nwoodman

-

Posts

1,892 -

Joined

-

Last visited

-

Days Won

15

Content Type

Profiles

Forums

Events

Everything posted by nwoodman

-

It seems strange to me that Fairfax groups bond returns and equity returns together to create an average return on “investments’. I think this actually does their investment framework a disservice. I am sure HWIC are acutely aware that the only returns that matter are real returns and that guides a lot of their investment positioning. Might be a fun job on a rainy day to back out inflation and to get their “real return on investments” which is likely more telling of their investment prowess. Their bond positioning this time around has been fantastic, some of the best in the business for my money. Capital allocation going forwards, is why/was the discount applied. A full re-rating will occur if they can demonstrate to the market that they are re-investing this windfall in quality assets.

-

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

New puppy day in our house. We named him Louis. Obviously started our listening this evening with this one…..indeed it is. Looking forward to laughing off every chewed cable, shoe etc for the next year or so, but a small price to pay -

0669.HK Techtronic Industries. Love Milwaukee tools but the shorts may be more right than wrong on this one. Proceeds go to JPY margin.

-

Brilliant, many thanks

-

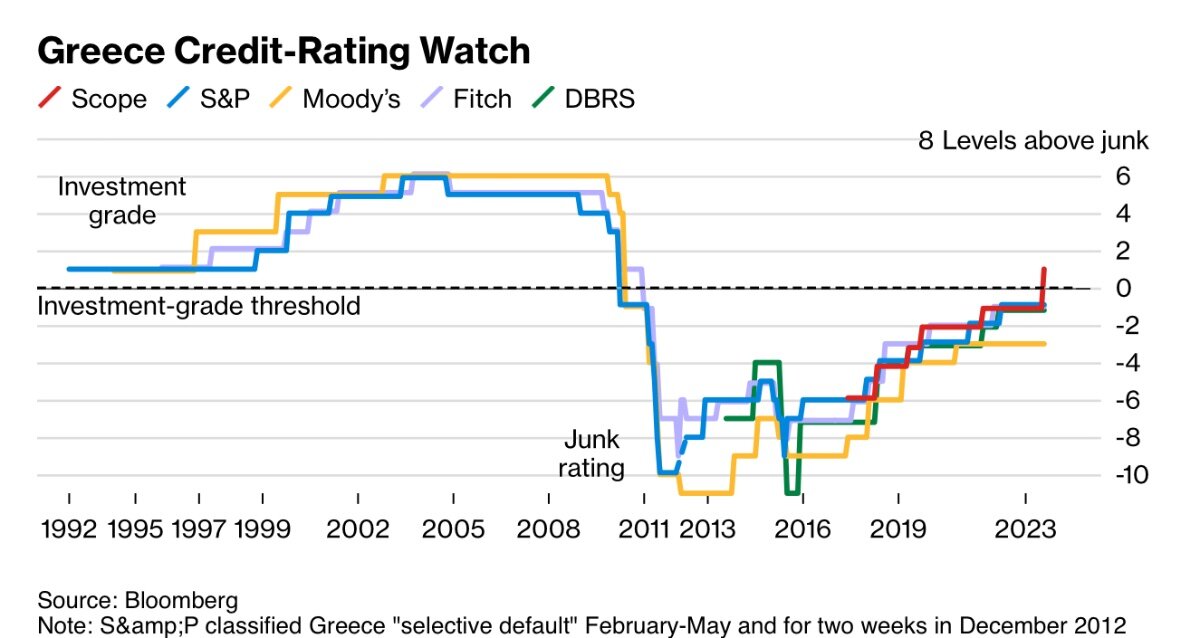

Recent interview with Dennis Shen, lead analyst for Greece, after Scope Ratings’ (European Ratings Agency) upgrade of Greece to an investment-grade (IG) rating of BBB-. Quite the feat. In terms of risks moving forwards this response was interesting: DS: Greece’s ratings are constrained at BBB- by several meaningful credit challenges. The elevated level of government debt remains a core challenge. High debt exposes Greece to ongoing risk whenever there is a pivot of market sentiment towards questioning the debt sustainability of the euro area’s more-indebted sovereign borrowers. Further reducing this debt could make Greece more resilient. Furthermore, policy risks prevail as Greece transitions from dependence on conditional official-sector credit towards favouring less-conditional market-based funding. Thirdly, the banks and external sector display fragilities. Another challenge is modest long-run potential growth of around 1%. Environmental challenges are relevant here as climate risk curtails long-run growth if heatwaves and wildfires damage Greece’s crucial tourism and agriculture sectors. A Bank of Greece-commissioned analysis from 2011 concluded climate change may cost the Greek economy anywhere from EUR 577bn to EUR 701bn by 2100. That is three times the size of the Greek economy today. Climate risk represents a meaningful long-run risk relevant for Greece’s ratings as the most exposed economy of the European Union. https://www.fxempire.com/news/article/greece-qa-investment-grade-is-an-exceptional-achievement-but-multiple-challenges-remain-1368772 Link to Scopes upgrade note https://www.scopegroup.com/ScopeGroupApi/api/analysis?id=097c203b-4b26-4fed-8117-b2086e3afdda Bloomberg coverage https://www.bloomberg.com/news/articles/2023-08-07/greece-and-its-banks-are-one-step-closer-to-wider-investor-pool?utm_campaign=socialflow-organic&cmpid%3D=socialflow-twitter-economics&utm_content=economics&utm_medium=social&utm_source=twitter#xj4y7vzkg

-

A recent interview with MS emerging market analyst Marshall Stocker on why Greece is their top holding https://www.cnbc.com/video/2023/08/15/morgan-stanley-says-greece-is-its-top-holding-in-its-em-fund.html

-

Greece continues to power ahead. Hard to believe it is the shining light of Europe, but there you have it. “Optimism about manufacturing’s prospect in the index of purchasing managers (PMI) reached 53.5 in July.” “By contrast, the PMI in the 20 eurozone countries averaged 42.7, its lowest level since May 2020, at the height of the pandemic lockdown. In Austria and Germany, for example, July PMI stood at 38.8 and was underwater in France 45.1 and Ireland 47.0.” https://www.ekathimerini.com/economy/1217515/greek-industrial-production-expands-prospects-are-deemed-good/#

-

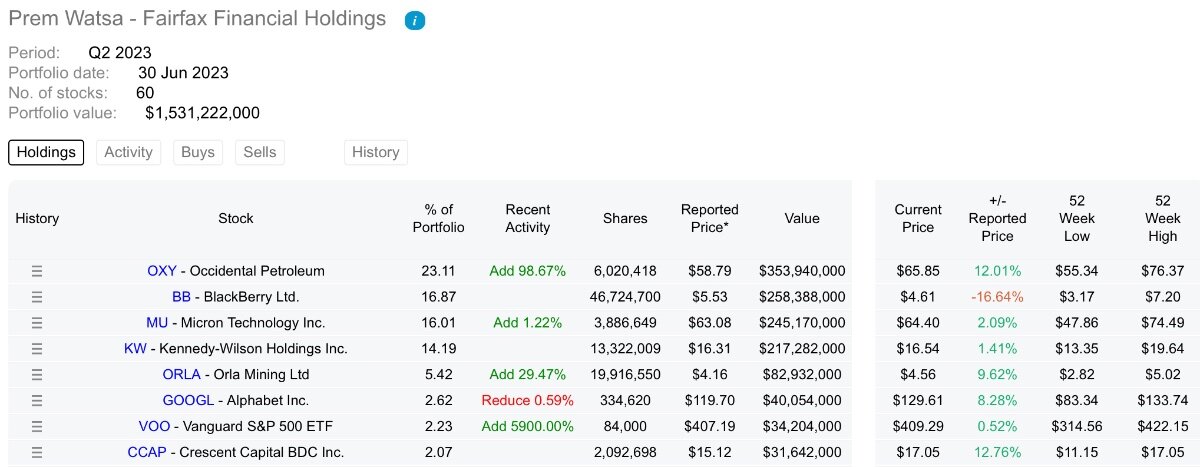

That’s a big weighting to OXY. Don’t disapprove, as I was kind of kicking myself I didn’t buy some in the mid 50’s. However, I do prefer these type of positions in my long term compounders. The index position is a head scratcher at these levels though. It’s funny, a lot of people have bagged Gaynor at MKL for his myriad of holdings and argued why not just have an ETF position. FFH seem to think so. All appears more rump, less tail albeit with a slight inflationary bias and in the case of OXY leveraging the implied BRK put.

-

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

Died Pretty - Doughboy Hollow - one of my favourite albums of the 90’s. RIP Ron Peno, who passed away yesterday after a brave fight with the big C.

-

Thanks doesn't quite do it justice, but thanks anyway

-

It is a bit of an island, I agree. On a more nostalgic note, it was only a few years ago that we were all talking about coiled springs. It kind of feels like the entire mattress is exploding. I just had to get that crap analogy out of my system; apologies for making you the recipient.

-

Anyone watching Thomas Cook. I know the Indian markets are on fire but THOMASCOOK.BO is up around 8% today and 35% since June 30 when it was around a $300M position. Even after this run it is around 60% off it's 2018 highs. Another position to add to the regression to the mean list.

-

Trimmed some more AAPL AND BRK.B and reduced USD margin

-

Greatly appreciated

-

Won’t hold you to it but do you think it is fixed? At least this will give me cause to do my own DD.

-

Coming from the slowest, I take it to mean 1029/834=1.23x’s book would be the maximum price paid. This would still be very accretive to shareholders for a compounder of 12%+ and in line with their intended aim of 15%. I think the 18% reference is more an ‘as evidenced by our long term record” Edit: just listening to the CC replay now and I am pretty sure Prem said if we were to buy back at 1375 by “year end” we would be doing our shareholders a favour, so perhaps 1.15 is more appropriate. Average 1.2x’s A very enlightening comment nonetheless

-

That’s brilliant. Not dissimilar to what many here think is close to a minimum FV at the moment. Roughly 10x’s what they think minimum earnings will be too.

-

There appears to be some mismatch, hence the earnings cratering this quarter. It is basically the amount they missed estimates by, so it appears to be somewhat of a minor surprise in an otherwise good report. Management is saying it is temporary. I would defer to them. It would be interesting to learn more via the CC as the individual P&L’s aren’t readily available so it is a bit of a black box. The question was how much of the excess of fair value could we add to book. If you assume nothing the answer is still OK.

-

Very true. It sounds like they might be doing a bit of a Wile E Coyote with the hedges having saved them for a while. Just as long as Poseidon doesn’t become a mill stone in an otherwise compelling story. With so many positive developments it kind of gets lost in the noise for the moment.

-

Best to stay reasonably conservative. Who really knows what Poseidon is worth as a highly leveraged capital-intensive business in a world with more normal interest rates. Given their massive drop in earnings, a $400 million haircut over "fair value" doesn't sound too outrageous to me. Q1 23 $50.1m vs $49.7 Q1 22 Q2 23 $6.3m vs $72m Q2 22 Q3 $58m Q3 22 Q4 $78m Q4 22 Total $258 FY 22 The earnings release had this to say "Share of profit of Poseidon (formerly Atlas) decreased to $6.3 million from $72.0 million due to higher interest expense, interest rate hedging losses (compared to hedging gains in the prior year) that fluctuate quarterly, and transaction costs related to the first quarter privatization of Poseidon. The company expects Poseidon’s earnings will normalize throughout the year." Hopefully, this gets discussed in the CC.

-

Haven’t they given up some of this optionality, at least for this year, with the 6 month US Treasury bond forward contracts they entered into last quarter or does that show up in the bond losses for this quarter? It was only $3bn then and $2.5bn now so maybe it isn’t all that material on a $33bn bond portfolio.

-

Solid results, the marks on bonds hurt but that is the time we live in. Most impressive was the CR, I thought it would be edging up more as they are grew their book. Poseidon is getting whacked but promising to hear that things are likely to stabilise from here. All seems to be tracking in the right direction and certainly justifies the run up in share price. The true earnings potential hasn’t been realised yet.

-

Give it time, the "market" has been a bit slow to catch on. Totally agree with an earlier post, more than happy for it to compound at double digits for the next decade and always trade at book. Berkshire and Markel P/B's make my fingers itchy.

-

Which activities in life brings you the most fun?

nwoodman replied to Charlie's topic in General Discussion

Stunning! Is this part of the John Muir Trail? Doubt I will ever get time or permission to do one of the big triple crown hikes (AT, PCT, CDT), but the JMT is at the top of my hiking bucket list. -

Which activities in life brings you the most fun?

nwoodman replied to Charlie's topic in General Discussion

Nice hang