Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

Dexterra – DXT.TO Dexterra is a publicly traded company based in Canada (ticker DXT.TO). Fairfax owns 50.9% of Dexterra (32.0 million shares). As a result, from a financial perspective for Fairfax, Dexterra’s financial results are consolidated. Dexterra’s stock is currently trading at about C$10.10/share ($7.20/share). This puts the market value of Fairfax’s stake in Dexterra at about $230 million. Fairfax has a carrying value for Dexterra of $98 million. The excess of FV over CV for Dexterra is $132 million. This is economic value that has been created by Fairfax that is not captured in its book value. Dexterra pays a dividend of C$0.10/quarter = C$0.40/year ($0.29/year) = $9.1 million per year. This gives Fairfax a yield to CV of 9.3% ($9.1/$98). A short history of the company In 2018, Fairfax purchased Carillion Canada out of bankruptcy. The problem with Carillion was its UK parent went bankrupt. Fairfax paid about five times free cash flow for the Canadian operations. In 2020, Dexterra acquired Horizon North Logistics in a reverse takeover. Fairfax owned 49% of the combined company. This deal closed in May of 2020 (as Covid was raging). At the time, Dexterra’s CEO, John MacCuish, set the audacious target for C$1 billion in revenue and C$100 million in EBITDA in the ‘next few years.’ Dexterra has likely been a bit of a frustrating investment for Fairfax. But that may be changing. Part of the problems were external – the reverse takeover of Horizon North was completed in May of 2020, right in the teeth of Covid. And covid hit both Dexterra’s and Horizon North’s businesses very hard. Spiking inflation in 2022 then hit Dexterra hard (it took time for the different business units to reprice contracts higher). Part of the problem was a big misstep by the former CEO and an ill-fated foray into modular housing (this unit was sold in 2024). However, it appears the management team at Dexterra has stabilized its business and is shifting back into growth mode. They recently expanded into the US and this now gives the company a long runway for growth. The stock has responded – at C$10.10/share, it is trading at all-time highs. Management presentation from September 2025 https://ir.dexterra.com/wp-content/uploads/2025/09/Investor-Presentation_September-2025.pdf Comments from Prem about Dexterra from the 2024AR. "Dexterra is on track to achieve its vision of becoming a leader in delivering quality solutions to create, manage and operate infrastructure across North America. Mark Becker and the team made significant progress in 2024. Dexterra delivered strong profitability, free cash flow and organic growth from continuing operations. The company also closed an important U.S. acquisition in the facilities management space and sold its modular business consistent with its capital light philosophy. The company has reorganized the existing business from an operating and reporting perspective into two segments – support services and asset-based services. This change provides a clear strategic direction for the future. Dexterra enters 2025 with good prospects, a strong balance sheet and debt well under 1x EBITDA. It has the financial flexibility to continue to scale the support services business through organic growth and strategic, niche acquisitions. Dexterra is carried on our balance sheet at $97 million ($3.08 per share), which is significantly less than the market value of $170 million or $5.42 per share (Cdn$7.80). Dexterra has paid Cdn$49 million in dividends to Fairfax since our initial investment in 2018."

-

@glider3834, that is great work. Bottom line, it appears Eurolife has been a cash cow for Fairfax right from the beginning in 2016. It looks like €813 million for 80% of Eurolife’s life insurance business is good price for Eurobank. Which is also good for Fairfax given their large ownership stake in Eurobank. . Of the dividends paid to FFH Group Holdings from 2016 to 2021, i wonder if it was split between Fairfax and OMERS. Or if it all went to Fairfax.

-

A few final thoughts (for now) on Fairfax's recent sale of Eurolife's life insurance business to Eurobank: The importance of having a seat at the table Over the years, I have been quite critical of Fairfax’s initial investment in Eurobank. Eurolife has been a very good investment for Fairfax. At least that is my assumption given what we know today. We will know much more as Fairfax discloses more details on the transaction. It is likely that a big reason Fairfax was able to purchase 80% of Eurolife in 2015/16 was because it was already a large shareholder of Eurobank. I tend to look at Fairfax and its various holdings/decisions in a very narrow way. This can sometimes (often?) be too simplified of a way to look at things. Readers need to keep this in mind. ————— Minority partners Using a minority partner (OMERS in this case) allowed Fairfax to buy 80% of Eurolife when it was short on cash in 2016. Fairfax took out OMERS in 2021. Having the ability to use the balance sheet of trusted, long term external partners like OMERS is a big benefit for Fairfax. In a kind of an ironic twist, Fairfax could now use the significant proceeds from the sale of its 80% stake in Eurolife’s life insurance business ($944.7 million) to take out its minority partner in Allied World. Essentially, it’s kind of like Fairfax trading its 80% ownership position in Eurolife’s non-core life insurance business for the 16.6% of Allied World that is currently owned by minority partners (bringing Fairfax’s ownership in Allied World to 100%). Allied World has been Fairfax’s top performing P/C insurance subsidiary in recent years. That looks like a very good trade in my book. ————— 'Transaction tree' In sports it can be quite interesting to put together a 'trade tree' for when a player is traded which visually captures all subsequent trades of the players and draft picks involved. It would be really interesting to try and construct a 'transaction tree' for Fairfax that captures an initial investment and then (over the years) all the subsequent 'trades' in the form of money in (dividends and proceeds as the asset is monetized) and money out (what the proceeds were then reinvested into). In a chart. This would provide a very interesting take on the long term value creation that has been happening at Fairfax, especially in recent years. It would show how one good transaction often leads to many more good transactions in future years. Yes, this is hard to do in practice. However, I think it has merits as a thought exercise. It would likely really demonstrate the power of compounding and time - as it pertains to Fairfax's business model today (and how well they have been executing).

-

P/C insurance stocks have been aggressively selling off the past couple of days. What is the problem? I think it is muted top line growth - concerns the hard market is ending (has ended?). Fairfax has also been selling off. It is back below US$1,700. And I love it. My guess is Fairfax is going to report strong earnings in Q3. They are going to be all cashed up. And hurricane season is almost over. What will Fairfax do with all the excess capital they are generating? I hope they buy back a bunch more stock. They were buying aggressively in Q3 (at about $1,700/share). We also just got news from Fairfax of the sale of Eurolife’s life insurance business. That will provide a nice realized gain in Q1-2026 when it closes. Proceeds will be US$944.7 million (less $69 million for P/C insurance business in Cyprus).. Long term shareholders of Fairfax should welcome a low share price. It allows management to buy back a meaningful amount of stock at a low price. This is very accretive for long term shareholders. Capital allocation 101. With the stock at US$1,700, I prefer stock buybacks to taking out minority partners in Allied World and Odyssey. I think the stock is cheap - so prioritizing buybacks makes sense. The minority partners can be taken out down the road when the stock is more fully valued. Fairfax has a large number of excellent reinvestment opportunities - to compound its capital at above average rates of return. Its opportunity set is much, much larger than most P/C insurance companies. This gives them a big advantage as the hard market comes to an end. Fairfax is not a one trick pony.

-

I made the same error when I posted on Eurobank's takeout of Hellenic Bank. At least I am consistent. Thanks for pointing this out.

-

What return did Fairfax generate on its investment in Eurolife over the past 9 years? (The initial purchase closed August of 2016.) We will need to wait until Fairfax reports results to get the full picture. My guess is this investment has worked out very well (and perhaps even exceptionally well) for Fairfax and its shareholders. The return Fairfax earned will be comprised of the following items: Total amount paid by Fairfax for 80% stake in Eurolife Aug 2016 = 40% = $181.0 million (€162.5) 2017 to 2021 = 10% = amount paid? (My guess is about €40 million) July 2021 = 30% = $142.7 million (€120.7) Dividends paid from Eurolife to Fairfax (see details below for payments made from 2016 to 2019) Although we don't get the exact amount that went to Fairfax, we can assume it was a big number (compared to the amount they had invested). Total amount paid to Fairfax for its 80% stake in Eurolife's life insurance business: $944.7 million (€813). Value of 80% of Eurolife's P/C business which Fairfax continues to own. At Dec 31, 2024, shareholders' equity (100%) = €66.1 million (US$68) If we value the business at 1.5x BV = US$100 million. This puts Fairfax's ownership stake at about US$80 million. Summary Fairfax paid $181 million in August 2016 for 40% of Eurolife. Over the next three years it received large dividend payments from Eurolife (likely covering much of the initial purchase price). It invested about another $190 million from 2017 to 2021 to increase its ownership to 80%. In October 2025 it sold its 80% stake in Euolife's life insurance business for $944.7 million. It is retaining its 80% ownership position in Eurolife's P/C insurance business likely worth about $80 million. This is important to understand because it gives us the opportunity to evaluate the management team at Fairfax and their capital allocation abilities. Comments from Prem about the Eurolife purchase from Fairfax’s 2019AR. "Through the crisis in Greece, we acquired a gem in Eurolife, a Greek property and casualty and life insurance company that operates predominantly in Greece but also in Romania. Alex Sarrigeorgiou has run Eurolife since 2004, following Eurobank’s decision to grow its insurance business, and we acquired it with OMERS as our partner in 2016. Since our initial 40% purchase of Eurolife in 2016 for €163 million, Eurolife has earned €347 million and paid dividends of €298 million and shareholders’ equity has increased from €400 million to €720 million at the end of 2019 after the payment of dividends. This phenomenal performance was predominantly because Eurolife had a significant holding of Greek government bonds whose rates went from 8% to 1% during that time period while its non-life business had an average combined ratio of 72%. We currently own 50% and equity account for Eurolife but plan to buy the rest of OMERS’ shares in 2020."

-

@giulio, thanks for posting. This continues to simmer away on the back burner...

-

It might make sense to come at it from two angles: What is driving the gold price higher? Is it a cyclical (short term) or secular (longer term) thing? What is going on at the company? On both fronts, I think it makes sense to continue to hold Orla. Yes, it will be volatile.

-

I agree. I have been harping for years about 'move to quality.' It's not just on the buy side (new purchases). It's also internal expectations within Fairfax - these have been raised. Holdings are expected to be profitable. To actually deliver a 15% return over time. That wasn't the case pre-2017 - back then it was more of a hope. And when they floundered (which happened often) they were constantly bailed out by mom and dad (Fairfax). There seems to a much, much better financial discipline within Fairfax these days. And it looks like this financial discipline is getting institutionalized / becoming part of the culture. I just look at what was going on in 2015, 2016 and 2017 (and previous years). Since about 2018, everything has gotten much better. It is hard to put it into words. Since 2018, compounding has been working its magic. Value is being created. Much more than is generally appreciated. That is likely why Fairfax is buying back a meaningful amount of stock at US$1,700/share. They see all the hidden value.

-

Below are some of my key take-aways from Fairfax’s recently announced sale of its 80% stake in Eurolife’s life insurance business to Eurobank (who owns the other 20%) for proceeds of US$944.7 million. Fairfax will also buy 45% of Eurobank’s P/C insurance business in Cyprus for $69 million. Both transactions are expected to close in Q1 2025. 1.) This is a very large transaction. Proceeds to Fairfax will be $876 million ($944.7m less $69m). 2.) This is a strategic transaction. Financial services in SE Europe is moving to an integrated model - banking, wealth management and insurance. Life insurance is a core business for Eurobank (buyer). Not for Fairfax (seller). Fairfax continues to own 80% of Eurolife’s P/C insurance business in Greece/Bulgaria. And expands into Cyprus (buying 45% of Eurobank’s P/C insurance business in Cyprus for $69 million). 3.) The price being paid is fair for both parties (P/BV = 1.45 x at Aug 31, 2025). This makes sense given Fairfax owns about 32.3% of Eurobank. 4.) This deal demonstrates that Fairfax is a good long term partner. When it needed cash back in 2016, Eurobank sold 80% of Eurolife to Fairfax. Now that it is flush with cash, the life insurance asset is being returned to Eurobank - where it has always belonged. This should help Fairfax with future deal flow. 5.) Fairfax’s use of minority partners has been brilliant. When Fairfax bought 80% of Eurolife in 2016 (for $361 million) they were also short on cash. They brought on OMERS as a short term partner, with each paying $180 million for 40% of Eurolife. Fairfax took out OMERS in 2021. 6.) This transaction allows Fairfax to successfully monetize another investment. Fairfax should book a large investment gain when the deal closes in Q1-2026. In very rough terms, Fairfax paid about $361 million in two instalments (2016 to 2021) for 80% of Eurolife. Fairfax has also received significant dividends from Eurolife. When the deal closes, Fairfax will be paid $944.7 million and will continue to own the legacy P/C insurance business of Eurolife. We will likely get more of the financial details when Fairfax reports Q3 results in a few weeks. 7.) This transaction will come as a surprise to investors/analysts. It shouldn’t. This is the third asset monetization of 2025 for Fairfax (after Sigma in Q1 and Praktiker in Q3). Each year Fairfax monetizes/revalues a number of assets - it is an important part of their business model. For 8 years Fairfax has been improving the quality of the assets (insurance and equities) on its balance sheet. With transactions like Eurolife, we are seeing the results. With much more to come. 8.) Over the past 5 years, Fairfax has been delivering a masterclass in capital allocation. This transaction is just the latest in a long list of accomplishments for the company. Welcome to ‘new Fairfax.’

-

@dartmonkey, what do you think Fairfax is trying to do when it comes to the average duration of their fixed income portfolio? As you see it, what primarily is the problem they are trying to solve?

-

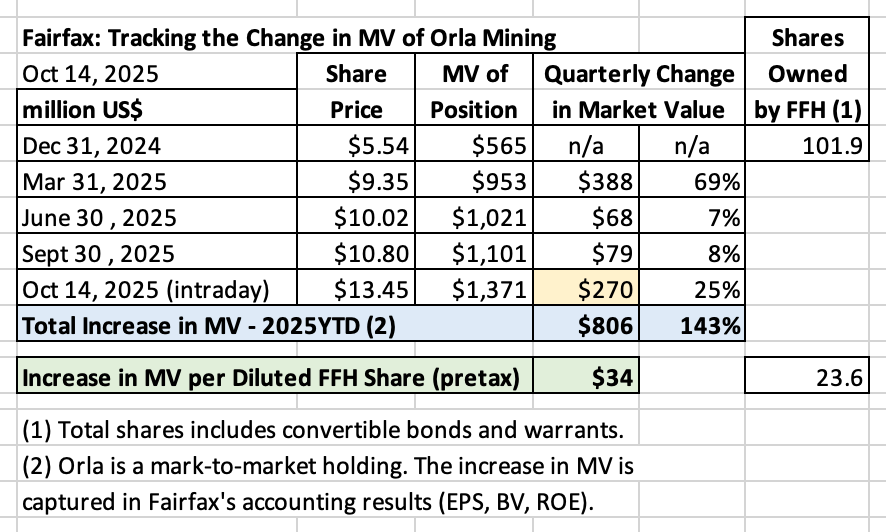

Orla Mining's stock is having a big move today. Fairfax's investment in Orla is up US$270 million since Sept 30 (+25%). YTD-2025, the investment is up $806 million, or 143%, or $34/FFH diluted share (pre-tax). Orla is quickly becoming one of Fairfax's best equity investments ever. Fairfax started building their position in Orla in Q3 2022. They slowly built it up with open market purchases over the next 2 years (to Q3, 2024). They got more aggressive with the position with the convertible and warrant deal in Nov 2024. Bottom line, this is a new investment for Fairfax. Fairfax's equity portfolio is having a banner year in 2025. Why did Orla's stock spike higher today? The company announced gold production for 2025 is expected to come in at the high end of their (revised) forecast. Earlier this year, Orla experienced a big issue at its Camino Rojo mine. It appears the plan the company put in place is working. From Orla's press release: "With pit stabilization at Camino Rojo progressing well and integration at Musselwhite advancing smoothly, both operations are performing well. We are now on track to achieve the high end of our revised production guidance." https://orlamining.com/news/orla-mining-reports-strong-gold-production-from-musselwhite-in-third-quarter/

-

@sholland, nice summary Feel free to use any of my material (that goes to others on the board). After all, much of what I post comes from others on the board. One suggestion is you might want to link readers to the most recent copy of my book/PDF.

-

@Munger_Disciple Great points. Two posts that I plan to write on Fairfax are: Treats shareholders honestly and fairly. Virtually 100% of his net worth is in the stock. Both of these points are very important. And are largely ignored by investors and analysts.

-

Bingo. Fairfax is not a clone of Berkshire Hathaway (and it is not trying to be). But Fairfax is the closest thing today that investors will be able to find to a much younger Berkshire Hathaway. This should allow Fairfax to compound capital at above average rate of return - with the prospect that returns could be even better. I think the one thing that slowed BRK’s compounding was the size of the company. Fairfax doesn’t have that problem. And given Fairfax will sell stuff (if/when it makes sense) and is very aggressive with share buybacks, I don’t think size is going to be a problem any time soon.

-

@Hamburg Investor, that was a great post. Thanks for taking the time to pack it full of interesting thoughts. It really highlights how many things can throw an investor off a great opportunity - even when it is staring them in the face/obvious. I especially liked the point about how much Berkshire Hathaway was changing over the decades.

-

I discovered Buffett in the early to mid-1990’s. I think he and Berkshire Hathaway were pretty well know by then. Hagstrom released his book ‘The Warren Buffett Way’ in 1995. I think the consensus view at the time was that Buffett was old school / likely past his prime. To your point, this was DEFINITELY the view in 1998 / 1999. Anything that wasn’t .com was avoided/shunned. I have invested in BRK over the years. And done reasonably well each time. But they were usually small positions and sold after a nice pop in price. With hindsight, I made a bunch of mistakes. But I do owe Warren Buffett a huge debt of gratitude. Buffett got me hooked on value investing as a framework. And that lead me to ‘the Corner of Berkshire and Fairfax’ in about 2003. And that lead me to Fairfax. And the other members of this wonderful forum. 22 years later the results have been magic. Funny how things work out sometimes

-

Fairfax's stock is down 1% on the news (sale of Eurolife's life insurance business). Yes, Fairfax is not being traded in Canada today (Canadian Thanksgiving). And volume in the US is anemic. But still... does this make any sense? I don't think it does. It just kinds of demonstrates how under-followed/misunderstood Fairfax still is. And I love it. There are many really interesting angles/learnings from this transaction. It will take me a day or two to get my (many) thoughts together. But here is one... The surprises we are getting from Fairfax these days continue to be skewed heavily to the good/very good variety. Welcome to ‘new Fairfax.’ This is what happens when you own a quality business. Fairfax is a quality business - and they own a growing number of quality businesses. There is a significant amount of embedded leverage there that investors/analysts (still) do not understand/appreciate. This might not sound like a big deal today. For long term Fairfax shareholders/followers, it is a big deal. This was not the case with the 2010-2020 version of Fairfax (what I like to call ‘old Fairfax.’) Many of the surprises back then were of the negative variety. More to come on this transaction over the next couple of days. To set the table a little bit, here is what Prem had to say about the purchase of Eurobank in Fairfax's 2015AR. "Late in 2015 we agreed to acquire 80% of Eurolife, a life and property and casualty insurance company which is the third largest insurer in Greece and which distributes its products through Eurobank’s network, for $347 million (€316 million) – at about its underlying book value. We got to know Alex Sarrigeorgiou in the last few years and were very impressed with him, his management team and their track record. The company writes €306 million in premiums – €248 million in life insurance and €58 million in property and casualty. Over the past ten years, the property and casualty operations have had a combined ratio of 60.0% while the life insurance operations produce stable earnings with plain vanilla products. Eurolife had net income in 2015 of €48.4 million, 45% from life and 55% from P&C. We welcome Alex Sarrigeorgiou and the over 300 employees of Eurolife to the Fairfax family. As we did with Brit, where OMERS purchased 30% from us to help us finance the acquisition, we expect OMERS to buy 40% of Eurolife’s shares at close to help us finance the acquisition. In the case of both Brit and Eurolife, we expect to be able to acquire the interests back within the five years after closing, after providing OMERS with an acceptable return. The team at OMERS has been a pleasure to deal with."

-

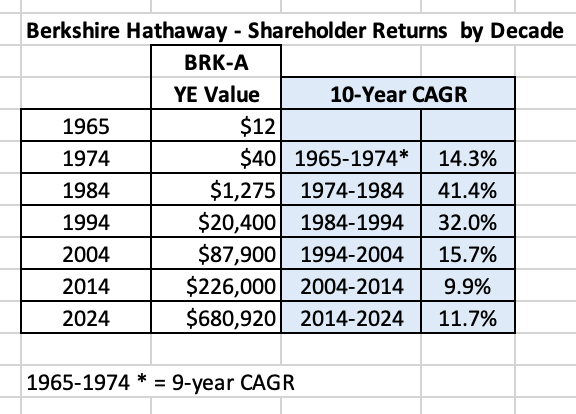

We are going to channel Charlie Munger and ask a question today. We are going to invert. Berkshire Hathaway has delivered an unbelievably high return for its shareholders over the past 59 years. However, two 10-year periods were MUCH better for investors than others: 1974 to 1984 = 41.4% 1984 to 1994 = 32% Starting point matters. Stocks were very cheap in 1974. And Berkshire Hathaway was a very small company. My question is what stopped an investor from buying Berkshire Hathaway in the 1980's or even the early 1990's? And then pulling a Rip Van Winkle? I have my own thoughts. But, before I share those, I would love to hear from other board members. Perhaps you care to share your own story. Or you have thoughts about Mr. Market (what other were thinking at the time). Or perhaps you were one of the few who bought Berkshire Hathaway decades ago, got your position size right, and pulled a Rip Van Winkle. What was your thinking that allowed you to do this? My guess is many more older board members got their investment in Berkshire Hathaway wrong than right - but I am happy to be corrected. This is a very relevant question/topic today because of Fairfax. Personally, I don't want to make the same mistake with Fairfax that I made with Berkshire Hathaway (grossly misjudging the opportunity). Of course, to do this I need to correctly diagnose the problem first: What was the mistake that I made with Berkshire Hathaway many years ago? (Or mistakes in my case.) But 'grossly misjudging the opportunity' is a cop out. It doesn't really say anything helpful. I am hoping to get into the juicy stuff with this thread (specifics). I look forward to discussing this important topic with other board members.

-

Listening to Baker Mayfield in the Q&A reminded me of the journey that Fairfax has been on in recent years. Understanding narrative is an important part of investing. Narrative follows results/stock price (it doesn't lead). I always thought it was the other way around. 'Just gotta be yourself...' Nice description of how Fairfax operates. Here is a short clip of the Q&A.

-

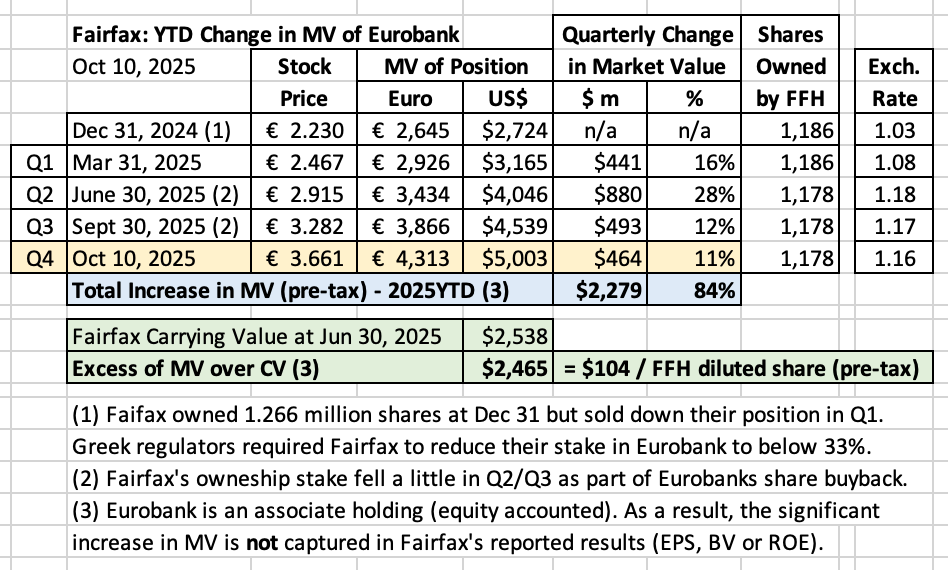

Fairfax's stake in Eurobank now has a market value of $5 billion. This makes it Fairfax's largest equity holding by far. How is it performing? YTD, the stock is up 84%. The MV of Fairfax's stake in Eurobank is up $2.3b. Fairfax has also been paid a dividend of $142 million, which puts the total gain on Eurobank at $2.42 billion. The excess of FV over CV is about $2.3b (accounting for the increase in CV in Q3), or $100 per diluted Fairfax share. This is value that has been building over the past couple of years that has not been captured in Fairfax's accounting results. This means Fairfax's reported EPS, BV and ROE has been understated in each of the past 4 years. (This is not unique to Eurobank). Investors need to keep this in mind when they compare Fairfax's past performance to P/C insurance peers (Fairfax's outperformance versus peers has been even better than what the accounting metrics show). Fairfax's equity portfolio is having a monster year. My guess is its total return this year is likely up around 25% (increase in intrinsic value). This is after very good years in 2024 and 2023. What we are seeing play out is the strength of Fairfax's business model. One that most other P/C companies refuse to copy. That is called a moat.

-

@glider3834, this is super interesting. Thanks for posting. Size: repurchasing 132,000 shares in one month is meaningful (0.6% of effective shares outstanding). 285,000 in the quarter = 1.3%. Value: Fairfax appears to have paid about US$1,740/share (rough guess) for the repurchases in September. This strongly suggests they see good value in their shares at this price level.

-

Fairfax’s stock did terribly from 2010 to 2020 for one big reason: the equity hedges. The short positions were a second smaller factor. Everything after this pales in comparison - I.E. excluding these two factors, Fairfax’s performance would have likely been ok (including lower interest income from how defensive they were with the duration of their fixed income portfolio beginning at the end of 2016). Fairfax booked about $250 million in realized gains when they sold off their corporate bond portfolio in 2021 (at a yield of 1%). And in 2002/03, Fairfax avoided billions in losses in their fixed income portfolio because of how defensive they were positioned. And because they were so short duration, in 2022/23 the earn through from much higher rates (much higher interest income) was very quick. When you add up all the puts and takes, Fairfax likely did very well with the total return they earned on their fixed income portfolio from late 2016 to 2023.

-

People who want Fairfax to lengthen the duration of their fixed income portfolio appear to be looking primarily at one thing - interest income. They want it to be big today and stay that way. It is very seductive to think this way (it sounds good/makes sense). I think it is really simplistic. But they do not talk about the risks of executing that strategy (going with a higher duration bond portfolio). Higher return often means taking on higher risks. Are you being compensated appropriately for taking the higher risk?

-

The yield on the US 10 year treasury is 4.15% today. When it comes to 10 year US bonds… are you getting paid an appropriate amount to take duration? The 2 year has a yield of 3.6%. Is a premium of 0.55% high enough? I don’t think it is… by a lot. It is pretty clear that the US has a big spending/debt problem. How does this problem always get resolved? High inflation. It’s not complicated. Tariffs? Inflationary. Not complicated. Deglobalization? Inflationary. Not complicated. The US can no longer be trusted. This did not start with Trump, although he is removing any doubts (it really got going with the confiscating of Russian assets/holdings/reserves). That means, all things being equal, the US should pay a higher interest rate on its treasuries to compensate for this risk. Fed? It WILL be stacked with Trump lackeys over the next year. Maybe they get it right. But maybe they don’t. (Remember ‘right’ will be whatever Trump wants them to do.) Trump cannot be trusted. Trump would not hesitate to throw the bond market under the bus if it furthered his personal aims. Trump is the master at doing unconventional stuff. I don’t think the 4 points above are debatable. Why would you want to own a 10 year US treasury yielding 4.15%, given all the significant risks outlined above? Because you want to blindly match duration with your insurance liabilities? That seems incredibly shortsighted to me. especially when you can get a 3.6% return with a 2 year treasury. Personally, I love how Fairfax is positioned with their fixed income portfolio. It seems really rational to me. Over time, we will get clarity on each of the 4 issues I highlighted above. As more information becomes available, my guess is Fairfax will act accordingly. Sounds good to me. PS: Gold just went through US$4,000. Why is gold in a bull market? Things that make you go hymmm…