Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

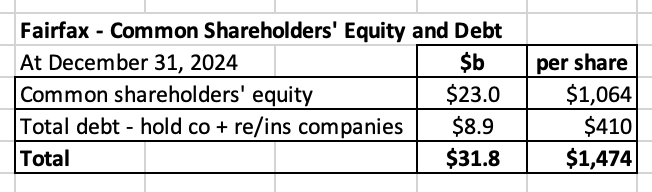

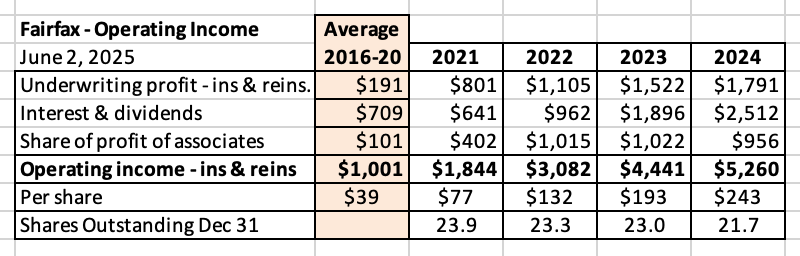

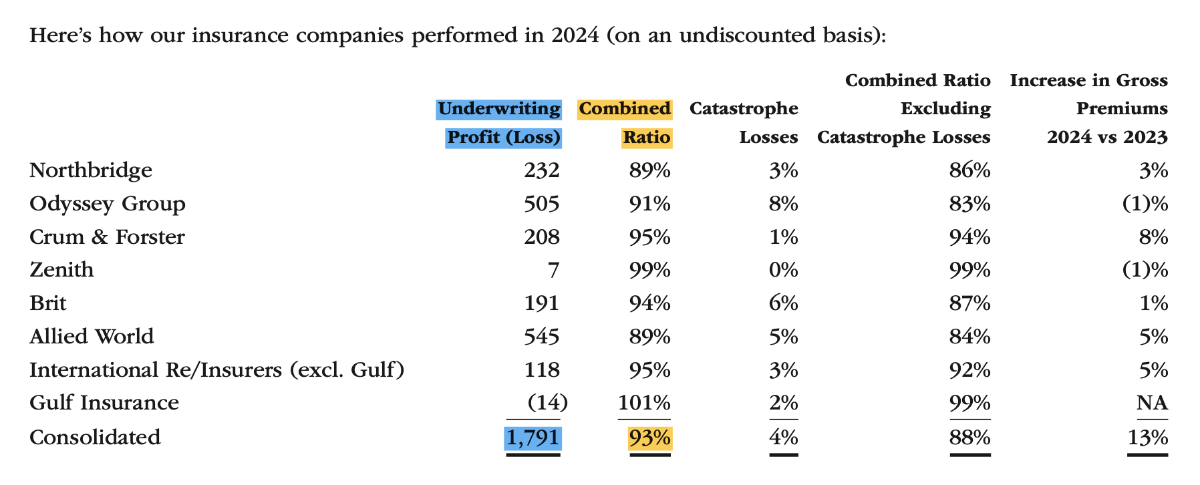

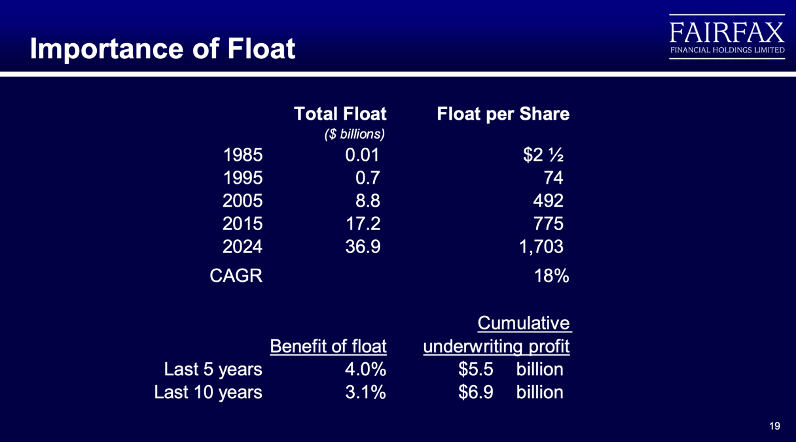

Leverage and Fairfax - A deep dive - Part 1 Introduction “Give me a lever long enough and a fulcrum on which to place it, and I shall move the world.” Greek philosopher Archimedes The fulcrum needs to be rock solid and well placed. The longer the lever the more power it can exert. Used properly, leverage allows one person (or a company in our example today) to figuratively move the world. ————— Leverage In our post today we are going to explore the concept of leverage. And what it means for Fairfax. To see what we can learn about the company today - and what it might mean for the company looking into the future. Getting back to our picture above… The fulcrum is Fairfax’s business model. (Company structure. P/C insurance business. Investment management business. People. Culture.) The lever is a sum of the various forms of leverage that Fairfax uses. Let’s get started. ————— Definition of leverage We are going to define leverage in a very broad way: Using other people and/or their money to boost returns and/or improve the quality of the company. The expectation is the return achieved will be greater than the cost involved. This definition allows us to include both financial and non-financial aspects of leverage (financial capital AND human capital). When investors think of leverage they tend to focus on/think only about the financial piece, and debt specifically. That is true (debt is one kind of leverage). But that is also a very narrow way to think about leverage. Especially when it comes to a company like Fairfax. There are many different kinds of financial leverage. Like float. There are also many different kinds of non-financial leverage. Like having access to a large network of exceptional capital allocators/entrepreneurs - outside of Fairfax (think deal flow). In this post we are going to review the many different ways that Fairfax uses leverage. We are going to stretch the definition - so much so that you might even disagree with us. I hope that happens - and you share your thinking. After all, engaging in constructive debate is how we all learn and get better as investors. If we want to make people uncomfortable, a good way to do it is to challenge conventional wisdom. —————- Buffett and leverage “If you’re smart you don’t need leverage; if you’re dumb, it will ruin you.” Warren Buffett “My partner Charlie says there is only three ways a smart person can go broke: liquor, ladies, and leverage. Now the truth is, the first two he just added because they started with ‘L’ – It’s leverage.” Warren Buffett Before we go any further we need to deal with the elephant in the room - yes, that guy named Warren Buffett. Buffett is the GOAT. Many P/C investors worship at the altar of Buffett. I am (generally) one of them. What does Buffett have to say about leverage? If you do a search online, Buffett probably has more great quotes on leverage than just about any other topic - and he is almost always telling investors that it is the devil and should not be used. Is this true? Does Buffett really dislike leverage? No, of course not. Buffett loves leverage. Buffett has said repeatedly that P/C insurance was the core engine that drove the fantastic returns that Berkshire Hathaway was able to deliver over the past 59 years. What was it about the P/C insurance business that Buffett liked so much? It was the low cost and growing float that it provided. And float is leverage. Context matters The lesson is leverage is not a four letter word - it is not inherently good or bad. Yes, leverage can be bad. But it can also be good. Obviously, which one it is (good or bad) depends on how it is being used. I know it sounds like blasphemy, but as investors there are some things we need to unlearn when it comes to Buffett’s teachings. How to think about leverage is one of them (in the context of our post today). Readers should try and keep an open mind as they keep reading… ————— A (short) review of the different types of leverage that Fairfax uses The goal of this post is to provide readers with an overview of the topic. I am also going to try and keep this post to a reasonable length (having said that, it is still going to be long). As a result, my review of each type of leverage that Fairfax uses is going to be very top line. This post will be broken into the following pieces: Financial Debt - At the holding company & re/insurance operating company level Float - From P/C insurance Equity - Minority partners (2015-2017) Fairfax total return swaps (late 2020/early 2021) Dutch auction (late 2021) - Minority partner Debt - Held by the equity holdings (public and private) Non-financial (human capital) External relationships/partnerships Fairfax has cultivated We are going to tackle the topic in three posts. This is the first and it introduces the topic and goes into the first two items listed above: debt and float. The second post should be out in the next week or so and will review items #3, 4 and 5 on our list above. The final post will review the remaining items and summarize what we have learned on the topic. Let’s get started. —————— Debt - At the holding company & re/insurance operating company level Fairfax borrows money to boost the returns it earns for shareholders. At December 31, 2024, Fairfax had borrowed a total of $8.86 billion - at the holding company and re/insurance company level. This does not include the debt of the non-insurance operating companies (like Recipe or Thomas Cook India) as Fairfax does not guarantee this debt. We will come back to this topic later in the post. What is the cost of the debt? In 2024 total interest paid by Fairfax on this debt was $456.6 million. My very rough guess is Fairfax is paying an average interest rate on its debt of around 5.6%. Importantly, the total amount of interest paid is tax deductible. So the after-tax rate paid by Fairfax is lower. Common shareholders’ equity (CSE) and debt Common shareholders equity at Fairfax totalled $23 billion at December 31, 2024 or $1,064/share. By using debt, Fairfax now has $31.8/billion, or $1,474/share it can use to generate a return for shareholders. What return is Fairfax delivering on its investments? Fairfax is current generating a total return of about 7.5% on its total investment portfolio. This return is well in excess of its cost to borrow (which I estimated earlier at about 5.6% pre-tax). Should an investor in Fairfax be worried about the amount of debt Fairfax is carrying? For help here, we can lean on the ratings agencies. Specifically AM Best (they are focussed on the P/C insurance industry). What does AM Best think? They have upgraded Fairfax’s credit rating twice in the past 2 years. Why? “The outlook revision to positive for Fairfax reflects the improved earnings profile of the consolidated group. Fairfax deployed significant cash into highly rated fixed income instruments as interest rates increased in 2022. This resulted in dividend and interest income run rate more than tripling by year-end 2023. This improved investment cash flow, coupled with continued stabilization of underwriting earnings at various operating subsidiaries, has resulted in improved operating performance metrics relative to peers in recent years, and prospectively.” https://news.ambest.com/PR/PressContent.aspx?refnum=34689&altsrc=9 Over the past 4 years, operating earnings at Fairfax have spiked higher. From an average of $1 billion per year (from 2016 to 2020) to $5.3 billion in 2024. That is a seismic improvement. The quality of the earnings that Fairfax is delivering has never been better. And look poised to grow further from here. As we reviewed, Fairfax’s total interest cost on its borrowings was $456.6 million in 2024. This is a small number compared to the operating earnings that Fairfax is delivering ($5.3 billion in 2024). Debt is an important source of leverage for Fairfax. But it is not its most important source (by far). Float Fairfax has $36.9 billion in float. This is $1,703/share. In the last 4 years, float per share has increased by 84% = CAGR of 16%. Yes, the size of float is massive. And it is growing in size. What is the cost of float? The cost of float is measured by looking at the combined ratio (CR). Fairfax’s insurance companies delivered a CR of 93% in 2024, or an underwriting profit of $1.79 billion. This is also a measure of the quality of Fairfax’s P/C insurance franchise - like other parts of the company, it has been increasing in quality over the past 5 years. This means the cost of Fairfax’s float is zero. Actually, it is much better than that. Fairfax is getting paid to hold its float - it was paid about $1.79 billion in 2024. So Fairfax has $36.9 billion in float. And it is getting paid to hold it. Crazy but true. What can Fairfax do with its float? It can invest it. And keep what it earns. Wow! This explains the power of the P/C insurance model Warren Buffett has said repeatedly that P/C insurance (and the growing, low cost float that it provides) was the engine that propelled Berkshire Hathaway’s unbelievable growth since National Indemnity was purchased in 1967. Common shareholders’ equity (CSE), debt and float Fairfax has a large and growing float. It is getting paid handsomely to hold it. And it gets to keep everything it earns from it. Given its size (and cost), float is by far the most important kind of leverage Fairfax uses. Float is 1.6 x (larger) than the size of shareholders’ equity. Adding all three together (CSE + debt + float), Fairfax has $69 billion, or $3,171 per share, that it is able to invest to earn a return for shareholders. Investment leverage We can measure Fairfax’s investment leverage by dividing the total by CSE. $68.7 billion / $23 billion = 3.0x Fairfax has very high investment leverage. This amplifies the impact of Fairfax’s investment returns on its return on equity. What is the return of the investment portfolio? Fairfax has an investment portfolio of $69 billion Fairfax’s investment portfolio is currently generating a pre-tax return of about 7.5% or about $5.175 billion per year. This is $240 per Fairfax share. Cost of debt was $457 million in 2024. ‘Cost’ of float was a benefit (underwriting profit) of $1.8 billion in 2024. Is Fairfax’s use of leverage boosting the earnings of the company? Yes. Big time. This is a very powerful combination / result. Fairfax’s use of debt and float are examples of structural uses of leverage for Fairfax - a permanent part of the capital structure of the company. Debt and float fall on the liability side of Fairfax’s balance sheet. Next, we will review some examples of leverage that Fairfax employs that are more tactical in nature - temporary, to take advantage of a short term opportunities when they pop up. With our next example, we are going to review how they use the asset side of their balance sheet to get leverage. We will review the remaining ways that Fairfax uses leverage in part 2 of our post. It should be out in about a week.

-

I am cheering for OKC. It would be great to see them win it all. I would love to see Presti rewarded for what he was able to do after losing Durant. The crazy thing is OKC is loaded with young talent and draft picks… If they win this year they might be able to become as close to a dynasty as we will see in the NBA. I think the challenge for OKC might be how young/inexperienced they are. Indiana is a good team. Nice to see them get through in the East.

-

@SafetyinNumbers , regarding the comparison to BRK, you highlight the differences in the two companies (correctly so). Fairfax today is not a clone of 1990’s Berkshire Hathaway. The comparison is the fact they both exploit the P/C insurance model to deliver exceptional results for shareholders over an extended period of time. Exactly how Fairfax will do it will be very different from how Berkshire Hathaway did it. I know you understand this. Fairfax and Berkshire Hathaway are like two kids. As a parent, you want both of your kids to be successful. Do they need to get there by doing exactly the same thing? No, expecting that would be stupid (for you and the kids). They need to find their own way. Just like successful companies. Fairfax, like many kids, has made its share of mistakes over the years (with both insurance and investment management). But each time, it has also learned from these mistakes. As a result it is now a more mature, stronger company. This makes it more valuable (IMHO). It means it is a learning organization.

-

@SafetyinNumbers, you bring up a great topic: leverage. As you point out, Fairfax has an enormous amount of leverage to float. More than most P/C insurance companies. But they also have other kinds of leverage: - Debt - at holding company With their insurance business: - Minority interests With their investment management business: - FFH total return swaps - Debt - at operating company (Recipe is a good example) They also have significant non-financial leverage today: - Relationships - with other external capital allocators. This positively impacts deal flow (which @nwoodman has commented on in the past). A good recent recent example of this is the PacWest real estate portfolio (and team) that Kennedy Wilson purchased. Fairfax and KW were very opportunistic - the deal closed in something like a month. Pac West was forced to sell one of its best assets. Fairfax now has $5 billion earning a yield of something like 8% on average. KW is a stronger company (they have added another business/income stream to their business). This deal happened because of KW and their relationship with PacWest. Bottom line, Fairfax uses a lot of different kinds of leverage today. Most importantly, they use it responsibly. It will help Fairfax deliver higher results moving forward (compared to if they did not use it). This is not well understood by most investors/analysts. This is leading them to underestimate Fairfax’s future results. This in turn leads many of them to undervalue the company (still).

-

@nwoodman, I agree. Fairfax has alignment on the investment management side of the business today. They have ‘tweaked’ their investment framework over the past 8 years. And the people they have in their investment team today are a great fit for that improved investing framework. Of course, I am speculating when I say this. But the turnaround in the investment management side of the business has been too pronounced to just be happenstance. But there is much more to this story. Fairfax is loaded with exceptional talent in its P/C insurance business. Of course, Andy Barnard is the GOAT. But the next level of executives are also exceptional. Like @gfp said, this also really stood out to me attending the last two AGM’s and having the opportunity to listen to the different leaders talk. But there is much more to this story. Fairfax has completely reimagined its equity portfolio over the past 8 years. They are now partnered with an amazing collection of outstanding capital allocators: - Fokion Karavias - Eurobank - David Sokol - Poseidon - Hari Marar - Bangalore International Airport - Pierre Lassonde - Orla Mining (gold) and Foran Mining (copper) - Byron Trott - BDT Capital Partners - Alan Waterous - Waterous/Strathcona - Christine Magee - Sleep Country - Alan Kestenbaum - Stelco (yes, this position was sold late in 2024 for a massive gain) There are many more names I could have put on this list. At Fairfax today we have a wicked confluence of events that have all come together at the same time - it is like magic. The business model for insurance. The business model for investment management. How the two businesses are staffed. The people Fairfax is now partnered with in their equity holdings. Fairfax - as a company - is now running like a high performance racing car. But there is even more to the story. And that is the external environment. Fairfax’s business model/capabilities/partnerships today are perfectly matched to the current business/investment environment (elevated volatility, higher inflation, extreme focus on short term). And there is one more thing… Fairfax trades at a valuation that is lower than peers (P/BV and PE). And when you include the value that is ‘hiding’ today on its balance sheet (one example is excess of FV over CV for non-insurance associate and consolidated holdings), it is trading at a valuation that is much lower than peers. So an investor can get everything discussed above when it is (still) trading at a large margin of safety. Except Fairfax has just taken their improved race car on the track - they have only run a couple of laps. The race has just gotten started. For Fairfax. This is a similar set up to Berkshire Hathaway in the 1990’s. How many investors missed out on investing in Berkshire Hathaway back then? Fairfax is being similarly underestimated today. (And I love it.) The company is much higher quality (for the reasons discussed above) than most investors think. You don’t make money by thinking (and doing) what everyone else is thinking (and doing).

-

The FFH-TRS could well become Fairfax's best ever investment. And that is because the amount they likely had to put out was very small. And the return has been massive. Does anyone know how to calculate the return on an investment like this? The FFH-TRS is also interesting as an investment. With this investment, Fairfax acted like a hedge fund. In my post on Recipe, Fairfax has acted like a private equity fund ('LBO light'). With their investment in Ki (and Digit before), Fairfax acted like a venture capital fund. With their investment in PacWest (with Kennedy Wilson), Fairfax acted like a distress debt fund. Importantly, Fairfax has developed these capabilities largely internally. They also have a global presence (especially India). Fairfax is also partnered with some amazing entrepreneurs/individuals (with its basket of equity holdings). It really is amazing the platform that Fairfax has built with its investment management business - it is incredibly diverse. This gives them an enormous amount of flexibility moving forward. They fish in so many different ponds. And they are very good at what they do.

-

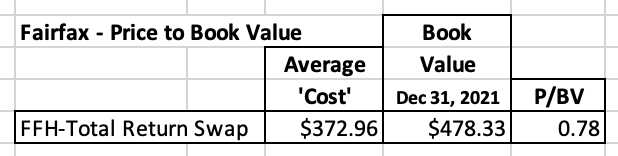

Fairfax Total Return Swaps – A stealth buyback of 1.96 million shares? (Hat tip to @SafetyinNumbers for helping me with this post.) Fairfax’s second largest equity holding is the total return swaps that it holds giving it exposure to 1.76 million Fairfax shares (FFH-TRS). The position has a notional value of $3.0 billion at May 27, 2025. This position represents about 12% of Fairfax’s total equity portfolio of $24.3 billion. Fairfax put on this position in late 2020/early 2021 when their shares were trading at a ridiculously low price (US$373/share). The initial position size was 1.96 million shares. In Q4, 2024, Fairfax reduced the position to 1.76 million shares (more on this later in the post). When they put this position on, Fairfax was thinking big - below is what Prem had to say in Fairfax’s 2020 annual report: “We think this will be a great investment for Fairfax, perhaps our best yet!” Prem Watsa 2020AR How has the investment performed over the past 4.5 years? Since being put on, the FFH-TRS position has delivered to Fairfax a total return of about $2.54 billion. This is before carrying costs. That is an exceptional return over a 4.5-year period. As Fairfax telegraphed in their 2020 annual report, the FFH-TRS has become one of their best investments ever. The total return for this investment can be calculated by adding together two components: The increase in market value of the current position = $2.34 billion The increase in value of the position that was exited in Q4, 2024 = $208 million The FFH-TRS investment is just one example of the many exceptional investments/decisions the team at Fairfax have made over the past 7 or 8 years. The value creation for Fairfax and its shareholders has been enormous. Over the past 5 years the senior management team at Fairfax has been delivering a master class in how to do capital allocation. This might sound like hyperbole – but it isn’t. The genius of the FFH-TRS investment has been lost on many investors/analysts. Probably because a total return swap is a non-traditional type of investment for a P/C insurance company to make (it is a tool more commonly used by hedge funds). So, it has been largely ignored by investors/analysts in their analysis of the company and its potential impact on earnings. This is one reason why investors/analysts have been consistently too low with their earnings estimates for Fairfax. Given the importance of this investment, let’s review it in more detail. Margin of safety Was Fairfax’s investment in FFH-TRS made with a margin of safety? The traditional way to value an insurance company is to use price to book value (P/BV). Fairfax’s FFH-TRS investment was established in late 2020/early 2021 at an average price of $373/share. At December 31, 2020, Fairfax’s book value was $478.33/share. Fairfax established their position at a P/BV multiple of 0.78. Fairfax’s purchase was made with a very large margin of safety. Circle of competence Was the FFH-TRS in Fairfax’s circle of competence? Yes, this is a stupid question. Fairfax understood this investment better than anyone else. Back in late 2020/early 2021 – Fairfax KNEW what Fairfax was worth. They knew the company was being criminally undervalued by Mr. Market. And they yelled it from the roof tops – in June of 2020, CEO Prem Watsa bought $150 million in stock paying $311/share. So, this was a HIGH CERTAINTY investment for Fairfax - which also made it a very low risk investment for Fairfax. The quote below is from Fairfax’s news release from June 15, 2020: ----------- Prem Watsa Acquires Additional Shares of Fairfax Mr. Watsa commented as follows in connection with this purchase: “At our AGM and on our first quarter earnings release call, I said that our shares are ‘ridiculously cheap’. That statement reflected my recognition that in the 35 years since Fairfax began, I have never seen Fairfax shares sell at a bigger discount to their intrinsic value than they have recently. I have now backed up my strong words by purchasing close to US$150 million of Fairfax shares in the market over the last few days, as I believe that this will be an excellent long term investment.” Fairfax news release June 15, 2020 ------------ Position size What should an investor do when they find a great investment that they understand better than anybody else and it is trading at a historically cheap valuation? They should ‘back up the truck.’ They should make the investment a concentrated position. What did Fairfax do? They got out their elephant gun. In late 2020/early 2021 Fairfax established a position in FFH-TRS that gave them exposure to 1.96 million Fairfax shares. This position represented 7.5% of Fairfax’s effective shares outstanding (26.18 million). How did Fairfax pay? The FFH-TRS position had a notional value of $731 million. That is what it would have cost Fairfax to buy 1.96 million shares. Back in late 2020/early 2021, Fairfax did not have a lot of extra cash. The hard market in P/C insurance was taking off. Therefore, the priority for excess capital was to grow the P/C insurance business. Fairfax also closed out its last short position in December 2020 and this resulted in a $529 million investment loss. So, Fairfax got creative. They pulled a play from the hedge fund playbook. They didn’t buy shares directly. They did the next best thing… they put on the FFH-total return swap position. This kept their capital outlay to a minimum. And they got exposure to the underlying stock (without actually owning it). This investment demonstrates Fairfax’s management team at their best FFH-TRS investment: Purchased with a large margin of safety In their circle of competence Concentrated position. Very creative in execution – used total return swaps With this investment, Fairfax was very rational. And opportunistic. The FFH-TRS has been a brilliant investment by Fairfax - especially given the circumstances. What is the outlook for this investment? Three things are happening at Fairfax at the same time: Growing earnings – The fundamentals of the company continue to improve. Multiple expansion – Sentiment/narrative is improving. Lower share count – Company continues to be aggressive buying back shares. As a result, Fairfax’s share price has spiked higher in recent years. Despite the big move higher, Fairfax’s share price today continues to trade at a discount – especially when compared to P/C insurance peers. Bottom line, the outlook for the FFH-TRS investment is very good. What is Fairfax’s exit strategy for this investment? At the end of the day, the FFH-TRS position is an investment for Fairfax. Like all their investments, they have an exit strategy. In Q4, 2024, Fairfax did reduce the position size by 203,800 shares, from 1.96 million shares to 1.76 million shares. Why did they do this? Perhaps the primary reason was to reduce the position size of the investment. Not because they felt the investment had become fully valued. But guess what happened to the shares? The 203,800 shares were purchased (and cancelled) from the counterparty by Fairfax. The reduction in the FFH-TRS position ended up being executed as a share buyback by Fairfax. The cost buy back 203,800 shares in December 2024 was about $284 million ($1,393/share). In 2024, the FFH-TRS investment increased in value by about $922 million. The buyback was funded from the increase in the value of the position. This might explain what Fairfax’s end game is with its FFH-TRS investment – it is really a stealth buyback of 1.9 million Fairfax shares. With the buyback funded over time by the return being delivered by the investment. Yes, that is brilliant capital allocation. ————— A note on share buybacks Fairfax has said they believe their stock is very undervalued. They have also said that as the hard market in insurance slows, they will look to use excess capital to buy back their stock more aggressively (and that is what we saw them do in 2024). Every $100 increase in the Fairfax’s share price equals a $175 million investment gain (pre-tax) on the FFH-TRS position. The FFH-TRS investment makes share buybacks an even more compelling capital allocation decision for Fairfax. Is the FFH-TRS investment just like a buyback? When Fairfax buys back stock, the company (and investors) get a double benefit to EPS: The FFH-TRS investment increases the numerator (earnings). Buybacks lower the denominator (per share). The FFH-TRS is the next best thing to doing a big buyback. ————— An underappreciated investment within the analyst community Analysts really struggled to understand the FFH-TRS investment. This can be seen in the Q&A portion of Fairfax’s Q4, 2020 conference call that took place in February of 2021. Prem’s answer to question from Mark Dwelle (RBC) on the Q4 conference call in February of 2021. Mark Dwelle: “My second question relates to executing the total return swap with respect to Fairfax shares. I guess, I was just curious why you pursue that structure, rather than just buying back the stock, if you felt like that was the good opportunity? I mean, is this a capital constraint that you couldn't really buy back that much?” Prem Watsa: “…yes, we have to be very careful in terms of how much we can buy back. When we looked at Fairfax as a stock and looked at everything else that we could buy... we paid US$344 per shares, our book value is $478. I mean, if you (do) the math, just on (a) book value basis, we'd have about $200 million gain. And Fairfax stock price for book value is worth another 200 million. We just think it's a terrific investment and our total return swap structure was a very good way for us to do it. And so we did it.” Why buy the TRS-FFH versus simply buying back stock? Fairfax did not have the cash at the time to buy back a significant amount of Fairfax stock directly. Again, from the Q4 2021 conference call. Mark Dwelle: “I don't disagree with you that it was a good strike price, I guess it was really -- the form of the transaction rather than just actually buying the shares, using a derivative instead is just -- it's a little bit unusual. I haven't usually seen that with most of the companies that I've followed. So that was really my main question.” Prem Watsa: “Yes, so, Mark, our point is just that we wanted to… have more than $1 billion in cash … we just wanted to be financially sound, and in all ways, as opposed to use that cash at this point in time.” ————— Comments from Prem about the total return swap position from the 2020AR. (Please note, in early 2021, Fairfax increased the size of the FFH-TRS position from 1.4 to 1.96 million shares). “Throughout much of last year following the pandemic-induced market plunge, I made public statements to the effect that our belief was that Fairfax shares were trading in the market at a ridiculously cheap price. In the summer I backed that up by personally purchasing close to $150 million of shares. Additionally, following our value investing philosophy, since the latter part of 2020 Fairfax has purchased total return swaps with respect to 1.4 million subordinate voting shares of Fairfax with a total market value at the time of those agreements of $484.9 million ($344.45 per share). We think this will be a great investment for Fairfax, perhaps our best yet!” “Investment returns are very sensitive to end date values, so with a stock price of only $341 per share at the end of December 2020, our five and ten year and longer returns have been affected. We expect this to change as Fairfax begins to reflect intrinsic values again. Nothing that a $1,000 share price won’t solve!” Prem Watsa Fairfax 2020AR ————— Total Return Swap: Some Additional Details The other major benefit of a total return swap is that it enables the TRS receiver to make a leveraged investment, thus making maximum use of its investment capital. Unlike in a repurchase agreement where there is a transfer of asset ownership, there is no ownership transfer in a TRS contract. This means that the total return receiver does not have to lay out substantial capital to purchase the asset. Instead, a TRS allows the receiver to benefit from the underlying asset without actually owning it, making it the most preferred form of financing for hedge funds and Special Purpose Vehicles. There are several types of risk that parties in a TRS contract are subjected to. One of these is counterparty risk. When a hedge fund enters into multiple TRS contracts on similar underlying assets, any decline in the value of these assets will result in reduced returns as the fund continues to make regular payments to the TRS payer/owner. If the decline in the value of assets continues over an extended period and the hedge fund is not adequately capitalized, the payer will be at risk of the fund’s default. The risk may be heightened by the high secrecy of hedge funds and the treatment of such assets as off-balance sheet items. Both parties in a TRS contract are affected by interest rate risk. The payments made by the total return receiver are equal to LIBOR +/- an agreed-upon spread. An increase in LIBOR during the agreement increases payments due to the payer, while a decrease in LIBOR decreases the payments to the payer. Interest rate risk is higher on the receiver’s side, and they may hedge the risk through interest rate derivatives such as futures. https://corporatefinanceinstitute.com/resources/derivatives/total-return-swap-trs/

-

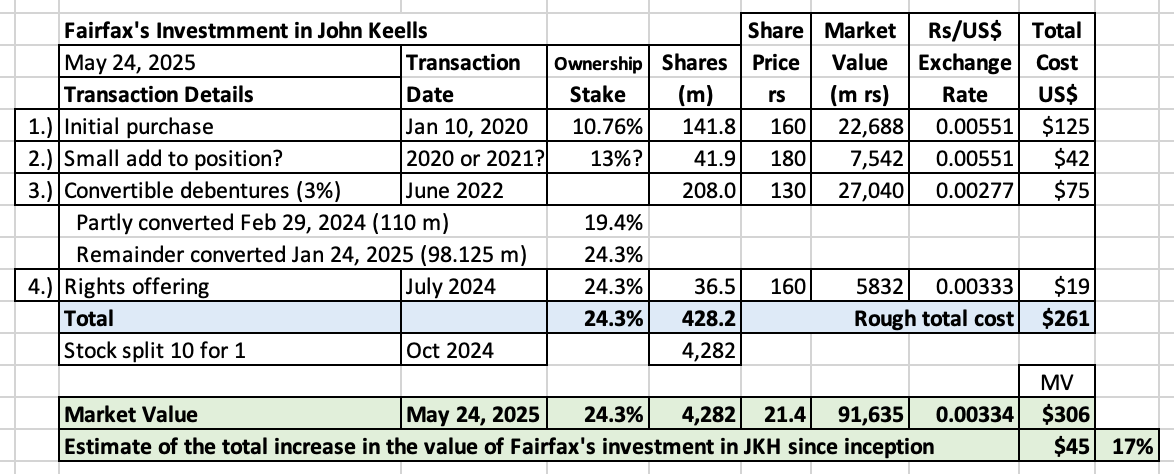

@glider3834 , thanks for the update on John Keells. It motivated me to do an update myself... ---------- John Keells Holdings With a market value of around $300 million, John Keells Holdings (JKH) is a top 20 equity holding for Fairfax (about #18 as of today). JKH is the largest publicly traded conglomerate in Sri Lanka with an operating history of more than 150 years. The group has 7 business segments – leisure, property, transportation, consumer foods, retail and financial services. In Sri Lanka, Fairfax also owns 15% in JKH Group entity Nations Trust Bank and an 78% stake in general insurer Fairfirst. ---------- JKH corporate website: https://www.keells.com/investor-relations/ Corporate presentation February 2025: https://www.keells.com/resource/reports/investor-presentations/investor-presentation-Q3-2025.pdf ----------- A short review of Fairfax’s investment in JKH: Fairfax made their initial investment of $125 million in JKH in 2020 (for a 10.76% position). It appears Fairfax purchased more shares in 2021, increasing their position to about 13%. In June of 2022, JKH raised $75 million (convertible debentures) to help the company get through the economic/currency crisis and fund the construction of the Columbo West International (Container) Terminal (CWIT) in the port of Columbo. Fairfax purchased all debentures and converted them to stock in 2024 and 2025. Post conversion, Fairfax owned about 24.3% of JKH. In July 2024, JKH raised another $150 million in a rights offering to allow it to complete the large City of Dreams real estate project. Fairfax participated proportionately, which kept their ownership position in JKH at 24.3%. In October 2024 (when the rights offering closed), JKH did a 10-for-1 stock split. From 2020 to 2025, Fairfax invested a total of $261 million in JKH. The market value of their position is about $306 million. The total return is about $45 million or 17% (not including interest earned on convertible debentures). It is surprising that Fairfax's investment is up at all, given the size of the economic/currency crisis that hit the country in 2022. @glider3834 , as you pointed out, Fairfax was very opportunistic with its $75 million investment in 2022. This part of their investment is up about 100% (including currency). Importantly, JKH looks well positioned as an investment for Fairfax moving forward. ———— Comments from Prem about John Keells from Fairfax’s 2024AR. “Led by its outstanding Chairman and CEO Krishan Balendra, John Keells Holdings (JKH) is the largest listed conglomerate with over 150 years of history in Sri Lanka, with a significant presence and great record in leisure, consumer foods, retail, transportation, property and financial services and a great long-term record. In the middle of the external crisis faced by Sri Lanka, the company raised $75 million in equity capital, entirely provided by Fairfax in the form of convertible debentures, to fund the West Container terminal in the port of Colombo. Its construction has progressed well, and the first phase of operation is expected to commence in March 2025. In 2024, JKH raised $80 million through a rights issue for LKR 160 per share to fund the completion of the City of Dreams Sri Lanka (casino resorts). JKH is developing the resort in strategic partnership with Melco Resorts & Entertainment, a Hong Kong based gaming and entertainment company, the casino resort is expected to commence in mid-2025. Fairfax participated in the rights issue to the extent of its entitlement. Post conversion of the debentures in January 2025, Fairfax’s shareholding increased to 24.5%, making it the largest shareholder of the company. The Sri Lankan economy appears to have stabilized after severe macroeconomic turbulence with a GDP growth outlook of approximately 3.5% in 2025, primarily driven by the revival of tourism. External debt restructuring, IMF funding, and financial assistance from India have helped Sri Lanka come out of the crisis and rebuild its foreign exchange reserve, providing a much-needed buffer against external shocks. Both the Sri Lankan economy and JKH are poised to perform well going forward. Both the currency and the underlying stock have appreciated considerably since our investment. Fairfax is currently carrying the investment at $282 million against its market value of $331 million.” Prem Watsa – Fairfax 2024AR ———— Sri Lanka's economy grew 5% in 2024 in strong rebound from financial crisis https://www.reuters.com/markets/asia/sri-lankas-economy-grew-5-2024-rebounding-crisis-2025-03-18/ First fully automated terminal at Colombo Port commences operations https://youtu.be/tsmULl9SgjY?si=kGsklSgMETo4J9m2 ———— At February 28, 2025, Fairfax owned 24.31% of John Keells (from the corporate presentation linked above).

-

When it comes to capital allocation, the management team at Fairfax has executing exceptionally well over the past 7 or 8 years. I thought it would be interesting to try and identify what their 'best' decision has been. I expanded the time-frame to 10 years. Please let us know what you think. In the comment section, please let us know what your choice was and why (especially if you choose 'other'). I did not define what I meant by 'best'. You get to decide this for yourself. Please let us know what your definition is: Past return delivered? Future return potential? Made Fairfax an improved/stronger company? Some combination of the above? Something else entirely? How will the Corner of Berkshire/Fairfax mob vote? I have no idea. But I look forward to the discussing/debating this critically important topic. What is my choice? It is going to be the 'Other' bucket. I'll provide details in a couple of days - I want other board members to go first. PS: It is instructive to put together a list of some of the items that did not make the list. Here are a few: Sale of First Capital in 2018 for $1 billion gain (after tax) Sale of pet insurance business in 2022 for $1 billion gain (after tax) Sale of Resolute Forest Products in 2022 at top of the lumber cycle Sale of Stelco in 2024 to Cleveland Cliffs for nosebleed high price

-

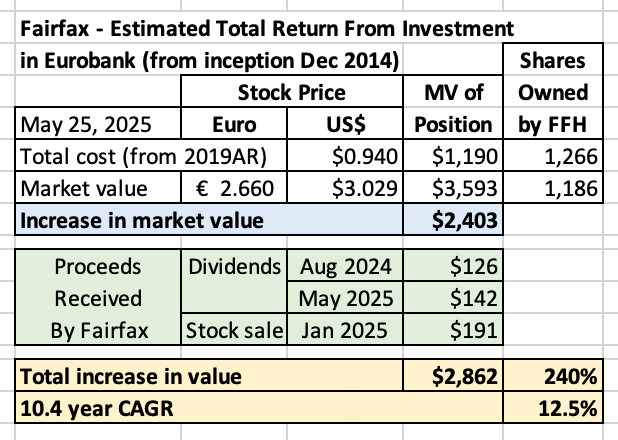

With a cost basis for Fairfax of $1.19 billion, my guess is this includes the initial investment in Eurobank in Dec 2014 of $444 million that went up in smoke. What does the 10-year CAGR of 12.5% tell us? On its own, very little. It really matters only to investors who bought Fairfax back in 2014 (or earlier) and still hold their shares today. All of my shares in Fairfax were bought late in 2020. Do I care about what Eurobank's CAGR was for Fairfax from 2014 to 2020? No. What I care deeply about is what Eurobank’s CAGR for Fairfax was from 2020 to 2025. And it has been stellar. Sequence of returns matters. Eurobank is the poster child of how important this is for an investor (to understand). Yes, Eurobank sucked as an investment from 2014 to 2020 (Greece was in a depression). And it has absolutely rocked as an investment from 2021 to 2025. The Greek economy is doing well. Eurobank is exceptionally well managed. Despite the big move higher, the stock is cheap. And its prospects have never looked better.

-

Has Eurobank quietly become Fairfax’s best equity investment ever? It has delivered a total return from inception (Dec 2014) of about $2.8b. Of note, the entire return has come over the last 4.5 years. Trading at €2.66/share, Eurobank’s stock is still undervalued - suggesting there is much more upside to come from here. The dividend Fairfax is receiving from Eurobank is larger than the cumulative dividends Fairfax is receiving in a year from all of its mark to market common stock holdings. Many of Fairfax equity holdings are generating lots of cash (Eurobank, Poseidon, Recipe etc). Some of that cash is making its way to Fairfax. Welcome to new Fairfax.

-

@nwoodman, you make many great comments. The deal flow angle might be key moving forward - kind of what happened with Sleep Country. It makes sense entrepreneurs will want to parter with Fairfax (for the reasons you provided). I am also learning that when evaluating Fairfax’s investments it is critical to understand how much capital they are putting in and what the return on that will be (and not focus less on deal size). Sleep Country is a good example of this. The minority partner angle is also super interesting to me - where Fairfax uses equity to get ‘other people’s money’ - which is another important source of leverage. Fairfax used this extensively when making their many insurance acquisitions from 2015 to 2017. And they used it again as a source of cash when they sold 9.9% of Odyssey to fund the dutch auction (2 million share buyback at $500/share). Leverage allows Fairfax to earn a higher return on its equity. We typically only look at debt to understand Fairfax’s leverage. We probably should include the equity (minority partners) as well. I find it really interesting how unique/creative Fairfax is when it comes to capital allocation.

-

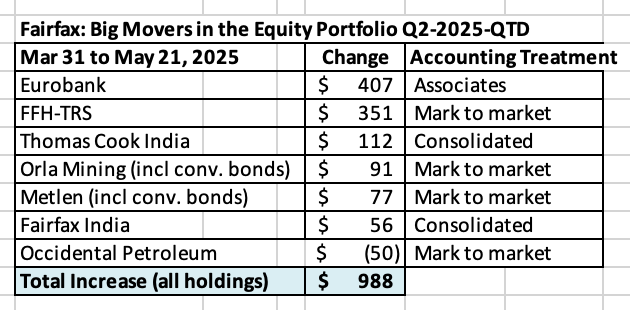

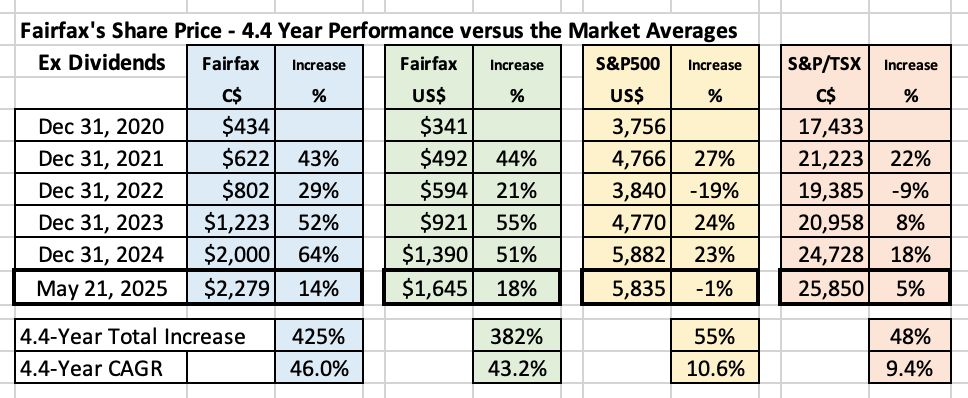

How is Fairfax's equity portfolio performing so far in Q2-2025? Very well. To May 21, it has increased in value from $23.2b to $24.2b. QTD is up about $988m or $46/share (pre-tax). The two largest holdings, Eurobank and FFH-TRS are the two stars. International is doing well. I have attached my Excel spreadsheet at the bottom of this post for those who want to dig into more detail. PS: Digit is also up nicely QTD. This is not included in my summary. Fairfax May 21 2025.xlsx

-

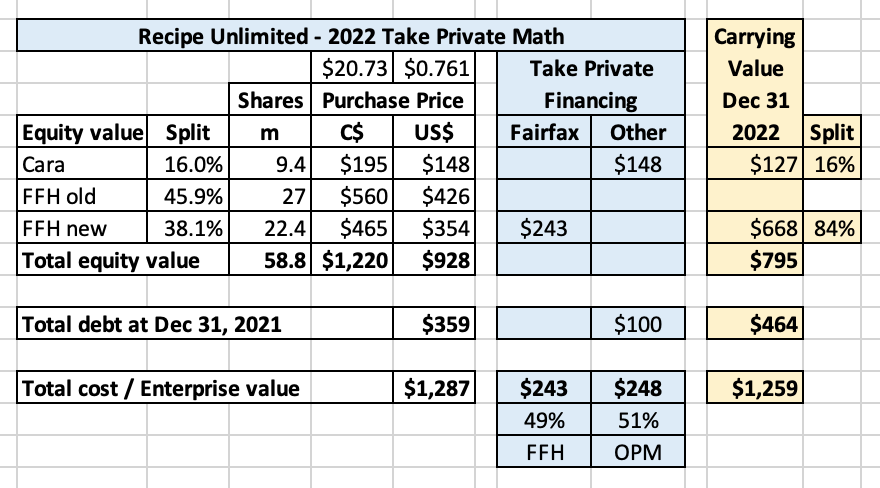

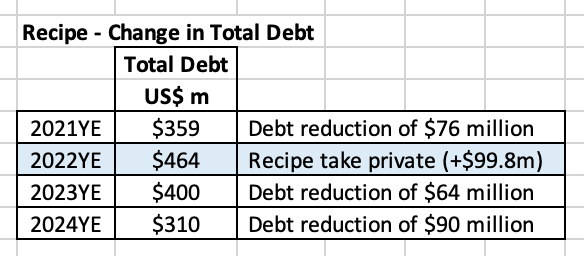

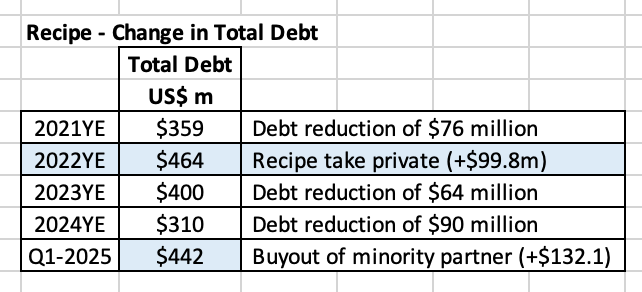

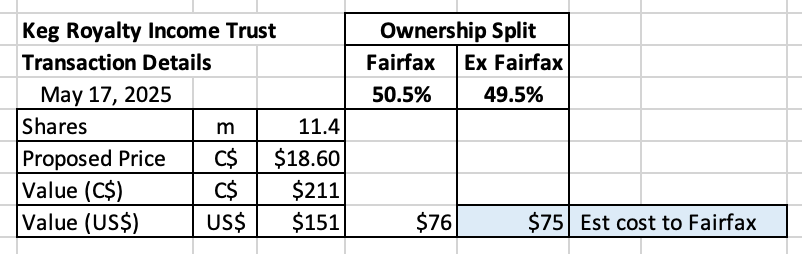

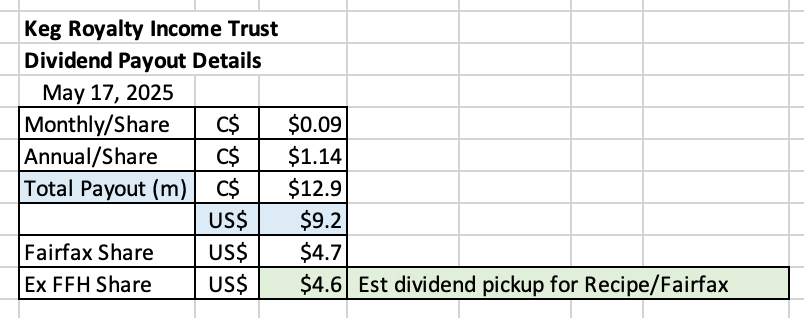

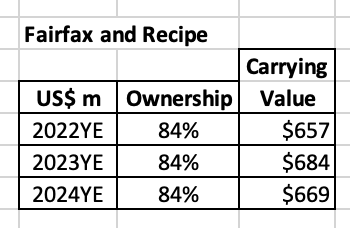

Recipe - Eating more of its own cooking Introduction Fairfax has been executing/undergoing a remarkable transformation over the past 7 or 8 years. The fundamentals of its two core businesses - insurance and investment management - have been steadily improving. As a result, beginning in 2021, operating earnings at the company began to spike higher. Investors are liking what they are seeing - Fairfax’s P/BV multiple has been expanding. Spiking earnings, expanding multiple and much lower share count is rocket fuel for a stock - Fairfax’s share price (US$) is up 382% since Dec 31, 2020. There is still much to learn about how the many improvements that Fairfax has been making to its business over the past 7 or 8 years will impact fundamentals/financial results in the coming years. Doing deep dives into different parts of Fairfax’s business helps us improve our understanding of the company. In turn, this helps us: Properly value the business/company. Ensure we have the correct position size with our investment. My guess is Fairfax’s transformation is still in its early innings. ————- Recipe Unlimited Today we will do a deep dive on one of Fairfax’s larger equity holdings, Recipe Unlimited. In 1H 2025, Fairfax made two investments that increase its ownership in Recipe (and all of its restaurant banners) to 100%. So this is a good time to do an updated post on Recipe - to see what we can learn about both Recipe and Fairfax. This post will cover the following topics: A short review of Recipe Unlimited In late 2022, Fairfax takes Recipe private. LBO M&A model used by private equity. In Q1 2025, Fairfax takes out its minority partner in Recipe - Cara Holdings In May 2025, Fairfax proposes to takeout The Keg Royalties Income Fund (‘KRIF’) What does Fairfax do next with its investment in Recipe? What did we learn about Fairfax - putting it all together Let’s get started by doing a quick review of Recipe. ————— 1.) A short review of Recipe Unlimited Who is Recipe Unlimited? From Recipe’s corporate website: https://www.recipeunlimited.com/en/our-brands.html “Recipe Unlimited Corporation is Canada’s leading full service restaurant company. We are a nationally recognized franchisor of choice with 1,200+ restaurants located in more than 300 communities across Canada, including many international locations. Home to such iconic brands as Swiss Chalet, Harvey’s, St.Hubert, The Keg, Montana’s, Kelseys, Bier Markt, East Side Mario’s, Landing Group, New York Fries, The Pickle Barrel & Catering, State and Main, Elephant and Castle, Original Joe’s, The Burgers Priest, Fresh, Blanco Cantina and Añejo.” What is Recipe’s business model? About 80% of Recipe’s 1,200 restaurants are franchised and 20% are corporate owned (2022 stat). The franchise business model has many advantages for the parent company (Recipe): Capital light - The capital needed to run the restaurant comes from/is obtained by the franchisee. An important source of leverage. Operationally light - The day to day operations of the restaurant are managed by the franchisee. They have the local know-how. Steady income streams - An up front fee is charged to new franchisees. And an ongoing royalty fee (percent of total sales) is collected from all franchisees. With Recipe, Fairfax is not really in the restaurant business (which is a very tough business). It is really in the franchise business (attracting, supporting and retaining a large group of wealthy entrepreneurs/business partners as franchisees). This is an important distinction. Stable earnings What this means is Recipe has a business that generates solid and (relatively) stable earnings. In 2024, the company generated about $82 million (C$114 million) in free cash flow. ———— In 1997, Warren Buffett bought Dairy Queen. My guess is what attracted him to the business were the financial characteristics of the franchise model that provides a steady source of excess capital that Berkshire Hathaway can then redeploy into other opportunities/businesses. https://www.berkshirehathaway.com/news/oct2197.html ———— 2.) In late 2022, Recipe is taken private On September 1, 2022, Recipe (then a public company) agreed to be taken private by Fairfax. Fairfax paid $354 million (C$465 million) to take out the public shareholders. Fairfax increased their stake in Recipe from 46% to 84%. Cara Holdings (founding Phelan family) continued to hold a 16% equity stake in Recipe. There were two very good reasons for Fairfax to take Recipe private: Financial - Fairfax was able to take Recipe private at a very attractive (low) price. Operational - In 2021, Recipe got focussed on integrating/rationalizing/optimizing the many large restaurant banner mergers/acquisitions completed from 2013 to 2018 (CARA Operations, Prime Restaurants, New York Fries, St-Hubert, Original Joe’s, The Keg). This was going to be a multi-year process. Fairfax decided this could best be done as a private company. There are a couple of other important benefits to being a private company: CEO is able to focus 100% on operating the business - responsibilities of being a publicly traded company are eliminated. Management is able to run the business with a long term focus - not possible as a publicly traded company (where hitting the expected quarterly earnings number is the primary focus). Prem’s comments about the Recipe purchase from Fairfax’s 2022AR: “We decided to take Recipe private, and on August 9, 2022 we offered a 53% premium to the pre-announcement stock price. 99% of the shareholders tendered to the bid. We felt that as Recipe had undergone many acquisitions since it went public in April 2015, it was best to rationalize its operations in a private format. The Phelan family decided to stay with us for 16% and we have the remaining 84%. Frank Hennessey continues as CEO with Ken Grondin as CFO.” Fairfax was opportunistic - They bought low Fairfax was very opportunistic with the timing of its purchase of Recipe. From 2018 to 2019 (before Covid), Recipe’s share price traded in a range from C$25 to C$28/share. Covid hit the full-service restaurant business in Canada hard (lock downs). In 1H 2020, Recipe’s shares traded below C$10/share. In September 2022, when Fairfax announced its take-private offer, Recipe’s shares were trading below $C14.00/share. Fairfax’s takeout price was C$20.70/share, which was well below where the stock had traded in 2018/2019 (pre-Covid). In September 2022, Canada’s full-service restaurant industry was just emerging from Covid - earnings had not yet rebounded to pre-Covid levels. Fairfax was able to take Recipe private at a very attractive price. It did not have to pay a premium, which normally happens when a public company is taken private. Recipe was also a high certainty acquisition for Fairfax. They understood the company very well - its past, present and future potential. This made the Recipe take-out a very low risk investment for Fairfax. In 2021, Recipe was deleveraging its balance sheet Setting the table Recipe’s dividend was suspended in 2020 shortly after Covid hit. Recipe did not pay a dividend in 2021 (the Canadian government did not allow companies who had received Covid assistance to pay a dividend) - its free cash flow was used to reduce debt, which came down by $76 million (C$95 million). Prem’s comments about Recipe from Fairfax’s 2021AR: “Recipe survived another tough year in 2021 as lockdowns closed its restaurants for long periods during the year. In spite of these lockdowns, Recipe pivoted to e-commerce sales, curbside pick-up and home delivery to generate system sales of Cdn$2.7 billion, up 12% from 2020 and down 22% from 2019. E-commerce sales now account for Cdn$675 million or almost 25% of Recipe’s system sales, up from Cdn$340 million or 10% of system sales in 2019. Recipe’s franchise revenue was Cdn$150 million in 2021, up 18% from 2020, and EBITDA for the year was Cdn$144 million, down 33% from pre-pandemic levels of Cdn$216 million. Recipe was able to reduce its debt outstanding by Cdn$95 million in 2021, capping an outstanding performance by Frank Hennessey and his team.” How was the take-private of Recipe financed? In 2022, Fairfax paid a total of $354 million to take Recipe private. This was comprised of two parts: Cash consideration from Fairfax of $242.5 million. Increase in borrowings at Recipe of $99.8 million. (Paying down debt in 2021 certainly was well timed.) In taking Recipe private, Fairfax tapped a second source of ‘other people’s money’: Cara Operations continued on as a 16% minority equity partner. Fairfax only had to pay $242.5 million in cash to take Recipe private and increase its ownership from 46% to 84%. Fairfax also used ‘other people’s money’ of $248 million to help pay for the take private (debt from Recipe and equity from Cara Operations). Using leverage (other people’s money) was a way for Fairfax to keep its capital contribution low. This is a proven/smart way to generate a higher return on its equity investment in Recipe (ROE). What does this transaction look like? It kind of looks like the leveraged buyout merger and acquisition model that is used by private equity. Not exactly… but it does share many of the same characteristics. This might be important. Let’s explore this more. Details on the Recipe purchase from Fairfax’s 2022AR: “On October 28, 2022 the company acquired all of the multiple voting shares (“MVS”) and subordinate voting shares in the capital of Recipe, other than those shares owned by the company and 9,398,729 MVS owned by Cara Holdings Limited, at a cash purchase price of Cdn$20.73 per share or $342.3 (Cdn$465.9) in aggregate, comprised of cash consideration of $242.5 (Cdn$330.0) and an increase in borrowings by Recipe of $99.8 (Cdn$135.9).” 3.) Leveraged buyout (LBO) merger and acquisition (M&A) model The LBO M&A model used by private equity can be summarized as follows: Buy another company (using a lot of leverage). Improve its operations. Use the cash flow from the business to reduce leverage. Sell the company for a big profit 5 or so years later. A small up-front equity investment can deliver an exceptional rate of return. The mechanics of an LBO An LBO is a method used to buy another company by primarily using other people’s money (usually debt). The financial sponsor (the acquiring company) provides a small amount of equity capital (perhaps 1/3 of the total purchase price). Lenders provide the debt, which is used to pay the majority of the purchase price (perhaps 2/3 of the total purchase price). The financial assets of the acquired company are used as collateral to obtain the debt financing. The debt is non-recourse to the financial sponsor. The free cash flow of the acquired company is used to: Pay the interest costs. Pay down debt. Grow the business. Funding most of the purchase price with debt applies a significant amount of leverage to the deal for the financial sponsor. As the debt is paid down the value of the equity increases. Because a small amount of equity was used to make the initial purchase, over a 5-year period the return on equity for the financial sponsor can be quite large. Key: For this model to work the company being acquired has to generate solid and consistent free cash flow. The leverage (usually debt) needs to get paid down over time. Let’s apply what we learned to Fairfax’s take-private of Recipe to see what we can learn. 3.) Fairfax’s ‘LBO light’ M&A model If it If it looks like a duck, swims like a duck, and quacks like a duck, then it probably is a duck. Fairfax is not a private equity shop. It is a P/C insurance company. As a result, it is going to ‘tweak’ the LBO M&A model described above to fit its business model. Looking at the Recipe take-private deal, Fairfax made two important ‘tweaks’ to the traditional LBO M&A model: The amount of debt put on Recipe’s balance was reasonable - both the incremental amount ($99.8 million) and the total amount ($464 million). Fairfax also used equity to fund part of the total purchase price (this keeps the D/E ratio reasonable). They included a minority partner (Cara Operations) in the take-private deal. Fairfax knew Cara well (had been partnered with them since 2013) - they were a long term, trusted partner. Cara owned 16% of Recipe’s publicly traded shares and they agreed to roll their ownership stake over into the private company. Fairfax has a long history of using minority partners when making large acquisitions (insurance and non-insurance businesses). It looks to me like Fairfax has been using an ‘LBO light’ M&A model for years. I call it ‘light’ because they go easy on the total amount of leverage they use (which lowers the risk). And they sometimes use both debt and equity as sources of leverage (which lowers the risk even more). Fairfax has a stated return target of 15% when making equity investments. Using a modest amount of leverage helps Fairfax achieve this target. Cash flow is super important OK, it has been couple of years since Recipe was taken private at the end of 2022. As we discussed, under the LBO M&A model free cash flow is used to reduce leverage. What did Recipe do in 2023 and 2024? Recipe reduced total debt by $64 million in 2023 and another $90 million in 2024. These actions further support our ‘LBO light’ M&A model thesis for Fairfax. OK, with total debt at Recipe low, what does Fairfax do next? We got our answer in Q1 of 2025. ————— 4.) In Q1 2025, Fairfax takes out its minority partner in Recipe - Cara Holdings Transaction details In Q1 2025, Fairfax took out its minority partner in Recipe - Cara Holdings, who owned a 16% stake. It appears Fairfax paid US$157.6 million. (We didn’t get confirmation from Fairfax of the exact amount - but I think this number is directionally accurate). Cara Holdings is owned by the Phelan Family. The Phelan family’s roots in Recipe/Cara go back to 1850 when Thomas Patrick Phelan began selling apples and newspapers to passengers on the Niagara steamboats. Historical timeline for Recipe and its accumulation/roll-up of Canadian restaurant banners: https://www.recipeunlimited.com/en/about/timeline.html How was the purchase of Cara Operations stake in Recipe financed? Recipe took on more debt ($132.1 million) to fund the takeout of Cara Holdings. Total debt at Recipe continues to be very manageable. Over the next year, the free cash flow of Recipe will likely be used to pay down Recipe’s debt. From Fairfax’s Q1 2025 Interim Report: “During the first quarter of 2025 Recipe increased its borrowings by $132.1 (Cdn$190.0) to partially fund the repurchase and cancellation of its common shares not owned by Fairfax as described in note 12.” “Net borrowings on revolving credit facilities and short term loans - non-insurance companies of $160.7 and purchases of subsidiary shares from non-controlling interests of $157.6 in 2025, primarily reflected additional draws by Recipe on its revolving credit facility to repurchase and cancel its common shares not owned by Fairfax.” We come full circle Fairfax used minority partner Cara Operations as a short term source of cash/leverage when it to took Recipe private in 2022. At the time, Fairfax contributed cash of only $243 million, which boosted its ownership position from 46% to 84%. Contributing no new cash, Fairfax now owns 100% of Recipe and its free cash flow ($80 million in 2024). The return on Fairfax’s $243 million investment in Recipe over the past 2.5 years has been very good. With Fairfax now owning 100% of Recipe and total debt at a reasonable level, what does Fairfax do next? We got our answer on May 5, 2025. ———— 5.) In May 2025, Fairfax’s proposes to takeout The Keg Royalties Income Fund (‘KRIF’) Transaction details Recipe owns 100% of all of its large restaurant banners, except the Keg. From an ownership perspective, the Keg has two pieces: The corporate entity, Keg Restaurants Limited (KRL), which is 100% owned by Recipe. The subsidiary, KRIF, which is publicly traded. Fairfax owns 50.5% of KRIF. KRIF holds the trademarks and intellectual property used by the Keg. KRIF collects a royalty of 4% of sales (on corporate and franchised restaurants) from KRL. KRIF pays out its earnings in a monthly distribution to shareholders. KRIF corporate website: https://thekeg.com/en/keg-income-fund Fairfax is offering to pay C$18.60/share for KRIF. This values 100% of the company at US$151 million. It will cost Fairfax about $75 million to buy the 49.5% of KRIF it does not own. Details of Fairfax’s offer: https://thekeg.com/en/keg-income-fund/05052025 KRIF currently pays out a month distribution to shareholders of C$0.0946/share. The total payout for KRIF is US$9.2 million per year. Why do this transaction? There are a number of benefits to Recipe and Fairfax from doing this transaction. Structure/Operational benefits As we mentioned earlier in this post, one of the primary reasons Recipe was taken private in late 2022 was to better support the ‘rationalization’ of its operations (consolidate/integrate the many different restaurant banners that were merged/purchased from 2013 to 2018). The purchase of the KRIF will give Recipe 100% control of the Keg. This will allow Recipe to complete its rationalization efforts (as it will control 100% of its large restaurant banners - the KRIF layer can be eliminated (people, reporting and complexity). This purchase brings to a close the aggressive roll-up strategy that Recipe/Cara executed from 2013 to 2018. Strategic benefits - the future Having 100% control of the Keg will give Recipe greater flexibility - and allow it to manage the banner as it sees fit moving forward - unconstrained by the needs of KRIF. The Keg has the potential to be a growth driver for Recipe moving forward (international expansion). Having a more conventional capital structure should also assist the company in financing its growth initiatives at the Keg. Financial The price being paid ($151 million) to take KRIF private is reasonable. Fairfax owns 50.5% of KRIF, so the cash required to complete the take private is $75 million. This purchase will grow Recipe’s total earnings as 100% of KRIF earnings will now accrue to Recipe. How will the takeout of KRIF be financed? We do not know how Fairfax will finance the KRIF purchase when it closes later in 2025. There is a good chance it could be funded by Recipe (from increased borrowings). Summary The purchase of KRIF will give Recipe 100% ownership of the Keg. This provides meaningful operational and strategic benefits to Recipe. The financial benefits are solid. The purchase of KRIF also brings to a close the aggressive roll-up strategy that Recipe/Cara executed from 2013 to 2018 (with Recipe now owning 100% of its major restaurant banners.) ————— 6.) What does Fairfax do next with its investment in Recipe? The economic value of Fairfax’s investment in Recipe has been growing nicely over the past 2.5 years. The increase in economic value has not been captured by a corresponding increase in Fairfax’s (accounting) carrying value for Recipe. (The carrying value for Recipe is what is reflected in Fairfax’s book value.) The value creation at Recipe in recent years has been hidden. Fairfax will find a way to surface the hidden value in the future. Moving forward, Fairfax has three broad options with Recipe: Keep the business - Use it as a cash cow. Strategic sale - Sell to another player in the industry. IPO - Sell all or part of the company to the public. Of course, it is impossible to know what Fairfax ultimately will do. We do know that they will be opportunistic - they will sell investments when it makes sense. The bottom line, with their decisions and execution over the past 3 years, Fairfax has put themselves in a very good position - they have lots of very good options. Welcome to ‘new Fairfax’. ————— 7.) What did we learn about Fairfax - putting it all together With the takeout of KRIF, Recipe will own 100% of its restaurant banners. With the takeout of CARA Operations, Fairfax now owns 100% of Recipe. Both transactions greatly simplify Recipe’s structure. Recipe/Fairfax will also have greater flexibility to manage its total business and its many restaurant banners as it sees fit moving forward - unconstrained by the needs/wants of minority partners. These transaction have been financed using an ‘LBO light’ model - with the majority of the cash coming primarily from Recipe (debt, which is then paid off with its free cash flow). These transactions satisfy the dual objectives of capital allocation done well: Operationally, they make Recipe a much stronger / more resilient company. They provide a solid rate of return to Fairfax and its shareholders. ————— Fairfax has been very active with its investment in Recipe Unlimited over the past 3 years. What did we learn about Fairfax’s senior team and how they do capital allocation? Below are some thoughts: Strategic - Goal was to get 100% control of Recipe and 100% control of all its banners. Long term focus- Required execution of a multi-year strategy to achieve the goal. Patient - Did not get impatient and force things/timing. Let the opportunity play out naturally over time. Opportunistic - The takeout of Recipe’s minority shareholders in 2022 was done at a low price. The takeout of the Keg minority shareholders in 2025 was done at a fair price (this transaction has not closed yet as of May 2025). Creative - Used debt (Recipes balance sheet) and equity (Cara Operations) to fund much of the total purchase price. Free cash flow of Recipe was used to reduce leverage. Delivered a solid return to Fairfax and its shareholders. Fairfax has developed many different capabilities when it comes to capital allocation When it comes to how it allocates capital, Fairfax has developed a number of different capabilities over the past 7 or 8 years. ‘LBO light’ is just one example of a model that Fairfax has successfully utilized in recent years with many of its take-private purchases (Sleep Country and Peak Achievements being two of the most recent examples). As we learned with Recipe and what Fairfax has done with this investment since 2022, this ‘LBO light’ capability is not ‘theoretical.’ Fairfax has clearly demonstrated they know what they are doing. It is a proven capability. When it comes to capital allocation, having a full toolbox of proven capabilities allows Fairfax to be very patient and opportunistic. In turn, this should allow them to earn a higher rate of return on the business over time. And that is what we are starting to see. The bigger picture - an important source of liquidity Having 100% ownership of operating businesses like Recipe makes Fairfax a more resilient company from a financial perspective. Recipe provides a stable and growing source of free cash flow for Fairfax that is not correlated with the P/C insurance business. Recipe is a desirable asset. It could be sold (all or part) to raise cash. ========== Prem’s comments about Recipe from Fairfax’s 2024AR. “Recipe surpassed its record-breaking system sales in 2023 (adjusted for the 53rd week) with system sales of Cdn$3.6 billion in 2024.Revenue was up 0.5% driven by improvements in corporate restaurants and the consumer packaged goods business. The company delivered Cdn$114 million in free cash flow and reduced overall leverage to less than 2x. With a strong underlying business, Frank Hennessey, Ken Grondin and their team are focused on top line growth. Expansion is under way in the United States and Indian markets, complemented by organic growth in Canada from new restaurants. The company will also be launching new products in its already sizable consumer packaged goods business (where Recipe’s brands are sold in grocery stores). Recipe is carried on our balance sheet at 10x free cash flow.” Recipe’s 2024 free cash flow and valuation Free cash flow (2024) = C$114 million = US$82m Recipe share (84%) = US$69 million Fairfax’s carrying value for 84% stake in Recipe = $669 million (at Dec 31, 2024) = 9.7 x 2024 FCF

-

Ouch! I had to edit my post…

-

@nwoodman, great concise summary of the current set-up with Fairfax today. Of course, those who do not follow the company closely do not appreciate how much leverage (how many large coiled springs) Fairfax has ‘hidden’ under the hood. Of course investments like Eurobank, Poseidon, BIAL and Ki are not ‘hidden’ - but their likely impact on Fairfax’s future results are not well understood or priced into the stock today. This provides a large margin of safety, even at Fairfax’s current price. This probably explains why Fairfax remained aggressive with share buybacks in Q1 - they KNOW what Fairfax is worth. PS: For those people who anchor heavily to book value, Eurobank, Poseidon, BIAL and Ki are 4 examples of where Fairfax’s book value is understated. There are more (Sigma is a good example from Q1). The turnaround of the equity portfolio that started in 2018 is really starting to produce results. We are just starting to grasp the importance/impact of this development. Andy Barnard taking the reins of the insurance business in 2011 was a seminal moment for that business. It is only in the last couple of years that investors are beginning to grasping the quality of the insurance business. It was a long journey. It takes time for investors to connect the dots and update their views/narrative. My view is something similar happened at Hamblin Watsa around 2018. The investment management framework was adjusted/improved. 7 years later the benefits of the changes are now flowing through to reported results. But much of the benefits (economic value that has been created) have happened under the hood - and have not yet been captured in accounting results (EPS and book value). ‘Time is the friend of the wonderful business.’ Insurance and investment management business engines are both wonderful businesses at Fairfax. They are now compounding at a high rate of return (some of that compounding is not being captured in reported results). Time has become Fairfax’s friend. And the friend of its shareholders.

-

To make the decentralized model work you need to have entrepreneurs running each of the 60 profit centers. They then need to drill that mindset down through each of the profit centers. The question for Markel is were these people (the entrepreneurs) driven out of the organization over the past 5 years? Is Markel now staffed with people who prefer/skills align with a centralized structure? I have no idea. It will be interesting to see what happens moving forward. In my past life I worked for both types of companies: - Kraft Foods - highly centralized structure - Saputo Foods - highly decentralized structure What I learned is most people fit one or the other structure. Not both. It is not a simple matter of re-training. Especially the leadership roles.

-

@73 Reds , I think the set-up for Fairfax today resembles a much younger Berkshire Hathaway (1990's version) - in terms of the leverage (float) and the future return potential. Of course, how Fairfax does it will differ greatly from how Berkshire Hathaway did it. Today, Fairfax is ploughing new ground. To your point, back in 1990 the smart thing to do was to simply buy Berkshire Hathaway and sit back and let Buffett work his magic. It is deceptively simple. And incredibly difficult to actually do - that is why so many (like me) missed making the big money with Berkshire Hathaway. I find my understanding on many investing topics is still lacking - things like culture and moats. So I keep trying to learn a little more - sometimes this results in me updating an old post (like the one above). It is a constant process of continuous learning - and that is one of the things I really like about investing.

-