Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

@anshulp thanks for posting

-

@bluedevil, thanks for sharing… I’ll listen to the video in the next couple of days.

-

@Hoodlum, that is s great quote from The Once and Future C&F book from Marc Adee. Reading the book gave me a much greater appreciation of the incredible journey that Fairfax and its P/C insurance businesses have been on for the past 25 years. It largely helps confirm much of what I suspected was/is happening. Marc mentioned numerous times they were ‘planting acorns’ that have, over time, grown into oak trees. My guess is that was not just happening at C&F, but at most of Fairfax’s insurance businesses. It is amazing the turnaround that has happened since 2000 at the P/C insurance businesses. The book also provides many great examples of how P/C insurance companies can lose their way… and how long it can take to right the ship (sometimes decades). I also liked Marc’s style… he was very humble (you don’t know what you don’t know).

-

+1

-

Reported BV. That is the number most people focus on. The silver lining to having an understated BV is it makes it easier to deliver a high ROE.

-

Ok, what are some of the opportunities for Fairfax to deliver an ROE that is higher than 15%? @TB, I will start with the counter/quick thoughts on the items on your list: 1.) BV is materially understated. Excess of FV over CV is probably about $2.6 billion at June 30 = $120/share. It is increasing at about $600 million per year for the past 5 years. This value creation is not captured in past accounting results (like EPS, BV or ROE). It WILL get captured at some point (Fairfax is very opportunistic in surfacing value like this). When it gets surfaced, reported earnings will pop. And ROE will pop. 2.) Leadership transition: Fairfax has been transitioning to the next generation of leadership over the past 5 years. Fairfax’s bench is very strong (employee retention has been outstanding). The people they are transitioning to/giving more responsibility to are internal and look very capable. Peter Clarke is just one of many good examples. 3.) In a soft insurance market Fairfax will likely get an opportunity to grow their P/C insurance business (many insurance stocks will be on sale). They were able to grow in the last soft market when they were cash constrained (they are no longer cash constrained). 4.) Fairfax underperformed from 2010 to 2020. They look well positioned to now outperform from 2020 to 2030. 5.) Fairfax’s - measured by market cap - is a very small company. They are in the sweet spot (in terms of size) - big enough to have a large opportunity set but not too big (like BRK). 6.) Fairfax has been upgraded by the ratings agencies twice in the past 30 months (AM Best, S&P Global). The reason? The much improved financial position of Fairfax and the stability of future earnings. 7.) Fairfax has done a good job of navigating the political situation in its various markets. This will likely continue (look at their most recent hire in India). But there is much more. Fairfax is littered with examples of equities/holdings that are materially undervalued on its books (not just the excess of MV over CV that I mentioned earlier). Fairfax India’s MV is its stock price. Its stock price is way under its BV. Its BV is way under its intrinsic value. The poster child here is BIAL. How undervalued is BIAL? My guess is well over $1 billion. What is Ki going to be worth in another couple of years? What is Poseidon worth? What is Recipe and AGT Foods worth? For the past 5 years an enormous amount of value is being created in Fairfax’s collection of equity holdings. This is not being captured in accounting results. But it will be in the coming years (as I said, Fairfax is very good at surfacing value that is hidden on its balance sheet). There is also going to be enormous value creation with the equity holdings in the coming years. Fairfax has partnered with an exceptional group of founders/CEO’s/entrepreneurs. This is a new development - what we see the next 5 years could be special (in terms of value creation). Fairfax also has resource holdings with material upside potential: Orla gold: we could be in the early innings of a bull market in gold. Foran Mining: copper prices are expected to be materially higher in the coming years. And I haven’t even discussed what they are going to do with +$4 billion in earnings each of the next 5 years… how will they allocate it? What incremental return will it deliver in year 3 and 4 and 5? Fairfax’s capital allocation the past 5 years has been exceptional. The value creation has been massive. Do we expect them to suddenly get stupid? I could go on. Bottom line, Fairfax has many tailwinds that are not baked in to my 15% ROE estimate (on average) for the next 5 years. Please note, I am not expecting a smooth 15% per year.

-

@TB, in terms of ROE, I think 15% is a good baseline average to use for the next 5 years. That is as far as my crystal ball sees. I think you do a good job of highlighting some risks. But I think if you look at the risks it makes sense to also look at the opportunities (the things that could drive a higher ROE that 15% on average). My guess is the opportunities are greater than the risks. That is why I think my 15% ROE estimate is conservative. What are some of the opportunities? I am on dish detail tonight. More to come

-

@73 Reds, you make a great point. As much as Fairfax has grown its P/C insurance business over the past 10 years, underwriting profit only represents about 20% of its 5 different income streams. When the P/C insurance business shifts from hard market to soft market Fairfax will simply/easily shift capital from insurance to other better returning opportunities. Even when the P/C insurance market softens, Fairfax will be able to continue to deliver a strong ROE. It is uniquely positioned today in this regard in P/C insurance. Buffett was able to deliver outstanding ROE for BRK shareholders for decades. Regardless of the P/C insurance cycle (hard or soft market). Fairfax, because of the platform it has today and the external environment, is similarly positioned today. I don’t think Fairfax sill deliver an ROE has high as the one BRK delivered in the 1980’s and 1990’s. But I do think Fairfax will be able to deliver a very good ROE in the coming years. Although, as a outlined in my previous post in this thread, Fairfax will do it in a very different way than BRK did.

-

@Maverick47, my view is a number of factors have come together for Fairfax over the past 5 years that have resulted in a unique business model in P/C insurance. I don’t think it is the Berkshire Hathaway business model (conglomerate). Fairfax has built a unique platform. Their focus the past 10 years has been to aggressively grow their insurance business. Much more so that BRK ever has. As a result, Fairfax has been increasing the amount of leverage it has (to float) on a per share basis. At the same time, the quality of their insurance business has improved dramatically. I just finished reading Mark Adee’s book, Once and Future Crum and Forster, and it provided more insight into the many improvements. https://www.cfins.com/the-once-and-future-cf-landing/ At the same time, Fairfax has built out a wonderful investment management platform. It has spent decades building extensive capabilities. Venture capital (start-up) investor. Private equity investor (LBO light). International investor (India, Greece). Value investor. Sometimes they are planting acorns that are growing to oaks (to steal a metaphor from Mark Adee). Other times that are more tactical. They have a wonderful breadth of capabilities. At the same time, Fairfax has been building out its business/relationships with outstanding external capital allocators. This is having a big impact on deal flow - they are likely now getting many more juicy opportunities than they have the money for - a first class problem to have. Bottom line, Fairfax’s investment management business is much more diversified than Berkshire Hathaway has ever been. That also bodes well for longevity of its model - it is increasingly not reliant on any one person. The external environment has also changed in recent years. We have moved away from a zero interest rate world (with suppressed volatility). And we appear to moving into a higher inflation/interest rate regime (with higher volatility). The current external environment is ideally suited to Fairfax and their business model. When I put it all together, I think Fairfax is poised to perform exceptionally well over the next 5 years. I think a 15% ROE is a good baseline number to use (on average). I think this estimate has a margin of safety built into it.

-

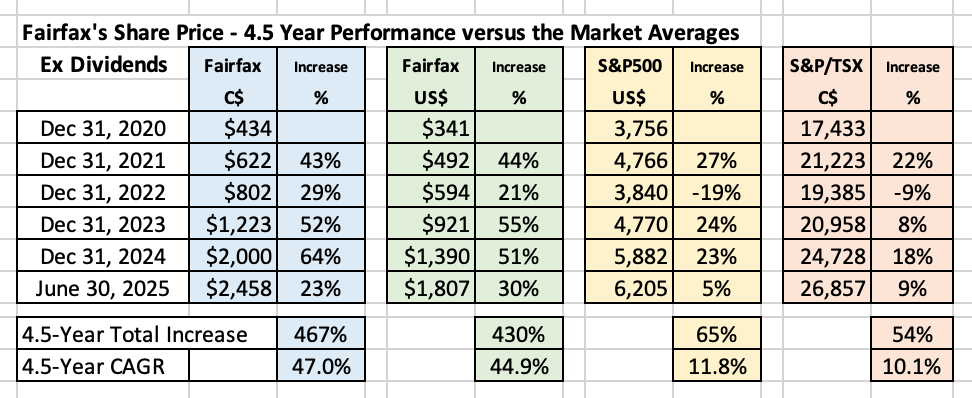

Is it time to sell Fairfax? What can Philip Fisher Teach us? Over the past 4.5 years, Fairfax’s stock has delivered a total return (US$) of 430% and a CAGR of 44.9%. Over this same time frame, it has also paid a total of $60 in dividends ($10/share in January of 2021, 2022 and 2023 and $15/share in 2024 and 2025). How does this compare to the overall market? Over the past 4.5 years, the S&P500 has delivered a total return of 65% and a CAGR of 11.8% (not including dividends). The performance of Fairfax’s share price the past 4.5 years has been excellent - both in absolute and in relative terms. Is it time to sell Fairfax? After such a massive increase in the share price, what is a rational investor to do? Why SELL of course. At least that is what I probably would have done in the past. Successful investors need to get two things right: when to buy AND when to sell. Over my career as an investor, I have been much better at the ‘when to buy’ decision than the ‘when to sell’ decision. I have a history of selling my big winners way too early. An example? After more than a 100% gain over a couple of years, I sold most of my concentrated position in Apple in 2016 - right around the time some guy named Warren Buffett started to buy shares. What was my mistake? My sell decision was focussed primarily on price. Back in 2014 and 2015, Apple was well managed. The fundamentals of the business were improving. Capital allocation at the company was very good. Its prospects were very good. In summary, Apple was a high quality company. Even after the big spike in the share price over 24 months the stock was still cheap when I sold it in 2016. The crazy part is I knew all of this - I follow my largest positions very closely. Mistakes will be made All investors make mistakes. The key is to not make a habit of it. Past mistakes, if learned from and corrected, can sew the seeds for the big winners in the future. Clearly, the ‘when to sell’ part of my investing framework needed to be improved. ————— If It’s Gone This High Already, How Can It Possibly Go Higher? I love this quote from Peter Lynch. “If I’d bothered to ask myself, “how can this stock possibly go higher,” I would never have bought Subaru after it already had gone up twentyfold. But I checked the fundamentals, realized that Subaru was still cheap, bought the stock, and made sevenfold after that. “The point is, there’s no arbitrary limit to how high a stock go, and if the story is still good, the earnings continue to improve, and the fundamentals haven’t changed, “can’t go much higher” is a terrible reason to snub a stock. Shame on all those experts who advise clients to sell automatically after they double their money. You’ll never get a tenbagger doing that. “Frankly, I’ve never been able to predict which stocks will go up tenfold, or which will go up fivefold. I try to stick with them as long as the story’s intact, hoping to be pleasantly surprised. The success of a company isn’t the surprise, but what the shares bring often is.” Peter Lynch - One Up on Wall Street – p. 266 & 267 Bottom line, using the stock price as your primary guide for ‘when to sell’ is a pretty poor approach. Especially when you find a great company, like I had done with Apple. ————— In age remainder of this post, let’s explore the ‘when to sell’ decision in a little more detail to see what we can learn. Let’s start with a simple question: When does it make sense to sell a stock? I have come up with 7 ‘typical’ reasons. Yes, our list is arbitrary. But it will provide a useful way to discuss the topic of ‘when to sell’ a stock. We are also going to get some help from Philip Fisher (and Chapter 6 of his book, Common Stocks and Uncommon Profits). ————— Who is Philip Fisher? Fisher is one of the GOAT’s. After Graham, he likely had the greatest influence on Buffett’s investing style. (Munger was also a big fan of Fisher.) In 1990, Buffett said his investing style was 85% Graham and 15% Fisher. Did Buffett’s shift even more towards Fisher after 1990? Probably. Fisher is worthy of study. ————— 7 reasons to sell a stock. The first 2 reasons are personal. And the next 5 reasons are financial. What are the personal reasons to sell a stock? 1.) Life need - you need some cash to cover a life expense. Perhaps you are buying a house and you need money for a down payment. Perhaps you are older and you want to help your kids out (with school or to ‘pay it forward’ early). It is best to plan ahead for big life events so the cash is available when you need it. Buffett says if you need the cash in the next 5 years it probably shouldn’t be invested in stocks. Personally, I shorten this time period to three years. It is important to have a financial plan. Part of that plan will include your near-term large life spending needs. You may need to sell some stocks to have an appropriate amount of cash on hand to ensure your life spending needs for the coming years are covered. 2.) When a single holding gets too big - you need to sleep well at night. For unsophisticated investors, concentration is generally a terrible idea. That is because they don’t have the time/inclination/skill that is needed to be successful with a concentrated stock portfolio. For these investors, diversification is a key strategy. As part of that framework, it is important to have a maximum position size for an individual stock (perhaps something like 5%). For sophisticated investors having a concentrated portfolio can work. But even then, it makes sense to have a maximum position size for an individual stock (for Buffett it was 40%). For both types of investors, when a stock goes over that position size it should be sold - to bring the weighting back down to the maximum position size. Selling a stock for personal reasons generally has little to do with the company, management, fundamentals, prospects or the valuation of the business. Given Fairfax’s spike higher over the last 5 years, this reason for selling is likely on the minds of many Fairfax shareholders. This is an important topic and needs/warrants its own (lengthy) post so we aren’t going to go in to any more detail on it here. Let’s now pivot and look at some of the financial reasons for selling a stock. What are the financial reasons to sell a stock? We have come up with 5 financial reasons to sell at stock. The first 3 are defensive in nature. And the last 2 are offensive in nature. ————- 3.) If you made a mistake with your purchase. Your understanding of a company will generally be at its lowest level when you make your first purchase of shares. Mistakes will happen when investing. That is a given. It is best to figure this out quickly. And then act. Sounds pretty simple… You made a mistake. You recognize you made a mistake. You quickly correct the mistake. You are golden. That is what any rational investor would do. So what’s the problem? Ego. (Often the enemy of being rational.) Ego stops you from recognizing that you made a mistake. Mistakes usually result in losses. Most investors have a hard time selling stocks that are in a loss position. Instead, they wait for the stock to return to their purchase price - they will sell it then (they tell themselves). The problem is mistakes don’t usually return to an investors purchase price. “None of us likes to admit to himself that he has been wrong. If we have made a mistake in buying a stock but can sell the stock at a small profit, we have somehow lost any sense of having been foolish. On the other hand, if we sell at a small loss we are quite unhappy about the whole matter. This reaction, while completely natural and normal, is probably one of the most dangerous in which we can indulge ourselves in the entire investment process.” Philip Fisher - Common Stocks and Uncommon Profits Holding on to mistakes then results in a second bigger problem. The funds can’t be redeployed into a better opportunity. “More money has probably been lost by investors holding a stock they really did not want until they could “at least come out even” than from any other single reason. If to these actual losses are added the profits that might have been made through the proper reinvestment of these funds if such reinvestment had been made when the mistake was first realized, the cost of self-indulgence becomes truly tremendous.” Philip Fisher - Common Stocks and Uncommon Profits The bigger cost of holding on to mistakes is the opportunity cost. The financial cost can be massive - and only grows the longer the mistake is held. This is an example of compounding working in reverse. Good luck getting wealthy with a bunch of stocks like this in your portfolio. There are two direct financial costs to making a mistake with your original purchase: The decline in value of the mistake you continue to own. The opportunity cost: What you could have earned if you had shifted the funds to a better opportunity. Given enough time, the second ‘loss’ can be much bigger than the first. There is another cost of holding on to mistakes - that is the significant psychological cost to the investor. These positions suck the life out of an investor over time - these positions are like the dementors in the Harry Potter movies. Being a successful investor is exceptionally difficult. It is important to be in a good mental state as much as possible. This will allow you to think and act in a more rational way over time. It is rational to sell a stock when you become confident/convinced that you have made a mistake. And the sooner you act the better. ————- The next two reasons you might want to sell a stock apply to businesses you have owned for years. Sometimes things change. Management. Fundamentals. Prospects. Industry. And what was once a good investment is no longer the case. 4.) Management disappoints/frustrates Management is a critical part of the investing decision. That is because bad management can destroy shareholder value. Fisher provides two general types of causes that might result in management messing up badly. Perhaps the existing management team loses their way. Like Fairfax did from 2012 to 2018. “Sometimes management deteriorates because success has affected one or more key executives. Smugness, complacency, or inertia replace the former drive and ingenuity.” Philip Fisher - Common Stocks and Uncommon Profits Or the issue might happen after a leadership transition. Like perhaps what is happening with Markel today. “More often it occurs because a new set of top executives do not measure up to the standard of performance set by their predecessors. Either they no longer hold to the policies that have made the company outstandingly successful, or they do not have the ability to continue to carry out such policies.” Philip Fisher - Common Stocks and Uncommon Profits When management messes up badly, it is generally best to sit things out. You can get back in after management demonstrates they have corrected their ways. Like Fairfax eventually did. We will see with Markel. The next reason to sell is often tied at the hip with management. ————- 5.) When the economic characteristics/fundamentals of the business deteriorate in a meaningful way. Very few businesses last forever - even the very good ones. Sometimes the issues are internal - the company loses out to competitors. Sometimes the issues are external - an entire industry gets disrupted. And its economics deteriorate over the years. Like what happened to newspapers. The important thing is to monitor the situation and to stay open minded. When ‘the story’ takes a permanent turn for the worse then it makes sense to sell. We can combine 4.) and 5.) together to make the following point. A few exceptional companies will be very good investments over the medium term. Even fewer companies will remain very good investments over the long term. The next reason to sell is offensive in nature. ————— 6.) You find a much better opportunity. Here is how Fisher put it: “If the evidence is clear-cut and the investor feels quite sure of his ground, it will, even after paying capital gains taxes, probably pay him handsomely to switch into the situation with seemingly better prospects.” Philip Fisher - Common Stocks and Uncommon Profits This sounds easy. But this reason for selling a stock is full of potential pitfalls. And that is because of all the different assumptions that are involved in the decision (on both the sell and the buy sides) and the uncertainty it brings. What if the company you plan to sell is a better value than you think? What if the company you want to buy is not as good of a value as you think? A variation of Peter Lynch’s observation: Most importantly, you don’t want to cut your flowers and replace them by planting a bunch of weeds. Of course, investors don’t think they are doing this (when they swap an investment). But this is often what actually happens to investors and it is likely one of the big reasons their investment returns lag over time. Selling a stock that you already own to buy a brand new stock should only happen when you have a high degree of certainty on all aspects of the decision. ————— 7.) The stock is trading at a premium to its intrinsic value. This is the reason to sell a stock that was espoused by Ben Graham. Buy when a stock is cheap (margin of safety). Sell when a stock is no longer cheap. Rinse and repeat. Get rich. The biggest strength of this framework is it is very easy to understand for retail investors. And it is also easy to teach. It is important to remember: Graham’s goal was to come up with an investing framework that could easily be taught to the general public. He was not trying to come up with an investing framework that would optimize results for sophisticated investors. Here is the interesting thing. Fisher did not list this as a reason to sell. Was this a mistake by Fisher? A reason he missed? No. Fisher didn’t list this as a reason to sell because he was playing a completely different game than Graham was. ————— Let’s flip the script. Is there ever a situation when a stock should never be sold? According to Fisher, the answer is yes. Let’s explore this next. But we will move from the realm of the average retail investor to that of a sophisticated investor. ————— Philip Fisher There is a different way to play the investing game than the one that I outlined above. This method was first developed by Philip Fisher. And then picked up by none other than Warren Buffett/Charlie Munger. What were some of important building blocks of Fisher’s investing framework? Only own high quality companies - determined primarily by qualitative factors (like management). Not determined primarily by quantitative factors. In many ways, Fisher’s approach is the opposite of Graham’s approach. Concentrate in the best ideas. Hold positions forever. Fisher is unique in his sell strategy. That is what we want to focus on here. Buy and hold forever “If the job has been correctly done when a common stock is purchased, the time to sell it is—almost never.” Philip Fisher - Common Stocks and Uncommon Profits This is, of course, one of the really important things Warren Buffett learned from Fisher. When you own an outstanding company you should never sell it. Even when it appears it might be overvalued. Volatility and Mr Market Fisher agreed with Graham that Mr Market was a manic depressive that should be exploited. But only to buy low. When an investor sells a position when it is ‘no longer cheap’ they are now - perversely - allowing themselves to be exploited by Mr Market. They are getting tricked into selling a great company (who is likely to grow into an even bigger long term winner). Investors stop looking at their investment as a business - and they use price as their primary valuation tool. John Train published ‘The Money Masters’ in 1980. He profiled 9 investors, including Philip Fisher. Below is how he summarized Philip Fisher’s thinking on ‘when to sell’: “…if you have chosen the company properly in the first place, with a reasonable prospect that in ten years, say, the stock will have tripled or quadrupled, is it so important that it’s 35 percent overpriced today? And there’s always the possibility that the stock’s price reflects good news you don’t know about yet. “Silliest of all, says Fisher, is selling out just because a stock has gone up a lot. The truly great company—the only kind he is interested in buying—will grow on and on, and its stock likewise. That it has advanced substantially since you bought it only means that everything is going just as it should.” John Train (on Philip Fisher) - The Money Masters ————— Warren Buffett (at the prodding of Charlie Munger) Embraces Fisher As you can see from the above quote, Philip Fisher was playing a very different game than most other investors. Including most value investors. Buffett’s genius was not going ‘all in’ on Fisher’s methodology - but in using it for part of his investment portfolio. When Buffett found an exceptional company - and he knew it - he held it for the long term. Decades. He might add to it on weakness. But he never sold it when it ran up in price. He didn’t sell it when it was ‘no longer cheap.’ He didn’t even sell it when it was obviously overvalued. And Buffett has said that 12 decisions over 60 years is what separates his results from those of average investors (or one decision every 5 years). But what allowed these 12 decisions to become outstanding investments was what he learned from Fisher - it was his holding period of decades. This approach is impossible for most investors to pull off. And that is because they are playing a completely different game. Fisher was content to get rich slow. Investors (throughout history) are focussed on getting rich as quickly as possible. As a result, Fisher’s approach is impossible for most investors to execute. ————— What is my key takeaway from Philip Fisher? I have no desire to try and become a 100% Philip Fisher type of investor. I don’t have the time, the desire or the skill to invest that way. But like Buffett, i think I can become a 15% Philip Fisher type of investor. And that is because every 5 years or so, I have usually been able find one outstanding investment. Something I understand exceptionally well. Where my view of the business is different from ‘consensus’. Moving forward, when I find an outstanding business, I am going to try and get better at my sell discipline - and not be tempted to sell my position. When it gets fairly valued. And also when it appears that it might be overvalued. Does this post have anything to do with Fairfax? Yes. I think Fairfax might have blossomed over the past 5 years into one of those outstanding investments that Philip Fisher (and Warren Buffett) were always on the lookout for. ————— One final word on the topic of selling from Peter Lynch My biggest mistake was that I always sold stocks way too early. In fact, I got a call from Warren Buffett in 1989. My daughter picks up the phone and says, "It's Mr. Buffett on the line." And I pick up the phone and I hear, "This is Warren Buffett from Omaha, Nebraska." You know, he talks so fast. "And I love your book, One Up On Wall Street, and I want to use a line from it in my year-end report. I have to have it. Can I please use it? I said, "Sure. What's the line?" He says, "Selling your winners and holding your losers is like cutting the flowers and watering the weeds.” That one line he picked up in my whole book has been my greatest mistake. Peter Lynch - Forbes India, Collectors Edition - November 2017 Let’s go back to what Lynch said at the beginning of this post. “I try to stick with them as long as the story’s intact.” Doesn’t this sounds similar to Fisher’s approach when it came to selling?

-

@awagner85, sorry, I don’t have an answer for you. For the number I use in my spreadsheet I took the number Fairfax published in the 2024AR and subtracted 80 million. With Eurobank now buying back shares (and Fairfax selling on a pro-rated basis) it is going to get even more difficult to have an exact number. But not having an exact number doesn’t bother me. I know I am going to be off with lots of my share count numbers for different holdings. Over time, we will get updates - when we do, I do my best to update my numbers then. With my spreadsheet, my goal is to be roughly right - that is good enough for me.

-

@Crip1, I loved your post. I am thinking along the same line as you. I have been reading up on Philip Fisher. in particular his selling discipline. His view was if you find an exceptional business you would be an idiot to sell it (at pretty much any price). I am working on a post on this topic (it is probably about a week away from being done). Buffett says 12 investments over 60 years is what separated him from being an average investor. When he found an exceptional business he didn’t sell it - at any price. Buffett said way back that he was 85% Graham and 15% Fisher. I think the ‘buy exceptional businesses and when you find one (that is the really hard part) you never sell them (as long as they continue to be exceptional)’ is what Buffett learned from Fisher. Buffett and Fisher play a different game than most other investors - find exceptional businesses and then ride them for as long as possible (ignoring the price volatility - in both directions). What I have been trying to figure out for the past 18 months: Is Fairfax an exceptional business? I think they might be. The answer to that question informs my sell decision on the stock. Below is a quote from John Train’s book The Money Masters, where he profiles Philip Fisher. Ignore the highlighted and underlined parts (they are not mine).

-

The median earnings estimate for Fairfax for Q2 is about $40/share. I am going to stick my neck out and take the over (yes, that was my attempt at humour). Q2 could be a very good quarter for Fairfax. There are lots of tailwinds for reported earnings. And even more good news. 1.) The equity portfolio is up about $2.0 billion or $91/share in Q2. The market to market piece is up about $36/share (pre-tax). 2.) Digit is up significantly in Q2. Part of Fairfax’s position is mark to market. We should see a nice sized unrealized gain here. 3.) Interest rates are lower at June 30 than March 31. This means Fairfax will see unrealized gains in its bond portfolio. This gain will boost reported unrealized gains even more (so it will likely surprise people - in a good way). Yes, there will be an offset with IFRS 17. But there will be a net benefit to Fairfax. 4.) Currency will be another tailwind. US$ strength has been a headwind to Fairfax’s reported results for the past couple of years (net income and the OCI impact on book value). US$ weakness is a tailwind to Fairfax’s reported results (net income and OCI impact on book value). One could argue that US$ strength is another example of how Fairfax’s book value today is understated. 5.) Underwriting results should be solid. It will be interesting to see where reserve releases come in - if they are similar to Q1 we could see a beat here too. The excess of FV over CV for associate and consolidated holdings just keeps blowing out more and more each quarter. My guess is Q2 will come in at around $2.5 billion. This is up from $1.4 billion at March 31, 2025, which is an increase of $900 million in the quarter ($42/share pre-tax). This will not be captured in Fairfax’s Q2 accounting results but it is economic value that is being created. Bottom line, Fairfax is poised to report a nice beat when it reports Q2 earnings. But its increase in economic value in Q2 will be much better than the reported results. Book value is becoming a less useful as a tool to value Fairfax. Investors who worship primarily at the P/BV altar need to think about this…

-

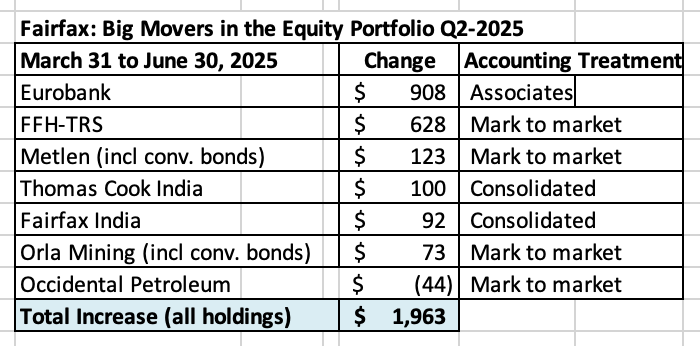

Estimate of change in MV of Fairfax’s equity portfolio in Q2, 2025 In Q2-2025, Fairfax’s equity portfolio (the holdings that I track) increased in market value by about $2.0 billion (pre-tax), or 8.5%. In Q1-2025, the increase in market value was about $785 million (pre-tax), or 3.5%. The market value of Fairfax’s equity holdings has increased substantially over the first 6 months of 2025. The equity portfolio had a total value of about $25.1 billion at June 30, 2025. Included in our estimates are details from Fairfax’s Q1-2025 interim earnings report and 13F. Notes: The FFH-TRS position is included in the mark to market bucket and at its notional value (this position has a market value of $3.2 billion). Convertible bonds, warrants and debentures are also included in the mark to market bucket. Digit: My tracker does not include Digit, Fairfax’s publicly traded P/C insurance company in India. Part of Fairfax’s ownership position in Digit is market to market. Digit’s shares were up quite a bit in Q2. This should result in a nice sized unrealized gain for Fairfax in Q2. Currency: US$ weakness is another tailwind for Fairfax. Where the benefit shows up in reported results is a little complicated (net income or OCI). The ‘tracker portfolio’ is not an exact match to Fairfax’s actual holdings. It is useful only as a tool to understand the rough change in value of Fairfax’s equity portfolio (and not the precise change). Split of holdings by accounting treatment About 49% of Fairfax’s equity holdings are mark to market - and will fluctuate each quarter with changes in equity markets. The other 51% are Associates and Consolidated holdings. Split of total gains by accounting treatment The total change is an increase of about $2.0 billion = $91/share (pre-tax) The mark to market change is an increase of about $784 million = $36.35/share. What were the big movers in the equity portfolio in Q2, 2025? The usual suspects – Eurobank and FFH-TRS - continue to perform very well (yes, this is an understatement). Lots of other holdings had strong quarters: Metlen, Thomas Cook India, Fairfax India and Orla. The biggest laggard was Occidental. Excess of fair value over carrying value For associate and consolidated holdings, the excess of fair value to carrying value is about $2.7 billion or $126/share (pre-tax). The 'excess of FV to CV’ has been materially increasing in recent years. This is economic value that has been created by Fairfax that is not captured in accounting value (earnings or book value) – it is one good example of how book value is understated at Fairfax. (Note, the carrying value we use in our tracker for associate and consolidated holdings is from March 31, 2025 so our number will likely be a little high). Excess of FV over CV = $2.7 billion = $126/share (pre-tax) Associates = $1.9 billion Consolidated = $0.8 billion ---------- This spreadsheet contains errors. It also contains some information that is dated (like the carrying value for associate and consolidated holdings). Please keep this in mind. The spreadsheet is updated as new information becomes available. Fairfax June 30 2025.xlsx

-

The Greek Freak (Eurobank) is making a strong push to be MVP of Fairfax's equity holdings in 2025. The market value of Eurobank is up $908m in Q2 (currency is a tailwind). Since inception, the total return from this investment is now about $3.34b. It is nuts what this investment has delivered for Fairfax over the past 5 years. And at Euro 2.916 the stock still look like good value (i.e. it does not look overpriced). Excess of FV over MV is about $1.6b (my estimate for June 30, 2025), or about $74/share pre-tax. This is economic value that is being created at Fairfax that is not being captured in accounting value (EPS and book value).

-

The glory years for the packaged goods industry (like Kraft) was likely the decades before 2000. Buffett purchased General Foods in late 1970’s/early 1980’s. Brilliant purchase. He nailed it. General Foods was taken out by Philip Morris in 1985. Philip Morris then purchased Kraft in 1988 and merged the two companies in 1989. In 2007, Philip Morris spun off Kraft General Foods. Brilliant move by PM (they KNEW the moat/fundamentals of the business were deteriorating). Buffett bought Kraft in 2007 (after it was spun off from PM) and he owned more than 8% of the company by early 2008. The problem is the packaged foods business in 2008 was not the same as the business in the early 1980’s and Buffett seems to have completely missed the important changes that were happening under the hood. The first big change was the slow shift in power from the big manufacturers to the big retailers (and their store brands). Costco and Kirkland Signature is the poster child of this. In Canada the best example was Loblaws and their President's Choice brand. More recently, direct to consumer has appeared to shift power away from both the big manufacturers and big retailers to mid size and smaller manufacturers (the Amazon Prime phenomenon). Kraft Heinz also had its own issues. Terrible management. As an example, when Heinz bought Kraft in 2015, in Canada they gassed the whole senior management team at Kraft (i.e. they didn’t keep the best people). This juiced profits for a short period of time - driven by cost savings. And then the business got torched. This is a great example of the problems that can happen when you manage a business focussed on maximizing cash generation over the very short term. Buffett first invested in Heinz in 2013. Heinz then purchased Kraft in 2015. Since Kraft Heinz started trading in 2015 it had been an unmitigated disaster for retail investors. The IPO price was $84/share. 10 years later the shares are trading at $25.61. The opportunity cost has been enormous. I wonder how many retail investors bought the Kraft Heinz IPO because of Buffett's significant ownership position. Back in 2015 Buffett got three things wrong with this investment: 1.) Management - terrible 2.) The moat/economics of the business - it was rapidly deteriorating 3.) When the above two became obvious Buffett did nothing = massive opportunity cost. What is the learning: all great investors make mistakes. ---------- Here is summary of Buffett's investment in Kraft Heinz https://thefinancecorner.substack.com/p/deep-dive-into-kraft-heinz-khc

-

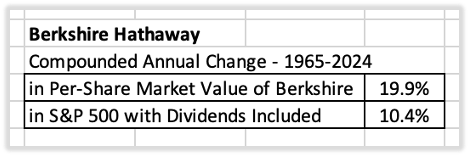

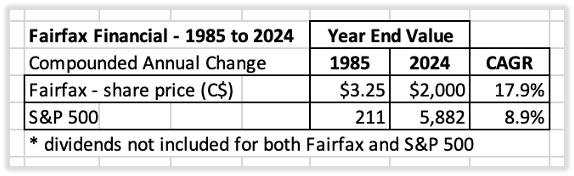

How to make the big money? Patience. To state the obvious, outperforming the market averages is very difficult. Especially over a longer timeframe like 10 years. So why manage your own investments? Investors usually do it for the opportunity to make the big money - to materially outperform the market averages. How can an investor do that? That is what we are going to explore in this post. The post has been broken into the following parts: Learning from the master: how did Warren Buffett do it? Time, compounding and exponential growth. What do investors actually do? How to make the big money. Berkshire Hathaway shareholders – the GOAT of retail investors. Fairfax Financial – looks very well positioned. ————— “In 58 years of Berkshire management, most of my capital-allocation decisions have been no better than so-so… Our satisfactory results have been the product of about a dozen truly good decisions – that would be about one every five years. “The lesson for investors: The weeds wither away in significance as the flowers bloom. Over time, it takes just a few winners to work wonders. And, yes, it helps to start early and live into your 90s as well.” Warren Buffett - Berkshire Hathaway 2022AR Part 1: Learning from the master: How did Buffett do it? Warren Buffett has been able to significantly outperform the market averages since 1965. Over the past 59 years (to YE 2024), Berkshire Hathaway stock has delivered a CAGR of 19.9%, which is almost 2 times the CAGR of the S&P 500 of 10.4% (including dividends). Yes, Buffett has delivered the ‘big money’ for Berkshire Hathaway’s shareholders. But here is what is really interesting. Buffett readily admits most of his capital allocation decisions over this 59-year time period were ‘so-so.’ He goes on to explain that his significant outperformance was driven by a small number of ‘truly good decisions.’ Buffett puts the number at 12, or one about every 5 years. This looks like it could be important. Let’s explore this further. What is Warren Buffett’s greatest attribute? Yes, this is kind of a dumb thing to ask. Let’s do it anyway. What is it about Warren Buffett that has allowed him to consistently generate such outstanding results over the past 59 years? Intellect? Work ethic? Thirst for knowledge? Character? Self-awareness? Management skills? Obviously, all of the above attributes are important and will help an investor achieve success. But lots of investors have many of these attributes - and yet they still underperform the market averages over time (let alone outperform to the degree that Buffett did). Is there something else, not listed above, that perhaps explains Buffett’s significant outperformance? I think there is something else… I think Buffett’s greatest strength might be his patience. (And patience is joined at the hip with temperament.) Before you throw your phone/tablet in disgust, let me explain. We need to peel the layers back. Buffett’s holding period is not months. Or years. For his ‘truly good decisions,’ the investments that become needle movers for Berkshire Hathaway, his holding period can be measured in decades. And that is very different from almost any other investor out there. That is something Buffett does that pretty much no one else does. (Please name another successful investor who did it this way… I can’t think of another one.) After patience, I think Buffett’s next greatest strength might be how he sizes his positions, especially his best ideas. And not just at the time of purchase - but also over time. How to size a position is exceptionally difficult to do and is a topic that deserves its own post - so we will not explore it further here. There are a couple of lessons here: Really, really good investment opportunities are very rare. Over his lifetime, Buffett points to 12 that worked out for him - or one about every 5 years. But finding a great investment is not enough on its own. Great patience is also required. It can take a decade or more for some investments to fully bloom. Of the two skills - finding a great investment and having great patience with it - the second is the one that is incredibly rare today. ————— Part 2: Time, compounding and exponential growth What is the greatest advantage of an investor? It is time. Why time? Time is what allows compounding to work its magic. Compounding is simple to explain but wicked difficult for most people to actually understand. I like the description in the drawing below. It is ‘boring’ for years and then it gets very ‘exciting’. Given enough time, compounding inevitably results in exponential growth. Or at least that is what one would think. More on this later. The goal of all investors is to get their portfolio to the ‘exciting’ part of compounding curve (the hockey stick part) - because it is life changing when it happens. Compound Interest drawing by Carl Richards Buffett’s genius? It is understanding that patience and time are two sides of the same coin. Together, they allow an investor to fully maximize the benefits of compounding. This in turn, can lead to exponential growth. Patience: this is how the big money is made. Let’s take a quick trip into the archives One of my all-time favorite books on investing is Reminiscences of a Stock Operator by Edwin Lefebvre. It was first published all the way back in 1923 in The Saturday Evening Post (in serial form over two years). Of all the memorable quotes in this book the following might be my favorite: “And right here let me say one thing: After spending many years in Wall Street and after making and losing millions of dollars I want to tell you this: It never was my thinking that made the big money for me. It always was my sitting.Got that? My sitting tight! It is no trick at all to be right on the market. You always find lots of early bulls in bull markets and early bears in bear markets. I've known many men who were right at exactly the right time, and began buying or selling stocks when prices were at the very level which should show the greatest profit. And their experience invariably matched mine - that is, they made no real money out of it. Men who can both be right and sit tight are uncommon. I found it one of the hardest things to learn. But it is only after a stock operator has firmly grasped this that he can make big money…” Reminiscences of a Stock Operator What is the lesson to be learned? Finding a great investment is hard. Holding a great investment for years, perhaps decades - that is much more difficult. Should we be surprised that Buffett is in a league of his own? ————— Part 3: What do investors actually do? “Selling your winners and holding your losers is like cutting the flowers and watering the weeds.” Peter Lynch Warren Buffett liked this quote so much he contacted Peter Lynch and asked him if he could use it. What is the average holding period for retail investors? I think it is around 5.5 months. And falling over time. Retail investors are like Edward Scissorhands. The flowers in their garden don’t stand a chance. Actually, we probably need to update Peter Lynch’s quote. These days, retail investors are so active buying and selling stocks in their portfolio - it’s like they completely raze their garden at least one time every year or two. What’s the chance the flowers are getting cut? Probably close to 100%. Should we be surprised that most retail investors achieve such poor results over time? What about the professional/smart money? The performance of professional/smart money is measured by investors quarterly… so they can’t be patient with their holdings. Deliver sub-par results over a couple of quarters and retail investors start to pull the plug. The professional/smart money has to chase short-term performance if they want to stay in business (or get paid their bonus) - which usually means owning whatever are the most popular stocks at a given time (the list of which is always changing). The bottom line, ‘patience’ is not a word that is in the vocabulary of retail and professional investors or in their toolboxes. Patience is primarily the stomach part of investing. Not the brain part. This probably tells us something… Ben Carlson has a good article on the subject of holding period. Buy & Hold is Dead, Long Live Buy & Hold (Feb 2023) - https://awealthofcommonsense.com/2023/02/buy-hold-is-dead-long-live-buy-hold/ (As an aside, ‘The Compound’ has become one of my favorite podcasts to listen to. Josh, Michael, Ben and guests are great. They have a bunch of different formats depending on what you are interested in. https://podcasts.thecompoundnews.com) Taking profits Why do retail investors turn their portfolio over so much? Lots of reasons. To buy something they think is better. To get rid of a mistake. To try and time the market. Macro call. Hot tip. I could list another 10 ‘good’ reasons. Let’s be optimistic. We are told taking profits is a sensible thing to do. Yes? But remember, in this post, we are trying to learn how to make the big money. Here is another great quote from the book ‘Reminiscences of a Stock Operator’: “They say you never grow poor taking profits. No. you don’t. But neither do you grow rich taking a four-point profit in a bull market.” Reminiscences of a Stock Operator When investors sell their best ideas, they are cutting the flowers in their portfolio. And because the really good ideas (that actually work out) are exceptionally rare (Buffett found one about every 5 years), the proceeds are recycled back into inferior ideas - investors water their weeds. Of course, at the time investors don’t think they are doing this (they think they are doing the opposite). This is like throwing sand in the gears of the compounding machine we discussed earlier. And hurts investment results. Investors get stuck in the ‘boring’ stage (from the napkin drawing above). As a result, many investors never actually get to the ‘exciting’ stage in their lifetime - the hockey stick part of compounding that becomes life changing. What does the investment industry have to say on this topic? I find it is helpful to follow the money. Incentives matter. A lot. How does everyone in the industry get paid? Fees. And fees generally come from activity. Action. Churn. Chasing short term performance. Yes, the exact opposite of patience. ————— Part 4: How to make the big money Buffett’s very simple model: · Step 1: Identify a ‘truly good’ investment and size the position appropriately. · Step 2: Exercise great patience and let it grow undisturbed, sometimes for decades. Truly great investments (the needle movers) are exceedingly rare. When you discover one, you need to size it appropriately. And then you hang on to it. For a long, long time. Do we have any real-life examples of ‘patience’ actually working out for a retail investor? Yes. A company named Berkshire Hathaway. ————— Part 5: Berkshire Hathaway Shareholders – The GOAT of Retail Investors Investors have known for decades that Berkshire Hathaway was run by one of the best capital allocators of all time. All an investor had to do was buy shares and watch the Buffett flower bloom every year… bigger, brighter and more beautiful. Importantly, investors had years to watch (learn) and get their position sized right. How many investors followed Berkshire Hathaway over the decades? Lots. How many investors never bought shares? Lots. How many investors bought shares and then sold them after a small gain? Lots. How many investors bought shares and then held them for a decade or longer? Very few. But the few who did were able to build great wealth over time. These investors exercised great patience - and were richly rewarded. These investors had a ‘truly great idea’ - buy Berkshire Hathaway stock. But their real genius - what separated them (and their returns) from all other investors - was their patience. Like Buffett, they held the stock for the long-term. Why didn’t these investors sell out? That is a great question. I don’t know. Because I sold my Berkshire Hathaway stock each time I owned it - after what I thought was a nice gain. With hindsight, I was a dummy. I was happy making a small profit. And I completely missed the big move - when it was staring me right in the face. So, what does all of this have to do with Fairfax? Maybe nothing. Maybe everything. ————— Part 6: Fairfax Financial – Looks Very Well Positioned Similar to Berkshire Hathaway, Fairfax has an outstanding long-term track record. Fairfax was founded in 1985. Over the past 39 years the company has delivered a compound return of 17.9% (not including dividends). Over the same time-frame, the S&P500 has delivered a compound return of 8.9% (not including dividends). Fairfax has significantly outperformed the S&P 500 over the past 39 years. However, unlike Berkshire Hathaway, Fairfax had a pretty big stumble from about 2010-2017. The investing side of the business messed up (the insurance side of the business continued to perform well). Business results suffered. However, from about 2016 to 2020 the company got to work correcting its past mistakes. By 2021, the turnaround was largely complete. Operating income increased from an average of $1 billion per year from 2016-2020, to $1.8 billion in 2021, to $3.1 billion in 2022, to $4.4 billion in 2023 and $5.3 billion in 2024. Since around 2018, Fairfax’s capital allocation decisions have been very good - best-in-class among P/C insurers. I have written about this extensively in other posts so I am not going to rehash things here. Bottom line, the set-up at Fairfax today - with both insurance and investment businesses - has never looked better. Now I generally hate comparing Fairfax with Berkshire Hathaway because they are such different companies. But I am going to break my rule in this post. Here is what I am wondering… Does Fairfax today look like a much younger Berkshire Hathaway? Here are some of the similarities I see between Fairfax today and a Berkshire Hathaway from 30 years ago: Business model: Built squarely on the P/C insurance / float model (Berkshire Hathaway has more of a conglomerate business model today). Capital allocation: Master capital allocator (Fairfax has been hitting the ball out of the park in this regard since 2018 - that is a pretty good timeframe to use to evaluate the current management team). Significant, sustainable earnings: Fairfax earned $3.9 billion in 2024 (amount attributable to Fairfax shareholders). And this level of earnings looks sustainable moving forward. Size: Fairfax is still small in size - good capital allocation decisions move the needle in terms of financial results (earnings and book value growth). All of the above + the power of compounding = opportunity for exponential growth over the next decade. To quote Warren Buffett: ‘Time is the friend of the wonderful business.’ Valuation: Fairfax’s stock is trading today at a low valuation - both compared to P/C insurance peers and the overall stock market. The set up today for Fairfax looks - to me - an awful lot like a much younger Berkshire Hathaway. Fairfax is poised to become a compounding machine in the coming years. If that happens, Fairfax will become what Buffett calls a ‘truly good decision’ for investors.

-

@gfp, thanks for clarifying the amount of float leverage that BRK had in the mid 1990’s. That is very instructive/interesting. I agree with your assessment on Fairfax. One of the reasons, which is rarely discussed, is the high likelihood of Fairfax delivering material upside surprises (in the coming years). Over the past 5 years Fairfax has been consistently delivering upside surprises pretty much every year (of some kind). Wonderful businesses do this (i.e. BRK in the 1980’s and 1990’s). And we know that these types of businesses are exceedingly rare. That is why they should never be sold. Especially if you understand it well (that circle of competence thing). Even if they appear overvalued at times (and I wouldn’t call Fairfax overvalued today). ‘Is Fairfax a high quality company?’ The reason I keep asking this question is the answer informs the ‘When to sell?’ question. At least it does for me.

-

Great discussion. @nwoodman, I find your posts/PDF’s to be very valuable/useful. Please keep them coming

-

I saw the 2 Twitter posts below from Everyday Capitalist. With Fairfax crossing C$2,500 (US$1,807) today it resonated with me. "The bear case is easy. The bull case is hard. Always has been, always will be." This has been especially true for Fairfax and its improbable run over the past 5 years. And it continues to be true today. Investors beware. ---------- ----------

-

This is a really interesting and important topic. My guess is if Fairfax's BV is understated it should make it easier for the company to deliver higher than expected ROE in the coming years. Part of the challenge with Fairfax is they only have a few years of +15% ROE under their belt. Lots of investors likely expect reversion to the mean (at a minimum, for it to come back down to its historic average). If Fairfax continues to deliver a +15% ROE for 6 or 7 or 8 straight years (on average)... well, at some point my guess is it will be recognized/rewarded in the multiple and, therefore, in the price of the stock. I think some of this is what we have been seeing play out over the past year. The question is 'How high a quality company is Fairfax?' We will only know with certainly after the fact (we will only be able to connect the dots looking back). We won't know prospectively (before the fact). And, of course, that is what makes investing such an interesting exercise/discipline.

-

@gfp , this is wonderful, thought provoking post. It leads to the following questions: 1.) What is the 'true' book value of Fairfax? 2.) What is the appropriate multiple to apply to BV for Fairfax as the company exists today? If an investor gets the answer to one of these questions wrong they will probably value the company incorrectly. If they get both answers wrong... well their resulting valuation of the company will be quite off. My guess is using simple historical numbers (BV and multiple) to value Fairfax has led many investors astray over the past 5 years. And it is probably still happening today. Of course, we know BV for Fairfax is understated. But by how much? The multiple question is also very interesting. Clearly, Fairfax deserves a higher multiple than it has received in the recent past. But how much higher? My guess is: 1.) Economic BV at Fairfax today is quite a bit higher than most investors think. 2.) The multiple(to reported BV) to use to properly value Fairfax today is higher than most investors think. ————— Now the benefit of having an understated book value is it should lead to a higher ROE. So the relationship between BV, ROE, multiple and stock price should make sense over time.

-

@Marco Van Basten I appreciate the comment as it does put a smile on my face to hear that other posters have had success with their investment in Fairfax. Here are some thoughts... The run that Fairfax has had over the past 5 years has been epic. No one (including me) expected it. This includes Fairfax (they said so at the 2024 AGM). I got lucky in 2020. Fairfax stayed cheap through Q2 and Q3. Sanjeev and others were pounding the drum all through the summer of 2020. Because of their posting, I re-established a position in Fairfax in October and I 'backed up the truck' in November right after the vaccine news was announced (largely on the assumption Fairfax's equity portfolio would spike). So I owe a big debt of gratitude to those posting back in 2020. Over the past 5 years, the quality and volume of posts on Fairfax has been outstanding. I am a good aggregator. Much of the material that found its way into my posts over the years came from others on this board. I have said this before... but I feel like the front man of a very successful band. We all owe a big debt of gratitude everyone who has posted on Fairfax over the past 5 years. Including those who pushed back, especially in the early days. That push back resulted in deeper thinking and better analysis - which has paid big dividends over the years (as the Fairfax story continued to improve). I have not been a buy and hold investor, historically speaking. This is the first time I have held a concentrated position in one stock continuously for 5 years. Others on this board have been very good influences on me in this regard. @SafetyinNumbers and @bearprowler6 are two who come immediately to mind. The only reason I kept posting so much was because my position size stayed large. So, once again, thanks to other posters on this forum. Analysis is useless on its own. It needs to be combined with action to be useful. A person's investing framework and psychological makeup is what determines success when it comes to investing. If you have had success with your investment in Fairfax over the past 5 years, it is primarily because of the person you see in the mirror each morning. Not because of me or any other posters on this board. This is really important. Because the success you have with your investment in Fairfax from today looking forward... will also be primarily determined by that same person you see in the mirror each morning. Anyways, how things have played out with Fairfax over the last 5 years has been nuts. A lot of luck has been involved. And help and support from lots of other first class people. And, yes, some good decisions. The best part? In some important respects, I think Fairfax is just getting started (in terms of its current iteration as a company). And I can't wait to see how the next 5 years plays out. When it comes to understanding Fairfax, I think we still have much to learn.

-

I apologize for re-posting some articles multiple times. I am encountering a few issues: My longer posts generally can't be edit after they are posted. And they don't load the charts the first time they are posted. So I have to post the article and then edit it (adding charts) and then copy/repost it. And then delete the original post. Sometimes my quality control messes up. I normally ignore small errors. But if I see a bigger error and want to edit - my only option is to re-post the entire article. Because, as I said, I can't edit my longer posts. Bottom line, it is not a big deal (to me). I just thought some of you might be wondering what is going on when some posts appear and then disappear... and then re-appear.

-

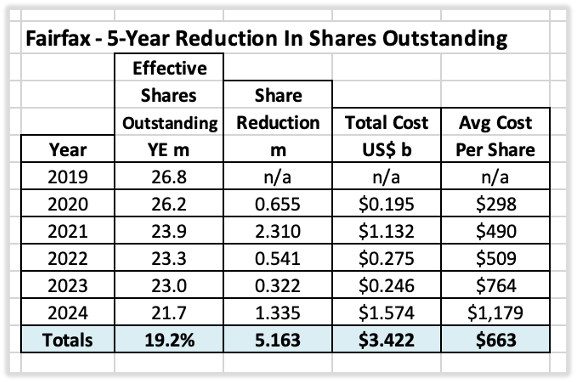

What kind of a value investor is Fairfax? Graham, Buffett, Templeton, Singleton or Lynch? To the question “What kind of an investor is Fairfax?” most people would answer “value investor.” That is the right answer but it doesn’t really tell us much. What kind of a value investor? To answer this question, we are going to look at what Fairfax has been doing for the past three years. What have they actually been buying? What can we learn? But first, let’s set the table. 1.) "The single most important thing (when investing in the stock market)… is to know what you own." Peter Lynch The problem with Peter Lynch is he says so many smart (and funny) things that his ‘most important thing’ gets lost in the shuffle. This is the ‘north star’ of everything else he writes. From this naturally flows another of Peter Lynch’s nuggets of gold. 2.) "The best stock to buy is the one you already own." Peter Lynch This makes intuitive sense. You have already done the research on the stocks you own. You know ‘the story’ and you like it (that’s why you own it). Assuming the fundamentals are still solid, then buying more should be a no brainer. Buffett takes this idea a little further with the following quote: 3.) "Diversification may preserve wealth, but concentration builds wealth." Warren Buffett The idea is to invest with conviction around your best ideas. Especially if the stock is on sale. This leads us to our next point. 4.)"‘The three most important words in investing are margin of safety." Warren Buffett Ben Graham introduced ‘margin of safety’ as the central concept of investing in Chapter 20 of his book, The Intelligent Investor. The idea is to only purchase stocks when they are trading at a big discount to their intrinsic value (buy something for $0.50 that is worth $1.00). This approach limits your downside if you are wrong and it provides significant upside if you are right. What do we get when we combine these four points? Often, your best investment is to simply buy more of something you already own - especially when it is on sale. One added twist: 5.) "If you search world-wide, you will find more bargains and better bargains than by studying only one nation." John Templeton Invest wherever in the world the best opportunities are. What does all of this have to do with Fairfax? Well, guess what Fairfax has been doing for the past 5 years? It has invested close to $8.1 billion in stuff it already owns. Yes, Fairfax has been investing in new ventures but the amount spent is much smaller. In short, Fairfax has been feasting at the buffet of businesses it already owns. High certainty/low risk investing Investing in what you already own is an example of high certainty investing. High certainty means low risk. This is a highly rational way to invest. Let’s review the actual investments that Fairfax has been making the past 5 years (2020 to 2024) that fit this theme to see what we can learn. ————— 1.) Buy Fairfax stock: NCIB/Dutch Auction and Fairfax Total Return Swaps Buybacks: NCIB/Dutch Auction Over the past 5 years, Fairfax has been very aggressive with share buybacks. Both with its NCIB and with its Dutch auction (taking out 2 million shares at $500/share in December 2021). From 2020 to 2024, Fairfax reduced effective shares outstanding from 26.8 million to 21.7 million, a reduction of 5.2 million or 19.2%. To do this, the total cost to Fairfax was $3.4 billion, or an average of $663/share. But the ‘buy Fairfax stock’ story is even better than this. We will discuss why next. Fairfax Total Return Swaps Fairfax also made an investment. In late 2020 and early 2021 they purchased total return swaps that gave them exposure to 1.96 million Fairfax shares at an average price of $373/share. This gave them exposure to another 7.3% of total shares outstanding at Fairfax. Fairfax reduced their exposure to 1.76 million shares in Q4, 2024. Let’s put the 2 together: Stock Buybacks + FFH TRS Can we come up with a rough estimate of the total value creation from these two activities over the past 5 years? We are not looking for a precision. We are looking to understand magnitude – about how big was the benefit to Fairfax? Let’s treat the stock buybacks (the reduction in effective shares outstanding) as an investment. Fairfax ‘paid’ $663/share for 5.16 million Fairfax shares. With Fairfax shares trading at $1,765/share, the ‘return’ to Fairfax from this investment has been $5.69 billion. The FFH-TRS position has delivered a return of $2.45 billion (before carrying costs). Together, these two investments have delivered a ‘gain’ of $8.14 billion to Fairfax and its shareholders over the past 5 years. To provide perspective of the size of this ‘gain’, common shareholders’ equity at Fairfax was $13.0 billion at December 31, 2019 (the start of this ‘investment’). Share buybacks should be done when shares are trading below intrinsic value. Fairfax bought back shares - and in significant quantities – when they were trading well below intrinsic value. Value investing at its best. And exceptional capital allocation. Who does this string of purchases remind you of? Not Lynch, Buffet or Graham. Who then? Henry Singleton. Who is this guy? “I mentioned to you last year that we are focused on buying back our shares over the next ten years as and when we get the opportunity to do so at attractive prices. Henry Singleton from Teledyne was our hero as he reduced shares outstanding from approximately 88 million to 12 million over about 15 years.” Prem Watsa – Fairfax 2018AR At the time, many people laughed at Prem for making this comment. I don’t think these same people are laughing at Prem today. ————— 2.) Increase Ownership of Insurance Businesses - Buy Out Partners = $2.26 billion Insurance is Fairfax’s most important economic engine. Growth in the insurance business over time will support sustainable profit growth at the company. And higher profits lead to higher intrinsic value (and a higher share price). All other P/C insurance companies have two general ways to grow their insurance business: Organic growth – capitalize on the hard market in P/C insurance Acquisitions Fairfax has a third way to grow its insurance business. Buy out partners Fairfax is flush with cash today. It has been generating record earnings in recent years. And earnings are expected to be very robust in the coming years. What to do? This is a great time to take out its P/C insurance partners. And that is what Fairfax has been doing. Over the past 4 years, Fairfax has spent $2.26 billion on 7 different transactions. In some transactions Fairfax took out the majority partner (Singapore Re and Gulf Insurance group). In others, they took out the minority partner (Eurolife, Allied World, Brit). Fairfax (and its shareholders) now own a greater share of the earnings of all of these high-quality P/C insurance companies. ————— 3.) Increase in Ownership of Equity Investments: Let’s now look at what Fairfax has been doing in its equity portfolio over the past 5 years. We are only going to look at what Fairfax has been doing with equity holdings that it already owned at December 31, 2019. To help with our analysis, we are going to split the equity holdings into two buckets: Consolidated equity holdings (where Fairfax owns more than 50% or exercises control) Equity holdings – excluding consolidated holdings Consolidated Equities = $1.34 billion Fairfax has invested $1.34 billion over the past 4.5 years in its consolidated equity holdings. The biggest purchases were Recipe and Peak Achievement. These are well managed companies with strong franchises and solid prospects. By materially increasing the number and size of companies in this bucket of holdings, Fairfax is growing an important 5thincome stream. One that is not correlated to the P/C insurance cycle. Equity Holdings (excluding consolidated holdings) = $1.1 billion Fairfax has invested $1.1 billion over the past 4.5 years in its other equity holdings (excluding consolidated holdings). Fairfax expanded the size of its partnership with Kennedy Wilson and the purchase of the PacWest construction loan portfolio in 2023 has become a home run investment for both companies. Metlen (formerly known as Mytilineos), Poseidon (Seaspan) and Altius have all been good to very good investments. ————— Summary Over the past five years, Fairfax has invested a total of $8.1 billion to increase its stakes in businesses that it already owns. As a result, Fairfax (and its shareholders) now own a greater proportion of the future earnings streams of these many quality businesses. The FFH-TRS investment has also been delivering an exceptional return. With these activities, Fairfax is growing the numerator of the EPS formula. At the same time, Fairfax has also been aggressively reducing the share count. With this activity, Fairfax is shrinking the denominator of the EPS formula. The combination of these two activities is spiking EPS at Fairfax. Conclusion: What did we learn? How Fairfax is investing right now is incredibly simple: Invest in what you know (high certainty/low risk). Be opportunistic (buy at a discount). Act with conviction (size bets appropriately… i.e. ‘back up the truck’ when appropriate) Cast a wide net (go global). What Fairfax has been doing over the past 5 years is exceptionally rational. Simple. Boring. And in aggregate, it has been delivering an exceptional return to Fairfax and long-term shareholders. I think the masters would approve of what Fairfax has been doing. In short, Fairfax has been putting on a master-class in value investing and capital allocation over the past five years. So, after all that, let’s get back to our initial question. What kind of an investor is Fairfax? Fairfax is a value investor. Their approach is a hybrid of 5 masters: Graham, Buffett, Templeton, Singleton and Lynch.