurobank. The excess of FV over CV is going to balloon in size in Q2. It could easily keep growing by $500 to $750 million each of the next couple of years. My guess is Fairfax is going to sit tight with this holdings for at least the next year or two. There is likely too much torque to the upside (fundamentals) to sell a big chunk now.

-

My estimate is diluted EPS for Q2 will come in around $65/share. I am not sure how to model all the different impacts from IFRS, so how this shakes out will impact my number. Here are a few assumptions that went into my estimate: Underwriting income = $380 million (CR = 95%) Interest and dividends: $605 million Share of profit of associates = $240 million Non-insurance consolidated companies = $75 million Investment gains (realized and unrealized) = $1.2 billion (stocks, bonds, Digit, IIFL Finance). I have tried to net out the impact of interest rates on the bond portfolio and IFRS. Interest Expense = $196 million Corporate Expense = $110 million Tax rate = 24% (I hope we get an update from Fairfax on the call of what this should be moving forward). I am watching for any adverse development in runoff (I think this is running at around $200 to $250 million per year). I built in $50 million to my estimate above. Excess of fair value over carrying value might increase by +$1 billion in Q2 = $45/share (pre-tax) or about $35/share after tax. I continue to believe a significant amount of value (over what is being reported in accounting results) is also building in the equity holdings that are private. The most recent examples are the sales of Sigma in Q1 and Praktiker in July. The sale of Praktiker might net an investment gain of $100 million when Fairfax reports Q3 results. When I weave it all together my guess is economic value increased at Fairfax by well over $100/share in Q2. Outstanding. What is interesting is my $65/share estimate is likely close to the average of those who voted. Thanks to everyone for chiming in. It was interesting/insightful to read the logic that others were using. And to be clear - I hope I am way off with my estimate - and those who voted for $100/share are proven correct!

-

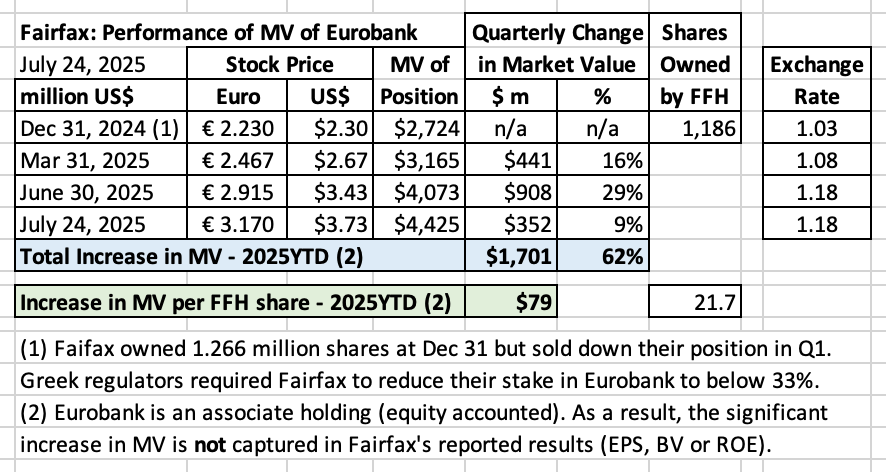

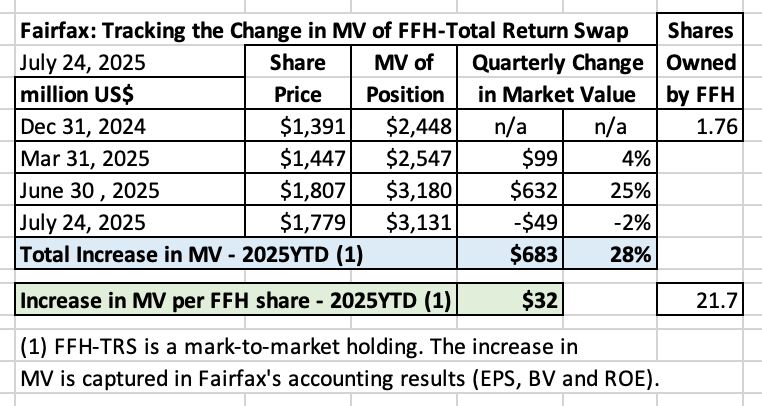

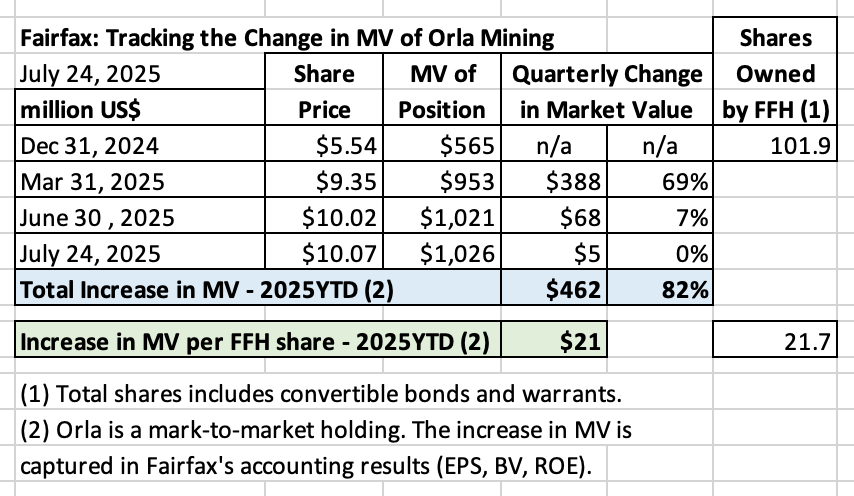

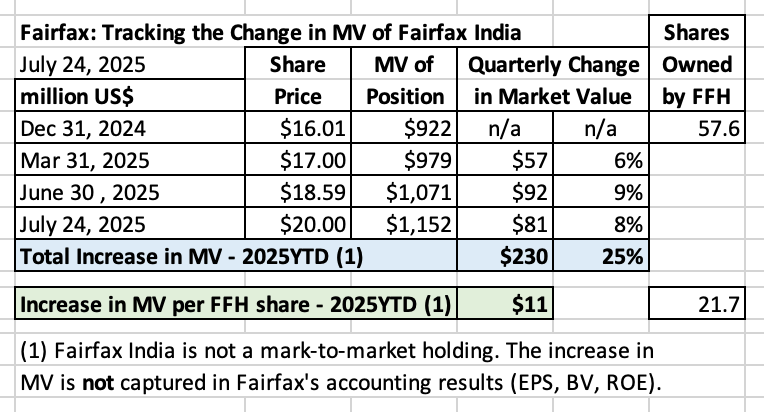

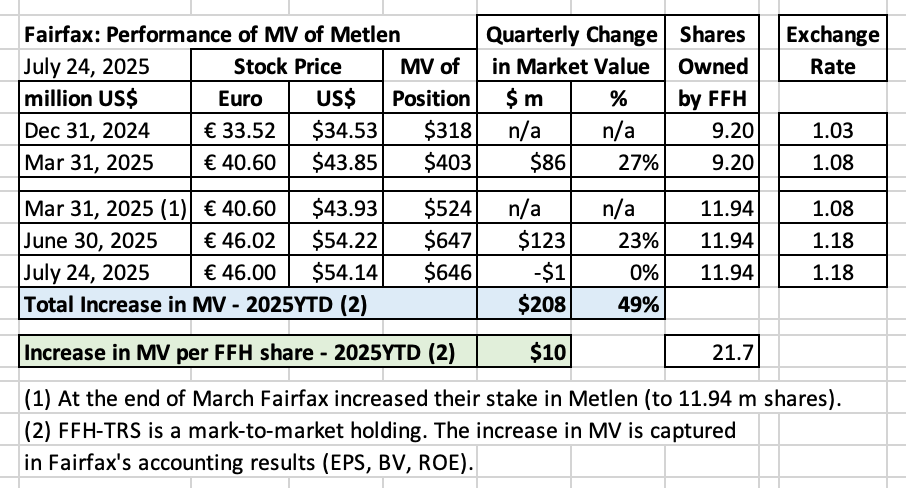

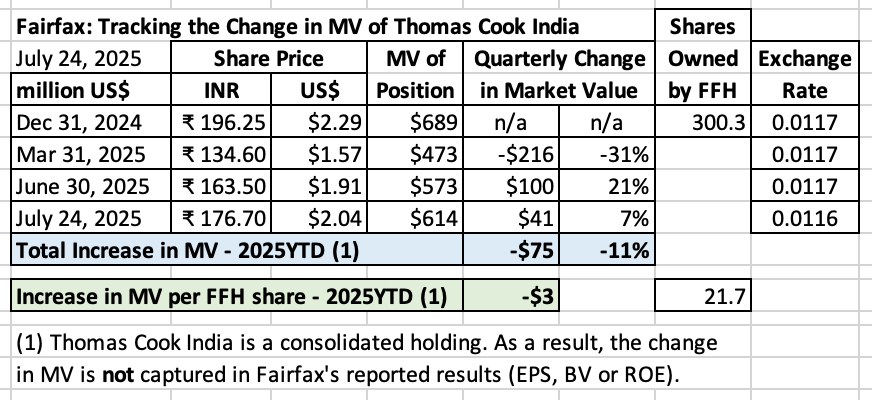

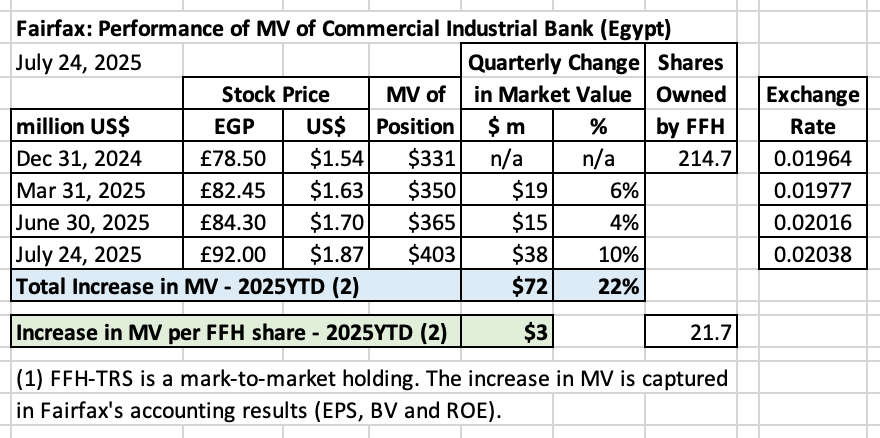

How are Fairfax’s equity holdings performing YTD in 2025? The value of Fairfax’s equity portfolio is about $26 billion. About 50% of Fairfax’s equity portfolio are private holdings ($13 billion). We don’t have a lot of visibility with these holdings. About 50% of Fairfax’s equity portfolio are publicly traded holdings ($13 billion). Therefore, we have much more visibility with these holdings. Among other things, we can track the changes in market value of the individual holdings. In this post we will look at Fairfax’s largest publicly traded holdings to see what we can learn. What holdings will we look at? To keep our analysis somewhat top-line, we will only look at holdings where the market value of Fairfax’s stake is more than $300 million. Holdings with a MV below $300 million are quite small - representing 1% or less of Fairfax’s total equity portfolio. Holdings this small are not material to the analysis we are performing today. Fairfax has 8 holdings that are publicly traded that have a market cap over $300 million. We will review them all (not just the winners) so we get a complete picture of how this basket of holdings is performing. Eurobank - EUROB.AT FFH-Total Return Swap - FFH.TO, FRFHF Orla Mining - OLA.TO, ORLA Fairfax India - FIH-U.TO Metlen Energy and Metals - MYTIL.AT Thomas Cook India - THOMASCOOK.BO Commercial Industrial Bank (Egypt) John Keells (Sri Lanka) We will look at the year-to-date performance of each holding. We will break it out by quarter - this will help us understand what might be coming when Fairfax reports Q2 results. And it will also give us some insight into how Q3 is looking (about 3 weeks in). At the end of our post, we will summarize the results. A note on volatility Yes, equities are very volatile. The market value of individual stocks can swing dramatically (often 40%) in any given year. Looking at stocks over a 7 month period (like I am doing) should be done with an appropriate amount of scepticism. Why do it? Because it provides an interesting data point. And a bunch of data points - when put together - can start to paint a picture. Let’s get started. ————— 1.) Eurobank - EUROB.AT Eurobank is - by far - Fairfax’s largest equity holding (public or private). YTD-2025, the market value of Fairfax’s position in Eurobank is up $1.7b, or 62%, or $79 per Fairfax share (pre-tax). Yes, that is exceptional performance. The management team at Eurobank continues to execute very well. The Greek economy continues to perform well. Greek banks are also getting re-rated higher, moving their valuations closer to European banking peers. Weak US$ has also been a tailwind in 2025. Eurobank is an associate holding (equity accounted) so the significant YTD gain in market value is not being captured in Fairfax’s accounting results (EPS, BV or ROE). ————— 2.) Fairfax - Total Return Swap - FFH.TO, FRFHF FFH-TRS is - by far - Fairfax’s 2nd largest equity holding (public or private). YTD-2025, the market value of Fairfax’s position in FFH-TRS is up $683 million, or 28%, or $32 per Fairfax share (pre-tax). Yes, that is exceptional performance. Fairfax continues to perform very well. At the same time, the stock is also getting re-rated higher, moving its valuation closer to P/C insurance peers. FFH-TRS is a mark-to-market holding so the significant YTD gain in market value will be captured in Fairfax’s accounting results (EPS, BV or ROE). —————— 3.) Orla Mining - OLA.TO, ORLA Fairfax’s 3rd largest publicly traded equity holding is Orla (a gold miner). YTD-2025, the market value of Fairfax’s position in Orla is up $462 million, or 82%, or $21 per Fairfax share (pre-tax). What is causing the strong performance? Gold is viewed as being a hedge against two things: uncertainty and inflation. Gold appears to be in a bull market. Orla announced today that it was experiencing some challenges at its Camino Rojo property (which caused the stock to sell off). This is a good reminder of the volatility that comes with owning equities, especially commodity companies. Orla is a mark-to-market holding so the YTD gain in market value will captured in Fairfax’s accounting results (EPS, BV or ROE). —————— 4.) Fairfax India - FIH-U.TO Fairfax’s 4th largest publicly traded equity holding is Fairfax India. YTD-2025, the market value of Fairfax’s position in Fairfax India is up $230 million, or 25%, or $11 per Fairfax share (pre-tax). That is solid performance. Fairfax India’s biggest holding - by far - is Bangalore International Airport (BIAL), the third largest airport in India (they own 74% of the trophy asset). India is expected to be the top performing major economy over next decade. Fairfax India is not a mark-to-market holding so the YTD gain in market value will not be captured in Fairfax’s accounting results (EPS, BV or ROE). —————— 5.) Metlen Energy and Metals - MYTIL.AT Fairfax’s 5th largest publicly traded equity holding is Metlen Energy and Metals. YTD-2025, the market value of Fairfax’s position in Metlen is up about $208 million, or 49%, or $10 per Fairfax share (pre-tax). Yes, that is exceptional performance. There are lots of tailwinds for the company. The stock will likely begin trading on LSE on Aug 4. Weak US$ is also a tailwind for the stock. Metlen is a mark-to-market holding so the YTD gain in market value will be captured in Fairfax’s accounting results (EPS, BV or ROE). —————— 6.) Thomas Cook India - THOMASCOOK.BO Fairfax’s 6th largest publicly traded equity holding is Thomas Cook India (TCI). YTD-2025, the market value of Fairfax’s stake in TCI is down $75 million. Indian stocks sold off quite a bit in Q1. Since then, TCI has rebounded strongly - the stock was up in Q2 and it is up again in July. TCI is a consolidated holding so the decline in market value is not captured in Fairfax’s accounting results (EPS, BV or ROE). —————- 7.) Commercial Industrial Bank (Egypt) Fairfax’s 7th largest publicly traded equity holding is Commercial Industrial Bank (CIB), an Egyptian bank. YTD-2025, the market value of Fairfax’s position in CIB is up $72 million, or 22%, or $3 per Fairfax share (pre-tax). CIB is a mark-to-market holding so the YTD gain in market value will be captured in Fairfax’s accounting results (EPS, BV or ROE). —————— 8.) John Keells (Sri Lanka) Fairfax’s 8th largest publicly traded equity holding is John Keells (JKL), a large conglomerate located in Sri Lanka. YTD-2025, the market value of Fairfax’s position in JKL is up $26 million, or 8%, or $1 per Fairfax share (pre-tax). JKL is an associate holding (equity accounted) so the YTD gain in market value is not being captured in Fairfax’s accounting results (EPS, BV or ROE). —————— How are Fairfax’s largest publicly traded equities performing YTD 2025? In summary, Fairfax’s 8 largest publicly traded equities are performing very well. YTD-2025, in aggregate, they have increased in market value by $3.3 billion, or 39%, or $153 per Fairfax share (pretax). Our analysis does not include 55% of Fairfax’s equity holdings YTD-2025, Fairfax’s total equity portfolio has increased in value by much more than $3.3 billion. At July 22, 2025, Fairfax’s total equity portfolio was about $26 billion. The market value of the 8 companies included in our analysis above is about $11.8 billion, or 45% of the total. This means our analysis does not capture any of the value creation that has been happening at the remaining 55% of the equity holdings. These are mostly private holdings - well run and well positioned companies with solid prospects. What else did we learn? Fairfax runs a concentrated portfolio. Its two largest holdings (Eurobank and FFH-TRS) continue their exceptionally strong performance (it has been the same story with these two holdings for 4 straight years). The strong performance is broad based - 6 of 8 holdings have increased in market value by 20% or more. The holdings do not look expensive. The increase in market value is not due to out-of-control speculative behaviour on the part of investors. Rather it appears to be undervaluation being corrected combined with improving fundamentals. Economic results versus accounting results The economic results being delivered by Fairfax’s equity portfolio are much higher than the accounting results. Of the total increase in market value of $3.3 billion, about $1.4 billion (44%) is mark-to-market. This increase will show up in Fairfax’s reported results (EPS, BV and ROE). The other $1.9 billion (56%), or $86 per Fairfax share (pre-tax), in value creation will not show up in Fairfax’s reported results. The gap between economic/intrinsic value and book value is widening at Fairfax (and has been for years). The quality of Fairfax’s equity portfolio is shining though Fairfax has been hard at work since about 2018 improving the quality of its total equity portfolio. 7 years later, the benefits can be seen from the consistently strong performance of the group of holdings. This bodes well for future results. The investment portfolio is tracking to deliver a strong year in 2025 Total return on the total investment portfolio (bonds and stocks) is tracking to exceed 10% in 2025. This would put the average over the past 3 years at about 9.5%. Yes, we will see some quarter to quarter volatility. But looking out a couple of years, the significant value creation is unmistakeable. Seeing the value of Fairfax’s business model Fairfax’s P/C insurance operations have never been better positioned. Fairfax’s investment management business has never been better positioned. Over the past 5 years, Fairfax’s management team has been putting on a capital allocation clinic. In turn, Fairfax has been delivering best-in-class results. At the same time, the quality and certainty of Fairfax’s earnings has never been better. We are getting to an interesting part of the P/C insurance cycle - the hard market is slowing. Fairfax is uniquely positioned. As P/C insurance slows Fairfax will be able to shift capital to its investment management business (where it has an amazing range of proven capabilities) - Fairfax will have much better reinvestment opportunities than peers. This will allow Fairfax to keep both its top-line growth steady and return on invested capital high (and likely better than peers). The exceptional YTD results being posted by its 8 largest publicly traded equity holdings (+39%) is just the latest data point showcasing Fairfax’s capabilities and the superior strength of its business model (especially compared to P/C insurance peers).

-

Orla Mining has reported an issue requiring the company to temporarily halt operations at its Camino Rojo mine. The stock is currently down 13.5%. This will be something to monitor. https://orlamining.com/news/orla-mining-reports-pit-wall-event-at-camino-rojo/ Vancouver, BC – July 23, 2025 – Orla Mining Ltd. (TSX: OLA; NYSE: ORLA) (“Orla” or the “Company”) reports that an uncontrolled material movement event occurred today on the pit wall at its Camino Rojo Oxide Mine in Zacatecas, Mexico. The event occurred along the temporary north wall of the open pit, which included ore material expected to be mined as part of the ultimate open pit. There were no injuries or equipment damage as a result of the material movement, which was detected early by the pit monitoring systems. The event was caused by significant rain. There was no environmental damage resulting from the incident; however, rainwater diversion channels will need to be re-established to prevent further material subsidence in the pit. While the main access throughout the pit was not affected, mining in the pit has been temporarily suspended. Pit access has been restricted to the necessary technical and operating personnel to support the appropriate geotechnical assessments required for safe remediation and resumption of mining activities. Crushing and stacking of stockpiled material onto the heap leach will continue in the interim. The Company is currently assessing any potential impact of the pit wall event on its full-year production guidance for Camino Rojo. The relevant authorities are being notified as appropriate, and Orla is implementing appropriate remediation measures. The safety of all personnel remains the Company’s top priority as it undertakes a comprehensive analysis to ensure the ongoing stability of mining operations.

-

Q2-2025 is shaping up to be a very good quarter for Fairfax. So let's use this as an opportunity to have a little fun. Let's see how smart the mob at 'Corner of Berkshire and Fairfax' really is. Are we a bunch of cheerleaders? Or are we living in the real world? We will have our answer after Fairfax reports results (well, at least another data point). So please make your thoughts known. Vote. And if you have thick skin, in the comment section, let us know: What diluted EPS range did you pick? What do you see as the key 3 or 4 drivers of earnings in Q2 (be as specific as possible). What are 2 or 3 things you are watching most closely when Fairfax reports (want to learn)? After Fairfax reports results, we will crown the winners (those board members who picked the correct range). I am most interested in seeing how the average compares to what Fairfax actually reports. Can someone also post what current analyst expectations are for diluted EPS for Fairfax for Q2? I will chime in with my thoughts in about a week. I want others to have a chance to get this party started ---------- Note: Of course, this does not include the change in 'excess of FV over CV' for associate and consolidated holdings. This is significant economic value that is building at Fairfax that is not being captured in accounting results.

-

@TB , I have said before that Justin Trudeau (when he was leader of the Federal Liberal party) will go down as the worst Prime Minister in modern Canadian history. One (of many) good examples was how they broke the Canada's best-in-class immigration system (it has become a mess). Part of the fail also involves international students and foreign workers. And now asylum seekers (as non-Canadians who should be leaving do everything they can to stay). The good news is steps are being taken to fix the problems. We are probably year two into the fix. It will probably be a 3 to 5-year process to climb back out of the hole. And mistakes will be made. I am confident Carney will be a much better Prime Minister than Trudeau. How much better? It is much too early to tell. ----------- In terms of Canada's issues with India, it needs to be handled through back channels. That appears to be what Carney is doing. Trudeau's preferred way of managing delicate/thorny problems was through public opinion polls/the media. US (Trump's first term). China. Saudi Arabia. India. The Middle East. etc. Needless to say, Trudeau's standing in the world was the highest when he first got elected in 2015 (even Trump liked him then) and then deteriorated every year after (hitting rock bottom in late 2024 when the Liberal's finally found a way to force him out as leader).

-

Travelers reported Q2 results today. The hard market continues to roll. Chug, chug, chug. It will be interesting to see what WRB and CB have to say. “Overall landscape is very positive.” Business insurance - holding up well. Retention - indicator of market stability. Continued strong retention rates. Tort inflation - is it an issue? “It appears everyone is pricing for it.” Interesting that Travelers decided to sell their Canadian P/C business. Reason? Canadian market is becoming concentrated and incumbents are much better positioned. So growing the business made little sense (especially given we are likely near the end of the hard market). Selling the business at 1.8 x BV to a much larger incumbent was the rational thing for Travelers to do. This suggests the big players are being very rational. Encouraging.

-

The key takeaway for me from the Praktiker news is further confirmation that Fairfax continues to execute exceptionally well with its collection of equity holdings. It really is amazing what they have been able to accomplish since about 2018. Praktiker was one of the legacy holdings (purchased before 2018) that they decided to keep. It is now being monetized for what looks like an exceptional gain. Praktiker was a consolidated holding. It is a good example of the significant value that has been building for years at Fairfax with this bucket of holdings (economic value that was not being captured in the reported accounting results). In recent years, Fairfax has significantly increased the size and number of companies in this bucket (recent additions: Recipe, Grivalia Hospitality, Sleep Country, Meadow Foods and Peak Achievement). It will be interesting to follow reported results for this group of holdings. My guess is economic value creation will continue to run ahead of the accounting results. Over time, this will provide another large and growing stream of ‘surprise’ earnings for Fairfax (when Fairfax monetizes the ‘hidden’ asset). @Crip1, you make a great point. We have stopped complaining about the equities that Fairfax owns. And now we are debating how much money they have made on their equities - is it a really big number? Or an obscenely big number? As a long term follower of the company, it is an incredible shift in the narrative (that has been slowly playing out over a couple of years). A similar shift is playing out with their P/C insurance business. In terms of narrative for Fairfax as a company, we reached maximum pessimism in 2020. In 2021 and 2022, the narrative continued to be quite negative on the company. In wasn’t until 2023 that it was ok for an investor to admit they owned Fairfax - but even then, detractors felt it was a head fake (and therefore likely a stupid idea to own the stock). In 2024, it became indisputable that Fairfax results had been transformed (and for the better). But the multiple given to the stock continued to be low (small premium to BV, but still well below peers). In 2024, the sentiment gauge for Fairfax probably got back to 5 out of 10. Half way through 2025 (today), my guess is the sentiment gauge for Fairfax is probably around 6 out of 10. Much better than it was 5 short years ago. Some optimism is building - but it is not excessive. And it is certainly not euphoric. It will be interesting to see how the next couple of years play out. It really has been - and is - a special time to own this company. For investors who made Fairfax a concentrated position in 2020, it has been like winning the lottery every year for 5-straight years - it has been a very surreal experience (for me anyways).

-

Doing a quick Google search I came across two sale/leasebacks. Not sure how many of these transactions were done/how much of the property was owned by Grivalia/Eurobank. Grivalia Properties Sept 30, 2015 Report On March 18, 2015, the Company, following the permission granted from the Annual General Shareholders Meeting held on March 17, 2015, completed the transaction relating to the acquisition of a property from Praktiker Hellas SA located in Heracleion, Crete and its immediate long term lease back to Praktiker. The acquisition price was €8.500 (excluding acquisition costs of €62). The fair value of the property as evaluated by independent valuators at the acquisition date was €8.830. It is noted that the acquisition was financed through the existing funds of the Company which originated from its 2014 Share Capital Increase. On May 19, 2015, the Company following the permission granted from the Extraordinary General Shareholders Meeting held on August 28, 2014, completed the transaction relating to the acquisition of a property from Praktiker Hellas SA located in Mandra, Western Attica and its immediate long term lease back to Praktiker. The acquisition price was €6.500 (excluding acquisition costs of €48). The fair value of the property as evaluated by independent valuators at the acquisition date was €7.905. It is noted that the acquisition was financed through the existing funds of the Company which originated from its 2014 Share Capital Increase. https://www.athexgroup.gr/en/documents/10180/43442/Financial Statement - Full Notes GRIVALIA PROPERTIES R.E.I.C. (2015%2CNine-Month Statement%2CBoth).pdf/4441ee77-b86d-4a02-93e8-8980db1984a4

-

@TB, what has me most excited about Fairfax these days is the size of earnings (and its quality/certainty), their significant reinvestment opportunities (much better than peers), and the impact of compounding over the next 5 years. I also really like who they are partnered with their equity holdings (the quality of the CEO's/founders) - and view this is another significant tailwind for economic value creation. So my thesis is very much forward looking. Back in the 1990's and 2000's the big mistake I made with Berkshire Hathaway is I was too focussed on rear view mirror metrics (like BV). So I grossly underestimated the significant value creation that kept happening year after year after year.

-

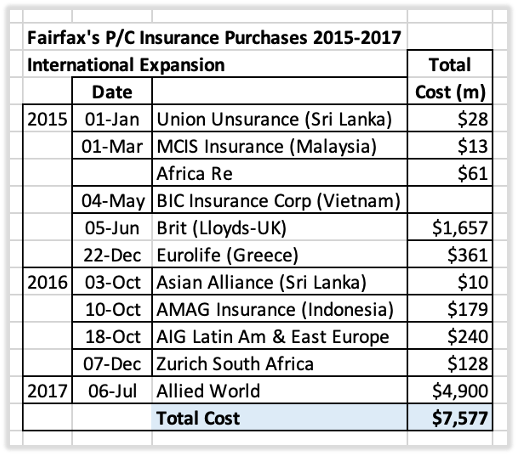

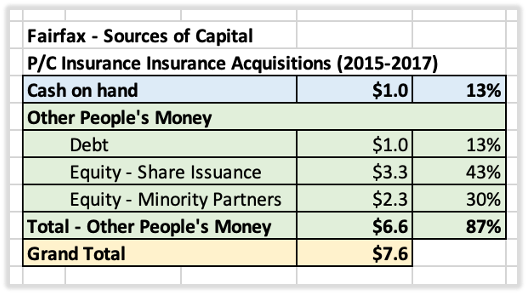

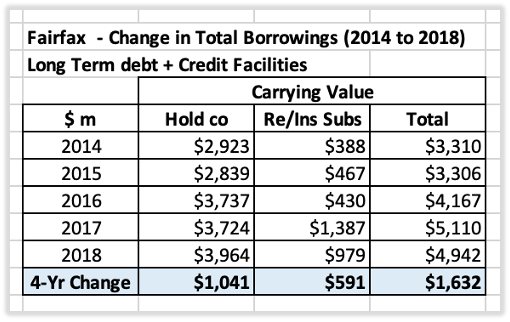

An Example: Grow P/C Insurance by Acquisition (2015-2017) – ‘Fortune Favours the Bold’ Yes, a discussion of leverage can get really theoretical. So, to help us on our quest (to learn more about the topic and Fairfax) let’s pivot and look at a real-world example. Growth by acquisition – P/C Insurance Expansion (2015-2017) From 2015 to 2017, Fairfax executed an aggressive acquisition strategy to build out its global P/C insurance footprint. At the time, PC insurance was in a soft market. As a result, top-line growth was stagnant and underwriting margins were under pressure. The investment management side of the business was also struggling - bond yields were very low. As a result, the stocks of P/C insurance companies were cheap. This was the perfect time to grow by acquisition. From 2015 to 2017, Fairfax made 11 different purchases of P/C insurance companies. The total cost was $7.6 billion. To provide context, at the end of 2014, common shareholders’ equity at Fairfax was $8.4 billion. Fairfax saw a big opportunity and they acted with conviction and backed up the truck. How did Fairfax pay for the acquisitions? This is where our story gets quite interesting. Below is a very rough estimate of how Fairfax came up with the $7.6 billion total cost. Fairfax supplied $1 billion in cash, or 13% of the total cost. Other people supplied about $6.6 billion of the total cost, or 87%. ‘Other people’s money’ came from three sources: Debt of $1 billion (held at the Fairfax level). Equity - Share issuance (Fairfax shares) of $3.3 billion. Equity - Minority partners (of the P/C insurance companies being acquired) of $2.3 billion. Fairfax used a significant amount of leverage when executing its aggressive grow by acquisition strategy. Let’s now review in a little more detail each of our leverage metrics: debt, equity and float. ———— Debt = $1 billion Fairfax needed to be careful with the amount of debt it used. It needed to keep the ratings agencies and insurance regulators happy. Holding company debt at Fairfax increased from $2.92 billion in 2014 to $3.96 billion in 2018, an increase of $1.04 billion over 4 years. What was the cost? Below are some of debt offerings Fairfax closed in 2015 and 2016: February 20, 2015 - $350 million of 4.95% senior notes due 2025. March 22, 2016 - C$400 million of 4.5% senior notes due 2023 December 16, 2016 - C$450 million of 4.7% senior notes due 2026. The increase in total debt was reasonable. And the cost was low (a blended rate of about 4.75%). ———— Equity At $5.6 billion, equity supplied the majority of the funds for Fairfax’s acquisitions. The funding from equity came from two sources: one public and one private. Equity – Share issuance (public markets) = $3.3 billion From 2015 to 2017, Fairfax issued a total of 7.25 million shares at an average price of $456/share for total proceeds of $3.3 billion. Using a familiar playbook Fairfax has a history of using equity to grow per share value for long term shareholders. Fairfax (generally) issued equity when it was trading at a premium to its intrinsic value. And it bought shares back when they were trading at a discount to its intrinsic value. But Fairfax had a problem in the 2015 to 2017 period. As we explained earlier, P/C insurance stocks in general were on sale. At the same time, Fairfax’s investment management business was underperforming. As a result, Fairfax’s shares were also on sale - trading only at a slight premium to book value. What was the cost? Fairfax’s book value at December 31, 2017 was $450/share. Fairfax issued a significant number of shares at 1 x BV. Long term Fairfax shareholders paid a high cost. This was not a good time to issue equity. So, Fairfax needed to limit the amount of its own equity that it used (the quantity of its own shares that it issued). What else could Fairfax do? What happened was classic Fairfax. They got creative. And came up with a novel solution. That is what we will explore next. ———— Equity – Minority partners (private markets) = $2.3 billion Minority partners supplied Fairfax with $2.3 billion. This was/is NOT a traditional source of capital for a P/C insurance company. Fairfax brought on minority partners for their three largest acquisitions: Brit: OMERS purchased 30%. Eurolife: OMERS purchased 40% Allied World: OMERS and CPPIB purchased 32.5% What was the cost to Fairfax? Allied World paid dividends to its minority partners in 2019, 2020 and 2021 of $126 million. This provided minority partners with an 8.0% return (using $1,560 million as the cost base). If accurate, this is a solid return for the minority partners (remember, this was a time when interest rates were very low). The cost to Fairfax was modest. By bringing on minority equity partners Fairfax was able to get access to much more capital. This allowed them to be very aggressive and maximize the size of their acquisitions. Importantly, Fairfax had complete control of all P/C insurance acquisitions - its partners were passive partners. One more thing: Call option feature When the equity deal is put in place with the minority partner it includes a call option feature. The call option gives Fairfax the right - but not the obligation - to buy out their minority partner at a specified price and by a specified date. Fairfax profits if the underlying asset increases in price. This is very important – for reasons we will explore in other posts. ———— What was the impact on float? From 2014 to 2017, total float at Fairfax increased from $15.1 to $22.7 billion, or 50%. This was a significant increase. The increase in float came primarily from the P/C insurance acquisitions. Total numbers are nice to look at. But what really matters to long term shareholders are the per share numbers: Given the high number of Fairfax shares that were issued, the per share increase in float was a much smaller 15%. And importantly, Fairfax shareholders did not own 100% of the $817/share of float. Minority partners owned big chunks of Eurolife, Brit and Allied World. So, on a per share basis, the amount of float that actually accrued to common shareholders was likely up only a small amount at December 31, 2017 (compared to December 31, 2014). Does this mean Fairfax made a big mistake with its aggressive P/C insurance acquisition campaign from 2015 to 2017? Great question. Let’s explore this next. ———— Big capital allocation decisions need to be evaluated over a 5 to 10-year time horizon. To evaluate Fairfax’s P/C insurance acquisition strategy from 2015 to 2017, let’s fast forward to December 31, 2024. How do things look 7 years later? Since 2018, Fairfax has been aggressively ‘deleveraging’ the equity part of its balance sheet. It has been buying back stock. And it has been taking out its minority partners. At the same time, Fairfax has been aggressively growing its P/C insurance business. Let’s review each of these in more detail. Equity ‘deleveraging’ part 1 – Share buybacks (effective): Before embarking on its P/C insurance expansion, shares outstanding at Fairfax was 21.2 million (Dec 31-2014). Shares outstanding peaked at 27.8 million (Dec 31-2017). At Dec 31-2024, the share count had fallen to 21.7 million. Over the past 7 years, Fairfax has been able to re-purchase almost all the shares that it issued from 2015 to 2017. But the story gets better. Fairfax was able to repurchase the shares at an average cost of $637/share. This was a crazy low average price. (And it was only a slight premium to the average issue price of $456.) Equity ‘deleveraging’ part 2: Take-out minority partners Fairfax has been slowly taking out its minority partners. As a result, at December 31, 2024, Fairfax owned: Brit = 100% Eurolife = 80% (remaining 20% is owned by Eurobank) Allied World = 83.4% My guess is Fairfax will increase its ownership stake in Allied World to 100% in the next 24 months. And because of the call option feature, Fairfax has been able to take out its minority partners at a very reasonable price (it has not had to pay a premium). ———— Let’s now pivot and look at Fairfax’s insurance business. How does it look? P/C insurance business Fairfax’s P/C insurance business has been completely transformed over the past 10 years. The transformation has happened in two phases: P/C insurance growth by acquisition (2015 to 2017) – Build out global platform. Hard market (2020 to 2024) – Grow organically. At the same time, Fairfax has been able to get effective shares outstanding back down to 2014 levels. Over the past 10 years, measured per share: NPW has increased by 304%, which is a CAGR of 15.3%. Float has increased by 198%, which is a CAGR of 11.5%. And with Fairfax taking out its minority partners, almost all of this growth has accrued to Fairfax’s long term shareholders. Summary What have we learned? In 2014, Fairfax saw a significant opportunity to grow its P/C insurance business through acquisition. To capitalize on it they did the following: Acted with conviction and sized their bet very well. They made a large number of acquisitions. They bought quality. They did not overpay. P/C insurance companies were out of favour. The acquisitions were made with a margin of safety. They were very creative with their use of leverage. Fairfax used ‘other people’s money’ to fund the majority of its purchases: a mix of debt and equity (Fairfax shares and minority partners). Using minority partners allowed Fairfax to keep total debt and new share issuance (Fairfax shares) to a reasonable level. With hindsight, Fairfax’s timing was perfect. The company had a couple of years to integrate the new businesses before the start of the hard market in late 2019. Fairfax has been able to fully exploit the historic hard market over the past 5 years. Growing organically in a hard market is the best kind of growth (it is very profitable). Ten years later, Fairfax’s P/C insurance business has been transformed. It is much larger (global), much higher quality and much more profitable. The insurance business is much more diversified and has much better growth prospects. Re/insurance float (the best kind of leverage) per share increased by 198% over the past 10 years, a CAGR of 11.5%. In turn, this has also transformed Fairfax and spiked earnings higher. A significant amount of the earnings that have been generated in recent years has been used to ‘deleverage’ the equity part of Fairfax’s balance sheet. Effective shares outstanding have been reduced back to 2014 levels – and shares were repurchased at very favourable prices. And Fairfax has begun the process of taking out its minority partners, also at very favourable prices (given all the growth that has occurred). Fairfax has been playing the long game. Their actions have been very shareholder friendly. Over the past 10 years, the per share value creation for long-term Fairfax shareholders has been enormous. Yes, some luck was involved. But as we learn from Fortuna, the Roman goddess of luck, ‘fortune favors the bold.’ ———— Addressing the elephant in the room My guess is many of you feel that it is wrong to view equity issuance (specifically share issuance and using minority partners) as a type of leverage. I do it because I think it gives an investor a slightly different and interesting way to look at equity issuance (shares, minority partners etc). Especially for firms, like Fairfax, who actively use ‘equity’ as an important part of their capital allocation framework (using it tactically - flexing it up and down in different ways over the years). Kind of like a temporary source of financing (yes, 10 years is short term for Fairfax). Please let me know your thoughts on this topic.

-

Why does it feel like I have seen this movie before? I continue to think the only way to understand what Trump is doing is to view it through the lens of a good old fashioned shakedown from the mafia.

-

Another week... time for another Eurobank update. In Q2, Fairfax's stake was up about $900 million. 10 days into Q3, it is up another $300 million. Pretty crazy. With a MV of $4.4 billion, this is becoming a monster sized position for Fairfax. It appears all Greek banks are getting re-rated higher. The weak US$ is another tailwind. Excess of FV over CV at Fairfax continues to blow out (get bigger).

-

I am not an accountant. So please feel free to correct my errors. But it looks to me like 'issue' that Fairfax is having is different from that of Berkshire Hathaway. By issue, I mean the increase in economic value that is not being captured in accounting value. For BRK, I think the 'problem' was primarily with the consolidated holdings. For Fairfax the 'problem' today is primarily with the associate holdings. (Although I think Fairfax may have an emerging 'problem' with its consolidated holdings.) The interesting things is for Fairfax we can see the size of the problem, because Fairfax reports excess of fair value over carrying value (and we can actually do the calculation ourselves). The problem Fairfax has is the CV for many of its associate holdings is criminally low. Eurobank is the poster child. But there are other examples (like Thomas Cook India and Dexterra). We can see the size of the problem for Fairfax's publicly traded companies. As their share prices rip higher, the excess of FV over CV is spiking higher. The continuous, significant value creation that has been happening for years with many of Fairfax's equity holdings has not been captured in any of the accounting results like EPS, BV or ROE. What this means is Fairfax's stellar reported results of the past 4 or 5 years are materially understated - Fairfax's economic results have been even better than the reported accounting results. It's like all of this 'hidden' value creation is getting put into a large and growing off- balance sheet bucket. Over time, Fairfax will find a way to monetize this off-balance sheet asset. Like the sale of Sigma in Q1 (a small holding for Fairfax), which resulted in a 'surprise' realized gain of $178.7 million. When this happens it will juice EPS, BV and ROE. And for Fairfax, excess of FV over CV is just one of many examples of where value is hidden. There are many others. Other P/C insurance companies do not have this same set-up (billions in value creation that has already happened but has not yet been captured in accounting results... that is just sitting there waiting to be monetized). Don't get me wrong.. I am not complaining. I love it. Fairfax today is playing like Scottie Scheffler on the PGA tour - and at the same time, with all the value that is growing/hiding on their balance sheet, it's like they are also now being given a couple of mulligans for future events (that will allow them to post better future results). It's just not fair (to the other players). Nuts.

-

So Fairfax is on track to deliver a 20% ROE in 2025. This does not include the increase of $1.1 billion in excess of FV over CV of associate and consolidated holdings. Eurobank is up quite a bit to start Q3… It looks like economic value is increasing much more than accounting value. Is Fairfax contracting BRK disease? Where BV loses its relevance as a valuation measure for investors?

-

How is Fairfax's investment in Metlen performing? Very well. Fairfax invested about $250 million, with much of the investment happening in late 2022. Today it has a MV of $650 million, an increase of $400 million (not including dividends received or interest paid on the exchangable bonds). Melten is Fairfax's 8th largest holding today. On Aug 7, 2025, Melten will IPO on the LSE (it will retain a secondary listing on the Athens exchange. Given its size (market cap) Metlen is a strong candidate to be added to FTSE100. Euro strength versus the US$ has been a strong tailwind for the MV of Fairfax's large position in Melten.