Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

I think your total number is directionally correct. But I don’t think effective shares will fall by nearly that much. I think most of the repurchases in Q1 will go to offset the compensation program (which Prem reviewed in his letter in the 2024AR). Share repurchases from this point forward will reduce effective shares outstanding. At least I think that is what Fairfax has done in the past.

-

The thread from Bob does a nice job of explaining what is happening under the hood. Trump’s economic plan is completely snarling supply chains. How well did that go during Covid? So why are financial markets going higher? Because they KNOW a snarled/slowing economy will force Trump to reverse course. Yes, the emperor has no clothes.

-

This is the best non-political take of the current situation in the US and where things might be going that I have heard. In the second half of the interview he discusses his inflation outlook - he thinks it will likely trend higher than consensus currently expects… Rogoff is one smart cookie.

-

Here is a good video review of what has transpired over the past couple of weeks. Facts matter. We now have enough information we can start to evaluate how well Trump’s economic plan is being implemented / communicated. To state the obvious - it is a big, big deal (what Trump is trying to do). It looks to me like we are seeing an epic level of incompetence - in terms of how this is being handled and communicated. (Now pretend you are a country on other side of the table from these guys…)

-

Well, it's time for people to get out of their ivory towers when it comes to Trump’s economic plan. Time to pivot and see what the impact his policies are actually having on the American economy (businesses and consumers). The rubber is just starting to hit the road (the impacts are just starting to happen). Watch the video below to hear from a small business owner. It is eye opening what he is having to deal with. Liberation Day: ‘I am rapidly being liberated from my money.’ Of interest, his tariff costs are increasing from $2.3 million last year to a projected $100 million this year (based on current tariff levels). No he won’t be absorbing the tariff in his profit margin. Bottom line, his business will be shrinking dramatically. Many good paying jobs in the US, like at this company, will be vaporized. Will production of the products he sells be moving back to the US? No. American manufacturers aren’t interested. The volumes are too low. At the same time, labour costs are high. And labour is unavailable. The products being tariffed will not be available for Americans to buy. Nobody is benefitting. Trumps policies are simply raising prices for consumers. ‘It is a tax.’ Simple. Big businesses go to Washington and lobby for and get exemptions from tariffs. Small businesses are not so lucky. ‘Exasperating.’ Expect more stories like this in the coming weeks and months.

-

The benefits of having a decentralized operating structure Investors spend a lot of time trying to understanding the numbers. Because it is relatively easy. Other things like company structure and culture gets very little attention. Because they are much more difficult things to understand and evaluate. Fairfax has a decentralized operating structure. One advantage of having a decentralized operating structure is it promotes an entrepreneur mindset among employees. This can be a very powerful driver of results - today and (more importantly) in the future. In recent months Fairfax has been explaining to shareholders the importance of its decentralized operating structure. Prem included a long section on this topic in his letter to shareholders in the 2024AR. This covered the big picture. And at Fairfax’s AGM in April of 2025, we heard from the presidents of Northbridge and Allied World. Their comments got more into the weeds. Going to Fairfax’s AGM and listening to the presidents speak - attendees get to see/hear first-hand: The quality of the people running the insurance businesses. The entrepreneurial spirit that is shining through the different companies. Fairfax’s structure attracts and rewards entrepreneurs. Fairfax has been methodically/patiently working at it for 39 years. Today, Fairfax has put together an amazing collection of companies - all lead by entrepreneurs - both in its insurance companies and non-insurance equity investments. This positions the company exceptionally well for the future. What Fairfax has built over the past 39 years would be exceptionally difficult to duplicate - and it would take a long time. A decentralized operating structure is an important part of Fairfax’s moat. Even if it is not well understood by investors. In this post we will explore Fairfax’s decentralized operating structure: Part 1: The big picture - Prem Watsa Part 2: Grow organically - Silvy Wright - President - Northbridge Part 3: Grow by acquisition - Lou Iglesias - President - Allied World ————— Part 1: The big picture – Prem Watsa In the 2024 annual report, Prem began his shareholder letter by discussing Fairfax’s decentralized operating structure and its importance to the success of the company. We have included the full quote below (it is long). Comments from Prem in Fairfax's 2024AR: "Since we began in 1985, 39 years ago, our book value per share has compounded at 18.7% per year (including dividends) while our common stock price has compounded at 19.2% (including dividends) annually. As I have mentioned previously, our success throughout our history and again in 2024, has come under a decentralized structure with outstanding management executing a disciplined approach to underwriting. "Over the years, those who have followed Fairfax, read our letters and attended our annual meeting, are well aware that we are passionately devoted to the decentralized operating philosophy. This year, I want to spend more time on this subject. Aside from helping inform our shareholders about our thinking in the past and present, I have an ulterior motive that comes from an eye on the future. As Fairfax rolls into the future, your Chairman (gradually) passes leadership to the next generation, and they, in turn, to later generations; it is very important that we memorialize why decentralization is such a critical feature of Fairfax. I want and expect Fairfax to thrive over the next 100 years, and well beyond. To do so, I believe it is of paramount importance that we never abandon our decentralized approach! "So, why are we so fervently attached to this model? At its foundation, decentralization places its faith in the many rather than the few. Embedded in the Guiding Principles, which we have published every year in this report, is our deep and abiding respect for the fact that we are all created equal before God. All of our offices display prominently The Golden Rule; treat others as you want to be treated yourself as depicted in all the religions of the world. All of our CEO’s have a plaque with the following quote Ronald Reagan loved so much and kept on his desk: “There is no limit to what a man can do or where he can go if he doesn’t care who gets the credit.” Decentralization is the best system for unleashing the power of the many, rather than being limited to the talents of the few. And it aligns so perfectly with the foundational values of Fairfax since its inception. Our optimism in what empowered people can accomplish is unbounded! "What are the advantages of an empowering, decentralized operating system? Let me count the ways: 1.) Ownership and Accountability "Each of our CEO’s is given full autonomy over all underwriting and operational functions within their company, other than investments. They set strategy and tactics. They are responsible for managing risk within the limits of their allocated capital. Accordingly, they are fully accountable for underwriting performance and its results. The decisions implemented in their companies are their own, not those passed down from above. 2.) Management Retention "A direct benefit of this Ownership Culture is the exceptional continuity of management we enjoy at Fairfax. As I write this, our Presidents and Senior Executives at Fairfax average close to 20 years of service. We are big believers in the benefits that come from this continuity. Rather than shuttling in new leaders every four or five years, our companies are able to continually build on success, without undergoing the strategic U-turns that management turnover often brings. 3.) Flexibility and Nimbleness "The autonomy our companies enjoy allows a degree of operating agility absent from large, centralized organizations. Our performance during the recent hard market years of 2020 to 2023 bear this out, as we advantageously expanded at an industry leading pace! We rely on the expertise and judgment at each of our companies, and we do not prescribe from the top. For example, when the cyber insurance market underwent radical change at the end of 2020, we had four of our major companies dramatically expand their activity, each pursuing a different strategy. Had we imposed a one-size-fits-all approach to this challenging class, the growth would have been a fraction of what it was. 4.) Reduced Leakage from Acquisitions "We do not, as a general rule, look to integrate acquisitions into existing operations, which means we keep much more of the business and people we acquire. Our industry is replete with examples of acquisitions that have little to show after three or four years because people have left and portfolios have melted away! 5.) Financial Flexibility "Maintaining independent, separately capitalized companies gives us a source of financial flexibility. While it will always be the case that none of our companies is for sale, there may be times it makes sense for us to sell a minority stake. Witness the sale of 10% of Odyssey a few years ago, enabling us to make a large share re-purchase at an opportune time. "At Fairfax, for today and the future, we believe the best conditions for operating success depend on the Three Ts: Trust must be reciprocal between the holding and operating companies. Trust has to be earned and its strength increases over time. Decentralization cannot work without it. Transparency with clear and open communication is required at all times. Talent is necessary to operate successfully at a high level in a challenging industry. "There are those who might look at Fairfax from the outside and lay out a plan that would, on paper, describe myriad benefits to be obtained by abandoning our approach. They would do so without being able to quantify the intangible benefits we enjoy. It is vitally important to me that the Fairfax approach does not change because I believe our long-term success depends on it!!" Prem Watsa – Fairfax 2024 Annual Report ————— Part 2: Driving organic growth - Silvy Wright - President - Northbridge Background The Athappan Cup was established at Fairfax in 2024. It will be awarded at the AGM each year to one of Fairfax’s insurance companies for underwriting excellence. The first-ever winner of the award was Northbridge Financial. The company delivered a 90.1% CR over the past 5 years - with reserve redundancies every year. What was Northbridge’s secret sauce? At the AGM, Silvy Wright gave us some insight into what has enabled Northbridge’s stellar performance over the past 5 years. She took attendees back in time. And highlighted the importance of Fairfax’s decentralized operating structure - and how it allowed Northbridge to transform its Canadian operations in 2012 (operationally - the brining together what had been 4 separate companies). Today, we are seeing the benefits of this transformation in the underwriting results that Northbridge has been able to deliver over the past 5 years. Comments from Silvy Wright at Fairfax’s AGM in April 2025: “(A)s you can appreciate, we've all had different journeys, and mine started in 1994. So I just want to take just a few moments to share an employee experience. And that's me. “In 1994, I joined Markel. And Markel, as you all know, was the first company Prem bought. And in 1994, Markel was about $60 million in revenue (and) 60 people… I was not a president 30 years ago. Well, my parents would have been pretty proud if that happened. But I wasn't the president back then. (When) I joined, I was an accountant, but with a strong entrepreneurial drive. “And it was very clear to me, when I joined Markel, that Prem's philosophy on decentralization really inspired that entrepreneurial spirit in Markel. There were 60 of us. And when I refer to entrepreneurial spirit, I'm thinking you feel like an owner of the company, so you work like an owner of the company. You've got the freedom to take risks or you have the freedom to challenge the status quo. And then you have a great sense of pride of what you do. And that spirit lived in all 60 people, from the collections manager who collected every dollar like her own, to the underwriting head who developed strong relationships with the customers. And within that environment, all the employees built the leading transportation insurer of Canada. “Now of course, it didn't happen overnight, but over the years, that's what all the employees did. So flash forward, so I'm still here, 16 years later, I learned a lot at Markel, a lot of freedom, a lot of mistakes, learning along the way, and I was appointed the CEO of Northbridge Financial (in 2011). Northbridge Financial represented the Canadian insurance operations of four separate companies. “And at that time -- I know you're not going to like this Prem. But at that time, we asked for the unthinkable. And that is to bring the 4 companies together from an operational perspective. And we asked for that because we really wanted to compete more effectively in the changing landscape in Canada. Not for layoffs -- we didn't have layoffs. But we knew that we could leverage the combined talents of the group. We can leverage the diverse portfolios that we had in the various companies so that we could be a stronger force with the broker distribution and then obviously to leverage scale to invest in that company. So that's what we did. “But the top goal of that beginning was not that obvious. The obvious was, okay, you're going to make changes, you better make a profit. The top goal was not that. The top goal, having been with Fairfax already 16 years at that time, was to build the culture and the entrepreneurial spirit that I knew creates success in the long term. “And so that's what we did. We empower -- we continuously fostered an employee empowerment. And empowerment does not work if it just sits at the top, right? Yes, presidents have freedom. But the success is when you cascade that empowerment throughout the organization. When people feel that they have the freedom to challenge the status quo, to come up to the president and share an idea, and that's what we've done. And we're not perfect, but we've unleashed a lot of talent, and it's all in the talent of those employees that we have established a very good record. And now we have a nice shiny silver cup. “So, with that, thank you… Prem… the trust… we both took a risk, and it paid off.” Silvy Wright - Fairfax's AGM - April 2025 ————— Part 3: Driving growth by acquisition – Lou Iglesias – President – Allied World Background Fairfax purchased Allied World in 2017. In terms of size, at the time it was a massive purchase for Fairfax. Allied World has since become a big success story for Fairfax (and the senior management team and employees of Allied World). It was a purchase that almost didn’t happen. Why it did happen is instructive. At the AGM, Lou Iglesias told attendees the story of why Allied World decided to sell their business to Fairfax back in 2017. The story highlights the importance of Fairfax’s decentralized operating structure - and how it was a key part of Allied World’s decision-making process. And how it will likely help Fairfax with acquisitions in the future. Comments from Lou Iglesias at Fairfax’s AGM in April of 2025: “It's good to see everybody. Obviously, one of the themes at the AGM this year is decentralization. So, I thought I would… talk about Allied World and decentralization and how it affects an operating company. And I'd like to start with a little story. I know some of my new friends that I met last night would like to hear a story about that. “So going back to 2016, 2017 time-frame. At Allied, we were looking for a transaction, right? We were a midsized public company. We thought getting a bigger, better platform would help us continue our journey, build our company out. We felt that we still had the ability to create a lot of value. “So we were talking to several suitors. And one, we got pretty far along with. We were working with them for over a year, and we're getting close to the finish line. And so now we're getting into the details. And we started to realize that this would be a merger and that it would be likely that Allied World would be broken up. And that didn't sit very well with us. It wasn't what we wanted as a company. So that transaction never happened. “Shortly after that, we get a call from Fairfax. And at the time, we didn't know a lot about Fairfax. We were a little bit tired of working for over a year on a transaction that didn't work, and we were a little reluctant. But Prem said, wait a minute, Fairfax does things differently. You should hear us out. And we all know Prem could be very convincing. So we took the meeting, and we heard a lot about the Fairfax culture, which sounded very good to us. And we heard a lot about decentralization in the independent operating model, which sounded great to us because, again, we felt that we still had a great runway to build our company out. “So we finished a meeting. I went across the street to the restaurant with John Bender and Wes DuPont, who are sitting up there and a couple of others. And being the good underwriters that we are, we were kind of skeptical, a little bit. Prem loves to tell that story. We're a little skeptical, but we did our diligence, and we found out, yes, that is how they do it at Fairfax. And we did the transaction. And very quickly, since Fairfax exceeded most of our expectations, the skepticism went away, right? So very quickly, we got past that. “But the point of this story is, number one, decentralization was so important to Allied World that it's likely that we may never have been part of Fairfax if it wasn't for it. And I think the second thing to take away is that I think Fairfax is going to have the #1 slot to talk to companies and acquire companies that still feel that they could do great things, right? Because that's the platform that you want to be able to move your company forward. So we had our own same management team, staff, strategies, no layoffs, right, and we move forward. “So where does that bring us today? So if you look at the full 6 years that we've been part of the Fairfax family we've posted over $1.6 billion of underwriting profit, over $3.6 billion of net income. Our combined ratio has improved for 6 years in a row every year. In 2024, just last year, we had $540 million of underwriting income, which is a record for Allied World and our third record year in a row. And we've more than doubled the size of the company at over $7.2 billion since we were acquired. “So, a lot of things go into that. I credit our people, who I think are fantastic, and Andy talked about people. The ability to keep the best people certainly is a huge part of the results that I just talked about. That's one thing. We have great professionals at our company. “But I'd also say, I could say with great confidence that in a centralized company or in a merged company, that level of performance I don't think would have been possible. And prior to Allied World, I was with a large centralized company for many years so I could see the differences pretty clearly. And they're stark, right? The ability to run your business, the ability to carry out your strategy seamlessly, to keep the best people, the lack of bureaucracy which is a really, really big benefit for all the Fairfax companies, is tremendous. “And last thing I really want to touch on is trust because I don't believe that you could have a successful decentralized operation without trust, right? And we trust Fairfax explicitly. We believe they trust us as well. But trust equals transparency, right? So you could have decentralization. We have a tremendous amount of transparency without having to write thousands of reports, right? Andy and I, in a 1-hour call, will cover what would take me 7 hours of reports that I would have had to write, okay? Transparency is key. “And I also think that Fairfax deserves a tremendous amount of credit. It's not easy to run a large decentralized company as successfully as they do, a large global company. It takes dedication, takes discipline, professionalism, and it takes a very unique skill set to be able to do it effectively. So great credit to Fairfax. And I think all the operating companies benefit tremendously.” Lou Iglesias - Fairfax's AGM - April 2025

-

Japan, Europe, China have all called Trump’s bluff. We could probably include Powell. What an epic fail.

-

@John Hjorth , I am following the real estate market for a couple of reasons: Canada has had a housing bubble. It was the economy here from 2010 to 2022. Where it goes from here will have important implications for Canada's economy. My wife and I sold our house in 2021. We are happy renters today. If prices in Vancouver came down that would tilt the calculus a little more in favour of owning. Nothing imminent. But I am open minded. I have three kids who are all 20 to 25 years of age. Today, they all want to live in Vancouver. If real estate comes down in price, we might get a generational buying opportunity here in Vancouver. If that happened we might help our kids out (not sure what that help would look like). I view any real estate purchase not as an investment. I am good at compounding financial assets. Even at lower prices, any real estate purchase would likely deliver sub par returns (compared to what I can earn in financial assets). So a big consideration for me is how much of my portfolio I want to put into an asset (real estate) that is likely to earn sub-par returns moving forward. Yes, that is a first world problem. But I do need to be careful not to over-reach (and take my current financial situation for granted). Having said that, I tend to be too cautious when it comes to real estate - and that is because it is not how I am wired (from an investment perspective). Bottom line, real estate in Vancouver is on my radar. Nothing is imminent. But I am trying to be inquisitive and open minded. Perhaps a fat pitch comes along. Perhaps we are already there and I just don't see it (that too conservative thing). --------- PS: The generational estate planning thing has been going exceptionally well. I plan on doing an update on this topic. Real estate is an emerging topic...

-

@cubsfan , I think most people agree that the US has some legitimate trade issues that need to be addressed. People are disagreeing with Trump’s logic/methods being used (to solve the issues). 1.) His policies completely lack credibility - what little Trump has put into writing makes no sense (I refer you to Trump’s reciprocal tarriff chart). 2.) He changes his mind almost daily - so his objectives/aims aren’t coherent (slogans aren’t enough). When the Japanese recently met with US negotiators, the US negotiators asked the Japanese what concessions they were going to offer. The Japanese asked the US negotiators what they wanted. The US negotiators could not answer that simple question. Further, Trump’s methods are bizarre - he is playing the victim card. He is shredding trust. Why would you sign an agreement with a counterparty you no longer trust?

-

In the downtown core of Vancouver today nominal prices of condo's (per square foot) are getting close to where they were back in 2018. Same with single family houses in the West part of the city (Dunbar area) where I currently live/rent. If inflation was zero, then looking at nominal would be useful. But inflation since 2018 has been significant = about 20% in Canada. So if nominal prices are flat over the past 6 years, that means we have had a 20% correction in real prices = bear market decline. And given the current situation in Canada (high level of economic uncertainty/slowing economy) demand for real estate has fallen off a cliff (historic lows) in what is usually the strongest part of the year for real estate. At the same time, supply is growing (spiking when it comes to condos). Months of supply is ballooning higher. My base case is prices continue to move sideways (perhaps come down a little) in nominal terms and inflation continues to run at 2.5 to 3% over the next couple of years. In real terms, perhaps prices come down a total of 25% or 30%. The key for Canadian real estate over the next year will likely be the path of the economy.

-

The last time financial markets were in turmoil was during the US regional banking crisis in spring of 2023. Fairfax & Kennedy Wilson were opportunistic. The initial investment in PacWest loans has performed very well. More importantly they used the crisis to build a new business/income stream - making both companies stronger in the process. There are many really important lessons that come from this investment. Relationships matter. Fairfax has built an extensive network of external relationships/partnerships across industries and geographies. This capability leads to deal flow. Fairfax's phone is starting to ring again. This is a great example of how extreme volatility in financial markets has been a good thing for Fairfax and its shareholders. Something to keep in mind in the current environment. ---------- In June of 2023, Kennedy Wilson and Fairfax purchased a $4.5 billion construction loan portfolio from PacWest. PacWest was caught in the regional bank crisis and they were forced to sell their best assets at a discount. At Fairfax’s AGM in April 2025, Bill McMorrow from Kennedy Wilson provided an update. How has the investment performed? Was it a good decision? There are to angles to this transaction: Initial transaction – purchase of the $4.5 billion construction loan portfolio. 27 of those 65 loans have been paid off at par (they were bought at a discount). Since inception, the loans have generated almost $500 million of interest income. The current portfolio is generating roughly $350 million a year in interest income. Building the business One of the conditions of the original deal with PacWest was the 40 people who were running the loan portfolio would also move over the Kennedy Wilson. At the same time, the regional banks backed away from the multifamily and student housing market. Over the past 18 months, the new team at Kennedy Wilson has generated about $5.5 billion of new loan originations. As a result, interest income of $350 million is expected to grow significantly in the coming years. “It was another one of these success stories that really turned out well for both our companies.” Bill McMorrow ----------- Comments from Prem about Kennedy Wilson in Fairfax 2024AR. “Since we met Bill McMorrow and Kennedy Wilson in 2010, we have invested $1.3 billion alongside them in real estate, have received cash proceeds of $1.1 billion and still have real estate worth about $650 million. Our average annual realized return on completed projects is approximately 22%. We also own 10% of the company. More recently, we have been investing with Kennedy Wilson and the team from Pacific Western Bank that joined them, in first mortgage loans secured by high-quality apartment buildings predominantly in the western parts of the United States, with a loan-to-valuation of 52%. At the end of 2024, we had invested in $4.4 billion of first mortgage loans in the U.S. at an average yield of 7.8% and an average maturity of 1.7 years with two, one-year renewal rights, and in $440 million of first mortgage loans in the U.K. and Ireland at an average yield of 6.9% and an average maturity of 1.6 years.”

-

I found this video helpful. It appeared from the start that what Trump/the US was doing was nuts. As more time goes by, this thesis is getting proved right. The question is:Wwhere do we go from here? The longer this science experiment runs the worse things are going to get for American’s. Perhaps the real question is how much pain can American’s endure? It looks to me like we are going to find out. What does this mean for stocks? How is anything going on right now good for stocks? The question is: How bad does it get from here? We also know that Trump is a survivor. So there is also a good chance that he changes his mind. if this happens, stocks would rocket higher. Yes, what a crazy set-up.

-

What did I learn from attending Fairfax’s AGM this year? I still have a lot to learn. Guess how much analysts write about Fairfax’s culture in their reports? They don't (other than perhaps a passing mention). Guess how much I have written about culture in my 650 page book on Fairfax? Very little. Yes, I am an idiot. ---------- Looking at all US listed companies, the performance of Fairfax’s share price since 1985 (over the last 39 years) puts it at #8 on the list. Amazing. How did it do it? Because of its culture. Its culture is shining today as brightly as ever. Its culture is its moat - and it is getting wider and stronger with each passing year. ----------- ‘You can lead a horse to water, but you can’t make it drink.’ Fairfax is doing their best to help investors better understand its culture. Below is one example: the comments made at the AGM by Andy Barnard, who is Chairman of Fairfax’s insurance operations: “So of course, we had a fantastic year in 2024, $1.8 billion of underwriting profit. 7 of our companies achieved record underwriting profits during 2024, which we're very pleased and happy and proud to see. “(W)hat I'd like to focus on… is the reasons that we've been able to achieve this success. And I'd like to go back to that slide that Prem shows every year… that shows the tenure of our CEOs across Fairfax because I really don't think there is any more important factor behind our success than what that slide reveals. “Continuity of management is just so vitally important in our industry as it is in many businesses. (B)ut I think it's especially important in the insurance business. It allows us, over time, to build, to grow, to improve our operations. And we do so without the distractions and the disruptions that come from changes at the top. “Now for those of you that might follow the trade press in our industry, you would see amongst many of our competitors, and I'm sort of referring to the global commercial, property and casualty market, which is really the main theatre that we operate in. But for so many of these companies, it's just a revolving door. And it's not just… the CEO. (B)ut it is also many of their key executives. And this creates circumstances that make it very hard for companies to have the stability that enables them to thrive and improve and build and grow over time. “At Fairfax, our decentralized operating philosophy, whereby we keep our company separate and autonomous creates a much more favourable, much more rewarding environment for our CEOs and for their management teams. And it is that environment that allows them to continue to build and grow and improve their operations. And that's what you're seeing in the results that we've been able to achieve at Fairfax. “And so -- we've said this many times. We may say it every one of these meetings, we are so blessed. And this gets better and better every year because of that continuity, but we are so blessed with the remarkable collection of CEOs and leaders that we have running our companies. And again, I don't think there is any more important explanation for the underwriting success that we've been able to achieve. “Prem referred to our moat, the culture of Fairfax being our moat. This retention of employees is really something that is attributable to the unique culture that we've had at Fairfax: supportive, rewarding, empowering. And that's what's enabled us to have this remarkable duration. I would say if you compare us to any of the major companies in that global P&C world. I don't, think you would find anyone with close to the duration of tenure at the top. And not just at the top, at the very top, but also amongst their senior management teams that you find at Fairfax.”

-

Prem’s presentation from Fairfax’s recently held AGM is now available. If you want to get a good overview of the company, this is a great place to start. It clearly demonstrates how well the company is managed and how well it is positioned today. https://www.fairfax.ca/wp-content/uploads/2025/04/Fairfax_AGM_2025.pdf

-

I am watching the condo market in Toronto. Specifically the new-build market. It is now clear that the increase in prices for new-builds from 2015 to 2022 was a bubble. The questions I have: Does the air come out slowly (like it has been) or does the decline get a little more unruly? Does the issues in the condo market impact the larger real estate market? Vancouver has the same issues, just on a much smaller scale. I have been following the guy in the video for the past couple of years. He has been a great resource. He has nailed what has been happening. A generation of new-condo ‘investors’ are in the process of getting cleaned out. They are going to learn the age old lesson: Leverage is a wonderful thing when the bubble is forming. But it is catastrophic/death when the bubble pops. And it is popping for new-builds. The question is if the damage is contained to new-builds or if it spreads.

-

As Canadians cut back on travel to the US, what are they doing? Eating out in Canada more. Reservations at restaurants are up 20%. Who is one on the winners? Fairfax. They own Recipe. With 1,200 locations, it is the largest full-service restaurant company in Canada. It appears Recipe has become a Fairfax holding that is generating a solid amount of free cash flow (C$114 million in 2024). Leverage has come down (the take-private of Recipe in 2022 was largely funded with borrowings at Recipe - similar I think to what Fairfax has done recently with the take private of Peak Achievement). Smart. Fairfax gets a control position of a business it likes. The additional debt taken on to fund the purchase is paid down over time. Rinse and repeat. Over time, Fairfax ends up with a control position in a growing number of businesses that it likes. (AGT Food and Ingredients is another example of Fairfax using this strategy. It was taken private in 2019. In Q1, 2025, AGT sold its rail/infrastructure assets for C$192 million and used the proceeds to pay down debt.) Comments from Prem about Recipe from Fairfax’s 2024AR: “Recipe surpassed its record-breaking system sales in 2023 (adjusted for the 53rd week) with system sales of $3.6 billion in 2024.Revenue was up 0.5% driven by improvements in corporate restaurants and the consumer packaged goods business. The company delivered Cdn$114 million in free cash flow and reduced overall leverage to less than 2x.With a strong underlying business, Frank Hennessey, Ken Grondin and their team are focused on top line growth. Expansion is under way in the United States and Indian markets, complemented by organic growth in Canada from new restaurants.The company will also be launching new products in its already sizable consumer packaged goods business (where Recipe’s brands are sold in grocery stores). Recipe is carried on our balance sheet at 10x free cash flow.” —————- Article from the Globe and Mail As Canadians ditch travel to the U.S., restaurants get a boost https://www.theglobeandmail.com/business/article-travel-boycott-us-canada-restaurants/ “Canadians are saving a bundle by cancelling their trips to the U.S., and one of the big beneficiaries of the travel boycott appears to be restaurants here at home.” “The number of reservations at Canadian restaurants has grown more than 20 per cent so far in April compared to last year, continuing a months-long trend of Canada leading many other countries in restaurant dining growth.”

-

@Txvestor , I am certainly not an expert on shipbuilding. I watched the 20 minute video at the bottom of the link you provided. Here are some thoughts: 1.) The US has a very small capability to build ships today. 2.) What capability it has serves the military - that likely means it is high cost/bloated/ highly inefficient. How long will it take for the US to create an efficient shipbuilding industry? A decade? Longer? Because to builds ships you need to build out the infrastructure - raw materials, energy, suppliers and highly skilled labour. Any ships built in the next few years will likely be small in number and among the highest cost in the world. My guess is that will not make current Chinese ships worth less. These new policies are going to hit immediately. The policies are not well thought out - they are a blunt tool. Some Americans are going to make a killing (follow the lobby money). Some Americans are going to get killed (like workers at the smaller ports who lose volume). Blunt tools = arbitrary outcomes, especially in the short term. Costs to ship goods are going to go up immediately and by a lot. And my guess is it will be US consumers who end up footing the bill. That is what happened with Covid - so it seems reasonable to me to use this as a base case for the current situation. Is it just me… or are significant cost pressures building again in the US economy? These pressures are not cyclical… they are structural. Making America great again is going to be extremely expensive - and it is likely going to slowly play out over many years. —————- One thing to watch might be how the different shipping alliances respond. During Covid, they operated in a cooperative way and made historic amounts of money. With the recent changes in the alliances, we may not get the same level of cooperation - if it gets destructive then that would not be good (for them). So that might be something to watch for. (That is always a risk with an oligopoly.)

-

I don’t have any specific insight into how Seaspan will be impacted by what Trump is doing. There are too many unknowns. So the analysis tends to be garbage in - garbage out. Private: I like the fact that Seaspan is private and not publicly traded - this lets the management team think long term with their decisions. Strong ownership group: I think the ownership group is very strong (financially etc). This is especially important in times like today (lots of uncertainty). Track record: at the beginning of Covid there was a lot of handwringing about how Covid would impact the shipping industry. Seaspan’s business performed better than expected. I will be closely monitoring the situation. Bottom line, we need (much) more information. Covid completely snarled supply chains. The current situation looks pretty nuts (in terms of messing up global logistics). As everyone tries to reroute etc, perhaps demand for containerships will increase (like what happened with Covid). That scenario might be bullish for Seaspan.

-

@SharperDingaan , I think what people are missing is Trump can’t be trusted (I am putting it politely). There will never be an actual ‘deal,’ in terms of what people think that means (and how you wrote). Yes, he will do a ‘deal.’ And then when it suits him, he will demand to renegotiate (he will manufacture a reason and the MAGA crowd will buy it hook line and sinker). It will be a constant state of flux for other countries. The USMCA trade deal with Canada and Mexico is a great example. Trump was the one who actually did that deal and it went into effect in 2020. But Trump has now decided a deal is not really a deal. It is just the next stage in him/the US extracting its pound of flesh. Because it can. It is a completely bizarre way to run a country. It is right out of some third world banana republic (might is right, lies, corruption…). I agree with you. The only way to manage this shit show is to stall and delay. If you negotiate in good faith he will simply view you as weak and keep coming for more. Trump is a predator. He eats. He is never satiated. Welcome to the new USA. (And many Americans wonder why the rest of the world is getting so pissed. They view the T-Rex is the victim in their world.)

-

+1. @73 Reds , I have always enjoyed our interactions. I respect your approach a great deal. When I post, sometimes I am talking about a topic. Other times I am talking to myself. Sometimes both. Board members need to keep this in mind

-

@Castanza , good for you. Love it. We all need to find out 'happy place.' Having a 33% cash weighting allows me to do the same thing. Cheers!

-

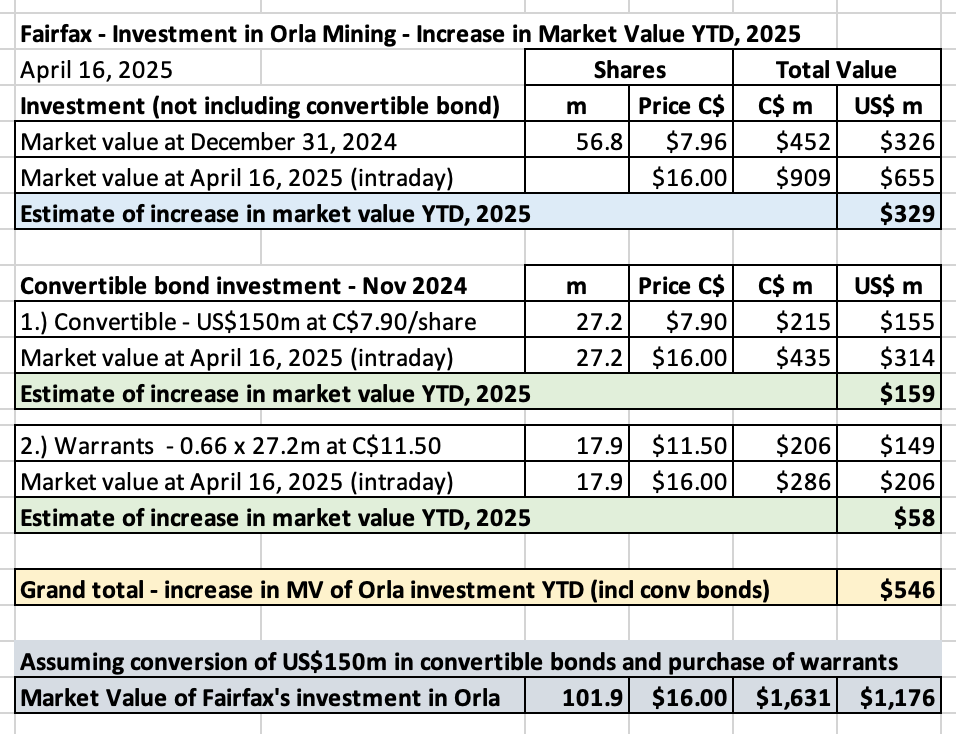

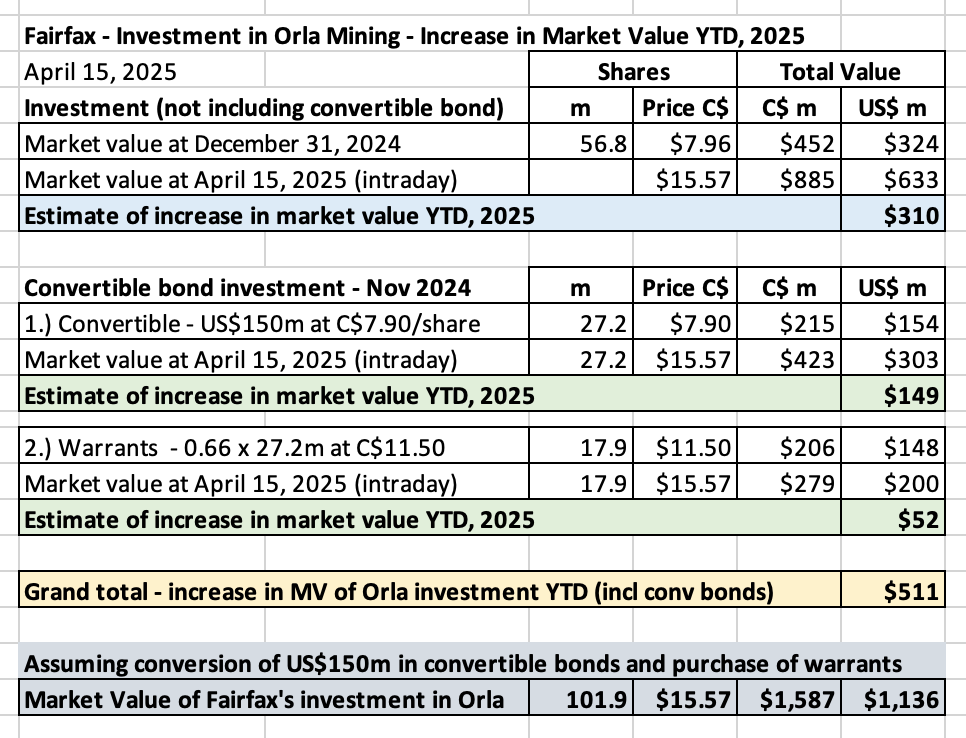

@73 Reds , my view is the tail risks to lots of things are getting wider. It doesn't mean bad things are going to happen... it just means the risks of bad things happening are increasing. My solution, as I have said before, is to increase my cash weighting. Fairfax is the only single stock I hold today. I continue to think they are well positioned in the current environment. For Fairfax, some of the tailwinds / headwinds are shifting. I have posted on Orla Mining recent... the market value of Fairfax's position is up about $550 million YTD 2025 - that is a clear tailwind. The cratering of the US$ is also an emerging tailwind for Fairfax (book value more than earnings), likely in the hundreds of millions (rough guess). So I will continue to monitor things. Today my portfolio is about 33% cash, 33% Fairfax and 33% broad based index/ETF's (largest weighting XEQT). I consider Fairfax to be a pretty defensive holding. So about 33% of my portfolio is directly exposed to equity markets. My total return in 2025 is about 1% as of today. I consider myself lucky to have escaped most of the carnage so far (thank you cash and Fairfax). There are times when preservation of capital is more important than return on capital (look at the 1970 to 1975 period). I think we might be in one of those times. Having said all that, if equity markets continue to sell off I likely will buy equities. I am not a permanent bear. I am just trying to be rational and navigate my family's finances through the rapids. Like I have said many times before, I do not need any more money. My primary risk is me - that I do something stupid that blows up my portfolio. Like underestimating the damage that Trump might do to the global/Canadian economy and financial markets. If something bad happens, that will be on me - not Trump or any of his policies. I take responsibility for my situation - I am not a victim. (Perhaps that is why I keep writing the same stuff on Trump - it is intended as a warning to me and what I might be inclined to do in more normal times.) ---------- Life stage is an important overlay. If I was younger (with a day job and owning a primary residence), I would likely be leaning out more on the risk spectrum.

-

Well, this is certainly not going well for anybody - poor, rich, American, non-American. Extreme volatility in financial markets is NEVER a good sign. If it continues something will break. This science experiment is quickly going from bad to worse - the US is starting to learn that moving to a centrally planned economy can be a bitch (it doesn’t work). The problem is how do you put out a fire when you put the arsonist in control? The answer, of course, is you can’t. Once it gets raging, it will probably need to burn itself out (the MAGA crowd is acting like dry kindling). Just ask Jasper, Alberta how well that goes. What a crazy set-up. This shit show is going to make poor American’s better off? Does anyone seriously believe that anymore? Strap in boys and girls, this ride is just getting started. Unbelievable. We are living in one of those times that people will talk about in decades to come. They will be asking a simple question ‘what were they thinking?’ PS: This is not to suggest that there were not serious issues that needed to be addressed. But throwing the baby out with the bathwater is idiotic. And that is what we are slowly learning.

-

Orla Mining - OLA.TO - Planting a Seed Below is an update on Orla Mining. At $1.2 billion, this holding has quickly become Fairfax's 4th largest equity holding. What can we learn about Fairfax from this investment? That is one of the things we will explore in this post. ————— Orla’s share price has been on fire over the past 6 months. What is going on? Gold is viewed as being a hedge against two things: Uncertainty Inflation Today, we have both. So, it is not surprising that the price of gold prices has been ripping higher. And we should not be surprised that the share price of Orla has also been ripping higher. Where do we go from here? President Trump is just beginning his second term. My guess is high uncertainty will likely be with us for at least the next 3.5 years. Tariffs are a central part of President Trump’s economic plan. Tariffs are inflationary. My guess is inflation will continue to be elevated (around 3%?) for the next few years. Bottom line, the bull market in gold we are currently experiencing could continue to run for a couple more years. If this happens, Fairfax’s investment in Orla could just be getting started. ————— Experience matters Yes, Orla is looking like a terrific investment for Fairfax. But there is a bigger lesson to be learned from Orla. Fairfax has a very seasoned investment team at their corporate office and at Hamblin Watsa. Some on the team were around in the 1970’s and 1980’s – the last time we were in a protracted inflationary environment like today. That experience likely led Fairfax to initiate their investment in Orla back in late 2022. In the current environment (high uncertainty and persistent inflation), experience matters more than ever. Fairfax looks very well positioned to not only survive – but also to be able to thrive in the current environment. Having that experience/capability is a big benefit for Fairfax (and its shareholders). Investments like Orla are real-life examples of this capability and the benefit it provides. ————— Orla Mining is Fairfax’s newest large resource/commodity type of investment. Shares were acquired from Q3-2022 to Q3-2024. In November of 2024, Fairfax purchased $150 million in convertible bonds (with warrants) as part of Orla’s acquisition of the Musselwhite mine. Orla is a gold miner and gold prices have been moving higher over the past year (spiking higher in recent months). Orla’s share price has also spiked higher from C$7.96 at December 31, 2024 to C$16.00 at April 16, 2025 (intraday, as I update this post). How has Fairfax’s investment performed YTD in 2025? YTD 2025, Fairfax’s position in Orla has increased in value by about $546 million. The convertible bond investment is looking especially well timed (made in November 2024). Including the convertible bonds and warrants, Fairfax has exposure to 101.9 million shares of Orla. At April 16, 2025, this holding had a market value of $1.176 billion. Orla has become Fairfax’s 4th largest equity holding. How has Fairfax’s investment in Orla performed since inception? At April 16, 2025, Fairfax’s investment in Orla is up about $656 million, or 125%. That is a pretty crazy return given: Fairfax only started building a position in Orla in Q3, 2022. Fairfax materially added to their position in November 2024 (6 months ago). The play with this investment: That gold prices stay higher for longer. That the management team at Orla is above average. And will be able to expand the company from a single asset producer to a multi asset intermediate-sized gold producer. That the strong ownership structure (Fairfax, Newmont, Pierre Lassonde, Agnico Eagle) will be a competitive advantage. This allows the management team at Orla to be strategic and think long-term with its decisions. This should help ensure that the capital allocation decisions made by the management team at Orla are rational and shareholder friendly. With its investment in Orla, Fairfax has planted another seed in its large equity portfolio. In a very short time period this investment has already turned into another home run for Fairfax. It will be interesting to see in the coming years if the price of gold can continue its improbable march higher. ————— On November 18, 2024, Orla made a large acquisition – they purchased the Musselwhite gold mine in Canada from Newmont Mining. As part of the financing, Fairfax invested US$150 million in convertible bonds: Coupon: 4.5%; Term: 5 years Convertible at C$7.90 18-month non-call, callable at 130% of strike thereafter Warrant: 0.66x warrant exercisable at C$11.50 – Five-year term from closing The purchase of Musselwhite looks like another solid move by the Orla management team. There appears to be significant optionality to the purchase (significant opportunity for resource growth, which is part of the Pierre Lasonde playbook). At November 18, 2024, Orla’s stock closed at C$5.99/share. At April 16, 2025, Orla’s stock traded at C$16.00/share. Orla’s share price is higher than both the conversion price for the convertible bonds (C$7.90/share) and the exercise price for the warrants ($11.50/share). Who is Orla Mining? Orla Mining Ltd. is a Vancouver-based company that acquires, explores, develops, and operates mineral properties to produce gold, silver, zinc, lead, and copper. Company’s website: https://orlamining.com/investors/ Company Presentation (March 2025): https://wp-orlamining-2024.s3.ca-central-1.amazonaws.com/media/2025/03/Orla-Corporate-Presentation-March-2025.pdf Orla Mining's projects include: Camino Rojo: A 100% owned, operating oxide heap leach mine in Zacatecas, Mexico South Railroad: A feasibility-stage heap leach project in Nevada Cerro Quema: A pre-feasibility-stage heap leach project in Panama Musselwhite Gold Mine: An acquired project in Ontario, Canada CEO: is Jason Simpson, who has over 27 years of experience in mining engineering, project construction, and operations leadership. Non-Executive Chairman, Director: Mr. Jeannes served as President and Chief Executive Officer of Goldcorp Inc. from 2009 until April 2016. ————— Bet on the jockey/partnering with outstanding investors It should be noted that Fairfax is not blindly throwing darts with their resource/commodity investments. They are partnering with other highly successful people / investors - some of whom have extraordinary long term track records. With Orla, Fairfax is partnering with Pierre Lassonde who is ‘recognized as one of Canada’s foremost experts in the area of mining and precious metals.’ Lassonde co-founded Franco-Nevada in 1985. Fairfax is also partnered with Pierre Lassonde and Agnico Eagle with its investment in Foran Mining, a copper mining project in Canada. Jurisdiction: The vast majority of the production for Fairfax’s resource/commodity investments is located in North America. This is a much lower risk jurisdiction than other parts of the world. My guess is this is not a fluke. All of Orla’s mines are located in North America. ————— Comments from Prem about Orla Mining from Fairfax’s 2024AR. "Orla Mining, run by Jason Simpson and his exceptional team, had a transformative 2024. In November, Orla announced the acquisition of the Musselwhite gold mine in Ontario from Newmont. Fairfax participated via a $150 million investment in convertible bonds (4.5% coupon, Cdn$7.90 conversion price and 0.66 of a warrant with a Cdn$11.50 per share exercise price). Musselwhite is a low-cost, long-life asset in one of the best mining jurisdictions in the world. The addition of Musselwhite will more than double Orla’s annual gold production to approximately 300,000 ounces a year. Orla’s Camino Rojo open pit mine in Mexico continues to perform extremely well, producing approximately 137,000 ounces of gold in 2024. Exploration activity at Camino is indicating the viability of an underground mine at the site with attractive economics. Lastly, progress continues to be made in permitting their South Railroad mine in Nevada.South Railroad is likely to be a low-cost mine with high free-cash flow. Orla generates attractive levels of free cash flow and has ample liquidity to fund its development and exploration activity. Orla is carried at its listed price of $5.47 per share (Cdn$7.87) or $311 million." Prem Watsa – Fairfax 2024AR

-

Driven by uncertainty and inflation fears, gold continues its improbably run higher. Who was smart enough to buy gold stocks 2 years ago? Yes, Fairfax was. Their stake in Orla is now up +US$500 million YTD-2025. Yes, not too shabby. Orla now has a market value of $1.136 billion. My guess is their cost basis is a little over $500 million. This puts the total return on this investment at about $600 million in less than 2 years (+119%). See the second chart below. That is nuts. They sold Resolute Forest Products in 2022 at the top of the last lumber cycle at a premium valuation. They sold Stelco in late 2024 at a bubble-high price. Their recent investment in Orla (they started building out their stake in 2023), a gold producer, has more than doubled in value in less than 2 years. They own a large piece of a copper mine that will begin production later in 2025. Active management is back. And Fairfax has been putting on a clinic the past 5 years. Can't wait to see what they do in the coming years. $ORLA $OLA.TO ---------- ----------- What is going on with gold today makes me think back to a Conan skit... Raffi knows - Gold is best!