Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

Article discussing the Straight of Hormuz. I have been asking: “when will it open?” Implicit in that question is “when will it get back to normal?” Perhaps we see the straight open. With a much lower number of tankers getting through (you pick the reason why). A better outcome than what exists today… but still pretty bad for the global economy. Look at what the Houthis (with their limited resources) did to shipping in the Red Sea… lasting for an extended period. ————— Iran does not need to close the Strait of Hormuz to disrupt it The real threat lies not in blocking the waterway, but in quietly turning its approaches into a zone of uncertainty that global shipping cannot ignore. https://www.aljazeera.com/opinions/2026/3/20/iran-does-not-need-to-close-the-strait-of-hormuz-to-disrupt-it

-

@73 Reds, I have no opinion today on if the war should have been started. I do not have enough information. Like why the US/Israeli's did what they did - we will find out when memoirs are written down the road. My point is we are in the very early stages (the '*uck around' part) - the fun part. The 'find out' part is coming - sometimes the not so fun part. All I am saying is I also have no idea how this is going to play out. Is it proper to characterize what the US/Israeli's have done so far as 'reckless'. Given every thing we have been told it certainly points in that direction to me. But I remain open minded. Again, we will only know with the passage of time. "*uck around and find out" (FAFO) is a slang phrase acting as a warning that reckless actions (*ucking around) will lead to severe consequences (finding out). It implies a direct relationship between irresponsible behavior and negative outcomes, acting as a "told-you-so" retort or a cautionary threat regarding natural consequences.

-

It takes two to tango. If the US 'packed up today and left', yes, the bombing of Iran from the US might stop. What if Iran keeps the Straight of Hormuz closed? Iran would be idiots to open the straight without guarantees from US/Israeli's. My guess is the Israeli's will not hesitate to continue taking out the Iranian leadership moving forward. Like the war in Iraq, and Afganistan, and Vietnam, etc... it is pretty hard to evaluate how the various parties have done in a war when we are three weeks in. We are still in the 'rah-rah' Disney phase of this war (for the US anyways).

-

Interesting take on the war in Iran from a 'barrel counter.' No idea how it plays out... the longer it continues the more disruptive things get (economy, inflation, bond yields, equities etc). The solution is pretty simple: the key actors (Trump and the Iranian regime) simply need to act rationally. Of course, that is probably the biggest reason why the war continues... Perhaps another way to look at it... who gets hurt more if the war continues? I think it is Trump/US. This is because we are likely getting to an inflection point with the world economy / inflation / interest rates etc. The pressure on Trump/US will start to ratchet higher - and the severe adverse impact on the US (inflation, interest rates, economy, financial markets etc) will likely start to emerge more fully. What a crazy situation.

-

Fairfax did not tell us on the Q4 conference call (they usually do). I took this to mean that it was lower. I think the last number we got from the company was 2.4 years. If current trends continue in financial markets, there are going to be a lot of puts and takes when Fairfax reports Q1 results: Equities sell off Spike in bond yields I will update my equity tracker at quarter end. Volatility is a very good thing for Fairfax. For example: the spike in bond yields will allow Fairfax to extend duration, which will lock in $2.5B in interest and dividend income for a few more years. But it will result in a sizeable loss in fixed income (offset by a large gain due to IFRS - not sure of magnitude). So there will be some short term noise. But long term gain.

-

Fairfax's $50B fixed income portfolio is positioned very conservatively: Low average duration Mostly in government bonds 6 months ago there was a lot of hand wringing about falling rates and what this would do Fairfax's interest income. Bond yields across the curve are spiking. The 2 year Treasury yield is up about 50 basis points over the past 3 weeks. This will give Fairfax the opportunity to extend the average duration of their fixed income portfolio. Interest and dividend income is Fairfax's largest income stream. Extending the average duration would lock this income stream in at a very high level ($2.5B) for a few more years. Bottom line, Fairfax's fixed income portfolio is perfectly positioned for the current environment.

-

@petec, your comment above is one of the reasons why I love this board so much. Your critique (as per usual) was focussed on ideas and logic. Not personal. Please keep them coming (you and others). Healthy debate is one way we all learn and improve as investors (and hopefully generate better results over time).

-

@bearprowler6, you make a great point. And I whole heartedly agree.

-

Agreed. The impact of this will be very asymmetrical depending on where you live. Europe looks screwed. Among other things, they need to get their LNG filled before the next winter.

-

Well said. Volatility = opportunity. Great volatility = great opportunity. The key is to not get so bent out of shape that you miss the opportunity. For interest sake, what sectors are you seeing the greatest opportunities right now? (I.e. 20 to 40% gain in next 6-12 months.) my guess is that is not market averages (off about 6 to 8% from all-time highs).

-

I don’t think Trump is going to learn anything. Some in the US will. But I don’t think it probably matters. It is crazy times. Look how easy it was for Trump to do what he just did. And the impact is is having on the rest of the world (not the US). He is 18 months into his term. We all still have 2.5 years to go.

-

Another interesting angle is the US. Gulf countries partnered with the US because they felt it would provide security - who would dare attack them? What they learned is the US doesn’t give a shit about them. Trump said only 1% of US energy needs come from the Gulf region - the current excursion is a big nothing burger for the US economy. My guess is - much like the rest of the world - the Gulf region will be putting their big boy pants on after the war and taking more control of their security. This probably also means finding a more reliable long term partner - one that is more aligned with their interests. Can anyone say China? The tectonics of the geopolitical world are shifting. PS: The US is not ‘winning.’ China and Russia? Big-time winners from what is going on in the Gulf. For these 2 countries, Trump is the gift that keeps on giving - and my guess is Trump is not done giving by a long shot. He is looking more and more like a cancer - easy to miss in the short run but eventually devastating in the long run.

-

One of the interesting things is closing the Straight of Hormaz is a one-time event for Iran. They only get to play this card once. And that is because every Gulf country will be implementing a back up plan once the current conflict ends (pipelines etc). The fact that virtually no one has a back up plan tells you something about what participants thought the likelihood of this event was in the first place. Now they have new information. My point is Iran has to get everything they want before opening up the Straight of Hormuz. Because they will never have this much leverage over the world/region ever again. It really is an interesting situation.

-

The short answer is we do not have enough information today… what is happening has never happened before. We may learn prospectively that it was a big nothing burger. Of that is was a big deal. Or something in between. What happened in the 1970’s was unthinkable when it happened. As a result, it was probably underestimated - especially in the beginning - in terms of its ultimate impact of the economy, inflation, interest rates and financial markets (not to mention geopolitics). I have no idea how the current situation plays out. It probably isn’t a big deal. But the chances it might be a big deal are increasing - the longer it lasts and if it keeps escalating.

-

Financial markets look a little like they did back in Jan/Feb of 2020. In North America we knew Covid was coming - and countries like China shut down their economies. How did financial markets in North America respond? Crickets. Well for a couple of months anyways. And this makes sense - who had seen Covid before? Fast forward to today. Of course the situation today is completely different. But it is the same in one important respect… we have never seen before what is happening today (war in middle east, closure of straight of Hormuz, energy infrastructure being shuttered/destroyed). Covid was a massive demand shock. This is a massive supply shock. This could be a big nothing burger - financial markets could well be right (that is what is priced in today). Like when Covid hit, I am not so sure…

-

The original investment in AGT ($150M) was made in July 2017. The driver of this investment was a guy named Paul Rivette. Three things stand out with this investment: Very dynamic founder (magnetic personality) Terrible balance sheet Terrible business (commodity business - no moat and highly volatile). After Fairfax’s initial purchase in 2017 the business results got worse. To the point it had to be taken private (requiring Fairfax to invest another $220M in April 2019 to stop the bleeding). How has the business performed over the past 7 years? It still looks like a pretty tough business - just look at how the IPO went and where the stock is trading today. What we do know about Fairfax is they do not walk away from investments… even when they probably should (no idea why this is). Farmers Edge and Boat Rocker (also from the 2014 to 2017 vintage) are still costing Fairfax $. My view is Seaspan was the first ‘new Fairfax’ investment. Sokol was a proven operator (not just a good talker) Fairfax’s investment was focussed on fixing the balance sheet of the company Sokol’s vision was to transition Seaspan from a container shipper to a finance company (largely eliminate the volatility of the business). AGT and Seaspan are great examples of old Fairfax and new Fairfax. Now 2017 to 2019 was a transition. I think Fairfax probably knew in 2016 or 2017 they needed to make some changes to their investment framework. So the shift was gradual over a couple of years. Fast forward to today… when was the last time they made a terrible investment? Their hit rate went from less than 30% (pre 2018) to over 90% (post 2018 and later). That might be a fluke. Or because the macro gods smiled on them. I don’t think it is primarily either of those - I think it is because they implemented a better framework: Premium on strong management (not just good talkers) Strong balance sheet Profitable operations (minimizing mom/dads need to bail kid out when they mess up financially) And now that they see how well the new investment framework works - they are likely institutionalizing it.

-

Sigma Companies International – March 2025 – Base Hits Matter As we work our way through Fairfax's 2025 annual report, we have been highlighting a few of the things that caught our attention. The Sigma sale (and sizeable realized gain) is both important and instructive for a number of different reasons. That is what we explore in our short post today. Value Investing in Practice “All intelligent investing is value investing — acquiring more that you are paying for. You must value the business in order to value the stock.” Charlie Munger The Sigma investment is a clear example of value investing in practice. In 2017, Fairfax invested $41.4 million to acquire an 81% interest in Sigma Companies International Corp. For Fairfax, this was a relatively small investment. Seven years later, Fairfax realized $327 million of total value: $284 million cash received $43 million retained ownership interest $178.7 million realized gain The investment delivered a 31% compound annual return. The formula is simple: 1. Buy a good business at a price well below its value. 2. Support strong management. 3. Be patient. Value investing may be out of favour in many parts of today’s market, but it continues to work exceptionally well for Fairfax. Sigma is simply one of the latest examples. In recent years Fairfax has also realized significant gains from investments such as Poseidon (2026), Orla Mining (2025), Stelco (2024), Ambridge Partners (2023), Resolute Forest Products (2022) and pet insurance (2022). Corporate Baseball Sigma highlights another important feature of Fairfax’s investment approach. The initial investment was small, but the outcome was meaningful. Fairfax has produced several “home runs” in recent years — investments that generated over $1 billion in gains. But the company has also produced many “singles” — investments that created $100 million or more in value, like Sigma. In baseball terms, Fairfax has been hitting for both power and average. The home runs attract the headlines. The singles quietly keep the scoreboard moving. Importantly, Fairfax is not simply swinging for the fences. The company’s investment process has evolved in recent years. It is making more consistent contact — generating a steady stream of profitable investments. Each successful investment moves the runners around the bases. Capital is redeployed into new opportunities, compounding over time. In corporate baseball, that combination — consistently getting on base and power — is what wins championships. Comments from Prem about Sigma from Fairfax's 2025AR. In 2017 we purchased an 81% interest in Sigma Companies International for $41 million. Led by Victor Pais, Sigma is a manufacturer and supplier of products used in water, stormwater and drainage infrastructure. Victor and team did an outstanding job navigating some turbulent times while at the same time building a great company. Early in 2025, Victor sold the company, with our interest being $284 million cash and a 16% ownership in the acquiring company worth $43 million for a 31% annual compound return. We wish Victor and the team all the best in the future. Comments about Fairfax’s initial investment in Sigma from Fairfax’s 2017AR “On August 2, 2017 the company acquired an 81.2% non-voting equity interest in Sigma Companies International Corp. (‘‘Sigma’’) for cash consideration of $41.4. Sigma, through its subsidiary, is engaged in global water and wastewater infrastructure projects.” Fairfax’s 2017AR

-

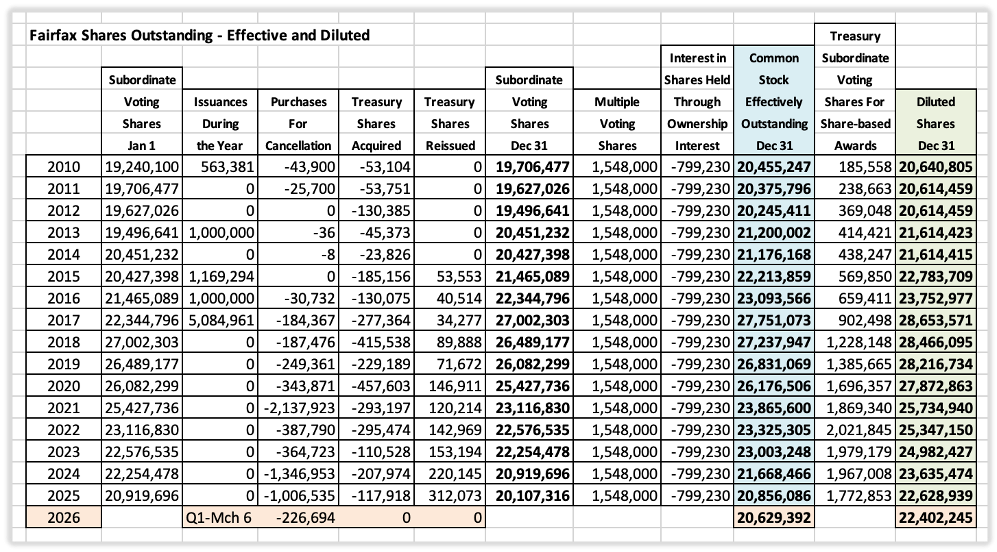

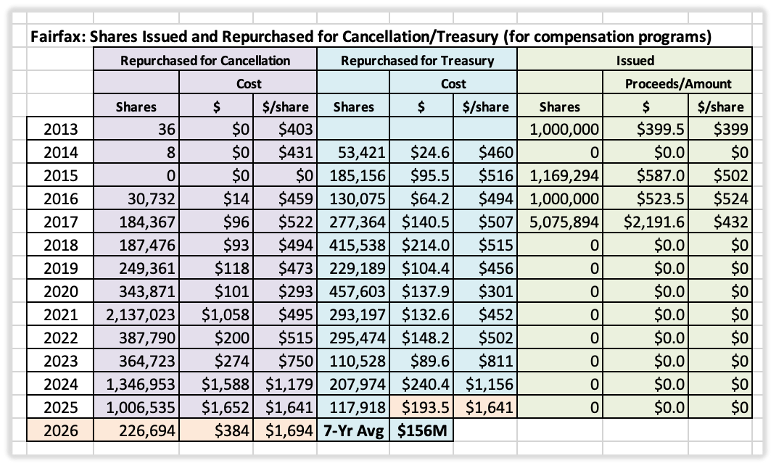

Shares Outstanding – Effective and Diluted As I have said many times before, I am not an accountant. Please let me know if I have messed up with my post below Fairfax’s share count tells an important part of the company’s capital allocation story. Over the past 15 years, two major trends stand out: 2013 to 2017: share count increased as Fairfax funded a significant international expansion in property and casualty insurance. 2018 to 2025: share count declined sharply as Fairfax repurchased shares aggressively at prices well below intrinsic value. As a result, Fairfax’s share count is now approaching 2013 levels — even though the company itself is much larger, more diversified, and more profitable than it was back then. That decline in share count has materially boosted per-share results, especially: earnings per share (EPS) book value per share (BVPS) But there is an important wrinkle. Diluted shares outstanding have not fallen nearly as quickly as basic shares outstanding. Why? Because Fairfax has been buying back shares aggressively while also using stock-based compensation programs to encourage long-term employee ownership. That distinction matters for investors. Why investors should care For Fairfax shareholders, share count is not just an accounting detail. It directly affects per-share value. If the share count falls, each remaining share owns a larger piece of the business. That lifts per-share measures like EPS and BVPS. But not all share counts tell you the same thing. Basic shares tell you how many shares economically participate in the business today. Diluted shares tell you how many shares could participate in the future after stock awards vest. Both matter. But they answer different questions. Basic, effective, and diluted shares Basic shares outstanding Basic shares outstanding are the shares currently issued and outstanding, excluding treasury shares. Basic shares outstanding = issued shares − treasury shares These are the shares currently entitled to the company’s earnings and book value. For most practical purposes, this is the current economic share count. Effective shares outstanding Investors sometimes use the term effective shares outstanding to mean the share count that reflects the actual economic ownership of the business today. At Fairfax, effective shares are essentially the same as basic shares outstanding. That is because treasury shares have already been removed from the outstanding share count. They do not currently participate in earnings or book value. So when analyzing Fairfax: Effective shares ≈ basic shares outstanding This is the share count that should be used when thinking about book value per share. Diluted shares outstanding Diluted shares outstanding include not only current shares outstanding, but also shares that may be issued in the future under stock-based compensation plans and other equity-linked arrangements. These can include: restricted share awards RSUs other share-based compensation Diluted shares are therefore higher than basic shares because they reflect the potential future share count. This is why diluted shares are used in calculating EPS. Why Fairfax’s diluted shares have not fallen as quickly The answer lies in Fairfax’s compensation programs. Fairfax has been repurchasing shares aggressively, which reduces basic shares outstanding. At the same time, Fairfax grants stock-based awards to employees that vest over time. These awards are included in diluted shares outstanding before they fully vest. So the math works like this: buybacks reduce basic shares unvested stock awards keep diluted shares elevated That is why diluted shares have not been falling like the basic share count. It is also worth noting that the increase in treasury shares over the past decade largely reflects the growth of the organization itself. As Fairfax expanded globally and added employees, the company accumulated additional treasury shares to support its stock-based compensation programs. Over the past seven years, Fairfax has spent about $155 million per year on average purchasing shares for treasury to support these programs. Fairfax’s stock-based compensation is different from most companies This is where Fairfax stands apart. At many companies, stock-based compensation is a source of ongoing dilution because new shares are issued to employees year after year. Existing shareholders end up paying the price through a steadily rising share count. Fairfax’s approach is different. Instead of issuing new shares, Fairfax generally buys shares in the open market and holds them in treasury. When employee awards vest, those shares are reissued from treasury. That distinction matters. Economically, Fairfax is not printing new shares out of thin air. It is using cash to buy stock in the market and then using those shares as compensation. That makes Fairfax’s stock-based compensation look much more like cash compensation delivered in stock form than the typical Silicon Valley model of endless dilution. What Prem says Prem Watsa explained the philosophy clearly in Fairfax’s 2025 Annual Report: “We continue to encourage all our employees to be shareholders of Fairfax. We think it will be a great investment for them over the long term and great for the company to have our employees as shareholders in the company.” He also described how the executive bonus program works: “As part of that initiative, close to 10 years ago we decided to have a general principle that our annual bonuses to senior executives across the company would be awarded 50% in cash and 50% in Fairfax shares that vest in five years.” And importantly: “As these bonus shares are awarded, the company buys the shares in the market … and they are recorded as treasury shares… As the shares are vested and or exercised, the shares are then reissued and come out of treasury shares and back into shares outstanding.” That is an important point for investors: Fairfax is buying the shares in the market first. That reduces the risk of the kind of structural dilution often seen elsewhere. The two key programs 1. Executive annual bonus program Senior executives receive annual bonuses: 50% in cash 50% in Fairfax shares with a 5-year vesting period This structure encourages long-term thinking and ties compensation to the long-run performance of Fairfax stock. 2. Employee Stock Ownership Plan Fairfax also has a broad employee stock ownership plan available to most employees. Employees may allocate up to: 10% of salary into Fairfax shares The company then matches: 30% automatically up to an additional 20% if performance targets are met, primarily underwriting profitability This is not just an executive perk. It is a broad ownership program designed to make employees think like owners. That matters culturally. Why this can benefit long-term shareholders Stock-based compensation often deserves skepticism. In many companies, it is overused, poorly structured, and highly dilutive. But Fairfax’s system has several features that make it more shareholder-friendly. 1. It aligns employees with shareholders Employees become owners. Their upside is tied to Fairfax’s long-term per-share performance. That is especially important in a decentralized organization where culture and capital allocation discipline matter. 2. It improves retention Long vesting periods create an incentive for talented employees and managers to stay. That matters at Fairfax, where long-term underwriting discipline, investment judgment, and operating autonomy are core advantages. 3. It is a real expense Fairfax’s stock-based compensation is not free. It runs through compensation expense. So the cost is already reflected in earnings. This is a crucial point. Investors should not pretend the compensation has no cost. But neither should they treat it as if Fairfax is simply handing away stock at no economic sacrifice. Fairfax is paying employees, and part of that pay is delivered in stock purchased with cash in the open market. 4. It may reflect smart capital allocation An underappreciated feature of Fairfax’s approach is timing. Over the years, Fairfax appears to have built a meaningful treasury stock position when its shares were available at attractive prices. If that is what happened, then management was not only funding compensation programs — it was also allocating capital intelligently. In that case, treasury shares may represent a stockpile built at favorable prices for future employee compensation. That is very different from careless dilution. So which share count should investors use? For book value per share: Use basic/effective shares outstanding Why? Because unvested awards are not yet outstanding shares. They do not currently participate in book value. For earnings per share: Use diluted shares outstanding Why? Because EPS is meant to capture the earnings attributable to the share count that could exist after awards vest. Bottom line Fairfax’s share count story is driven by two opposing forces: buybacks, which reduce the current share count and increase per-share ownership stock-based compensation, which creates a pipeline of future shares included in diluted share count The result is that: basic/effective shares show the ownership structure today diluted shares show the potential ownership structure after stock awards vest For Fairfax, this distinction is especially important because the company’s stock-based compensation program is not typical. Fairfax is not relying on endless issuance of cheap stock. It is generally buying shares in the market, expensing the compensation properly, and using long vesting periods to build an ownership culture across the organization. That does not mean the program is costless. It is not. It is a real compensation expense. Over the past seven years, the company has spent about $155 million per year on average purchasing shares for treasury to support these programs. But for long-term shareholders, Fairfax’s approach appears far more aligned, disciplined, and shareholder-friendly than the stock-compensation models used by many other companies. In short, Fairfax’s program does create some dilution in diluted EPS. But it also strengthens culture, retention, and alignment — and it does so in a way that is far more thoughtful than the typical corporate SBC playbook.

-

An update to an important story… India to Cancel IDBI Bank Stake Sale Due to Low Bids India plans to cancel the bids received for a majority stake in IDBI Bank as they fell short of the minimum price required, according to sources. Bloomberg posted on X, highlighting that the decision comes after evaluating the financial offers submitted by potential buyers. The government had aimed to divest its stake in the bank to raise funds and reduce its involvement in the banking sector. However, the bids did not meet the financial expectations set by the authorities, leading to the decision to scrap the sale process. The move reflects the challenges faced in attracting investors willing to meet the valuation criteria for state-owned assets. The government will now reassess its strategy for the bank's divestment, considering alternative approaches to achieve its financial objectives. https://www.binance.com/en/square/post/03-13-2026-india-to-cancel-idbi-bank-stake-sale-due-to-low-bids-301151962570865

-

The war in Iran has been a massive gift for Russia for two simple reasons: With the price of oil skyrocketing they are likely making big money As the US depletes its stores of weapons in Iran/region, they will have little to send to Ukraine The longer the war goes the better for Russia. Do you think they are helping Iran out behind the scenes? (Follow the money is probably instructive in this case...)

-

My mental model in the war in Iran is the US and the Israeli's are 'in control.' I am wondering if this is accurate today. Iran 'controls' the Straight of Hormuz. The longer they remain in control of the straight, the more their position improves. (Iran simply needs to not lose.) My assumption has been that Trump and Isreal will exit (declare victory) and the war will be over. But what if Iran keeps the Straight of Hormuz closed? It makes no sense to me that Iran would open the straight without a signed deal with the US/Israeli's (the fact that Trump is unreliable - putting it politely - is another fly in the ointment). The current leader of Iran had his father, wife and kid killed by US/Iranian strikes. He knows the US/Israeli's are now actively trying to take him out. How do you negotiate with someone who is actively trying to kill you? My guess is Iran is motivated to inflict pain on the US. How? Keep the straight closed for a couple of months. Oil at $150 (or even $200) will cause inflation expectations to ramp higher - this will cause interest rates to ramp higher. Obviously, the stock market expects this to be a big nothing burger (averages are near all time highs - which is almost always the right call). No idea how this plays out. The Straight of Hormuz has never been shut down before. We are in uncharted waters. What makes this conflict so interesting is the pain it is causing is highly disproportionate. It is barely (so far) impacting the US. It is having a big impact on oil importing countries (Europe, India, Japan etc). And it is having a massive impact on the economies of Gulf countries (who were not consulted before hand). This will likely become a much more important story the longer the straight remains closed. Trump is the master a pivoting when he needs to. I am starting to wonder if he has miscalculated this time. We will find out in the coming weeks and months. Crazy times. There is a reason no previous president has done what the US/Israeli's have just done - the risk of the Straight of Hormuz being closed for an extended period was too high (and the catastrophic impact this would have on the global economy). We are now in uncharted territory. Trump might be about to learn a very hard lesson: wars are very easy to start. And sometimes much more difficult to end. PS: Having said all of that, by base case is this ends up being a big nothing burger for financial markets. But it looks to me like the tail risks are getting larger the longer the straight remains closed.

-

@Duke In Shadows, yes, I was thinking about how I wroded that part... I changed my original to: "When describing what he learned from George Soros, Stanley Druckenmiller has said that what matters in investing is not simply whether you are right or wrong, but how much money you make when you are right and how much you lose when you are wrong. Poseidon is a textbook case. Fairfax was right — and the position was large enough to matter." I can't change the actual post (I am not able to edit my longer posts - I usually get an error message when I try). When it comes to the associate/private holdings, Fairfax has been doing a very good job of working closely with management - and this includes coming up with a mutually agreed to exit strategy. Especially for the large positions. That is much easier for Fairfax when the management team is very good.

-

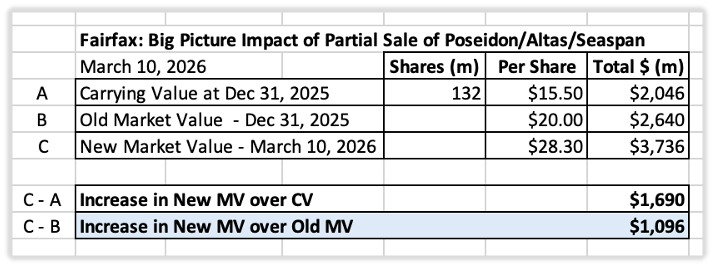

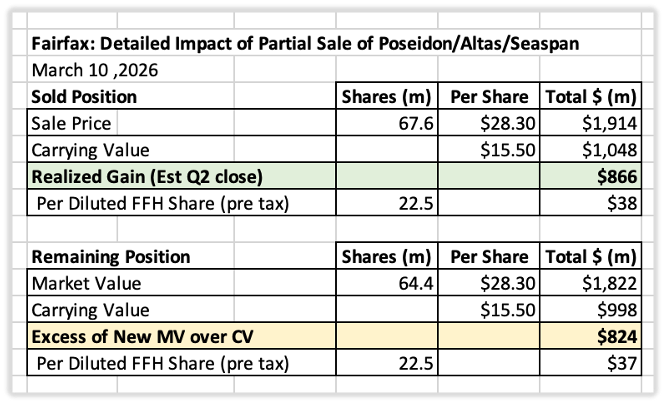

@djokovic1, I appreciate the comment. there are so many interesting angles to the Poseidon sale. A big one for me is the hidden value theme (that it is much more than most people realize) and that it will become a more important driver of future reported results (as positions get monetized). Both of those ideas are being confirmed with the Poseidon sale. In terms of Mr. Market, there has been one constant in the 25 years I have been following Fairfax - Mr. Market just doesn't like the company, its leadership and its business model. (The 'proof' is the stock price.) There are lots of reasons for this. While it is a little annoying at times (like today), it really is a very good thing for Fairfax. And that is because it will give them the opportunity to continue to buy back ~1 million shares every year at a very attractive valuation. 2026YE P/BV = ~1.15, and an investor gets all the hidden value for free (it will provide a material boost to future earnings like we are seeing this year with Poseidon). That is crazy cheap for a company like Fairfax. 1H 2026 is shaping up to be a very active and interesting period for Fairfax: Sources of capital: Debt Issuance: $475M ($292 + $183) Eurolife sale: $945M Poseidon sale: $1.9B Dividends from insurance co's: ? Uses of capital: Dividend payment: ~$300M YTD Share buybacks: $384 ($1,692/share) Some share buybacks will be for compensation programs AGT IPO: $400M (~$250 conversion + $150 new) Under Armour: ~$150M (increase in position) Kennedy Wilson take Private: $1.65B Allied World: $1B? (buy out minority partner) IDBI Bank: $8B? (no idea on if this happens or amount) Bottom line, Fairfax has a lot of uses of capital. So it is not surprising to see them monetize 50% of Poseidon. I would not be surprised to see them monetize one or two more positions. ---------- As @glider3834 pointed out: 'Subsequent to December 31, 2025, the company purchased for cancellation 226,694 subordinate voting shares under the terms of its normal course issuer bids at a cost of $384.0'

-

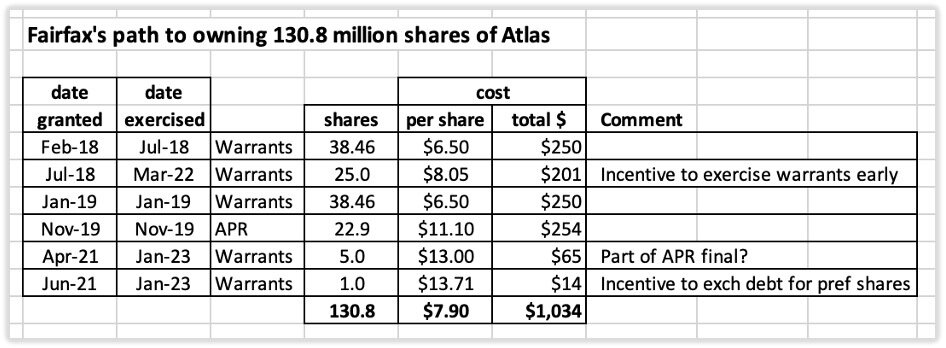

Poseidon: Fairfax’s Latest Capital Allocation Home Run Fairfax has been delivering a capital allocation master-class over the past five years. That may sound like hyperbole. It is not. All one has to do is look at the facts — at what management has actually done, not what the market says about it. The latest example arrived yesterday morning with Fairfax’s partial sale of its Poseidon investment. This is a significant transaction. Not only because of its immediate financial impact, but because of what it reveals about Fairfax’s business model, its investment framework, and management’s increasingly impressive record as capital allocators. A Big Transaction in a Big Holding Poseidon is Fairfax’s third-largest equity holding. At December 31, 2025, Fairfax carried its investment in Poseidon at approximately $2.0 billion, or $15.50 per share, while the position’s market value was approximately $2.6 billion, or $20.00 per share. That meant excess of fair value over carrying value stood at roughly $600 million. Yesterday, Fairfax announced that it had agreed to sell approximately 50% of its Poseidon position — 67.6 million shares— at $28.30 per share, for aggregate proceeds of approximately US$1.91 billion. That sale price changes the picture dramatically. At $28.30 per share, Fairfax’s full Poseidon stake is effectively being valued at approximately $3.7 billion. Compared to year-end 2025, that is an increase of roughly: $1.7 billion above carrying value $1.1 billion above market value That is a very large uplift in value on one of Fairfax’s largest holdings. How the Value Shows Up What makes the transaction especially interesting is that it surfaces value in two different ways. First, Fairfax will record a realized investment gain on the shares being sold. On the roughly half of the position that is being monetized, the company is expected to book an investment gain of approximately $866 million when the transaction closes in the second quarter. Second, the sale price establishes a fresh market-based valuation benchmark for the half of the position Fairfax continues to own. After the sale, Fairfax will still retain an ownership interest of approximately 22.1% in Poseidon. Using the transaction price, the remaining common equity stake would have a market value of about $1.8 billion. Excess of fair value over carrying value on that remaining position rises to approximately $824 million, up from $600 million at year-end. Put differently, this one transaction surfaces roughly $1.1 billion of additional value for Fairfax shareholders between the realized gain and the higher implied value of the continuing stake. That is an outstanding result. Fairfax has, in effect, managed to have its cake and eat it too: it has crystallized a very large gain while still retaining a significant ownership interest in the business. A Home Run, Made More Powerful by Size The investment performance since inception is remarkable. Fairfax first began investing in Seaspan in 2018. Over a period of roughly four years, it invested a little over $1 billion to build a position of approximately 132 million shares, representing about 43% of the company. Very rough math suggests Fairfax paid about $7.90 per share on average. Today’s sale price is $28.30 per share. That means an initial investment of roughly $1 billion has now become a position worth approximately $3.7 billion, before considering the dividends Fairfax has received along the way. Include those dividend payments and the total value created likely approaches $4 billion. On very rough math, Fairfax has generated close to $3 billion of profit from this investment over an eight-year period. Yes, the percentage return is excellent — roughly 300%. But what makes the outcome truly exceptional is not simply the return. It is the size of the bet. Back in 2018, Fairfax’s common shareholders’ equity was approximately $11.8 billion. A $1 billion investment was not a small side position. It was a major capital allocation decision. It was a high-conviction bet. Stanley Druckenmiller once observed that what matters in investing is not simply whether you are right or wrong, but how much money you make when you are right and how much you lose when you are wrong. Poseidon is a textbook case. Fairfax was right, and the position was large enough to matter. Mr. Market Still Does Not Quite Get It As is so often the case with Fairfax, the market’s reaction was curiously muted. Despite the scale of the transaction and the value it surfaces, Fairfax shares finished the day up only about 1%. That reaction suggests that many investors still do not fully grasp either the immediate financial implications or the broader significance of what management has accomplished. This is not new. Fairfax has often monetized assets at attractive prices with surprisingly little market recognition (initially). One is reminded of the sale of the pet insurance business in 2022, which generated a gain of roughly $1.2 billion and was likewise not met with the kind of re-rating one might have expected. That the stock did not sell off this time may count as progress. Earnings Estimates Are Going Higher This transaction also has a near-term consequence that should be obvious: analyst estimates for 2026 are likely headed higher. Between the Poseidon sale and the recently announced sale of Eurolife’s life insurance business, Fairfax is now set to book approximately $1.2 billion of investment gains in the second quarter alone: Poseidon: ~$866 million Eurolife life insurance business: ~$350 million That is about $53 per diluted share after tax. The amount is material, and it is not reflected in analyst models today. Upward earnings revisions are coming. More importantly, we are only about ten weeks into the year. There are still more than forty weeks to go. Fairfax may well surface additional value before 2026 is done. Against that backdrop, an earnings estimate of $190 to $200 per diluted share for 2026 is beginning to look conservative. At a share price of roughly $1,685, Fairfax is trading at less than 9 times normalized earnings. For a company with Fairfax’s collection of assets, balance sheet strength, management quality, and capital allocation track record, that remains a remarkably low valuation. The Hidden Value Flywheel For some time now, we have been making the case that Fairfax is carrying a very large amount of hidden value on its balance sheet. At year-end 2025, a conservative estimate placed this figure at more than $4.5 billion. To some, that may have sounded overly optimistic. Transactions like this are a useful reminder that hidden value is not imaginary. It is simply unrealized — until management chooses to realize part of it. That is an important distinction. The Poseidon sale did not create value out of thin air. It revealed value that had already been built inside the business and its investment portfolio. And importantly, this transaction only modestly reduces the broader reservoir of unrealized value that still resides within Fairfax. That is why this matters so much. The sale of Poseidon is not just a one-off gain. It is evidence that Fairfax’s hidden value flywheel is real and that it can become a meaningful source of future reported earnings over time. Fairfax Sells Assets — That Is Part of the Model One of the recurring mistakes made by investors analyzing Fairfax is to treat asset sales as unusual or non-recurring. They are neither. Monetizing assets is a normal part of Fairfax’s business model. It has been for decades. Why does Fairfax sell assets? First, to realize strong returns. Second, to improve the quality of the company by recycling capital into new opportunities with superior prospective returns. This is what good capital allocation looks like. It is not passive. It is not static. It is a continuous process of building value, harvesting value, and reallocating capital. Will the gains be lumpy from quarter to quarter or year to year? Of course. But over a two- or three-year period, the pattern is much smoother and much easier to understand. Fairfax’s investment gains should not be viewed as random windfalls. They are better understood as the periodic monetization of value that has been compounding quietly beneath the surface. Poseidon is an excellent example. New Information Matters The other important thing this sale provides is information. Fairfax has been steadily increasing the size of its private equity holdings. By definition, these positions are harder for outside investors to value with confidence. Public marks are limited. Accounting carrying values can understate economic value. As a result, many observers default to skepticism. Asset sales help solve that problem. They create market-based reference points. In this case, Fairfax sold approximately half its Poseidon position to three separate buyers, including one existing shareholder increasing its stake and two new strategic investors. It is reasonable to conclude that these are informed counterparties and that $28.30 per share is a credible estimate of current fair market value. That matters not just for Poseidon, but for how investors should think about Fairfax’s broader portfolio of privately held assets. “Bet on the Jockey” Perhaps the most interesting aspect of the Poseidon investment is what it says about the evolution of Fairfax’s investment framework. My long-standing view is that Fairfax made an important adjustment around 2018. Management quality — the “jockey” — appears to have become an even more central part of the decision-making process. Poseidon was one of the earliest and clearest examples of this shift. Fairfax invested in Seaspan because of David Sokol. That was, at the time, a contrarian call. Sokol had once been viewed as Warren Buffett’s heir apparent at Berkshire Hathaway. After the Lubrizol episode, however, he was clearly out of favor in many circles. Fairfax looked past the controversy and focused on the underlying record and capability of the operator. That is classic contrarian investing: buy low, not only in securities, but sometimes in people’s reputations. It has worked out fabulously well. Over the past eight years, David Sokol and CEO Bing Chen have done an outstanding job building the business. Fairfax’s 2025 annual report makes this plain. Since 2017, the fleet has grown from 89 ships to 184, revenue has risen from $831 million to $2.5 billion, net income has increased from $175 million to $727 million, and earnings per share have climbed from $1.33 to $2.49 despite a much larger share count. Those are not the results of financial engineering. They reflect real operating execution. Fairfax’s gain on Poseidon is, in the end, the direct consequence of partnering with capable people and backing them with meaningful capital. 2018 Was a Very Good Vintage It is also worth noting that Poseidon was not the only example of this pattern. In 2018, Fairfax also made a major investment in Stelco, partnering with Alan Kestenbaum — another clear “bet on the jockey.” That investment, too, became a major success. Fairfax’s roughly $193 million initial investment ultimately delivered a total return of approximately $568 million, or about 294%, over six years. Some of that capital was likely recycled into Orla Mining in late 2024, which itself has already become another highly successful Fairfax investment. That sequence is worth studying. Fairfax identifies strong operators, invests at attractive valuations, supports them over time, monetizes when appropriate, and recycles the capital into the next above-average opportunity. This is not accidental. It is a system. Final Thought The Poseidon sale tells us several things. It tells us that Fairfax continues to uncover and monetize value in size. It tells us that the company’s hidden value is real. It tells us that management understands how to recycle capital intelligently. And it tells us that Fairfax’s growing emphasis on backing exceptional operators has produced excellent results. Most importantly, it tells us that Fairfax is still being underestimated. The market tends to focus on reported earnings in the next quarter. Fairfax is building value across a much longer time horizon. That difference in perspective continues to create opportunity for shareholders willing to do the work. Poseidon is not just a successful investment. It is a case study in how Fairfax compounds capital.

-

Shareholders got out of bed this morning to discover that they had been given a $1.1B gift. Fairfax sold ~50% of their position in Poseidon/Seaspan. In Q2 $FFH.TO will book ~$866M gain. Excess of FV over CV will increase to ~$824M (from ~$600M at Dec 31). Outstanding! Who says: "you can't have your cake and eat it (too)"? There are so many important take-aways from this transaction... What is the key take-away from this transaction for Fairfax shareholders? What says the mob at CofBF? The best part? The reaction from Mr. Market - the news was largely ignored (the stock - already dirt cheap - finished up on the day ~1%). It kind of reminds me of when Fairfax sold their pet insurance business in 2022 for a $1.2B gain - and the stock promptly sold off). So I guess we should be thankful?