nwoodman

-

Posts

1,892 -

Joined

-

Last visited

-

Days Won

15

Content Type

Profiles

Forums

Events

Everything posted by nwoodman

-

Added to 7974.T Nintendo Co

-

Decent beat by Kennedy Wilson (KW) Q2 EPS of $0.28/share https://ir.kennedywilson.com/~/media/Files/K/Kennedy-Wilson-IR-V2/documents/kw-2023-06-30-8k-ex-99-1-10-q-supplemental-release.pdf

-

Quite possibly, as you say we are in the process of finding out. One thing I have tried (unsuccessfully) to handicap is their network. I think your view of the world is more pragmatic - it’s extensive and the compounders get the capital. A couple of questions to you and the board 1. One that intrigues me is Foran Mining. How did that investment come about? I guess I am interested to know if it was a brokered deal (third party) or part of their network. 2. Also has anyone prised the lid off the Exco position? This appears to be a cash spewing black box when energy prices are favourable. https://www.kirkland.com/-/media/publications/article/2019/11/new-york-law-journal-exco-bankruptcy-restructuring.pdf?rev=334e0f6d637e47039cf954208197a785&hash=1158DA38C7721AD4AFABFA24D5DD257B Normally not an energy/commodities guy but these two investments look like they are already home runs with a lot of potential upside

-

I have been thinking a lot lately that one of the magic ingredients to these styles of companies is deal flow. Berkshire was able to use their brand and capital to backstop companies during the GFC but the phone nary rang during Covid (I know the Fed backstopped before things got truly interesting). Perhaps Fairfax's deal flow is lower quality, and they are less discerning than Berkshire or Markel. However, they always seem to have something on the go. Often to the point of more ideas than capital i.e over leveraged. Even their misadventures have yielded silver linings, Greece being the prime example. Anyway, back to your thoughtful post, the more partners you have turning over rocks on your behalf, the better

-

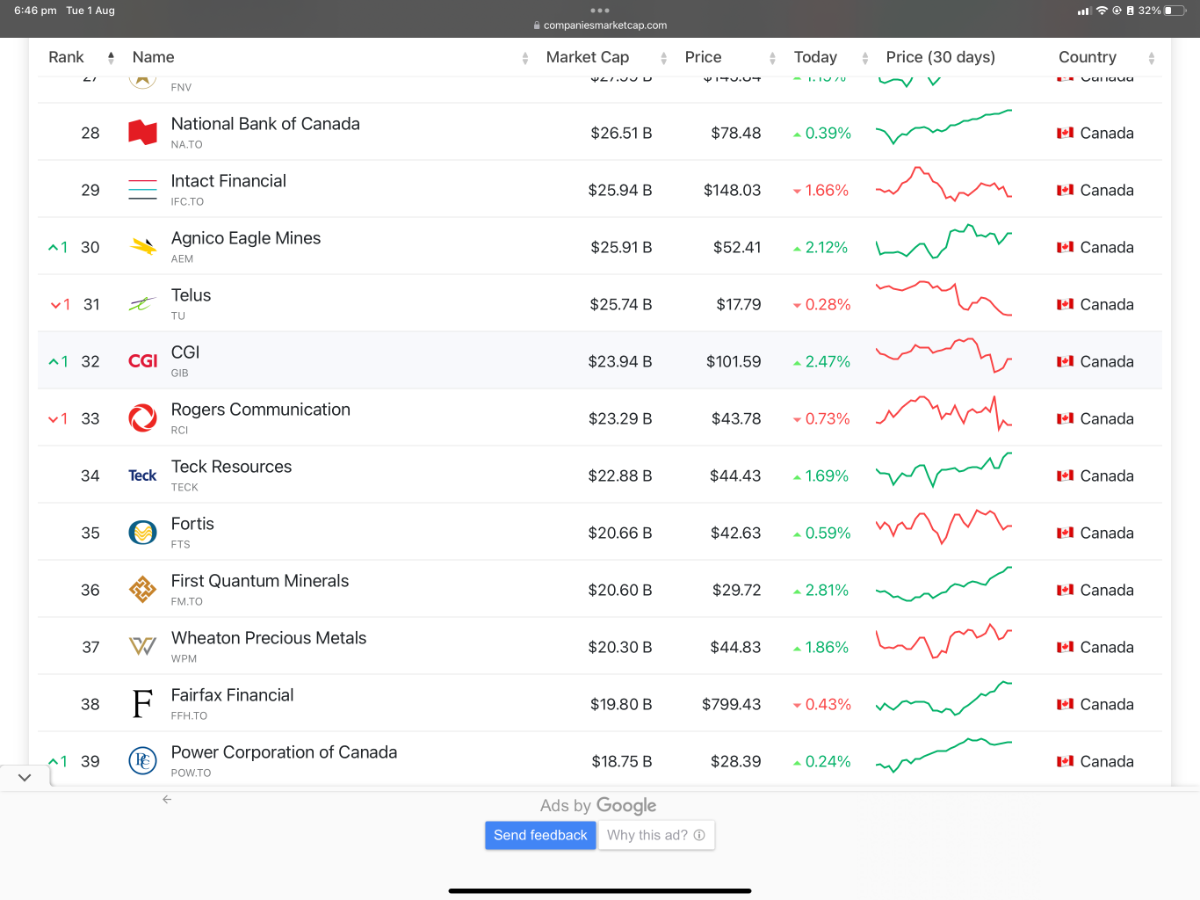

Personally think a market cap of $20bn is a real milestone. Just a shade off at the moment. If things keep evolving as they are, then they should crack the top 30 Canadian companies next year https://companiesmarketcap.com/canada/largest-companies-in-canada-by-market-cap/

-

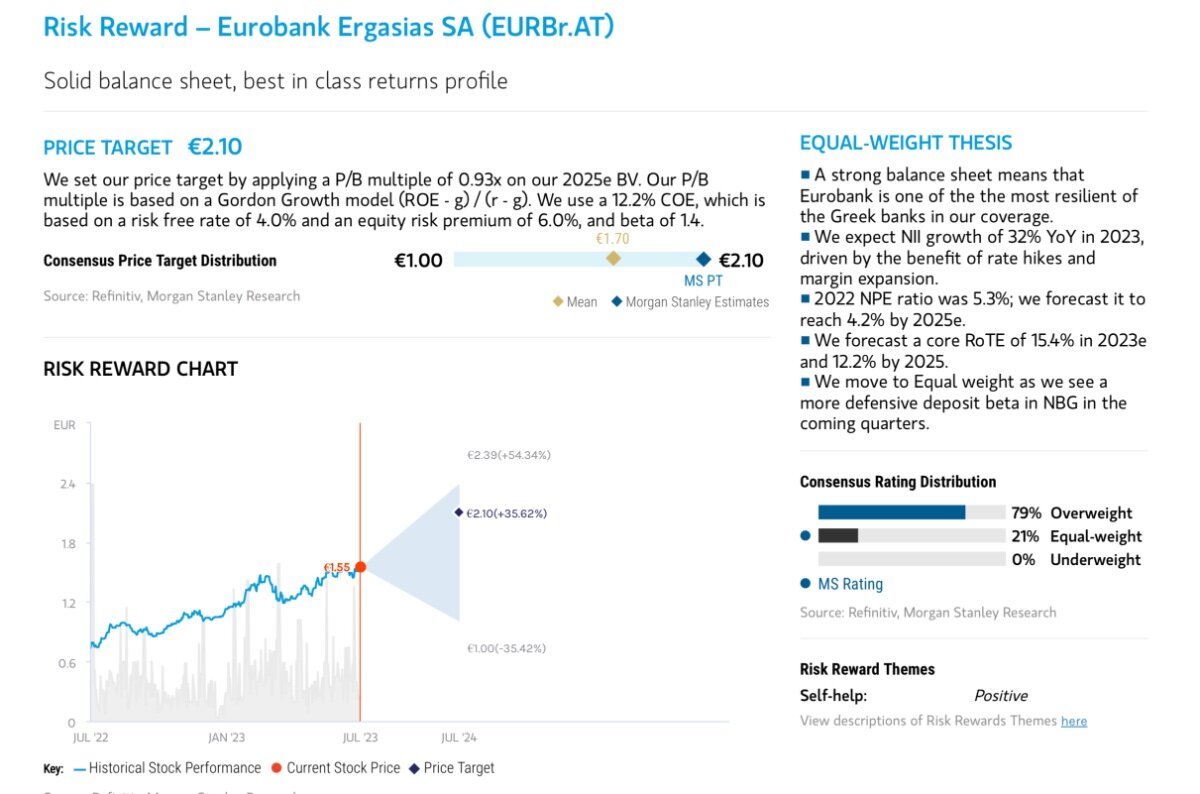

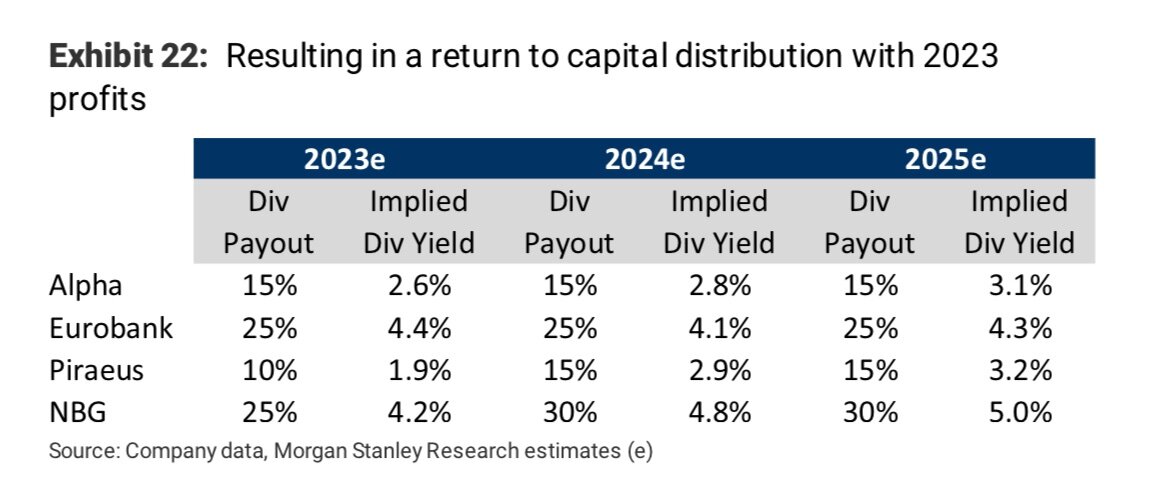

Guidance for RoTBV at >15%. Almost seems ludricous that they would trade at <TBV. Morgan Stanley’s take attached. I just hope they hurry up with the buybacks and are able to pick up the HFSF stake around these prices. Like buying dollars for 70 cents. https://www.reuters.com/article/eurobank-holdings-stakesale-idUKL8N3962ML EUROBANK_20230731_0000.pdf

-

Tidy set of results. Like FFH, still looks cheap even after the run up

-

Some positive news for Foran Mining “Base metals explorer and developer Foran Mining has received Ministerial approval for its McIlvenna Bay project, in Saskatchewan, concluding the environmental impact assessment (EIA) process for the copper/zinc/gold/silver project.” https://m.miningweekly.com/article/foran-wraps-up-eia-for-planned-saskatchewan-copper-mine-2023-07-27 Fairfax position size is ~$200m (23%) From Foran’s website “With Probable Mineral Reserves of 25.7 Mt at 2.51% CuEq containing 697 million pounds of copper and 1.4 billion pounds of zinc included in a Mineral Resource of 39 million Indicated tonnes grading 2.04% CuEq for 1.0 billion pounds of copper and 1.9 billion pounds of zinc and 5 million Inferred tonnes grading 1.8% CuEq for 104 million pounds of copper and 282 million pounds of zinc.” “The McIlvenna Bay Project is levered to commodity prices. At spot prices as at April 4, 2022 (copper US$4.81/lb), the initial phase project delivers a pre-tax NPV7% of C$1.1 billion and IRR of 54% (C$1.3B and 44% after-tax). The Deposit remains open and regional exploration continues to demonstrate the exciting potential to increase throughput and mine life. Copper price currently $3.87/lb Edit: We should have some updates shortly on the summer drilling program. There is a very good chance that the drilling at TESLA will continue to shore up reserves. The joys of exploration, blue sky baby https://foranmining.com/wp-content/uploads/2023/04/News-Release-Foran-Announces-New-Copper-Gold-Rich-Lens-Discovery-at-Tesla.pdf

-

He’s done it with pharmaceuticals in the past ”Buffett has said that a basket approach to the pharmaceutical sector makes sense given the difficulty in handicapping drug pipelines” https://www.barrons.com/articles/why-warren-buffetts-berkshire-hathaway-fell-out-of-love-with-jpmorgan-51605629567

-

Potential deal flow too. Definitely some good crossover with Berkshire Energy. You probably saw the interview with Buffett and Able in Japan

-

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

Sinead O’Connor - Troy. RiP -

Movies and TV shows (general recommendation thread)

nwoodman replied to Liberty's topic in General Discussion

Don’t want to do this one too much, but it was the good wife that pointed out to me that the Mum in that episode is Jamie Lee Curtis. Did not recognise her and testimony to the performance and the make-up. -

Movies and TV shows (general recommendation thread)

nwoodman replied to Liberty's topic in General Discussion

Yep watching it now. So good. Loved the first season but S2 is even better. It is hard to put a finger on why it resonates so much but it does, guess that is just great production values. One of the best shows of the year so far. Edit: Holy shit, just watched E6 Fishes, the family holiday dinner. Our own various family catastrophes have some perspective -

For me it is visibility and while below “book’ value, a decent margin of safety. They are firing on the equity front so there is a little arbitrage there as it flows to book. My buys lately are only an increase of around 10% on a large position and are a rotation out of PE 30 names eg AAPL. I would be interested to know if anyone is doing a major change in capital allocation eg low to say 20% of their portfolio. If these are only minor adds that are being reported then the datum of “what you are buying” is low value but not worthless. What I will say is your recent comment about them buying positions consistent with MKL and BRK and your disappointment if they weren’t differentiating struck a chord and I have pondered it considerably. Thank-you.

-

FFH

-

Trimmed AAPL, exited KMX,GOOGL

-

Gut-wrenching in terms of what could have been but a testament to them fishing in the right waters.

-

An outstanding report. The section on distressed investing in Greece (p.112) and the case study on the Greek company Terna Energy (p.159) may be of interest to FFH investors too. Mytilineos (Eur4.5bn) was rumoured to be pursuing a stake in Terna (Eur2.2bn) earlier this year but later refuted.

-

I hear you. I have held Eurobank in the past but soured on owning Fairfax positions, especially after ORH, ATCO etc. Probably irrational but the real loser is the taxman

-

Yep @Viking great work. I am sure at the time they thought they could replicate the sugar hit from belatedly following Buffett into Bank of Ireland (valuation and timing is all). For many years it didn’t work, but damn they learnt a lot about Greece and that is paying off in spades now. As @glider3834rightly points out, Eurobank has a number of opportunities in front of them, a bright future indeed. Where Fairfax is playing, deal flow counts. I think some of the more trying investments and their patience actually further their prospects far more than the market gives them credit for. Damn we all make mistakes. It is what we do with that hard won experience going forwards that counts. It is all to easy to dwell on the things that haven’t worked, I did, but so glad I changed my mind, a low hurdle helps

-

FRFHF

-

Financial DD underway for IDBI bank “Kotak Mahindra Bank and Canadian billionaire Prem Watsa-led Fairfax India Holdings have shown interest in acquiring majority stake in IDBI bank. The other bidders are said to be Sumitomo Mitsui Financial Group and Emirates NBD.” “The process is expected to conclude by September and the final bids may be in by December.” “The government is keen to wrap up the transaction by March 2024, according to sources.” https://www.thehindubusinessline.com/money-and-banking/financial-due-diligence-underway-at-idbi-bank/article67059941.ece/amp/

-

MS released an updated note on the Greek Banks (attached). Fairfax owns approx $2bn of Eurobank shares. Eurobank closed on Friday at EUR 1.55. Eurobank is not paying a dividend this year as the funds are being used to repurchase shares. From the Q1 press release "Rewarding shareholders is now becoming key in our strategy. Specifically for 2023, the amount earmarked for dividend distribution will be used in an optimal way to bid for the 1.4% HFSF stake through a share buyback scheme. For next year onwards, we envisage a payout ratio of at least 25%, in the form of cash dividends and share buybacks. Overall, we are pleased that we consistently outperform our targets for several years.” greek_20230709_0000.pdf

-

Not an insurance insider, but the issue I have with this sort of "industry gossip" is that it is never specific. What long tail lines are they actually talking about? Riverstone? Are they pre/post Andy Barnard? At least give us a hint or STFU. If anything it sounds like a view that is about 13 years out of date. When they picked up Allied World, Rivett actually named Med Mal as a potential issue but that those policies were all written prior to Fairfax's involvement https://www.canadianunderwriter.ca/insurance/how-fairfaxs-allied-world-acquisition-is-working-out-1004163093/ If the perception that there is an insurance "sword of Damoclese" hanging over the company I hope it persists for another few years and they retire 15-20% of shares outstanding in the meantime. If they are talking about Riverstone then there may well be some skeletons but from my perspective the run-off business is idling From the 2023 AR "RiverStone, our run-off operation, ....... The industry continues to be challenging, especially in the United States with the plaintiff bar, armed with third-party litigation funding, continuing an aggressive push to create new mass torts. We continue to see development on asbestos claims as well as recent emerging claims such as molestation and opioids. Given the nature of these claims, the results can be lumpy, with significant uncertainty around the eventual exposures and potential outcomes. RiverStone has been kept very busy focusing on our own latent claims and has not entered into any traditional third-party run-off acquisitions over the last number of years other than some small, very successful captive insurance deals. " What is a runoff operation? In insurance, a runoff operation refers to the process of managing a block of policies that a company has decided to stop writing or renewing. Essentially, the insurer continues to service the policies in the block (by paying claims, for example) until they expire, are cancelled, or all potential claim obligations have been settled. During the runoff period, the insurer does not write new business or renew existing policies in that block. The decision to put a block of business into runoff might be due to various strategic reasons, such as a change in the company's risk appetite, a decision to exit a particular market, or a response to regulatory changes or shifts in the business environment.

-

Positively gushing, thanks for the link “The rating upgrades recognize the removal of ratings drag from Odyssey Group’s parent company, Fairfax Financial Holdings Limited (Fairfax), which has demonstrated sustained improvement in its overall credit profile in recent years. Fairfax has reduced its debt leverage materially and improved its overall operating performance, while maintaining consistently sound balance sheet strength and financial flexibility. As a result, debt servicing metrics have improved sustainably, reducing the burden imposed on Fairfax subsidiaries and supporting the removal of ratings drag on Odyssey Group.” Can take or leave ratings agencies a the best of times but this is well deserved . Fairfax with a strong balance sheet who woulda thunk.