glider3834

-

Posts

1,082 -

Joined

-

Last visited

-

Days Won

5

3 Followers

glider3834's Achievements

")

-

unfortunately I don't have a sub must have been a one off complimentary article

-

cheers gfp I suspect Exor could be larger for Fairfax overall - in the past they have split new equity investments between the different insurance subs here is a Barron's piece on Exor from earlier this year https://www.barrons.com/articles/buy-exor-stock-price-pick-ferrari-ef15ef21 interesting too given Jamie Lowry value investing presentation a few years ago

-

yep potentially

-

they look to be under 5% now on another tech stock Micron - by my estimate this was likely a double for Fairfax maybe around $200M profit or so a few years ago but they missed the big run up since Well the flip side on Micron I guess is 1. they are fishing in the right waters & 2. after they reduced Micron, they upped their Orla stake & we know that has worked out pretty well too Can't win them all hey

-

thanks gfp for your comments so would it be right to say, even where unrealised gain or loss for TRS, there is still a movement of collateral, held as restricted, which could be in the form of cash or T-bills either received from counterparty(TRS gains) or sent to counterparty (TRS losses) - is that right? And then I guess I was trying to get to the issue of taxation - do you think they would have different re-measurement dates & keep unrealized to defer tax?

-

thanks for posting - agree this is a must read

-

Looking at sedi filings it looks like Fairfax bought ~167K shares over Jan-Feb-26 and then looking at AR below, looks like they may have bought another ~59K in the first week of March. 'Subsequent to December 31, 2025, the company purchased for cancellation 226,694 subordinate voting shares under the terms of its normal course issuer bids at a cost of $384.0' AR2025

-

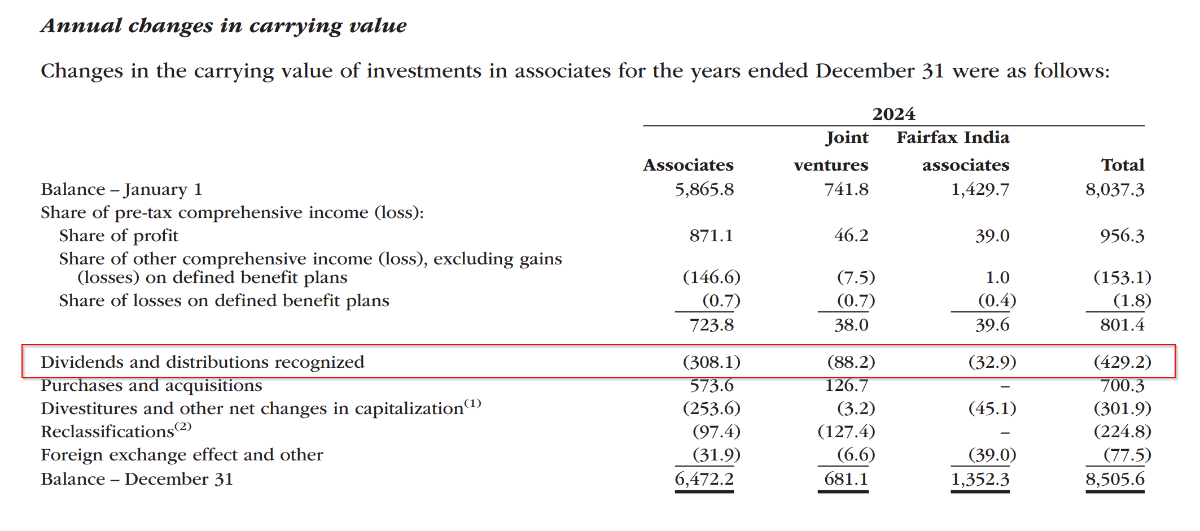

For India based non-insurance associates and share of profit, there are those that owned by Fairfax India and others owned via FFH. So p126 is showing share of profit for those under Fairfax India. Below is the split for share of profit for india non-insurance associates held by FFH and those held via Fairfax India

-

I don't think I totally answered your question with my post below - but I will keep it just in case others find it useful rather than delete and maybe have another look at your question. For the interest and dividends line, I believe these are dividends they receive on common and preferred stocks after investment expenses. Dividends from associates subtract from the carrying value of the associate investment and treated as return of capital, as you already recognise the share of profit from associate. For controlled subs as I understand, dividends are eliminated on consolidation to prevent double counting as they are an internal transaction and not external income.

-

I believe they repurchased less in '24 and '25 over same period and a little more around 62k in '23

-

'Eddie Bauer (the clothing brand) and Bauer Hockey (the equipment manufacturer) are not related. They are two separate, distinct companies founded at different times by unrelated individuals.' source - gemini

-

agree if approved then it would be similar to Digit Life where FAL directly owns shares ( but a different %) in Digit Life

-

Fairfax via FAL looking to secure majority control ownership of Digit Insurance via merger with Go Digit Infoworks, subject to regulatory approvals/shareholder vote https://www.godigit.com/content/dam/godigit/general/investor-relations/stock-exchange-disclosures/board-meeting-outcome-19-12-2025-and-press-release.pdf 'Until the Digit Insurance company and holding company are merged, we have not reflected the mark-to-market gain on our 49% of common shares in Digit ($110 million as of December 31, 2024).' (AR 2024)

-

another consideration looking at price to book, ROE and what is appropriate multiple is to consider over the last 7 years the goodwill & intangibles portion of book value for Fairfax's 5 largest insurers has actually been reduced in aggregate, due to acquisition related accounting eg amortization of customer relationships - even though these businesses have grown significantly.

-

Seaspan/Poseidon Maybe moving into ethane carrier space - looks to be MOU at this stage https://www.tradewindsnews.com/gas/seaspan-mulls-billion-dollar-order-for-up-to-six-vlec-newbuildings/2-1-1904696