Viking

-

Posts

4,694 -

Joined

-

Last visited

-

Days Won

35

Content Type

Profiles

Forums

Events

Posts posted by Viking

-

-

11 hours ago, OliverSung said:

After lurking for years reading this forum, I'm jumping in real quick to plug the write-up I posted today on Fairfax. There isn't much new under the sun than what's already been said here (any one of you seems to know loads more than I do) but it may help you tie things together. Also, my working model is available for download at the bottom of the post. Feel free to change it around based on your own assumptions.

@OliverSung Nice write-up. It is very difficult to write a comprehensive article on Fairfax given the many important pieces - and the significant changes over the past 5 and 10 years. I really enjoyed reading you article. Thanks for posting. -

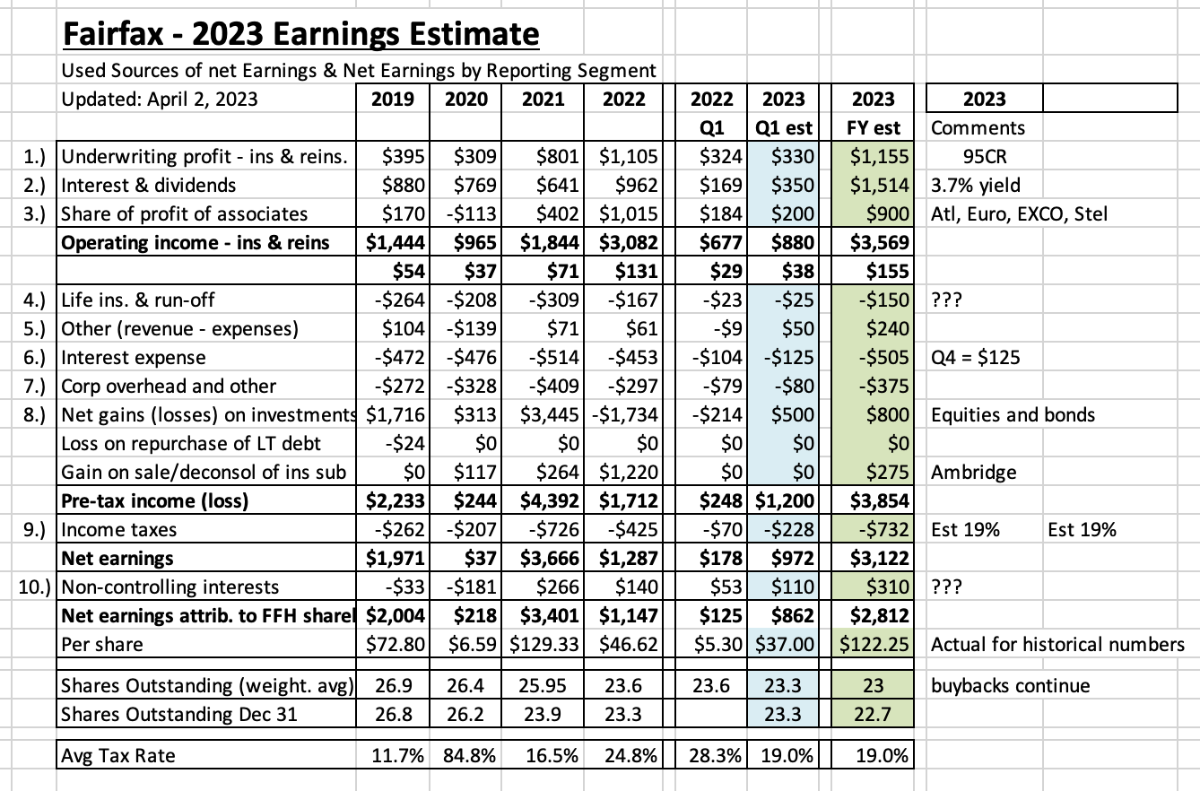

22 hours ago, Viking said:

With Fairfax Q1 earnings coming on Thursday I thought it would be good as a primer to post an update to my last estimate (April 2).

----------

The big change that will happen in Q1 is the move to IFRS-17 accounting. Fairfax said that reported BV at Dec 31, 2022, will be increasing by $94/share. It will likely take a couple of quarters of results to better understand how IFRS-17 impacts Fairfax's reported results.

----------

My comments below are NOT including any changes resulting from the move to IFRS-17.

My guess is Fairfax will earn about $37/share in Q1. That would put March 31 book value at US$685 = $658 + $37 - $10 div. Shares are trading today at $694 = 1 x BV.

Fairfax will see about a $300 million gain in the market value of its associate common stock holdings (equity accounted) in Q1. This will put the market value of associate holdings at about $575 million over carrying value (about $25/share pre-tax). This is not captured in book value.

The sale of Ambridge did not happen in Q1. When this sale closes, likely in Q2, Fairfax will book a $275 million pre-tax gain (about $10/share after tax).

I am not expecting much in the way of share buybacks in Q1. The dividend is paid in Q1 and this is about a $250 million use of cash (common and preferred). Fairfax is now generating significant cash flow in underwriting profit and interest and dividend income each quarter (est $700 million in Q1). The sale of Resolute for $625 million also closed in Q1. The sale of Ambridge will bring in more ($275 million cash and $125 million promissory note). It will be interesting to see what Fairfax does with the all the cash moving forward.

When I weave it all together: Fairfax looks poised to report a very good Q1. More importantly, 'the story' at Fairfax continues to get better.

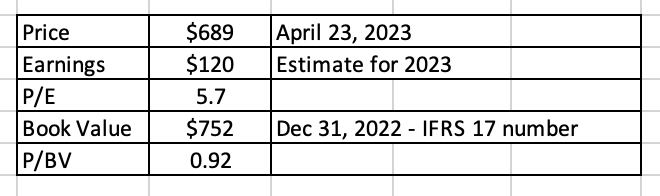

Shares continue to look cheap. My current estimate is Fairfax will earn about $122/share in 2023 = P/E of 5.7 ($694/$122). My 2023 year-end BV estimate is $770 = forward P/BV multiple = 0.90

Assumptions:

1. Underwriting profit = $330 million = flat to PY. My guess is net premiums earned will come in +10% to PY. CR will be a little higher than 2022 (when it was a stellar 93.1).

2. Interest and dividends = $350 million. Q4 2022 came in at $314 million. Fairfax said current run rate is $1.5 billion per year.

3. Share of profit of associates = $200 million. Slightly higher than PY.

4. Life ins & run-off = - $25 million. A little more than PY.

5. Other (revenue - expenses) = $50 million. Expect increase in ownership of Recipe to start to move the needle here in 2023.

6. Interest expense = $125 million. Same as Q4, 2022.

7. Corporate overhead = - $80 million. Same as PY. (no idea)

8. Net gains = $500 million. Equity gains = $375-$400 and bond gains = $100-$150 million. Mostly unrealized.

9. Income taxes = - $228 million. 19%? Guess.

10. Non-controlling interest = $110 million? Guess.

With the Fairfax Q1 report set to be released after markets close on Thursday here are a few of the things i will be watching.Insurance:

1.) what is top line growth? Over or under 10%?

what increases is reinsurance seeing? Especially at Odyssey?

2.) what is the CR? Over or under 95?

- some insurers are reporting elevated cat losses in Q1 compared to PY.3.) update on hard market. What is outlook for 2023?

Fixed income portfolio4.) what kind of increase do we see in interest income? What is new run rate for interest and dividend income?

- Run rate was $950 million end of Q2, $1.2 billion the end of Q3 and $1.5 billion the end of Q4.

5.) did average duration of bond portfolio get pushed out closer to 2 years?

- 1.2 years at end of Q2 and 1.6 years at end of Q4.

- this is a big deal. If Fairfax is able to push duration out to 2 (or more) years then investors will get more comfortable that $1.5 billion will be durable for years. That could be a game changer for Fairfax - that should lead to multiple expansion.

6.) given fall in interest rates in March, do we see mark to market gains in fixed income?

- if duration was pushed out in Q1 then this could be a big number (given how much rates came down in March).

Equity Portfolio

7.) what is amount of mark to market gain?

8.) Resolute closed in Q1. Proceeds were $625 million. Will be used for?

Other

9.) share of profits of associates?

10.) Book value?

11.) share buybacks during quarter?

12.) what is net debt?

13.) capital allocation priority moving forward?

Updates/Commentary:

14.) Ambridge Partners: $400 million sale. On track?15.) GIG purchase of Kipco’s 46% stake: timing on close?

16.) Digit IPO: timing update?

—————

I am estimating Fairfax will earn $122/share in 2023. After we see Q1 results, does this number need to change?

-

With Fairfax Q1 earnings coming on Thursday I thought it would be good as a primer to post an update to my last estimate (April 2).

----------

The big change that will happen in Q1 is the move to IFRS-17 accounting. Fairfax said that reported BV at Dec 31, 2022, will be increasing by $94/share. It will likely take a couple of quarters of results to better understand how IFRS-17 impacts Fairfax's reported results.

----------

My comments below are NOT including any changes resulting from the move to IFRS-17.

My guess is Fairfax will earn about $37/share in Q1. That would put March 31 book value at US$685 = $658 + $37 - $10 div. Shares are trading today at $694 = 1 x BV.

Fairfax will see about a $300 million gain in the market value of its associate common stock holdings (equity accounted) in Q1. This will put the market value of associate holdings at about $575 million over carrying value (about $25/share pre-tax). This is not captured in book value.

The sale of Ambridge did not happen in Q1. When this sale closes, likely in Q2, Fairfax will book a $275 million pre-tax gain (about $10/share after tax).

I am not expecting much in the way of share buybacks in Q1. The dividend is paid in Q1 and this is about a $250 million use of cash (common and preferred). Fairfax is now generating significant cash flow in underwriting profit and interest and dividend income each quarter (est $700 million in Q1). The sale of Resolute for $625 million also closed in Q1. The sale of Ambridge will bring in more ($275 million cash and $125 million promissory note). It will be interesting to see what Fairfax does with the all the cash moving forward.

When I weave it all together: Fairfax looks poised to report a very good Q1. More importantly, 'the story' at Fairfax continues to get better.

Shares continue to look cheap. My current estimate is Fairfax will earn about $122/share in 2023 = P/E of 5.7 ($694/$122). My 2023 year-end BV estimate is $770 = forward P/BV multiple = 0.90

Assumptions:

1. Underwriting profit = $330 million = flat to PY. My guess is net premiums earned will come in +10% to PY. CR will be a little higher than 2022 (when it was a stellar 93.1).

2. Interest and dividends = $350 million. Q4 2022 came in at $314 million. Fairfax said current run rate is $1.5 billion per year.

3. Share of profit of associates = $200 million. Slightly higher than PY.

4. Life ins & run-off = - $25 million. A little more than PY.

5. Other (revenue - expenses) = $50 million. Expect increase in ownership of Recipe to start to move the needle here in 2023.

6. Interest expense = $125 million. Same as Q4, 2022.

7. Corporate overhead = - $80 million. Same as PY. (no idea)

8. Net gains = $500 million. Equity gains = $375-$400 and bond gains = $100-$150 million. Mostly unrealized.

9. Income taxes = - $228 million. 19%? Guess.

10. Non-controlling interest = $110 million? Guess.

-

3 hours ago, Spekulatius said:

@Viking I looked at KW recently and this looks like an overlevered entity. It wont do well with interest where they are. The bonds are trading around 10% and that was the reason I was looking at this. The equity looks like it's too "hot to touch", imo.

@Spekulatius I agree. I am not looking to invest in Kennedy Wilson the stock. Fairfax’s ownership of 10% of Kennedy Wilson is likely table stakes (as Jamie Dimon would say). It looks like Fairfax has been getting good value from the KW relationship.

It is interesting looking at all the different relationships that Fairfax has been cultivating over the years. Stuff like Kipco in Kuwait. Relationship started in 2010. And culminated in sale of Kipco’s stake in GIG to Fairfax this year. Kennedy Wilson is another, this time focussed on global real estate. Lots also going on in Greece. And of course, even more in India. These relationships can take a decade to bear fruit. And Fairfax is extracting more value from these relationships with each passing year. It really is impressive the network across assets and geographies that they have built. Its almost like the senior team at Fairfax has been working on a portrait for years and we are just now able to start to make the picture out.

-

@Parsad yes, Buffett and Munger will not be around forever. And, yes, that is hard to take. However, the heir apparent is out there right now. In fact, there are likely a bunch on them out here. And that is what i love about investing: it is a process of constant change and constant learning. Life continues to get better. As Buffett says, living in ‘the West’ is a gift. You have won the birth lottery.

“Who is the next Buffet”’. That should really be the title of your post. Not “I’m sad.” They are out there. And right now. A gift. We just need to find them

When Buffett is no longer around he is not going to want us to be sad. Rather, he is going to want to reward the investing principals stood for. Ben Graham passed the torch to Warren Buffett and Peter Lynch. Investing legends. Who are the next torchbearers? That is what i want to know.

When Buffett is no longer around he is not going to want us to be sad. Rather, he is going to want to reward the investing principals stood for. Ben Graham passed the torch to Warren Buffett and Peter Lynch. Investing legends. Who are the next torchbearers? That is what i want to know.

PS: is is not likely Greg Abel (and that is not intended to be a slight on Greg Abel).

-

55 minutes ago, glider3834 said:

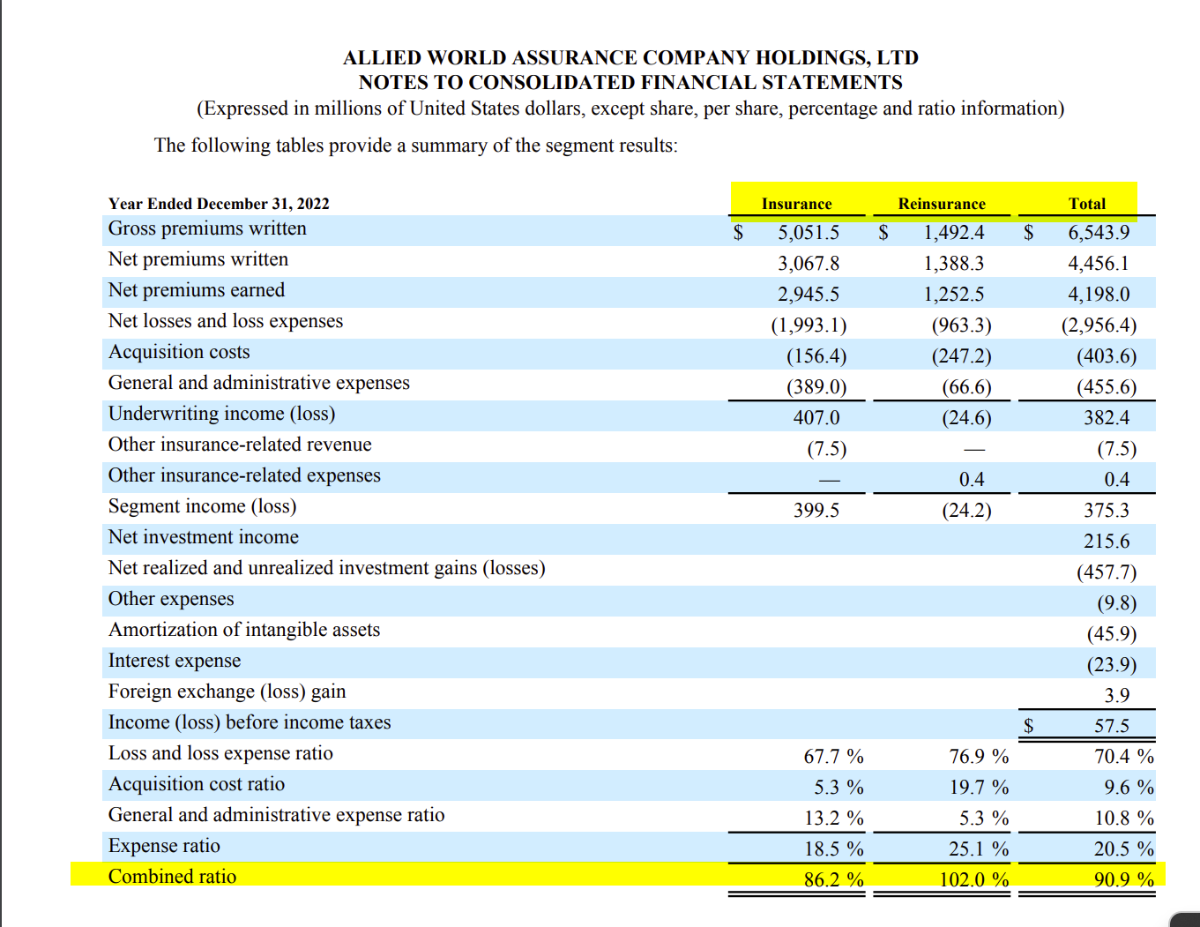

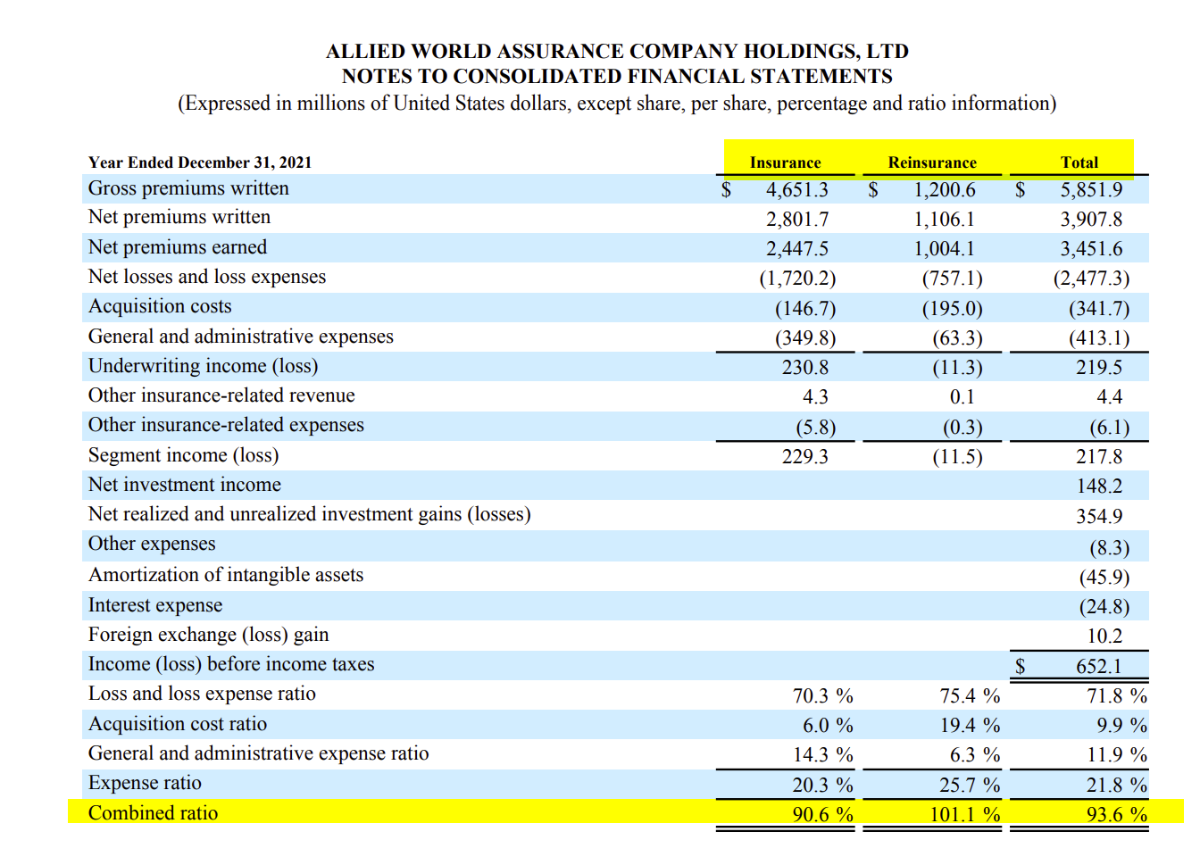

also viking I think we can say the reinsurance hard market conditions IMHO are a bigger tailwind for Fairfax's underwriting profitability than they are for Markel or WR Berkley which I believe have smaller reinsurance businesses.

Take Allied World for example, its insurance business wrote an 86.2% combined ratio(CR) in 2022 but the 102% combined ratio from its reinsurance business took its overall CR to 90.9% (see below)

Higher reinsurance pricing provides opportunity for Allied to bring down its reinsurance CR & derive more underwriting profit.

2022

2021

@glider3834 Great catch. What happens if Fairfax's insurance business (CR) moves a little closer to Markel and WR Berkley's in the coming years? Much higher re-insurance rates should help Allied and especially Odyssey. And those two are the big dogs at Fairfax. Cat exposure has been the big issue at Brit and Fairfax has said they are looking to reduce Brit's exposure to cat. Small iterative changes.

I also wonder how much WRB's results the past few years have benefitted from super low reinsurance pricing (below cost). Now that reinsurance pricing is spiking... maybe WRB's results get a little more lumpy. If that happens the P/BV multiple on the stock will likely come down a little. Something to watch moving forward.

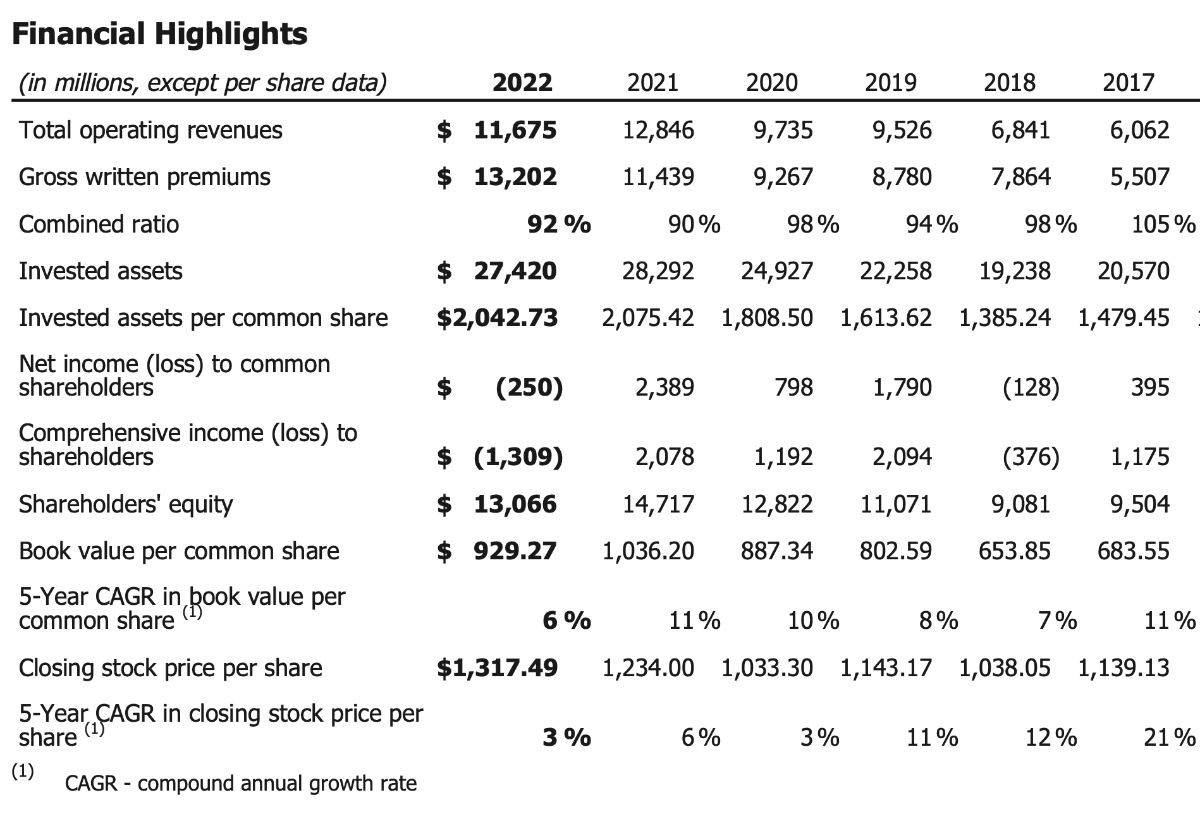

I have listened to Tom Gaynor at Markel for years. Great stories. I keep hearing "ignore our results this year... we are focussed on the long term." It kind of reminds me of 'old Fairfax'. Here are Markel's 5 year results (see table below) - and I don't think Markel pays a dividend:

- 5 year CAGR in book value per common share of 6%

- 5 year CAGR in closing stock price per share of 3%

As a reminder, we have been in a hard market for insurance since late 2019. And interest rates are the highest they have been in +15 years. As an insurance company, if you aren't hitting the ball out of the park right now when will you?

----------

Investing is like driving on the freeway. Sometimes you get boxed in on your lane and can't get out. Meanwhile, traffic two lanes over is motoring. It gets really frustrating as an investor when you get boxed in - it can last for years (cough - Fairfax - cough, cough).

It looks to me like the lane has just opened up for Fairfax. They have no one in front of them for miles and they are putting the pedal to the metal and making up for lost time. At the same time, others are now stuck in traffic a few lanes over...

Leadership sometimes changes.

----------

The table below is from Markel's 2022AR.

-

Comparing Fairfax, Markel and WR Berkley is interesting. Their market caps today are similar. But what about the size of their insurance businesses? And their investment portfolios? Yes, all three have different business models. However, all three are still insurance companies at their core. Let’s take a quick look at some of the key metrics and see what we can learn.

Fairfax Financial, Markel and WR Berkley all have similar market caps today.

- Markel = $18.3 billion

- Fairfax = $16.0 billion

- WR Berkley = $15.6 billion

This suggests investors expect future earnings (total $) to be roughly similar. Let’s start by looking at the insurance side of the businesses and net premiums written.

Net premiums written (2022):

- Fairfax = $22.3 billion

- WR Berkley = $10 million

- Markel = $8.2 billion

Fairfax’s net premiums written is larger than both Markel and WR Berkley combined. That is a big difference. What about underwriting profit?

Underwriting profit (2022):

- WR Berkley = $960 million

- Fairfax = $950 million (when you net out losses from runoff)

- Markel = $610 million

In terms of underwriting profit, WRB and Fairfax are earning similar amounts (total $) and Markel is earning quite a bit less. However, both WRB and Markel each have a much lower CR. Let’s now pivot and look at the investments side of the businesses.

Investment portfolio (2022):

- Fairfax = $55.5 billion

- Markel = $27.4 billion

- WR Berkley = $22.9 billion

Fairfax’s investment portfolio is larger than both Markel and WR Berkley combined. What about interest and dividend income?

Interest and dividend income:

2022 2023E

- Fairfax = $960 million $1.5 billion

- WR Berkley = $780 million $940 million

- Markel = $450 million $620 million

In 2023, Fairfax is going to earn about the same as WRB and Markel combined. That is significant outperformance.

Yes, Markel has Markel Ventures. Fairfax also has significant equity holdings. ‘Share of profit of associates’ for Fairfax is expected to be about $900 million in 2023 and my guess is this is larger than what Markel Ventures will deliver in 2023. WRB is much smaller.

What about realized investment gains? This bucket of earnings has always been a significant advantage for Fairfax over Markel and WRB and my guess is this will continue in the future.

What are analysts expecting for net earnings in 2023?

- Fairfax = $2.5 billion

- WRB = $1.3 billion

- Markel = $1 billion

Analysts expect Fairfax to earn more than WRB and Markel combined.

What is the learning from all of this? Fairfax's market cap / earnings does not make any sense when compared to Markel and WR Berkley. Same market cap for 2 times the earnings? That only makes sense if you think earnings for Fairfax are inflated. Or not durable. This suggests to me that investors still do not appreciate what has happened with Fairfax's investment portfolio over the past couple of years:

- Share of profit of associates: delivering close to $1 billion per year moving forward

- Interest and dividend income delivering more than $1.5 billion in 2023, 2024 and 2025.

As a result, Fairfax's stock continues to be very undervalued when compared to peers.

Note: share count is basic (easier to find). The table above is meant to be directional (not precise) to allow very top line comparisons to be made for the three companies.

——————

Notes:

- WRB and Markel have better quality insurance businesses (much lower CR)

- Fairfax’s fixed income portfolio is much larger and looks better positioned today.

- Fairfax’s net debt is likely higher (interest costs are included in net earnings estimate).

- Fairfax’s insurance business is much more international.

- WRB has been a very consistent performer over the years (by far, the most consistent of the three).

-

1

1

-

Over the past 2 years Kennedy Wilson has become a much more important part of Fairfax’s investment portfolio. A very successful real estate investment partnership has blossomed to now include a significant real estate debt platform. Since 2010 the real estate investment partnership has delivered gains of about $470 million (annual return of 22% on completed projects since 2010). Started two short years ago, the real estate debt platform is on track to deliver (much more?) than $190 million in interest income in 2023 ($2.4 billion invested at a 7.9% floating rate at Dec 31, 2022).

The real estate debt platform increased from $1.44 billion (average yield 4.7% = interest income of $68 million) at Dec 31, 2021 to $2.4 billion (average yield 7.9% = interest income $190 million) at Dec 31, 2022. At the same level of growth this platform could increase to $3.5 billion in 2023 and at 7.9% yield = $277 million in interest income. This will be something to monitor when Fairfax reports quarterly results during 2023.

The expansion of the relationship with Kennedy Wilson provides another good example of how Fairfax over the last 5 years has been:

1.) leveraging and expanding existing, successful, long term partnerships

2.) methodically diversifying their investment portfolio - in this case the fixed income part

The result is yet another new, growing, significant and steady stream of earnings for Fairfax.

—————

What is the timeline of Fairfax’s various investments in/with Kennedy Wilson?

Started in 2010

-

Kennedy Wilson stock (KW)

- initial equity investment was US$100 million (9% of company)

- today position is worth $200 million (13.3 million shares x $14.98/share)

- current annual dividend of $0.96 = 6.4% yield = $12.8 million in interest income per year

- Wade Burton is on the board (along with Stanley Zax, who sold Zenith to Fairfax in 2010)

-

investment partnership:

- started with $278 million in 2010

- Prem’s 2022 letter: “we have invested $1.2 billion alongside with them in real estate, have received cash proceeds of $1.1 billion and still have real estate worth about $570 million. Our average annual realized return on completed projects is approximately 22%.”

Expanded in 2020

-

Real estate debt platform: to pursue first mortgage loans secured by high-quality real estate in the Western U.S., Ireland and the U.K.

- 2020 = initial amount of $2 billion

-

2022 = increased to $5 billion

- Prem’s 2022 letter: “$2.4 billion invested through Kennedy Wilson in well-secured first mortgages, primarily on high quality residential apartment buildings, at a floating rate (currently 7.9%)” = $190 million in interest income.

Expanded further in 2022

-

2022: Perpetual preferred equity investment = $300 million

- pays an annual dividend of 4.75% = $14.25 million

- includes 7-Year warrants for 13 million shares at strike price of $23/share.

What does Fairfax see in Kennedy Wilson?

Prem’s comment from the 2022 press release from Kennedy Wilson: “We are pleased to make this new investment in Kennedy Wilson and to build on our outstanding partnership that dates back to 2010,” said Prem Watsa, Chairman and CEO of Fairfax. “We believe in their global business model, the strength of their high-quality, income-generating assets, and their best-in-class management team.”

- https://ir.kennedywilson.com

- Q4 2022 InvestorPresentation: https://ir.kennedywilson.com/~/media/Files/K/Kennedy-Wilson-IR-V2/reports-and-presentations/presentations/q4-2022-investors-presentation.pdf

—————

Interesting trivia point: Bill McMorrow (CEO and Chairman of KW) was the genesis behind Fairfax's investment in Bank of Ireland in 2011. I think Fairfax made over $1 billion from that one investment. Thank you Bill! (see Prem's comments below from 2011AR)

==========

2020: Kennedy Wilson and Fairfax Launch New $2 Billion Real Estate Debt Platform

“Kennedy Wilson and Fairfax first invested together in 2010 when the two companies acquired $250 million of real estate assets, including real estate secured loans and real property. Over the past decade, the companies have partnered on $7 billion in aggregate acquisitions, including over $3 billion of real estate related debt investments. In addition, Fairfax currently has an equity ownership interest in Kennedy Wilson of approximately 9%.”

—————

2022: Kennedy Wilson Announces $300 Million Perpetual Preferred Equity Investment From Fairfax Financial

“Kennedy Wilson and Fairfax began their relationship in 2010 when Fairfax made a $100 million equity investment in Kennedy Wilson. Over the past decade, the companies have partnered on $8 billion in aggregate acquisitions, including approximately $5 billion of real estate related debt investments. Fairfax currently has an equity ownership interest in Kennedy Wilson of approximately 9%.”

==========

Kennedy Wilson 2010AR: In 2010, Kennedy Wilson formed a $278 million investment partnership with Fairfax Financial, and the venture’s first major transaction was the purchase of a 65% interest in the Japanese apartment company. Kennedy Wilson previously owned 35% of the company.

- The added bonus of our Fairfax partnership was the addition of Stanley Zax to our Board of Directors. Stanley’s counsel and insights have been invaluable to our success in 2010 and 2011.

==========

2022AR Prem: Since we met Bill McMorrow and Kennedy Wilson in 2010, we have invested $1.2 billion alongside with them in real estate, have received cash proceeds of $1.1 billion and still have real estate worth about $570 million. Our average annual realized return on completed projects is approximately 22%. We also own 10% of the company. More recently we have been investing with Kennedy Wilson in first mortgage loans secured by high quality real estate in the western United States, Ireland and the United Kingdom with a loan-to-value ratio of 60% on average. At the end of 2022, we had invested in $2.0 billion of mortgage loans in the U.S. at an average yield of 8.1% and an average maturity of 1.7 years, and in approximately $350 million of mortgage loans in the U.K. and Europe at an average yield of 6.0% and an average maturity of 2.5 years.

- The combination of interest and dividends and profit from associates accounted for a 3.7% return on our portfolio in 2022, the highest return in the last five years (average 2.5%). We expect to earn these returns in 2023 as well, partly because we have $2.4 billion invested through Kennedy Wilson in well-secured first mortgages, primarily on high quality residential apartment buildings, at a floating rate (currently 7.9%).

——————

2021AR Prem: We have an outstanding partnership with Kennedy Wilson, led by its founder and CEO Bill McMorrow and Bill’s partners, Mary Ricks and Matt Windisch. Since we met them in 2010, we have invested $1,150 million in real estate, received cash proceeds of $1,070 million and still have real estate worth about $542 million. Our average annual realized return on completed projects is approximately 20%. We also own 9% of the company.

More recently we have been investing with Kennedy Wilson in first mortgage loans secured by high quality real estate in the western United States, Ireland and the United Kingdom with a loan to value ratio of 60% on average. At the end of 2021, we had committed to mortgage loans of $1.44 billion in the U.S. at an average yield of 4.7% and an average maturity of 1.9 years. We had also committed to approximately $500 million of mortgage loans in the U.K. and Europe at an average yield of 3.8% and an average maturity of 1.7 years. We are truly grateful to Bill and his team, and Wade Burton on our side, for a very profitable and enjoyable relationship. In February 2022, we committed to invest $300 million in a 4.75% perpetual preferred in Kennedy Wilson, with seven-year warrants exercisable at $23 per share.

—————

2020AR Prem: We have an outstanding partnership with Kennedy Wilson, led by its founder and CEO Bill McMorrow and Bill’s partners, Mary Ricks and Matt Windisch. Since we met them in 2010 we have invested $1,130 million in real estate, received cash proceeds of $1,054 million and still have real estate worth about $582 million. Our average annual realized return on completed projects is approximately 20%. We also own 9% of the company.

More recently we have been investing with Kennedy Wilson in first mortgage loans secured by high-quality real estate in the western United States, Ireland and the United Kingdom with a loan to value ratio of less than 60%. At the end of 2020 we had committed to mortgage loans of approximately $1.5 billion at an average yield of 5% and an average maturity of four years. We are very grateful to Bill and his team for a very profitable and enjoyable relationship.

——————

2019AR Prem: no special mention in his lette

- During 2019 the company recorded share of profit of a KWF LP of $57.0 (A53.6) related to the sale of investment property in Dublin, Ireland. The KWF LP was subsequently liquidated and its carrying value reduced to nil when the company received final cash distributions of $169.4 (A150.0).

—————

2018AR Prem: Kennedy Wilson. We have had an excellent relationship with Kennedy Wilson, its CEO Bill McMorrow and Bill’s partners, Mary Ricks and Matt Windisch, since we met them in 2010. We own 9.2% of the company. In 2018, Kennedy Wilson sold three of our joint venture properties in Dublin for a gain of $74 million, an average annual return of 21% on our original investment, and returned $107 million of the proceeds to Fairfax. Since inception in 2010, we have invested $855 million with Kennedy Wilson, received cash proceeds of $858 million and still have real estate worth about $351 million. Our average annual realized return since inception was 21%. We continue to acquire properties through Bill, Mary and Matt with the purchase of one office building on 26 acres in Denver, Colorado for $85 million with a cash on cash yield of 6.7%; three office buildings outside Portland, Oregon for $29 million with a cash on cash yield of 6.2%; and nine office buildings on 67 acres outside Los Angeles, California for $163 million with a cash on cash yield of 7.5%. These Class A office buildings are anchored by investment grade tenants in strong and growing markets and were available at quite significant discounts to replacement cost.

- During 2018 three KWF LPs sold investment property in Dublin, Ireland. The company recognized its share of profit of $73.6 (A64.2) from those sales in share of profit of associates in the consolidated statement of earnings. The three KWF LPs were subsequently liquidated and their carrying values reduced to nil when the company received final net distributions of $107.3 (A91.9).

—————

2017AR: no mention of significance

—————

2016AR Prem: We have invested $692 million in real estate investments with Kennedy Wilson over the last seven years. Through sales of real estate and mortgage loans, as well as refinancings, we have received distributions of $645 million. Our total net cash investment in real estate investments with Kennedy Wilson is therefore now $47 million, and that investment is probably worth about $284 million. Annual net investment income from these real estate investments amounts to $12 million. Also, we continue to own 10.7% of Kennedy Wilson (12.3 million shares): our cost was $11.10 per share, and the shares are currently trading at about $22. A big thank you to Bill McMorrow and his team at Kennedy Wilson.

—————

2015AR Prem: We have invested $645 million in real estate investments with Kennedy Wilson over the last six years. Through sales of real estate and mortgage loans, as well as refinancings, we have received distributions of $625 million. Our total net cash investment in real estate investments with Kennedy Wilson is therefore now $20 million, and that investment is probably worth about $237 million. In 2015 Kennedy Wilson sold its Japanese real estate for a gain of $78 million, a return of 45% on our original investment, and returned $125 million of the proceeds to Fairfax. Also, we continue to own 10.4% of Kennedy Wilson (12.2 million shares): our cost was $11.37 per share, and the shares are currently trading at about $20. A big thank you to Bill McMorrow and his team at Kennedy Wilson.

————

2014AR Prem: We have invested $629 million in real estate investments with Kennedy Wilson over the last five years. Through refinancings, sale of some loan portfolios and gains on hedging contracts on Japanese yen, we have received distributions of $465 million. Our total net cash investment in real estate investments with Kennedy Wilson is therefore now $164 million, and that investment is probably worth about $350 million. We have yet to sell though, while our cash flow return of 11.2% is very acceptable. Also, we continue to own 10.7% of Kennedy Wilson (11.5 million shares): our cost was $11.90 per share, and the shares are currently trading at $26.19.

- During 2014 the company sold its holdings in two KWF LPs and recognized net gains of $21.5 and $9.9 respectively.

—————

2013AR Prem: We continued to invest with Bill McMorrow from Kennedy Wilson in 2013. We invested in the Clancy Quay apartments and some well-leased office buildings in Dublin and we also invested in a U.K. loan pool. We have invested a net cumulative $305 million in real estate deals with Kennedy Wilson in California, Japan, the U.K. and Ireland – deals at significant discounts to replacement costs and with excellent unlevered cash on cash returns, in which Kennedy Wilson is the managing partner and an investor. Also, we continue to own a fully diluted 10.9% interest (11.5 million shares) in Kennedy Wilson.

- The KWF LPs are partnerships formed between the company and Kennedy-Wilson, Inc. and its affiliates (‘‘Kennedy-Wilson’’) to invest in U.S. and international real estate properties. The company participates as a limited partner in the KWF LPs, with limited partnership interests ranging from 50% to 90%. Kennedy-Wilson holds the remaining limited partnership interests in each of the KWF LPs and is also the General Partner. For the KWF LPs where the company may exercise veto rights over one or more key activities, those partnerships are considered joint ventures under IFRS 11. Where the company has no veto rights over key activities, the company is considered to have significant influence under IAS 28. The equity method of accounting is applied to all of the KWF LPs.

—————

2012AR Prem: We continued to purchase commercial real estate investments with Bill McMorrow and his team at Kennedy Wilson, as discussed in last year’s Annual Report. For example, we purchased, 50/50 with Kennedy Wilson, perhaps the finest office building in Dublin, built in 2009 and 100% leased to State Street Bank for 25 years, for one- third of its construction cost with an unleveraged yield of approximately 8.5%. We also own, with Kennedy Wilson, some of the finest apartment buildings in Dublin with similar return characteristics. Rest assured we return Bill’s calls very promptly!

—————

2011AR Prem: I have attended the Berkshire Hathaway shareholders’ meeting since there were only 200 shareholders in attendance about 30 years ago. I still find I learn something each year from Warren and Charlie. At the meeting in 2010, I met Bill McMorrow through Alan Parsow, who is a money manager based in Omaha and a great friend. Bill founded Kennedy Wilson, a real estate services and investment company, in 1988, and he now owns 26% of the company. As a result of this meeting, we invested $100 million in a Kennedy Wilson 6% preferred convertible at $12.41 per share, and later purchased $32.5 million of a 6.45% preferred convertible at $10.70 per share and 400,000 common shares at $10.70 per share. Fully diluted we own 18.5% of the company. In 2010 and 2011, we also invested $290 million in several real estate deals with Kennedy Wilson in California, Japan and the U.K. – deals at significant discounts to replacement cost and with excellent unlevered cash on cash returns, in which Kennedy Wilson is the managing partner and a minority investor. We are thrilled to be partners with Bill and his team, who always focus on the downside and have the expertise to manage these investments and finally harvest them. You never know what you will find at a Berkshire meeting!!

And there is more to the McMorrow story. While Bill was negotiating the purchase of some real estate loans from Bank of Ireland, he was really impressed with Ritchie Boucher, the Bank’s CEO. Bill introduced Ritchie to us, and we too were very impressed. With the help of our friends at Canadian Western Bank, one of the best banks in Canada, we thoroughly reviewed the opportunity and then quickly formed an investment group with Wilbur Ross, Mark Denning from Capital Research and Will Danoff at Fidelity, which purchased $1.6 billion of Bank of Ireland shares on a rights issue (Fairfax’s share was $387 million).

-

Kennedy Wilson stock (KW)

-

5 hours ago, glider3834 said:

@glider3834 Looks like the ratings agencies are giving Fairfax credit for the positioning of their fixed income portfolio and the much higher operating income that will be coming in 2023 and future years. Well done! Just another indication that the worm has turned.

----------

"The Long-Term ICR upgrade for Fairfax reflects its ability to limit investment volatility through year-end 2022, and the prospective earnings outlook from deploying substantial cash into higher yielding debt instruments. Fairfax has benefited from solid underlying returns among its core operating subsidiaries in recent years, despite elevated catastrophic losses in the North American market. Furthermore, due to its relatively low duration and strong cash position at year-end 2021, Fairfax’s unrealized losses from the market turmoil in 2022 were materially less than peer averages. The upgrade also considers that Fairfax’s financial leverage has improved materially compared with historically higher levels and has been consistently maintained at levels largely in line with comparably rated peers in recent years. AM Best expects that Fairfax will continue to maintain financial leverage at or near current levels going forward. The group’s capital position should continue to improve over time, as it benefits from higher levels of dividend and interest incomes, which should further reduce the group’s reliance on external debt."

-

I have spilt lots of ink writing what I like about Fairfax. Does that mean i am ignoring the risks? No, of course not. So let’s flip the script today and write about a few of the risks of investing in Fairfax. What am i missing?

For starters, there are the usual run-of-the-mill risks:

1.) Will this be another bad year for catastrophes?

2.) Is the hard market over?

3.) Is a severe recession coming?

These risks are important but out of Fairfax’s control. With this post, I want to discuss the risks that are more specific to Fairfax - and firmly in their control.

What are the risks of investing in Fairfax?

1.) Can management be trusted? 2010-2020 was a lost decade for Fairfax shareholders.

Buffett says "It takes 20 years to build a reputation and five minutes to ruin it. If you think about that, you'll do things differently." Well, Fairfax shredded their reputation not in 5 minutes but over a 10 years period.

What happened? Bad decisions. Poor communication. Terrible business results. Not a great combination. Long term shareholders capitulated in May of 2020, and the stock dropped to US$230. Yes covid was partly to blame. But only partly.

The interesting thing is things actually started improving at Fairfax in about 2018. For the past 5 years we have seen much better decisions. Better communication. Very good business results. Record high stock price.

Does that mean we are the clear? No. Trust can only be re-built with time. So we will see.

PS: Trust is the core building block of strong relationships. If Fairfax wants long term shareholders they need to be a trustworthy partner.

The next two risks fall under the ‘capital allocation’ bucket:

2.) Do they make another ‘equity hedge’ type decision? This is the big one for me.

This one decision cost Fairfax shareholders a total of $5.4 billion from 2010 to 2020 (an average loss of $494 million for 11 straight years). Most of the losses happened from 2010-2016. However, in one last slap in the face of investors, Fairfax delivered one final $529 million loss in 2020. (Yes, how could an ‘equity hedge’ lose that much money in the bear market of 2020?)

Fairfax has said many times over the past few years that the ‘equity hedge’ position was a mistake. Further, they have said they will no longer short individual stocks or market indices. This was THE key driver of underperformance at Fairfax from 2010-2020. So we know this specific mistake will not be repeated in the future.

But does Fairfax make another big bet that sets them back +5 years? I don’t see one today. But my eyes are wide open.

3.) Do they make a string of bad equity purchases in the near future?

Fairfax’s equity picks from 2014-2017 were mostly terrible. By my count Fairfax made 10 different purchases during this period that performed poorly and resulted in the company booking various losses of about $1.5 billion ($200 million on average per year) over the past 8 years.

The good news? It looks to me like something changed in about 2018. Fairfax’s equity purchases from 2018 to today have been very good. As well, the equities purchased from 2014-2017 that were under-performing have largely been fixed.

So I am not concerned today. But I do monitor each of their equity purchases.

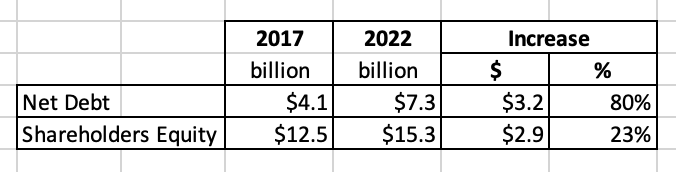

4.) financial leverage: increase in net debt

Fairfax is comfortable using leverage to boost shareholder returns. Over the past 5 years net debt at Fairfax has increased 80%. Over the same time period common shareholders equity has increased 23%.

I don’t see Fairfax’s current net debt level as a problem. However, for the next year or two, it would be nice to see net debt remain at this level (or even go a little lower). I expect earnings to be very good over the next few years and this should increase shareholders equity meaningfully. Net debt is something to monitor.

5.) corporate governance

Fairfax is a family controlled company (not unlike other founder led companies). Prem has a 10% economic interest and a 43.9% voting interest. Two of Prem’s kids currently serve as directors: Christine McLean and Ben Watsa.

When a company is performing well, the issue of family control tends not to matter. However, when the company is not performing well, the issue of family control can become a big issue. Minority shareholders have little recourse should they be unhappy with the decisions management is making.

This is what it is.

-

1 hour ago, glider3834 said:

Love it. Fairfax has learned they are not a private equity turn-around shop. It appears much more work needs to be done at Blackberry. An exit of Blackberry at a fair price would let Fairfax shift the proceeds into other opportunities with better risk/reward/management. It would be an opportunity to further improve the quality of the equity portfolio.

—————Blackberry is a great example of ‘old Fairfax’: buy a declining business that was poorly managed that needed lots of strategic help from Fairfax to right the ship. Result? Loads of work. And a decade of very poor performance. As a result, this investment caused significant reputational damage to Fairfax (it was such a large position for years).

—————

And, of course, there is also the psychological benefit of exiting Blackberry. For long-term shareholders.

-

56 minutes ago, jfan said:

An aside to this topic of FFH still being cheap despite the run up in pricing and the question of what to do at this point.

I think the concept of economic elasticity might be helpful:

ie:

- Thinking on the margins instead of absolutes

- What is the return/risk on the next marginal dollar?

- Anchoring bias on the prior absolute purchase price vs what the purchase price today means relative to its fundamentals

My normalized EPS is ~ $110 USD or $140 CAD. Even if I'm wrong, and EPS is really 1/2 of this, at these current prices, the earning's yield is 7.8%. Compared to the S&P 500 historical return of 7-8%, my general feel of the risk of margin compression, top-line growth deceleration, persistent share count dilution, probability of reinvestment success, etc between these 2 options, FFH seems better positioned.

The question for me is: "what is the rational thing to do with my future savings"?

I posted before that I would probably continue to hold my position, but the more I think about it, perhaps the rational thing to do is buy more given the opportunity set I have in front of me.

@jfan the thing i struggle with the most when valuing a company like Fairfax is what multiple to attach. My miss with Apple in 2016 was mostly multiple related, which increased from something like 10 x earnings to 30 x earnings over the next 5 years. Mr Market went from hating the stock to loving it.

So what multiple should Fairfax trade at given its execution the past couple of years, current situation and near term prospects? 1.2 x BV seems low but reasonable as a next step. My guess is BV will come in around US$690 when Q1 is reported (i am ignoring IFRS 17 until after Fairfax reports). So this suggests to me a low fair price for Fairfax today is around $830. With shares trading today at $690 this suggests Fairfax is 20% undervalued. This seems too low to me, given the current set up for the company.

How has the mood of Mr Market changed with Fairfax?

- 2020: extreme pessimism

- 2021: pessimism

- 2022: neutral

- 2023/2024: slow shift to mild optimism?

If Fairfax delivers $120/share in earnings in 2023 and again in 2024 then i think we will see Mr Market shift to mild optimism… and this should lead to multiple expansion. Perhaps we get to a conservative multiple of 1.2 x earnings by the end of 2024:

- BV at end of 2024 = $880/share ($660+$120+$120-$10-$10).- 1.2 x BV = $1,050/share

- stock price today = $690 = 50% return over next 7 quarters.

Impossible to know. But is is important to think/model how things might play out.

-

1 hour ago, Thrifty3000 said:

I can see EPS of $100 per share being the new lower bound for FFH. And, the share price obviously doesn't reflect that. However, I'm not sure I can confidently forecast when we might hit a normalized EPS beyond $150, so for now I'll be inclined to reduce my stake as Fairfax approaches my estimation of fair value on a modestly growing $100 per share earnings stream. Let's call it somewhere between $1,200 and $1,500 USD per share as of today.

Fairfax is experiencing some incredible tailwinds right now. But, the following headwinds 3 years from now aren't unthinkable:

- much softer insurance market

- much lower interest rates

- fairly valued share price (no more buybacks)

Each of those headwinds could act as gravity on the current $100 EPS, which means any new earnings from the invested free cash may only supplant rather than enhance EPS in the future.

I'm not suggesting another 7 year famine as much as I'm saying it's in the realm of possibility that normal earnings could be hovering somewhere below $150 per share in 3 years, and we could be staring at a sub $1,500 share price.

Don't get me wrong, when it comes to FFH I'm still jacked to the tits!

@Thrifty3000 my crystal ball only looks out about 2 years. I continue to estimate earnings of US$120 for both 2023 and 2024. Looking further out to 2025 and 2026, yes, lots of things could change. The key driver of earnings looking out a couple of years could well be capital allocation. Fairfax’s capital allocation track record since 2018 has been very good.Over 4 years, 2022 to 2025, i think Fairfax might generate more than $8 billion in free cash flow ($2 billion per year). If they invest this $8 billion wisely they could earn 10% per year (10% is a modest estimate). By the beginning of year 5 (2026) that would result in an incremental $800 million in earnings/increase in intrinsic value. That would be about $40/share pre-tax (my guess is share count will be close to 21 million in 4 years).

Fairfax today has no pot holes left to fill. No annual cash burn of $500 million from equity hedges. No annual cash burn of $200-$250 million from fixing broken equity holdings. Moving forward, pretty much all of the free cash flow will be invested into assets that will generate a future return for shareholders. That is a big, big deal for shareholders. The turn started in 2018. But it often takes years for good capital allocation decisions to flow through to reported results. We have seen much improved results at Fairfax in 2021 and 2022 (when you net out the loss from fixed income). The outlook for 2023 and 2024 is even better.

My guess is another tailwind is coming for Fairfax… and it is the fruits of years of good capital allocation decisions combined with the magic of compounding.

-

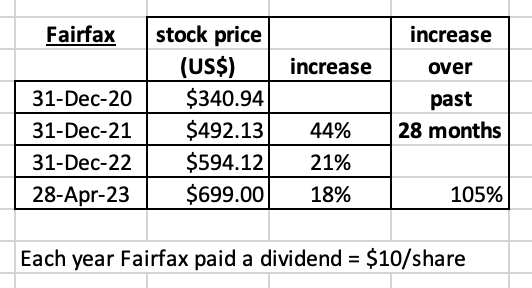

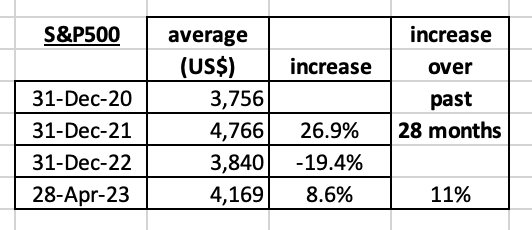

Is it time to sell Fairfax?

Fairfax’s stock has delivered a cumulative 105% return to investors over the past 28 months (since Dec 31, 2020). It has also paid three $10 dividends each year (all at once in January) so total returns have been even better.

How does this compare to the overall market? The S&P500 is up 11% over the past 28 months.

The performance of Fairfax’s share price the past 28 months has been breathtaking - both in absolute and relative terms. So what is a rational investor to do with their shares? Why SELL of course. At least that is what I would have probably done in the past.

—————

Successful investors need to get two things right: when to buy AND when to sell. Over my investment career I have been much better at the ‘when to buy’ decision than the ‘when to sell’ decision. I have a history of selling my big winners way too early. An example? After a +100% gain over a couple of years, I sold most of my concentrated position in Apple in early 2016 - right around the time some guy names Warren Buffett started to buy. What was my mistake? My sell decision was primarily focussed on price - not fundamentals. Apple’s underlying business in 2014 and 2015 was getting better each year. After a +100% gain over 24 months the stock was still cheap when I sold it - and their future prospects never looked better. The crazy part is I knew all of this - I follow my largest positions very closely. So selling Apple in 2016 was a big mistake. Right? Not necessarily. One of the things I really like about investing is your mistakes can often lead to your greatest successes.

What was the lesson? Clearly, I needed to get better at the ‘when to sell’ part of investing. Here is what Peter Lynch has to say:

- The key to knowing when to sell, he says, is knowing "why you bought it in the first place." Lynch says investors should sell if: The story has played out as expected and this is reflected in the price.

—————

Let’s get back to Fairfax. What’s happened with the fundamentals at Fairfax over the past 28 months? We don’t have Q1 results yet so let's just look at the 24 months from Dec 31, 2020 to Dec 31, 2022.

1.) insurance: we have been in a hard market the past 2 years.

- net written premiums were up 50% over the two years from 2020 to 2022. CR has been improving. Underwriting profit has increased a whopping 260% from $308 million in 2020 to $$1.1 billion in 2022.

- Digit: we also learned Fairfax owns a large chunk of a start-up insurance company in India that is growing like a weed...

2.) investments - fixed income: we have shifted from QE to QT over the past 2 years.

- at the end of 2020 interest rates were very low with central banks saying they would remain very low for years. Interest income at Fairfax was falling like a stone. 2020 = $717 million. 2021 = $568 million.

- 2 short years later, at the end of 2022, interest rates had spiked. Interest income has now spiked higher. 2022 = $874 million.

- more importantly, the guide from Fairfax is for interest income to come in around $1.4 billion for 2023, 2024 and 2025.

3.) investments - equities: stock picking and active management is back.

- over the last 2 years Fairfax’s various equity holdings have spike higher. Fairfax’s style of investing (active management, value, commodities, energy) appears ideally suited for the current environment.

- new investment: TRS of FFH shares, a position initiated late 2020 and early 2021, was up $500 million pre-tax in 2 years ($700 million the past 28 months).

- share of profit of associates has ballooned from -$113 million in 2020 to $1.1 billion in 2022. This should come in around $900 million per year moving forward.

4.) investments - realized gains: chug, chug, chug...

- pet insurance was sold in 2022 for $1 billion after tax gain = $40/share. This was like found money.

- Resolute Forest Products was sold at the top of the lumber cycle for $625 million plus $180 million CVR. Resolute had a carrying value of $134 million at Dec 31, 2020. This was a significant increase in value for shareholders.

5.) shares outstanding: has come down 11% from 26.2 million on Dec 31, 2020 to 23.3 million on Dec 31, 2022.

- in late 2021 Fairfax repurchased 2 million shares at $500/share.

----------

OK, let’s summarize things from a fundamental perspective. Over the past two years, Fairfax has delivered:

1.) record underwriting profit

2.) record interest and dividend income

3.) record share of profit of associates

4.) more than $2.5 billion in asset monetizations

5.) double digit decline in share count

So we have that interesting situation where Fairfax’s intrinsic value has been growing at 20-25% per year (2021 and 2022). Yes, the stock went up 21% in 2022 but my guess is intrinsic value in 2022 went up much more than that. So even after a 21% increase, the stock was likely cheaper at Dec 31, 2022 ($594) than it was on Dec 31, 2021 ($492).

How do Fairfax’s future prospects look? The three engines of their business (insurance, investments - fixed income and investments - equities) all look very well positioned in the current environment. For the first time in Fairfax’s history they are all performing well at the same time. And this set-up is expected to continue in the coming years. That suggests profitability at Fairfax should remain robust.

How do the usual valuation metrics look?

- P/E multiple: stock is trading at < 6 times 2023 earnings (est $120)

- P/BV multiple: stock is trading at about 1.06 x Dec 31 BV or 1 x est March 31 BV.

- ROE = 18% ($120 / $658)

- note: i did not use IFRS 17 BV = + $94/share at Dec 31, 2022. Using that measure just makes Fairfax stock look even cheaper.

Across all three metrics, Fairfax still looks cheap to dirt cheap. Less than 6 times earnings? An 18% ROE grower trading at 1 times BV?

So what is a rational investor to do after a 105% return in 28 months? What would Peter Lynch do? I think Peter Lynch would stick with this winning stock.

PS: The management team at Fairfax has been executing exceptionally well since about 2018. The fundamentals have been improving every year since then.

—————

The Peter Lynch Approach to Investing in "Understandable" Stocks

- https://home.csulb.edu/~pammerma/fin382/screener/lynch.htm

Lynch is an advocate of maintaining a long-term commitment to the stock market. He does not favor market timing, and indeed feels that it is impossible to do so. But that doesn’t necessarily mean investors should hold onto a single stock forever. Instead, Lynch says investors should review their holdings every few months, rechecking the company "story" to see if anything has changed either with the unfolding of the story or with the share price. The key to knowing when to sell, he says, is knowing "why you bought it in the first place." Lynch says investors should sell if:

- The story has played out as expected and this is reflected in the price; for instance, the price of a stalwart has gone up as much as could be expected.

- Something in the story fails to unfold as expected or the story changes, or fundamentals deteriorate; for instance, a cyclical’s inventories start to build, or a smaller firm enters a new growth stage.

For Lynch, a price drop is an opportunity to buy more of a good prospect at cheaper prices. It is much harder, he says, to stick with a winning stock once the price goes up, particularly with fast-growers where the tendency is to sell too soon rather than too late. With these firms, he suggests holding on until it is clear the firm is entering a different growth stage.

Rather than simply selling a stock, Lynch suggests "rotation"--selling the company and replacing it with another company with a similar story, but better prospects. The rotation approach maintains the investor’s long-term commitment to the stock market, and keeps the focus on fundamental value.

-

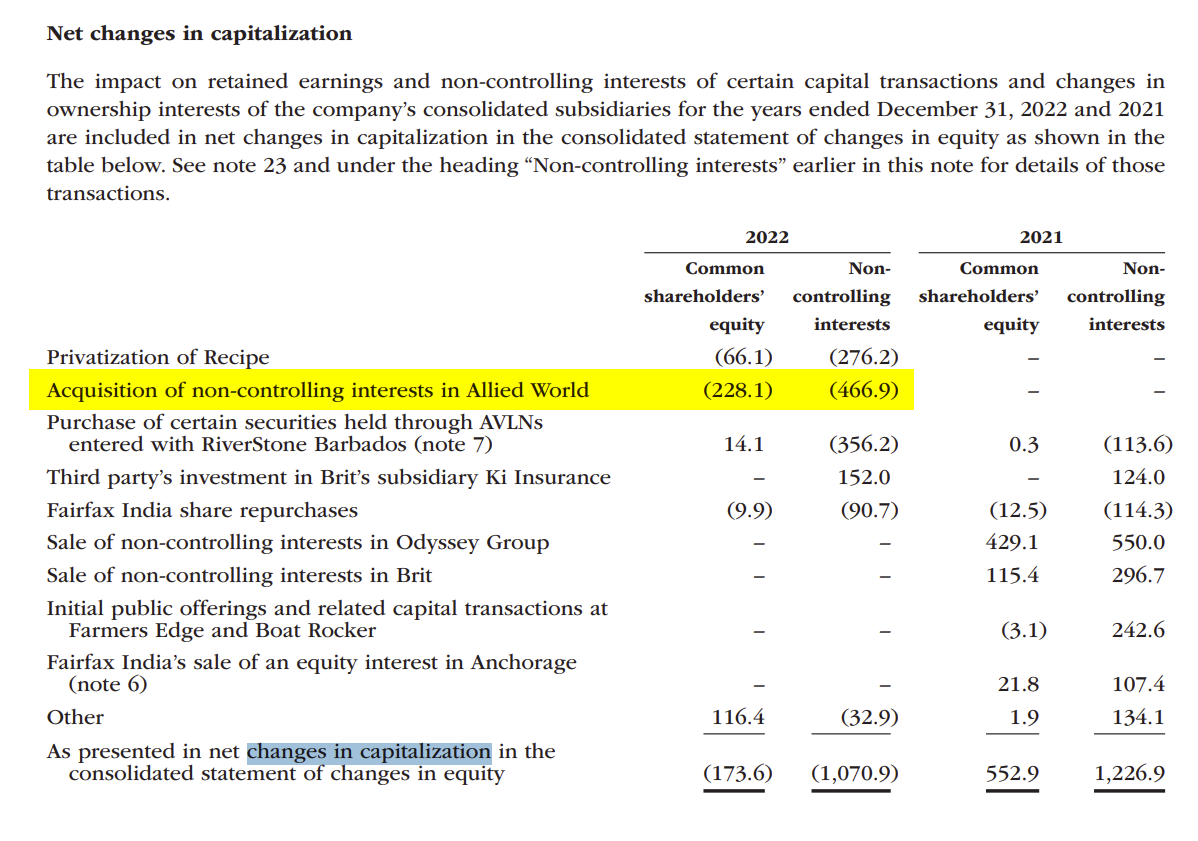

1 hour ago, glider3834 said:

viking suggested I put up a post on this subject - buyout of 12% stake from Allied minority shareholders - I won't detail all the background here but just the key points - just to qualify I am not an expert on IFRS accounting, I have cobbled this info together from filings and we are missing shareholder agreement bw minority investors & Fairfax.

I guess the purpose of this post is to try and look at the mechanics of this deal and how future transactions with minority interests in Allied, Odyssey, Brit or other subs might look.

So here we go

1. What did Fairfax pay for the 12% stake in Allied?

Fairfax paid $650M cash to minority shareholders for their 12% stake in Allied in Sep-22, this is actually equal to the minority shareholders original investment in July 2017.

Here is the calculation (12%/29.1%) x $1580M = $650M

So we could infer that its likely Fairfax will need to spend $930M to acquire the remaining 17.1% stake in Allied now held by minority shareholders.

Question: Can we also infer that this is the buyout price template for Odyssey & Brit minority stakes as well?

2. What was Fairfax's equity financing cost for this deal? Minority shareholders received a priority, fixed 8% annual dividend (or $126.4M on $1580M investment) from Allied.

Putting 1. & 2. together - both the equity financing and buyout price are fixed. Fairfax benefit is that it retains all the upside from Allied's revenue, net income and shareholder equity growth.

3. What is the immediate cash benefit to Fairfax of this deal?

By my estimate = $22.7M per annum

Calculation

8% dividend paid on 12% stake = $52M less $29.3M (after-tax interest cost on senior notes used to fund deal ie $650M x 5.63% x (1-0.2) - lets assume a 20% tax rate

Any further upside that Fairfax receives from this acquired 12% share of Allied over & above $52M is gravy.

4. How is fair value of consideration (including accrued dividend) of $733.5M calculated?

This is equal to $650M cash paid plus $38.5M accrued dividend paid (on 12% stake for 1 Jan to 27 Sep) plus (I am estimating) $45M fair value of call option exercised.

5. Does the 12% Allied buyout impact earnings or book value?It increases Fairfax's share of Allied's operating earning & going forward EPS - common sharesIt reduced BVPS as the fair value of consideration (excluding accrued dividend paid) = $695M was more than $467M carrying value of 12% stake in Allied - so the difference is a $228M reduction in common shareholder equity (important point this impacts shareholders equity (specifically its a loss of retained earnings) and it doesn't run through the earnings statement).

I hope I haven't given anyone a headache! lol

@glider3834 that was very well explained. Thank you for taking the time to figure out all the different pieces to this deal. It will help us lots moving forward… my guess is Fairfax will buy back another chunk of Allied World this year.

It appears to me that the the real benefit to Fairfax is it cleans up their balance sheet. They no longer have to make the fixed payments. And if they fund future buy backs with cash then it can be viewed as deleveraging. Which given the amount of debt they currently have would be a good thing.

-

3 hours ago, Thrifty3000 said:

Bought back 87,000 shares last month. That’s a nice pace.

@Thrifty3000 what Fairfax does with capital allocation in 2023 will be super interesting to follow. They could easily take out 1 million shares = 4% of shares outstanding. Fairfax had to pay the dividend in Q1 = @ $250 million so it makes sense share buybacks might be lighter to start the year. I really like what they have been doing the last couple of years - a nice balance between:- strengthen balance sheet - buy out minority partners - Allied World last year

- growth - organic - support subs - hard market- growth - acquisition - insurance - GIG is a good example here

- growth - acquisition - non-insurance - Recipe is a good example here

- share buybacks

-

Interesting tug of war going on in oil markets. Fundamentals (supply and demand) vs financial markets (futures activity - net speculative demand is down substantially and short interest is up substantially). The winner? By July/Aug we should know. I am betting the fundamental side wins out… yesterday i was happy to add to SU the last 2 days close to C$40.

- “hated bull market” - music to my ears.

- Josh thinks we might see an economic slow down in 2H and much higher oil prices.

-

6 hours ago, Luca said:

Thanks for sharing, yeah, with a triple in valuation, very nice returns on equity+continued higher interest rates above 4% and no big disasters would produce an insane amount of cash. If the Stars Allign the underwriting could also jump on top and than we could really see a big lift off here. What is the likely hood of a stronger soft market happening? Premiums declining? I know @Viking mentioned its softening a bit already. The great thing is really that the valuation is so undemanding that the upside is quite free and the downside over 10 years is quite limited.

Thanks for all the hard work for everyone who shares details here, helped me a lot to figure out fairfax!

@Luca On the Chubb call yesterday Evan Greenberg sounded pretty confident that 2023 would be another solid year in terms of top line growth (high single digit). This suggests to me that that the hard market is slowing - but we are still in a hard market.

What comes next? Looking at history i think it is normal after the hard market to get a couple of sideway years (not hard or soft). And then a soft market. No one really knows… so we take it one quarter at a time.

-

1

-

-

Fairfax has grown their excess and surplus lines insurance in the US by about 80% over the past 2 years. They were the 4th largest player in 2022, up from 7th in 2020.

What is excess and surplus lines insurance (E&S)? Progressive explains it well:

- Excess and surplus lines (E&S) insurance is a market that protects high-risk businesses that standard insurers won’t cover. This market is also known as surplus lines or non-admitted insurance.

- Companies with unusual or elevated risks often need E&S insurance because the admitted market considers them too risky to cover. These businesses could get a policy through a qualified E&S carrier.

- https://www.progressivecommercial.com/business-insurance/excess-and-surplus-insurance/

----------

Excess & Specialty - US Top 25 – 2022

Top US excess and surplus carriers see premiums surge, market share slip in 2022

- https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/top-us-excess-and-surplus-carriers-see-premiums-surge-market-share-slip-in-2022-75096783

- “Fairfax Financial was the lone company among the top 10 that picked up market share in 2022, rising to 5.0% from 4.8%. The company also experienced a 26.6% surge in premiums.”

-----------

Excess & Specialty - US Top 25 – 2021

Most top E&S insurers see market shares decline in 2021; premiums rise YOY

- https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/most-top-e-s-insurers-see-market-shares-decline-in-2021-premiums-rise-yoy-70287307

- “Fairfax Financial Holdings Limited, the fourth-largest insurer in the rankings, was the only company among top 10 players to log a year-over-year increase in market share. The insurer's share of the E&S market rose to 4.77% from 4.50%. Fairfax Financial jumped two spots in the rankings, thanks to a 40% increase in premiums to $3.0 billion from $2.14 billion a year ago.”

-

18 hours ago, Viking said:

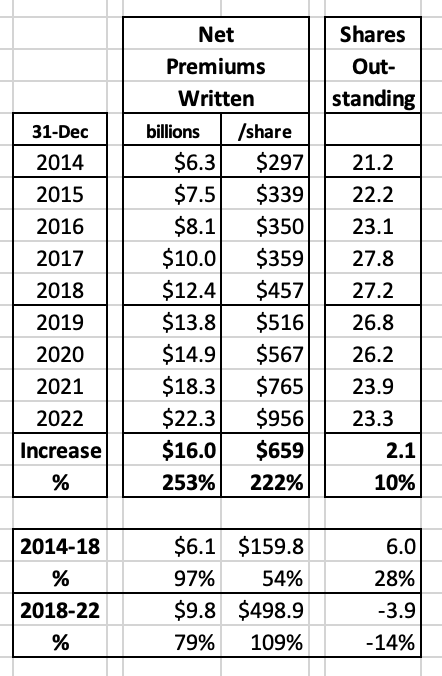

Is Fairfax a growth company? I realize that sounds like a dumb thing to ask. I mean this is Fairfax after all. But hey, just for fun, what do the numbers say? Fairfax has compounded net written premiums from $6.3 billion in 2014 to $22.3 billion in 2022, which is a compound growth rate of 17% each year for the past 8 years. And my guess is we will get around 10% growth for each of the next two years, which would give us compound growth over 10 years of +15%. Really? That performance is pretty impressive.

Guess how many large cap Canadian companies have grown their top line by +15% per year for 10 years? Not many. Apparently not many P&C insurance companies either. Like a goat going up a mountain, Fairfax has been nimbly and quickly climbing the rankings of the largest global P&C insurers… last year they were top 25 and this year they quietly moved into the top 20 list.

So let’s ask that question again… is Fairfax a growth company? Yup.

WOW! A Canadian company that is competing against the best the world has to offer… and not just playing the game (that participation award thing we love here in Canada) but actually winning? That is crazy. Canada must be so proud! Like invite Prem to Ottawa. And hold a parade and celebrate!

Except… ummm… no one in Canada seems to know that Fairfax exists let alone that it has been growing like a weed. It looks like most investors are also in the same boat. Because how does Mr. Market reward a fast grower’s stock price?

Fairfax’s stock price price is dirt cheap. Makes no sense to me. But, hey, we all know Mr. Market is always right. Right? Except of course… when Mr. Market is completely wrong. (That is called a fat pitch by some country bumpkin who lives in Omaha). But hey, that is a story for another day.

Today, let’s dig into what happened at Fairfax over the past 8 years to drive all that top line growth. And why I am optimistic over the near term (even thought the hard market looks like it is slowing).

————

The 17% growth in net written premiums that Fairfax has delivered over the past 8 years has happened in two pretty distinct phases. Then i will take a stab at what might come next:

- phase 1: Acquisitions (2015-2017)

- phase 2: Organic - hard market (2019-2023)

- phase 3: Take-out of minority partners (2022-2025)

As one would expect, there is some overlap with these phases. So let’s peel back the onion a little bit and review what happened in each phase. What did Fairfax do? What was the cost? Was it good for shareholders? By digging a little deeper, we can learn more about Fairfax. And better evaluate the performance of the management team.

Phase 1: Acquisitions (2015 to 2017)

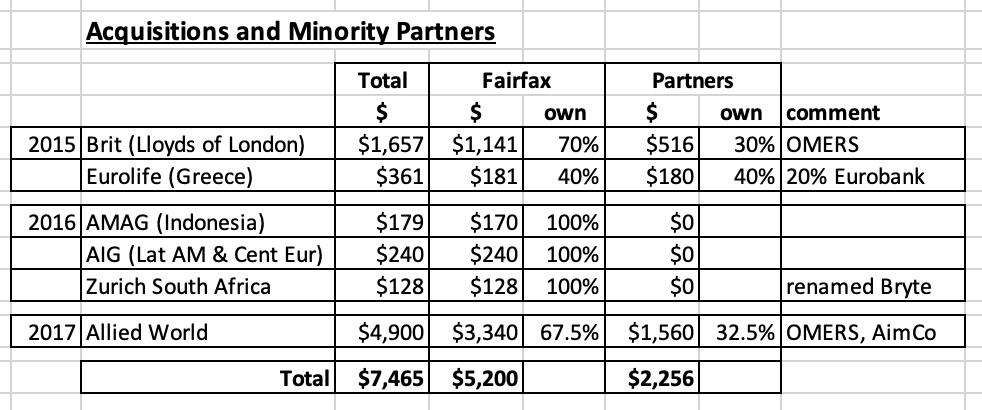

Fairfax has used acquisitions to help fuel its growth through its entire existence. And unlike many P&C insurers, Fairfax has long had an international presence. Over a three year period, from 2015-2017 Fairfax made 6 separate acquisitions that cost a total of $7.5 billion.

How did Fairfax pay for the acquisitions? At the time, Fairfax was short on cash as the investment side of the business was underperforming (losses from equity hedges… yes, sorry to keep picking that scab). Fairfax funded the purchases though:

- stock issuance = $3.34 billion (7.225 million shares at $462/share)

- minority partners = $2.256 billion (see above)

- asset monetizations = Bank of Ireland, Ridley, ICICI Lombard, First Capital

The deal with the minority partners is interesting: From 2015AR: “In the case of both Brit and Eurolife, we expect to be able to acquire the interests back within the five years after closing, after providing OMERS with an acceptable return. The team at OMERS has been a pleasure to deal with.” Allied World is structured similarly. Finding a temporary partner was a very creative funding solution. I think the partners make an annual rate of return (of around 8% per year?) and Fairfax is able to buy the stakes back when they have the cash and at an acceptable price (negotiated when the deal is struck, I think).

Timing? In hindsight, 2015-2017 was a good time to buy insurance companies. Reasonable prices. Right before the start of the hard market. The timing was likely not a fluke. Fairfax was being opportunistic.

How much did Fairfax grow? Net premiums written increased from $6.3 billion in 2014 to $12.4 billion in 2018, for total growth of 97% over 4 years (see the table at the bottom of this post). Yes, the share count did increase quite a bit so growth per share was lower at 54% (more on this later).

Growth by acquisition can be good but it carries risks. Do you overpay? Are there hidden issues (such as poor reserving)? Are there integration/culture issues? What is the best way for an insurance company to grow? A hard market. And that is what started in the second half of 2019.

Phase 2: Organic - hard market (2019-2023)

Hard markets for P&C insurers are exceptionally rare. The last one was in 2001-2004. What makes a hard market so good? The opportunity to charge higher premiums. And to apply more stringent underwriting (more favourable terms and conditions). For well run insurers like Fairfax a hard market is like a gift from the insurance gods.

Fairfax was positioned perfectly for the hard market that started in 2H 2019. And they have been taking full advantage of it for close to 4 years now.

How much did Fairfax grow? Net premiums increased from $12.4 billion in 2018 to $22.3 billion in 2022, for total growth of 79% over 4 years. However, during this period the share count decreased quite a bit so growth per share was higher at 109%. That is rocket ship emoji type organic growth in 4 years time.

The hard market is the best way for an insurance company to grow but they do not last forever. And it certainly looks like the current hard market is slowing. My guess is Fairfax will post mid to high single digit growth in net premiums written in 2023. Does that mean the growth story is over? No. Because Fairfax has set the table nicely for what will drive the next big phase of growth for the company: the buying out their minority partners.

Phase 3: Take-out of minority partners (2022-2025)

Fairfax started executing this strategy over the past couple of years. But it picked up steam in 2022 with the Allied World transaction.

- 2021 Singapore Re: paid $103 million to increase ownership from 28.1% to 96% (now 100%)

- 2018 & 2021 Eurolife: increased ownership from 40% to 50% and then to 80%. The last 30% was purchased from OMERS for $143 million.

- 2022 Allied World: cost $733 million to increase ownership from 70.9% to 82.9%

Why is this strategy picking up steam? Fairfax is now generating around $2.5 billion in free cash flow per year. It started in 2022 but was masked in the reported results by the large unrealized losses in the bond portfolio. As we begin 2023, we are going to see reported earnings spike higher. My conservative estimate is Fairfax is going to earn $120/share in 2023 = $2.8 billion. The biggest chunk of this is interest and dividends at $1.5 billion. The next biggest chunk is underwriting profit of $1.1 billion. The quality of the earnings are the best in Fairfax’s history.

So what will Fairfax do with this Smaug like mountain of gold that is rolling in every quarter? Let’s quickly review capital allocation:

- strong financial condition: while debt levels are a little elevated, shareholders equity will be spiking over the next couple of years. So no need to pay down debt.

- support growth of subsidiaries in hard market? As the hard market slows, this will not be needed.

- buy out minority partners - bingo, we have a winner

- share buybacks - well, we actually have two winners

And what just got announced? Fairfax is buying out Kipco and increasing its ownership in GIG from 43.7% to 90%. It is interesting how the deal will be financed: $200 million at closing and $165 million each year for the next 4 years. GIG’s earnings will likely come close to covering each of the annual payments due to Kipco. So the total cost of $860 million is being spread over 4 years. Very creative.

In GIG’s case, yes i realize Fairfax bought out the majority partner. Same with Singapore Re. Both deals fit the theme perfectly.

Moving forward i expect Fairfax to continue buying out their minority partners in the insurance businesses. These transactions are very low risk (Fairfax knows the assets) and they offer a solid rate of return (what ever was being paid to minority partners; likely around 8%?). Taking out the minority partners also simplifies Fairfax’s structure and makes the company easier to understand.

Some on this board have stated buying out minority partners is kind of like doing a share buyback. Because shareholders get an even bigger piece of Fairfax’s growing earnings.

Share buybacks: With all the free cash flow Fairfax is generating we should also see more significant share buybacks moving forward. If Fairfax repurchases 600,000 shares per year (about $420 million/year at the current price) we could see total shares count drop to 22 million by the end of 2024. This would return the share count to where it was in 2015. In turn, this will boost net written premiums per share.

Conclusion: So after all this, what did we learn? The management team at Fairfax has been masterful at taking advantage of the changing environment - both the external (in the insurance market) and internal (at Fairfax). Their planning, creativity and execution over the last 8 years has built Fairfax into a global insurance giant that is exceptionally well positioned in the current environment.

What does this mean for investors? Growth investing is identifying and investing in companies with above average growth prospects compared to the industry/peers. Over time higher growth - leads to higher earnings - leads to a higher stock price. For growth investing to work the company needs to be successful; does the growth and higher profitability actually happen?

What does this have to do with Fairfax? Well the growth has already happened at Fairfax. And profitability is spiking. And yet little of this is reflected in the stock price - yet.

Investors in Fairfax today are getting years of growth that has already happened (top and bottom line) for free. That, of course, sounds preposterous. But it is true.

How can that happen? Its not that complicated. The current narrative around the company is completely wrong. Fairfax is a great example of how dumb the ‘smart money’ can be at times.

“One more thing”: Fairfax owns a significant amount of Digit Insurance. Who is Digit? Digit is one of the fastest growing general insurance companies in India. We may see an IPO in 2023. But that is a story for another day.

—————

- Allied World (17.1% = @ $1 billion?): “The company has the option to purchase the remaining interests of the minority shareholders in Allied World at certain dates until September 2024.”

- Odyssey ($900 million): “The company has the option to purchase the interests of CPPIB and OMERS in Odyssey Group at certain dates commencing in January 2025.”

- Brit ($375 million): “The company has the option to purchase OMERS’ interest in Brit at certain dates commencing in October 2023.”

—————

Let’s quickly review share count. Fairfax issued a total of 7.2 million shares in 2015, 2016 and 2017 to help fund its aggressive international insurance expansion. The new shares were issued at an average price of $462/share. At December 31 2022, the ‘effective shares outstanding’ at Fairfax has fallen to 23.3 million shares. Over the last 5 years (2018-2022), Fairfax has reduced its share count by approximately 4.4 million shares or 15.9%. The average price paid to buy back shares was $464/share. The average price paid for the shares repurchased by Fairfax over the past 5 years is the same price that the shares were issued at from 2015-2017. Fairfax’s book value at Dec 31, 2022 was $658/share (old BV). Bottom line, Fairfax was extremely opportunistic and was able to repurchase a significant quantity of shares at a very low price - and offset most of the dilution that happened from 2015-2017.

Of interest, in 2021 Fairfax sold 10% of Odyssey Re for $900 million to help fund a buy back of 2 million shares of Fairfax at $500/share. Fairfax knew their shares were crazy cheap at $500. But they did not have the cash at the time. So they put together another deal with OMERS structured the same as the Brit and Allied deals. Creative. Opportunistic.

—————

A Fairfax company did make one large insurance acquisition in 2021. Gulf Insurance Group (GIG) practically stole AXA’s gulf insurance business. AXA was kind of a forced seller and GIG got a great price (who in their right mind would buy an insurance business in the middle of covid… yes, a company affiliated with Fairfax). The acquisition increased GIG’s size by about 80% and gives them considerable scale in MENA - they are now one of the largest P&C insurers in the region.

—————

I re-wrote my conclusion to the article i posted yesterday. This is more on-point.Conclusion: So after all this, what did we learn? The management team at Fairfax has been masterful at taking advantage of the changing environment - both the external (in the insurance market) and internal (at Fairfax). Their planning, creativity and execution over the last 8 years has built Fairfax into a global insurance giant that is exceptionally well positioned in the current environment.

What does this mean for investors? Growth investing is identifying and investing in companies with above average growth prospects compared to the industry/peers. Over time higher growth - leads to higher earnings - leads to a higher stock price. For growth investing to work the company needs to be successful; does the growth and higher profitability actually happen?

What does this have to do with Fairfax? Well the growth has already happened at Fairfax. And profitability is spiking. And yet little of this is reflected in the stock price - yet.

Investors in Fairfax today are getting years of growth that has already happened (top and bottom line) for free. That, of course, sounds preposterous. But it is true.

How can that happen? Its not that complicated. The current narrative around the company is completely wrong. Fairfax is a great example of how dumb the ‘smart money’ can be at times.

-

Is Fairfax a growth company? I realize that sounds like a dumb thing to ask. I mean this is Fairfax after all. But hey, just for fun, what do the numbers say? Fairfax has compounded net written premiums from $6.3 billion in 2014 to $22.3 billion in 2022, which is a compound growth rate of 17% each year for the past 8 years. And my guess is we will get around 10% growth for each of the next two years, which would give us compound growth over 10 years of +15%. Really? That performance is pretty impressive.

Guess how many large cap Canadian companies have grown their top line by +15% per year for 10 years? Not many. Apparently not many P&C insurance companies either. Like a goat going up a mountain, Fairfax has been nimbly and quickly climbing the rankings of the largest global P&C insurers… last year they were top 25 and this year they quietly moved into the top 20 list.

So let’s ask that question again… is Fairfax a growth company? Yup.