nwoodman

-

Posts

1,892 -

Joined

-

Last visited

-

Days Won

15

Content Type

Profiles

Forums

Events

Everything posted by nwoodman

-

Thanks, a really interesting anecdote for my boys. Greatly appreciated I always find it helpful to learn more about the parents of people I am interested in. Could I trouble you for a short anecdote on Dad and how he came to be invested in Berkshire in the first place? I realise you are travelling so no hurry.

-

Indulge us. From what you have mentioned Berkshire and Gallagher have been key stakes. Your posts have been really helpful in terms of developing my own views on investing and in particular the Charlie Munger’s view of “sitting on your hand”. I am in the process of trying to illustrate this concept to my kids (young adults). I think your journey would provide a useful analogy in addition to the usual investing gurus as I believe your net worth delta is arguably more impressive as it did not rely on OPM?

-

I’ll take the $84 bn market cap right now if it’s in the offing , kind of thought that might be a story for 2030+. However very pleasing to see that they have some other assets in mind other than, perhaps, a particular bank

-

The way I don't lose too much sleep over the potential appointment is to think about Ben more along the lines of Howard Buffett's future chairmanship of Berkshire. I will say that listening to Ben's recent interviews etc, he seems to be pretty sharp. It wasn't that long ago that Prem was going to start giving the CCs a miss and leaving it up to the other execs, and there are some talented folks in that mix. Perhaps we will see Prem consider pulling back a little now that the share price has recovered somewhat. He is certainly a lot quieter in terms of media at the moment, it wasn't that long ago it was "Prem Everywhere". There is zero value in hauling it over the coals, but it sure is a different Fairfax post Paul Rivett, too.

-

Personal Account Retirement Account Last year https://thecobf.com/forum/topic/20016-share-your-portfolio-2023/?do=findComment&comment=517254

-

+1 or perhaps that should be +1200 USD.

-

It sounds like the sale will be delayed until after the election (April/May). As far as I can tell it is still a two horse race: https://www.financialexpress.com/business/banking-finance-no-hurried-merger-if-another-bank-acquires-idbi-bank-3283816/

-

If there was a single narrative that could get Fairfax trading at 1.5x’s book it would have to be India

-

Good way to look at it. I would normally be in the bitching camp but am ambivalent as it it is great to see them having the confidence in their current financial position.

-

Zeihan on India - demographic tailwinds good for at least 40 years

-

Movies and TV shows (general recommendation thread)

nwoodman replied to Liberty's topic in General Discussion

+1 Brilliant. The first two seasons were good but S3 seems to have turned it up a notch. -

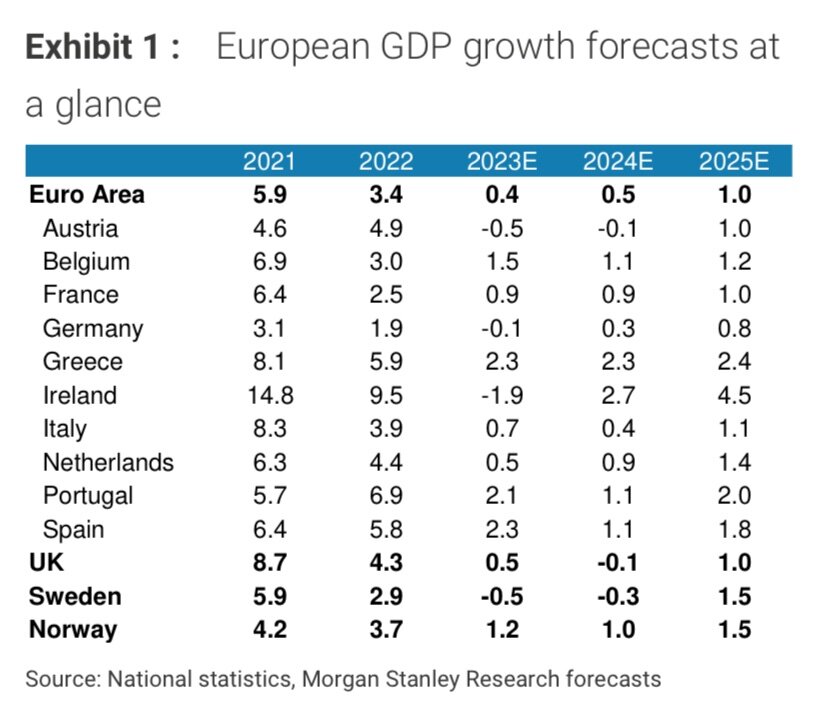

Well deserved and are likely to outperform over the next couple of years. MS recently released their outlook for 24/25 and this forecast caught my eye: While growth is forecast to slow they are still likely to be one of Europe’s top performers. They also had the following to say: “Fiscal consolidation under way: Greece has returned to primary surplus already in 2023. With the country's debt/GDP ratio at around 170% of GDP as of end of 2022, fiscal consolidation is a priority for the government. We expect the government to converge to a 2% primary surplus already in 2024. Debt/GDP should remain on a downward trajectory, reaching 148% of GDP by the end of 2025 on our forecast. Even if interest rates remain elevated, the debt comprises mostly institutional loans at a fixed rate, making its interest rate bill less sensitive to interest rate increases. Back to investment grade: After more than a decade, Greece returned to IG (DBRS and S&P). Moody’s and Fitch remain below IG, and we think that it will only be a matter of time before the two agencies also move to IG, the latest in 1H24, in our view. One of the more immediate benefits of IG status will be Greece's inclusion in indices as well as eligibility under the ECB’s collateral framework, and hence for ECB asset purchases. Current rules, with the exception of PEPP, list that a government bond needs to hold IG status from at least one of DBRS, S&P, Fitch and Moody’s. The upgrade of Greek government bonds to IG should also have positive spillovers onto the Greek economy by lowering the country’s cost of borrowing as well as by attracting more investment.” Non- paywalled link to the Economist Article https://archive.is/dx5Qj YEARAHEAD_20231112_2100.PDF

-

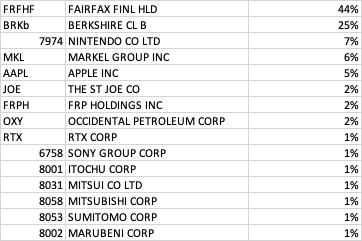

+44%. Thanks FFH and Mr Market. Running 1.3x’s leverage, so I take my hat off to those unleveraged board members with alphas of 20-40%, truly impressive.

-

Merry Christmas. Thank-you one and all for so much food for thought, such a magnificent collection of clever people.

-

Haven’t fully crunched the numbers but this growth in lending seems somewhat higher than GDP growth. Eyeballing it seems around 12-13% CAGR over the 9 years from the graph. Something to keep an eye on and a good test for the RBI. https://asia.nikkei.com/Business/Business-Spotlight/Indian-consumer-borrowing-surges-raising-fears-of-defaults “The central bank's change of risk weightings could prod lenders to increase rates, thereby discouraging consumers from reckless borrowing, analysts say. If banks choose to absorb the cost, their margins will shrink, making unsecured loans a less attractive segment. Financial services company Paytm said in a statement that it would reduce the disbursal of small loans "on the back of recent macro development and regulatory guidance." "That nudge from RBI to be cautious on unsecured retail lending can push lenders to slow growth in this segment, which can also impact overall bank credit growth by up to 100 basis points," research company Jefferies wrote in a note.”

-

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

Now that’s my kind of funeral. RIP Shane McGowan Full Service https://www.youtube.com/live/tO8rWUq1U_A?si=_JmDkmBHp6CEmj8h -

Great post, but are you seeing something across the entire entity less stat requirements that can’t be solved “in a stroke of a pen” or is it more a sub risk. Along the lines of we had liquidity but it was good until reached for but has now ceased to exist. I.e multi cats.

-

-

I will leave it to more intelligent participants to answer your question directly. However, I did enjoy the body of your post especially the examples. My feeling it was a conscious decision by Charlie in terms of the problems he enjoyed thinking about and solving. I doubt going from $20m to $2bn for Charlie made that much of a difference in terms of lifestyle anyway. From what I can gather though he thoroughly loved giving it away and getting to use both sides of his brain. What an amazing man.

-

Am I wrong in seeing this as simply debt recycling and not really news? I don’t see it as necessarily improving medium term liquidity in itself at the HoldCo, but I question whether this is a real problem anyway. It is silly for me to even remotely make a comparison to my own situation but I see the cash balance in a sub as transferrable in minutes, so the aggregate cash is my primary concern. I realise that there are tighter regulatory controls for insurance Co’s. I think all being equal, their ability to generate profits that I thought were 5 years off, fixes this issue nicely.

-

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

I agree, it's almost a little over produced. Definitely a band that delivers live though. I had the good fortune to see another Australian export, Parkway Drive at Knottfest earlier this year. They blew me and the crowd away. Got home and listened to a few of their albums and it was the same deal, something seemed to be missing. As you say, some bands/ music styles are just better live. -

Thanks @SafetyinNumbers. That multiple is mighty impressive. “That is a near-30 per cent premium to Heathrow's regulated asset base. It is also about 13 times next year's ebitda, projected to fall given the cut in regulated landing fees. Listed competitors travel at around 10 times. Vinci, which bought 50.1 per cent of Gatwick in 2018, paid more, but that was for a pre-pandemic majority purchase. Ardian and PIF might end up stuck at 25 percent.”

-

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

I am amazed he lasted this long! Great band, Fairy Tale of New York and A Pair of Brown Eyes are my faves. -

Cheers, paywalled for me. Any additional metrics or info? Thanks @netcash1 for flagging this

-

Such a formative figure and at the top of his game to the very last. “We all are learning, modifying, or destroying ideas all the time. Rapid destruction of your ideas when the time is right is one of the most valuable qualities you can acquire. You must force yourself to consider arguments on the other side” In terms of his framework invert to solve, the courage to blow up your best idea and arguing both sides of an argument were a game changer for me. Still haven’t mastered it, but at least he made me aware.