Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

@djokovic1, there is lots of really interesting stuff to talk about here. It appears one of the changes between Fairfax and Markel has been their focus over the past decade. - Fairfax’s focus has been its P/C insurance business - growth and improving its quality. - Markel’s focus appears to have been Markel Ventures. Its P/C insurance business has hit some speed bumps (and couldn’t have come at a worse time - during the hard market). As a result, it appears Fairfax believes more than ever that P/C insurance is its core business engine. This has important implications when it comes to the amount of leverage and the rates of return the company will be able to generate over the next decade. I think lots of investors (including me) focus on Fairfax’s investment management business. And don’t fully appreciate the strategic beauty of what Fairfax has accomplished with its insurance business over the past decade - and what it means for the company moving forward. This likely causes investors to underestimate Fairfax and the returns it is capable of delivering. ————— As it got older as a company, Berkshire Hathaway shifted more and more capital to its non-insurance businesses. As a result, the importance of P/C insurance shrunk dramatically over time. As Fairfax gets older as a company, it appears to be leaning into its P/C insurance business. P/C insurance is becoming more important over time.

-

2003 was a wild year for Fairfax shareholders. I added at C$70. The return for my portfolio that year was 87%. I was very lucky - at the time, I was able to lean on the knowledge of other posters on this board. The interesting thing is in 22 short years, Fairfax has completely changed as a company. Especially on the insurance side of things. I am really looking forward to reading David’s book, The Fairfax Way. I am hoping it will provide some insights (give us a better understanding) into the many changes that have been happening at the company. https://www.amazon.ca/Fairfax-Way-Inside-Lasting-Success/dp/1037802195

-

@Marco Van Basten, Buffett nailed Apple. It still didn’t matter to CAGR (even with Apple they have remained at average). The reason? The size of BRK. Yes, there are other important reasons for Berkshire’s slowing CAGR. But I continue to believe size is the main problem. It likely isn’t going to get any easier.

-

@Maverick47, I appreciate the comment. More than anything, the purpose of my post was to serve as a thought exercise - at a very high level - to stimulate thinking on an important topic (buying back stock). My original post was going to be “Is a persistently low stock price a good thing for Fairfax?” As you can see, it changed quite a bit (got turned on its head). Another reason buybacks are such an important topic for Fairfax is I think there is a good chance the shares could remain on sale for years (for a whole bunch of reasons). By on sale, I mean trade below intrinsic value (and well below at times). If this happens, its not crazy to think they could continue to take out 4 to 5% of shares outstanding each year over the next couple of years. IMHO, that would be a great thing for the company (and long term shareholders). Their share count (effective) is back to where it was before they went on their big P/C insurance global expansion (2015-2017). The other interesting thing is they are currently generating so much excess capital they still have lots left over after buybacks to continue to drive the top line growth (including taking out their minority partners in P/C insurance).

-

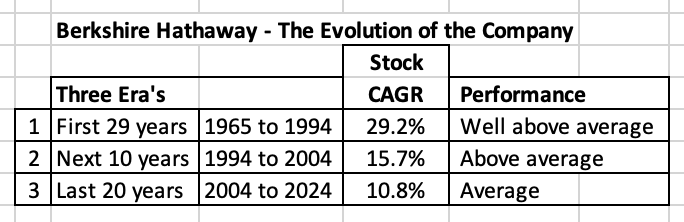

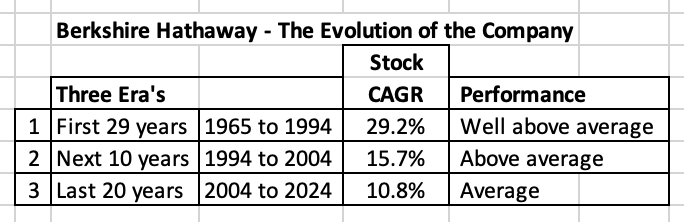

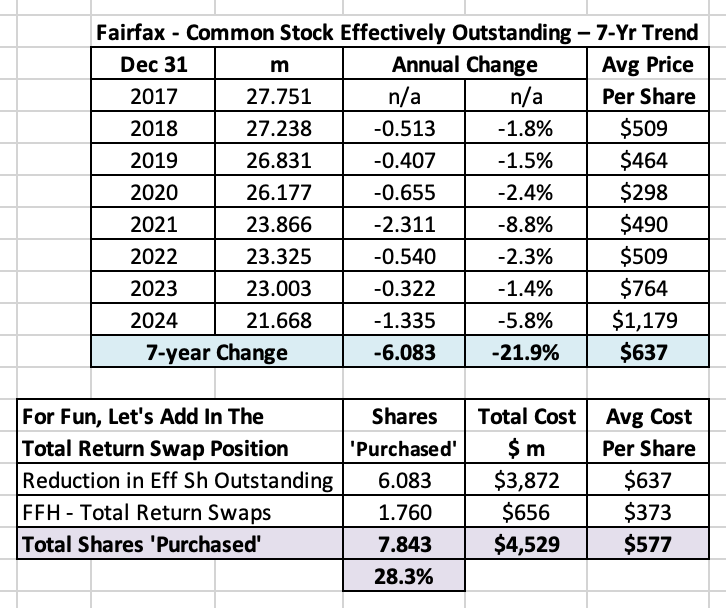

What is Berkshire Hathaway’s biggest problem today? ‘Only a fool learns from his own mistakes. The wise man learns from the mistakes of others.' Otto von Bismarck Berkshire Hathaway served as the inspiration for Fairfax’s creation way back in 1985 (when Hamblin Watsa purchased Markel’s insurance operations in Canada). Today, Berkshire Hathaway is at a much different life stage as a company than Fairfax. Being a much younger and smaller company, Fairfax has the opportunity to learn a great deal more from Berkshire Hathaway. Berkshire Hathaway is almost 60 years old as a company (in its present form). If Buffett could do it all over again, would he do anything differently? Of course he would. But let’s try and focus our discussion a little more. Today, we are going to ask a simple question: What is Berkshire Hathaway’s biggest problem today? Berkshire Hathaway’s biggest problem today is its size - it has grow into a massive company. Berkshire Hathaway has a market cap of over $1 trillion, making it the 9th largest publicly traded company in the US. I don’t think this is a controversial thing to say. And that is because Warren Buffett has been warning investors about this problem for decades. It has been getting worse every year. And it will continue to get worse every year moving forward. Why is size a problem? Berkshire Hathaway generates an enormous amount of excess capital every year. But because of its size, it now has a very limited opportunity set. This makes reinvestment of its excess capital very difficult. This lowers the rate of return the company is able to earn. As a result, the growing size of Berkshire Hathaway has been slowing the CAGR of the stock for decades. From a well above average rate of 29.2% for the first 30 years (1965 to 1994). To an above average rate of 15.7% for the next 10 years (1994 to 2004). To an average rate of 10.8% for the past 20 years (2004 to 2024). The rate of return being generated today is not a terrible thing. But clearly it is not what it once was. What is the root cause of the problem? The root cause of the problem is the power of compounding and time. As any investor knows (especially Buffett) compounding is an amazing and unstoppable force. Especially when given enough time. The result is magic. Decades ago, Berkshire Hathaway’s share price got to the exciting part of compounding curve (the hockey stick part). Ok… Yes, Buffett is the GOAT. Are we done? No, not so fast. Let’s ask another question: Was there anything Buffett could have done to stop the problem from happening? No, I don’t think there was anything Buffett could have done to stop Berkshire Hathaway from becoming such a large company. Ok. Dead end. Let’s reframe the question: Was there anything Buffett could have done to slow the problem from happening? Yes, I think there likely were some things Buffett could have done to slow Berkshire Hathaway from becoming such a large company. Like what? I can think of two things: Stock buybacks Buy and hold forever (steep aversion to selling anything) Both of these are big topics. Today, I am going to focus only on buybacks. How does buying back stock shrink the size of a company? Share buybacks are paid for using cash. This shrinks both assets and shareholders’ equity. Lower shareholders equity shrinks the size of the company. Stock Buybacks One of the reason’s Berkshire Hathaway got so big was Buffett refused to do any stock buybacks for many years. Even during extended periods when the company’s stock was cheap. Yes, Buffett had a good reason for not doing buybacks - he could usually earn a better return by allocating excess capital in other ways. This was clearly the right short term decision. And, with hindsight, arguably the wrong long term decision for the company and shareholders. Quality at a fair price “A great business at a fair price is superior to a fair business at a great price.” Charlie Munger Price/valuation might have been part of the problem. Perhaps Buffett was simply being too cheap - only wanting to buy back Berkshire Hathaway stock when it was wicked cheap (not just cheap). This would have severely restricted the opportunity for Buffett to buy back stock. This also makes no sense. Munger (supposedly) taught Buffett that it was preferable to buy “a great business at a fair price.” Why would this logic not apply to Berkshire Hathaway itself? Berkshire Hathaway was not just a great business… it was the best business in the world. And at many times in the past its shares were available at a fair price. A double standard? What is puzzling is Buffett loves it when companies he owns do big share buybacks (when their stock is trading at a low valuation). Apple is the best recent example. Buffett has been a big cheerleader of Apple’s buybacks for years. (Interestingly, massive buybacks have helped slow Apple’s own ‘too big’ size problem.) When it came to buybacks, Buffett seemed to have two standards - one for Berkshire Hathaway and another for the publicly traded stocks it owned. Buffett finally capitulates In 2011, Buffett finally relented and issued an official buyback policy for Berkshire Hathaway. But he set a buyback valuation threshold of 1.2 x BV. Really? That cheap? The result was Berkshire Hathaway repurchased few shares in the subsequent years. In 2018, Buffett ended the buyback valuation threshold of 1.2 x BV and gave management more discretion with when doing buybacks. As a result, the pace of buybacks increased quite a bit. But Buffett was decades too late - Berkshire Hathaway had already become a monster in size. The window of opportunity to use buybacks as a way to keep Berkshire Hathaway small was long gone. The Berkshire Hathaway multiverse Now imagine an alternate universe - imagine a past where Buffett was more open minded to share buybacks - actually did them in size at the appropriate times. Perhaps up to valuation threshold of 1.5 x BV - hardly a stretch for a company of Berkshire Hathaway’s quality. Would that have perhaps lowered past returns a little for investors? Probably a little. But it would have kept the size of the company smaller, perhaps much smaller. And this would have likely allowed the company to continue to compound at a much higher rate of return for a longer period of time - perhaps much longer. Summary Buffett has known for decades that Berkshire Hathaway was becoming too large of a company. After all, if anyone understands the power of compounding and time it is Buffett. I think it can be convincingly argued that Buffett did not do enough to manage that specific problem, especially 20 or even 30 years ago (when it was becoming apparent). Like being more open minded with stock buybacks (the concept and the price at which they made sense). Is this perhaps an example of where Buffett was not thinking long term enough? Yes, that question is a bit of a mind-bender. But it appears ‘long term’ to Buffett might have meant ‘during his lifetime’ (in terms of Berkshire Hathaway being an above average compounding machine). Of course, Berkshire Hathaway is a wonderful company. But it is no longer an above average compounding machine. And the risk for the company moving forward is it shifts from an ‘average’ to ‘below average’ rate of return for long term shareholders. Is there a lesson here for Fairfax? Yes, I think there is. An important one that is not on the radar today of long term investors. Buybacks are good because of all the usual reasons: When done at favourable prices (i.e. below intrinsic value), they deliver significant value. They increase the ownership stake of long term shareholders. They are a high certainty capital allocation activity. They are a sign management is rational and working in the best interests of long term shareholders. For compounding machines like Fairfax, we now have one more good reason to do buybacks. Especially when looking 10 or 20 years into the future. By meaningfully shrinking the size of the company (with aggressive buybacks over a long period of time), it allows compounding to continue at above average rates of return for a much longer period of time - it extends the runway of a compounding machine. Another important lesson: Don’t cheap out on the price you pay. As Charlie Munger taught investors, pay a fair price for a quality business - this will allow you to buy back many more shares than would otherwise be the case. What has Fairfax been doing? Fairfax has been aggressively buying back its stock since 2017. From 2017 to 2024, it has reduced effective shares outstanding by 6.1 million, or 21.9%, at an average cost of $637/share. The shares were repurchased at a crazy low price. And a significant number of shares have been repurchased. And if we include the FFH-total return swaps, Fairfax got exposure to 7.8 million of its shares, or 28.3%, at an average cost of $577/share. A very good news story is even better. In 2025, Fairfax has continued to buyback shares. YTD (to September 30, 2025), my guess is they have taken out around 400,000 more shares. In August and September, shares were likely repurchased at around $1,700/share. We will get details when Fairfax reports Q3 results on November 6, 2025. It appears Fairfax is comfortable paying ‘a fair price for a great business.’ This is another example of Fairfax moving up the quality ladder when deploying their excess capital. Bottom line, it looks like Fairfax has gotten the memo - they appear to understand Berkshire Hathaway’s size problem. And the management team at Fairfax appears to be doing something about it - in a pretty aggressive way. With buybacks it looks like Fairfax is thinking long term - the benefits of the buybacks being done today will flow to shareholders for decades into the future. This discussion leads us to another really important and related topic. Is having a chronically low share price (valuation) a good or a bad thing for Fairfax? Having a chronically low share price (valuation) has been a gift for Fairfax and its shareholders. It has allowed the company to buy back an enormous amount of stock over the past 7 years - to get exposure to 28.3% of its effective shares outstanding at a very low average price ($577/share). This was also a high certainty/low risk use of capital for Fairfax. The interesting thing is aggressive share buybacks have not impaired the company’s ability to grow its top line (the NPW of its P/C insurance business have increased in size by about 150% from 2017 to 2024). As a result, the per share value creation for long term Fairfax shareholders has been enormous. Bottom line, a low share price - especially if it persists for years - is a big benefit for long term Fairfax shareholders. Remember this when you look at Fairfax’s stock price each day.

-

@Haryana, when I think about earnings for Fairfax, I tend to look at the big picture - the annual increase in ‘economic EPS’. In my post back on Oct 18, I put out an estimated for 2025 of about $240/share. The build comes from three items (see below). The actual amount for each item will slosh around from quarter to quarter. We will see how Q4 finishes. I try to be conservative with my estimates. And I only update them a couple of times over the year. Yes, Q3 is shaping up to be a stronger quarter than I have built into my current estimates. Perhaps I will do an update in November. The more important number to me than what Fairfax might earn in 2025 is determining what is a ‘normalized’ level of ‘economic EPS’ is for the company today. For 2025, pretty much everything has been a tailwind for Fairfax - so I think $240/share is too high to use as a normalized economic EPS. My guess is normalized economic earnings for Fairfax are (conservatively valued) likely running around $200/share. And this amount should continue to grow nicely in the coming years. Bottom line, I prefer to be conservative with my estimates. With Fairfax’s stock trading at $1,650, it looks pretty cheap to me. I hope management vacuums up a bunch of shares at these prices. —————- From my post on Oct 18: “My guess is Fairfax is on track to earn about US$185/share in 2025 (accounting earnings). The change in excess of FV over CV for associate and consolidated holdings is on track to be about another $40/share in 2025 (after tax). And then there is the stuff we don’t see that is also increasing in value… let’s conservatively assume another $15/share. That puts the economic EPS at about $240/share in 2025.”

-

@Haryana, that is true. So we will see how things play out moving forward. At the end of the day, I do appreciate all the input from all the board members as we all continue on our journey of trying to improve our understanding of Fairfax, investing and accounting

-

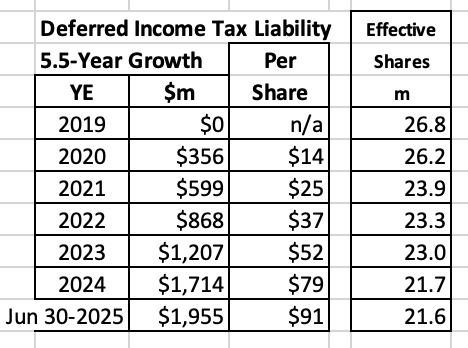

The trend in the deferred income tax liability at Fairfax is interesting - it has been growing like a weed, especially when measured per share. Today, it is a benefit for Fairfax of $91/share. Looks like this is an emerging benefit for Fairfax. As I said before, @Maverick47, thanks for bringing this forward and getting it on the radar of investors.

-

@Maverick47, that is very clear… thanks for connecting the dots on this topic for me. Much appreciated.

-

@Maverick47, thanks for bringing this important topic forward. And thanks to everyone who has chimed in - adding lots of value to the discussion. So am I understanding this correctly? Fairfax has two ‘non-perilous’ sources of leverage: Deferred tax liability = $1.7 billion at Dec 31, 2024 Float (insurance) = $35.4 billion at Dec 31, 2024 (P/C insurance) Is $1.7 billion the right number to use for Fairfax to (roughly) match what Buffett simply calls ‘deferred taxes’? Why does this matter to Fairfax shareholders? These two items give Fairfax “access to two low-cost, non-perilous sources of leverage that allow (the company) to safely own far more assets than (their) equity capital alone would permit.” Below is how Buffett described these two items in 1999. From Bershire Hathaway’s Owner Manual (1999) “…Berkshire has access to two low-cost, non-perilous sources of leverage that allow us to safely own far more assets than our equity capital alone would permit: deferred taxes and "float," the funds of others that our insurance business holds because it receives premiums before needing to pay out losses. Both of these funding sources have grown rapidly and now total about $32 billion. “Better yet, this funding to date has been cost-free. Deferred tax liabilities bear no interest. And as long as we can break even in our insurance underwriting - which we have done, on the average, during our 32 years in the business - the cost of the float developed from that operation is zero. Neither item, of course, is equity; these are real liabilities. But they are liabilities without covenants or due dates attached to them. In effect, they give us the benefit of debt - an ability to have more assets working for us - but saddle us with none of its drawbacks. “Of course, there is no guarantee that we can obtain our float in the future at no cost. But we feel our chances of attaining that goal are as good as those of anyone in the insurance business.” https://www.berkshirehathaway.com/owners.html

-

@anshulp, thanks for creating a separate thread for this topic. I am looking forward to getting a full picture of the company. And getting a behind the scenes look to many important events. 'Fair and Friendly' was a revelation in that regard and this new book should be even better. It cracks me up how most Canadians have never heard of Fairfax or Prem, given what they have accomplished. This book should really help in that regard. The author has started posting on X/Twitter so board members might want to follow him to get insights into the book.

-

@John Hjorth, I have no doubt the book is legit. And I have no concerns. As I said before, I look forward to reading the book. The more information that gets out on Fairfax the better - it is a great company and its story deserves to be told. I hope the author has read my stuff and found it helpful when writing his book. I hope/expect his book reaches a much larger audience than my writing does.

-

No. I have not been involved with this book. That is a very funny coincidence.

-

A new book is coming out on Fairfax called ‘The Fairfax Way: Inside Prem Watsa’s Secret to Lasting Success’. I am really looking forward to getting a copy… Available for pre-ordered (Nov 18 release). It is desperately needed. Looks to me like the author (David Thomas) nailed the timing of its release. https://www.amazon.ca/Fairfax-Way-Inside-Lasting-Success/dp/1037802195 ---------- About the author (from Amazon): DAVID THOMAS has had a front-row seat on the Canadian business world for several decades in Toronto, serving twice as Editor of the Financial Post and leading the reporting team at the Globe and Mail’s Report on Business. He served stints as Editor-in-Chief at MoneySense, Marketing and Canadian Business, and as Business Editor at Maclean’s. He was born in Vancouver and is currently based in London, England, where you can still buy newspapers at the convenience store.

-

A question for board members... what is the economic impact on Fairfax of buying out their minority partners in Allied World and Odyssey? What is the impact on Fairfax's P/C insurance business? Is taking out a minority partner essentially the same thing as making an acquisition of another large P/C insurance company? Does this activity not grow Fairfax's P/C insurance business? NPW. And underwriting profit. Except here's the kicker... What is the price Fairfax will have to pay to buy more of these 2 exceptional companies? Because of the call option feature, I think Fairfax will be able to take out the minority partners at a very attractive price/valuation. Someone please explain to me what I am missing? ----------- The fact that Fairfax has not taken out their minority partner in Allied World tells us something important (I think). I think it tells us that Fairfax is continuing to find better opportunities in which to deploy their excess capital. If true, that will be bullish for future returns.

-

From my perspective, the most important factor when analyzing Fairfax is capital allocation. This will impact Fairfax's results much more than anything else in the coming years. The management team at Fairfax has been delivering a clinic in capital allocation over the past 5 years. My guess is they will continue to make good decisions - and this means they will likely continue to compound excess capital at above average rates of return in the coming years. I try not to get stuck in the weeds. Like tying to guess the path of interest rates over the next couple of years. Equities are volatile. This is shaping up to be a banner year - although no one is giving Fairfax credit for the big gains that are not mark to market (like the big move in Eurobank). Some years will be better than others. Over time, the returns from holding equities will be much better than if they simply held bonds. The insurance cycle is... cyclical. Fairfax has been around for 39 years. For most of that time, P/C insurance has been in a soft market (hard markets are very rare). And Fairfax has grown its insurance business like a weed. For a better comp, look at the last 10 years. Fairfax doubled the size of its insurance business in a soft market. And then doubled it again in a hard market. Sorry, I do not understand all of the hand wringing today about a soft market. The problem that many investors have is they want to know today exactly what Fairfax is going to do in the coming years. Unfortunately, that is not possible with Fairfax. That lack of visibility is not a problem (for Fairfax and for long term investors). It is one of the core strengths of their business model.

-

Chuck Akre - How to Find a Compounding Machine Chuck Akre is one of the investing greats. He delivered very good returns over the long term for his investors. He also was a very good communicator and teacher. In our post today, we will explore Akre’s wisdom. To see what it can teach us about Fairfax. Over his lifetime, Chuck Akre tried to answer two questions: What makes a great investment? What makes a great investor? ————— Akre’s north star: rate of return “The bottom line of all investing is rate of return.” Chuck Akre Early in his journey, Akre focussed on understanding the power of compounding and how it should be incorporated into an investment framework. For Akre, the answer was rate of return. The goal of an investor was to earn an above average rate of return (high return on equity). For an investor to earn an above average rate of return they need to invest in businesses that earn an above average rate of return. Investors should only fish in the ‘above average rate of return’ pond. What makes a great investment? What is it about the business that allows it to earn an above average rate of return over the long term? Akre found an answer to this question. The investment framework he developed he called the 3 legged stool The 3 legged stool Akre’s investment framework describes the characteristics of a great business. Leg 1.) Exceptional / high quality business. High rate of return business. Generates high returns on invested capital. Leg 2.) High quality management Demonstrable skill (able) at running the business (operations). Long track record. Integrity (honest) - Treats shareholders as partners. Management (results) should be evaluated using per share metrics (to ensure no dilution is happening). Leg 3.) Good reinvestment opportunities This is what allows high return businesses to keep earning high returns into the future. Creates long term value by unleashing the power of compounding. Want to see both a history and a long runway of future opportunity. Of the three legs, the third is the most important. Find a stock that checks all three boxes and your have found a compounding machine. That is investing nirvana. One more important input. Purchase price Don’t overpay. This will allow you to earn higher future returns (this results in better compounding). Summary “Everything should be made as simple as possible, but not simpler.” Albert Eintstein Yes, this is a deceptively simple framework. Here is how Chuck Akre summarizes his approach: "The three areas of analysis – business, management, and reinvestment – are the key components of what we call our ‘three-legged stool.’ When we find a business that satisfies all three of our requirements, we refer to it as a ‘compounding machine,’ and we seek to purchase shares at a modest valuation." Chuck Akre ————- Additional comments: How to think about risk When you find a company that checks all the boxes: Exceptional quality Strong management Abundant reinvestment opportunities Purchased at a discount Investing using this framework exposes an investor to below average risk. (Akre did not define risk in terms of price volatility.) When to sell The hardest part of investing is being patient and holding a winning investment for the long term. You will be tempted to sell it. It will probably be a mistake (according to Akre). It is very difficult to find a great investment - it takes years. So when you find one it should be held. Even if it looks overvalued at times. Not surprisingly, Akre had a concentrated portfolio. That had low turnover. How to measure the performance of a management team The change in the share price over time. Per share metrics are the ones that matter. On the importance of making (and learnings from) mistakes “Good judgement comes from experience. And experience comes from bad judgement.” An old saying often repeated by Akre. Markel Akre was a fan of Markel (the historical performance of the company back when it was a compounding machine). It would interesting to get his thoughts on the company today. ————— Trying to solve the investment puzzle - Chuck Akre - Talks at Google https://youtu.be/O38I7QIc_eQ?si=diFIZa5m16SmmwfE ————— How does Fairfax look using Akre’s investment framework? Leg 1.) Exceptional / high quality business? Fairfax has compounded BVPS at 19% for the past 39 years. The model it uses is similar to the one used by Berkshire Hathaway in the 1980’s and 1990’s (when it was more leveraged to P/C insurance). Leg 2.) High quality management The management team at Fairfax is exceptional. They are equally good at: Running the business (P/C insurance and investment management). They have a long track record of excellence in both businesses. When it comes to capital allocation over the past 5 years, their performance has been best-in-class compared to P/C insurance peers. High integrity. Shareholders are viewed as valued partners. The communication is very good. Management is focussed on driving per share value for long term shareholders. Leg 3.) Good reinvestment opportunities Fairfax has developed an amazing range of capabilities across both P/C insurance and investment management businesses. With P/C insurance, the company now has a global platform. This gives it a large opportunity set to continue its growth (organically or by acquisition). With investment management, the company has a diverse set of capabilities. Traditional asset classes: fixed income and equities. Alternative asset classes: private equity, venture capital, commodities, real estate. Global reach, with specialty in India. Built (earned) over decades, Fairfax has an extensive network of external partners. OMERS (funding). Kennedy Wilson (real estate). These relationships help enormously with deal flow. In short, the opportunity set today for Fairfax has never been better in the company’s history. Capital will be allocated to where it is able to earn the best return. This should allow the company to continue to earn above average rates of return in the coming years. In turn, this should create enormous value for long term shareholders. Fairfax checks all three boxes of Akre’s three legged stool - it looks like a compounding machine. But we need to look at one more important input - valuation. How is the stock being valued today? Before making any adjustments, Fairfax’s stock looks cheap. Make adjustments for excess of FV over CV for associated and consolidated holdings and the stock looks even cheaper.

-

That is a simply brilliant way (mental model) to help think about the current situation. Thank you for sharing (I may borrow it to use in a future post )

-

A picture is worth 1,000 words. The best performing insurance company (over the past 5 years) is available at the cheapest valuation (compared to peers). What to do? Panic, of course. I love Mr. Market. (My guess is Fairfax does too.)

-

If Fairfax India is successful in buying IDBI, yes, it will be interesting to see the details. Amount paid Valuation How it is paid for (where the cash comes from): Fairfax India/Fairfax/External partners Restrictions/demands from government Creativity used in how the deal is structured Impact on CSB It will also be interesting to see how investors react to the news/details. The reaction from investors will likely be focussed on the short term (price paid versus value received). It wouldn’t surprise me to see a lot of negativity. But we will see (perhaps I am living too much in the past).

-

One way to estimate the increase in intrinsic value in a given year at Fairfax is to sum three buckets: Reported EPS The change in excess of fair value over carrying value for associate and consolidated holdings (after tax). The change (increase in value) in everything else not captured in 1 and 2 (after tax). The first two buckets are pretty straight forward. Fairfax tells us what these amounts are when they report their financial results. The third bucket is not straight forward as Fairfax doesn’t help us (very much). We tend to find out about this bucket prospectively - after Fairfax monetizes and asset (sells or revalues it). Some examples: The recent sale of Fairfax’s 80% stake in Eurolife’s life insurance business for $944.7 million. Speculation is it could result in an investment gain of about $300 million when it closes in Q1, 2025 (about $15/share pretax). BIAL. How much has this airport increased in value in 2025? Has that been captured in buckets 1.) or 2.) above? Ki Insurance. How much has Ki increased in value in 2025? Has that been captured in buckets 1.) or 2.) above? Poseidon. This is another big holding for Fairfax. I don’t think its carrying value has changed much over the past 3 years. Does this make sense? I could go on. There are lots of examples of value that is likely building at Fairfax each year that is not captured in buckets 1.) or 2.) above. An important change: This was happening at Fairfax in the past. But it was primarily in the P/C insurance side of the business. Not the equity holdings (for reasons we have discussed many times before). That dynamic changed beginning (roughly) about 5 years ago. Now it is happening both with the P/C insurance and the equity holdings. Compounding: Compounding doesn’t care if the value is known to investors or not. Or to put it another way - ‘hidden value’ will compound over time just like ‘known value.’ This is important. A big unknown number (if my thesis is correct) is quietly getting much bigger. What if I am completely wrong? Investors ignore buckets 2.) and 3.) when they analyze/value Fairfax. So it is not built into the stock price. So there is no downside to my thesis (if I am wrong)… only upside (if I am right).

-

My guess is Fairfax is on track to earn about US$185/share in 2025 (accounting earnings). The change in excess of FV over CV for associate and consolidated holdings is on track to be about another $40/share in 2025 (after tax). And then there is the stuff we don’t see that is also increasing in value… let’s conservatively assume another $15/share. That puts the economic EPS at about $240/share in 2025. Book value at Jan 1, 2025 was $1,060. That puts economic ROE at 23% (off beginning equity). And economic P/E at under 7x. Yes, economic earnings in 2025 are elevated. My guess is a ‘normalized’ economic EPS is probably about $190 to $200/share. That puts ROE at 18%. And PE at 8.7x. In late Nov/Dec of 2024 (and over the first quarter of 2025) Fairfax traded at about $1,400/share. Today it trades at $1,660. As I outlined above, intrinsic value has probably increased about $240/share over the past year. What that means to me is Fairfax is trading at a similar valuation today to what it was trading at a year ago (when it was $1,400/share).

-

Owning home and asset allocation/portfolio management

Viking replied to Milu's topic in General Discussion

I think it makes sense to look at asset allocation and portfolio management through different lenses. Each one provides a different perspective on a very important topic. I think the basic building block to a financial plan is net worth. Another building block is an annual cash flow statement. And having some basic goals (one year and longer term). The composition of net worth is an important part of the puzzle. This includes things like pensions. It makes sense to me that an investment portfolio will be constructed in a way that it aligns with both your life situation (net worth and cash flow) and the financial goals you have set for the year (and years). PS: My wife and I are both happy renters today. -

I did the same. I explain my thinking below. I manage my Fairfax investment in two ways: Core position Flex position The core position is the (relatively) new part for me. I have held a large core position in Fairfax since late October/early November 2020. At a little over 5 years, this is the longest time period I have ever owned a core position in Fairfax. (It is the longest period of time I have owned a core position in any stock.) Flexing my position size is something I have done with Fairfax on and off for +20 years. I sometimes buy more of the stock when it sells off/gets cheaper. And then I lighten up when the stock moves higher. With my flex position in Fairfax I am looking for a small gain (the exact amount will vary each time and will depend on the set-up). Normally, I find I get 2 or 3 nice opportunities each year to flex my position in Fairfax. Times when the stock sells off - where I like the short term risk/reward set up. Why did I ‘flex’ my position higher today? Stock closed today at $1,660/share. Three days ago it closed at $1,790/share. Decline was 7.3%. It looks to me like the stock has sold off over the past week for reasons that have nothing to do with Fairfax. (I.E. all financials are selling off.) Fairfax’s fundamentals continue to improve - I really like the sale of Fairfax’s 80% stake in Eurolife’s life insurance business for $944.7 million (expected to close in Q1-2026). Strong earnings - I expect Fairfax to deliver very good Q3 earnings report. My guess is BV will be comfortably over $1,200/share. This puts the P/BV at about 1.38 Hidden value - Excess of FV over CV for associate and consolidated holdings is likely $100/share (after tax). That puts ‘adjusted’ P/BV at about 1.28 ($1,660/$1,300) Hidden value part 2 - Of course, we know intrinsic value is much higher than ‘adjusted’ BV of $1,300. Let’s be conservative and add another $100/share (Eurolife sale will crystallize a nice investment gain in Q1-2026…). This puts Fairfax’s value (measured conservatively) at $1,400/share. This puts the. P/FV at 1.19 Today. Fairfax thinks its stock price is cheap - Fairfax was an aggressive buyer of its shares in Q2, paying about $1,700/share. Seasonality - As @SafetyinNumbers has pointed out many time before, Fairfax’s share price tends to underperform during hurricane season (which runs until about the end of October). A headwind will end soon. All cashed up - As I said earlier, I expect Fairfax to deliver strong Q3 earnings - they will be all cashed up in early November. What will they do? Well, being all cashed up, with shares trading below $1,700 and with hurricane season behind them… why not buy back a bunch of stock to year end? Added motivation - Fairfax still owns 1.76 million shares of FFH-TRS. Every $100 increase in Fairfax’s share price delivers an investment gain of $176 million to Fairfax. This makes buying back stock when it is undervalued (like it is today) an even better decision. A near term risk to my ‘flex’ trade: it appears the hard market in P/C insurance is coming to an end. Lots of P/C insurance companies will report in the next 2 weeks. It they disappoint in the top line (revenue) we could see a big sell off in P/C insurance stocks. Important: I flex my positions in stocks I am happy holding for the long term (with the increased position size). There is always a good chance the stock could get much cheaper from here (especially in the short term). Anyways, I do not post this as investment advice. My logic could turn out to be completely wrong. Please consult your investment advisor before making any investment decisions. My post above is intended to be for information/entertainment purposes

-

What made the view ‘make sense’ when rates were 0-2%? It was because rates subsequently moved much higher than anyone imagined from 2022 to 2023. Fast forward to today. What if interest rates spike again from current levels in the coming years - much higher than anyone imagines today? Is October 2025 really all that different than December 2021? Is our crystal ball - when it comes to understadning the future path of interest rates - really that much better today? PS: I have no idea where interest rates go from here in the coming years. But I am not ruling out that they might go much higher.