Viking

-

Posts

4,689 -

Joined

-

Last visited

-

Days Won

35

Content Type

Profiles

Forums

Events

Posts posted by Viking

-

-

1 hour ago, Spekulatius said:

It all depend on what the US Fed is doing. All the other central banks are more or less just following the Fed, they just have to. If they don’t and the Fed raises rates, their currency will get trashed.

It’s especially true for Canada, because their economy is so closely tied to the US economy.

@Spekulatius at the end of the day, what the Fed does will impact Canadian inflation in a big way. But the Bank of Canada also has an important role to play (feels kind of strange to write that). The Bank of Canada was already on pause (since January). There was only one reason for them to hike this week… and it had little to do with the Fed. Or the Canadian dollar. High inflation (4%ish) is starting to get entrenched as the new normal here. I think the tipping point was the strong rebound in the resale housing market since January (they paused and housing took off).

i am beginning to think there is only one thing that is going to get inflation under control - and that is a recession. My guess is the US is in the same boat. Central banks are going to have to chose. I was surprised the Bank of Canada increase rates - with their premature pause in January i thought they had already made the decision to let inflation run at 4% for a few years (that is how you solve a too much debt problem). It looks like i might be wrong - and the Bank of Canada just might be coming to the conclusion they need a recession - and higher unemployment - to get inflation all the way back down to their 2% target.

—————

A big problem the Bank of Canada has is they only control the monetary side of the equation. As i posted earlier, the federal government and some of the provincial governments are spending like drunken sailors. So the fiscal response is highly stimulative today. At the same time the government is bringing in a record number of foreign students/foreign workers/immigrants and that is also highly stimulative to the Canadian economy. So we have this crazy set up where monetary and fiscal policies are working at cross purposes. So i am very interested to see where we go from here… the Bank of Canada might need to hike a few more times. If they keep going they will get a recession at some point.

————-I am looking forward to seeing what the Fed does next week and, perhaps more importantly, what their communication is. I wonder if they learn the lesson of Canada and Australia - a pause is just an illusion. It simply gives inflation more time to work its dark magic on the economy. The last thing the Fed needs is a rebound in US housing and the stock market taking off - which is probably what happens if they pause.

-

On 6/7/2023 at 4:22 AM, nwoodman said:

Awesome, but even more awesome that you are like a blood hound on the scent. Thanks for posting as the IRDAI figures have not been updated in a while

@nwoodman and @glider3834 thanks for all the info on Digit. Another nice tailwind for Fairfax. Love it. -

28 minutes ago, changegonnacome said:

I gave you the motivation for the invasion...counter to the consensus narratives of Putin the imperialist............to say it hasn't worked out is an understatement.....clearly.....my thread has been focused on the cause, motivations and reason for the invasion on Feb 21st....and what precipitated it.

Have a read of what I wrote...you've misunderstood what I've said.....and mischaracterized it.

Can I ask @Viking do you think that the West courting Ukraine to be a close alley, even hanging out NATO membership might have played even a small part in antagonizing Russia, its 800ilb gorilla neighbor with nukes. Might't

I also explained why Belarus/Ukraine.....remain a special case and a redline re: NATO....Finland/Sweden joining NATO would not have triggered an invastion the same way a pathway to Ukraine joinig NATO would.....and its to do with a land invasion from Central Europe.....its how Russia dies, if it ever dies....its certainly how Russia most recently nearly died in WWII:

With all due respect i think you are way overthinking this thing. The simplest answer is usually the right one. Why did Putin do it? Because he thought he could get away with it. He miscalculated. And now he and Russia is screwed.

Why does any dictator do anything? Might is right. Hunger for more. Legacy. Hubris. A toxic combination. I love history (and Russian history). Putin is simply trying to do do what many Russian leaders before him have tried in previous centuries. The problem for Putin was even before the war in Ukraine, Russia was already a corpse of an empire. Like i said above, he miscalculated. And all he has done with his catastrophic invasion is expose how rotten Russia really is to the rest of the world and accelerated the country’s decline. Empires disappear all the time. Just look up ‘Ottoman’ or ‘Austro-Hungarian’ or ‘British’ or ‘German’. And when they disappear most do not go quietly into the night… their leaders often do really stupid things (like trying to return to the ‘good old days’) to hasten the end.

-

30 minutes ago, Spekulatius said:

Mearsheimer has a very selective interpretation of facts as it relates Putin, imo.

Great description of this guy. He has a simple, narrow narrative that appeals to lots of people (simple narratives are a must for the masses… repetition too…). He finds lots of facts to support his simple narrative (very easy). And ignores everything else… the other 70% that refutes his narrative. I find i learn next to nothing when i listen to Mearsheimer. He is a dog with a bone. And i am not looking to get brainwashed… There are lots of other great sources of information out there. -

3 hours ago, changegonnacome said:

Dont know about you - but generally an ounce of prevention is worth a tonne of cure........to ensure US nukes never end up in Ukraine......the best strategy is to ensure Ukraine never ends up in NATO. No? That not a good strategy you think as the temporary Russian leader you currently are in your imagination?

Clearly i am an idiot. ‘Ounce of prevention’? Seriously? What have they prevented? And check out the ‘tonne of cure’ below… that is a cure? Seriously?

So Russia decided to invade a sovereign country because of the risk of nukes getting placed there. As a result of their actions, they also are now directly responsible for:

1.) forcing Finland to join Nato. Hello nukes very close. FYI, Finland is about the same distance from Moscow as Ukraine (in rocket terms).

2.) forcing Sweden to join Nato. The Baltic Sea now belongs to Nato.

3.) revitalizing Nato, which was crumbling and close to becoming obsolete before the invasion.

4.) forcing all countries in Europe to aggressively re-arm, including big ones like Germany. So in the coming years Russia is going to be surrounded by hostile and armed to the teeth neighbours. (Yes, people in Europe get hostile when they see the atrocities of what Russia is doing to Ukraine today).5.) killing to date 20,000 of its own citizens (Russians!) with 100,000 casualties (Russians!)

6.) materially impairing the living standard of most Russians, likely for a generation

7.) materially impairing the future prospects of most Russian children

8.) forcing hundreds of thousands of young Russian men to flee the country to avoid fighting in the war

9.) economically speaking, has effectively become China’s concubine

Man looks to me like Russia just nailed it with this invasion. My list above is just scratching the surface of what they have ‘achieved’.

-

2 hours ago, bizaro86 said:

*one also mentioned that she thought Calgary was safer than Vancouver as an equal factor to the cost savings.

@bizaro86 Parts of Vancouver are really in decline; Chinatown being an easy current example. Tent cities have popped up everywhere (not just a Vancouver thing… i saw it even in rural BC) - and it has now become a way of life for many. Catch and release is looking like a disaster; especially when mental illness is involved. The Provincial government is using BC as a test kitchen when it comes to drug use/treatment in general and i am not sure the reality on the ground is going to live up to the theory in the study. My read is we are reaching a tipping point where it is going to become an important factor at the polls. Vancouver just had a civic election and a right of center party swept the slate (extremely rare occurrence). Voters are getting pissed off.

B.C.’s drug decriminalization experiment is off to disastrous start -

1 hour ago, ICUMD said:

Canadian banks are pretty sound I think given their oligopoly and with new immigrants entering the banking system.

What is more interesting to me is whether the thesis of structurally higher interest rates is correct or not. Inflation is high and a lot of debt/ asset is held in the form of mortgages. Many of these mortgages will reset in the next 3-5 yrs.

This could 'deflate' the housing market. Perhaps this is the true intent of the BOC.

About 66% (2/3) of Canadians own their primary residence and 33% rent.

40% of all Canadian home owners carry no mortgage on their property. 50% of Vancouver home owners carry no mortgage. So higher interest rates have little impact for these people.

And of the 60% who carry a mortgage a mortgage probably 2/3 of this group have likely owned for 10 years so their mortgage is very small. Here rising interest rates matter some.

So my guess is 20% of Canadian home owners are likely stressed by the increase in interest rates. Some of these will have fixed rate mortgages (5 year fixed being the most popular) so it will take a few years for higher rates to fully impact even this group.

If i am close, that means 13% of Canadians (20% x 66%) are feeling the heat of higher rates (via their mortgage). My guess is some of these people will get help from their parents (who are sitting on significant wealth). This might explain a little why higher interest rates is not having its usual impact in slowing economic activity.

—————Oh, and lets not forget about savers. My 91 year old mother in law is now earning 4.5% to 5% on her GIC’s, up from zero 18 short months ago. This is a material increase for her. And she is spending her newfound source of income. Lots of seniors out there in the same boat.

And let’s not forget about all those Canadians who are sitting on enormous real estate gains, many of whom are mortgage free. Add in pensions. A decade of stock and bond market gains. That is an enormous amount of wealth that is impacting spending patterns - and it is largely insensitive to interest rates. Do they care if your restaurant bill went up 10%? Does it change their behaviour? Nope.

Bottom line, the Bank of Canada is slowly learning that the old models need to be updated…

-

1 hour ago, SharperDingaan said:

This is press spin; the reality is that 'structurally higher interest rates' will only be temporary.

Simply 'cause as more people get forced into selling their homes because the mortgage is no longer affordable, that rise in supply will rapidly lower house prices. More cash going to debt service, and less borrow capacity from the lower housing value, lowers spend, lowers employment, and lowers the interest rate. The real question is how best to use the deliberate 'spin' of 'highest interest rate in 20+ years'; versus 'the end of record low interest rates', and 'return to historic interest rates'.

Canadian banks will do very well, but there are a lot of better alternatives.

Normal curve restoration, extended real estate loan provisioning, CBDC, fintech, etc. are still to come, and will take at least a decade to flush through. While all though that time electric grids are being rebuilt, transport fleets moved over to electric, and lower income housing being built/re-built in mass, etc. Not a bad thing.

SD

@SharperDingaan my guess is employment is the key moving forward. If employment stays reasonable strong then i have a hard time seeing how house prices move much lower in Vancouver/Toronto. I think we will need to see a recession and higher unemployment to cause house prices to fall. And even then, the fall likely will be mild (10% from here?).

We have a severe shortage of housing right now. Very low listings of homes for resale. Exceptionally low vacancy rate (around 1% i think). So the market is frozen right now. No one can move. (Rent increase for new tenants is running close to 20%; rent increase for existing tenant was 2% this year - as mandated by provincial government - after a 1.5% increase in 2022.)

Canada also had about 1 million immigrants come in over the last year: international students, foreign workers and regular immigration. Most want to live in Toronto or Vancouver.

Cost to build a condo in Vancouver is C$1,100-$1,200 a square foot. For a 2 bedroom 850 square foot apartment that is $1 million. Interest costs for builders is spiking so this cost is likely too low. About 1/3 of a builders costs today are now taxes (municipal, provincial, federal) - all levels of government need housing to chug along.

Bottom line, the real estate market is Vancouver and Toronto is NUTS. It is completely warped out of shape (like a pretzel).

The crazy thing is the housing boom has made millions of Canadians millionaires. It has also become a cultural thing… want to get rich? Buy real estate. It is everywhere in society. Hockey is no longer Canada’s pastime - it is now real estate.

At the end of the day, i am watching real estate closely. I have three kids, the first of who just graduated from university. I would love for all three to live in Vancouver (we all like each other…). If they don’t live in Vancouver it will likely be Toronto (the center of the world for employment in Canada).

-

5 hours ago, John Hjorth said:

Well, the Canadian residential real estate market has over the years been discussed to skinlessness here on CoBF - I read all those discussions as about a bubble, that consistently, persistently and stubbornly refuses to burst.

What is your view and thinking on what will happen to the major Canadian banks in such a screnario? I think I have observed that you aren't shy of holding american banks when they are cheap, but I haven't seen you engage with Canadian banks at all, I think.

@John Hjorth my guess is the Canadian banks will do ok. Canadians do not default on their mortgages. In terms of return, if you look at the last 5 years, Canadian banks have delivered a total return = dividend payout. I have bought a basket of the Canadian banks over the past year when they have sold off aggressively… and then sold them when they went up 3 or 4% (in tax free accounts). I have done this a couple of times.

Canada right now has a number of attractive options if someone wanted to build a high yield dividend payout portfolio with an average dividend yield of around 5.5% (and likely a conservative total return of around 8-10% moving forward). For Canadian, in taxable accounts, income in the form of dividends is taxed at a very low level.

- Canadian banks- Canadian telco’s

- Canadian pipelines

- Canadian energy

—————“In Canada, mortgages are typically recourse loans. However, in Alberta and Saskatchewan—non-recourse loans are more common. If you put less than a 20% down payment on your home, you would be required to have the CMHC insurance, which automatically makes your mortgage a recourse loan.”

-

30 minutes ago, A_Hamilton said:

I'd close out, was a great trade at a silly price, less attractive now. The other thing is that TRS are priced at SOFR + a spread, so this isn't necessarily cheap capital.

The key is what Fairfax thinks:- fair value is for their stock is today (1.3 x BV?)

- what the prospects are for earnings over the next 12, 24, 36 months (my base case is $120/year)

- what the plan is for share buybacks (as the hard market ends, share buybacks could increase materially to reduction of +4% per year if they wanted)

Fairfax, of course, has better information than we do. I would continue to hold the TRS.

-

Yesterday, the Bank of Canada delivered a surprise rate increase. Today they provided more details of why… what a shocker:

“A lot of uncertainty remains. But it’s possible long-term interest rates will be higher in the coming years than what Canadians are used to,” Beaudry said on Thursday. By outlining these key forces, Beaudry said he hopes he “will help people be prepared in the eventuality that we have entered a new era of structurally higher interest rates.”

—————

Bank of Canada Suggests Higher Rates May Not Have as Much Bite

In a speech to the Greater Victoria Chamber of Commerce a day after policymakers raised the benchmark borrowing rate to 4.75%, Deputy Governor Paul Beaudry flagged concerns about a reversal in core inflation and said officials were surprised by household spending on goods and services.He also said that neutral rates — a theoretical level of borrowing costs that neither stimulate nor restrict the economy — may drift to higher levels compared to before the pandemic. Beaudry said stalling globalization, rising wages, and increasing investment opportunities in artificial intelligence as well as the transition to a low-carbon economy were contributing to the increase.

“A base-case scenario where the real neutral rate remains broadly in its pre-pandemic range is possible, but the risks appear mostly tilted to the upside,” Beaudry said, adding that there was “meaningful risk” neutral rates could go up.

While Beaudry was careful to note that the current neutral rate is still volatile, the comments will fuel speculation policymakers at the Bank of Canada are increasingly of the view their aggressive increases to interest rates are less restrictive.

The statement, which came a day after the bank raised borrowing costs for the first time in three meetings, also highlighted the possibility rates need to move higher for longer in order to bring inflation to heel.

“A lot of uncertainty remains. But it’s possible long-term interest rates will be higher in the coming years than what Canadians are used to,” Beaudry said on Thursday. By outlining these key forces, Beaudry said he hopes he “will help people be prepared in the eventuality that we have entered a new era of structurally higher interest rates.”

-

19 hours ago, giulio said:

Ps. @Viking I really struggle to understand this "Capital preservation is paramount; not return. And you see it in Berkshires results... they are not close to what they were". Downside protection has always been paramount at BRK but to say they are not interested in return would be paradoxical! Returns are a product of your opportunity set...I am glad they have been "inactive" in the recent past, but you can rest assured Buffett will swing BIG if the opportunity knocks!

@giulio Sorry if my wording is not clear. My view is Buffett today has capital preservation as his single most important objective. It hit me like a bag of bricks when I watched him a couple of years ago when he had the online only annual meeting Q&A. He said that many long term shareholders had a majority of their wealth (and their families wealth) in Berkshire and he felt a massive responsibility to ensure that this wealth would be protected so it could be passed to future generations.

Now don't get me wrong... Yes, Buffett also wants to make a decent return for shareholders. Now it is possible that Buffett has had the exact same mindset over the decades since he started. And Berkshires size is primarily what is causing returns to fall dramatically (from those earned in the past).

-

We have seen a massive increase in interest rates over the past year; far in excess of what anyone felt would happen. The Fed is also engaged in QT. We have a banking crisis at regional US banks, which is tightening credit. The Treasury needs to issue something like $1 trillion over the next 6 months to refinance and refill coffers (which will suck liquidity out of the system). Looks to me like risks to the economy are pretty elevated right now. Or traditional monetary policy no longer works - that new paradigm / this time is different thing.

Does this mean people should move to cash? No, of course not. My base case is the US and global economies keep rolling along with slow growth.

But i am very happy right now to lock in gains on a part of my portfolio. My cash weighting is back up to 35%. Happy to sit in the weeds (with cash earning a risk free 4%) and wait for some market dislocation where Mr Market serves up some fat pitches. I am pretty certain i will get at least a couple mouth watering opportunities in the coming months/year. Just like 2022. And 2021. And 2020…

Buy and hold (index investing) worked like a charm when we lived in a QE world. It didn’t really matter what you owned… everything went up - every year. In the QT world of today, i wonder if active management might do a little better…

-

14 minutes ago, valuesource said:

I think they're a long way from backing off on repurchases.

i agree. Prem has said that they feel their shares are worth much more than book value. My guess is he is probably thinking a minimum of 1.3 x BV (i am probably low). Fairfax also know earnings could total $300/share over the next 11 quarters. Book value today is $800. Book value could easily be $1,100 the end of 2025. At a 1.3 x multiple that would put the value of Fairfax shares (low end) at $1,400 at Dec 2025. Buying shares today at $750 is a bargain for Fairfax. -

1 hour ago, dartmonkey said:

How about this:

2019: In the past, to protect our equity exposures in uncertain times, we shorted indices (mainly the S&P500 and Russell 2000) and a few common stocks. After much thought and discussion, it became clear to me that shorting is dangerous, very short term in nature and anathema to long term value investing. As I mentioned to you in last year’s annual report, shorting has cost us, cumulatively, net of our gains on common stock, approximately $2 billion! This will not be repeated! In the future, we may use options with a potential finite loss to hedge our equity exposure, but we will never again indulge anew in shorting with uncapped exposure. Your Chairman continues to learn–slowly!!

2020: I said in our 2019 annual report that we would not short stock market indices (like the S&P500) or common stocks of individual companies ever again, and our last remaining short position was closed out in 2020 (not soon enough, as it cost us $529 million in 2020).

So in the 2019AR Prem said “After much thought and discussion, it became clear to me that shorting is dangerous, very short term in nature and anathema to long term value investing.”

And what did we learn in the 2020AR? When Prem said what he said above they STILL HAD a massive short position on. And they kept it in place for another year. That cost Fairfax shareholders another $529 million.

That stream of communication was not one of Prem’s finer moments. When questioned about the miscommunication i am pretty sure he said… well in 2019 i said i would not put on a NEW position. The loss was not a new position… so my previous communication was accurate. Technically correct, but…

This was an example of terrible communication by a CEO.

Fairfax is no longer a small family owned Canadian business. They are now a Goliath… a top 20 global insurer. Simply an amazing story. Put simply, Fairfax has entered the big leagues. Prem is now going to be held to a new standard in terms of communication. And rightly so. So many Canadian companies have failed to make this transition (Saputo being the best immediate example i can think of). If Prem wants to be viewed as a best-in-class global company he needs to improve on the communication (especially to shareholders). Or not. And suffer the consequences. His choice.

—————Just to be clear, i am not a Prem hater. I am a hard marker (ask my kids). Call a spade a spade.

Prem has many strengths. He has been able to attract and retain outstanding people. People at Fairfax appear to really like him and enjoy working for the company. He/Fairfax has built a huge collection of amazing relationships in the business/political world. He is strategic. And focussed on the long term. I have no doubt that he is a first-class human being. He has Fairfax poised to do exceptionally well over the next few years. And like all of us, yes, he also has flaws. Am i happy he is CEO of Fairfax? Of course.

-

44 minutes ago, longlake95 said:

He's being Buffett like. Trying to attract true-owner mentality types - like this crowd. Can't say I disagree.

The problem is Fairfax does not run the business to attract a long-term shareholder base. The decisions/results/communication they delivered 2010-2020 are all the proof that is needed on that front. It was terrible (on balance). My guess is many long-term shareholders capitulated and sold in the bloodbath in 2020. Trust in management was lost and at an all time low.

Fairfax is a blank canvas today. They are starting over and building a new relationship with shareholders. If they want long term shareholders they need to play their part. They need to re-establish trust. Communication needs to be stellar.

Look at Buffett today. He is running Berkshire like a trust. Capital preservation is paramount; not return. And you see it in Berkshires results... they are not close to what they were. (I am not saying this is how Fairfax should be run.)

Will I hold Fairfax long-term? I don't know is the honest answer. We are still too early into the turnaround. I love the set-up for the company right now. Management has delivered for the past 5 years.

At the end of the day... I call it fit. To own a stock long term there has to be a match with how a shareholder is wired and how a company is run.

----------

At the AGM I asked Prem what lessons Fairfax had learned from the lost decade for shareholders (2010-2020). And had any processes changed within Fairfax to make sure the same TYPES of mistakes are not made again. I got a non-answer. Which of course WAS an answer.

Another question at the AGM was if Fairfax carried too much debt (operated with too much leverage). Prem's answer was they could sell Odyssey and be debt free.

I found the answers to both questions to be lacking. But I remain open minded.

-

37 minutes ago, cwericb said:

Now that we have hit this new milestone, I wish Prem would do a stock split and lower the per share of Fairfax and make it more attractive to smaller shareholders. There must be a ton of small investors in the market place with smaller portfolios. But for a small investor who would like to add say, $2,500 in FFH shares to his portfolio, what? he needs to buy two and a half shares?

With all the complaints about the market not recognizing the true value of Fairfax I think this is one of the reasons why. Lowering the share price to, say $50 or even $100, would not only focus a lot more attention on Fairfax but it would likely soon lead to an escalated share price.

Most of the Canadian banks have done this from time to time. What’s so special about Fairfax? Ego? Or am I missing something?

JMHO.

I would also like to see a stock split. Perhaps 5 for 1. As you said, this would open Fairfax up to more smaller investors. This would also improve liquidity, especially in the US. I don't see a stock split as likely.

-

Thanks to everyone who took the time to participate in the poll. The poll is still open if you have not voted yet and wish to do so. It is great to get an idea what a large group of board members are thinking at a specific point in time. I must say, i was surprised by the results. The COBF mob, 46 strong, assigned a fair value to Fairfax of about $1,070/share. Actually, this is low as 14 respondents chose the highest value option ($1,200 or more). The ranges on the poll were way off (needed fewer on the low end and more on the high end).

My key take-away? Most board members who follow Fairfax feel, despite the run-up the past 30 months, that the stock is still very undervalued.

What did I vote? $900-$999 = midpoint of US$950. Today.

To come up with my number I used two rules of thumb:

- PE = $120/share (normalized earnings today) 8 x multiple = $960

- P/BV = BV of $800 x 1.1 = $880 (I went with 1.1 here - instead of something higher - because of the significant one time bump from IFRS-17)

Yes, both my earnings and book value multiples are very low. But that is how I see Mr. Market valuing Fairfax today (sentiment/confidence in management, while improving, is still low). As was mentioned by others, Fairfax is a complex animal. And there is the risk of another 'equity hedge' type of decision.

There has been an enormous number of changes happening under the hood at Fairfax over the past couple of years. This makes it more difficult to forecast future earnings and book value growth - so most investors (not the ones on this board) continue to undervalue Fairfax. As Fairfax executes well and delivers solid results - and new (higher) run rates get reported (and baked into historical numbers) over the next couple of years this will get easier. As the larger investment community gets more comfortable that the higher numbers are durable we should see multiple expansion (hopefully closer to other insurance peers). It would not surprise me to see Fairfax's stock deliver another couple of years of 20% to 30% annual returns - driven by mid teens growth in book value and multiple expansion.

-

6 hours ago, kodiak said:

My estimates of intrinsic value and where this will trade in 36 or even 60 months do not assume any major buybacks from the company. It is possible that Fairfax takes the share count from the current 23 million shares to 18 or even 15 million depending on how much cash the insurance business generates once premium growth starts to slow down. In a world of zero premium growth and respectable combined ratios, Fairfax will not be required to keep injecting capital into these businesses, as they have over the last few years to fund the growth in premiums. Once premiums stop growing, these same insurance subsidiaries will begin to send capital back to the parent. The uses of this capital will include the buying back of all the remaining insurance stubs from OMERS. I would also expect them to take a couple more public companies private and finally, buyback shares below 120% of book value. If they earn $150 per year for three years, that generates over $11 billion in capital. That capital is going to go somewhere. After the minority cleanups, we might see some meaningful repurchases. Those are not in my projections. If they happen, the chances of a $2,000 or $2,500 Fairfax share price in less than 5 years grows considerably. At the current price of $730, this stock is simply too cheap and I would argue a better deal at $730 than $500 one year ago. People selling at $730 today simply aren't doing the work to calculate the earnings power of Fairfax or must be finding other stocks to own. I would love to know what they are buying to justify selling Fairfax. They have to be fantastically cheap stocks with a wonderful margin of safety.

I am selling other things in my portfolio to currently buy shares of NextNAV, a $300 million market cap failed SPAC that owns a portfolio of 2.4 billion POPs of nationwide spectrum in the 900 MHz band. This spectrum is worth between $1.5 and $2.5 billion and should be monetized over the next 24 months. The stock is $2.67 and I expect the shares to be worth easily north of $10 each in 24 months. They also have a cutting edge alternative to GPS which you get for free and could be worth $10 or $15 in 3-5 years. Finally, the corporate governance is fantastic, with heavy inside ownership, very smart spectrum folks on the Board and a history of making money for investors. Even with all that potential upside, I am not going to sell Fairfax to fund the purchase of NN shares.

@kodiak i also see share buybacks as a potential catalysts for Fairfax. With all the cash they are currently generating it will be interesting to see how much they allocate to share buybacks: do they go big (5% or more in one year) or do they go small (2 to 3% in one year). Fairfax will likely be opportunistic… allocate capital to the best available opportunity. -

What is your estimate of the 'intrinsic value' of Fairfax's stock as of today? What says the COBF mob? The stock closed on Friday at US$734 = C$987.

If your intrinsic value is a range, please vote where mid-point falls.

After you vote, can you provide a brief comment (if you are comfortable): what is your number (or range) for intrinsic value? How did you come up with your estimate? Or simply comment on whatever you would like. I want to keep things pretty vague so we get as much original thinking as possible.

Fairfax's stock has had a pretty incredible run the past 30 months. Has it passed your estimate of intrinsic value? Please let other board members know your thoughts.

----------

It would be interesting to know what management at Fairfax thinks the intrinsic value of their stock is as of today.

----------

What is 'intrinsic value' and how is it calculated? Go with whatever you think it is. Below is Buffett's definition.

Buffett ( Berkshire Hathway’s manual ), “The intrinsic value can be defined simply. It is the discounted value of the cash that can be taken out of a business during its remaining life. As our definition suggests, intrinsic value is an estimate rather than a price figure. And it is definitely an estimate that must be changed as interest rates move or forecast or future cash flows are revised. Two people looking at the same set of facts almost inevitably come up with slightly different intrinsic value figures.”

-

Lot of quality companies hitting (or close) to new 52 week lows. Lots of commodity stocks hitting 52 week lows. Financials are hated. Most insurance stocks are selling off. Retail stocks got whacked today and many are dirt cheap. Lots of companies also trading where they were trading 5 years ago. It is like the market is in a bear market right in front of our face. Except we don't see it looking at the market averages - because of the run in AI stocks. So I started nibbling today on a bunch of different things. If stocks keep selling off this could get quite interesting...

-

2 hours ago, Haryana said:

What is the point of pumping the prospects if we refusing to buy stock at current price?

I tend to hold concentrated positions. When i concentrate i like to get into the weeds. We are constantly getting new news. So the story is constantly changing. Sometimes the changes are minor… sometimes they are major. I like to post what i learn. And i enjoy the feedback from other posters. Be inquisitive and be open minded. Now that might look like ‘pumping’ a stock. I view it more as tending to the eggs in my basket. It works for me.

With Fairfax, i have a core position - something i plan on holding for a few years (as of today). At times i will buy more and flex if bigger. Sometimes quite a bit bigger. Other times i will sell some and flex my position size lower. ‘Flexing’ will depend on lots of different things: changes to the FFH ‘story’ (fundamentals), the price of FFH stock (Mr Market), what is going on in the overall stock market (that opportunity cost thing)… too many variables to list.

Fairfax is a VERY volatile stock - moves of 20-30% each year are not uncommon. We are entering hurricane season. Having said that, my guess is Fairfax will be aggressive buying back stock this year via the NCIB so the stock may continue to surprise to the upside. No idea where the stock price will go over the short term. But over the next few years i am confident the stock will continue to power higher. And i am confident because of the work i put in to understand the investment. It is a constantly evolving process - involving lots of lengthy posts along the way.

-

Thanks to everyone for responding. The COBF mob gave Fairfax management an average grade of 7.7 out of 10, with 38 votes cast. That is a solid vote of confidence from a pretty knowledgeable group of investors, many of whom are also likely shareholders. It would have been interesting have done this poll 2 years ago. Please continue to vote if you have not yet done so and would like to.

I voted 8. No company I follow would get a 10 (i am a hard marker, although that likely does not look like the case when I post on Fairfax). The big mis-step from the past (equity hedges) was the primary reason I did not go with a 9.

The turnaround engineered by the management team at Fairfax the past 5 years has been impressive. The company is exceptionally well positioned today. With one arm no longer tied behind their back, I am looking forward to seeing what they are capable of doing over the next couple of years.

-

13 hours ago, nwoodman said:

Thanks for that. Morningstar's Brett Horn also posted an update on the 19th of May that I think sums up where a lot of analysts are at. Full note attached but some key quotes below:

"While its primary business is insurance, Fairfax is in some ways more of an investment fund. Chairman and CEO Prem Watsa has a long history of bold investment bets and has shown a willingness to be unorthodox when it comes to portfolio construction. As a result, compared with other insurers, the company's results tend to be driven more by results on the investment side. We're somewhat skeptical of this approach, as we believe disciplined underwriting is a more reliable path to long-term value creation, and Fairfax's underwriting record is relatively poor."

"We think investors attracted to the stock due to a belief in Watsa’s ability to produce alpha should consider his record over the past decade, which includes some big wins but also substantial losses and missed opportunities. Fairfax has seen a lot of ups and downs, but its performance has been trending toward mediocrity."

"We believe that Prem Watsa’s investment philosophy, willingness to make outsize bets, and potential to generate alpha are the primary attractions for many investors. Fairfax’s name is often included in discussions about the “mini-Berkshires” that seek to distinguish themselves on the investment side, but we think this narrative is misleading. Watsa has had some dramatic successes on the investment side, with the most impactful being his gain of over $3 billion from credit default swaps and equity market hedges during the financial crisis. But he has had notable misses as well, including a sizable investment in Blackberry, and we don’t think his record could justify framing his investment skills as a structural competitive advantage. The company’s preferred metric is growth in book value per share, which has grown at a 6% CAGR over the past 10 years, a fairly mediocre result even considering the dividends Fairfax has paid."

What I think is interesting is that even with the mistakes of the past, FFH has been able to compound book value at a decent rate even while paying out a non-trivial dividend. We have all argued the merits of the dividend previously, but it is what it is.

When I bought back into the company in 2021, it was under the premise that management would ultimately prove that they could compound over the longer term at a rate of 11% albeit lumpy. So regression to the mean was the basic premise.

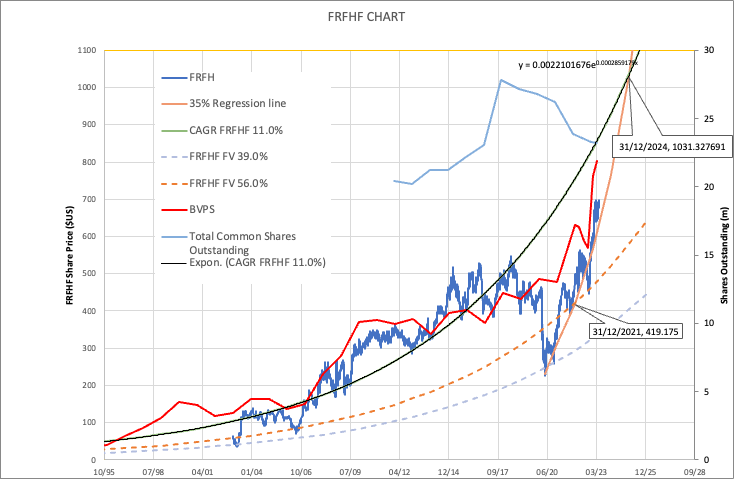

Based on this crude assumption, I remember the friendly arguments on the board at the time about whether it was cheaper in 2020 or 2021. Either way, if you thought the company was a regress to the mean type play, it was possibly worth $1000 by the end of 2024. At the time this seemed a little nuts, but it now looks like book value reaching $1000 is a very high probability. I dug out the graph back then and updated key metrics but not the original estimated regression to the mean line. The 35% CAGR regression is still intact, and book value is closing in again at 11%. Importantly share price is coming down with repurchases at prices less than book.

For our friendly analyst to arrive at a fair value price of only CAD790 per share assumes some pretty low growth rates and some big cat losses. However, if FFH is indeed an 11% compounder, over the longer term, then ultimately even Brett would have to capitulate and reprice Fairfax to at least 1.1x's book.

Morningstar has a fair value for Fairfax of C$730 = US$537/share. Fairfax shares are trading today at US$714. What can we learn from Morningstar's report on Fairfax? Unfortunately, I think we learn much more about Morningstar from this 'report' than we do about Fairfax. And it does not inspire confidence. If this organization can be so out of touch on Fairfax - is this representative of the quality of rest of their research?

----------

Why am I so bullish on Fairfax? Because I am focussed on the present and the future. Graham (the guy who taught Buffett) teaches us a stock is simply worth the present value of its future cash flows. Yes, the past matters... but what matters much more is the future.

The Morningstar report is focussed pretty much solely on the past. 2008. And 2010-2016. And this might generally be ok for most companies. But it does not work for companies where important things have changed. Turnarounds. And lots of important things have changed at Fairfax over the past few years. Things that already had a big, positive impact on earnings in 2021 and 2022. With much more to come 2023, 2024 and 2025.

This explains, at least partially, why it takes turnaround type stocks like Fairfax so long to re-rate. It takes years of better/excellent results before analysts and investors get comfortable that things have indeed changed in a sustainable way for the better. Only after the new and improved financial results are embedded in historical results for years does the ‘narrative’ change. This actually makes sense for a company like Fairfax that was so out of favor.

—————

What is Morningstar missing in their report? An analysis of Fairfax as it exists today: a company that is earning:

1.) record underwriting profit

2.) record interest and dividend income

3.) record share of profit of associates

4.) solid investment gains

While also reducing their share count.

They do not provide any detailed forward looking information and estimates. No detail of the important building blocks. No math. In sort, their analysis is exclusively backward looking. And as a result, worse that useless for a company like Fairfax (a turnaround).

----------

Conclusion: Fairfax, as it exists today, is misunderstood. Lots of analysts and investors are stuck in the past.

So what is an investor to do? Patience and time. Fairfax needs to deliver results. The narrative will slowly change and reflect the current reality. And Fairfax shareholders should be rewarded handsomely.

-

1

1

-

Historic Milestone

in Fairfax Financial

Posted · Edited by Viking

“Those who cannot remember the past are condemned to repeat it." (George Santayana)

Given it has come up in discussion on this thread, I thought this would be useful to review what has to be Fairfax’s biggest ever investment mistake: the equity hedges.

Why are they Fairfax's biggest investment mistake? The ‘equity hedges’ were in place from 2010 to 2016… and they caused investment losses of $4.4 billion; an average loss of $628 million per year for 7 straight years.

Shareholders equity in 2010 was $7.7 billion. So losing $628 million in ONE YEAR was a big deal. And, as a reminder, this happened, on average, for 7 straight years. Book value per share was $376 in 2010 and in 2016 it has fallen to $367. Yes, Fairfax did pay a $10/share dividend every year so shareholders did earn a positive return over these years.

Why did Fairfax put on the equity hedge trade? They were afraid “the North American economy may experience a time period like the U.S. in the 1930s and Japan since 1990.”

From Prem’s letter 2010AR: “2010 was a disappointing year for HWIC’s investment results because of the two factors mentioned earlier. Hedging our common stock investment portfolio cost us $936.6 million or $45.61 per share in 2010. Our hedging program masked the excellent common stock returns we earned in 2010, of which a significant amount was realized ($522.1 million). We began 2010 with about 30% of our common stock hedged. In May and June we decided to increase our hedge to approximately 100%. Our view was twofold: our capital had benefitted greatly from our common stock portfolio and we wanted to protect our gains, and we worried about the unintended consequences of too much debt in the system – worldwide! If the 2008/2009 recession was like any other recession that the U.S. has experienced in the past 50 years, we would not be hedging today. However, we worry, as we have mentioned to you many times in the past, that the North American economy may experience a time period like the U.S. in the 1930s and Japan since 1990, during which nominal GNP remains flat for 10 to 20 years with many bouts of deflation.“

Why did Fairfax exit the equity hedge trade? The US presidential election on November 8, 2016.

From Prem’s letter 2016AR: “Unfortunately, the presidential election on November 8, 2016 changed the world for us, so we reacted quickly by removing all our index hedges and some of our individual short positions and reducing the duration of our fixed income portfolios to approximately one year – all of which resulted in a $1.2 billion net loss on our investments in 2016 which, in turn, resulted in a loss in 2016 of $512 million or $24.18 per share.”

But our sad story does not end here because even though Fairfax exited all of their equity hedge positions late in 2016 they continued with some short positions. From 2017-2019, Fairfax lost another $514 million on short positions.

From Prem’s letter 2019AR: “In the past, to protect our equity exposures in uncertain times, we shorted indices (mainly the S&P500 and Russell 2000) and a few common stocks. After much thought and discussion, it became clear to me that shorting is dangerous, very short term in nature and anathema to long term value investing. As I mentioned to you in last year’s annual report, shorting has cost us, cumulatively, net of our gains on common stock, approximately $2 billion! This will not be repeated! In the future, we may use options with a potential finite loss to hedge our equity exposure, but we will never again indulge anew in shorting with uncapped exposure. Your Chairman continues to learn–slowly!!”

But even after the mea culpa above in 2019 shareholders learned in 2020 that there was still one last mystery short position on the books. Only after another $529 million in losses in 2020, did Fairfax finally come to the conclusion that shorting was a tricky business. Margin and unlimited losses can be a bitch, especially in a decade long bull market (S&P500 was 1,133 on Jan 1, 2010 and 3,756 on Dec 31, 2020).

And there we have it: Fairfax’s lost decade for shareholders from 2010-2020.

From Prem’s letter 2020AR: “I said in our 2019 annual report that we would not short stock market indices (like the S&P500) or common stocks of individual companies ever again, and our last remaining short position was closed out in 2020 (not soon enough, as it cost us $529 million in 2020).”

So as they began 2021, Fairfax shareholders were finally able to close the book on the whole ‘equity hedge/short’ trades.

What was the cost to Fairfax?

1.) Investment losses of $5.4 billion from 2010-2020, or $494 million per year on average.

2.) Additional significant opportunity cost - easily in the billions.

3.) The massive size of the losses each year likely warped capital allocation decisions, especially 2010-2016 when the losses were larger.

4.) Long lasting harm to Fairfax’s reputation in the investment community.

5.) Exit of many long-term shareholders.

What went wrong? The size and duration of the position. The losses were massive. And they were allowed to go on (pretty much) for 11 straight years.

What explains the mistake? No idea. But my guess is hubris.

Hubris Comes From Ancient Greece: “English picked up both the concept of hubris and the term for that particular brand of cockiness from the ancient Greeks, who considered hubris a dangerous character flaw capable of provoking the wrath of the gods. In classical Greek tragedy, hubris was often a fatal shortcoming that brought about the fall of the tragic hero. Typically, overconfidence led the hero to attempt to overstep the boundaries of human limitations and assume a godlike status, and the gods inevitably humbled the offender with a sharp reminder of their mortality.” Merriam-Webster

Will Fairfax make the same mistake again? Well this is where things get interesting. Fairfax has stated publicly numerous times that they won’t make that exact same mistake again. To the best of my knowledge, they have never discussed publicly the failures with their internal processes that allowed such flawed investment to be made (in such a large size and for such a long duration). Did they identify the internal failures? Have they made the internal changes necessary to ensure it (a terrible investment decisions that results in another lost decade for shareholders) does not happen again? I’m not sure… I do think something changed at Hamblin Watsa around 2018 - and for the better. Their capital allocation decisions for the past +5 years have been stellar. And that will be the subject of a future long-form post, so stay tuned.

Summary:

As shareholders, I think it is important that we discuss/remember not only Fairfax’s successes but also their failures. I call it 'eyes wide open'. The equity hedges were an unmitigated disaster for Fairfax and its shareholders. There is no way to put lipstick on this pig.

—————

Fairfax's 2016AR:

Prem’s Letter: "Unfortunately, the presidential election on November 8, 2016 changed the world for us, so we reacted quickly by removing all our index hedges and some of our individual short positions and reducing the duration of our fixed income portfolios to approximately one year – all of which resulted in a $1.2 billion net loss on our investments in 2016 which, in turn, resulted in a loss in 2016 of $512 million or $24.18 per share."

"When we removed our hedges near the end of 2016, we realized a loss of $2.6 billion in 2016, but that included $1.6 billion which had gone through our statements in prior years. As discussed earlier, since 2010 we have had $4.4 billion of cumulative net hedging losses and $0.5 billion of unrealized losses on deflation swaps (which we still hold), offset entirely by net gains on stocks of $2.7 billion and net gains on bonds of $2.2 billion. The volatility of our earnings caused by our hedges and long bond portfolios is over – and as I said earlier, we are focused on once again producing excellent investment returns."

Equity contracts

Throughout 2015 and most of 2016, the company had economically hedged its equity and equity-related holdings (comprised of common stocks, convertible preferred stocks, convertible bonds, non-insurance investments in associates and equity-related derivatives) against a potential significant decline in equity markets by way of short positions effected through equity and equity index total return swaps (including short positions in certain equity indexes and individual equities) and equity index put options (S&P 500) as set out in the table below. The company’s equity hedges were structured to provide a return that was inverse to changes in the fair values of the indexes and certain individual equities.

As a result of fundamental changes in the U.S. that may bolster economic growth and business development in the future, the company discontinued its economic equity hedging strategy during the fourth quarter of 2016. Accordingly, the company closed out $6,350.6 notional amount of short positions effected through equity index total return swaps (comprised of Russell 2000, S&P 500 and S&P/TSX 60 short equity index total return swaps). The short equity index total return swaps closed out in 2016 produced a realized loss of $2,665.4 (of which $1,710.2 had been recorded as unrealized losses in prior years). The company continues to maintain short equity and equity index total return swaps for investment purposes, and no longer considers them to be hedges of the company’s equity and equity-related holdings. During 2016 the company paid net cash of $915.8 (2015 – received net cash of $303.3) in connection with the closures and reset provisions of its short equity and equity index total return swaps (excluding the impact of collateral requirements).