giulio

-

Posts

298 -

Joined

-

Last visited

-

Days Won

2

3 Followers

Recent Profile Visitors

2,892 profile views

giulio's Achievements

")

-

I am not sure about USD vs CAD conversion, still crazy to me.

-

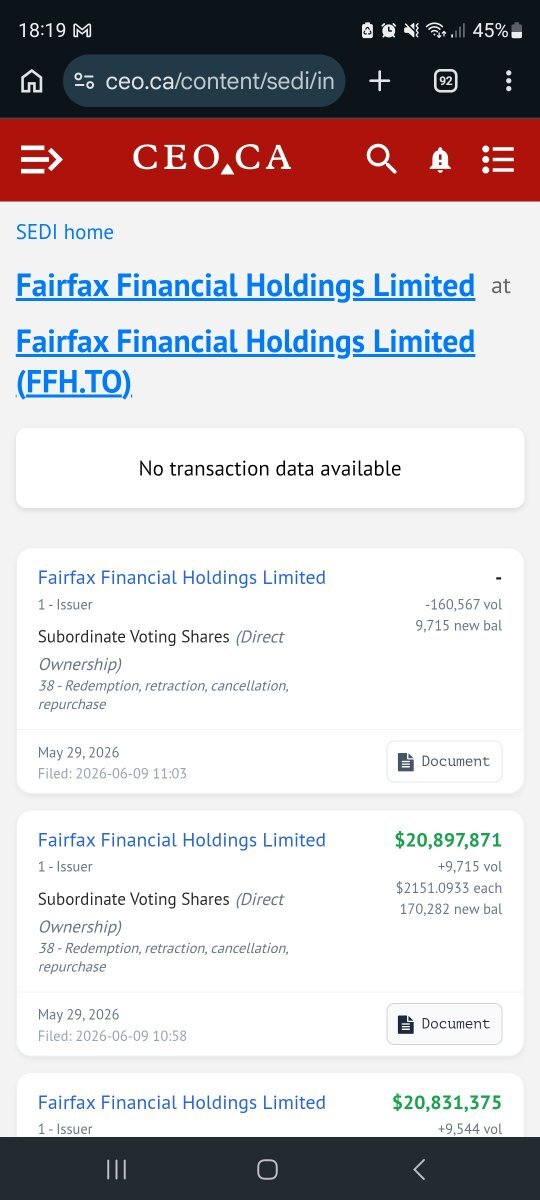

https://ceo.ca/content/sedi/issuers/2458 FFH did a 1B tender offer in 2022, financed by selling 10% of Odyssey. Another 1B bought back in 1 day in 2026 under their NCIB. Crazy.

-

I bought Panthera Resources (PAT - LSE), <1% position, essentially a lottery ticket on the results of their litigation process against India. $70M mkt cap, litigation claim is $1.6B but it will updated since gold price is ~25% higher now than when they filed initially. From what I read, they should have a strong legal basis. They are backed and fully funded by LCM (litigation capital management) who are highly selective in the cases they agree to support and have a good track record. Final hearing in Jan 2027, expected outcome announced by end of 2027. Wish me luck!

-

170k bought back, 160k cancelled

-

If you write an email to Watsa to complain about the Micron sale, don't forget to cc Li Lu!

-

You were absolutely spot on. I used fih 30.4% stake and 15crore (after tax as reported in the article I linked). 43.6% is held by Anchorage, I assumed they got the rest. I am looking forward to know how they financed the increased stake in IIFL capital...

-

https://economictimes.indiatimes.com/industry/transportation/airlines-/-aviation/bengaluru-airport-operator-bial-hands-over-rs-16-crore-dividend-to-karnataka-govt-arm/articleshow/131309196.cms?from=mdr BIAL paid a dividend of Rs3 per share. FIH share should be $3.6M.

-

https://www.hindustantimes.com/india-news/centre-looks-to-revive-stalled-idbi-bank-sale-process-report-101779091726437-amp.html Efforts are underway to make a deal feasible, including setting a price that captures the bank’s intrinsic value and lowers the reliance on its share price, the people said

-

Small adds to stvn, tdg and fih

-

I hope the image is readable. Just wanted to highlight that CR for FFH has been in very good shape since at least 2013 (I don't track earlier years), with the exception of 2017 (big acquisition). What many cite is that since 2020 BOTH underwriting profits and investment gains have been performing pretty well. @Viking maybe rates stay around where they are? + or - 50bps? It's also a possibility...ECB is about to raise rate apparently!

-

2.5% position in TDG, starter, hoping results tomorrow don't move the price too much on the upside (TDG pre announce in april)

-

Director Lauren Templeton speaking at Guy Spier's events during Brk weekend. starts at 5.05.00

-

As far as I am concerned, all your points are valid and well articulated. I am sure other posters find them useful as well: this is a discussion forum and if we all agreed with each other it wouldn't be fun and the learning opportunities would be far less. If FIH is a big position for you, you should definitely attend the AGM and voice your concerns, just don't go there with the expectation to hear the answers YOU want. I understand your frustration but there's not much the COBF can do, just sell it and be "psychologically short" a la Ackman. FWIW, I sized the position taking into account positives and the negatives and I am not in love with the stock: if the upside materializes great (I might trim it, keep it at 5% and redeploy proceeds elsewhere), if not I'll just sell and move on without losing money and a second of sleep. 3 years ago I bought VW and Porsche Holding thinking there was 4x upside, limited downside thanks big cash balances and a family willing to surface value through buybacks, spinoffs, costs cuts and dividends. I lost 50% but the position was sized appropriately and didn't impact returns too much. I took the loss, learned my lessons and bought other stuff. I encourage you to keep posting your analysis and discuss ideas. Just keep a joyful and playful attitude, we are blessed to be able to do this! Best, G

-

FIH put $300M in Sanmar in 2016 through bonds at 13%. they were redeemed for 434M in 2019. FIH then reinvested 217M and finally sold their stake for 27M. The loss is ~60M overall. Terrible investment, big opportunity costs but less bad than it might seem. My guess is Sanmar would have required additional liquidity (as reported in AR 2025) and equity injections due to their debt level. Their raw materials costs possibly spiked up given the Iran war and higher oil prices. IMO, FIH did well in taking the L and moving on. You can't get them all right!