Viking

-

Posts

4,689 -

Joined

-

Last visited

-

Days Won

35

Content Type

Profiles

Forums

Events

Posts posted by Viking

-

-

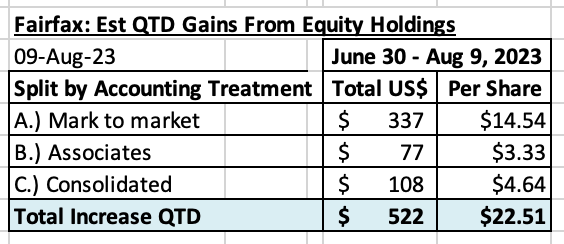

@nwoodman , your post on Thomas Cook motivated me to do an update.

As of Aug 9, Fairfax's equity holdings (that I track) are up about $522 million ($22.51/share) so far in Q3. Great start to the quarter. Split by accounting treatment can be seen below. I have attached my Excel file if you want a closer look.

Top 5 Movers? All up this quarter:

- FFH TRS = $169 million

- Eurobank = $108 million

- Thomas Cook India = $102 million

- John Keells = $51

- Mytilineos = $33

-

6 hours ago, backtothebeach said:

Great work! It's eye-opening to see how much information is actually out there about a company's dealings, if one reads absolutely everything available. I assume you are not only reading FFH's filings, but also filings of a long list of companies they are involved with, press releases, maybe even court cases, and who knows what else. Doing that over years/decades and keeping track of all of it...amazing. Thank you for sharing it so generously!

One aesthetic point, the disclaimer in the footer "This document is not intended to be financial advice. Its purpose is to educate and entertain." on every page is the same size as the main text and very close to it, so it kind of interferes with the reading. Maybe make it half size, a different font, and a bit further from the text.

@backtothebeach Yes, I also found the footer to be annoying. I changed the footer as you suggested. I also did a re-write of Chapter 1, making the information current. Scroll up to the first post in this thread to view the new (updated) PDF file. Please keep the suggestions for improvement coming.

-

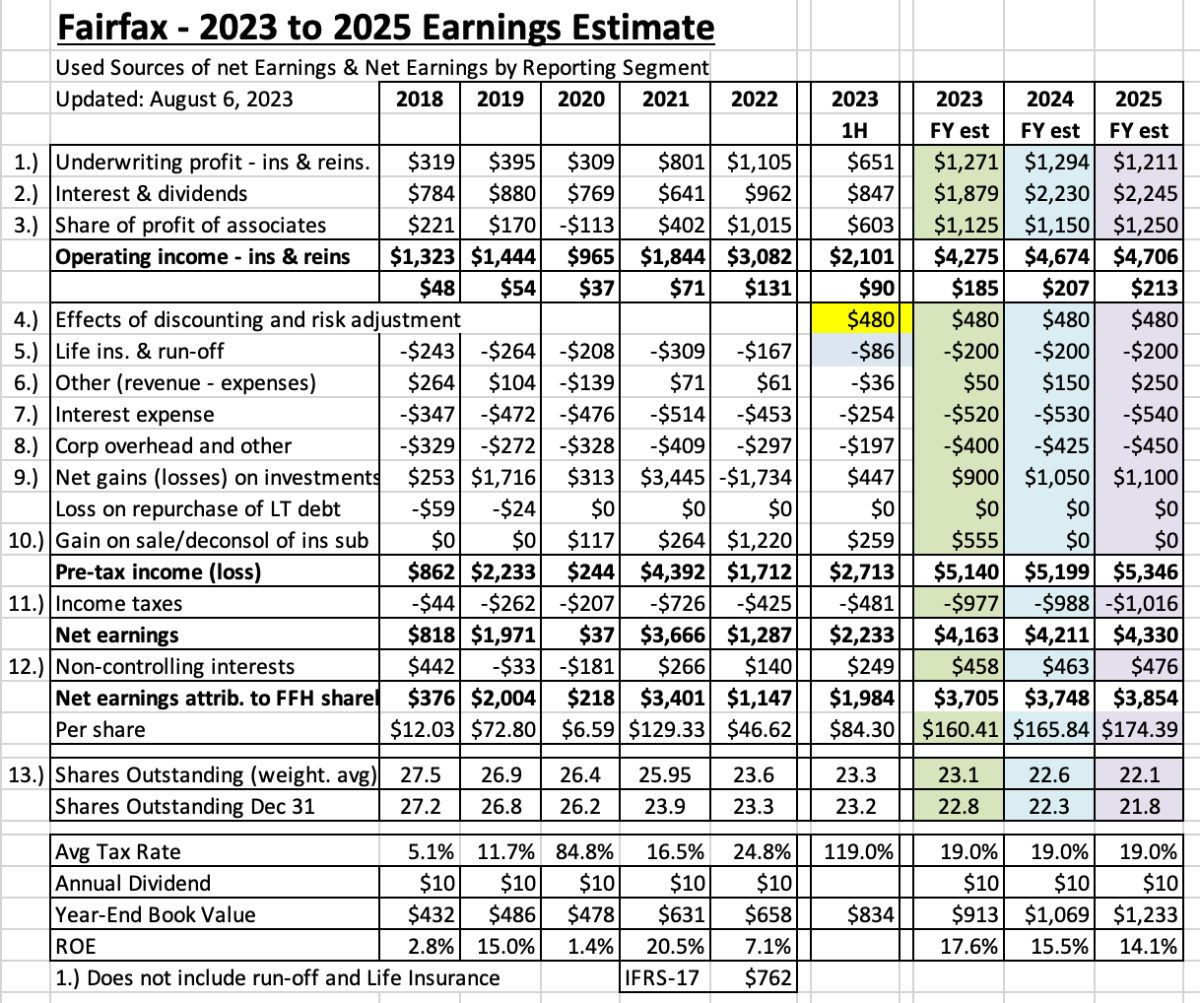

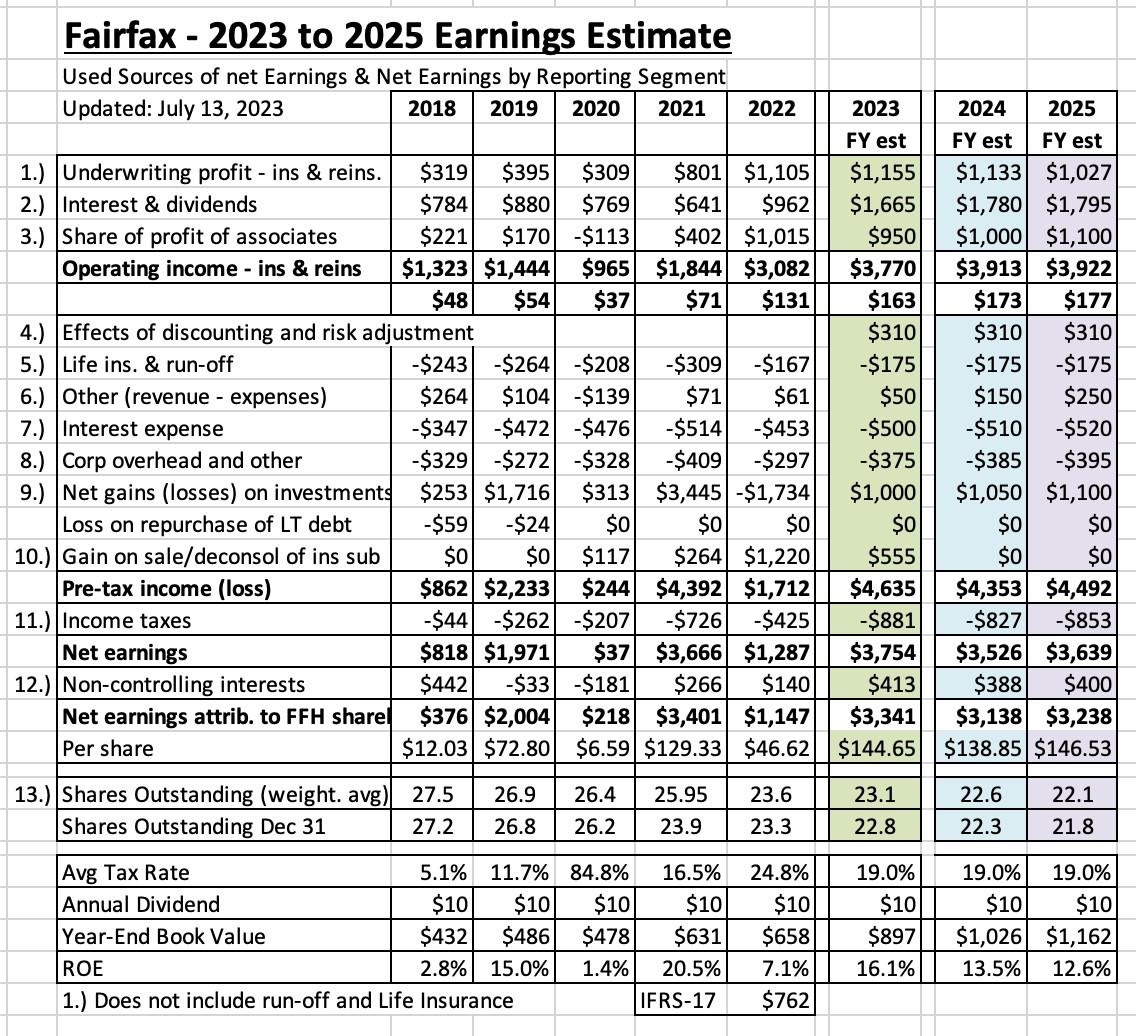

Fairfax just reported Q2-2023 results. The surprise for me? Underwriting profit, interest and dividend income and share of profit of associates all came in higher than I expected.

As a result, I decided it was time to update my earnings estimates for Fairfax for 2023, 2024 and 2025. I have the highest confidence level in my 2023 forecast. My 2025 forecast is largely an educated guess. A lot can change in 2 years (both good and bad). Please keep this in mind as you are reading.

Conclusion:

Let's skip ahead to the conclusion. My rough estimate is Fairfax will earn about $160/share in 2023. This is up from my last estimate which was $145/share (made in early July). The increase reflects the better-than-expected operating earnings Fairfax reported for Q2.

For 2024, my new estimate is $166/share and for 2025 it is $174/share.

The big ‘miss’ with my estimates in 2024 and 2025 is likely capital allocation. We don’t know what the management team at Fairfax is going to do with all the earnings (around $3.6 billion) that is likely coming in each of the next 2.5 years. Looking at the last 5 years, the management team has been outstanding with capital allocation. My guess is they will continue to make good decisions (on balance) and this will benefit shareholders - providing a possible tailwind to my forecasts.

I am also assuming interest rates remain roughly at current levels. Of course, this will not be the case. But if rates rise - or go lower - Fairfax will have lots of puts and takes.

Below is an 8-year snapshot for Fairfax. It communicates in a concise manner dramatic transformation that has happened at this company, beginning in 2021. It is a pretty amazing story.

What are the key assumptions?

1.) underwriting profit: Estimated to increase to a record $1.3 billion in 2023.

- I am forecasting Fairfax’s combined ratio (CR) to remain flat at 94.5 in 2023 (the same as 2022).

- When the Gulf Insurance Group transaction closes in 2H-2023, Fairfax should get a nice boost to its insurance business. I think GIG will add about $1.7 billion to net written premiums, which should drive low double-digit top-line growth in 2024.

- The hard market will end at some point. But do things quickly turn ugly? Probably not, but I am not sure.

2.) interest and dividend income: Estimated to increase to a record $1.9 billion in 2023.

- The average duration of the fixed income portfolio was increased to 2.4 years in 1H-2023.

- GIG should add about $2.4 billion to the total investment portfolio.

- PacWest loans will deliver incremental interest income (of $80-$90 million?), with half coming in 2H-2023 and the other half in 1H-2024.

- Eurobank: the plan is to start paying a dividend in 2024. If this happens, we might see dividend income increase by $40 to $50 million.

- Potential headwind: Short-term treasury rates might come down in 2024. If this happens, interest income on cash/short term balances could fall.

3.) Share of profit of associates: Estimated to increase to a record $1.1 billion in 2023.

- Earnings at Eurobank, Poseidon/Atlas, EXCO, Stelco and Fairfax India, in aggregate, should continue to grow nicely.

- 2023 headwind: Sale of Resolute Forest Products - Contributed $159 million in 2022.

- 2024 headwind: I estimate GIG will contribute $100 million in 2023. When Fairfax’s purchase of Kipco’s stake is approved the financial results for this holding will be reported with Fairfax’s insurance operations. In anticipation of this deal closing later in 2H-2023, I removed $100 million from my 2024 estimate.

4.) Effects of discounting and risk adjustment (IFRS 17). Interest rate changes drive this bucket. My estimates here could be a little messed up. Given I am forecasting interest rates to remain about where they are today, I am leaving this number the same over the forecast period (at my estimate for June 30, 2023).

5.) Life insurance and runoff. This combination of businesses lost $167 million in 2022. I am forecasting this bucket to lose $200 million in each of the next three years.

6.) Other (revenue-expenses): improving results from consolidated holdings.

In the near term, we could get write downs in both Boat Rocker and Farmers Edge. With Covid in the rear-view mirror, earnings at Recipe could move higher ($100 million per year?). Earnings at Dexterra are growing again. AGT is a sleeper holding. Grivalia Hospitality is in its peak investment phase; earnings could grow nicely looking out a year or two. This bucket is poised to grow nicely for Fairfax in the coming years.

7.) Interest expense: A slight increase.

8.) Corporate overhead and other: A slight increase.

9.) Net gains on investments: Estimated to come in around $900 million in 2023.

- My estimates assume (this is very general):

- Mark-to-market equity holdings of about $7.8 billion increase in value by 10% per year, or $800 million.

- A small bump of $200 to $250 million per year for additional gains (equities and fixed income).

----------

My estimated total return on the investment portfolio for each year is as follows:

- 2023 = 8.0% = $4.5bn / $56bn

- 2024 = 7.6% = $4.5bn / $59bn

- 2025 = 7.8% = $4.7bn / $61bn

What is the math? For each year, add the following line items: 2.) + 3.) + 6.) + 9.) and divided the total by the estimated value of Fairfax’s investment portfolio. These estimated annual percent returns, while high compared to recent years, are driven largely by the spike in interest and dividends and share of profit of associates.

----------

10.) Gain on sale/deconsol of insurance sub: This is a wild card.

This is where I put the large asset sales. In 2022, it was the sale of pet insurance business. In 2023, it was the sale of Ambridge and the pending purchase of GIG (resulting in a write-up of the existing holding).

For 2024 and 2025, I estimate no gains from sales/write up of assets. There could be something:

- Perhaps we get a Digit or AGT IPO.

- Perhaps Fairfax sells another holding for a large gain.

This ‘bucket’ is perhaps where I will be most wrong with my forecast. Developments here will likely have a material positive impact to Fairfax’s reported results (earnings and book value).

11.) Income taxes: estimated at 19%

12.) Non-controlling interests: estimated at 11% (not really sure)

13.) Shares Outstanding: Estimated that effective shares outstanding is reduced by 500,000 per year. This is in line with a normal year from Fairfax.

Notes:

- Underwriting profit: Includes insurance and reinsurance; does not include runoff or Eurolife life insurance.

- Interest and dividends: Includes insurance, reinsurance and runoff.

-

@StubbleJumper and @Tommm50 , great comments. I have said many times, i am not an insurance guy. So i really appreciate hearing from those who work(ed) in the industry. I appreciate the colour. And please point out the flaws in my logic in my posts… otherwise i will just keep repeating my mistakes. Thank you.

-

12 minutes ago, StubbleJumper said:

Mr. Market likely doesn't believe that EPS of $150 is sustainable. Your EPS of $150 contains $60 of underwriting income which can disappear pretty quickly if capital flows into the industry, and the $100 of interest can turn into $75 by 2027 if the fed moves away from it's tightening process and instead adopts a loosening posture.

FFH will almost certainly have 2 or 3 good years of income and its share price likely has some distance left to go, but we need to attenuate our long-term expectations. Ignore the PE ratio entirely when you are at the top of the insurance cycle. Instead develop a forecast of BV for December 2025 and select what you believe is an appropriate multiple of book for a company that is selling a commodity product (insurance policies) in an industry with minimal barriers to entry. That BV multiple should likely be one of 0.8x, 0.9X, 1.0x, 1.1x or 1.2x. As a point of interest, CAD$1375 is roughly 1.2x...

SJ

@StubbleJumper i have enormous respect for your knowledge about all things insurance. So please keep the comments coming. I agree there is a risk that the hard market could quickly reverse and become a shit show - which would hit underwriting income. But what is the probability of that actually happening? My understanding is when the last hard market ended things went sideways for 3 or 4 years - it did not deteriorate into a shit show. My point is risks need to be considered. And probabilities attached.

Insurance companies are laser focussed on generating an acceptable return for shareholders. Pricing (rate increases) look like it actually accelerated a little higher in Q2.

With my estimates/forecasts i lean heavily on what i think i know. That is why i only like to look out about 2 years. As new information becomes available i will make updates.

-

2 hours ago, StubbleJumper said:

On that point, historically they would be correct. The insurance cycle is self-correcting to the extent that attractive profits have always attracted new capital which subsequently made the attractive profits disappear.

I will write once again what I wrote in January. If you give one of FFH's subs an extra $1 of capital, they can use it to write $2 of premium. That $2 of premium will earn 12-cents underwriting profit for the sub (Q2 CR=94). As we all know, the sub collects the premium long before it pays out an indemnity, so it gets float for a year of probably roughly $1 from writing those $2 of premium. The incremental $1 plus the original $1 of capital that you gave the sub can be invested today in a boring 12-month US treasury which closed Friday at 5.29%. So, in total, that incremental dollar of capital that you gave the Fairfax sub can earn about 22.58 cents of operating income.

The profitability is ridiculous. A 20%+ margin will eventually attract new capital to the industry. As it always does, new capital will eventually push down underwriting profitability. There's a reason why Prem expressed a degree of surprise during the conference call that this hard market has endured as long as it has, and that new capital does not seem to be flowing into the industry.

That being said, FFH has a few years of strong profits baked in. There will be at least 2 or 3 good years of profits, but understand that it will not continue forever. I see some truly enthusiastic valuation levels being proposed on this board for a company that sells a commodity product with few barriers to entry. There's still room for the price to run, but that will be mainly from the earnings that will be retained over the coming 2 or 3 years rather than some marked increase in fundamental valuation.

SJ

@StubbleJumper i agree that the insurance market will soften at some point in the future. I also think the investment side of Fairfax is being underestimated. Investors don’t know what they are going to do with all the cash that will be rolling in so they are very conservative with their return estimates from investments. My big miss with Fairfax the past couple of years is how well they are executing on the capital allocation front and the impact that is having on earnings. As a result my past earnings estimates (looking foolishly high when made) have been too conservative. I expect Fairfax will continue to allocate capital well in the coming years. My guess is increasing returns from investments will more than offset any slow down in underwriting profit looking out a few years. -

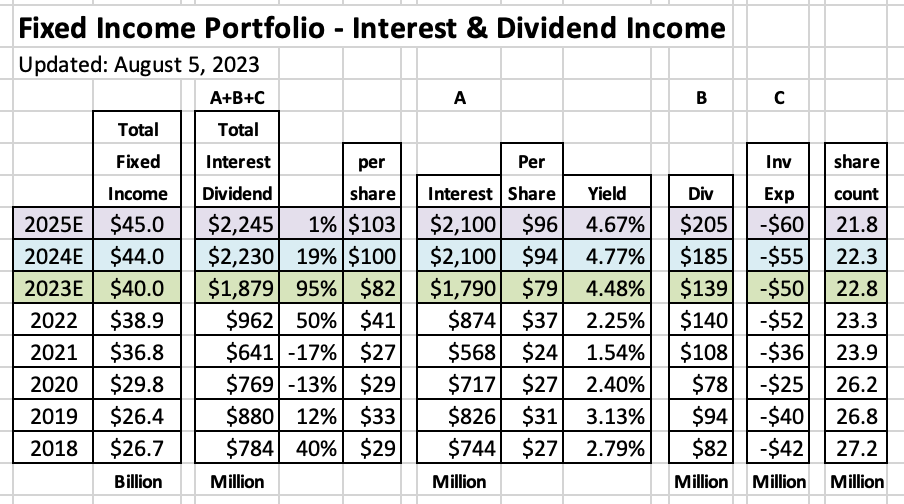

The key to forecasting is getting the ‘big rocks’ right. From an earnings perspective, there is no more important item to Fairfax today than ‘interest and dividend income.’ This one ‘bucket’ now represents about 40% of Fairfax’s total pre-tax earnings. Next year it could be as high as 45% of pre-tax earnings. So, if we can get can get our estimates for this part of earnings modelled properly we should be well on our way to coming up with a quality earnings estimate for the company as a whole.

When looking at ‘interest and dividends’ for Fairfax, dividends represent about 7% of the total. Interest income represents about 93% of the total, so that is what we are going to focus on.

Two items drive interest income:

- The size of the fixed income portfolio

- The average yield earned on the investments held in the portfolio

It is quite simple. It is relatively easy to calculate. It is not volatile quarter to quarter. And it is predictable, looking out a couple of years. This is why ‘interest and dividend income’ is considered the highest quality source of earnings for an insurance company.

So, let’s look at Fairfax and see what we can learn.

How big is the fixed income portfolio at Fairfax and how fast is it growing?

The fixed income portfolio at Fairfax is about $40 billion today. In 2016, it was $20.3 billion. Over the last 7 years, the size of the portfolio has doubled, which is growth of about 10% per year.

Growth in 2024 should be similar (at 10%, or $4 billion). The GIG acquisition will add around $2.4 billion to investments when it closes later this year. Earnings are coming in strong and we are still in a hard market, which should also support modest growth of the fixed income portfolio in 2024.

Next, let’s review the average yield.

From 2016 to 2022, Fairfax earned an average of about 2.4% on its fixed income portfolio (see chart below). Yes, that is a low number. Fairfax has been very conservative with the positioning of their fixed income portfolio over the past 7 years (low duration and high-quality holdings).

What about 2023? The average yield in 2023 is estimated to be about 4.5%.

What about 2024? The average yield in 2024 is estimated to be about 4.8%.

The average yield that Fairfax is earnings on its fixed income portfolio has doubled.

This is important:

- The size of Fairfax’s fixed income portfolio has doubled over the past 7 years.

- At the same time, the rate of return that Fairfax is earnings on its fixed income portfolio looks like it is also poised to double.

Investors are getting served up a double-double with Fairfax’s fixed income portfolio (that line will only make sense to Tim’s coffee drinkers).

What does it mean for Fairfax?

Interest income is poised to increase from $514 million in 2016 to an estimated $2.1 billion in 2024. That is a 300% increase over 8 years. Exactly what you would expect when the size of the portfolio doubles and the rate of return also doubles.

Average duration

In the first quarter we learned that Fairfax had materially extended the average duration of their fixed income portfolio and as of June 30, 2023, it was at 2.4 years (from 1.6 years at Dec 31, 2022, and 1.2 years at Dec 31, 2021). This is important because it locks in the rate of return on a large part of the portfolio for a couple of years making the earnings stream more durable.

What does this mean for investors?

The most important bucket of earnings for Fairfax (for a P&C insurer), interest and dividend income, is poised to deliver a record amount in 2024. And 2025 looks promising as well.

Efficient Market Theory

Of course, everything I have written above is from publicly available information. So, it is priced into the share price of Fairfax’s stock today. Right?

Fairfax’s Price Earnings Ratio = 5.6 = $843 / 2023 $150E per share (as of Aug 4, 2023)

My current estimate (another word for guess) is Fairfax could earn about $150/share in both 2023 and 2024 (that will be the topic of a future post). Given my analysis of interest income above, I trust my earnings number (please note, that doesn’t mean you should!).

So, the appropriate question for me to ask: “is 5.6 an appropriate multiple to pay to get $150 in estimated earnings from Fairfax.” Mr. Market thinks so. I disagree. I think the multiple is too low. My guess is Mr. Market does not yet fully grasp the significance of what a fixed income double-double means for the future earnings of Fairfax.

Dividends

- Extending its close partnership with Kennedy Wilson (KW), Fairfax also invested $200 million in preferred shares of KW with a 6% dividend. This will deliver an incremental $12 million in dividend income to Fairfax each year.

- Eurobank would like to start paying a dividend, likely in 2024. As a result, I have added $40 million in dividends to my forecast for 2024.

Interest & dividend income = interest income + dividend income - investment expenses.

—————

Interest rates are once again moving higher

Interest rates have moved higher in recent months. As a result, Fairfax will have the ability to continue to re-invest maturing bonds at higher yields. This suggests interest income has not peaked.

-

4 hours ago, StubbleJumper said:

No. He's likely not part of an old shorting club, but more likely an analyst who is trying to intelligently publish opinions on 40 or 50 different stocks and cannot do a credible job of any of them. The investment losses that preoccupy him are a nothing as they are mainly unrealized losses on bonds that will be held to maturity, and thus will reverse over the next 2 or 3 years, irrespective of what happens to interest rates over that time. The other thing to ignore are the IFRS 17 discounting issues as they too will reverse over a few years (there is no economic significance to them). And then the Farmers Edge charge is the third thing to ignore as that reflects a bad decision made five years ago or so. None of those things make a whit of difference about the economic value of the company on a going-forward basis, but I understand how an analyst who cannot invest adequate time in the company might view those items as significant.

SJ

@StubbleJumper i agree with everything you said. There are a few analysts out there who clearly do not follow Fairfax all that closely. But they are at least smart enough to raise their price targets over time (to reflect improving quality of earnings). The problem with Morningstar is they are sticking with C$790/share fair value estimate for the stock. That makes them look like idiots. It reflects badly on Morningstar as a company. RBC uses Morningstar as part of its research coverage offered to investors. So it also makes RBC look foolish, given Fairfax is a very large Canadian company.

The solution is for Morningstar to end coverage of Fairfax. But to @Parsad ‘s comment, some investors probably make decisions based on what companies like Morningstar have to say - and that just creates fat pitches for other investors. So i guess i should welcome their idiocy.

-

6 minutes ago, John Hjorth said:

Thank you for what is to me a gem! -Yes, it's contextual, but still a quite comprehensive write-up on an Insurance company, that is actually quite complicated.

One question here for both Lars [ @Viking ] and Sanjeev [ @Parsad ] : I suppose it's intentional, that non-CoBF members [so called CoBF guests] can download the attached file in the starting post of this topic, right? [Actually, that is not an obviousness to me personally.]

@John Hjorth thank you for your comments.

To answer your question, yes, guests can download the PDF file for free. That is why the post was put in the Books thread. Making the file available for free was very important to me - its goal is to educate and entertain. To do this it also needs to be accessible to all. Hopefully it pulls more investors to this wonderful forum and motivates them to become active, contributing members.

-

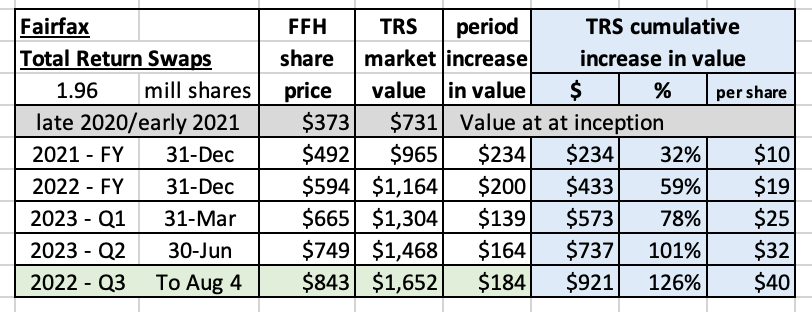

The movie 'Groundhog Day' keeps playing out for Fairfax shareholders and the Total Return Swaps. Another month has gone by and Fairfax is once again sitting on another big unrealized gain for this position. Five weeks into Q3 the position is up another $184 million, or $8/share.

The cumulative gain on this one investment is now about $921 million, or $40/share (pre-tax) in 32 months. Well, Bill Murray does get the girl in the end. Fairfax shareholders are making out pretty good themselves.

----------

Let's try and conceptualize what this size of a gain means for an insurer like Fairfax.

Fairfax has earned an average of $345 million per year on this investment since inception. Most insurers invest primarily in fixed income instruments. What size of a fixed income portfolio would Fairfax need to earn $345 million per year in interest income? With a yield of 4.5%, Fairfax would need a fixed income portfolio of $7.7 billion to generate $345 million in interest income.

So the TRS position the past 32 months has generated a return equivalent to a $7.7 billion fixed income portfolio. That is insurance speak for 'holy shit!'

For perspective, WR Berkley had a total investment portfolio of $22.9 billion at Dec 31, 2022; Markel was $27.4 billion. So $7.7 billion is a big deal. The TRS position is definitely punching above its weight for Fairfax right now.

And the success of the TRS position demonstrated the power of Fairfax's business model when it comes to investing versus a traditional insurer. At least when it's working, like The TRS position has been for the past 32 months.

Tax treatment: does anyone have any insight on the tax treatment of interest income and gains from a TRS?

What is the TRS-FFH investment?

In late 2020 and early 2021, Fairfax purchased total return swaps giving it exposure to 1.96 million Fairfax shares with an average notional amount (cost) of US$373/share.

At the time, Fairfax had about 26.2 million effective shares outstanding, so this investment represented 7.5% of the company’s shares. Effective shares outstanding at the end of Q2, 2023 dropped to 23.2 million so this investment now represents 8.4% of the company’s shares.

-

Updated June 23, 2024

I have completed another update of my book/collection of posts on Fairfax. I am calling this version ‘Second Edition’ because it has lots of updates from the last one published in early April. I am also changing the sub-title to ‘Emergence of a Wonderful Company’ because I think it better captures Fairfax as the company/opportunity exists today (and where it is going). The original version was published 10 months ago and had 14 chapters and 192 pages. Volume 2 has 17 chapters and +400 pages of information/analysis on Fairfax.

I have also made some structure changes:

- Much of Chapter 1 (intro to Fairfax) has been changed. Most of the repetition is gone.

- Chapter 2 (earnings estimate) has been completely updated and edited.

- I added a new Chapter - for misc topics.

- A number of posts have been moved to different chapters (that better capture their content).

- I have edited some of the titles to make them easier to understand when reading the table of contents.

- Any new content from the past 2 months (since the last update) has been added.

Please note, not everything in the book has been brought up to date to June 2024. That would have required a couple of months of work… and by the time it was done, much of it would be out of date again. My current plan is to keep updated parts of the document as time goes by. It continues to be a working document for me.

The bottom line, this document should be a much better resource for board members / investors than what existed before. I hope you find it useful.

Viking

---------

For members who enjoy reading my posts on Fairfax I have attached at the bottom of this post two documents:

1.) Fairfax - The Emergence of a Wonderful Companyt: PDF file contains about 80 of my best posts on Fairfax, organized into 17 chapters (now +400 pages long).

2.) Excel workbook: companion document to the PDF file, contains 11 worksheets (see below for details).

Sanjeev, thanks for everything you do running this board. For all the members on this investing forum, ‘thank you’ for breaking bread on a daily basis and sharing your thoughts on investing and life. Over the years, it has been a life changing experience for me and my family. What is contained in this document is the collective wisdom of this group. Let’s hope i have captured it reasonably well.

I always appreciate getting some feedback… maybe one or two things you like and one or two things you don’t. What is missing? Thank you.

A message from the legal department: Both documents are incomplete and contain errors. What is contained in the attached documents is not intended to be investing/financial advice. Its purpose is to educate and entertain.

-----------

The Excel file contains 11 worksheets:

1.) FFH-23: lists and tracks many of Fairfax's equity holdings in real time

2.) Size: ranking of Fairfax's equity holdings by size

3.) Moves: detailed compilation of many on Fairfax's transitions going back to 2010 - organized by year4.) 23 Earn Est: detailed 2023 earnings estimate

5.) Premiums: the build for 'underwriting profit'

6.) Interest: the build for 'interest and dividend income'7.) Associates: the build for 'share of profit of associates'

8.) Consol: Non-insurance Consolidated Companies

9.) Investments: the build for return on the total investment portfolio

10.) Shares: reviews 'effective shares outstanding'

11.) Float: the build for float

12.) 13yr View: A 13 year view of many key metrics for Fairfax

13.) IFRS 17: Effects of discounting and risk adjustment - quarterly summary of build

-

1

1

-

-

3 hours ago, nwoodman said:

Best to stay reasonably conservative. Who really knows what Poseidon is worth as a highly leveraged capital-intensive business in a world with more normal interest rates. Given their massive drop in earnings, a $400 million haircut over "fair value" doesn't sound too outrageous to me.

Q1 23 $50.1m vs $49.7 Q1 22

Q2 23 $6.3m vs $72m Q2 22

Q3 $58m Q3 22

Q4 $78m Q4 22

Total $258 FY 22

The earnings release had this to say

"Share of profit of Poseidon (formerly Atlas) decreased to $6.3 million from $72.0 million due to higher interest expense, interest rate hedging losses (compared to hedging gains in the prior year) that fluctuate quarterly, and transaction costs related to the first quarter privatization of Poseidon. The company expects Poseidon’s earnings will normalize throughout the year."

Hopefully, this gets discussed in the CC.

@nwoodman Atlas has been my watch-out for a while. Unlike Fairfax, they appeared unprepared for higher rates. Head scratcher for me. I am pretty sure Eurobank had some hedges or something so they actually benefitted from higher rates early in 2022 - my thinking at the time was someone from Fairfax got to them and Eurobank got positioned properly. But Atlas… disappointing. I am not concerned. Its just a step back for the business - before they continue to move forward. Thank god they are a private company where it is much easier to take the medicine and get on with it. -

2 hours ago, SafetyinNumbers said:

Great highlights Viking. Trevor Scott pointed out that Fair Value of Associates over Carrying Value has grown to $33/share and adds it to BV to get what I’m calling adjusted book value (ABV). On that measure ABV grew from $822 to $867 which is more than it’s been in a very long time and was very recently very negative. Given how cheap Eurobank and FIH are alone, I expect this number to keep growing. I think it will be easy for PMs to justify paying over IFRS book value if they can point to ABV and I think they will be absolutely right to do so. It probably has better correlation to the stock price too.

@SafetyinNumbers that is a great point. The difference between fair value and carrying value for associate and consolidated holdings is significant and should be included in the discussion of BV. Additional margin of safety. -

2 hours ago, AlwaysDay1 said:

@Viking if I understand correctly you are saying that they will be able to roll their bonds at higher yields now. How does the interest from this behavior differ from the "dividend and interest income" of 500m per quarter? Where is this latter interest/dividend income from? Is it not from fixed income securities? Thanks.

@AlwaysDay1 my writing is a little unclear at times… i am saying 2 things will likely bump interest and dividend income to over $500 million in Q3:1.) incremental interest earned from $1.8 billion PacWest portfolio

2.) incremental interest earned from bonds that mature and are rolled over at higher maturities

-

2 hours ago, LC said:

Viking, I think they mentioned 10% percent on the new 1.8b mortgage bonds- so maybe more like 45m per q in incremental interest?

Also, do we know if they have extended duration on the bond portfolio?

@LC here is my logic. 10% on $1.8bn = $180mn. But we need to net out what they were earning on the $1.8 billion previously. My guess is 5% = $90 million. So we get $90 million in incremental earnings. Some of this will be investment gains (not dividends) as the bonds were purchased at a discount. So my guess is incremental interest and dividend amount will be $80 million or $20 million per quarter.I didn’t come across the dividend amount. Please share (if anyone else knows).

-

1 hour ago, glider3834 said:

pretty decent jump on consolidated interest & dividends $464M in Q2 ( vs $382M Q1)

That was the number that slapped me upside the head when i was reading… WOW! -

Great quarter. Boring. But let’s look under the hood to see what we can learn. Here are three key takeaways:

1.) interest and dividend income = $464.6 million. This is now running at $1.86 billion/year. This does not include:

- the higher interest income from the $1.8 billion in PacWest loan portfolio. This closed late in Q2. My guess is this will add $20 million per quarter to interest income.

- as bonds continue to mature, Fairfax will be able to re-invest them at a much higher rate.My guess is Interest and dividend income for Q3 will be above $500 million. That would put it at $2 billion per year. That is $86/share. Fairfax is trading at 9.4 x estimated annual interest and dividend income. Holy shit Batman!

2.) combined ratio = 93.9. This was an elevated quarter for catastrophe losses… so this is a very good result. What happened? “…prudent expense management and decreased catastrophe losses.” Reading that in a Fairfax press release is music to my ears. Fairfax said they were decreasing Brit’s exposure to catastrophes and it appears we are seeing the benefits of this play out (probably company wide). My thesis is Fairfax has been slowly improving the quality of their insurance businesses for the last decade (under Andy Barnard’s leadership) and results this quarter support this idea. And how about Allied World’s CR of 91%… this sub looks like it has supplanted Odyssey as Fairfax’s top performing insurance sub.

3.) interest rates spiked late in Q2. We knew Fairfax was going to take a hit on their fixed income holdings in the quarter and now we know the number: a loss of $405.3 million. But this is a great thing for Fairfax. Their balance sheet has completely digested the spike in interest rates we have seen over the past 6 quarters. This is a big deal.

Higher interest rates are a big tailwind for Fairfax. Their fixed income portfolio is still pretty low duration (2.5 years at the end of Q1). So lots of bonds will be rolling off every quarter. And Fairfax will now be able to reinvest at much higher rates, locking it in for years into the future. I hope we learn on the conference call what the average duration of the fixed income portfolio was at the end of Q2.

-

1

-

-

4 hours ago, OCLMTL said:

HI Viking,

my first ever post here after lurking for a long time. Thanks for the incredible contribution to this website, along with other board members.

To your point of things being so great for 33 months and, despite this, only trading at max 6x 2023 (and 2024-2025E) earnings is beyond my comprehension. It’s a silly % of the my portfolio as is and yet, I sometimes wonder if 100% is not the appropriate number. I’ve rarely come across such a dislocation of reality vs perception in a large cap, high quality company in my entire career. I’m trying to find FFH specific (real) risks and all I see are industry/weather/cat risks that could be major headwinds… I can totally see long/short funds piling into FFH and shorting a basket of P&Cs on the other side to make an incredibly profitable trade while staying “market neutral”. Let’s see what Thursday evening brings us…

@OCLMTL welcome to the wild side (posting). Thanks for sharing your thoughts. I agree with you that the current valuation makes no sense… even with the big move in the share price. we are learning a few things:1.) Fairfax shares got stupid cheap. So everyone’s starting/reference point is wrong.

2.) The phenomenal growth in the insurance companies over the past decade spiked the earnings power of the company - but low interest rates and Fairfax’s strategy of going low duration hid this increase in earnings power for a couple of years.

3.) the execution by the team at Fairfax is still being grossly under appreciated. Especially what they did with their fixed income portfolio. The spike in earnings is happening. It is sustainable. But few understand or believe.

4.) Investment professionals are still in denial. Its almost like a badge of honour in the industry to say ‘i haven’t followed Fairfax for the past five years’ and then they follow it up with ‘oh, and don’t invest in that company… its a mess.’ Meanwhile their clients portfolios underperform. Psychology is such an important part of investing.

I was talking to a family member about Fairfax tonight (they are way up on their investment) and they asked me if it was time to sell and lock in crazy big gains? I said ‘forget how much you are up for a second. You own a well run company and it is trading at 5.5 x earnings and its future prospects are very good. What do you think you should do?’ They got a blinding glimpse of the obvious - they decided to stay invested. I probably should have told them to stop looking at the stock price every day… hard when it keeps hitting fresh all time highs.

-

2 hours ago, Maxwave28 said:

Viking, thank you for all of your thoughtful analysis. I truly appreciate it.

Newbie question for you b/c I dont understand exactly how it is working, on your earning estimate below I believe #4 represents the new IFRS discounting of reserves. If so I thought that might have been a one time adjustment but the below projects this recurring albeit at a smaller amount into the future. Was wondering if that is to capture the delta b/w the old way of reserve accounting and the new IFRS mandated way of discounting or am i totally missing it.

@Maxwave28 your understanding is correct. When i do my updates i use the old accounting logic as much as possible. And 4.) becomes a plug kind of number. We will learn more about IFRS 17 when Fairfax reports tomorrow. My expectation is it will impact 4.)My hope is, over time, we will slowly learn what drives 4.) and how much (like changes in interest rates). So we can make educated guesses in models. Right now i feel like i am flying a little blind. I am not concerned.

-

53 minutes ago, steph said:

thank you Viking for sharing all your work with us. Much appreciated.

@steph you are welcome. I learn so much from other posters… and what i learn usually makes its way into my future posts. This is a great community. We are very lucky right now. I have been following Fairfax for about 20 years. Only 2 other times has the set up looked as favourable as it does today: 2003 (short attack) and 2006/07 (short attack when they were sitting on giant CDS position). We all need to thank the gods for how everything with Fairfax has played out over the past 33 months. It has been a crazy wonderful ride. And the stock still trades well under 6 x 2023E earnings. Nuts.-

1

-

-

3 hours ago, nwoodman said:

I have been thinking a lot lately that one of the magic ingredients to these styles of companies is deal flow. Berkshire was able to use their brand and capital to backstop companies during the GFC but the phone nary rang during Covid (I know the Fed backstopped before things got truly interesting). Perhaps Fairfax's deal flow is lower quality, and they are less discerning than Berkshire or Markel. However, they always seem to have something on the go. Often to the point of more ideas than capital i.e over leveraged. Even their misadventures have yielded silver linings, Greece being the prime example. Anyway, back to your thoughtful post, the more partners you have turning over rocks on your behalf, the better

@nwoodman great comment. But i would take it a step further. I think Fairfax has been winnowing the vast collection of contacts they have. I think they know today who the top performers are. And the top performers are the ones getting the cash. And this has been happening for a few years. How will we know? Future results… when they keep surprising to the upside. -

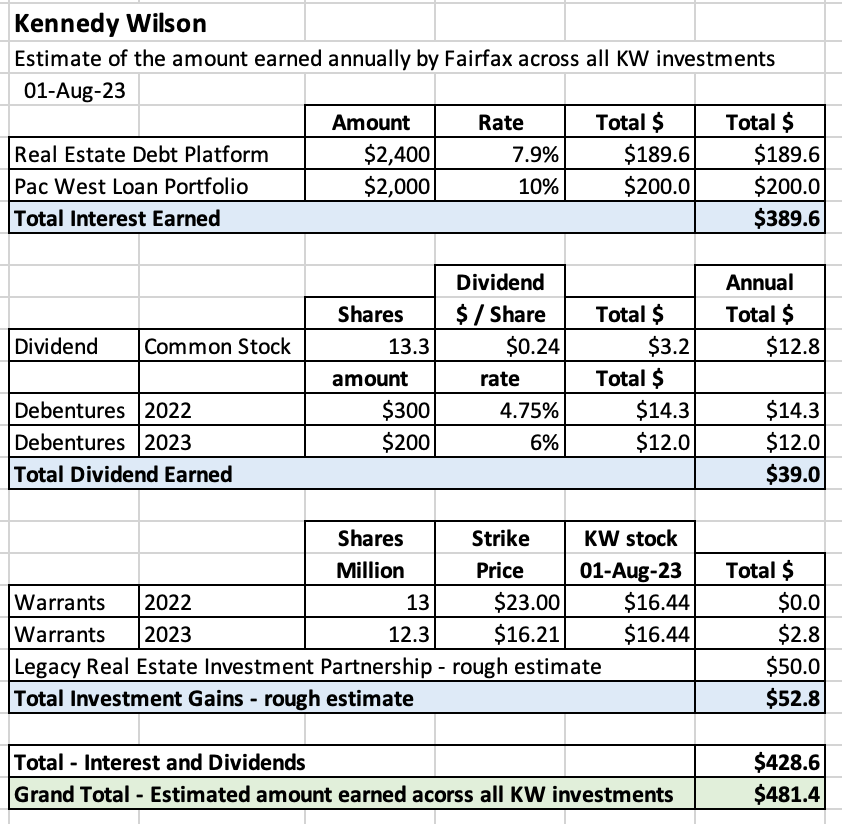

Kennedy Wilson is a misunderstood and underappreciated part of Fairfax’s investment portfolio. Most investors think of Kennedy Wilson through the lens of an equity holding. Looking at the performance of KW’s stock price the past 5 years… what a dog! Woof! KW shares were trading around $21.40 five years ago and today they closed at $16.44/share.

What a terrible investment by Fairfax. Right? Wrong.

Kennedy Wilson has been one of Fairfax’s best investments. What is wrong with the analysis above? It completely misses the point of WHY Fairfax is invested in Kennedy Wilson – it is to tap into Kennedy Wilson’s extensive global real estate expertise.

First, let’s do a quick review.

Fairfax began its relationship with Kennedy Wilson in 2010. A very successful real estate investment partnership has recently blossomed to now include a significant real estate debt platform. Over the past 3 years, Kennedy Wilson has become a much more important part of Fairfax’s investment portfolio. The partnership now includes both equity and fixed income investments:

- 2010: $100 million direct investment in Kennedy Wilson stock

- 2010: Real estate investment partnerships

- 2020: Real estate debt platform

-

2022: $300 million debenture (4.75%)

- 7-year warrants for 13 million common shares with strike price of $23.

- 2023: Purchase of $2.3 billion in real estate loans from PacWest

-

2023: $200 million debenture (6%)

- 7-year warrants for 12.3 million common shares with strike price of $16.21

Roughly, how much does Fairfax currently earn annually from its different investments with Kennedy Wilson?

My very rough estimate is around $481 million. Fairfax has about $5.7 billion invested with Kennedy Wilson so this represents about a 8.4% annual rate of return for Fairfax (mostly interest and dividends).

Of this total, about $429 million is interest and dividends. The PacWest loan transaction just closed so the incremental earnings from this investment will start to show in the interest and dividend income bucket starting in Q3.

The expansion of the relationship with Kennedy Wilson provides another good example of how Fairfax over the last 5 years has been:

- Leveraging and expanding existing, successful, long-term partnerships

- Methodically diversifying their investment portfolio - in this case into real estate

The result is yet another new, growing, significant and steady stream of earnings for Fairfax.

—————

What is the timeline of Fairfax’s various investments in/with Kennedy Wilson?

Started in 2010

-

Kennedy Wilson (KW) stock

- initial equity investment was US$100 million (9% of company)

- today position is worth $200 million (13.3 million shares x $14.98/share)

- current annual dividend of $0.96 = 6.4% yield = $12.8 million in dividend income per year

- Wade Burton is on the board (along with Stanley Zax, who sold Zenith to Fairfax in 2010)

-

investment partnership:

- started with $278 million in 2010

- Prem’s 2022 letter: “we have invested $1.2 billion alongside with them in real estate, have received cash proceeds of $1.1 billion and still have real estate worth about $570 million. Our average annual realized return on completed projects is approximately 22%.”

Expanded in 2020

-

Launched a real estate debt platform: to pursue first mortgage loans secured by high-quality real estate in the Western U.S., Ireland and the U.K.

- 2020 = initial amount of $2 billion

- 2022 = increased to $5 billion

- Prem’s 2022 letter: “$2.4 billion invested through Kennedy Wilson in well-secured first mortgages, primarily on high quality residential apartment buildings, at a floating rate (currently 7.9%)” = $190 million in interest income.

Expanded further in 2022

-

2022: KW perpetual preferred equity investment = $300 million

- pays an annual dividend of 4.75% = $14.25 million

- includes 7-Year warrants for 13 million shares at strike price of $23/share.

Expanded further in 2023

-

PacWest debt purchase of $2.3 billion: KW is buying loans at a discount for $2.1 billion, of which Fairfax is buying $2 billion (95%). Fairfax is also assuming $1.7 billion in future funding obligations.

- Average loan to value is 51%.

- More than 70% of the loans relate to multifamily or student residences; the remainder are a mix of industrial, hotel and life sciences office property projects.

- Fairfax expects the average annual return to exceed 10%.

- Remaining term to maturity is 1.7 years, with some loans carrying extension rights (max 2 years).

-

2023: KW perpetual preferred equity investment = $200 million

- pays an annual dividend of 6% = $12 million

- includes 7-Year warrants for 12.3 million shares at strike price of $16.21/share.

Ownership of stock:

- Kennedy Wilson has 139.4 million shares outstanding

- Fairfax owns 13.3 million = 9.5%

-

Fairfax also owns warrants:

- 13 million at $23

- 12.3 million at $16.21

- If Fairfax exercises all warrants it would own 38.6 million shares = 23.4% (164.7 total)

Fairfax is getting paid 4.75% and 6% while waiting for the warrants to get in the money (they have seven years).

What does Fairfax see in Kennedy Wilson?

Prem’s comment from the 2022 press release from Kennedy Wilson announcing the PacWest transaction: “We are pleased to make this new investment in Kennedy Wilson and to build on our outstanding partnership that dates back to 2010,” said Prem Watsa, Chairman and CEO of Fairfax. “We believe in their global business model, the strength of their high-quality, income-generating assets, and their best-in-class management team.”

- https://ir.kennedywilson.com

- Q4 2022 Investor Presentation: https://ir.kennedywilson.com/~/media/Files/K/Kennedy-Wilson-IR-V2/reports-and-presentations/presentations/q4-2022-investors-presentation.pdf

—————

Interesting trivia point: Bill McMorrow (CEO and Chairman of KW) was the genesis behind Fairfax's investment in Bank of Ireland in 2011. Fairfax made around $1 billion from that one investment. Thank you, Bill! (see Prem's comments below from 2011AR)

—————

2020: Kennedy Wilson and Fairfax Launch New $2 Billion Real Estate Debt Platform

“Kennedy Wilson and Fairfax first invested together in 2010 when the two companies acquired $250 million of real estate assets, including real estate secured loans and real property. Over the past decade, the companies have partnered on $7 billion in aggregate acquisitions, including over $3 billion of real estate related debt investments. In addition, Fairfax currently has an equity ownership interest in Kennedy Wilson of approximately 9%.”

2022: Kennedy Wilson Announces $300 Million Perpetual Preferred Equity Investment From Fairfax Financial

“Kennedy Wilson and Fairfax began their relationship in 2010 when Fairfax made a $100 million equity investment in Kennedy Wilson. Over the past decade, the companies have partnered on $8 billion in aggregate acquisitions, including approximately $5 billion of real estate related debt investments. Fairfax currently has an equity ownership interest in KW of approximately 9%.”

—————

2023: Fairfax Financial Partners With Kennedy Wilson to Acquire Loan Portfolio From Pacific Western Bank, Makes Additional Equity Investment in Kennedy Wilson

Kennedy Wilson’s Press Release

“The acquisition of this Loan Portfolio from Pacific Western Bank highlights Kennedy Wilson’s historic ability to find off-market transactions during periods of uncertainty, move with speed, and build on our successful track record of investing through all real estate cycles,” said William McMorrow, Chairman and CEO at Kennedy Wilson. “The foundations of Kennedy Wilson are our deep relationships, our reputation as a great partner, and our strength in being nimble when opportunity arises; all of which came into play with this loan portfolio acquisition.”

—————

2022AR Prem: “Since we met Bill McMorrow and Kennedy Wilson in 2010, we have invested $1.2 billion alongside with them in real estate, have received cash proceeds of $1.1 billion and still have real estate worth about $570 million. Our average annual realized return on completed projects is approximately 22%. We also own 10% of the company. More recently we have been investing with Kennedy Wilson in first mortgage loans secured by high quality real estate in the western United States, Ireland and the United Kingdom with a loan-to-value ratio of 60% on average. At the end of 2022, we had invested in $2.0 billion of mortgage loans in the U.S. at an average yield of 8.1% and an average maturity of 1.7 years, and in approximately $350 million of mortgage loans in the U.K. and Europe at an average yield of 6.0% and an average maturity of 2.5 years.”

“The combination of interest and dividends and profit from associates accounted for a 3.7% return on our portfolio in 2022, the highest return in the last five years (average 2.5%). We expect to earn these returns in 2023 as well, partly because we have $2.4 billion invested through Kennedy Wilson in well-secured first mortgages, primarily on high quality residential apartment buildings, at a floating rate (currently 7.9%).”

—————

2013AR: “The KWF LPs are partnerships formed between the company and Kennedy-Wilson, Inc. and its affiliates to invest in U.S. and international real estate properties. The company participates as a limited partner in the KWF LPs, with limited partnership interests ranging from 50% to 90%. Kennedy-Wilson holds the remaining limited partnership interests in each of the KWF LPs and is also the General Partner. For the KWF LPs where the company may exercise veto rights over one or more key activities, those partnerships are considered joint ventures under IFRS 11. Where the company has no veto rights over key activities, the company is considered to have significant influence under IAS 28. The equity method of accounting is applied to all of the KWF LPs.”

—————

2011AR Prem: “I have attended the Berkshire Hathaway shareholders’ meeting since there were only 200 shareholders in attendance about 30 years ago. I still find I learn something each year from Warren and Charlie. At the meeting in 2010, I met Bill McMorrow through Alan Parsow, who is a money manager based in Omaha and a great friend. Bill founded Kennedy Wilson, a real estate services and investment company, in 1988, and he now owns 26% of the company. As a result of this meeting, we invested $100 million in a Kennedy Wilson 6% preferred convertible at $12.41 per share, and later purchased $32.5 million of a 6.45% preferred convertible at $10.70 per share and 400,000 common shares at $10.70 per share. Fully diluted we own 18.5% of the company. In 2010 and 2011, we also invested $290 million in several real estate deals with Kennedy Wilson in California, Japan and the U.K. – deals at significant discounts to replacement cost and with excellent unlevered cash on cash returns, in which Kennedy Wilson is the managing partner and a minority investor. We are thrilled to be partners with Bill and his team, who always focus on the downside and have the expertise to manage these investments and finally harvest them. You never know what you will find at a Berkshire meeting!!”

“And there is more to the McMorrow story. While Bill was negotiating the purchase of some real estate loans from Bank of Ireland, he was really impressed with Ritchie Boucher, the Bank’s CEO. Bill introduced Ritchie to us, and we too were very impressed. With the help of our friends at Canadian Western Bank, one of the best banks in Canada, we thoroughly reviewed the opportunity and then quickly formed an investment group with Wilbur Ross, Mark Denning from Capital Research and Will Danoff at Fidelity, which purchased $1.6 billion of Bank of Ireland shares on a rights issue (Fairfax’s share was $387 million).”

-

1 hour ago, nwoodman said:

Guidance for RoTBV at >15%. Almost seems ludricous that they would trade at <TBV. Morgan Stanley’s take attached. I just hope they hurry up with the buybacks and are able to pick up the HFSF stake around these prices. Like buying dollars for 70 cents.

https://www.reuters.com/article/eurobank-holdings-stakesale-idUKL8N3962ML

@nwoodman thanks for posting the article. Eurobank’s guidance for EPS was increased from €0.22/share to €0.28/share. Shares closed today at €1.59/share.

I am wondering if the earnings of Fairfax’s various associate and consolidated equity holdings will exceed expectations when they report on Thursday. Eurobank is the biggest, so we are already off to a great start. Recipe? Thomas Cook?

-

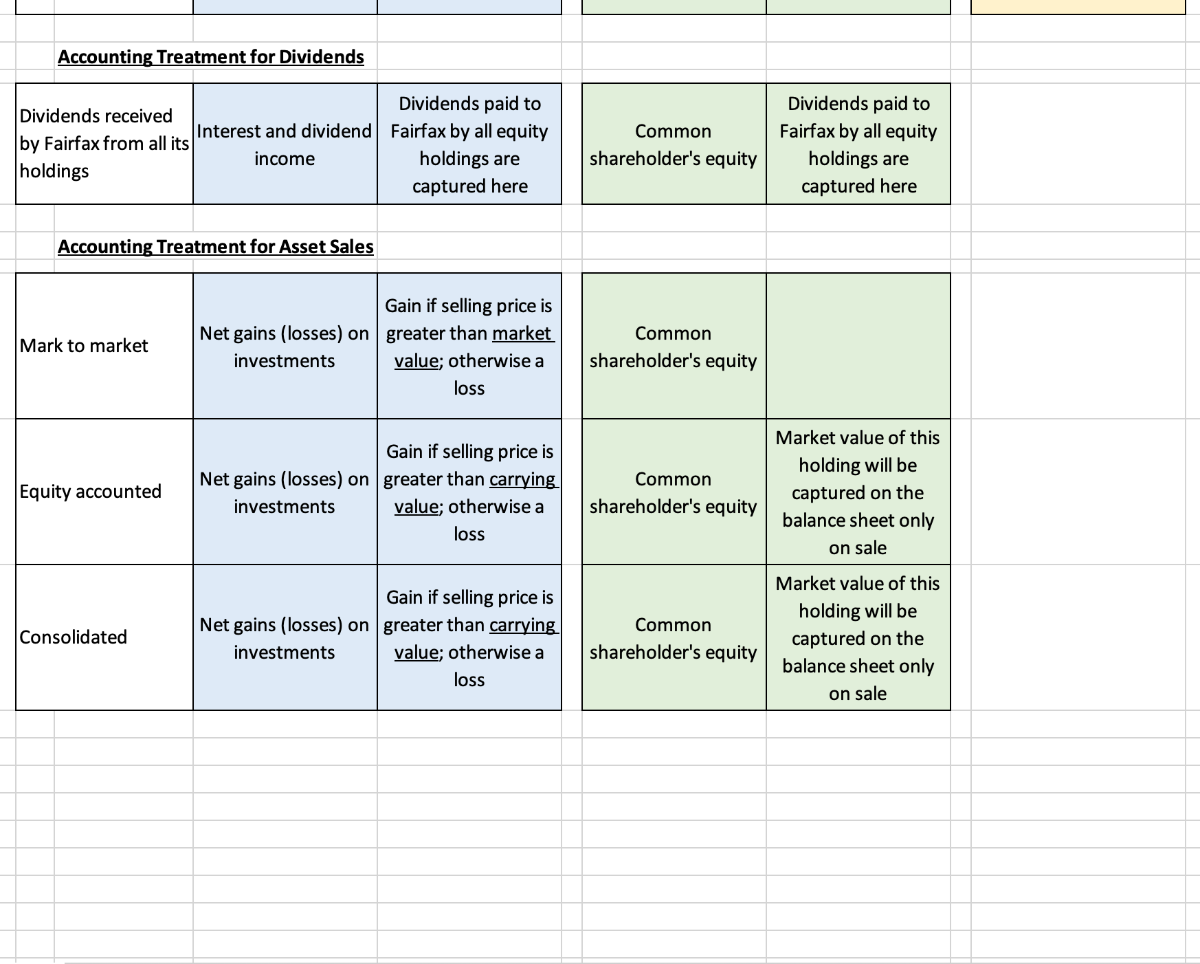

I need the help of board members. It can be confusing to understand how the business results of Fairfax's vast collection of equity holdings flows through to Fairfax's income statement and balance sheet at the end of each quarter. I have put together a 'cheat sheet' with 'rules of thumb' to help investors better understand this flow.

Does this look generally accurate? What is wrong? What is missing? Can the layout be improved?

Please feel free to rip it apart (you won't hurt my feelings). Comment on this thread or private message me. Thanks!

PS: it is one sheet, but I copied it with two pictures so it can be more easily read.

Fairfax 2023

in Fairfax Financial

Posted · Edited by Viking

What kind of an investor is Fairfax?

Most people would answer: ‘value investor.’ That is the right answer but it doesn’t really tell us much. What kind of a value investor?

To answer this question we are going to look at what Fairfax has been doing. What have they actually been buying? What can we learn? We are going to go back three years (June 30 2020, to Aug 11 2023).

—————

But first, let’s set the table.

1.) "The single most important thing (when investing in the stock market)… is to know what you own." Peter Lynch

The problem with Peter Lynch is he says so many smart (and funny) things that his ‘most important thing’ gets lost in the shuffle. This is the ‘north star’ of everything else he writes. From this naturally flows another of Peter Lynch’s nuggets of gold.

2.) "The best stock to buy is the one you already own." Peter Lynch

This makes intuitive sense. You have already done the research on the stocks you own. You know ‘the story’ and you like it (that’s why you own it). Assuming the fundamentals are still solid, then buying more should be a no brainer. Buffett takes this idea a little further with the following quote:

3.) "Diversification may preserve wealth, but concentration builds wealth." Warren Buffett

The idea is to invest with conviction around you best ideas. Especially if the stock is on sale. This leads us to our next point.

4.)"‘The three most important words in investing are margin of safety." Warren Buffett

Ben Graham introduced ‘margin of safety’ as the central concept of investing in Chapter 20 of his book, The Intelligent Investor. The idea is to only purchase stocks when they are trading at a big discount to their intrinsic value (buy something for $0.50 that is worth $1.00). This approach limits your downside if you are wrong and it provides significant upside if you are right.

What do we get when we combine these four points?

Often, your best investment is to simply buy more of something you already own - especially when it is on sale.

One added twist:

5.) "If you search world-wide, you will find more bargains and better bargains than by studying only one nation." John Templeton

Invest wherever in the world the best opportunities are.

—————

What does all of this have to do with Fairfax?

Well, guess what Fairfax has been doing for the past 3 years? It has invested close to $6.2 billion in stuff it already owns. Yes, during this time Fairfax has been investing in new ventures but the amount spent is much smaller. In short, Fairfax has been feasting at the buffet of companies it already owns.

Let’s review the actual investments that Fairfax has been making the past 3 years (Aug 2020 to Aug 2023) that fit this theme to see what we can learn.

1.) Buy Fairfax stock = $2.26 billion

Over the past 3 years Fairfax has ‘purchased’ 5.09 million shares of Fairfax, 19.3% of total effective shares outstanding, at an average cost of $445/share. With shares trading today at $843, the value creation for Fairfax shareholders has been $2 billion.

Fairfax saw incredible value in their shares. They invested with conviction (backed up the proverbial truck). Shareholders are now making out like bandits (the value created by Fairfax is flowing though to a much higher share price). Value investing at its best.

Who does this string of purchases remind you of?

Not Lynch, Buffet or Graham. Who then? Henry Singleton. Who is this guy?

From Prem’s letter in Fairfax’s 2018AR: ““I mentioned to you last year that we are focused on buying back our shares over the next ten years as and when we get the opportunity to do so at attractive prices. Henry Singleton from Teledyne was our hero as he reduced shares outstanding from approximately 88 million to 12 million over about 15 years.”

At the time, many laughed at Prem for making this comment. I don’t think these same people are laughing at Prem today.

2.) Increase Ownership of Insurance Businesses - Buy Out Partners = $1.9 billion

Insurance is the most important economic engine Fairfax has. Top line growth in the insurance businesses is critical to sustainable profit growth at Fairfax over time. And profitability is what determines the share price over the medium to long term.

Fairfax is slowly and methodically taking out the minority partners in its insurance companies. They spent $1.9 billion over the past 3 years doing this. As a result they own a larger share of (growing) future earnings of these high quality companies.

3.) Increase Ownership of Equity investments:

These are the equity investments that Fairfax exerts a great deal of control over. They invested $666 million the past three years. The big purchase was taking Recipe private and being able to buy the stock at a big pandemic discount.

These are the equity investments Fairfax doe not exert a great deal of control over. They invested $1.4 billion the past three years. The biggest deal was expanded the partnership with Kennedy Wilson in real estate, with the 2 transactions below being part of much the bigger deal (debt platform and PacWest loans). There are lots of solid single type of investments on this list.

In total, over the past three years, Fairfax has invested a total of $6.2 billion to increase ownership in companies it already owns. Many of the investments were opportunistic and made at bear market low prices. Investments were made all over the world - value drove the decision, not geography. As a result Fairfax (and its shareholders) now own a greater proportion of the future earnings streams of these many businesses. The returns on the investments made in recent years are starting to come in and they are very good (in aggregate). With lots of upside in the future.

Conclusion: What did we learn?

How Fairfax is investing right now is incredibly simple. Invest in what you know. Buy at a discount. Act with conviction. Cast a wide net (global). Boring. Safe. Generating a very good return for shareholders. Something i think the masters would approve of. In short, Fairfax has been putting on a master-class in value investing over the past three years.

So, after all that, let’s get back to our initial question.

What kind of an investor is Fairfax?

Fairfax is a value investor. Their approach is a hybrid of 5 masters: Lynch, Buffett, Graham, Templeton and Singleton.

—————

Some of the companies Fairfax owns are doing the same thing:

The best example is Stelco who has reduced shares count by 38% over the past 2.5 years, which has increased Fairfax’s stake in the company from 14.7% to 23.6%.

Actions like these provide additional benefits to Fairfax and its shareholders. When combined with what Fairfax is doing, they have a ‘multiplicative’ effect for Fairfax shareholders (in terms of owning larger proportion of future earnings).