nwoodman

-

Posts

1,891 -

Joined

-

Last visited

-

Days Won

15

Content Type

Profiles

Forums

Events

Everything posted by nwoodman

-

Given the large exposure Fairfax has to India, a separate thread for macro related info

-

Good stuff Glider. A couple of attachments 1. Eurobank Research MS Eurobank - Focus Shifts to Loan Growth.pdfMS Eurobank.pdf 2. MS Model 3. A link to a recent MS Podcast featuring Nida Iqbal the MS analyst on Eastern Europe, Middle East, and Africa (EEMEA) https://www.dropbox.com/s/quhxgbbck3oaj2w/MS Greek Bank Podcast.mp3?dl=0 Eurobank remains MS only overweight rec for Greece. Main reason is balance sheet clean up. 2022 is shaping up to be an absolute ripper for Fairfax. Between Atlas and Eurobank alone there could be >$100m of annual dividends heading Fairfax's way. Eurobank Model 10-21.xlsm

-

Movies and TV shows (general recommendation thread)

nwoodman replied to Liberty's topic in General Discussion

A big shoutout for the current spate of music doco's on Apple TV+. The Velvet Underground (Movie)- really enjoyed it. 2 hours was over in the blink of an eye. Todd Haynes directing style might not be for everyone but it worked for me...a masterpiece 1971: The year music changed everything (Series) - this filled in a lot of musical blanks for me. My Dad's record collection wasn't as diverse as it needed to be! Watch The Sound with Mark Ronson (Series) - Steps through the major advances in electronic music - Auto-tune, Sampling, Drum Machines etc. I didn't realise it but Mark's step father was Foreigner's guitarist Mick Jones. So he was living and breathing music from a young age. No muso, but this has inspired me to play around with Garage Band on the iPad for the first time in years. Who knows maybe one of those new Mac's with Logic Pro might be in my future -

Another article, they must be doing the rounds Digit Insurance to use funds to grow market share - Times of India (indiatimes.com) Key points: "According to Goyal, the ability to raise capital puts Digit in an advantageous position. “Last year, many non-life insurers grew aggressively. This year, the first quarter has been tough and some insurers had to release their claims reserves. We have been a bit cautious and had a good combined ratio in Q1 this year,” he said. The non-life industry is capital-constrained with three state-owned companies in loss and several Indian promoters not in a position to infuse capital. According to Goyal, Digit will use its capital to provide capacity to Indian industry including thermal power where there are capacity constraints with reinsurers backing out due to green reasons. "Digit Insurance has also reduced dependency on its call centre by enabling service requests on WhatsApp using artificial intelligence. “Earlier, for one lakh policies, we were handling 1,800 calls a day. Now, with 10x the number of policies, the call volume is around 2,300. We have, however, received 72,000 service requests on WhatsApp,” said Goyal."

-

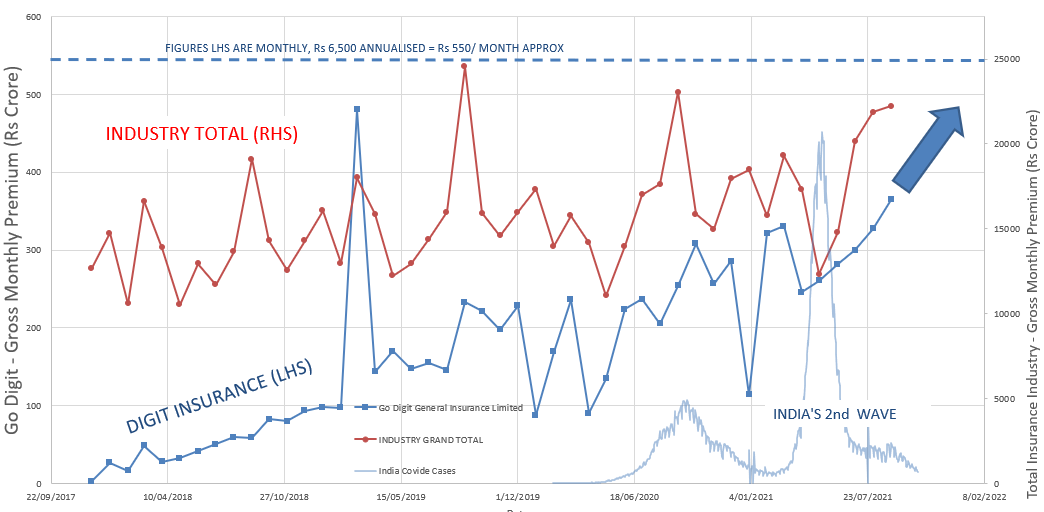

Based on the pickup in insurance after the second wave of COVID-19/Delta, that doesn't sound like a stretch at all. An update of the monthly IRDAI figures below, the different scales masks Digit's impressive growth. The overall insurance market is off to the races and Digit has hit the "nitro button". Oh and btw Thomas Cook just hit a 52W high

-

Never Been A More Exciting Time To Be In General Insurance, Says Digit Insurance’s Goyal (moneycontrol.com) - OCTOBER 15, 2021 A few key quotes: Q. From Digit’s perspective, how has the journey been so far? "Our customer ratings substantially improved on the back of digital and self-service processes and subsequent investments have gone here. Last year, we saw growth of 44 percent. In the current year, as the second wave hit, many players had stopped underwriting Covid-19 health insurance but we continued to do that and other business lines also saw a good amount of growth. So far, the first half has been good and growth has been almost 67 percent." Q. How is your solvency ratio looking like? "It was 180 as of June 30. After the approval of the recent capital raise I would expect it to be more than 300 by December 31. It will be one of the highest in the industry. Hoping the approval should come sometime this month and we will close the transaction within thirty days." Q. Any plans on listing? "Do we want to list? Yes. When? We don’t know at this stage. This is something we always thought that we wanted to be a listed company and have completed four years, we have raised a recent capital round. We will see where we are in 6-12 months’ time."

-

+1 @Viking Great write up, looking forward to your forthcoming book

-

Three stock picks from Matco Financial’s Anil Tahiliani "The markets have been extra volatile in recent weeks, but Matco Financial portfolio manager Anil Tahiliani isn’t shoring up extra cash for his clients, waiting for the skies to clear. Instead, his firm continues to invest in what it views as “solid, good companies” poised to grow over the long term. “Typically, we do well for clients at the early part of the economic cycle,” says Mr. Tahiliani, which he believes is where we’re at today, after the COVID-19 pandemic ravaged the global economy for most of 2020. While earnings growth won’t be as impressive in the coming quarters as it has been so far in 2021, when compared with a year earlier, Mr. Tahiliani expects it to remain strong as the global economy continues to recover. It’s why he’s sticking to his portfolio mix of about 95 per cent equities and 5 per cent cash. “To us, you should still be invested in equities,” he says. “You’re getting high dividend yields and stronger economic growth in Canada, the U.S. and globally.” Many investors also have little choice. “Equities are still the only game in town in order to meet inflation-adjusted returns and compared to bonds and other fixed-income products,” says Mr. Tahiliani, who oversees the Matco Canadian Equity Income Fund. Some of the fund’s top holdings today include Constellation Software Inc., National Bank of Canada, Bank of Montreal, Canadian National Railway Co. and Dollarama Inc. The fund’s one-year return, after fees of 1 per cent, is 23.8 per cent as of Sept. 30." His three picks were: 1. TFII-T 2. MG-T 3. FFH-T FFT-T: "Mr. Tahiliani describes Fairfax as “a unique play” – the company is a property and casualty insurer and a value investor. “What you’re getting with Fairfax is an insurance company, plus a diversified investment portfolio that consists of public and private investments,” he says. His firm purchased Fairfax shares in September, in part because of the company’s attractive valuation compared with its peers. Fairfax is “capital disciplined,” Mr. Tahiliani says. “It doesn’t pay up for assets, whether it’s buying other insurance companies or making public or private investments. [The company] is more looking for either distressed assets or turnaround assets that are selling at a discount, and that they can come in and buy below intrinsic value.” Fairfax is currently trading around $515 a share on the TSX, which is up about 25 per cent over the past year. It reached a 52-week high of $581 in May."

-

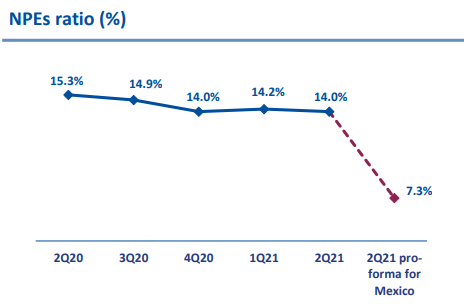

Thanks for the link. Another investment that has been 10 years in the making. “Via the great, ten-year ordeal, Greek companies endured, adapted and several (this is often overlooked) expanded and developed, having formed characteristics that allow them today, in the development phase, to look very high. And turn they have. FFH may have been too early/wrong with their investment in 2014. It doesn't matter now, the future of Eurobank is looking mighty bright. At Eurobank, we are happy that we were the first to open the way and everyone followed. And we are the first to have reached the 3rd quarter of 2021 with a single-digit NPL index of 7.5%," he noted. Graph below is from the 1H21 presentation, looks like they are still on track Update on Project Mexico UPDATE 1-Eurobank signs deal with doValue to sell bad loan portfolio notes (yahoo.com)

-

TSLA

-

NTDOY

-

+1 totally agree. A couple of quick points building on @Viking's and @glider3834comments above 1. While ATCO appears to be fully converted, the way it was structured made it much lower risk by moving up the capital structure eg warrants, senior note, prefs etc. Paid to wait - more Buffett. 2. They are going to have winners and losers. Currently the market is awarding them the title of "biggest loser" that's fine as it presents quite an opportunity. As their primary business is insurance I would be far more worried if the insurance companies were still writing at 100+ CRs. 3. As a basket their investments offer more winners than losers. At these prices they don't need to earn the title of the "biggest winner" to make an investor decent money. 4. Going one step further perhaps their investment framework is more suited to countries like India and its point in the economic cycle rather than overpriced DMs. So for me, FFH serves a dual purpose, deep discount on an OK insurance company and EM exposure. Deal flow counts for a lot when you are trying to allocate decent amounts of capital.

-

S&P Global Ratings - “Cyber Risks In a New Era: Reinsurers Could Unlock the Cyber Insurance Market” Greatly obliged

-

Well done again SJ. I had forgotten that provision, it was forced through as an amendment. I can read it and arrive at a slightly different interpretation but it is not completely at odds with your recollection. 1. Original Letter https://www.fairfax.ca/news/press-releases/press-release-details/2015/Fairfax-Calls-Special-Shareholders-Meeting-to-Consider-Amendment-to-Terms-of-Multiple-Voting-Shares/default.aspx 2. Amendments https://s1.q4cdn.com/579586326/files/doc_financials/2015/Chairman-Letter-(August).pdf

-

There has been a bit of chatter around insurance industry rags about cyber re/insurance after an S&P Global Ratings report was released a little while back. The tie in between BBY and Fairfax insurance businesses is likely not a new or unique thought. Does anyone know if a cybersecurity insurance tie-in has been discussed at any of the AGMs or anywhere else? Probably remiss of me but I don't think that much about Blackberry even though it is a fair chunk of FFH equity holdings, as a % it continues to decline. It is now in the mildly annoying but no longer a serious source of irritation, more like an option. Some snippets on the opportunity "Prices in the cyber re/insurance market could rise sharply between 2021 and 2023, in some cases doubling from current levels, according to a report from S&P Global Ratings. “Depending on the region and [terms and conditions], policyholders could expect rate adjustments of up to 100% because the risk level has fundamentally changed,” S&P Global Ratings said last week in its report, Cyber Risks In a New Era: Reinsurers Could Unlock the Cyber Insurance Market. https://www.canadianunderwriter.ca/insurance/will-cyber-insurance-rates-double-in-the-next-couple-years-1004213158/ Increasing Reinsurance Demand The report said the pandemic exacerbated the huge cyber reinsurance protection gap by causing existing and new clients to increase demand for the protect, requesting larger limits and more inclusions in their policies’ terms and conditions (T&C). “Primary insurers rely relatively heavily on the reinsurance market for cyber insurance because it has a relatively short track record compared with more traditional and mature property/casualty lines of business,” said S&P, estimating that they pass 35%-45% of global cyber premium to reinsurers, with some regional variation. Cyber Market Development S&P expects this business line to be one of the fastest growing insurance markets over the next decade. “The dynamic change in claims pattern, rise of cyber threats, and huge accumulation risk creates an opportunity for larger reinsurance capacity.” As a result of these trends, the number of reinsurers and insurers offering cyber coverage is rising, along with demand, but capacity is still limited, the report said S&P noted that the market would benefit from the development of a comprehensive retrocession market, as well as the use of insurance linked securities (ILS) or alternative capital to improve capacity. “The market faces increasing demand, but limited supply. In our opinion, lack of capacity could be holding back the development of a sustainable cyber re/insurance market,” the report affirmed. https://www.insurancejournal.com/news/international/2021/09/30/634535.htm cyber risks in a new era- reinsurers could unlock the cyber insurance market s.pdf

-

I thought this was an intriguing prospect to. I remember reading a lot about the potential for debt deflation given leverage in the system. Totally agree with SJ that this was a bet, not a hedge. They were looking for another MBS homerun. I ended up buying FFH as a hedge against their low ball offer on ORH in 2009. The deflation bets, hedges and even the shorts didn't worry me so much as Prem's rhetoric in 2017-2019 which I found quite remarkable, it just seemed plain confused and full of hubris. Citing individuals for massive changes in positioning eg Trump in my mind didn't warrant a multiple of book. The whole situation seemed, to quote my grandma, "discombobulated". The irony is that the index shorts may have actually helped repair his reputation in the market declines last year. Taking them off when he did, only inflicted double damage points. I sold out completely in 2019 and reinvested the funds (and got lucky). During the low's of 2020 ended up buying ATCO and later bought some FFH as a hedge, just in case of Fairfax played cute. The FFH position as subsequently grown somewhat using rather inflated currency (TSLA). A lot of what we are seeing now are seeds that were actually planted in 2017 and 2018 starting to take form. This is the best visibility/discount I can recall in the time I have been following the company. If you believe book value, then the only other low similar to this was the 9/11 sell off in 2001. It was pleasing last night to see the spike in Chemplast. While he may have lost the title of the Oracle of the North, perhaps the Oracle of India will suffice. I don't say that flippantly, foisting dogs like Farmer's Edge onto the market to have them crater only makes investors more gun shy. Chemplast is shaping up to be a win/win.

-

Excellent comments, especially the criticisms. My simple take is that this is an opportunity that is 10 years in the making. I am sure it wouldn't be lost on Prem that the opportunity that he got on Seaspan/Atlas was 10 years in the making too. Fixing the the insurance subs has probably taken just as long. I went back and grabbed the Y/E book values and overlaid them against daily prices. They don't capture the peaks or troughs but the average is around 1.1x's including today's massive discount and excluding my estimate of Q3 BV. The graph says to me that the market was more optimistic than the business warranted during the teens but is way too pessimistic now. The joys of a market. Given the share issuance during the period of optimism, I think Prem knew it too. If the thesis is correct then shares should be bought back in spades over the next few years. I would say in Baseball terms Prem and Team have a batting average that is not great but OK. Despite this they deserve a place in the big league and are finding some form again. There just may be a few home runs left in them yet and after a couple of good seasons the fans will be back.

-

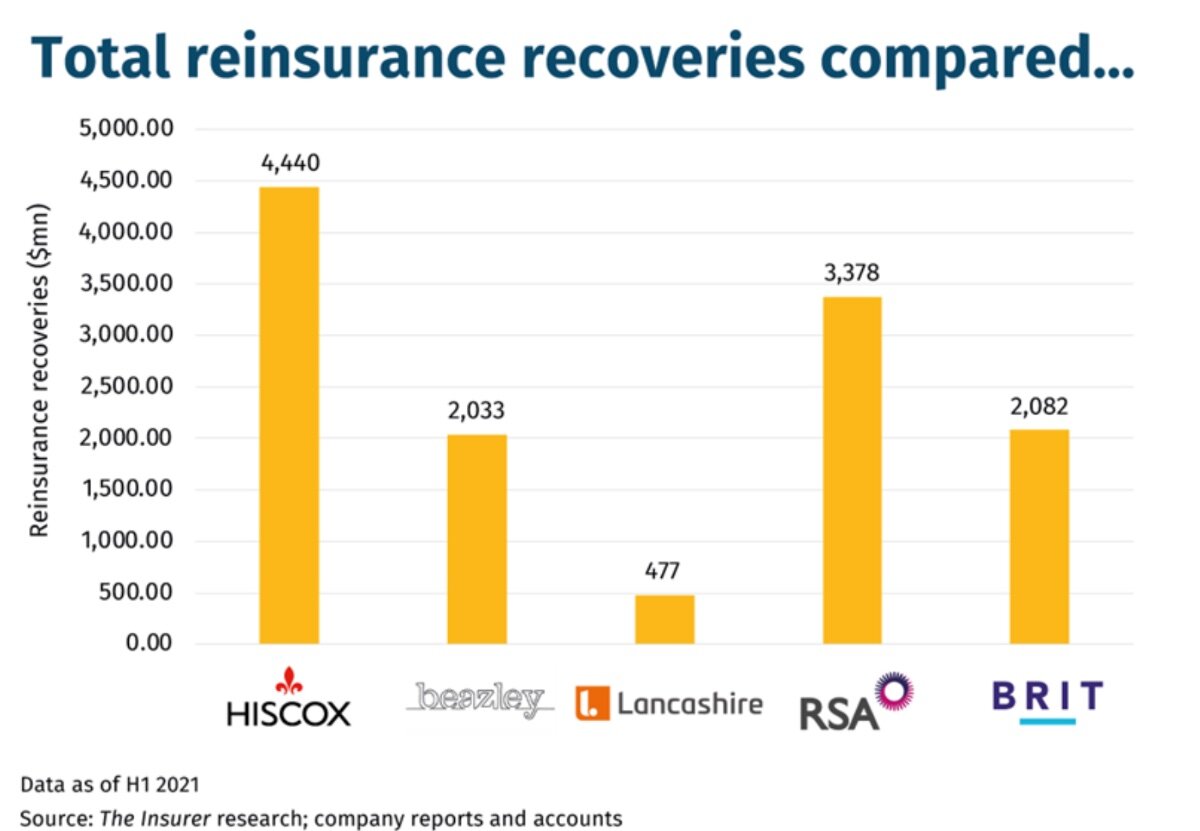

This article, 22nd September, implies that the issues around Covid BI reinsurance recoverables persists. While Hiscox was highlighted as having the greatest leverage, Brit is up there. Does anyone know how much of Brit’s book was/is BI? An extract from the CC below also reinforces the view that it is still a work in progress. The table below shows Brit’s recoverables to TE dropped quite significantly from H1/20 to H1/21 is a positive. https://www.theinsurer.com/analysis/hiscox-most-exposed-to-covid-bi-reinsurance-failure-as-impasse-continues/18350.article “As the industry-wide impasse between reinsurers and their cedants over certain Covid-19 claims continues, research by The Insurer shows Hiscox is leveraged at 2x tangible equity to reinsurance collectibles. The higher the number the greater an insurer’s sensitivity to reinsurance recoveries which have been booked as an asset on its balance sheet but are yet to be collected. Last month, Hiscox revealed its reinsurance recoveries had ballooned to a new record high of $4.4bn at H1 2021, a further leap on what was a new high of $3.6bn at year-end 2020.” “In contrast, a 10 percent adverse movement in reinsurance collectibles for Hiscox peers, such as Beazley and Lancashire or even Fairfax Financial-owned Brit Insurance, would have significantly lesser impact because they have substantially lower leverage.” From the recent CC Jaeme Gloyn Good. First question is on the on the reserve developments in the quarter and I guess for the first half of the year, kind of coming in the 1%-ish range. I'm seeing a little bit more favorable reserve development from other insurance companies. I'm just wondering if you can give us a little bit more detail as to what you're seeing on that front? If you can have any comments and maybe around Odyssey where we saw some unfavorable reserve development. Prem Watsa Jaeme, we've got Peter here who's our Chief Operating Officer, and he used to be the Chief Actuary. So, Peter, your comment. Peter Clarke Sure. I guess, Jaeme, I think what's distorting the numbers a little bit is we had approximately $60 million in development on COVID losses. So, that's sort of a one-off thing in our minds. And excluding the COVID losses, I think we had favorable development of around $90 million, which isn't that far off from the previous year. But generally speaking, it's the second half of the year where we do more thorough reserve reviews, specifically off the third quarter reserves and that's when we'll make more significant adjustments. Our reserves continue to be extremely strong and I think our companies are very conservative on the lost picks they're making on the current years. So, we would expect that we'll be building up some redundancy as we go through this strong pricing environment. Prem Watsa A basic view, Jaeme, that we've said for many, many years now is that the past reserves can develop favorably or unfavorably and we just want it to be developing favorably. And so it's a risk in the property casualty business and we've had favorable development, I think for more than a decade now and perhaps even longer than that. But that's a very important requisite in the property casualty business. Jaeme Gloyn Okay, understood. On those COVID loss development, can you describe what it was that was driving that? Is that anything related to BI [ph]? A little bit more color on those COVID reserve developments at all? Prem Watsa Sure thing. Peter? Peter Clarke Yes. Really, it relates on our reinsurance business primarily at Allied and Odyssey. And it's a non-U.S., so it's in Europe where there are still uncertainty around what's covered, what's not covered. Is it one event, many events? So it's really just IBNR that's still being put up on the reinsurance books, mostly in Europe. Jaeme Gloyn Okay. And related to BI, I guess? Peter Clarke Related to BI and some of the BI issues, you might remember the UK ruling came out late last year. That's still filtering through the system.

-

Indeed, and India has suffered. Programs like the proposed NMP Seem well considered and a sign that things are changing. There will be bumps in the road, but iit is a massive opportunity for India to advance and meet it's full potential.

-

Thanks Glider, whichever way you look at it the rubber band is stretched. Not sure what the thesis would be to sell at these prices. Can only figure it is end of quarter dressing or algos. What is going on under the hood at FFH all seems to be moving in the right direction.

-

Movies and TV shows (general recommendation thread)

nwoodman replied to Liberty's topic in General Discussion

At this price, I tend to agree. Also, saw your note on the Foundation Trilogy, thanks. That is what I have started with. I was hoping to get thru them prior to the Apple release but alas not. Still reading and watching the side by side is accretive. Also appreciate the observation that some of the characters from the later books have been meshed into the first two episodes, that makes more sense now -

That's a shame, there goes our hard market without a CAT or two to act as a wake up call. On a brighter note, I was recently thinking about what US5-10bn or so in float in the Indian market might be worth with CRs of 100 in the not too distant future. Assuming the capital allocation machine is working. Anyway the observation was more born out of what I have seen as a lumpy but long run average returns out of the likes of MKL, BRK and FFH. They seem to be 10-12% CAGR machines. My take is don't get starry eyed about the potential for significant returns buy with a healthy discount, nothing new in that. I think it applies particularly to FFH at the moment that is trading at a considerable discount. It goes without saying that as long as they don't blow up, a 10% return in a 2% borrowing world is more than acceptable....in fact that is an asset that is positively geared.

-

Movies and TV shows (general recommendation thread)

nwoodman replied to Liberty's topic in General Discussion

Watched the first episode of Foundation on Apple TV+. Very impressive production values. Never read Asimov’s books, so that is a work in progress which certainly helps. However, the kids were enthralled even without the background -

Totally agree, who the hell other than Fairfax fan boys know about Digit in the wider market, a couple of select PE players. In this small circle, the marks are not all that convincing but I am not saying they are way off. I would hazard a guess that they may even be conservative if let loose on an IPO mad Indian market at the moment. Digit will likely prove to be around 25% of “the Prem is a genius” or “Prem turns around Fairfax “ narrative at some point in the future but only after a few years and some other more mainstream investments that prove winners Eurobank (for the newcomers) and Atlas, and then the TRS. Even if the TRS takes a few years, the carrying cost is likely no more than OMERS, who knows maybe it is OMERS (9% funding guaranteed ) We are all here because we are value investors, and while we are here to make money I for one am also intrigued to see just how long regression to the mean actually occurs. I am betting no longer than 2024 and that the sum of the parts is growing at least 11% over the longer term. Not a high bar by any means. While we are all delighted that things are working out with a few of the investments and that there are green shoots all over the place, these seeds were sown at least 3 years ago. Many of these looked like they had withered on the vine even before Covid, so you can’t blame the market for being fascinated by shinier things. 11% CAGR kind of sucks if you bought and held but the long term opportunity cost after accounting for tax is likely acceptable. ie not completely wrong. The more I look at this Insurance/Float model you realise it is just not that exciting any more. Having said that your return is based on the price you pay and your returns suck if you drink the “Berkshire model” Kool Aid and over pay, you will not be bailed out by superior economics. You will do OK if you buy at a discount or better yet a deep discount which is where we are at with FFH I think everyone that has been in and out of FFH over the last 10-15 years knows that they are far from a 15% long term compounder. However from this point in time to get back to FV I think it will likely give you 20% CAGR for a few years. Nuts in this environment, but that’s the market for you. This will be extrapolated just as this period of “under performance” seems exaggerated. Agree with all though, that there are possibly structural and even mild cultural changes that may improve the odds of them not trading at such a large discount for long. Kkeep up the great work in terms of turning over the value rocks. It makes for interesting reading. However I must admit I am more interested In signs of misallocation at this stage that might halt or give pause to regression to the mean.

-

Very sad news. Not my area of expertise, but seems strange to have detailed on a straight section of track. Perhaps a mechanical fault rather than a structural issues with the rail itself? At Least 3 Killed In Amtrak Derailment https://www.npr.org/2021/09/25/1040734747/amtrak-train-derails-montana-injured Five Amtrak cars derailed around 3:55 p.m. Mountain Daylight Time and no other trains or equipment were involved, Weiss said. The train was traveling on a BNSF Railroad main track at the time, he said. Photos posted to social media showed several cars on their sides. Passengers were standing alongside the tracks, some carrying luggage. The images showed sunny skies, and it appeared the accident occurred along a straight section of tracks.