Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

@Hamburg Investor, great long term analysis of Fairfax’s insurance business. I agree with your finding - Fairfax’s insurance business has improved in profitability over the past 15 years or so. Andy getting put in charge of the group in 2011 was likely a catalyst. There is a lag from writing good business to when it actually shows up on the bottom line - depending on the line, it can be many years. (The opposite is also true.) It will be interesting to see what CR Fairfax is able to deliver in the coming years. I continue to think Fairfax’s insurance business is better than most investors think. And i also think future reserve releases could be robust (and not built into the stock price today). We will see. Of course why this matters so much is two things drive value creation at Fairfax - the return it earns on its: Insurance business Investment management business Both have NEVER been doing well at the same time. Except for the past couple of years. Not surprisingly, the value creation has been very strong.

-

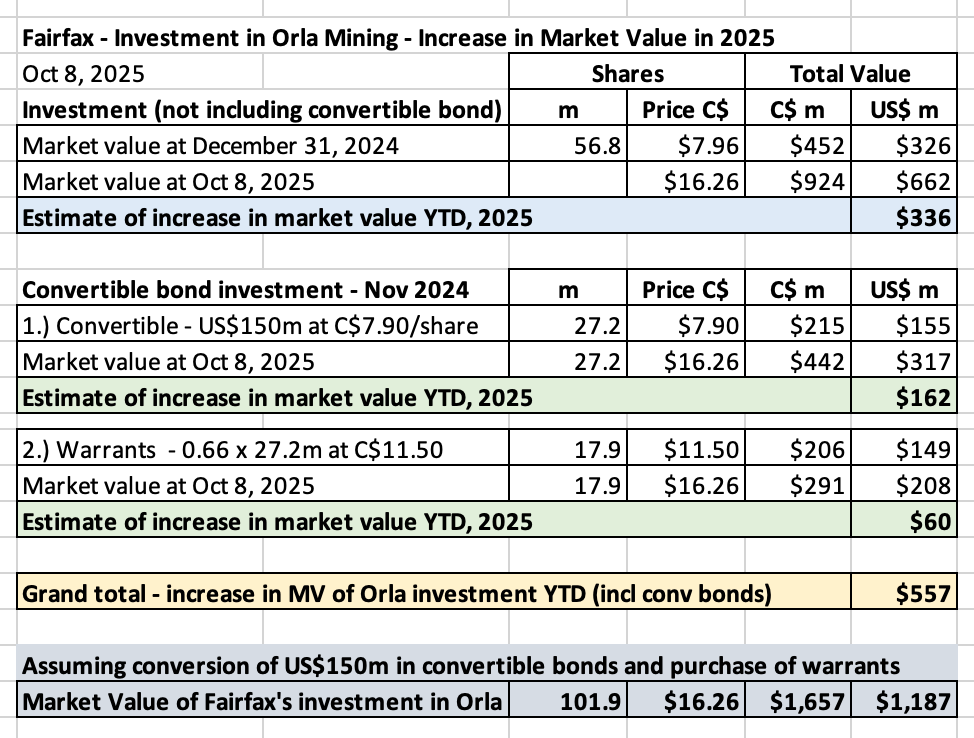

@Txvestor, here is the build I use for Orla. Looks like you aren't including the warrants. YTD, Orla is up $557 million. And it looks like gold is starting to go mainstream (as an investment). Jeff Gundlach (Doubleline) recently said he thought having a weighting for gold in a portfolio of 25% was appropriate. The yellow metal just passed US$4,000 an oz. If retail investors decide to get in on the action we could see a gold rush in 2026.

-

@cwericb, I think we can say with certainty that Canada just experienced the greatest housing bubble in history (from 2000 to 2022, but especially 2015 to 2022). Of course anyone who owned real estate won the proverbial lottery. Fortunately, I was one of them. But personally I look at my oversized real estate winnings as blind luck. And i will gladly take the win. My view is it is possible to see bubbles as they are blowing. But I also think it is impossible to call when a bubble will finally meet its end (and how it ends… with a pop or if the air comes out slowly).

-

I agree. Looking at it strictly from an investment perspective, a person in Vancouver or Toronto is likely better off renting (than owning). Residential real estate strictly from an investment perspective has been messed up in Vancouver/Toronto for at least a decade. It has been cash flow negative. It was all about capital appreciation. Which technically makes it a speculation and not an investment. Regardless, fortunes were made in the boom years (2010 to 2022). Today we have falling house/condo prices. To make matters worse we also have falling rents. And rising costs: property taxes, condo fees and insurance. Mortgage rates have also normalized at a higher level (compared to rates available pre-2022). When you are already cash flow negative, lower revenue and rising expenses = even more cash flow negative. And markets like Vancouver have rent controls - with the maximum allowable rent increase tied to inflation. The maximum allowable increase in 2026 is 2.3%. Canada has also reversed (for now) policies on immigration, foreign workers and international students. I think it just saw its population decline (for the first time ever?). No population growth is not good for landlords - vacancy rates are rising. Many ‘investors’ are bleeding cash. And watching the value of their property drop - with no sign of a turnaround. Not a great combination. As a result, many investors are selling their investment properties. That is a big reason listings (inventory) is so high today. Yes, this will all reverse. And probably quicker than most think today.

-

The housing market in Canada bottomed out in 2000 (from a price perspective). For the next 22 years it went higher - much higher. It reached its blow off top in Feb/March of 2022. For the past 3.5 years prices have been coming down. As much as 35% (in real terms) in parts of Toronto (suburbs) and about 20% in Vancouver. Much of Canada has more resilient (down a little?). Of course, there is no ‘housing market’ in Canada. Rather, there are many regions. And many different segments (single family, duplex, townhouse and condo/apartment). Each region/segment has its own thing going on. In very general terms, it appears Canada is getting its much needed housing correction. In some segments, like condo’s in Toronto, we might see a crash of sorts. A slowing economy and a steady increase in the number of listings is fighting with lower mortgage rates. A slowing economy/rising inventory levels appears to be winning. The following video is a great summary of where Canada’s housing market is at. With some interesting comments on where it might be going. Personally, I rent today. And I am a very happy renter (have been for the past 4.5 years). But if prices keep coming down where I live that might change. So I am interested to see where the real estate market goes from here.

-

Good news from Orla today. It appears they may have discovered more gold at Musselwhite. Fairfax has exposure to about 102 million shares of Orla. Stock is up US$1.10/share, which is a $110 million gain for Fairfax. ----------- Orla Mining Discovers Potential Two-Kilometre Extension at Musselwhite https://ca.finance.yahoo.com/news/orla-mining-discovers-potential-two-100000085.html VANCOUVER, BC, Oct. 6, 2025 /CNW/ - Orla Mining Ltd. (TSX: OLA) (NYSE: ORLA) ("Orla" or the "Company") announces major exploration success at the Musselwhite Mine in northwestern Ontario, with drilling confirming a potential two-kilometre extension of the mine's main gold trend beyond current resources. ...Resource Growth: With greater confidence in expansion potential, Musselwhite will be positioned to pursue opportunities that increase throughput, enhance gold production, and extend mine life significantly beyond current projections.

-

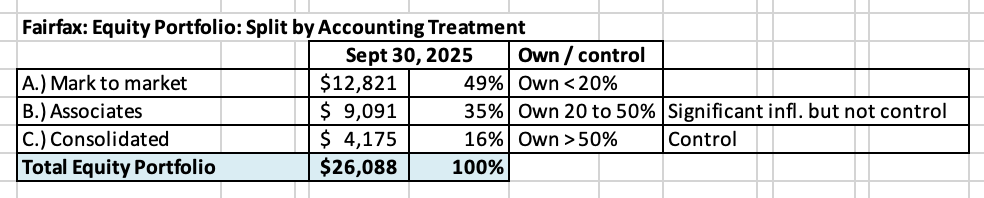

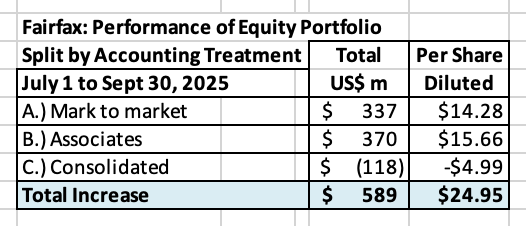

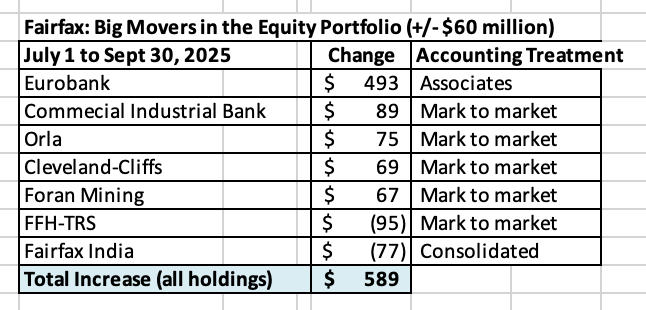

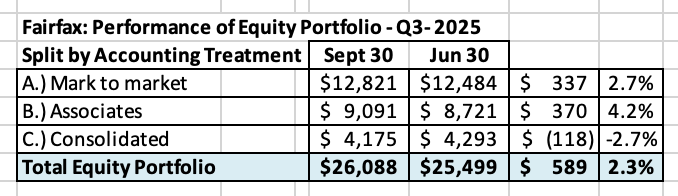

Estimate of change in MV of Fairfax’s equity portfolio in Q3-2025 A warning. When looking at Fairfax’s equity holdings, what matters to investors is the underlying business performance achieved by the holdings over time. Not the quarterly change in market value. Short term (quarterly) changes in market value will be volatile. As a result, short term (quarterly) changes in market value should be viewed with an appropriate amount of scepticism by investors. So why track quarterly changes? Because it is interesting. And it can provide some insight into one of Fairfax’s large income streams - investment gains (losses) - prior to the release of quarterly earnings. Importantly, over time (like a couple of years), the change in the market value of Fairfax’s equity holdings should roughly match the change in their intrinsic business value. ----------- In Q3-2025, Fairfax's equity portfolio increased in market value by about $589 million (pre-tax), or 2.3%. This does not include: The realized gain from the sale of Praktiker in Q3 ($75 million?). Any gain from the spin off of the Keg from Recipe in Q3. Fairfax's equity portfolio has performed very well in 2025: In Q1-2025, the increase in MV was $785 million (pre-tax), or 3.5%. In Q2-2025, the increase in MV was $1.96 billion (pre-tax), or 8.5%. This puts the 9 month increase in the equity portfolio at about $3.4 billion. At September 30, 2025, Fairfax’s equity portfolio had a total value of about $26.1 billion. Notes: Included in our estimates are details from Fairfax’s Q2-2025 interim earnings report and 13F report. The FFH-TRS position is included in the mark to market bucket and at its notional value (this position has a market value of $3.1 billion). Convertible bonds, warrants and debentures are also included in the mark to market bucket. Digit: My tracker does not include Digit, Fairfax’s publicly traded P/C insurance company in India. Part of Fairfax’s ownership position in Digit is market to market. Digit’s shares were down a small amount in Q3. Currency: US$ weakness has been a tailwind for Fairfax in 2025. Where the benefit shows up in reported results is a little complicated (net income or OCI). The ‘tracker portfolio’ is not an exact match to Fairfax’s actual holdings. It is useful only as a tool to understand the rough change in value of Fairfax’s equity portfolio (and not the precise change). Split of holdings by accounting treatment About 49% of Fairfax’s equity holdings are mark to market - and will fluctuate each quarter with changes in equity markets. The other 51% are Associates and Consolidated holdings. Split of total gains by accounting treatment The total change is an increase of about $589 million = $25/diluted share (pre-tax) The mark to market change is an increase of about $337 million = $14/ diluted share. What were the big movers in the equity portfolio in Q2, 2025? Eurobank continues its exceptional run in 2025 (and the past 5 years). Other strong performers in Q3 were Commercial Industrial Bank (Egypt), Orla (gold miner), Cleveland-Cliffs (steel producer), Foran Mining (copper start-up). The biggest laggards were FFH-TRS (Fairfax’s shares were down 3% in Q3) and Fairfax India (normal volatility). Excess of fair value over carrying value The excess of FV over CV for non-insurance associate and consolidated holdings is about $2.68 billion or $114/diluted share (pre-tax). This was $1.5 billion at December 31, 2024. This is up significantly in 2025. The 'excess of FV to CV’ has been materially increasing in recent years. This is economic value that has been created by Fairfax that is not captured in accounting results (earnings or book value) – it is one good example of how EPS and book value is understated at Fairfax. (Note, the carrying value we use in our tracker for associate and consolidated holdings is from June 30, 2025 so our excess number will be a little high). Excess of FV over CV = $2.68 billion = $114/share (diluted and pre-tax) Associates = $2.0 billion = $85/share Consolidated = $0.7 billion = $29/share Equity Tracker Spreadsheet explained: We have separated holdings by accounting treatment: Mark to market Associates – equity accounted Consolidated Other Holdings – total return swaps and warrants/debentures The value of each holding is calculated by multiplying the share price by the number of shares. All holdings are tracked in US$, so the values of non-US holdings have been adjusted for currency. This spreadsheet contains errors. It also contains some information that is dated (like the carrying value for associate and consolidated holdings). Please keep this in mind. The spreadsheet is updated as new information becomes available.

-

@Txvestor, when looking at the average duration of Fairfax's fixed income portfolio I think it is important to consider both the potential impact of changes in interest rates on both the income statement and the balance sheet. Fairfax is also a value investor... that is another important overlay. There is a very real possibility that Trump's policies are going to spike inflation in the coming years. After all, financial repression is how you solve a too much debt problem (an emerging problem for the US government). And Trump is very unconventional - he will not hesitate to throw bond holders under the bus if he thinks he can get away with it (remember, he is a real estate guy).

-

@Hoodlum, this is a very interesting development. Fairfax has been quite active with its Recipe investment in 2025: Increased ownership in Recipe to 100%. Increased ownership of The Keg to 100%. Purchased Canadian rights to Olive Garden. The first two transactions gave Fairfax 100% ownership/control of Recipe and also 100% control/ownership over all of its restaurant banners. From Recipe’s web site: “Recipe Unlimited Corporation is Canada’s leading full service restaurant company. We are a nationally recognized franchisor of choice with 1200+ restaurants located in more than 300 communities across Canada, including many international locations. Home to such iconic brands as Swiss Chalet, Harvey’s, St.Hubert, Montana’s, Kelseys, Bier Markt, East Side Mario’s, Landing Group, New York Fries, The Pickle Barrel & Catering, State and Main, Elephant and Castle, Original Joe’s, The Burgers Priest, Fresh, Blanco Cantina and Añejo.” What banner is missing from this list? The Keg. It appears we have our 4th transaction of the year involving Recipe. Spin off of the Keg out of Recipe, partnering with LFG Growth Partners/Richard Jaffray This is super interesting. My guess is the Keg might have been Recipe’s largest banner (in terms of system sales). The Keg has 105 restaurants. The segment they service is casual upscale. My guess is there are two angles to this transaction: 1.) Surfacing value / monetizing an asset It will be interesting to get details of the transaction: What is the ownership split between Fairfax and LFG Growth Partners? Who is the majority partner? Enterprise value: What is the value of the Keg as a standalone company? Does the transaction surface any value for Fairfax? Do we see a realized gain when Fairfax reports results in Q3? Capital structure: What is the equity / debt split? With recent take private transactions at Fairfax, we have seen a large amount of the purchase price come from the issuance of debt that is held at the operating company (that is non-recourse to Fairfax). Is this transaction largely a cash out for Fairfax? 2.) Partnering with an entrepreneur. Partnering with outstanding founders/entrepreneurs has been a consistent theme at Fairfax in recent years. Jeffrey Jaffray’s claim to fame is that he co-founded Cactus Club and built it into one of the leading casual fine dining brands in Canada. He exited Cactus Club in 2022, selling his stake to his partners (the Fuller family, who also own Earl’s). https://www.cactusclubcafe.com/our-story/ Sale of Cactus Club (2022) https://www.biv.com/news/hospitality-marketing-tourism/earls-owners-acquire-100-stake-cactus-club-8266770 Who is LGF Growth Partners? It looks to me like LGF Growth Partners is a very different animal than Recipe. LGF is much, much smaller. Focussed on the fine dining segment. And is much more entrepreneurial. From the company’s web site: “LFG Growth Partners is a team of leaders, founders, and go-getters driving growth in the hospitality industry. We build and scale brands that are inspired by culinary excellence, strategic innovation, and world-class service. “Founded and led by Richard Jaffray, a nationally-recognized entrepreneur and visionary, LFG brings together a team of industry leaders with decades of experience across operations, culinary arts, finance, real estate, and design. “At LFG, we believe people are the heart of every success story. We seek out greatness — in the partners we invest in and in the talent within our own team. As hands-on collaborators, we bring deep operational insight, strategic thinking and an entrepreneurial mindset to help our partners build on their success. Our growing portfolio of celebrated concepts include” Conclusion We should get more details on the spin out of the Keg as a stand alone company at Fairfax when the company reports Q3 results in late Oct/early Nov. Based on the small amount of information we have received so far, I like it. Fairfax has done a very good job in recent years with their capital allocation decisions - my guess is this has the potential to be another good one.

-

I do want to applogize to @petec and @Munger_Disciple for my comment. I like to be edgy… but I think this one crossed the line

-

@Munger_Disciple, thanks for answering my question. 1.) I am more optimistic on the underwriting front. Clearly, the hard market is slowing. But a slowing market is still a pretty good market. Having said that, there also is no one ‘insurance market’ - rather there are many insurance markets (by line of business and geography). Fairfax’s global, diversified footprint will allow them to find profitable niches to grow in. Also importantly, I think there is a good chance reserve releases could surprise to the upside in the coming years. If so, we could see Fairfax’s reported CR not only remain around 95 but actually go lower. 2.) On interest rates, I am in the higher for longer camp. Trump will do everything he can to lower short term rates. But there is a good chance his actions may spook the bond market and send longer term rates higher, giving Fairfax an opportunity to extend their average duration. Regardless, short term rates are coming down because of economic weakness… when the economy picks up my guess is short term rates will move higher again. And if inflation picks up, short term rates could move much higher. In terms of interest income, two things matter: average interest rate and size of fixed income portfolio. The fixed income portfolio is growing in size by more than 5% per year. At the same time, Fairfax is very conservatively positioned (mostly government bonds). As we learned with the KW/PacWest and Blizzard investments, Fairfax has options to shift part of the portfolio to higher yielding investments. Bottom line, there will be puts and takes to interest income moving forward. I am not expecting a big move in either direction (down or up) from current levels. 3.) The non-insurance consolidated bucket of equity holdings is poised to grow in size. Yes, I have been saying this for years. And it is the smallest income stream. But all big things start small. 4.) Reinvestment opportunities. There are so many things they can do here to drive incremental earnings/economic value. My guess is they buy out their minority partners in Allied World later in 2025. That will be a significant investment ($1 billion?) at a low price in a great business. Perhaps they take out their minority partner in Odyssey in 2026 ($900 million?). These investments boost the share of net earnings that accrue to Fairfax shareholders. 5.) Hidden value. I am also of the opinion that Fairfax has been building an enormous amount of hidden value since 2018 in many of their equity holdings. This is a big benefit of all the improvements they have driven into their equity portfolio (dramatically improving its overall quality). Quality equities are compounding machines - but it takes 5 or more years to really notice. We are there (in terms of lots of value already having been created). Excess of FV over CV for non-insurance associate and consolidated holdings is a large and obvious bucket - and it has been growing nicely each year since 2020 and is blowing out in 2025 (due to Eurobank). But there is more examples of hidden value creation at Fairfax than just this bucket of holdings. Fairfax will have a steady flow of large realized gains as it surfaces value from its equity holdings in the coming years. These will boost EPS, BVPS and ROE. When they happen, most investors will be surprised. Sigma is a good example of this in 2025. My guess is Praktiker will be a small but solid gain - we will find out when Fairfax reports Q3 results. There are many more of these coming in the future… and some really big ones (Eurobank). 6.) Exploiting volatility is in Fairfax’s DNA. My guess is volatility is not dead. And Fairfax will get many opportunities to exploit Mr. Market in the coming years. And now they are all cashed up. Look what they did in 2020/2021/2022 when they were cash poor? Do I know exactly what they are going to do? No. Do I need to know? No. But when they happen these investments will be needle movers. They are not baked into analysts estimates/expectations of investors. So they are not built into the stock price. Its like getting a really valuable call option for free. Summary For all the reasons listed above, I do not buy into the ‘cyclically high earnings’ argument. Again, it sounds right/kind of makes sense - and might apply to most P/C insurance companies. I just don’t think it applies to Fairfax today.

-

@Munger_Disciple, I do appreciate the push back. At the end of the day, we are all trying to better understand our investment in Fairfax. Having the opportunity to debate with others is a big help. i have a question, how do you define ‘cyclically high earnings’?

-

This line of thinking sounds smart... but I think it is missing the point. I have a simple question. Think back to 1980 and 1990's version of Berkshire Hathaway. Was the right way to think about BRK back then to 'not capitalize cyclical earnings too far into the future.' And I don't think anyone on this board is saying 'since the current ROE is so high, it should trade at a (big) x times book.' People have been calling for earnings at Fairfax to 'normalize' (at a much lower level) for each of the past 4 years. And they have been dead wrong. What are they missing? IMHO, they are missing the essence of what is really going on at Fairfax today. What has me excited about Fairfax today are three things; The significant amount of free cash flow they are current generating. The significant number of opportunities they have to reinvest this cash flow at high rates of return (the platform they have built, the skills they have developed and how well they are executing). The power of compounding. My view continues to be that 'the story' at Fairfax keeps shifting in important ways - it continues to get better. I think we are just entering the 'compounding' phase of the story. As we learned with BRK back in the 1980's and 1990's, that is the most exciting phase for an investor. And the best part is the stock is cheap. At $1,725, it is trading at 1.45 x Sept 30 BV (my guess is $1,200). But this does not include excess of FV over CV = $100 after tax. Including this Fairfax is trading at 1.33 x Sept 30 adjusted BV ($1,300). Intrinsic value is higher than my adjust BV number. This puts Fairfax's valuation well below other P/C insurance peers. So you get the best performing / best positioned company at the lowest valuation. What not to like?

-

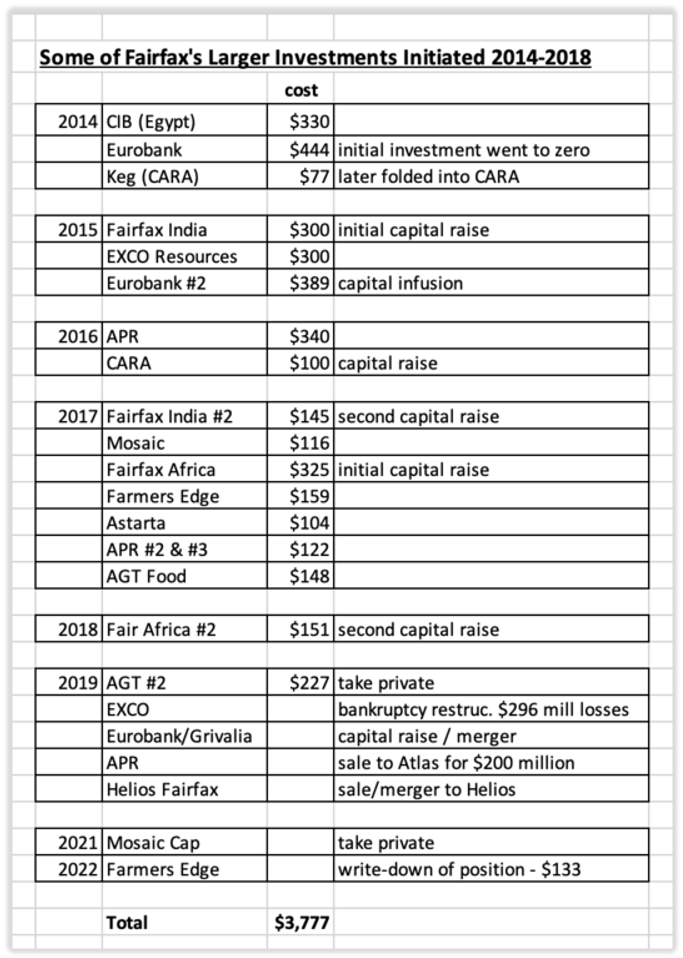

@petec, I love it when others disagree with me. I have moved more in your general direction. But I continue to think that Fairfax is a very different company today than it was in 2018. All three parts of the business/organization are making better decisions and as a result the performance of the company is much better: Senior management P/C insurance Investment management On the investment management front, here is a post that I wrote a while back reviewing many of their large investments from 2014-2017. Boat Rocker could be added to this list. (I didn't discuss large legacy investments like Blackberry and Resolute Forest Products). This list is how Fairfax was thinking and executing on the capital allocation front from 2014 to 2017. It is a shit show. Many of these companies had terrible management. Many had terrible balance sheets (they needed bailouts from Fairfax to keep the lights on). Other large shitty investments like Blackberry and Resolute Forest Products I did not include on my list because they were legacy investments. Now look at Fairfax's collection of equity holdings today. Most of these companies have good/great management. And they have strong balance sheets (the exceptions in recent years were Farmers Edge and Boat Rocker... investments from the 2014 to 2017 vintage). Fairfax has spent the past 7 years fixing all of the problem children. And the new investments made since 2018 have been good to outstanding. Their hit rate from 2014 to 2017 was terrible (Fairfax India being a notable exception). And Eurobank has transformed into a wonderful investment. Their hit rate on investments made from 2018 to today has been stellar. My view is something changed at around late 2017/early 2018 at Fairfax. They recognized they were not staffed to be a turn around shop. They changed their investment framework. They put a premium on: Management quality Fiscal responsibility (Fairfax would no longer be a piggy bank for bad businesses). It has taken Fairfax 7 years of hard work to clean up all of the messes (the Boat Rocker clean-up just happened). My view is there has also been changes in the P/C insurance business. Not as much as what has happened in investment management. A big part of run-off was sold (the good part). Fairfax has reduced its exposure to catastrophes. Reading the book Once and Future C&F I was struck by how long it takes to change an insurance business (more than 5 years). My thesis is Fairfax's insurance business is better today than it was in 2017... I just don't know how to explain it (yet). (And I don't know how much better...) This is really important because - if I am right - we have not seen this version of Fairfax before. =========== A Review of 2014 to 2017: Old Fairfax – too many ‘chronically-leaking boats’ April 14, 2023 “My conclusion from my own experiences and from much observation of other businesses is that a good managerial record (measured by economic returns) is far more a function of what business boat you get into than it is of how effectively you row (though intelligence and effort help considerably, of course, in any business, good or bad). Some years ago I wrote: “When a management with a reputation for brilliance tackles a business with a reputation for poor fundamental economics, it is the reputation of the business that remains intact.” Nothing has since changed my point of view on that matter. Should you find yourself in a chronically-leaking boat, energy devoted to changing vessels is likely to be more productive than energy devoted to patching leaks.” Warren Buffett – Berkshire Hathaway 1985AR Fairfax’s equity portfolio looks very well positioned today. Most of the equity holdings purchased since 2018 have been performing well. And, after years of hard work, the poor performing equity holdings (many purchased from 2014-2017) have largely been fixed and are now performing well. In fact, the equity portfolio looks better positioned today than at any other time in Fairfax’s recent history. We are increasingly seeing the benefits in improved reported results. A good recent example is ‘share of profit of associates,’ which spiked to more than $1 billion in 2022; the previous high was $402 million in 2021. What happened? Three things: 1.) Fairfax learned a few important lessons from the poor purchases they made from 2014-2017. It looks me like Fairfax has tweaked the methodologies used when allocating capital. · They are putting a premium on management. Hamblin Watsa has decided it is not a turn-around shop - looking to actively run poorly lead/challenged businesses. · They are also looking to invest in better balance sheets. Fairfax is no longer a piggy bank for poorly run companies in search of cash. Others on this board have pointed this out. 2.) The Fed and the ending of easy money (zero interest rates/QE) is likely a driver of the stronger performance the past two years of Fairfax’s equity holdings. Value investing is back. 3.) The timing of the cycle is finally working in Fairfax’s favour and is driving stronger performance of the equity holdings. Value, resource, and commodity stocks appear to be in a secular bull market. At the end of the day, all the above is likely partly responsible for the improvement we have seen in Fairfax's equity holdings in recent years. ————— It can be instructive to look into the past so we can learn. This helps us understand what has been baked into past results. In turn, this can help us understand what might happen in the future. What happened with the purchases from 2014-2017? A total of 10 investments are reviewed below. Fairfax invested a total of about $3.5 billion in these investments over the years. Over the past 8 years my math says Fairfax booked losses of about $1.5 billion on these holdings. That is almost $200 million, on average, each year. For example, in 2022, Fairfax wrote down its investment in Farmers Edge by $133 million. Stuff like that. The bigger cost to shareholders has been the opportunity cost. Prem tells us that Fairfax expects its equity investments to deliver returns of 15% per year. Applying a more modest 10% target, the $3.5 billion in investments (made 2014-2017) should have doubled in value by now to $7 billion. The opportunity cost of the poor investments made from 2014-2017 is likely an additional $2 billion. This is actually a good news post. The good news is: 1. The equity purchases made from 2018 to April 2023, as a group, look very good and are performing well. 2. As I will review below, the problem investments from 2014-2017 look like they are not only fixed - they are also poised to deliver solid returns for Fairfax shareholders moving forward. An 8 year-long headwind has now become a tailwind. As a result, I expect Fairfax’s $16 billion equity portfolio to generate a higher total return (percent and absolute) in the coming years than it has delivered over the last decade. Given its current construction, it could well compound at 12% over the next couple of years = $1.9 billion/year: dividends = $120 million share of profit of associates = $900 million consolidated earnings = $240 million mark-to-market investment gains = $650 million (not including fixed income) —————- Below is a short review of 10 large investments made over the 4 years from 2014-2017. 1.) EXCO Resources (2015): Fairfax’s initial investment was $300 million in 2015. We have since learned that shale was a bubble and it eviscerated something like $5 billion in capital up until 2020. Fairfax reported cumulative realized losses of $296 million on EXCO in 2019 (as per the AR). Learning: the old economic model for shale was a sham. The good news: energy looks like it is in a structural bull market; the new economic model for shale looks good - focussed on shareholder return. 2.) APR (2016): Fairfax invested a total of $462 million in APR in 2016 and 2017. In 2018 they sold it to Atlas for $200 million (in Atlas stock). The first thing Atlas did was replace the CEO. Learning: Terrible business. Poorly managed. The good news: APR is now Atlas’ problem. 3.) Fairfax Africa (2017): launched with much fanfare in 2017, Fairfax invested a total $476 million. Two short years later Fairfax exited its management of the business and moved the assets to a fund managed by Helios. The value of the Helios fund today is about $100 million. I am not sure what the total financial loss was for Fairfax on this investment, but it was significant. The damage to Fairfax’s reputation was also significant. Learning: Hubris on steroids? Terrible idea. Worse execution. The good news: Fairfax is partnered with Helios and looks well positioned moving forward in Africa. This is now a small investment for Fairfax. 4.) Farmers Edge (2017): Fairfax invested $159 million in Farmers Edge in 2017. Farmers Edge completed its IPO in 2021 and in the 2021 AR Fairfax said their total investment in Farmers Edge to that point was $376 million. The CEO ‘stepped down’ in April of 2022. In the 2022 AR, Fairfax said Farmer’s Edge had a carrying value of $71 million, after taking a $133 million write down in 2022. The market value of Fairfax stake was $5 million at Dec 31, 2022. My guess is this investment, because it performed so terribly post-IPO, has caused Fairfax some damage to its reputation (given Fairfax was the majority shareholder). Learning: Yup, SPAC’s were a bubble. The good news: carrying value is $71 million. This is now a small investment for Fairfax. 5.) Eurobank (2014): Fairfax invested $444 million in Eurobank in 2014. This initial investment went to close to zero later that year when the ECB mandated a 1-for-100 reverse share split. What was the problem? Greece was in the midst of a depression. What did Fairfax do? It doubled down and invested another $389 million in Eurobank in 2015. In 2019, Eurobank did a capital raise/merger with Grivalia. Greece elected a pro-business government in 2018. Eurobank fixed its balance sheet. Learning: Because the strategy worked in Ireland doesn’t mean it would work in Greece. The good news: Greece’s economy is well positioned. Eurobank, always well managed, is executing well and earnings are spiking. Share of profit of associates was $263 million in 2022, up from $162 million in 2021. Prem estimated Eurobank could earn €0.20/share in 2023; if so, Fairfax’s share of profits for Eurobank could be +$300 million in 2023. This investment is turning into a home run for Fairfax - a Greek tragedy turns to a triumph! 6.) AGT (2017): Fairfax invested $148 million in AGT in 2017. In 2019, as AGT was experiencing financial difficulties, Fairfax took AGT private, spending another $227 million (I think). Learning: It takes much more than a dynamic Canadian founder to succeed. The good news: from 2022 Fairfax AR: “AGT, run by founder and CEO Murad Al-Katib, had a record year in 2022, with EBITDA of over Cdn$150 million. This is a dramatic improvement from the time of the take-private transaction almost four years ago when the business was generating slightly over Cdn$60 million in EBITDA… Fairfax has an approximate 60% stake in AGT.” 7.) Commercial Industrial Bank (CIB) Egypt (2014): Fairfax invested $330 million in CIB in 2014. Today the position is worth about $240 million. Great company. Solid management. What is the problem? Egypt’s economy has been a slow-moving train wreck for decades - with constant currency devaluations. Learning: Constant currency devaluations (like 50% in the last year) hurt equity values. The good news: the bank is well managed. 8.) Mosaic Capital (2017): Fairfax invested $116 million in Mosaic in 2017. In 2021, Mosaic was taken private (not by Fairfax) with Fairfax owning 20% of the new investment. This investment went sideways for many years (that opportunity cost thing). Learning: not every investment you make is going to work out. The good news: Fairfax found a partner where Mosaic will hopefully be a better fit. 9.) Recipe/CARA (2014 & 2016): Fairfax made a couple of restaurant investments from 2014-2017: $77 million in the Keg in 2014 (merged with CARA in 2018) and $100 million in the CARA capital raise in $2016. Recipe/CARA was a poor investment for minority shareholders over its lifetime. Learning: the restaurant business in Canada is a tough business. Consolidating it proved to be even tougher. The good news: In the take private deal in 2022, Fairfax purchased Recipe at a Covid-low price. Recipe has a solid collection of assets that should be able to produce a solid amount of free cash flow for Fairfax moving forward. 10.) Astarta (2017): Fairfax invested $104 million in Astarta in 2017. Today that investment is worth around $45 million. I know very little about this investment. I wonder if it is not a similar situation to CIB, with opportunity cost being the big issue. Honorable mention: Torstar was initiated as a position before 2014 so I did not include it. However, Fairfax added to its position in 2014, 2016 and 2017 (yes, small amounts). In 2020 it sold the business and booked a $52 million loss. I see lots of self-inflicted wounds in the investments listed above – reading the list reminds me of the Monty Python skit “tis but a scratch".

-

@73 Reds, one of Berkshire Hathaway’s big problems in recent decades is size. If Buffett had been more aggressive/opportunistic with buybacks over the years it likely would have helped in this regard. Size wise, Fairfax is in a very good spot - big enough but not too big. One of the reasons I like their aggressive buybacks is they will keep the company in this sweet spot longer.

-

@Maverick47, yes, there are many interesting angles to position size and investing. My guess is most investors (small and institutional) are a mirror image of Mr. Market (in terms of what they do). There are lots of things an individual investor can do to get an edge. Two obvious things are time frame and position sizing. What probably surprised me the most with the 6 capital allocation 'decisions' that I reviewed was how skewed the relationship of risk to return was. Of course, a finance textbook would say low risk = low return. And high risk = high return. But most of Fairfax's big decisions were low risk = high return. They were able to do this because in each instance they had an edge that they were able to exploit. I am also REALLY surprised how limited the business models of most P/C insurance companies are (the investment management part). And how they don't have a choice (their ownership structure is the underlying reason why they do things the way they do). What that means is the big advantage Fairfax has today when it comes to capital allocation is a sustainable competitive advantage. It is an important part of Fairfax's moat. As Fairfax continues to execute well this strength will get more understood / appreciated in the coming years (like it has been in recent years). But just like with Berkshire Hathaway (in general) it probably will never get fully reflected in the stock price.

-

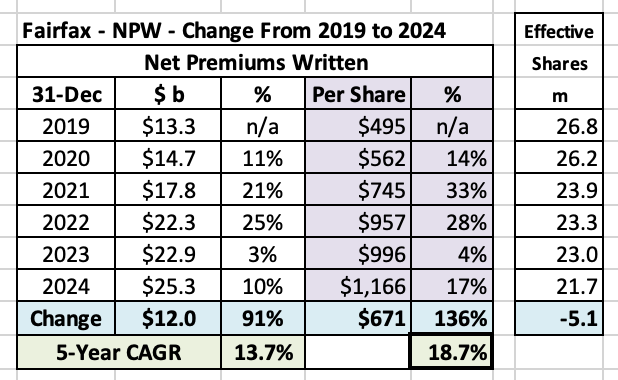

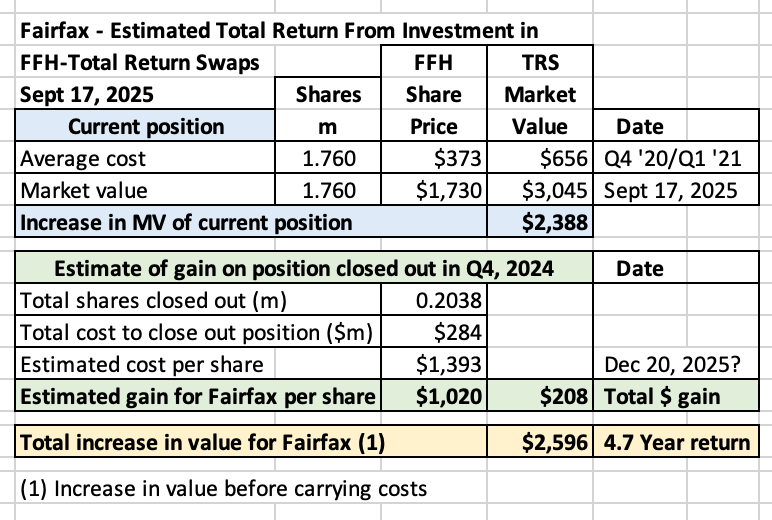

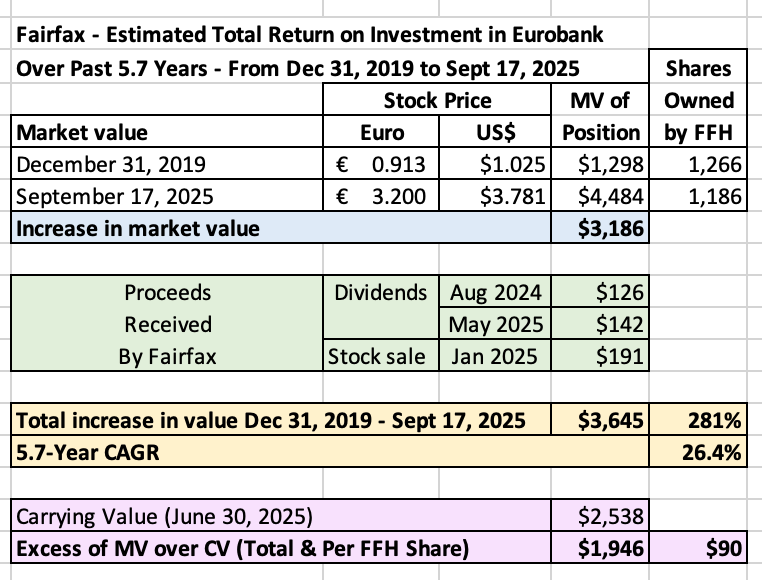

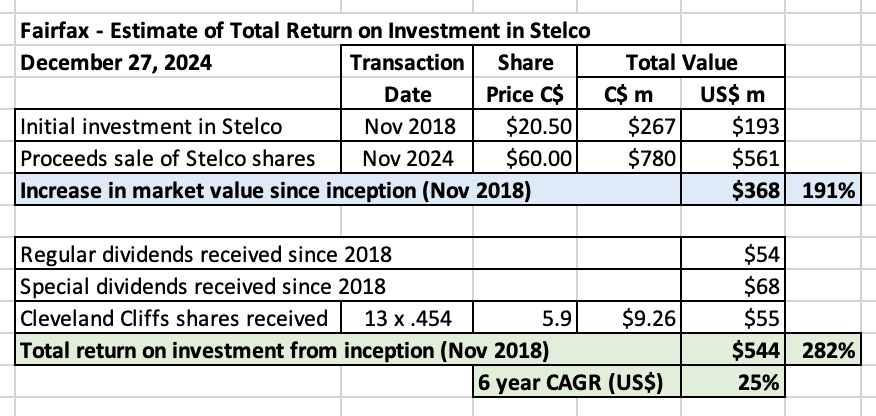

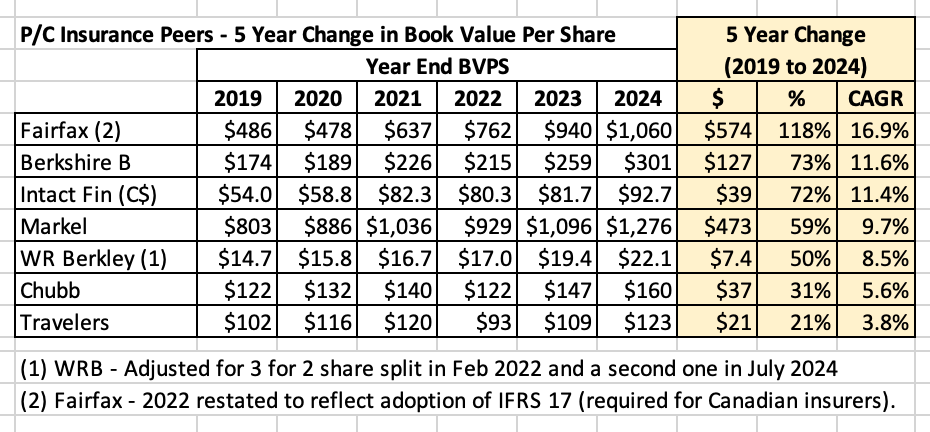

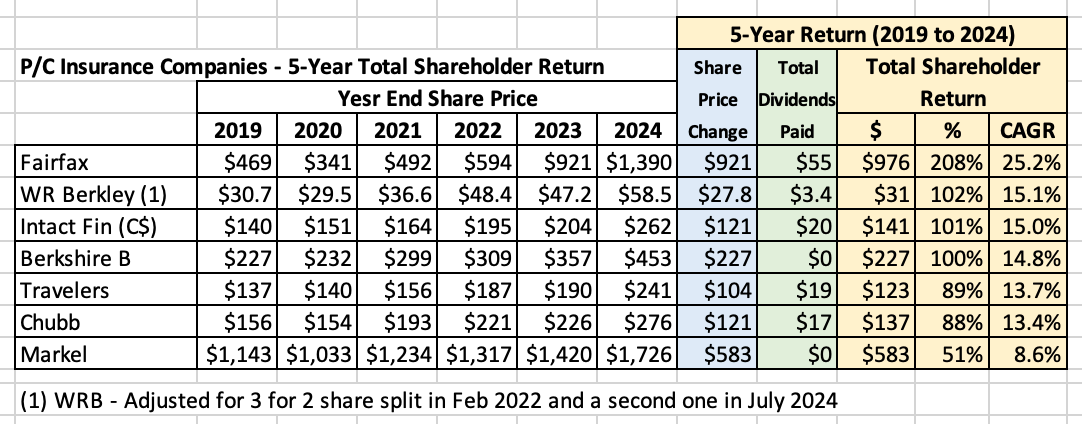

Part 4: Fairfax - Six examples of capital allocation decisions Ok. Let’s pivot from theory to the real world. Let’s look at an actual company. Fairfax Financial How good is the management team at Fairfax at sizing their capital allocation decisions? To help us answer this question we will look at six of Fairfax’s capital allocation decisions from the past 5 years: P/C insurance - Aggressively grow P/C insurance business in hard market. Fixed Income - Profit from greatest bond bull market in history / Avoid carnage of greatest bond bear market in history. Share buybacks - Aggressively buy back shares when they are trading at their cheapest valuation in history. Fairfax total return swaps - Get creative to exploit a wonderful opportunity. Eurobank - Exercising patience and letting a large legacy holding run. Asset sales - Capitalizing on volatility / Exploiting Mr. Market. ————— 1.) P/C insurance - Aggressively grow P/C insurance business in hard market. A hard market is the best of times for a P/C insurance company. Prices are high. And terms and conditions are favourable. Because of this one-two punch, business written in a hard market tends to be very profitable. But hard markets are created by fear. Well run P/C insurance companies are able to exploit this fear and significantly grow their business in a hard market. Fairfax’s top priority from a capital allocation perspective over the past 5 years has been to capitalize on the hard market in P/C insurance. Net premiums written at Fairfax have increased from $13.3 billion in 2019 to $25.3 billion in 2024, an increase of $12 billion or 91%. The 5-year CAGR has been 13.7%. Fairfax has been able to almost double the size of its P/C insurance business over the past 5 years (from a total $ perspective). That is a significant amount of organic (and highly profitable) growth when market conditions were at their best. Fairfax, and the P/C insurance team, has sized this capital allocation decision exceptionally well. ————— 2.) Fixed Income - Profit from greatest bond bull market in history / Avoid carnage of greatest bond bear market in history. In 2021, the 40-year historic bubble in bonds reached its blow-off top. Bond prices reached all-time highs and conversely bond yields reached all-time lows. Mr. Market was feeling positively euphoric when it came to fixed income investments - especially those that were long dated. 10-year US treasuries were trading at a yield of less than 1% for much of 2020 and 2021. Long duration bonds, with crazy low yields in 2020 and 2021, provided no margin of safety. Especially later in 2021, when it was clear that the economy was expanding and inflation was quickly becoming a big problem. What did Fairfax do in late 2021? 1.) They sold their large portfolio of corporate bonds that were yielding about 1%, locking in large, realized gains: “During 2021, we sold $5.2 billion in corporate bonds, mainly acquired in March/April of 2020, at a yield of approximately 1%, for a gain of $253 million.” Fairfax 2021AR 2.) They shortened the average duration of their fixed income portfolio ($37 billion in size at the time) to 1.2 years. And shifted the composition of the portfolio to higher quality holdings, mostly treasuries: “At the end of 2021, our fixed income portfolio, inclusive of cash and short-term treasuries, which effectively comprised 72% of our investment portfolio, had a very short duration of approximately 1.2 years and an average rating of AA-.” Fairfax 2021AR The team at Fairfax made these moves just months before the Fed (and other global central banks) unleashed hell on fixed income markets by spiking short interest rates. With hindsight, Fairfax's timing was close to perfect. Having a very short duration portfolio at the end of 2021 had two key benefits: It protected Fairfax’s balance sheet from interest rate risk - a rapid increase in interest rates would cause the value of bonds to plummet. This would then cause book value to fall. Long duration bonds were especially vulnerable. It provided valuable optionality - this would allow Fairfax to quickly take advantage of rising interest rates and dislocations in credit markets. What happened? When interest rates spiked in 2022 and 2023, Fairfax avoided taking billions in unrealized losses on their bond portfolio. And the earn through from higher rates was immediate - spiking interest income. With their strong financial position, Fairfax was able to fully and aggressively exploit the hard market in P/C insurance. The ratings agencies also upgraded Fairfax’s credit ratings. What about P/C insurance peers? When the bond bubble was raging, they were busy dancing to the music (Chuck Prince would have been proud of them). They kept blindly matching the average duration of fixed income portfolio with the average duration of their insurance liabilities. When interest rates spiked in 2022 and 2023, many P/C insurance companies got their heads handed to them - book value fell at many companies from 15 to 30%. Yes, it was not a solvency issue for these companies (although it could have been if losses from insurance had spiked at the same time). But the significant hit to their balance sheets was real. The earn through from higher rates was slow. And it hampered their ability to fully capitalize on the hard market in P/C insurance. Summary Fairfax was able to profit from the biggest bond bubble in history. And deftly largely side-step the biggest bond bear market in history. The financial benefits to Fairfax of these actions can be measured in the billions (the money made and then the losses avoided). Fairfax, and the fixed income team, sized this capital allocation decision exceptionally well (first selling $5.2 billion in corporate bonds and then shifting a $37 billion bond portfolio to 1.2 years average duration). PS: One other P/C insurance company had a very low average duration with their fixed income portfolio in late 2021. Who was it? Berkshire Hathaway. Why? At that time, holding duration was a very low return and very high risk strategy. Therefore, it made no sense. Of course Buffett understood this - and he acted accordingly. ————— 3.) Share buybacks - Aggressively buy back shares when they are trading at their cheapest valuation in history. Share buybacks are one of the capital allocation options available to management. They can be very beneficial for shareholders if they are done in a responsible manner (purchased at attractive prices) and sustained over many years. Share buybacks are such a good decision because of the certainty factor – of all the capital allocation options available to management, share buybacks carry the highest degree of certainty. “When companies with outstanding businesses and comfortable financial positions find their shares selling far below intrinsic value in the marketplace, no alternative action can benefit shareholders as surely as repurchases.” Warren Buffett – Berkshire Hathaway 1984AR Why are share buybacks so good? Warren Buffett highlights two benefits for shareholders: Higher per share intrinsic value – ‘Basic arithmetic’, according to Buffett. Higher multiple - Communicates to existing and prospective shareholders that management is rational and running the business in a manner that is friendly to/aligned with shareholders. It is counterintuitive, but for long term shareholders a low share price can be a big benefit - if the company is buying back shares and in a significant quantity. Especially if it persists for years. What did Fairfax do? Effective shares outstanding have been reduced from 26.8 million at December 31, 2019, to 21.7 million at December 31, 2024. This has been a decrease of 19.2% over the past 5 years. Fairfax spent a total of $3.4 billion - this was a significant amount of capital. Fairfax paid an average price of $663/share. At June 30, 2025, Fairfax’s book value was $1,058/share. Fairfax’s intrinsic value is much higher than its book value. Over the past 5 years (2020 to 2024), Fairfax was able to buy back a significant number of shares (19.2%) at an average price far below their intrinsic value. The value creation over the past 5 years has been enormous (in the $ billions). The management team at Fairfax has sized this capital allocation decision exceptionally well. To reinforce the sigificant benefit of Fairfax’s share buybacks, let’s go back to our first point. Total amounts (like net premiums written) matter to shareholders. However, what matters much more are the per share amounts (net premiums written per share). Net premiums written per share have increased from $495 per share in 2019 to $1,166 in 2024, an increase of $671/share or 136%. Per share, the 5-year CAGR has been 18.7%. This is much better than the 5-year CAGR for total net premiums written of 13.7%. —————- 4.) Fairfax total return swaps - Get creative to exploit a wonderful opportunity. In late 2020/early 2021, Fairfax purchased total return swaps giving it exposure to 1.96 million Fairfax shares at an average price of $373/share. In short, this was an investment for Fairfax. In itself. At the end of 2020, Fairfax had 26.2 million effective shares outstanding - so this position gave it exposure to 7.5% of shares outstanding. This was a significant investment (in terms of exposure). How has the investment performed? Since inception (over the past 4.7 years), the investment has delivered to Fairfax a total return of about $2.6 billion (before carrying costs). The FFH-TRS has become one of Fairfax’s best-ever investments. Fairfax has begun to unwind the position. In late 2024, the position was reduced from 1.96 million to 1.76 million shares. (Of interest, Fairfax bought back the 204,000 shares from the counterparty and retired them.) This investment is a great example of how creative Fairfax can be when it comes to capital allocation. At $2.6 billion, the financial benefit from investment this has been significant. The management team at Fairfax has sized this capital allocation decision exceptionally well. ————— 5.) Eurobank - Exercising patience and letting a large legacy holding run. Over the past 5.7 years, Fairfax’s investment in Eurobank has increased in value by $3.6 billion, a CAGR of 26.4%. Eurobank has quietly grown into Fairfax’s largest equity investment. Has Eurobank become Fairfax’s best-ever equity investment? What happened? Exceptional management - Over the past 7 years, the management team at Eurobank has been putting on a clinic. Their most recent great decision was the purchase of Hellenic Bank (at a price of 4 x earnings). Strong economic performance: The depression in Greece ended. For two elections in a row, Greece has elected a pro-business government to a majority. Animal spirits have been unleashed. And Greece has had one of Europe’s best performing economies. Increase in interest rates: Central banks around the world ended their disastrous zero interest rate policies. Higher interest rates have spiked earnings for banks. Patient controlling shareholder (Fairfax): Eurobank was given time to work through their issues. This also allowed them to think strategically and manage the business for the long-term. This investment is a great example of the benefits of doing nothing (in terms of position size). Fairfax has exercised great patience with this investment. This patience has allowed the position to mushroom in size from $1.3 billion at December 31, 2019, to $4.5 billion at September 17, 2025. The management team at Fairfax has sized this capital allocation decision exceptionally well. Excess of fair value over carrying value At September 17, 2025, the market value (MV) of Fairfax’s position in Eurobank was $4.5 billion. At June 30, 2025, the carrying value (CV) of Fairfax’s position in Eurobank was $2.5 billion. The excess of MV over CV is about $2 billion or $90 per Fairfax share (pre-tax). This is economic value that has been created by Fairfax in recent years that has not been captured/reflected in its accounting results (EPS, BV and ROE). ————— 6.) Asset sales - Capitalizing on volatility / Exploiting Mr. Market Why sell an asset? There are a number of good reasons to sell an asset. Perhaps another company - who is willing to pay up - values an asset at a much higher value than you do. There also can be important strategic reasons to sell an asset. Asset sales have been a very important part of Fairfax’s capital allocation framework over its entire existence, realizing significant value for Fairfax and its shareholders. Fairfax is unique among P/C insurance companies in how active it has been in using this important tool in the capital allocation toolbox. Below we will review three asset sales that Fairfax has executed in recent years: Pet insurance (2022) - Capitalizing on the mania in cats and dogs Pets have been a rapidly growing business segment in North America for the past 30 years. Covid took this growth to a higher level. Especially the services part of the business (veterinary services, pet insurance, supplies etc). On the service side, the business model was shifting to a ‘one stop shop’ model for pet owners – get all your pet needs taken care by one provider. The big players in the industry (like JAB Holding) were in a race to consolidate (to get scale) and the price for good assets went through the roof – reaching mania/bubble proportions. In June 2022, Fairfax announced that it had sold its pet insurance business (which resided in Crum & Forster) to JAB Holding for $1.4 billion. With the sale, Fairfax realized a gain of $1.2 billion pre-tax and $934 million after-tax. For a little background, Fairfax purchased Hartville Group for $34 million in 2013 and Pet Health for $89 million in 2014 and then sold the combined entity in 2022 for $1.4 billion. That is nuts. Fairfax has a long history of buying small insurance businesses and patiently incubating/growing them over a decade or more and then selling them for very large gains: First Capital, ICICI Lombard, Riverstone UK and now C&F pet insurance. Very impressive. Resolute Forest Products (2022) - Exiting a big mistake and capitalizing on the bubble in lumber In July 2022, Fairfax sold Resolute Forest Products (RFP) to Paper Excellence Group (a global diversified manufacturer of pulp and specialty, printing, writing and packaging papers) for total consideration of $665.6 million ($20.50/share). Fairfax got a premium price for the asset - Fairfax sold it for $20.50/share at the peak of the bull market in lumber. For perspective, back in March 2020, RFP shares traded as low as $1.20/share. Fairfax owned 30.5 million shares, so RFP’s market cap in March of 2020 was a total of $37 million. Two short years later Fairfax sold it for total proceeds of $665.6 million. Wow! Pre-pandemic, RFP’s shares traded at an average of about $6/share. In the historic lumber bull market of 2021, RFP’s shares traded at an average of about $12/share. Bottom line, at $20.50, Fairfax got an outstanding price for this company. With the sale, Fairfax also exited a big mistake - Fairfax got one of their worst ever equity purchases off their books. RFP also owned some pretty crappy businesses: newsprint, paper and tissue. And the ‘good’ business, lumber, was getting hit by higher mortgage rates. Bottom line, Fairfax sold what was overall (still) a very challenged business. Like with pet insurance, this is a great example of the significant benefits that can come from active management - sell an asset at a bubble high price and flip the proceeds into other assets selling at bear market low prices. Stelco (2024) - Capitalizing on the consolidation wave happening in the North American steel market Taking advantage of the consolidation happening in the North American steel industry, Stelco was sold to Cleveland-Cliffs in Q4, 2024, at a nosebleed-high price. The timing of the sale was perfect - in 2025, President Trump has imposed steep tariffs on Canadian steel, which severely hurts the business of a Canadian steel producer like Stelco. What kind of a return did Fairfax generate on its 6-year investment in Stelco? In November 2018, Fairfax invested $193 million in Stelco. Over the past 6 years, Fairfax earned a total return of $544 million on its investment in Stelco, or 282% = 6-year CAGR of 25%. Summary of asset sales With the three assets sales profiled above, we can clearly see the benefits of active management. In each example, Fairfax was able to exploit volatility / Mr. Market. Fairfax was able to execute both the pet insurance and RFP sales in 2022 in the middle of a bear market (in both stocks and bonds). Fairfax was then able to reinvest the significant proceeds into other assets that were selling at steep discounts and support the growth of the P/C insurance subsidiaries in the hard market. The sale of Stelco was also timed perfectly. In each the three examples, the management team at Fairfax got a premium valuation for the asset being sold. The management team at Fairfax sized each of these capital allocation decision exceptionally well. ————— Part 5: Summary of capital allocation and position size What are the key take aways/learnings from our 6 examples? 1.) Large size - Each example involved a significant amount of capital. Fairfax bet big. 2.) High return - Each example has delivered a minimum of $1 billion in value creation. Most delivered $2 billion. Some have delivered $3 billion. Each capital allocation decision has delivered an outstanding result/return. 3.) High frequency - Fairfax has been right a lot. Context matters. At the end of 2019, common shareholders’ equity at Fairfax was $13 billion. One exceptional capital allocation decision moves the needle for the company - is very impactful. But being right 6 different times? When you stack them up - one on top of the other - the impact on Fairfax and its business results has been magic. But there is much more to this story. 4.) Breadth - All parts of the organization are very good at sizing their capital allocation decisions. Head office Across P/C insurance and investment management businesses. Within investment management - across fixed income and equities. 5.) Complementary nature - Fairfax’s structure and business model allows the benefits from one decision to be leveraged with another. Example: Sell assets at a premium valuation and use the proceeds to grow P/C insurance in the hard market and buy back stock when it is trading at a very low valuation. 6.) Low risk - Each of the 6 decisions were very low risk / high return decisions for Fairfax. That demonstrated exceptional risk management. (Risk is defined as permanent loss of capital and not short term price volatility.) Fairfax is a P/C insurance company. Aggressively growing its P/C insurance business in a generational hard market was a very low risk decision. Taking the average duration of the bond portfolio to 1.2 years in late 2021 was exceptional risk management. Conversely, buying/holding long duration bonds in late 2021 was a very high risk thing to do (and is what most other P/C insurance companies were doing). When done well (like Fairfax has), share buybacks are an extremely low risk capital allocation activity - the company has a big informational advantage over Mr. Market (in terms of the business fundamentals, prospects and valuation). Fairfax total return swaps - Like with buybacks, Fairfax had a big informational advantage over Mr. Market when they entered into this position at a crazy low price of $373/share. Eurobank - Greece electing a pro-business government to a majority, an improving economy and rising interest rates de-risked this investment greatly. Selling assets at a nosebleed/bubble high prices is a very low risk capital allocation decision. 7.) Simple - Each of the 6 decisions that Fairfax made was a simple one. They were 1-foot hurdles for the company. Capital allocation is hard. Keeping it as simple as possible is important. 8.) Fairfax has been doing much more on the capital allocation / position sizing front than what has been covered in our 6 examples. We could have included another 10 or 15 examples in our analysis. And while they were not as large/impactful as the 6 we profiled they all have been impactful to Fairfax and its business results. What did we learn? In the words of the prophet Mae West: “Too much of a good thing can be wonderful." Warren Buffett - Berkshire Hathaway 1993AR Fairfax is very skilled at position sizing. Across the entire organization. And it looks like they are getting better. As a result, I think we can conclude that they are very good/skilled at capital allocation. They have the knowledge - They know what to do. They have the skill - They know how to do it. They have the desire - It is part of the company’s culture. They want and are rewarded for doing it. In short, how to do capital allocation well has become a habit at Fairfax. How good are they at capital allocation? Based on what we have seen over the past 5 years, I would give Fairfax a rating of 9 out of 10. Not a 10? No. Who would get a 10? The pre-2000 version of Warren Buffett/Berkshire Hathaway. —————— Summary - Fairfax and properly sizing a capital allocation decision: “Sizing is 70% to 80% of the equation. Part of the equation is seeing the investment, part of the investment is seeing myself in a good trading rhythm. It’s not whether you’re right or wrong, it’s how much you make when you’re right and how much you lose when you’re wrong…” Stanley Druckenmiller Over the 5-year period from 2019 to 2024, Fairfax has delivered: BVPS CAGR = 16.9% Share price CAGR = 25.2% This performance has been significantly better than other P/C insurance peers. This performance has happened because Fairfax is very good at capital allocation. One of the reasons is Fairfax is very skilled at sizing its decisions. Fairfax is like a star athlete that is just entering their prime. Is that how the stock is valued? No. the stock is valued at the low end of P/C insurance peers. That is a great set-up for a long term investor. Growing earnings + expanding multiple + lower share count = usually results in good to very good returns over time —————— Why do most P/C insurance companies fail at position sizing? 1.) Lack of skill. 2.) Structure. Timeframe - Wall Street works very short term. Quarterly. This makes it impossible to size positions properly. Ownership structure is also an impediment. Make what looks like a short term dumb decision and you could be out of a job. This is too risky for most management teams of publicly traded companies. Better to fail traditionally than to succeed unconventionally. Of the two, structure is the more important. It doesn’t allow it (or reward it). In short, the structure ensures the skill will never be developed. The 2 exceptions are Berkshire Hathaway and Fairfax. Both have a controlling shareholder. So structure is not an impediment - it is an enabler. The focus is on per share value creation for shareholders over the long term. Position size is recognized as an important and critical piece in the capital allocation puzzle - a valued skill that needs to be appreciated, developed and used properly.

-

Capital Allocation: How good is the management team at Fairfax? Today we are going to get into the weeds of capital allocation. We are going to get into position size. To see what it will teach us about Fairfax. The post today has been broken into the following 5 parts: Part 1: Introduction Part 2: Is management any good? Part 3: Sizing a capital allocation position/decision Part 4: Fairfax - Six examples of capital allocation decisions Part 5: Summary —————— Part 1: Introduction Capital allocation is the most important responsibility of a management team. Why? Capital allocation decisions are what drive the long-term performance of a company and important metrics like reported earnings, growth in book value and return on equity. In turn, these metrics drive the multiple given to the stock by Mr. Market and, finally, the share price and investment return for shareholders. Capital allocation is a skill. This is important because it means it can be learned (and mastered) over time. Skill defined: “an ability to do an activity or job well, especially because you have practiced it.” Cambridge Dictionary When done well, capital allocation does two important things: Delivers a solid return. Improves the quality of the company. Therefore, the fundamental task of an investor is to determine if management, over time, is making intelligent decisions regarding capital allocation. When it comes to capital allocation, an investor needs to answer two questions: 1.) Is management any good? Yes or no. 2.) If so, how good are they? On a scale from one to 10, what number are they? Scale: 1 = terrible, 5 = average and 10 = exceptional. Of the two questions, the first is the easiest to answer. But the answer to the second question is much more important. The first question can largely be answered by looking at business performance over a 5-year period. For a P/C insurance company, the best way to evaluate business performance is to look at the 5-year change in book value and the stock price. Yes, this is a blunt tool. To answer the second question, we need to get much more granular with our analysis. That is what we will do later in this post. ————— Part 2: Is management any good? To answer this question we will look at the 5-year change (2019 to 2024) in BVPS and the share price. To provide context, we will do this for 7 well run P/C insurance companies. Which company has delivered the highest 5-year CAGR in BVPS? Fairfax Financial, at 16.9%. It is much higher than the #2 performer, Berkshire Hathaway at 11.6%. Which company has delivered the highest 5-year CAGR in total shareholder return? Fairfax Financial, at 25.2%. It is much higher than the #2 performer, WR Berkley at 15.1%. Fairfax had the highest growth in BVPS. It makes sense that it also has had the highest increase in total shareholder return. Summary Of the 7 high quality P/C insurance companies listed above, looking at 5-year change in BVPS and share price, Fairfax has been the top performer over the past 5 years (2019 to 2024). And it is not close. This suggests Fairfax is quite good at capital allocation. And much better than P/C insurance peers. But just how good is Fairfax? That is the question we will try an answer next. ————— Part 3: Sizing a capital allocation position/decision Capital allocation - the importance of properly sizing a decision/position Today we are going to look at one very specific part of capital allocation - how to size a position/decision. We can summarize the capital allocation/investment process as follows: Find a good/great opportunity (in your circle of competence). Exploit/buy it (with a margin of safety). Get the position size right (size/concentrate capital in your best ideas). Exploit/hold it - as long as ‘the story’ remains intact. ‘Get the position size right’ is very difficult. Position size matters so much because of the outsized impact it can have on economic results. Getting position size right is one of the ways a company can outperform peers. Get it wrong? Things can get ugly fast. GOAT can turn to goat. The really interesting thing, given its importance, is how little this aspect of capital allocation is discussed. Are management teams evaluated (at least in part) based on how well they size their capital allocation decisions? No, they are not. As a result, position size is one of those topics that pretty much everyone agrees is really important. But it is also something that is not to be discussed in polite company. It is the elephant in the room. This is especially true for P/C insurance companies. When was the last time you read an analyst report and they discussed management, capital allocation and how good they were are position sizing? Never. But ignorance is a good thing when it comes to investing. The opposite of ignorance is knowledge. And knowledge is what gives an open minded investor an edge. And having an edge is what leads to outperformance. What is position size? Stanley Druckenmiller is one of the GOAT’s of investing. I like Druckenmiller’s description of position size the best: “Sizing is 70% to 80% of the equation. Part of the equation is seeing the investment, part of the investment is seeing myself in a good trading rhythm. It’s not whether you’re right or wrong, it’s how much you make when you’re right and how much you lose when you’re wrong…” Stanley Druckenmiller Now don’t get me wrong… I am not suggesting we all should become ‘traders’ like Druckenmiller. I love this quote so much because it provides an easy to understand way to think about position size. It is simple and concise: Position size is really important - if you want to earn above average returns. How often you are right or wrong is not what matters (for returns). How much you make when you are right is what really matters. This gets to the critical importance of properly sizing your capital allocation decisions/positions around your best ideas. Of course, Buffett is the master a sizing his capital allocation decisions. All of the investing greats were very good at properly sizing their positions. It was a skill they all learned and honed over time. ————— Keep reading the next post in this thread for Parts 4 and 5 (the article is too long to fit in one post).

-

The takeout of Singapore Re in 2022 is looking like a great purchase for Fairfax. Not massive in size. Was done right before the hard market in reinsurance started. This long term relationship ending in purchase epitomizes so many of the things that Fairfax does so well.

-

This quote from Buffett has really resonated with me in recent years. So much so, it might have warped my thinking a little. He was talking about leverage... but I think it also can be applied in a more general way. “It’s insane to risk what you have and need for something you don’t really need. ... You will not be way happier if you double your net worth.” I have enough. I am 60 years old. My wife is very risk averse (meaning if I blow up our portfolio it would hit her much harder than me). We live a simple life (we don't have expensive tastes). We only have financial assets (no real estate). And we have no company pensions (other than CPP). All of this feeds into how I have structured our investment portfolio (including weightings). The key is to be as rational as possible. To keep learning (lots to learn when it comes to retirement/estate planning). To be open minded. To make course corrections as required - it is a marathon not a sprint (these days for me anyways). My big problem is how I am wired. Not an issue right now. But definitely a risk and something that needs to be closely monitored.

-

@petec, 4 years ago (Sept of 2021) Fairfax was still (largely) a hated company. The stock was trading under US$450/share. It was trading below where it was trading pre-covid. Its price reflected investors views of the company at the time: Below average P/C insurance business. Below average at investment management. Below average management team. Looking back, of course this view was wrong. What changed? Everything. Is this a company with largely the same assets and management team using the same philosophy? Yes. And no. Anyways, I do really appreciate our debates.

-

Position size really is a super interesting part of investing. It is one of the most difficult parts. And it might be one of the most mis-understood parts. Probably because it is so situational. Context matters a great deal. As a result, I am not sure position size can be discussed meaningfully without providing at least some basic context. 1.) How are you measuring position size? In terms of total net worth? Or just in terms of total financial assets? - Investor A: 80% of net worth is financial assets. And 20% is real estate. - Investor B: 80% of net worth is real estate. And 20% is financial assets. 2.) What is the problem you are trying to solve for? (What is your objective?) - Investor A: Focussed on total return. - Investor B: Focussed on capital preservation. 3.) What is your risk tolerance? - Investor A: Not risk averse. - Investor B: Risk averse. Does a spouse's risk tolerance matter? 4.) What is your age / life stage? - Investor A: 35 years old. - Investor B: 60 years old. 5.) Perhaps most importantly, how good at investing are you? - Investor A: Average - Investor B: Very good. These are 5 questions that quickly came to mind… there are more.

-