nwoodman

-

Posts

1,891 -

Joined

-

Last visited

-

Days Won

15

Content Type

Profiles

Forums

Events

Everything posted by nwoodman

-

Is there a cheaper, higher quality float per share option than FFH itself? I think at the current share price they achieve both options you are considering.

-

Just a friendly reminder that you may want to reacquaint yourself with the T&Cs of attending that dinner

-

@petec, Great write up. Full disclosure: I am not an Ackman fan, so take the following with that bias noted. That said, I always appreciate your clarity of thought. Pershing committed $900 million at $100 a share, so the capital at risk is real and I do not dismiss it. But the fee architecture tells a different story. Pershing's advisory fee starts participating above a reference price of roughly $66, with a quarterly base fee on top. So while Ackman's equity may be underwater below $100, the manager can still be paid well before minorities fully benefit from a re-rating toward HHH's own internal NAV estimate of $118. The services agreement also includes a change-of-control make-whole provision approximating the present value of future fees, which speaks to how durable the arrangement is. For me, governance is not a line item in a SOTP. It is the discount rate applied to every other line item. The Berkshire comparison is where the thesis breaks for me. Buffett built the insurance operation first, proved underwriting discipline over multiple hard and soft cycles, and only then did the float become a compounding engine. HHH is attempting to invert that sequence. Vantage was founded in 2020 and the acquisition comes at the tail end of a hard market heading into a softer cycle. That is a young platform, acquired at a late point in the pricing environment, being positioned as the foundation of a compounding model. Pershing managing the Vantage portfolio without an incremental fee at the portfolio level is fair to acknowledge. But they are already being compensated under the broader services agreement, so the term "fee-free" deserves some scrutiny. Insurance compounding is not a structural outcome; it is a behavioural one. It requires patience in soft markets, a willingness to shrink, and the discipline to sit on cash. But you need the balance sheet to play that game. Everyone entering insurance believes they will underwrite with discipline, but the balance sheet is what allows you to actually maintain it through a full cycle. When the holdco above you is carrying close to $3 billion in debt and prefs, and the manager is compensated through a fee arrangement tied to market cap, the pressure to keep writing volume at inadequate prices can overwhelm intent. At Fairfax, underwriting discipline was proven over time and across cycles, and only then did float become a durable compounding engine. The stock did not re-rate because it was positioned as a compounder; it re-rated because the discipline was earned. HHH is explicitly modelling itself on what Berkshire and Fairfax built. That sets a high bar. The question is not whether the structure resembles a compounder, but whether the underlying behaviours, underwriting discipline, capital allocation patience, and governance , are actually present. The MPC assets are genuinely good. But the vehicle around them leaves me uneasy. The longer I watch this game, the wider the gap becomes between a well-designed balance sheet and what is actually defensible in insurance: underwriting culture, institutional memory, and discipline earned across cycles. That is something Ackman can aim to build over time, but it cannot be assumed or engineered upfront. As always appreciate the opportunity to think this through, and no doubt have missed some sitters in this reply

-

Tail Risk - Is It Part of Your Investment Framework?

nwoodman replied to Viking's topic in General Discussion

Great post. While I try to identify and handicap the tails, knowing what you own and margin of safety are key. I'd add one more layer: buy companies with plenty of scar tissue and management that acts rationally. Then sit tight, and make sure you still have a seat during the inevitable 50% drawdown. If you find yourself getting excited about volatility and downturns rather than fearful, that's a decent test that you own the right things. -

That would make sense, and it lines up well with @Haryana’s post identifying the new players. Jumping around a bit, this approach also looks consistent with what we’ve seen with Foran and Eldorado. Paraphrasing @Viking here, it still amazes me that many of us can join the dots on the capital recycling/allocation portion of Fairfax’s business, yet analysts continue to treat these as discrete, almost accidental, events that surely aren’t repeatable. If this investment book sat inside a private equity wrapper, I suspect the market would value it very differently (or at least would have 12 months ago ). Its arguably even more valuable now

-

Cheers, when one of the greats declares this, you have to take notice: “With the valuations of our peers implying an approximately $50 Strathcona share price, we are reminded of legendary oilman T. Boone Pickens’ line that sometimes it is “cheaper to drill for oil on the floor of the New York Stock Exchange than in the ground.” Setting aside relative valuation and focusing on absolute value, buying more of a business we know and understand well (our own) at a large discount to a reserves value predicated on WTI prices in the mid US$60s appears attractive to us. While in the past we have been unable to take advantage of the relative discount we have traded at due to our small float and low average daily trading volumes – which both limited the size of the opportunity and made a buyback self- defeating – this has improved in recent months, with Strathcona’s daily trading volumes recently averaging more than $30 million per day (up from a meager $1 to $2 million per day when we first went public). With volumes up, our shackles are now off and we have a new tool in our capital allocation tool kit. We intend to initiate our first normal course issuer bid (NCIB) in coming weeks, for up to 5% of shares outstanding. In allocating capital to the NCIB, our intent is to do so sporadically and opportunistically, rather than following a formula as a percent of free cash flow like has become popular (the best time to buy our shares will be when we have no free cash flow…). In all cases, we will seek to make repurchases when we view our stock as discounted to our intrinsic value, conservatively determined and then applying a margin of safety.” Wonderful news for SCR and FFH shareholders. The returns here if SCR can retire 5% per year at current prices or lower will bump this up FFH’s investment already impressive IRR league table. I hope Adam can make it to Toronto next month.

-

Interesting take. It strikes me ONE was the exit strategy from the start. Seaspan sits right inside the liner ecosystem and ONE was already one of the major counterparties. The consortium structure when Atlas Corp was taken private always looked like strategic operator + capital partners. FFH provides the balance sheet and stability to get the deal done, lets the business compound privately, and eventually the strategic owner consolidates. That doesn’t look like flipping assets to me, it looks more like brokering the asset into its natural long-term home while earning an appropriate return on capital along the way. The fact that many of their private positions appear to have pre-wired exit liquidity is one aspect of the Fairfax model the market seems to completely miss. A similar logic could eventually apply to Sleep Country Canada, although my sense is that if management continues to meet Fairfax’s hurdle rate they will simply keep backing them. So I think in the case of Poseidon, allowing a gradual buyout by the natural owner, only reinforces their reputation as patient capital.

-

The no sacred cows, is worth a lot IMHO

-

A quick follow-up. It has been reported overnight in multiple Turkish mainstream outlets, including Sözcü, Cumhuriyet, Yeni Akit and Medyascope, that Tom Barrack, Trump’s US Ambassador to Turkey, Special Envoy for Syria, Special Envoy for Iraq and one of the most geopolitically connected individuals in the current US administration, served as the personal reference behind Hafize Gaye Erkan’s appointment as President of Fairfax Banking & FinTech. The reporting traces a relationship that began at First Republic Bank, where Barrack is said to have championed Erkan’s advancement against internal board resistance, continued with a personal visit to her in Ankara during her tenure at the central bank, and culminated in the Fairfax introduction. On first read, that looks like a personnel footnote. It may be considerably more than that. The attached note explains why the Barrack thread may materially change the analytical frame on the Erkan appointment and what it suggests about what Fairfax is actually building. These things are easy to over-read, but ignoring them risks missing the moment entirely. Either way, it is fascinating to watch unfold and worth a few tokens to pull together a narrative that can be weighted even at 0.1%. Edit: I am sure we all love an analogy even if its on the hyperbolic side: “By hiring Hafize Gaye Erkan with the reported sponsorship of Tom Barrack, the firm has effectively installed a “geopolitical router” inside its corporate headquarters. This router connects Fairfax’s capital to: 1. The US Administration’s Inner Circle: Direct, relational access to the architects of US policy in Turkey and the Middle East. 2. Sovereign Wealth Networks: A four-decade link to the capital of the Gulf, where Fairfax already has a significant insurance footprint. 3. Regulated Banking Transitions: A peer-level relationship with sovereign banking regulators, and the institutional credibility that comes with it, at the precise moment Fairfax is attempting to close an $8 billion privatisation with the Government of India and the RBI.” Erkan - Barrack Supplementary March 2026.pdf

-

Thanks for this, burnt a few tokens with the usual vendors to generate some background notes. Pros and cons but this is where Prem and team shines, the look thru. Erkan Appointment Analysis.pdf

-

Yep, that caught my eye too. She has a fascinating back story, smart as a whip. A couple of minor red flags - early departures. However, I am 100% confident in Fairfax not pulling the trigger on a hire unless they are confident in the cultural fit. I managed to grab Peter Clarke’s ear on this last year at the AGM and it’s not just the individual it’s “their people” that may bring in that also have to be a fit. I get the feeling that that while they will preserve autonomy/decentralisation there is some real advantages to scale that they are now or soon will be, able to leverage. https://www.fairfax.ca/corporate/gaye-erkan-hafize/

-

Great podcast episode recommendation thread

nwoodman replied to Liberty's topic in General Discussion

Cheers @whiskybravo, these are “value investing” no brainers for my money. I have been fumbling around these concepts for 20-30 years. This brought it together nicely for me. You then have relatively low cost tech ($AUD100 for 10 days) available to directly measure lifestyle choices and it is enlightening to say the least. -

Great podcast episode recommendation thread

nwoodman replied to Liberty's topic in General Discussion

Perhaps slightly off topic, but I’ve found this set of videos genuinely insightful from a health perspective. They’re science-based and cut through a lot of the hysteria and noise that surrounds modern health advice, especially from "influencers". While the videos cover a wide range of topics (with some overlap and repetition), the core message is clear: many health problems are driven by chronic physiological stress rather than single “bad” habits. Dr Alex Wibberly's interest in the subject stems from repeatedly seeing the same patterns recur in real-world clinical settings. What appeals to me is the holistic way he approaches health, rather than searching for silver bullets. The advice consistently focuses on the what and why, before getting to the how. The take-home is that modern lifestyles keep us in a constant state of threat - poor sleep, irregular eating, stress, alcohol, ultra-processed food, etc. - which disrupts hormones, blood sugar regulation, recovery, and mental health. The encouraging part is that the low-hanging fruit is very simple and compounds over time (every value investor’s friend): regular sleep, real food, enough fibre, daylight, a walk after dinner, and reducing unnecessary stressors. When those basics are in place, the body often starts to regulate itself remarkably well. They may sound like motherhood statements, but the explanations are grounded, technical, and refreshingly free of hype. While not pre-diabetic, I’ve been doing a bit of personal experimentation with a CGM and was surprised by how small, mundane changes can make a big difference to blood sugar stability. It does make you reflect on how much of the “health industry” is focused on managing symptoms rather than encouraging a handful of simple, low-cost behavioural changes. The comments are also worth reading; they’re mostly thoughtful and measured. I also like the headline banner on his YouTube splash page: "How not to die" -

Good point. I should have clarified the above note. Using Book +%float, SOTP, DCF etc I get large numbers. The only time the valuation looks remotely FV is when I use legacy multiples based on stated book (anchoring). A fully blown soft market would bring valuations in line but a softish market still doesn’t justify the current price, let alone what it was trading at a few weeks ago. I guess a 30% “conglomerate discount” get’s you there too. It’s a weird one, but in a good way.

-

Or a lot of money gets left on the table. Trading a 65c dollar up to a 70c dollar has limited appeal, but I understand everyone’s situation is different. Guess it depends on one’s view of IV. I get the margin of safety arguments etc, we are all wired that way. I just think the historical handicapping of Fairfax at these multiples is just plain wrong. I do bottom ups continuously on the holdings and in turn the company and end up with numbers far higher than the analysts. Happy to be proven wrong but ironically it’s not a risk I am willing to take. Just my 2c.

-

Fair enough, my mental model of a “deep value” index fund with float leverage is no doubt wrong but I have always felt that there is more diversification here than most give credit.

-

Threw a few more on the pile myself. Currently 10%+ earnings yield on the lower end next years estimates, which I think are conservative. These corrections are a thing of joy and appear quite mechanical/algo driven especially with earnings next week and given we are close to the end of Hurricane season. Hopefully they are making full use of the NCIB and buying handing over fist.

-

I believe Oaktree/Brookfield are still in the running. Reputation will likely feature prominently in considerations. Fairfax via CSB and that whole patient capital thing may have an edge. If it comes to pass, then it will still be a decent chunk of capital but the fact that this has been on a go slow, probably suits Fairfax at the moment. Price is everything but there is an elegance in having a really big idea waiting at the end of a hard market that could potentially move the needle over the next decade. That’s the sort of Fairfax optionality that is not lost on this forum but the market still doesn’t get.

-

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

RIP Ace Frehley of KISS. I will always have a soft spot for the band, as the addition of the LP “Kiss Unmasked” doubled my record collection. https://www.rollingstone.com/music/music-news/kiss-guitarist-ace-frehley-dead-1235448770/ -

While smaller in quantum, I really like the call option Fairfax picked up on the Cyprus P&C subsidiary (ERB Asfalistiki). They’ve taken a 45% stake today for €59 million and, importantly, have the right to acquire the remaining 55% over time. That gives them a low-cost seat at the table in a growing regional franchise while freeing most of the Eurolife-Life proceeds for buybacks or redeployment elsewhere. This is part of their evolution too: realise mature value, keep some upside, and create embedded optionality. If the Cyprus business compounds well, they can step in for control; if not, they’ve risk-capped the exposure. They probably have more of these calls out there than at any time I can remember. Even if they are only 10-12% IRR ideas, they can pick them off at their choosing. So, even if they suffer from dislocated markets (or a high FFH share price), they have ideas that they can reach for that will make sense.

-

That’s gold . I don’t quite follow why some people discuss Fairfax’s bond book in isolation rather than looking at capital allocation holistically, within regulatory constraints. It’s been mentioned before that the decision to extend duration came from one of their equity people, not a siloed bond manager. Fairfax’s specialists aren’t operating independently, there are a lot of IQ points allocated to capital allocation, regardless of the instrument. If you think of some of their equity positions as permanent holdings (until fully valued), then the true economic duration of the portfolio is far longer than what you’d calculate just from their U.S. Treasuries. The current bond book provides flexibility and optionality, not a statement of risk appetite. Management has said repeatedly that Treasuries are the default parking spot while waiting for a meaningful credit dislocation. They’d prefer to own corporate credit, but only at the right spread. The beauty of Fairfax is that they’ll still take directional bets when they make sense, without being dogmatic about whether the idea is “macro” or “micro.” What’s changed over the past 15 years is how they execute, far less hubris, far more calibration. As has already been discussed, it’s now a far better capital-allocation machine these days. Even when if underlying thematics drive the positioning, there’s a clear emphasis on backing exceptional operators in each chosen space. If you want duration matching, there is plenty of of that available elsewhere, but don’t expect the sort of lumpy outperformance you get with Fairfax.

-

I think that’s the right take — the Eurolife “other structures” reference points mainly to Fairfax’s indirect exposure to Eurolife Life via its ~33 % Eurobank stake, plus its direct holdings in the remaining Eurolife P&C operations and the new 45 % interest in ERB Asfalistiki (Cyprus P&C). As for the current adjusted book value, does anyone hazard a guess? I’m getting roughly US $1,400 per share, which lines up with the incremental pieces since Q2: fair-value surplus on associates, Eurobank’s move to €3.66, the Eurolife gain, and Q3 earnings plus a month of Q4 run-rate. At the current US $1,738 share price, that’s about 1.25–1.26× adjusted book — roughly 75–80¢ on the dollar. It also supports the running thesis that management views buybacks below 1.3× (adjusted book value) as comfortably accretive, implying a nominal 12%+ IRR unlevered. They benefit from float leverage, so without labouring the maths, it meets their hurdle. Hardly an exact science on my part - and they likely have visibility into more embedded value than I’m crediting them for (Ki and others). Still, $1,400 appears to be a reasonable lower bound. Another way to frame it: if the stock eventually re-rates toward 1.5 times (adjusted book), you pick up a couple of extra points of CAGR on top of that base 12%. Probably back to the point where this isn't a "rocket surgery" idea, not that it has felt stretched by any means. Its just every time they do one of these "alchemy" (realisation of hidden value) moves, it's always fun to do some back-of-the-envelope numbers.

-

Eurobank has entered into a term sheet with Fairfax (as of October 13, 2025) to buy back 80% of Eurolife FFH Life Insurance for €813 million, implying a ~1.45× price-to-book multiple, with Fairfax retaining a minority interest via other structures. Fairfax will increase its involvement in Cyprus by acquiring 45% of Eurobank’s ERB Asfalistiki for €59 million, again at ~1.45× P/B https://www.eurobank.gr/en/group/grafeio-tupou/etairiki-anakoinosi-13-10-2025-i is it correct that they bought this 80% stake in Eurolife for approximately €316 million (about CAD 481.6 million) in late 2015? There were a bunch of decent divs along the way too. A decent chunk of change, are we getting set for an acquisition?

-

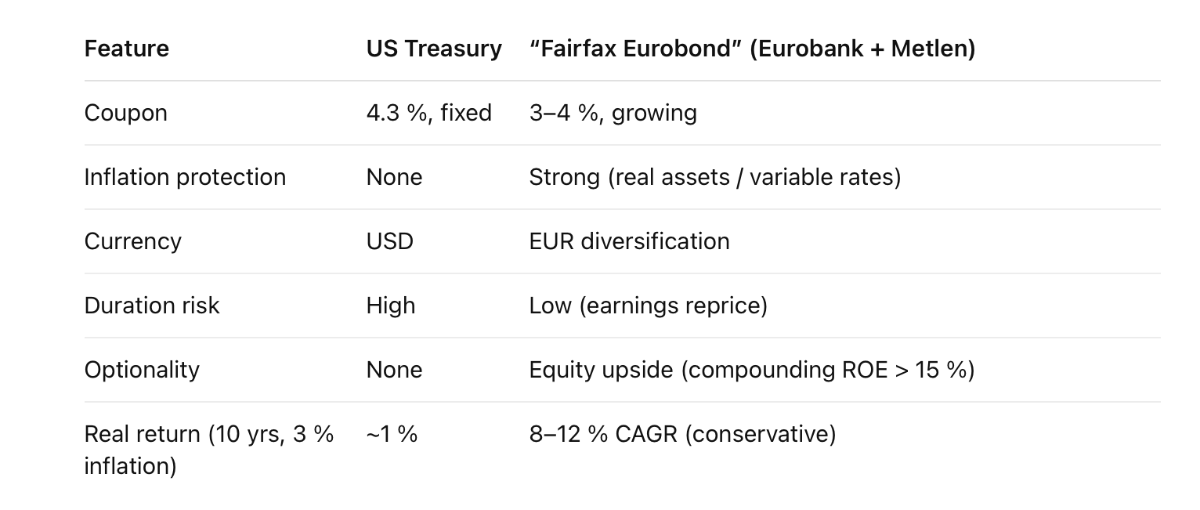

FWIW I see their Greek holdings as a quasi $5bn Inflation protected Eurobond. It’s obviously not a bond in a regulatory sense, but it behaves like one economically. There is even the remote possibility under both OSFI’s LICAT and Solvency II internal models, that they can petition to assign lower equity stress factors to holdings that have: 5 + years of stable, audited dividends, Low correlation with public-market indices, and Strategic / long-term intent (no trading) Far preferable to US Treasuries IMHO. While it doesn’t completely offset a cut in yields on a $50bn bond portfolio, along with some of their other positions, just give it time

-

Not sure the note (ChatGPT DR unedited) attached answers your question but was helpful for me. What is particularly humbling was my own mental model, that Sokol was going to elevate this shitco into a mini Mid American. Couldn’t get to the bottom of who’s bright idea this was but if they have moved on I wouldn’t be all that disappointed. Goes without saying I would be departing with them for my own false narrative. Edit: Fixed the butchered table in the doc Fairfax Financial’s Investment in APR Energy- A Comprehensive Review.pdf