nwoodman

-

Posts

1,892 -

Joined

-

Last visited

-

Days Won

15

Content Type

Profiles

Forums

Events

Everything posted by nwoodman

-

Trim to MKL-> USD Margin

-

Trims to KMX, AAPL, MU and BRK.B. Proceeds used to pay down USD margin

-

Update on this via the Economic Times: SAT stays Sebi order against IIFL Securities till further notice; stock surges 6% https://economictimes.indiatimes.com/markets/stocks/news/sat-stays-sebi-order-against-iifl-securities-till-further-notice-stock-surges-6/articleshow/101300444.cms MUMBAI - In an interim relief to IIFL Securities, the Securities Appellate Tribunal (SAT) on Tuesday stayed the order passed by the Securities and Exchange Board of India (Sebi) against the brokerage, barring it from onboarding any new clients for two years. The stay order bolstered the shares, which surged more than 6% to the day’s high of Rs 65.90.

-

Thanks for the link to the filings. Even after the runup, they look far from expensive.

-

Same, I might be wildly optimistic but they could be in the process of shaking up multiple industries…again. If not, then I don’t think you lose to much, as even the existing moat is massive. Every time I think about selling, the Phil Fischer in me asks which particular Apple device are you going to use to place the sell order from?

-

Good news June 19, 2023 02:00 AM Eastern Daylight Time OMAHA, Neb.--(BUSINESS WIRE)--(BRK.A; BRK.B) – Following the close of the markets in Japan today, Berkshire Hathaway’s wholly-owned subsidiary, National Indemnity Company, will notify Japan’s Kanto Local Finance Bureau that it has increased its ownership interest in five of the leading Japanese trading companies. The companies, listed alphabetically, are Itochu, Marubeni, Mitsubishi, Mitsui and Sumitomo. Presently these are the only publicly traded investments that Berkshire owns in Japan. Their aggregate value considerably exceeds that of Berkshire-held public stocks in any other country outside of the United States. Excluding shares of treasury stock, Berkshire Hathaway’s ownership interest in each of the five companies now averages more than 8½%. This reporting of ownership interest is consistent with how Berkshire Hathaway reports its ownership interest in U.S. based publicly traded companies. https://www.businesswire.com/news/home/20230618253567/en/

-

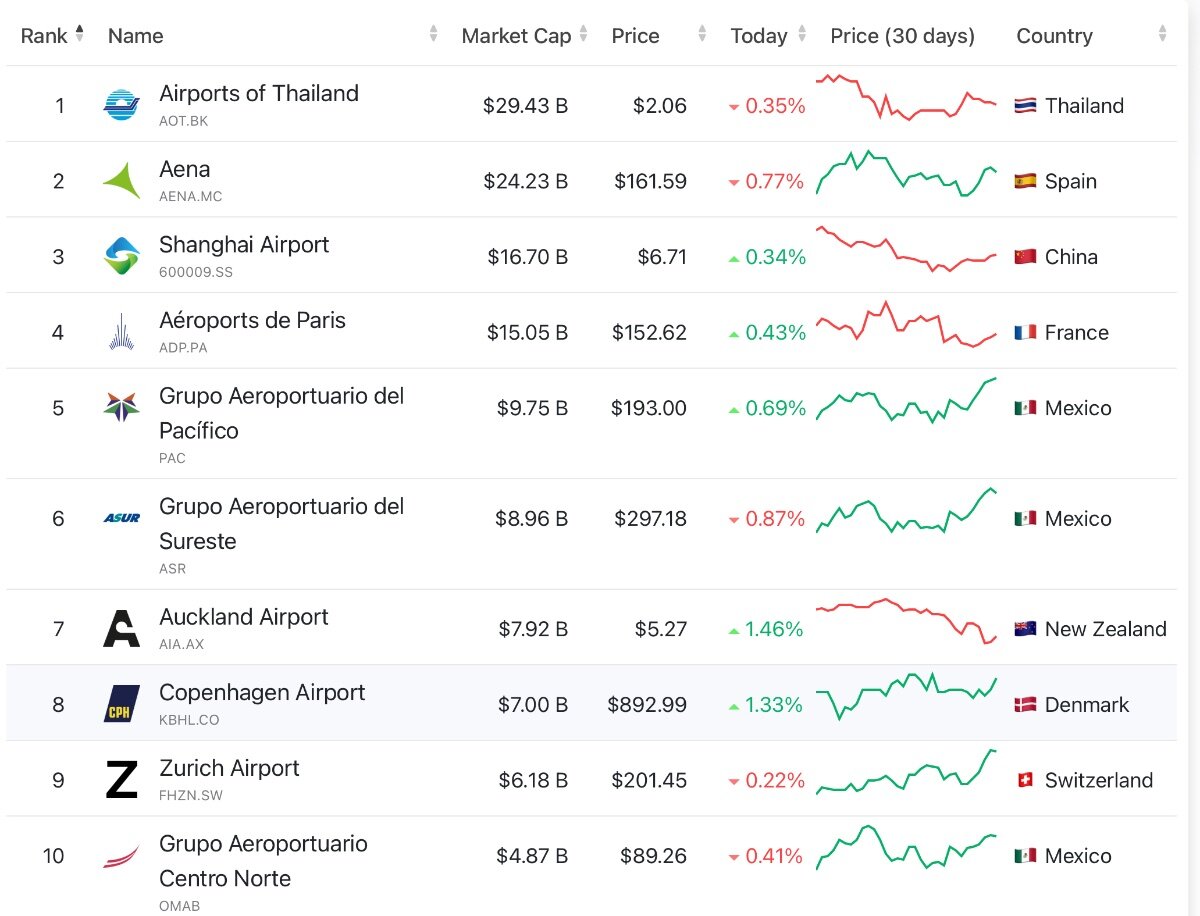

Not too difficult at all to make the case the Kempegowda Airport is mispriced. The recent small interest stakes valued the airport at $2.5 bn (Prem uses $3bn) Not sure about 6-7x’s in a decade ($20bn) but easy to see a “runway” to $10 bn or so by 2030. A remarkable investment. https://companiesmarketcap.com/airports/largest-airport-operating-companies-by-market-cap/

-

Thanks for the link. The final line was gold “While adding Fairfax in would have made their story even stronger, we can’t blame them as we’re sure they only included the Canadian insurance companies they could remember.”

-

Looks like Digit’s Life Insurance venture isn’t wasting anytime and will be releasing their first product in less than 30 days. You have to take a deep breath, but the opportunities here are pretty staggering IMHO. With the IRDAI potentially green lighting investing a portion of their life insurance float back into infrastructure. This could be one of those formative moments we look back on in 10 years time. The hoops they must have jumped through to get this license is testimony to the brands of both Fairfax and Kamesh Goyal. From the Economic Times: “Go Digit Life Insurance, in which both HDFC Bank and Axis Bank have bought stakes, plans to invest ₹500-600 crore (USD61m-73m)crore in the initial 18 months to start out as the country's 26th life insurer. Promoted by Prem Watsa's Fairfax and industry veteran Kamesh Goyal, the company aims to launch its first product within 30 days. "A large part of the ₹600 crore will be invested into tech and the company will focus on the protection line of business," said a source. The entry of Go Digit increases the number of insurers operating in the life insurance space, marking the first expansion since 2011. Apart from Fairfax and Goyal, HDFC Bank and Axis Bank have each acquired a 9.9% stake in the company. Go Digit received R3 certification of registration on Friday after obtaining R1 and R2 licenses. During this stage, the regulator scrutinises the financial condition of the promoters, foreign investors, and the management's general character. The regulator also evaluates the company's business plan, the expected volume of business, capital structure, and earning prospects. Srinivasan Parthasarathy, formerly the chief actuary of HDFC Life, has been appointed as the CEO, while Sanjay Vij, who previously led bancassurance in HDFC Life, is appointed as the deputy CEO. India's life insurance sector comprises a total of 25 companies, among which the Life Insurance Corporation of India (LIC) holds the dominant market share”

-

Excellent news. Digit has become the 26th Life Insurer in India https://irdai.gov.in/document-detail?documentId=3491346

-

Awesome, but even more awesome that you are like a blood hound on the scent. Thanks for posting as the IRDAI figures have not been updated in a while

-

Carmax (KMX) - Couch change purchase

-

This has also crossed my mind more than once. Very low probability but not zero, although the ties to DIS would make it a bit awkward unless there is implicit blessing.

-

“In addition to the Transaction, Fairfax also agreed to make a $200 million preferred equity investment in Kennedy Wilson. Under the terms of the agreement relating to the investment, Fairfax will acquire perpetual preferred stock that carries a 6.0% annual dividend rate and is callable by Kennedy Wilson at any time. Additionally, Fairfax acquired 7-year warrants for approximately 12.3 million common shares with an initial strike price of $16.21 per share, based on Kennedy Wilson’s closing price on June 2, 2023. The investment is subject to customary closing conditions and is expected to close during the second quarter of 2023.” Rather Buffett like. Shares out on KW currently stand at 137.2m, so they stand to pick up 12.3/(137.2+12.3)=8% at what could prove to be a very respectable strike price in a few years along with getting paid to wait with the prefs. They own around 9% now. The press release is now on their website https://www.fairfax.ca/news/press-releases/press-release-details/2023/Fairfax-Financial-Partners-With-Kennedy-Wilson-to-Acquire-Loan-Portfolio-From-Pacific-Western-Bank-Makes-Additional-Equity-Investment-in-Kennedy-Wilson/default.aspx

-

Kennedy Wilson 8K Filing The Company has entered into an agreement with Fairfax Financial Holdings Limited, a Canadian corporation, (collectively, with certain of its subsidiaries and affiliates, “Fairfax,” and together with KW, the “KW/FF Purchasers”) to together purchase 63 of the Initial Loans. The purchase price for such 63 Initial Loans and the Additional Loans (as described below) (collectively, the "KW/FF Loans") is a total of approximately $2.1 billion, subject to customary prorations and adjustments, and (i) will be paid to PacWest to acquire a total of approximately $2.3 billion in aggregate principal balance that is currently outstanding under the KW/FF Loans; and (ii) is the price for the entire portfolio of KW/FF Loans and may not necessarily be reflective of the price paid for any individual loan. The aggregate principal balance of the KW/FF Loans, which are floating rate, currently carries an average interest rate of approximately 8.6% and more than 70% of the KW/FF Loans are secured by multifamily or student housing development projects with the balance being a mix of industrial, hotel and life science office property development projects. https://otp.investis.com/clients/us/kennedy_wilson1/SEC/sec-show.aspx?Type=html&FilingId=16708374&CIK=0001408100&Index=10000

-

Nintendo 7974.T. Close to fully priced but their execution is blowing me away. Totally irrational but it has similar vibes to me as buying Apple in 2014.

-

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

Amyl and the Sniffers (based in Melbourne, Australia). Saw them as a support act for The Smashing Pumpkins. Amy blew me away, she epitomises why live music is so compelling. Energy levels through the roof. In this age of auto tune it so refreshing to have some punk vibes again . Another favourite at the moment is Fontaines DC (Dublin, Ireland) for similar reasons. -

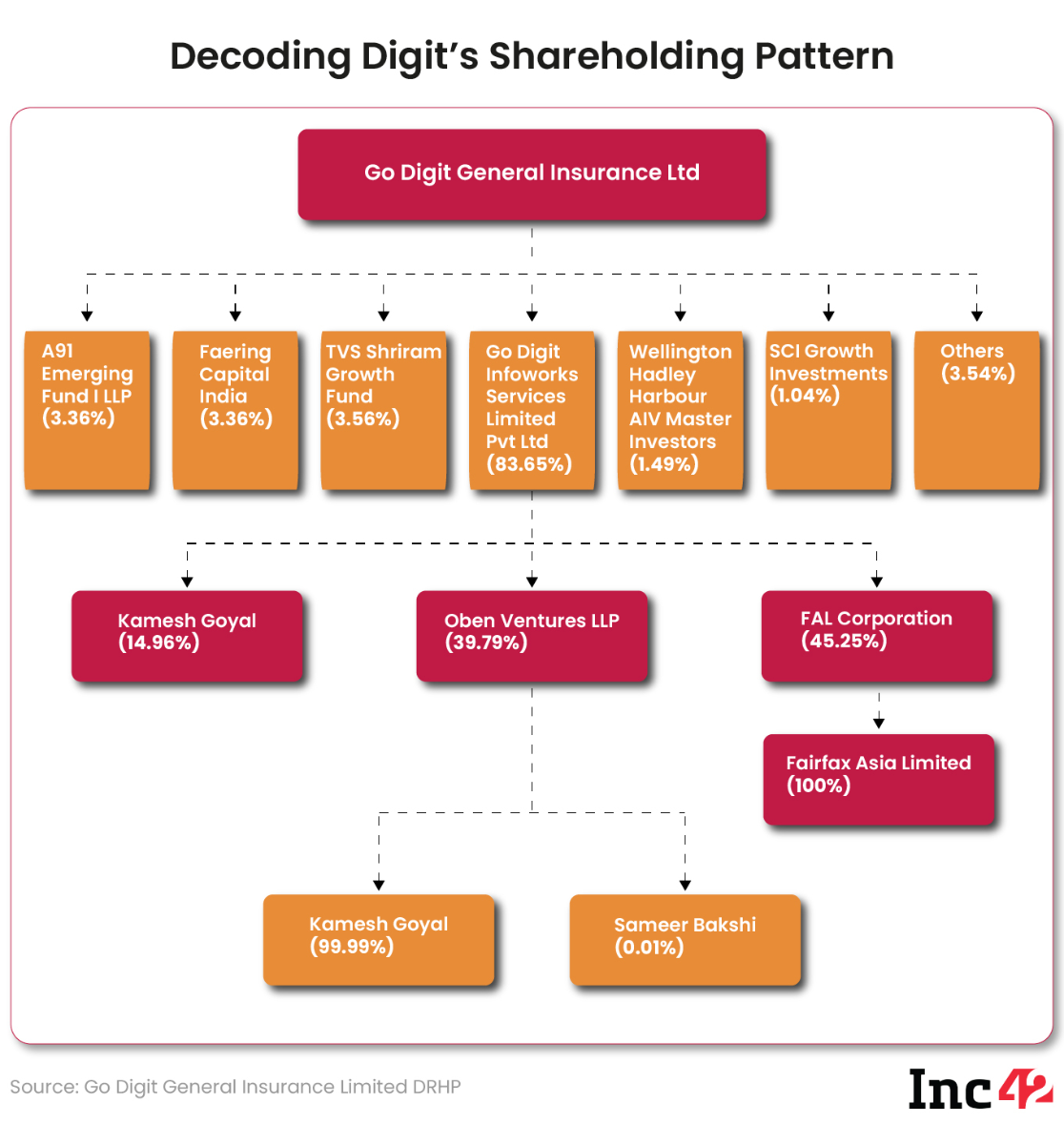

A recent article on Digit's entry into the life insurance sector. The article provides some color on the split between Fairfax and Kamesh Goyal in the new entity. Go Digit may enter life insurance in 6 months https://www.livemint.com/companies/news/go-digit-may-enter-life-insurance-in-6-months-11685640600722.html Fairfax Financial Holdings Ltd-backed Go Digit, led by Canadian billionaire Prem Watsa, is poised to enter India’s insurance market with the launch of a life insurance company in the next six months, two people familiar with the plans said. Go Digit will be the 25th firm in India’s insurance sector, which clocked new business premium of ₹3.7 trillion ($US45bn) in 2022-23. Currently, Watsa’s Fairfax, in a tie up with insurance industry veteran Kamesh Goyal, holds ownership of Go Digit General Insurance Ltd, a general insurance company. “The new life insurance joint venture being planned may have Fairfax holding a 40% stake in the firm initially," one of the two people said seeking anonymity. According to the two people, the proposed firm is likely to be named Go Digit Life Insurance Ltd, and will offer a range of life insurance policies. They said the company will have an initial capital of ₹700-1,000 crore ($US 85m-$120m) . Go Digit Infoworks Services Pvt. Ltd, the holding company, is expected to hold 80% as the primary promoter of the proposed JV. Additionally, Goyal and Oben Ventures LLP may collectively hold 40%, mirroring Fairfax’s stake in the company, the first person said. “The balance 20% could be held by banks as non-promoter strategic partners," he added. In response to a query, a spokesperson for Go Digit said: “Go Digit Life Insurance has submitted an application to the Irdai (Insurance Regulatory and Development Authority of India) to conduct life insurance operations in India. As the application is under consideration by the Irdai, we are unable to comment on matters pertaining to the regulatory approval status, proposed partnerships, or the shareholding structure of the company." “Following the launch, the company may place minority stakes with certain banks to strengthen its bancassurance network. This may lead to a proportionate reduction in stakes held by the partners, including Fairfax," he added. Fairfax has been looking to ramp up its investments in India over the past few months. India-born Watsa, while speaking in the India@75 virtual summit had said Fairfax Financial Holdings has invested $7 billion in India and will double it in the next 4-5 years. Fairfax Financial Holdings’ managed assets worth $81.2 billion for the quarter ended March, down 8.37% from a year earlier. The Toronto-based firm owns Fairfax India, whose investments are managed by Hamblin Watsa Investment Counsel Ltd and Fairbridge. Apart from Digit Insurance, Fairfax’s investments in India include Bengaluru International Airport, IIFL companies, National Stock Exchange, Sanmar, Fairchem Organics, Catholic Syrian Bank and Thomas Cook India. Prior to backing Digit Insurance as co-promoter, in 2019, Fairfax had sold its entire stake in ICICI Lombard General Insurance Co. Ltd for ₹2,626.5 crore, ending its 18 -year partnership as an investor. Go Digit Infoworks Services or Digit Insurance is the only startup bet so far by the Canadian investment behemoth in India. The startup, founded by Goyal, was the first unicorn of 2021, a year that saw an entrepreneurial boom with 44 new unicorns. FAL Corp. owns 45.3% in the holding company, Go Digit Infoworks Services Pvt. Ltd, which in turn owns a 83.47% stake in Go Digit General Insurance. On the other hand, Goyal and Oben Ventures LLP together hold 14.96% and 39.79% in Go Digit Infoworks Services. As per regulatory filings, Digit Insurance’s valuation tripled to $3.5 billion after it raised $200 million in July 2021. And now, the company is looking to list its shares on stock exchanges via an IPO. “The life insurance JV by Fairfax and Goyal may see an equally rapid growth, given the increased demand for insurance in India, post the (Covid-19) pandemic," said the first person. SBI Life Insurance is the largest private life insurer at present with a new business premium collection of ₹29,587.6 crore ($US3.6bn) in FY2023. State-run Life Insurance Corp. of India (LIC) is the country’s largest life insurer with a first year premium of ₹2.32 trillion ($USD 27.8 bn) and a market share of 62.58%. Watsa and Goyal’s proposed JV will be entering the business of life insurance at a time when the industry is faced with a new challenge with regards to growth due to changes in taxation rules, especially for the affluent mass. As per the new rules, the proceeds from any life insurance premium over an annual premium of ₹5 lakh ($US6,000) would be taxable from with effect from FY2024 that began on 1 April. However, according to the two persons, initially, Fairfax’s proposed Indian life insurance firm will primarily design small-to-medium ticket size policies, targeting the vast untapped mass of the world’s most populous country. And to do this, Go Digit’s life insurance company is looking to enter into distribution agreements with multiple Indian banks, according to the two persons. To be sure, Go Digit has already roped in private lenders Axis Bank Ltd. and HDFC Bank Ltd. as strategic bancassurance partners with a 9.8% stake each in lieu of an investment commitment of around ₹70 crore ($US8.5m).by each in the proposed privately-held life JV. As a reminder, this is the structure for Digit Insurance https://inc42.com/buzz/founder-kamesh-goyal-owns-over-45-stake-in-digit-insurance/

-

Thanks for this. I was just taking another look at the company, MYTIL.AT, impressive. While relatively small position (for now) compared with EUROB.AT. It has been a cracker for Fairfax. The market is taking quite a "shine" to Mytilineous, +80% or so over the last 12 months. I found this recent interview quite informative https://www.strategy-business.com/article/Powering-the-net-zero-transition-at-Greeces-Mytilineos

-

I can guarantee you Fairfax’s growth, as a company, is independent of Brett Horn’s comments

-

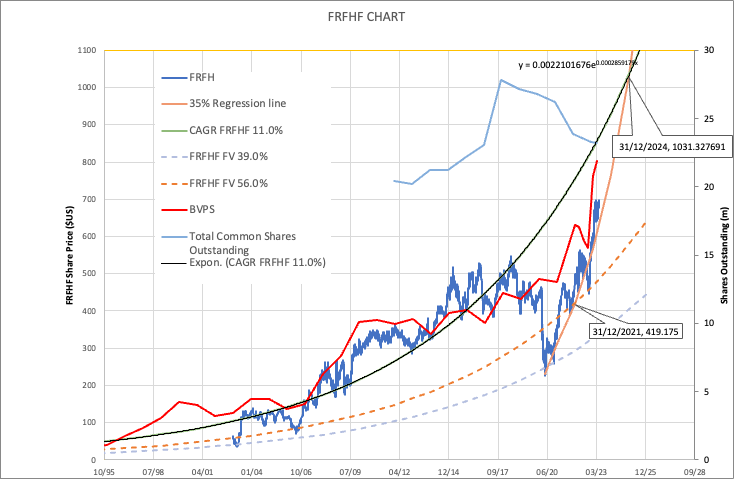

Thanks for that. Morningstar's Brett Horn also posted an update on the 19th of May that I think sums up where a lot of analysts are at. Full note attached but some key quotes below: "While its primary business is insurance, Fairfax is in some ways more of an investment fund. Chairman and CEO Prem Watsa has a long history of bold investment bets and has shown a willingness to be unorthodox when it comes to portfolio construction. As a result, compared with other insurers, the company's results tend to be driven more by results on the investment side. We're somewhat skeptical of this approach, as we believe disciplined underwriting is a more reliable path to long-term value creation, and Fairfax's underwriting record is relatively poor." "We think investors attracted to the stock due to a belief in Watsa’s ability to produce alpha should consider his record over the past decade, which includes some big wins but also substantial losses and missed opportunities. Fairfax has seen a lot of ups and downs, but its performance has been trending toward mediocrity." "We believe that Prem Watsa’s investment philosophy, willingness to make outsize bets, and potential to generate alpha are the primary attractions for many investors. Fairfax’s name is often included in discussions about the “mini-Berkshires” that seek to distinguish themselves on the investment side, but we think this narrative is misleading. Watsa has had some dramatic successes on the investment side, with the most impactful being his gain of over $3 billion from credit default swaps and equity market hedges during the financial crisis. But he has had notable misses as well, including a sizable investment in Blackberry, and we don’t think his record could justify framing his investment skills as a structural competitive advantage. The company’s preferred metric is growth in book value per share, which has grown at a 6% CAGR over the past 10 years, a fairly mediocre result even considering the dividends Fairfax has paid." What I think is interesting is that even with the mistakes of the past, FFH has been able to compound book value at a decent rate even while paying out a non-trivial dividend. We have all argued the merits of the dividend previously, but it is what it is. When I bought back into the company in 2021, it was under the premise that management would ultimately prove that they could compound over the longer term at a rate of 11% albeit lumpy. So regression to the mean was the basic premise. Based on this crude assumption, I remember the friendly arguments on the board at the time about whether it was cheaper in 2020 or 2021. Either way, if you thought the company was a regress to the mean type play, it was possibly worth $1000 by the end of 2024. At the time this seemed a little nuts, but it now looks like book value reaching $1000 is a very high probability. I dug out the graph back then and updated key metrics but not the original estimated regression to the mean line. The 35% CAGR regression is still intact, and book value is closing in again at 11%. Importantly share count is coming down with repurchases at prices less than book. For our friendly analyst to arrive at a fair value price of only CAD790 per share assumes some pretty low growth rates and some big cat losses. However, if FFH is indeed an 11% compounder, over the longer term, then ultimately even Brett would have to capitulate and reprice Fairfax to at least 1.1x's book. FFH - Fairfax Financial Holdings Ltd Shs Subord.Vtg Analysis & Rating - XTSE | Morningstar.pdf

-

The ultimate hedge. The TRS payer typically owns the stock and is renting both the upside and downside exposure to Fairfax.

-

This recent article in the Economic Times provided a good summary of some the key initiatives of the last 9 years of Modi’s government. Key areas of reform: GST, Unified Payment Interface, Direct Benefits Transfer, Insolvency & Bankruptcy Code, Make in India Nine years of Modi government: What India witnessed & how its economy has changed This nearly a decade-long period has changed India's economy in definite ways as Modi took decision after decision that made deep, lasting impacts on the economy. With India divided sharply between the supporters and detractors of Modinomics, it may be a matter of debate how good Modi's measures have proved for the economy. But few would disagree that Modi brought an unprecedented zeal to his reformist agenda. Below are a few of his decisions that changed India's economy: The Goods and Services Tax The GST was the reform of reforms, and Modi did pull it off with great success. The taxpayer base has nearly doubled since its launch and collections too have risen. The GST collections in April rose 12% from the year earlier to an all-time monthly high of ₹1.87 lakh crore. Majority of large states have reported a 20% plus GST growth over the same period last year, indicating a broad-level growth across sectors and states. Ninety million e-way bills were generated in March 2023, 11% higher than 81 million in the preceding month. The India stack Modi is probably the first Indian prime minister to leverage technology so much for his welfare programmes. His government's Unified Payment Interface (UPI) has revolutionised India's economy by facilitating digital payments even in villages. Behind the huge digital payments infrastructure that has come up in India is India Stack, a set of open APIs and digital public goods that aim to unlock the economic potential of identity, data, and payments at population scale, such as Aadhaar, UPI, Digilocker and, more recently, CoWin Vaccination Platform. The core idea behind India Stack is to lower the cost of transactions so that 1.3 billion people get access to socially and economically important services and that those services can be delivered by the private as well as public sector. It enables private innovation on the back of public infrastructure. India Stack created a set of open protocols or standards that are implemented by the institutions concerned. The UPI has helped private sector companies to rely on business models based on digital payments. India's tech-enabled governance is now admired the world over. India has developed a world-class digital public infrastructure to support its sustainable development goals with its journey having lessons for other countries embarking on their own digital transformation, IMF has said in a working paper recently, noting that digitalization has supported formalization of India's economy and Aadhaar has helped in direct transfer of payments to beneficiaries while reducing leakages. Merchant payments on UPI are expected to reach $1 trillion by FY26, driven by a growth rate of 40% to 50%, Bain and Company has said recently in a report. Point of sales terminals are expected to double to 13 million by FY26 from around 6 million currently. Direct Benefits Transfer Direct Benefits Transfer (DBT) was another revolutionary scheme that the Modi government utilised for financial inclusion of India's masses. In the 1980s, then PM Rajiv Gandhi had said that out of every rupee sent by the Centre government, only 15 paise reaches the poor. The DBT has changed that. With the help of the JAM (Jan Dhan + Aadhar + Mobile) trinity, the Modi government achieved the feat of transferring subsidies directly to the people through their bank accounts. Direct transfer of subsidies reduces leakages and delays while bringing transparency and accountability to the process, thus saving the 85 paise that used to go missing from a rupee. Financial inclusion not only helps with disbursal of benefits but also increases India's market size and financial inclusion. India saved $27 billion in key central government schemes through DBT as it is swift and eliminates corruption, the government informed in March. On an average, over 90 lakh DBT payments are processed in India daily to send money directly into the account of eligible beneficiaries of government schemes, the government had said last year. More than Rs 24.8 lakh crore had been transferred through DBT mode from 2013 to last year. The Insolvency and Bankruptcy Code Before the Insolvency and Bankruptcy Code (IBC) came into force in 2016, companies under bankruptcy proceedings would take inordinately long time to be liquidated. Nearly half of the cases took more than ten years and 15% more than 25 years to complete. The IBC provided for a market-linked and time-bound resolution of stressed assets. The IBC made it easier for banks to recover their defaulted loans. It offered a one-step mechanism for distressed businesses to resolve insolvency in an efficient and time-bound manner. It was a necessary reform when India's PSU banks were saddled with bad loans. However, the new bankruptcy resolution process has not delivered significantly improved outcomes from older debt recovery mechanisms although it has increased overall institutional capacity. The number of cases entering legacy debt recovery channels is growing five times faster than in the IBC, but it is still the most efficient channel available, handling the biggest chunk of soured credit. The insolvency resolution process mandated by the IBC has seen lengthening delays amid rising legal challenges and a shortage of tribunal benches. According to IBBI data, the 611 bankruptcy cases resolved under the IBC until December 2022 took, on average, 482 days, barring the time excluded by the NCLT. The IBC stipulates a maximum of 270 days to resolve corporate bankruptcy. Creditors recovered Rs 2.53 lakh crore, or 30.4% of their admitted claims, in these 611 cases. To be fair, in the case of 516 companies, the realisation was 84% against the fair value worked out when they were admitted to the process. The government is seeking to change the IBC to make it more efficient. Make in India Modi's Make in India project aimed to transform India's economy which has been serviced-led traditionally. Services have contributed more than manufacturing to India's economy. The Make in India programme was boosted recently with the announcement of Performance-Linked Incentives scheme in more than a dozen manufacturing sectors especially electronics and semiconductor chips. The PLI Scheme incentivizes domestic production in strategic growth sectors where India has a comparative advantage. This includes strengthening domestic manufacturing, forming resilient supply chains, making Indian industries more competitive and boosting the export potential. The PLI Scheme is expected to boost production and employment significantly, with benefits extending to the MSME eco-system. When Modi had launched the Make in India programme in 2014, there were many nay-sayers that doubted if India could emerge as a manufacturing power. It required a trained labour force and lots of capital. Nine years later, The Make in India plan seems to be finally on track with Apple setting up its manufacturing unit in India, a potent gesture to western companies that want to diversify their manufacturing away from China. One can say that Make in India was launched well in time. In eight years of its launch, global geopolitical situations have changed in India's favour. National Logistics Policy The logistics cost in India is 13 per cent of the GDP as compared with 8 per cent in developed economies, making it difficult for Indian exports to compete globally. Together with Modi's massive drive to build roads, trains, railways, ports and bridges, a logistics policy is set to revolutionise India's trade by making goods move faster across India. Under the recently launched National Logistics Policy, infrastructure ministries including rail, highways, ports and steel, will prepare sector-specific plans to increase logistics efficiency in consultation with various stakeholders. The policy aims to reduce the cost of logistics in India to be comparable to global benchmarks by 2030; improve the Logistics Performance Index ranking; and create a data-driven decision support mechanism for an efficient logistics ecosystem. India climbed up six places in the World Bank's Logistic Performance Index 2023, as investments in soft and hard infrastructure as well as technology helped the country improve its port performance. India is now ranked 38 in the 139 countries index, up from 44 in 2018. India's target is to be among top 25 countries by 2030.

-

Congrats, that’s a decent time especially with minimal training. You must have a good base fitness level

-

With another 5 missiing A few reports coming in of stolen oxygen bottles etc. It sounds like it has been a bit of a crazy season.