Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

Fairfax - A Deep Dive on Management and Culture

Viking replied to Viking's topic in Fairfax Financial

@RichardGibbons, you make a great point - it is complicated. Not just for Prem/Fairfax but for any company. It gets to the heart of what makes assessing management so difficult - it qualitative and comes down to judgement. As a result, two investors looking at the same information could come to very different conclusions. In my framework (right or wrong), much of my analysis is weighted to the past 5 years. Years 6 to 10 matter, but much less. More than 10 years is interesting but much less relevant (for me). It is important people understand that when they read my stuff. If I had completed the management chapter in late 2020 it would have had a very different tone. Fairfax is very active - buying and selling. They are involved in a number of transactions every year. Volume alone is going to put them in a tough spot every once in a while. Not that I am trying to make excuses for past behaviour. My view that Fairfax has moved up the quality ladder when making new purchases should help (if true). Taking companies private also helps. Buffett is an interesting comparison. He also had a few big stumbles over the years. Those are largely forgotten. Understanding Fairfax's long history pretty well, I am just so happy with where the company is at today. -

Fairfax - A Deep Dive on Management and Culture

Viking replied to Viking's topic in Fairfax Financial

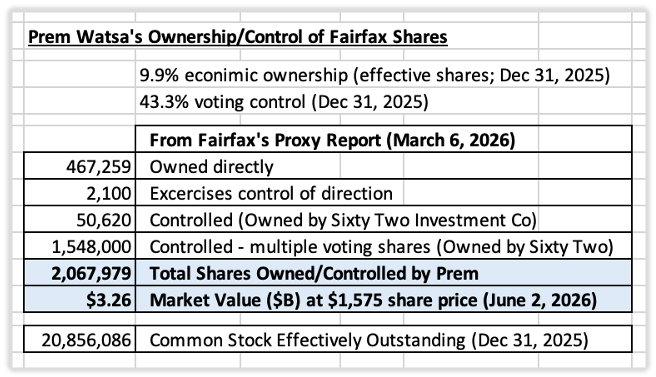

Article 2 in the series. Prem Watsa and Family Control Founder-led companies have historically been among the best long-term investments. When ownership, control, and management are concentrated in the hands of a capable founder, decisions are often made with a longer time horizon and a greater focus on value creation. Fairfax Financial is one such company. Prem Watsa founded Fairfax in 1985 and has led the company for nearly four decades. During that time, Fairfax has evolved from a small Canadian insurer into a global insurance, investment, and operating company with interests spanning dozens of countries and industries. For investors, understanding Prem's role is important because he remains Fairfax's largest individual shareholder, Chief Executive Officer, Chairman, and controlling voting shareholder. Fairfax's culture, capital allocation philosophy, and long-term orientation all reflect his influence. This article examines Prem's leadership record, ownership position, and family control structure—and what those factors mean for shareholders. Founder, Leader and Capital Allocator Prem Watsa founded Fairfax in 1985 and has led the company continuously ever since. Over that period, Fairfax's share price has compounded at approximately 19% annually, including dividends. This places Fairfax among the best long-term performing public companies in Canada and North America. But what makes Prem noteworthy is not simply what he achieved—it is how he achieved it. Warren Buffett has often said that he looks for three qualities in business leaders: Intelligence Initiative Integrity Of the three, Buffett considers integrity the most important because it forms the foundation of trust. Prem has demonstrated all three qualities throughout Fairfax's history. His intelligence is reflected in Fairfax's long-term record of capital allocation and value creation. His initiative is evident in the growth of Fairfax from a small Canadian insurer into a global organization. Most importantly, he has built a reputation for integrity that has earned the trust of shareholders, employees, customers, business partners, and communities. Two qualities have been especially important to Fairfax's success: temperament and an ability to attract talented people. Buffett has long argued that temperament is more important than intellect in investing. Throughout Fairfax's history, many of the company's most successful decisions required patience, conviction, and emotional discipline during periods of uncertainty. Throughout Fairfax's history, many of the company's most successful investments were made during periods of uncertainty and market stress. These decisions required patience, conviction, and emotional discipline. Prem has also demonstrated an uncommon ability to identify, recruit, develop, and retain talented managers. Fairfax's decentralized structure depends on capable leaders operating with significant autonomy. The depth and continuity of Fairfax's management team may ultimately prove to be one of Prem's most important accomplishments. As a result, Fairfax's success extends well beyond shareholder returns. Employees have built rewarding careers, customers have benefited from stable insurance partners, communities have received significant philanthropic support, and long-term shareholders have participated in one of the strongest compounding stories in modern Canadian business. Buffett on the importance of temperament – 1985 interview with Adam Smith: Adam Smith: What do you consider the most important quality for an investment manager? Warren Buffett: It's the temperament. You don't need tons of IQ in this business. I mean you have to have enough of IQ to get from here to downtown Omaha but you do not have to be able to play three-dimensional chess or being the top player in a bridge league. You need a stable personality and temperament that neither derives great pleasure from being with the crowd or against the crowd because this is not a business where you take polls; it's a business where you think. Ben Graham would say that you're not right or wrong because a thousand people agree with you and you're not right or wrong because a thousand people disagree with you. You're right because your facts and your reasoning are right. – Warren Buffett - Adam Smith’s Money World Interview 1985 Ownership, Compensation, and Alignment One of the most attractive features of Fairfax's governance structure is the alignment between management and shareholders. Prem's compensation package is unusually modest for a company of Fairfax's size and complexity. His annual salary is approximately C$600,000 and he receives no stock options or stock-based compensation. The more important consideration, however, is ownership. As of December 31, 2025, Prem owned or controlled approximately 2.1 million Fairfax shares, representing: 9.9% economic ownership 43.3% voting control At Fairfax's share price in mid-2026, that stake was worth more than $3 billion. As a result, the overwhelming majority of Prem's wealth remains tied to Fairfax's long-term success. Shareholders benefit from knowing that gains and losses are experienced alongside management. This alignment was demonstrated during the market turmoil of 2020. At a time when investor sentiment toward Fairfax was overwhelmingly negative, Prem personally purchased approximately US$150 million of Fairfax shares in the open market. He described Fairfax as trading at the largest discount to intrinsic value he had seen in the company's history. "At our AGM and on our first quarter earnings release call, I said that our shares are 'ridiculously cheap'. That statement reflected my recognition that in the 35 years since Fairfax began, I have never seen Fairfax shares sell at a bigger discount to their intrinsic value than they have recently. I have now backed up my strong words by purchasing close to US$150 million of Fairfax shares in the market over the last few days, as I believe that this will be an excellent long term investment." — Fairfax News Release, June 15, 2020 Actions often reveal more than words. Large insider purchases by already-wealthy founders are relatively uncommon and are generally viewed as one of the strongest indicators of management alignment. Family Control Fairfax is effectively a family-controlled company. While Prem owns ~10% of Fairfax's economic interest, his multiple-voting shares provide ~43% voting control. This gives the Watsa family substantial influence over Fairfax's strategic direction. For some investors, family control raises concerns. For others, it represents an important competitive advantage. The reality is that family-controlled structures can produce either excellent or poor outcomes depending on the quality of the controlling shareholder. When governance is strong, family control often promotes: Deep commitment to the business Long-term decision making Consistent capital allocation Preservation of corporate culture Stability during difficult periods Strong relationships with customers and employees Strong community focus and social purpose These characteristics can be especially valuable in insurance and investing, where the consequences of important decisions may take years to fully emerge. Fairfax's forty-year record suggests that family control has been a significant positive for shareholders. The structure has allowed management to think in decades rather than quarters, preserve Fairfax's culture, and maintain a consistent capital allocation philosophy through changing market environments. At the same time, investors should remain aware of the risks that accompany any founder-controlled organization. Potential concerns include succession planning, management entrenchment, and the possibility that future leaders may not possess the founder's abilities. No governance structure is perfect. Every structure involves trade-offs. What This Means for Shareholders Ownership structure matters because it influences incentives, decision making, and corporate culture. Fairfax remains a founder-led company with substantial insider ownership, significant voting control, and a leadership team whose financial interests are closely aligned with those of long-term shareholders. Prem's four-decade record of value creation, modest compensation, significant ownership position, and long-term orientation have all contributed to Fairfax's success. The historical evidence suggests that Fairfax's founder-led, family-controlled model has served shareholders exceptionally well. Fairfax's exceptional long-term performance, strong culture, and disciplined capital allocation are all closely tied to the leadership Prem has provided since 1985. The key question for investors is no longer whether this structure has worked under Prem Watsa. The historical record clearly answers that question. The more important question is whether Fairfax can preserve the culture, discipline, and capital allocation framework that Prem built once the next generation assumes greater responsibility. That question is examined later in this chapter when we turn to succession planning. Learn More About Prem Watsa Prem was inducted into the Canadian Business Hall of Fame in 2024. The six-minute biography prepared for his induction provides an excellent overview of his life, values, and the development of Fairfax. It is well worth watching for investors seeking a deeper understanding of the person who built Fairfax. To watch the 6-minute biography of Prem on YouTube, click the link below: - https://www.youtube.com/watch?v=SisxUC232t8

-

@LC, perhaps another way to ask the question is what cost base are you using when projecting future returns from the equity portfolio? Is it Fairfax’s carrying value? Or market value? The starting point matters. I use CV. Therefore, I think Fairfax will be able to outperform the broad market averages over the next 5 years. It really is an interesting thought exercise. The up-front assumptions matter a lot. I appreciate you taking the time to comment… this stuff really is complicated.

-

Fairfax - A Deep Dive on Management and Culture

Viking replied to Viking's topic in Fairfax Financial

Article 1 in the series. I look forward to hearing what other board members think... The Importance of Shareholder-Friendly Management In Berkshire Hathaway's 1977 Annual Report, Warren Buffett outlined four criteria for selecting investments: "We want the business to be: 1. One that we can understand, 2. With favorable long-term prospects, 3. Operated by honest and competent people, and 4. Available at a very attractive price." Notice that management is one of only four requirements. Buffett later explained why: “The certainty with which management can be evaluated, both as to its ability to realize the full potential of the business and to wisely employ its cash flows; The certainty with which management can be counted on to channel the rewards from the business to the shareholders rather than to itself.” Buffett's observation gets to the heart of shareholder-friendly management. Management's role extends beyond operating the business. It must also decide how the cash generated by the business is allocated. Over time, these capital allocation decisions can have an enormous impact on shareholder returns. Management therefore has two primary responsibilities. First, it must operate the business effectively. Second, it must allocate the resulting cash flows in a way that maximizes long-term shareholder value. For investors, evaluating management is not optional. It is a critical part of the investment process. Why Investors Often Ignore Management If management is so important, why do many investors spend relatively little time evaluating it? The answer is simple: management quality is largely a qualitative factor. Most investors naturally focus on quantitative measures such as earnings, profit margins, return on equity, and valuation ratios. These metrics are objective, easy to compare, and fit neatly into spreadsheets. Management quality is different. How do you measure integrity, judgment, capital allocation skill, long-term thinking, or shareholder alignment? There is no formula that can answer these questions. Evaluating management requires observation, experience, and judgment. Yet management often has a greater impact on long-term shareholder returns than many of the financial metrics investors spend their time analyzing. Management determines how capital is allocated, whether acquisitions are made, how much debt is assumed, whether shares are repurchased, and how corporate culture is developed. In The Outsiders, William Thorndike found that the CEOs who created the most value for shareholders distinguished themselves primarily through superior capital allocation. Over time, those decisions compound and can become a primary driver of shareholder returns. For this reason, qualitative analysis should not be viewed as a substitute for financial analysis. It is a necessary complement to it. A Framework for Evaluating Shareholder-Friendly Management Shareholders need to consider many factors when evaluating management. One of the most important is whether management consistently acts in the best interests of shareholders. Do executives think and act like owners? Do they allocate capital wisely? Do they communicate openly and honestly? While no framework can eliminate judgment, it can help investors ask the right questions. One useful approach is to evaluate management using seven criteria: Ownership Alignment – Do executives think and act like owners? Compensation – Are incentives tied to long-term value creation? Per-Share Value Creation – Does management focus on value per share rather than corporate size? Capital Allocation – Is capital deployed rationally and with discipline? Communication – Are shareholders treated as partners? Long-Term Orientation – Are decisions made with a multi-year perspective? Trust and Stewardship – Do actions consistently match words? No management team will score perfectly on every criterion. The goal is to identify management teams that consistently behave like owners and treat outside shareholders as partners. Evaluating Fairfax Through the Lens of Shareholder-Friendly Management Using this framework, Fairfax scores highly. Management owns a meaningful stake in the company, compensation is shareholder-friendly, capital allocation is a core competency, and the organization is managed with a distinctly long-term orientation. Most importantly, management has invested alongside shareholders and created substantial value over four decades. Ownership Alignment: A+ This is one of Fairfax's greatest strengths. Prem Watsa owns or controls approximately 10% of Fairfax's economic interest and more than 40% of the voting power. The vast majority of his net worth remains invested in Fairfax shares. Fairfax has also built an ownership culture throughout the organization. Senior executives receive 50% of their annual bonuses in Fairfax shares that vest over five years, while employees can participate in a stock ownership plan with meaningful company matching contributions. Management's alignment with shareholders was demonstrated again in 2020 when Prem purchased approximately $149 million of Fairfax shares in the open market during a period of extreme pessimism toward the company. Compensation: A+ Fairfax stands out relative to most public companies. For decades, Prem Watsa's annual salary has been C$600,000—remarkably modest given the size of the organization. Unlike many public-company CEOs, he has not relied on large stock option grants or aggressive incentive packages. His wealth has been created primarily through ownership, not compensation. Fairfax purchases in the open market the shares awarded under its compensation programs rather than issuing new shares. As a result, shareholders bear the economic cost of compensation but avoid the ongoing dilution that often accompanies stock-based compensation plans. This approach better aligns employee ownership with shareholder interests and helps protect per-share value. While Fairfax's compensation programs are shareholder-friendly in design, they still represent a meaningful economic cost that must ultimately be justified by improved performance, retention, and value creation. Focus on Per-Share Value Creation: A Fairfax has long emphasized growth in book value per share as its primary measure of success. Management's shareholder letters, annual meeting presentations, and public commentary consistently focus on per-share value creation, demonstrating a philosophy that prioritizes increasing shareholder value rather than simply increasing the size of the company. Just as importantly, management's actions have matched its words. Since 2020, Fairfax has repurchased a significant amount of its outstanding shares when they traded at meaningful discounts to intrinsic value. Rather than pursuing acquisitions or expanding the organization for the sake of growth, management chose to increase the ownership stake of existing shareholders. Capital Allocation: A+ William Thorndike argued that capital allocation is a CEO's most important responsibility because it has the greatest impact on long-term shareholder returns. By that standard, Fairfax's record is exceptional. Since 1985, Fairfax's share price has compounded at approximately 19% annually, including dividends. The record includes mistakes and periods of underperformance, but management has demonstrated an ability to learn, adapt, and continue creating value over four decades. Communication: B+ Fairfax provides more disclosure than most companies. Shareholder letters, annual meetings, and quarterly conference calls provide investors with substantial information about the business, investment portfolio, and culture. At the same time, Fairfax has never focused on promoting its story to Wall Street or cultivating media attention. Consistent with the philosophy described in The Outsiders, management appears to believe that operating the business and allocating capital are better uses of time than managing the short-term stock price. The result is a company that communicates extensively with shareholders, but on its own terms. Long-Term Orientation: A+ Long-term thinking has been a defining characteristic of Fairfax since its founding. Many of the company's most successful investments required years of patience before their value was recognized. Founder leadership and significant insider ownership reinforce this advantage by allowing management to focus on long-term value creation rather than quarterly expectations. Trust and Shareholder Stewardship: B+ Trust is earned through actions over long periods of time. Fairfax has built a reputation for integrity, fairness, and treating shareholders as partners. However, a balanced assessment should acknowledge that management's credibility was damaged during the difficult period from 2010 to 2020. The equity hedges persisted too long, several investments disappointed, and actual results often fell short of expectations. Importantly, the issue was not integrity. Rather, it was judgment and adaptability. Since 2020, Fairfax has rebuilt much of that credibility through actions rather than words. Strong operating performance, improved investment results, substantial share repurchases, and exceptional growth in book value and the share price have helped restore investor confidence. Overall Assessment Overall Grade: A Fairfax scores highly across all seven criteria. Management is strongly aligned with shareholders, compensation practices are disciplined, capital allocation has been exceptional, and long-term thinking is embedded throughout the organization. Most importantly, management has invested alongside shareholders and created substantial value over four decades. Viewed through the lens of shareholder friendliness, Fairfax compares favourably with almost any public company. On that measure, Fairfax earns an A. -

I decided to add a new chapter to my book on Fairfax: Management and Culture. I have six articles on the go. Rather than post them in the Fairfax 2026 thread I decided to post them in a separate thread. My articles are long and positing multiple articles really gums up the 2026 thread. My plan is to post the articles in this thread over the next week (perhaps one each day). Please keep comments in this thread focussed on management/culture. Keep general comments on the Fairfax 2026 thread. Let me know if you think this is a better way for me to post a series of articles. I look forward to hearing from board members on the content of the articles - that is how we all learn and improve (our understanding of Fairfax and as investors). To get started, here is the chapter overview: ------------ Chapter 7: Management and Culture Chapter Overview Most investors focus on financial statements, valuation metrics, and investment portfolios. Yet some of the most important drivers of long-term shareholder returns cannot be found in a spreadsheet. Management quality, organizational structure, incentives, and corporate culture often determine whether a good business becomes a great one. This is especially true at Fairfax. While investors often focus on underwriting results and investment performance, much of Fairfax's long-term success can be traced to its management philosophy, organizational structure, incentive systems, and culture. Understanding how Fairfax is led, how decisions are made, and how the organization is structured is essential to understanding the company itself. This chapter examines six aspects of Fairfax's management and culture: 1. What is shareholder-friendly management? We develop a framework for evaluating management quality and use it to assess Fairfax. 2. Who is Prem Watsa? We examine Fairfax's founder, largest shareholder, and chief architect, along with the implications of family control. 3. How is Fairfax organized? We explore Fairfax's decentralized operating model and why it may be one of the company's most important competitive advantages. 4. What is Fairfax's culture? We examine employee retention, management continuity, and the cultural traits that have shaped Fairfax's success. 5. How are incentives aligned? We review Fairfax's compensation and employee ownership programs to understand how the company encourages managers and employees to think like owners. 6. Can Fairfax succeed beyond Prem Watsa? We assess succession planning, leadership development, and the depth of Fairfax's management bench. The goal of this chapter is to determine whether Fairfax has built a management culture, organizational structure, and leadership pipeline capable of sustaining its success and compounding value for shareholders for decades to come. Keep reading for article 1.

-

Can you please define what you mean by equity portfolio? Are you talking stocks? Are you talking CDS/equity hedges (did well), equity hedges/shorts (did poorly) and TRS(did well)? What exactly are you trying to measure?

-

I think it is pretty much impossible to determine a rate of return on Fairfax’s equity book over the past 40 years. What do you include? CDS? Equity hedges? TRS? Some of these were risk management positions, others were investments? But we do know with certainty one thing: Fairfax’s share price compounded at 19% for the past 40 years (US$; dividends reinvested). That is elite performance. Clearly, Fairfax is doing a number of things exceptionally well. Fairfax has two businesses: Insurance Investments. We also know returns from the insurance business were weak pre-2010. As a result, I suspect investments have been an important driver of long term results. What did they return each year? No idea. And I don’t need to know… All I have to do is look at the stock price to know what I need to know. (Fairfax’s total performance has been elite.) I am a quickly becoming a Thordike desciple…. Capital allocation is the most important thing over the long term for a company like Fairfax. Capital allocation drives per share results over the long term more than anything. But assessing capital allocation is not easy - so most investors/analysts ignore it. Instead they focus on other things that are easier.

-

KW is an interesting company. I totally agree with you - retail shareholders in KW got taken out behind the woodshed owning the stock. But my read is Fairfax did ok. The stock they owned was table-stakes (as Jamie Dimon would say). It got Fairfax access to Kennedy Wilson’s deal flow. Real estate partnerships. Mortgage loans. ThePacWest deal was an absolute home run for Fairfax (still is). And in the end, it also allowed Fairfax to take KW out on the cheap (at least that is my initial uneducated read). Real estate is deeply out of favour - this is likely an ideal time to buy something like KW. Now having said all that… KW is a bit of a complex beast… so I could be completely off base in terms of how it works out for Fairfax. We will see. It reminds me a little of when Fairfax took Recipe private when Covid was still a thing here in Canada - Fairfax got it cheap (in terms of buying when there was a lot of pessimism).

-

Can you explain to me what the financials look like for each investment? What was the money Fairfax put in? (That is not the reported deal price.) What is the (likely) return they are going to generate off it in the coming years? Bottom line, I am being open minded with their new purchases. One reason is I haven’t spent a lot of time trying to understand them. I will get around to it. Another reason is Fairfax has been hitting the ball out of the park - as a result, I am giving them the benefit of the doubt. i don’t expect them to be perfect. Some investments will look like clunkers. Lynch said if you are right 6 times out of 10 you will do well in this business. I am not worried when it comes to Fairfax’s equity portfolio these days.

-

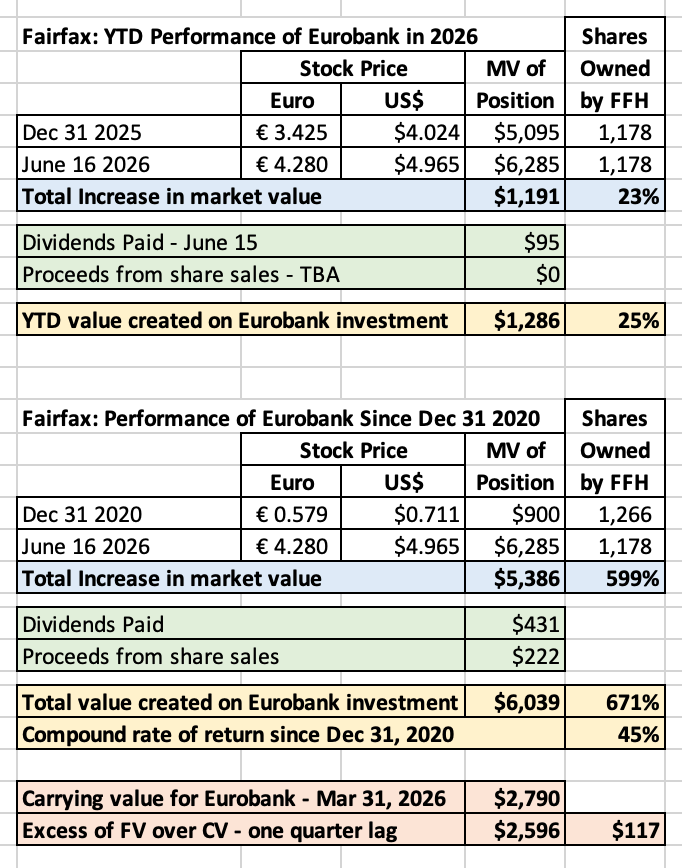

Is there a reason you use 15 years as the benchmark? Buffett has said that 5 years is a good timeframe to use to evaluate a management team. That is my preferred measure. Does year 6 to 10 performance matter? A little, but much less IMHO. What about year 11 to 15? Interesting… but too long ago to matter much IMHO. For instance… back in 2013, I did not use a 10 or 15 year timeframe to evaluate Fairfax’s management team at the time (their investment returns). That would have been pretty dumb, given the CDS and equity hedge positions (that worked fabulously well from 2007-2009) would have completely skewed results. The best way to evaluate Fairfax in 2013 was to look primarily at what they owned at the time, how the positions had performed recently (prior 5 years), and what their prospects were (next 5 years). (I did that and then sold all my shares in Fairfax.) Imagine using a 15 year timeframe to evaluate management at BlackBerry back in 2013? It would have told an investor to back up the truck… Really? One of the benefits of using 5 years is it makes calculating rate of return easier. Fairfax has a very concentrated portfolio: Eurobank FFH-TRS Poseidon Fairfax India - primarily BIAL Orla Mining Do I care today that Eurobank was a terrible business in 2014? Nope. What I care deeply about is what kind of business Eurobank is today - and it is a very good business. Could that change? Of course… that is why I listen to every quarterly call). Holdings get much smaller after the big 5. But there are a bunch of stars in there as well. Fairfax’s hit rate the past 5 years is nuts. To this, add the returns on the holdings they sold in the last 5 years: Resolute Forest Products Stelco Sigma Orla (part) Poseidon (part) All were massive home runs (5-year returns). And then, of course, we should also add the gains on the insurance businesses they IPO’d/sold in the last 5 years… this needs to get counted somewhere… Digit Pet insurance Ambridge Euolife’s life insurance business More massive gains… After all, at the end of the day, we are trying to evaluate a management team on their capital allocation skills. It should be fair and balanced and look at all the important pieces. How has Fairfax performed over the past 5 years? They have smoked - absolute and relative to the S&P500. Especially if you use the correct cost basis: FFH-TRS cost basis is not the starting value of Fairfax’s share price. It is much less. Interestingly, the last 5 years had two bear markets: 2022 and 2025 (I think just qualified). There was also a historic bear market in bonds. Yes, the starting point (Dec 31, 2020) was very favourable. But that is when you look at performance vs the S&P500. For the past 5 years, Fairfax’s capital allocation has been best-in-class and it is not close. The fact that people don’t get it is not surprising - this is Fairfax after all.

-

@djokovic1, thanks for the comment. Good luck with the pitch

-

Fairfax built their stake in Seaspan/Atlas over a number of years. And they made a number of different investments (the roll over of APR being one example). To keep the analysis simple (especially the time value of money part) I decided to take a FIFO approach. The key point: Seaspan has been one of Fairfax’s best-ever investments.

-

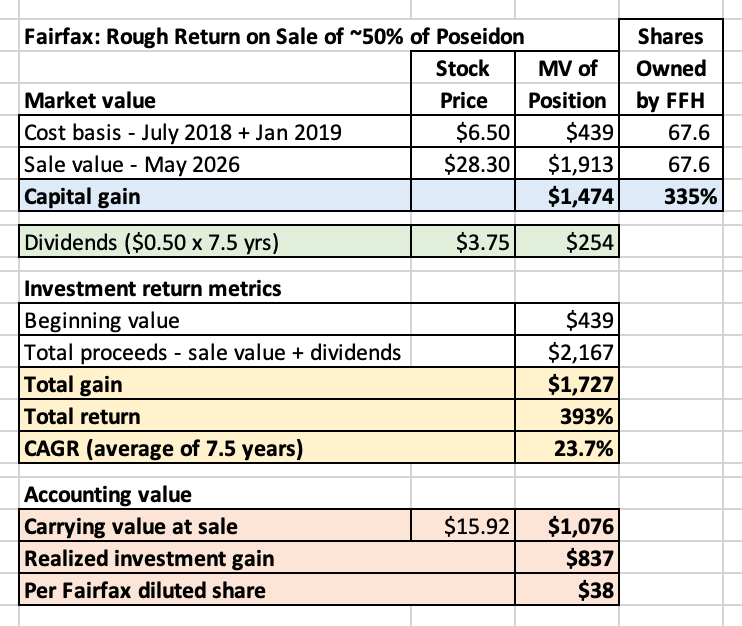

Poseidon: Another Home Run for Fairfax How did Fairfax do on the approximately 50% of its Poseidon position that it sold in May 2026? To answer that question, we will use a simplified approach. Fairfax first acquired shares of Seaspan in July 2018 by exercising warrants and purchasing 38.46 million shares at US$6.50 per share, for a total investment of $250 million. Fairfax completed an identical transaction in January 2019, bringing its ownership to 76.9 million shares at a total cost of $500 million. Over the following years, Fairfax increased its ownership stake. By early 2026, it owned approximately 132.6 million shares of Poseidon. In May 2026, Fairfax completed the sale of 67.6 million Poseidon shares at $28.30 per share, generating proceeds of approximately US$1.9 billion. To keep the analysis simple, Fairfax's original 2018 and 2019 purchases are used as the cost basis. We also assume annual dividends of $0.50 per share throughout the holding period and use a holding period of 7.5 years. This approach ignores subsequent share purchases, preferred shares, and the precise timing of cash flows. As a result, the figures should be viewed as an approximation rather than a precise internal rate of return. Using these assumptions, Fairfax generated approximately: Total profit: $1.7 billion Total return: 393% CAGR: 24% Regardless of the exact methodology used, the conclusion is clear: Poseidon has been one of Fairfax's most successful investments. The position was large, and the returns were extraordinary. Few investments combine both attributes. As a result, Poseidon created significant value for Fairfax shareholders. Importantly, Fairfax still owns a substantial stake in Poseidon (65 million shares). The results above capture only the value that has been realized to date and exclude the value of the shares that Fairfax continues to own.

-

@Txvestor, I get a lot of pushback on my 'New Fairfax' thesis. They went from being a sub par hitter for many years. And then out of nowhere they have become the best hitter (over the past 5 years). Yes, that could be ascribed to luck. But the timeframe is too long and the number of transactions is too large. My view is they became a much better hitter primarily because they changed their approach. Also, when I look at each investment (I like to get into the weeds)... I see a very consistent theme playing out. I think the 'optimize operations' theme is not widely understood or appreciated. This is right out of the Singleton playbook (and Buffett's... he likely lifted it from Singleton). Pre-2018, many of Fairfax's holdings were a mess (in terms of being well run, cash generating companies). Fast forward to today.. the exact opposite. My view is that is not happenstance - that is because of actions management at Fairfax took. Andy got to optimizing insurance around 2011. Fairfax did the same sort of thing with their investment portfolio beginning around 2018.

-

Here is an introduction to the chapter... Chapter 14: The Evolution of Fairfax's Investments Introduction Learning about a company's history can be a valuable exercise for investors. It provides context, helps explain management decisions, reveals how corporate cultures are shaped, and highlights lessons learned along the way. One of the defining characteristics of Fairfax over the past forty years has been its willingness to learn and adapt. The company has enjoyed remarkable successes. It has also made significant mistakes. What is most striking is not that both occurred—it is how Fairfax responded. Fairfax has one of the more colourful histories in modern investing. That history can be both a blessing and a curse. It offers important lessons, but it can also obscure the company that exists today. This chapter attempts to bridge that gap. The first article examines Fairfax's highly successful credit default swap strategy from 2005 to 2009—its version of The Big Short. The second reviews the costly equity hedge and short positions that followed, a decade-long mistake that weighed heavily on shareholder returns. The third analyzes Fairfax's equity investments from 2014 to 2017, a period marked by too many chronically leaking boats. The final article explores the emergence of New Fairfax beginning around 2018, as the company shifted toward higher-quality businesses, stronger management teams, and a more powerful compounding model. Together, these articles tell a story: Success → Mistake → Learning → Transformation More importantly, they explain how Fairfax became the company it is today. History is not the investment thesis. What matters most is where a company stands today—its management team, business fundamentals, capital allocation and future prospects. But understanding how Fairfax evolved provides important context for evaluating the business it has become and where it may be headed. In many ways, the transformation of Fairfax over the past decade is one of the most important parts of the Fairfax investment story.

-

New Fairfax: Moving Up the Quality Ladder (2018–Present) Here is the final article (#4) in my short history on some of Fairfax's investments. "Time is the friend of the wonderful company." — Warren Buffett Something changed at Fairfax around 2018. Trying to identify an exact date is a fool's errand. The transformation was gradual and remains ongoing today. But looking back, it is clear that Fairfax began refining its investment approach and upgrading the quality of the businesses it owned. The company did not abandon value investing. It evolved. What Changed? Three themes increasingly shaped Fairfax's investment decisions: Strong management teams. Strong balance sheets. Profitable businesses. Rather than trying to fix troubled companies, Fairfax increasingly partnered with capable operators who could create value on their own. The goal was no longer simply to buy cheap assets. The goal was to buy better businesses. This shift can be seen in many of Fairfax's major investments since 2018, including Stelco, Seaspan, Bangalore International Airport, Metlen and Orla Mining. At the same time, Fairfax began addressing mistakes from the previous decade. Underperforming investments were sold, restructured, recapitalized or merged with stronger partners. Capital was increasingly recycled from weaker opportunities into stronger ones. The quality of the portfolio steadily improved. Repairing the Past, Building the Future The benefits did not appear overnight. For several years, Fairfax was doing two jobs simultaneously. First, it was repairing the past. Weak investments needed to be sold, restructured or repositioned. These actions often produced short-term losses and disappointing reported results. Second, it was building the future. Successful investments rarely create immediate value. Management must execute. Earnings must grow. Intrinsic value must compound. In many cases, the largest gains emerge years after the original investment is made. As a result, the costs of repairing the portfolio partially obscured the value being created by newer investments. Today, that dynamic has largely reversed. Many of the major portfolio repairs have been completed. At the same time, a number of investments made since 2018 have matured and become meaningful contributors to value creation. Early Results The results can be seen across both new investments and legacy holdings. Stelco Fairfax invested approximately $193 million in Stelco in 2018. When the investment was sold in 2024, total value creation was approximately $544 million, including dividends, share-price appreciation and the value of shares received from Cleveland-Cliffs. The compound annual return was approximately 25%. Seaspan / Atlas / Poseidon Seaspan has become one of Fairfax's most successful investments. In 2026, Fairfax sold approximately half of its position in Poseidon at a substantial premium to carrying value, generating proceeds of roughly $1.9 billion and a pre-tax gain of $837 million. Even after the sale, Fairfax continues to own a significant interest in the business. The Hidden Gems Not all of Fairfax's success came from new investments. The company already owned several hidden gems within its portfolio. In some cases, Fairfax increased its ownership, strengthened the business and simply gave management time to execute. The best example is Eurobank. At the end of 2020, Fairfax's stake had a market value of approximately $900 million. By mid-2026, the investment had created roughly $6 billion of value through share-price appreciation, dividends and shares sold. The compound annual return has been 45%. This is an important distinction. Fairfax did not simply build a better portfolio. It also unlocked value from businesses it already owned. A More Powerful Business Model There is another important development that receives less attention. Fairfax has always centralized capital allocation while decentralizing operations. Since 2018, the company appears to have renewed its focus on improving the performance of the businesses it owns. The objective is not to run subsidiaries from head office. It is to partner with capable management teams, strengthen operations and increase earnings and cash generation. This creates a powerful feedback loop. Better businesses generate more cash. Fairfax can then redeploy that capital into the most attractive opportunities across the organization. Those investments generate additional earnings and cash flow, which can then be reinvested again. The company's earlier investments often consumed capital. Increasingly, its newer investments generate capital. That is a profound difference. In many respects, Fairfax today resembles a younger Berkshire Hathaway. Operations are decentralized. Capital allocation is centralized. Cash generated by one business can be redeployed into opportunities offering the highest returns elsewhere in the organization. The result is a stronger and more durable compounding engine. Why It Matters Understanding this history provides important context for evaluating Fairfax today. For much of the past decade, management's attention was divided between repairing weaker investments and building a stronger portfolio. Today, many of those legacy issues have been addressed. At the same time, the collection of businesses assembled and strengthened since 2018 is beginning to demonstrate its earning power through higher dividends, stronger operating results, increased earnings from associates and investment gains. Fairfax spent much of the past seven years moving up the quality ladder. What has emerged is a stronger collection of businesses, a more disciplined investment approach and a more powerful capital allocation engine. The portfolio repair phase is largely behind it. The compounding phase is increasingly in front of it.

-

One of the things that used to frustrate me about Prem was how generously he praised some of the CEOs running Fairfax's investments. He has always been loyal and people-focused, but the praise sometimes felt disconnected from the results being delivered by some. Today, it feels different. Prem has toned it down, and the calibre of the people running Fairfax's equities is noticeably higher. More importantly, the results are there to support the praise. In many ways, it reflects Fairfax's evolution since 2018: better businesses, better management teams, and better outcomes for shareholders.

-

It is always good to run the numbers. And size matters - focus on the largest holdings. Fairfax's largest holding by a country mile is Eurobank. How has it performed YTD? Value creation = ~$1.3 billion. Rate of return = 25%. Outstanding. The company just paid Fairfax a dividend ($95 million). But that timeframe is too short. Five year return is better. How has it performed since Dec 31, 2020? Value creation = $6.0 billion. Annual rate of return = 45%. Investors? A big yawn. Let's expand the analysis. What is Fairfax's second largest holding? It is FFH-TRS. How has it performed over the past 5 years? Despite being flat year over year, it has been outstanding. What is Fairfax's third largest holding? Poseidon. How has it performed over the past 5 years? It has been outstanding, with a big investment gain coming in Q2. BIAL? Orla? I could go on and on... Fairfax's equity investment have been having an epic run over the past 5 years. And investors? They aren't happy...

-

S&P500 total return has been ~12.7% since 2018. Fairfax’s equity portfolio has smoked that return over the same timeframe. Especially if you calculate Fairfax’s CAGR using carrying value (which is comically low) and include FFH-TRS (which has a very low cost basis). The problem is people do not appear to want to follow the math… (in fairness, it is complicated to calculate). PS: I am not trying to be punchy… I am in a good mood today (hate that when it happens) - I am trying to add some humour to my answers to make them more entertaining.

-

A: CAGR = 25% (I think that is in the ballpark for both holdings) I think Fairfax has been doing quite well since 2018 with their equity portfolio. Short answer: they are wired the way they are wired. These days, I like it. I don’t always understand it. But I didn’t like/understand the Stelco purchase - and I was the idiot. My focus these days with Fairfax is results - how are the individual positions performing and, more importantly, how is the total portfolio performing. Over the past 5 years they have been hitting the ball out of the park - so I am a happy camper. PS: they did load up on ‘quality’ big caps coming out the the Great Financial Crisis. Their problem was they had to sell them too early to cover losses from the equity hedges/shorts. Its not like they have never done it before.

-

I don’t think they are averse. I think they go to where they see the most value. Here is a question for you. The two biggest investments they made in 2018 were Seaspan and Stelco. What is/was the return (CAGR) each of these investments generated since then?

-

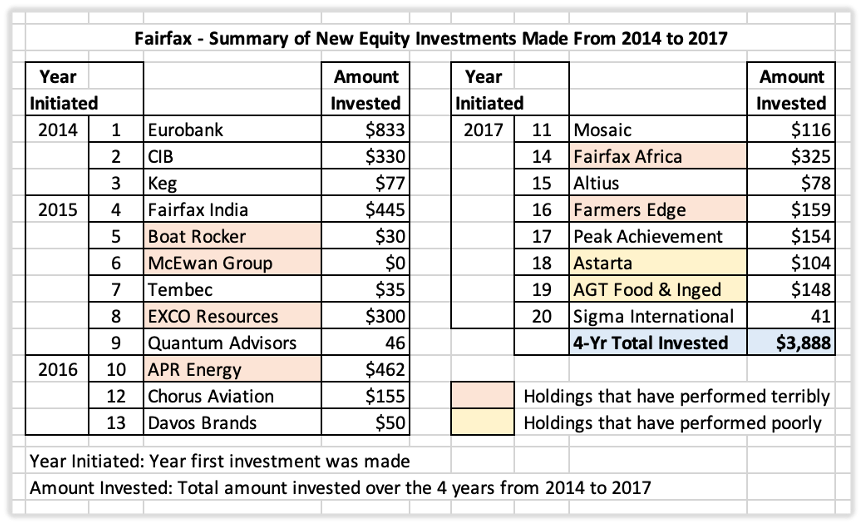

A Review of 2014 to 2017: Old Fairfax – Too Many “Chronically-Leaking Boats” This article #3 in my historical review of some of Fairfax's investments. “My conclusion from my own experiences and from much observation of other businesses is that a good managerial record (measured by economic returns) is far more a function of what business boat you get into than it is of how effectively you row… Should you find yourself in a chronically-leaking boat, energy devoted to changing vessels is likely to be more productive than energy devoted to patching leaks.” – Warren Buffett – Berkshire Hathaway 1985AR Fairfax defines value investing as purchasing securities at prices below intrinsic value while maintaining a margin of safety. The approach is explicitly long term and places unusual emphasis on downside protection and the avoidance of permanent capital loss. From 2014 to 2017, Fairfax doubled the size of its insurance business through aggressive international expansion. As a result, the company's investment portfolio grew significantly. Fairfax also expanded its equity holdings. During this four-year period, it established approximately 20 new positions and invested roughly $3.9 billion. The results were mixed. A number of investments performed well. Unfortunately, many did not. New Purchases: Too Many Clunkers Over the years, Fairfax invested approximately $2.2 billion in eight companies that would go on to produce disappointing results. Two investments largely went nowhere: Astarta AGT Food and Ingredients While neither investment resulted in a significant loss of capital, both generated little return for shareholders over a decade. The opportunity cost was substantial. Capital tied up in stagnant investments cannot be deployed into better opportunities. Six other investments performed much worse: Fairfax Africa EXCO Resources APR Energy Farmers Edge Boat Rocker McEwan Group These investments resulted in significant capital losses. Given Fairfax's emphasis on downside protection and avoiding permanent capital loss, the results were particularly disappointing. What Was the Problem? The problem was not that Fairfax had losing investments. Every investor has losers. The problem was that too many investments shared the same weaknesses. A pattern emerged across many of the holdings: Weak management Weak balance sheets Weak profitability Many suffered from all three. From 2014 to 2017, Fairfax accumulated too many businesses that could fairly be described as chronically-leaking boats. The Overall Portfolio Was Getting Worse The problem extended beyond the new purchases. At the same time Fairfax was making these investments, its equity hedges were forcing the company to sell some of its strongest holdings. Several existing investments were also struggling, including BlackBerry, Resolute Forest Products and Recipe. Fairfax was selling some of its better businesses while adding a number of weaker ones. The overall quality of the equity portfolio was deteriorating. Why This Was a Problem for Fairfax Weak businesses tend to share two characteristics. First, they often consume capital. Companies with weak economics frequently require additional investment simply to survive. Second, they demand management attention. Turnarounds are rarely passive investments. Neither was a good fit for Fairfax. Years of losses from the equity hedges had already reduced financial flexibility. At the same time, Fairfax operated with a highly decentralized structure and a lean head office. The company was not built to oversee numerous troubled businesses simultaneously. As business performance deteriorated, many investments required additional capital and more management attention. The situation became increasingly difficult to manage. The Real Lesson In hindsight, the issue was not bad luck. The issue was process. Fairfax's investment framework had drifted too far toward lower-quality businesses at precisely the time the company needed to move in the opposite direction. “Time is the enemy of the terrible company.” Many of the companies Fairfax was buying required additional capital, intensive oversight and successful turnarounds to generate acceptable returns. Those requirements were increasingly at odds with Fairfax's decentralized operating model and lean corporate structure. The result was a growing mismatch between the businesses Fairfax was buying and the organization Fairfax had become. Fairfax eventually recognized the problem and adjusted its approach. The result was the birth of what I like to call New Fairfax. That article - the last in our series - will be out tomorrow.

-

Here is a stab at what Fairfax might be thinking… Management believes the future is likely to feature higher highs and lower lows in inflation and interest rates. Long-term financing becomes more valuable. From that perspective, paying an extra 1% today for a 30-year bond may be a bargain. Imagine two scenarios: Scenario 1: The last 20 years (1982-2020) Inflation trends lower. Interest rates trend lower. Refinancing gets cheaper over time. In this world, issuing 30-year debt often looks expensive in hindsight because you could repeatedly refinance at lower rates. Scenario 2: Th current environment? Inflation is structurally higher. Government debt levels are much higher. Interest rates are more volatile. The risk of a future refinancing at higher rates is meaningful. In this world, a 30-year bond is valuable because it removes uncertainty. The company is effectively saying: "We are willing to pay a little more today so we never have to worry about what the bond market looks like in 2036, 2046, or 2056." This is very consistent with Fairfax's historical approach to risk management. The company often sacrifices a little current profitability to reduce exposure to adverse scenarios.

-

"The gains from CDS aren't unlimited whereas the losses from equity hedges are unlimited, right?" @Buffett_Groupie, I have added this to my article (to my original, as I can't edit the articles after they are posted to the board - likely because they are so long). I think it explains the assymetic difference in the CDS position and the equity hedge position. Thank you!

-

Here is the link to a good overview of Peller Estates. https://s201.q4cdn.com/211846765/files/doc_presentations/2026/APL-Investor-Presentation-Q3-26-FINAL.pdf The reported purchase price can be misleading... Part of the purchase price will likely be funded with an increase in debt at Peller Estates. The key is how much $ is Fairfax contributing. And what will that investment earn over time? The big question for me is: How good is the management team at Peller Estates? There are lots of interesting angles to this deal: Real estate portfolio and inventory = C$500M Recipe/Keg - this will work both ways... restaurant competitors might not like it. This is a long term business - much better fit as a private company. The sector (alcohol) is pretty out of favour. From an income stream perspective, another addition to the consolidated bucket for Fairfax.