nwoodman

-

Posts

1,892 -

Joined

-

Last visited

-

Days Won

15

Content Type

Profiles

Forums

Events

Everything posted by nwoodman

-

Many thanks . Great results and the increase in duration is just brilliant. When it comes to Bonds these guys really are Masters of the Universe. It is a treat to watch the balance sheet get stronger quarter by quarter.

-

@valuesource any chance you can delete your post. There are links to the release no need to cut and paste the whole thing and it makes the flow of this thread very distracting. Thanks in advance

-

A sucker for their music business.

-

6758.T SONY

-

I believe MINT broke this news. It is unconfirmed IRDAI approval as far as I can tell. Sounds promising, hopefully Fairfax confirms tonight or on the CC as I couldn’t find anything on the IRDAI website….yet

-

That pretty much encapsulates the Atlas thesis - long term meat and potatoes vs short term sugar hit. A good reminder of how patient capital (strong hands) could make a difference to this industry

-

Sounds promising, although “these two people” have quite the reputation. Hopefully the IRDAI provides confirmation shortly

-

-

Stating the obvious but the best outcome below IV is to do both.

-

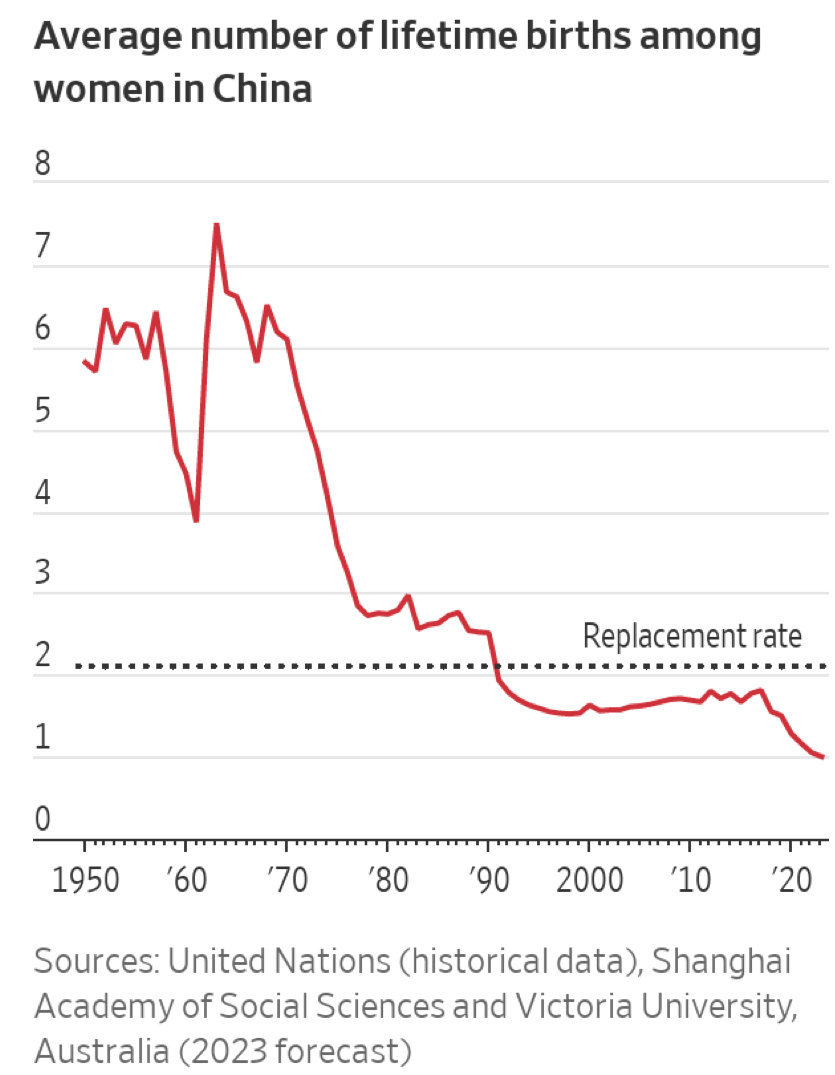

Good article in the WSJ today on the One Child Policy. How China Miscalculated Its Way to a Baby Bust "As the decades passed, a growing number of demographers and economists called out the policy as outdated and flawed. China’s fertility rate would have gone down on its own as life expectancies rose and economic conditions improved, they say. One factor missing from Song’s population math was human behavior. The government’s sometimes brutal enforcement, including forced abortions and sterilizations, as well as decadeslong propaganda about the benefits of having a small family, left a lasting one-child mindset. The modeling also failed to take into account the traditional preference for sons. If couples could only have one child, they would prefer to have a boy. Young women are now at the core of China’s demographic dilemma. They are increasingly reluctant to have children—and there are fewer of them every year. Greenhalgh, the Harvard anthropologist, said that the women growing up under the one-child policy were raised in line with Beijing’s goals of a smaller but what it called “higher-quality” population: well-educated, savvy and independent. “These women are not going to accept going back to the family to be housewives,” she said. Apart from cultural and social changes, Song’s model hadn’t taken into account economic forces, such as the enormous migration flows to cities unleashed by Deng’s reforms, which played a bigger role than anyone had imagined in pushing down fertility rates, researchers have said." “All of China’s population policies for decades have been based on erroneous projections,” Yi said. “China’s demographic crisis is beyond the imagination of Chinese officials and the international community.”

-

Good article, and by Seeking Alpha standards, extremely good. The source table for the Lloyds syndicates can be found here https://www.atlas-mag.net/en/article/ranking-of-top-20-lloyd-s-syndicates-in-2017 The site is quite helpful as below the table there is a link to prior years for a quick comparison. Given the hysteria around AI I really appreciate that Fairfax aren’t spruiking Ki. It is an exciting development nonetheless.

-

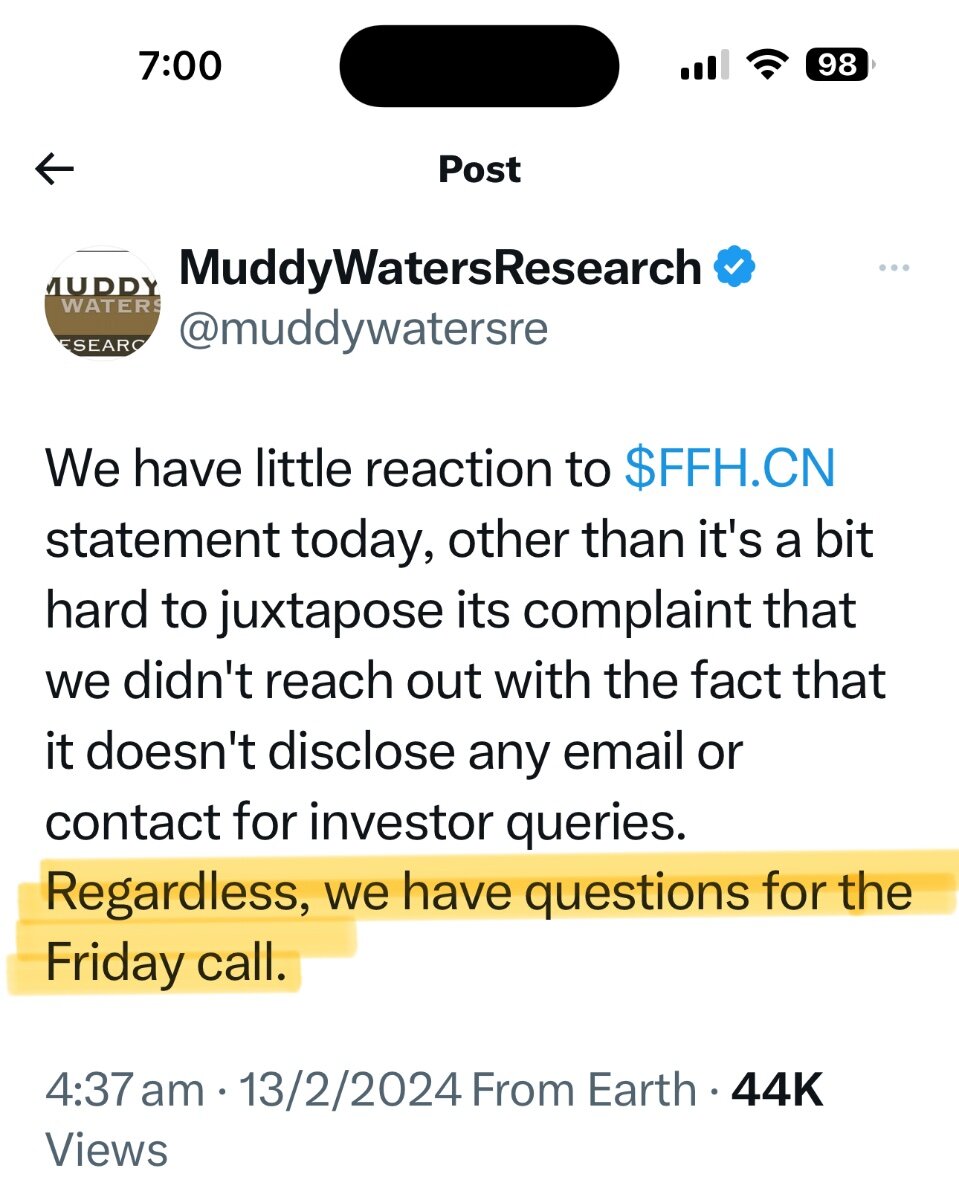

https://www.fairfax.ca/press-releases/fairfax-responds-further-to-short-seller-report/ To the best of our knowledge, Muddy Waters has never attended our conference calls and neverasked a question, called us or written to us, but instead went to CNBC during our quiet period with these one-sided, ill-informed allegations and insinuations in a transparent attempt to profit by short selling our stock. They may have successfully done this with other companies, but they have woefully misjudged the strength of Fairfax’s financials and prospects and we are confident the marketplace will reflect our strong fundamentals. Prem Watsa, Chairman and CEO of Fairfax, commented: “We are neither Berkshire Hathaway, nor GE, as Muddy Waters suggests. We are Fairfax, a strong and enduring company built over 38 years, committed to integrity, customer service, employee welfare and the communities we operate in. We have a unique Fair and Friendly culture throughout our organization. We strive to provide excellent returns to shareholders, and are committed to providing full disclosure in our annual report, highlighting both our pluses and minuses.

-

Thanks @glider3834, very helpful. The Excor black box has always been a bit of enigma with price discovery being flakey via OTC. It’s obviously very dependent on the oil price in terms of short term earnings and reserves longer term. I have never really understood the cloak and dagger around obtaining financials.

-

Love them or hate them, it matters to the ratings agencies. The upgrades we saw in 2023 are at odds with the MW thesis as will be the upgrades some of us are expecting this year.

-

Typically on large caps the maintenance requirement is 30%, but you would need to confirm. They are advising you that for Fairfax they are now only willing to do 50% if it is a “concentrated position”. The key questions are 1. What is the normal margin requirement for IB? Typically this varies by market cap. 2. What constitutes a concentrated position? It is very poorly worded.

-

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

I have always found musical discovery so much better on Spotify than Apple Music. However for those that like melodic house and electronic I rate this playlist updated weekly from Apple. This week’s set has some crackers. Probably showing my age but some great Ambient House vibes. THE UNDERGROUND If your idea of an amazing night out is a black-box room with sweaty walls, one light bulb, a banging system and a sign on the door that reads “no phones or photography allowed,” then this set is for you. Indulge in an open-minded mix of avant-garde house, techno and other forms of dance music that fall comfortably, intoxicatingly left of centre. We update this playlist every week. If you like a track, add it to your library Link

-

@Luca that's interesting. Rather than fill up this thread would you mind pm’ing me the full text, I wouldn’t mind reading it in its entirety

-

It's always possible that MW is on a fishing expedition, and this was the initial burley to see if they can land something more substantial via a whistleblower. I put this at 1%. After listening to both interviews, Block's knowledge of the company seemed cursory. In all honesty, it was almost like he scrolled through some of the conversations here from a few years ago, and that was where he stopped. Later discussions are obviously not overly accretive to his thesis. Looking forward to the results next week....oh, and Carson's detailed questions at the Q&A

-

Good commentary, a little light on the Div though

-

FRFHF

-

This is partly why the board was scratching it's collective head yesterday. My gut feeling is that MW has been “researching” for a while and knew their thesis was about to get run over by two freight trains - Fairfax equity positions and earnings. They dropped the report to get at least some return on their efforts.

-

The Q&A portion of the CC next Friday will be fascinating. Hardly make or break but if they do a good job of addressing these “issues”, then MW may have done us all a huge favour. I would see it as a great opportunity for some of the other members of the Fairfax C-Suite to shine. Some straight shooting and plain speaking would do wonders.

-

This! I have been pondering the “research” over multiple coffees and came to the conclusion this board pulled together a better short thesis in 2021. The very same board then blew it up as the facts changed dramatically. Muddy Waters has brought a lemon to a knife fight but is 3-4 years late. When I saw that a short report was out and the market reaction, I figured we were having an “asbestos moment’ in the insurance subs. It turned out to be nickel and diming some selective marks while totally ignoring others to suit the narrative. The nonsense about the 15% aspirational target, well that is getting solved as we speak. Talk about a storm in a teacup.

-

Ta, seeing the table from the quarterly reminded me that Eurobank is a 2.5 bn position today vs carrying of $1.8bn. Crickets on that one!

-

Thanks @KFS So after all the hyperbole the upshot is book value needs a 20% haircut, CAGR has only been 9% and Prem isn’t Buffet. That is a pretty weak short thesis. It's fascinating to see this guy floundering around. The only piece of the puzzle that he kind of gets right is the Omers debt dressed as equity. That has been done to death on this board. This financing cost is more than worth it to buyback shares at $US500 when they should do $150+ in earnings for a few years running.