Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

I always enjoy listening to Doomberg. Very rational. Very unconventional. He has no idea how the war in the middle east is going to play out. (That makes me feel better.) I think he thinks financial markets are asleep at the wheel…

-

+1. One of the things I love about investing is there is no one right way. The key is to find a framework that fits your intellect, psychological makeup and personal situation. You clearly have. Well done!

-

@Ulti, nice to hear your investment has been doing well. The BC government fought the expansion of the Trans Mountain pipeline expansion tooth and nail when it happened. Fortunately they were unsuccessful and the expansion went ahead. My understanding is there is an opportunity to now significantly expand the throughput of Trans Mountain. The BC government is now throwing this option out as justification for why no new pipelines are needed. My understadning is the Federal government has the ability to ok a pipeline project if it is ‘national in scope,’ But I think Carney is on record as saying he will only do national projects with the support of stakeholders (like provinces). The key will likely be voters. If support for a new pipeline continues to grow then the BC government will likely pivot - that is what they have done repeatedly in the past. I haven’t watched this podcast… but you might find it helpful.

-

@SharperDingaan, great post. I agree, Carney appears to be the right man for the times. To your point, he is not a career politician - he appears to have a plan and he is working the plan - with some urgency. Trump has absolutely been the most important catalyst. The fact Trudeau was epically bad is also working in his favour - hard not to look good after that performance.

-

Energy policy in Canada has been taken over by far left environmental groups. It now permeates government (legislation) and academia (what is taught). The narrative is energy (oil/gas) is the devil. It has become a core ideological belief. No discussion. No debate. If you want to debate their policies you are branded a climate denier (it is a wickedly effective way to shut down debate). I have an enormous amount of respect for what the left/environmental groups have been able to pull off. It was decades in the works. They were smart and methodical. The good news is Carney appears to be embracing a return to a more rational/pragmatic approach on important issues (beggars can't be choosers?). Canada has big problems. It needs to re-invent its economy. It is an energy superpower. The war in Iran will likely provide the country with a wonderful opportunity. We will see if the politicians are up to the challenge (it will require Federal and Provincial cooperation). They are doing things today that would have been unthinkable 18 months ago. Let's hope it continues. Politicians are being given lots of good 'excuses' to pivot energy policy to expand oil/gas. The NDP government in BC is probably the biggest obstacle today (far left and highly ideological). But with Carney as Prime Minister, Eby (Premier of BC) is looking and sounding more and more like an idiot on most important issues (when Trudeau was around he looked and sounded normal because they were singing off the same crazy song sheet). I am more optimistic. But being governed by ideologues is nuts (it's like being governed by a theocracy). PS: When it comes to oil/gas, I should also point out Quebec. When it comes to oil/gas their sensitivities are very similar to countries in Western Europe (those that despise oil/gas). It really is remarkable, given their receive massive transfer payments from Canada (they are technically a 'have not' province - a large portion of which comes from Alberta via oil/gas). Hypocrisy at its finest.

-

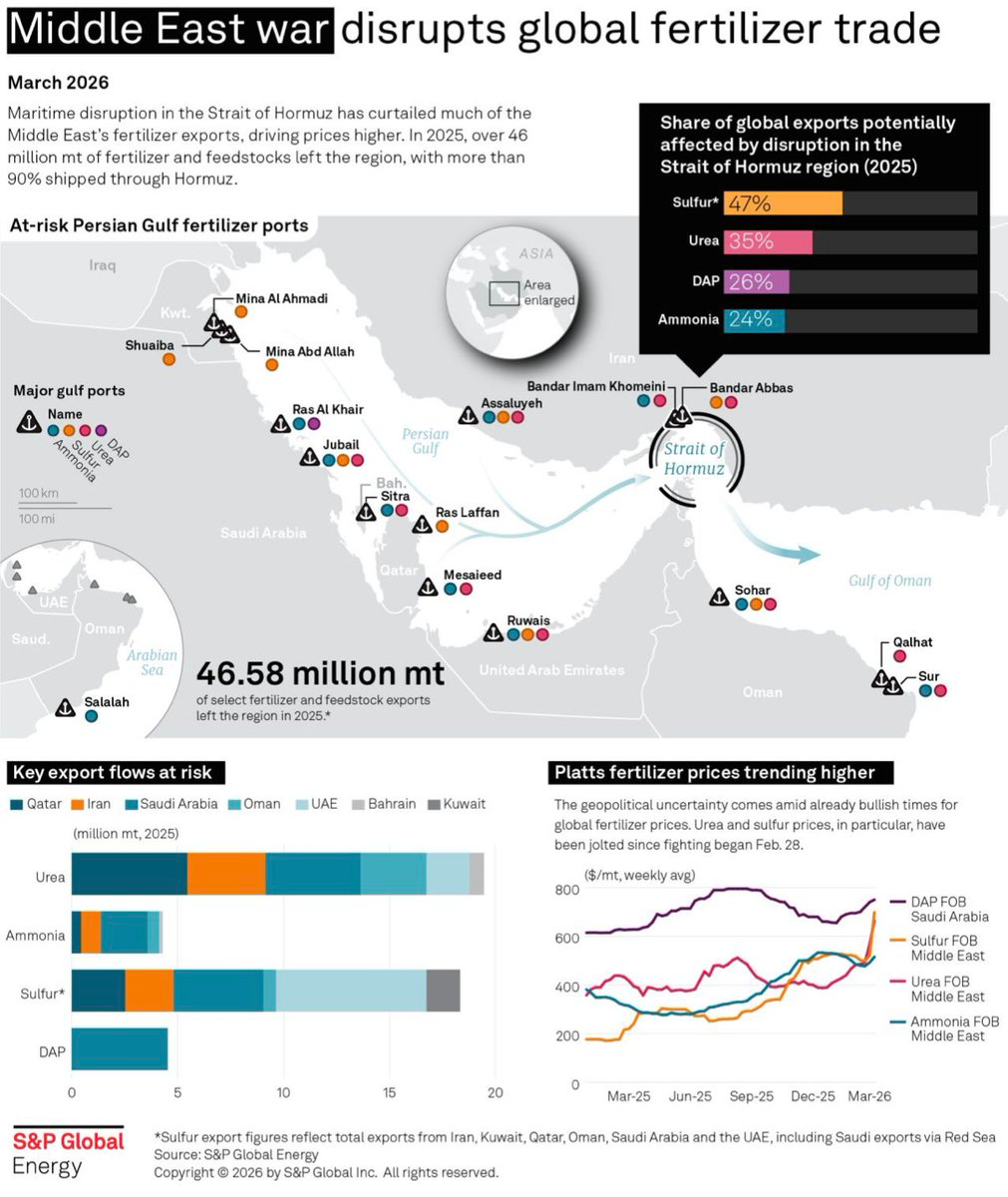

Here is a nice summary of importance of the Middle East to the fertilizer market. Like with oil and LNG, fertilizer is a critical input to the global economy. Much lower supply is a big problem. As is much higher prices.

-

@cubsfan, the US/Israeli’s have a massive military advantage. They appear to have performed each of their tactical missions very well. My focus is on the Straight of Hormuz. The last time checked, Iran was in control of the straight - Iran is deciding who gets through. A secondary point is Iran’s ability to send missiles and drones to destroy energy/civilian infrastructure in the Gulf - I think that threat remains. So despite the tactical success of the armies of the US/Israeli’s, it appears to me like Iran still has a great deal of leverage. My goal is primarily to understand what is going on. (And yes, I do like to use irony to make my points…)

-

I was a sceptic of Carney s at first. But the more I see the more I like. It looks to me like he is starting with getting Canada’s strategic positioning set: focus is on resources, selling to the world, being rational/pragmatic (a Canada first approach). His Davos speech summarized this nicely. Lately, we are seeing more tactical stuff (how he plans to make it happen). My guess is we will see more tactical stuff in the coming months. But it will take time - repositioning the Canadian economy is like moving a super tanker - it will take years. And the next couple of years could be pretty tough (we are just beginning to deal with our housing bubble). Canada lost its way for a decade. It went way left, got very ideological, destroyed the consensus that existed on important topics like immigration and completely blew out the deficit. And we had a housing bubble.

-

Here is a good graphic of the impact on oil markets of the closure of the Straight of Hormuz. It would be interesting to get the same for LNG and fertilizers. What you see below is the paper shortage. It largely hasn’t shown up yet as physical shortages. The longer the disruption goes on the more we will see it manifest in physical markets. Perhaps that is when financial markets start to care.

-

@cubsfan, personal attack? Really? I am happy to debate ideas.

-

@Xerxes, great point. The US and Isreal have very different objectives. At the same time, the ‘unthinkable’ is happening to all of the Gulf countries. What a toxic soup. Good to know it will all be resolved by the end of the week (financial markets are rallying). We are lucky to have Trump driving the bus.

-

@Parsad, you are assuming Trump, the Israeli’s and Iran are rational actors. I hope you are right and the worst is behind us. Below is what Iran wants. They have been very public in stating their aims. They have maximum leverage right now. Why would they give that up? Especially given everyone knows that Trump can’t be trusted to actually honour any potential deal (even his allies know this). It really is a crazy situation. I think there is a decent chance that Iran will ask for more than Trump/Israeli’s are willing to give. In that case, Iran would continue to block the straight and the war would have to continue. Financial markets are basically saying this war is over. Core Iranian Demands to End the Conflict 1) Immediate cessation of attacks (non-negotiable starting point) Iran consistently says the first prerequisite is that the U.S. and Israel stop all military operations This is framed as: “we did not start this war” → therefore the aggressor must stop first 2) Guarantees against future attacks Iran wants binding, enforceable guarantees that strikes will not resume They are explicitly rejecting: Temporary ceasefires “pause and resume” arrangements This is about regime security, not just tactical de-escalation. 3) Compensation / reparations Tehran is demanding financial compensation for war damage Some reports go further: Full reparations from the U.S. and Israel This is both economic and symbolic (accountability). 4) Withdrawal / rollback of U.S. presence in the region Iran has called for a U.S. withdrawal from the Gulf / regional military footprint This ties into a broader strategic goal: Reducing U.S. deterrence capability near Iran 5) Recognition of Iran’s rights and status Includes: Recognition of Iran’s “legitimate rights” (often interpreted as sovereignty + nuclear rights) This is ideological: Iran wants political legitimacy, not just a ceasefire 6) Punishment or accountability for “aggressors” Senior Iranian officials are demanding justice/punishment for those who initiated attacks This makes negotiations difficult because: It directly conflicts with U.S./Israeli positions

-

What did we learn over the past 24 hours. Trump is a master communicator - financial markets are loving it. What else did we learn? The US is not going to ‘obliterate’ Iran’s power infrastructure. (Can we say Iran won that game of chicken?) What about the Straight of Hormuz… what did we learn? Nothing has changed… and the status quo is likely to remain in place until Friday. The bad news is only small amounts of oil/LNG/fertilizer will be getting through. The longer this continues the more disruptive the consequences for the global economy - nothing has changed on that front (what is happening versus what is being said). The good news is we may have reached a short term stalemate - the US/Israel will stop bombing Iran and Iran will stop bombing the region. The fact the war is not escalating is good news. Where do we go from here? Hopefully we get a resolution of some sort this week. Because if we don’t, and more US resources get moved into the region, we could see things escalate again. What a crazy situation. PS: Here is where things get really interesting. If you are Trump and you want to escalate you need a reason. Well now that ‘peace talks’ have started… well, if they don’t result in a deal… well, Trump will not have choice… he will have his reason to escalate: he tried real hard at negotiations - but the Iranian’s were not interested in peace. He will have manufactured his reason to escalate the war. The best part? Whether actual negotiations are going on actually doesn’t matter. Yes, he is a diabolical genius.

-

Tail Risk - Is It Part of Your Investment Framework?

Viking replied to Viking's topic in General Discussion

@frommi, thanks for sharing. My basic strategy has been much more simple… when my ‘spidey sense’ starts to tingle I ‘buy cash.’ If the situation continues to deteriorate, I but more cash. The part that has always amazed me is financial markets tend to always look through the tail risk - markets stay high. This has helped me - as it provides time to collect more information and assess the situation. And usually gives me ample time to get my cash weighting to where I want it. I also think a person’s personal situation is quote important to this topic. As an example, I am: Retired More risk averse than when I was younger I have won the game (I have enough) My goal has shifted to capital preservation from return Most of my investments are in self directed tax free accounts. Transaction costs are near zero. And i don’t need to think about taxes. This gives me a great amount of flexibility (makes it very easy to move to cash and then to become fully invested again). My spouse is very risk averse Over the past 30 years I have been able to largely avoid every major market sell off. My guess is that has helped my returns. Where I have messed up is on the buy side after a big meltdown - often, I have been too pessimistic (slow to buy back in). My plan this time around is to scale back in using broad based index funds like XEQT. This gets around the problem of what to buy/circle of competence. -

The war in the Persian Gulf makes the discussion of tail risk timely. How do other board members think about this topic? Please note, I am not being a doomer here - I am not suggesting investors should head for the hills and move to 100% cash. Rather, I am simply wondering how board members think about the topic. It is rarely discussed... likely because it is generally best to ignore it. I find the topic to be very interesting. Because I think financial markets often get tail risks wrong. Which can create mouth watering opportunities for investors. My base-case assumption is the situation in the Persian Gulf gets 'resolved' (by 'resolved' the Straight of Hormuz gets opened and shipping returns to normal). But I thought this same thing 2 weeks ago - and so far I have been completely wrong... Tail Risk - Surviving What You Cannot Predict “The stock market is there to serve you, not to instruct you.” — Warren Buffett Introduction: The Wrong Question When geopolitical events emerge—such as the current conflict in the Persian Gulf—the instinctive investor question is: What should I do? Buy? Sell? Hedge? Get defensive? This is the wrong starting point. The right question is: What kind of event is this—and how does it fit within my framework? The conflict in the Persian Gulf is not a standard, forecastable variable. It is a tail risk. And tail risks require a fundamentally different way of thinking. What Is Tail Risk? Tail risks are low-probability, high-impact events that reside at the extreme ends of a probability distribution. In most environments: Outcomes cluster around expectations Volatility appears manageable Risk feels quantifiable Tail events violate all three. They are: Unexpected (relative to models) Discontinuous (they do not unfold smoothly) Systemic (they affect multiple variables simultaneously) Markets are not undone by what is expected—but by what is dismissed. The Buffett Lens: Focus on Survivability Buffett’s framework is not built on predicting tail events. It is built on ensuring they do not destroy you. Core principles: 1. Avoid permanent capital loss Not volatility—permanent impairment 2. Maintain financial strength Low leverage High liquidity Durable balance sheet 3. Stay within your circle of competence Avoid exposures you do not fully understand—especially under stress 4. Preserve optionality Cash and liquidity are not inefficiencies—they are strategic assets “You only find out who is swimming naked when the tide goes out.” — Warren Buffett Tail events are when the tide goes out. Why Tail Risks Matter Disproportionately Non-linearity of losses: A -50% drawdown requires +100% to recover. Compounding works against you. Destruction of the capital base Large losses reduce future earning power. Breakdown of diversification In stress: Correlations → 1 Liquidity disappears Forced selling dominates Model failure Standard risk tools assume: Normal distributions Stable relationships Continuous markets Tail events break all of them simultaneously. Historical Pattern: Ignored Until It Isn’t Markets repeatedly demonstrate the same behavioral flaw: They ignore risk—until they can’t. Case Studies 2008 Global Financial Crisis Structural fragility in housing and credit was visible. Action came only when collapse was unavoidable. 2020 COVID crash Information was available for months. Markets reacted only at the point of exponential spread. 1987 Black Monday A statistical impossibility—until it happened. LTCM (1998) Highly sophisticated models undone by correlation convergence and leverage. Bond bubble peak (2020–2021) Extreme duration risk ignored in a zero-rate environment. Dot-com bubble Valuation discipline abandoned until the system reset. The lesson: Tail risks are often observable in advance—but not acted upon. The Structural Drivers Tail events typically emerge from hidden fragility: Leverage Small shocks become existential threats. Liquidity illusion Assets assumed liquid cannot be sold without severe price impact. Correlation convergence Diversification fails when it is needed most. Reflexivity Selling triggers more selling. Feedback loops accelerate outcomes. These forces are always present. Tail events simply activate them simultaneously. The Core Investor Problem: How should you respond? In most cases: The correct action is to do nothing. Because: Tail risks rarely materialize Timing them requires two correct decisions: When to exit When to re-enter Few investors consistently achieve both. When “Do Nothing” Is Wrong The answer is situational. It depends on the tail risk (the Great Financial Crisis being perhaps the best example). And it depends on each investor's individual situation: Time horizon (age) Psychological (tolerance for volatility) Financial objectives (maximize return or preservation of capital) Portfolio structure Portfolio size (are you just getting started or have you already won the game?) Tax considerations There is no universal rule. And that is what makes the topic so interesting.

-

As the war with Iran continues, we are learning more about how the global economy works. Much of the analysis is focussed on oil and products refined from oil and LNG. There is another really important group of products produced in the Persian Gulf: fertilizers. And of course, fertilizers are a core input to grow food. For those not paying attention, food matters (availability and cost). A lot. What happens if the world runs short of fertilizer? People starve. Yes, not a problem for the US. They can afford to pay much higher prices. But much of the world can't. Bottom line, the longer the Straight of Hormuz remains closed the closer the global economy gets to crisis. On multiple dimensions. Of course the US/Israel knew this was likely how this whole thing was going to play out (Iran would block the Straight of Hormuz). And of course, they have a contingency plan for what to do. I wonder when they are going to let us know?

-

I hope you are right. It looks like we have a 1950’s game of chicken going on. Not sure that is the best way to resolve the war in the Persian Gulf… but it appears to be where we are at. The US/Israeli’s are driving the global economy car and Iran is driving the other car. Who wins in the game of chicken? In the classic game of chicken (two cars driving straight at each other), there isn’t a single “winner” in the conventional sense. The outcome depends on credibility, commitment, and psychology, not just courage. The payoff structure (intuition) Best outcome (individual): You keep going, the other swerves → you “win” Worst outcome (mutual): Neither swerves → catastrophic crash Second-best (mutual): Both swerve → no crash, but no dominance Second-worst (individual): You swerve, the other doesn’t → you “lose” Who actually “wins”? The player who convinces the other they won’t swerve. This is the key insight from game theory (Thomas Schelling): How does someone make that credible? 1. Commitment (burning the steering wheel) If one driver throws their steering wheel out the window, they’ve removed their ability to swerve. Now the other driver faces a binary choice: Swerve → survive Don’t swerve → both die Result: The committed player “wins” almost every time. 2. Reputation If one driver is known historically to never swerve, the other will yield. This is repeated-game logic: Past behavior shapes future expectations Reputation becomes a strategic asset 3. Asymmetric incentives If one player values survival less (or appears irrational), they gain leverage. A rational player must swerve against someone perceived as irrational This is sometimes called the “madman advantage” Equilibrium view (game theory) Chicken has two Nash equilibria: Player A goes straight, Player B swerves Player B goes straight, Player A swerves There is no stable equilibrium where both go straight (crash) or both swerve (unstable—someone is tempted to deviate). Key takeaway (important) The game is not about bravery — it’s about: Credible commitment Signaling Psychological dominance

-

It's a mess. We have a Provincial government that is very ideological. They have an extreme view of what reconciliation means. They are not being honest with British Columbians about what the implications are of their view of reconciliation (and the legislation they have enacted). The Federal government just threw gasoline on the fire (for no apparent reason). Bottom line, the easy fix is the NDP government repeals the parts of the legislation (DRIPA) that is causing all the problems. But they don't want to (it's an ideological thing for them - so who cares what the consequences are). The problem is most British Columbians (voters) are asleep at the wheel. The media has done a poor job of reporting on the issue (ad how important it is). The podcast below discusses what BC Government has done. Go to the 14:20 minute mark to miss all the small talk... The podcast below discusses what the Fed's have done to make matters worse. Go to the 22:45 minute mark to miss all the small talk...

-

Nuclear deterrence works for one simple reason: MAD (mutually assured destruction). It acts as a deterrent by making full-scale nuclear war irrational and unwinnable. If the US/Israeli's wipe out Iran's critical energy/infrastructure guess how Iran will respond? My uneducated guess is they will take out the energy/infrastructure of their neighbours. This would be a major escalation of the war - the US/Israeli's would be pressing the nuclear button (from an energy/infrastructure perspective). If that is how this plays out... the lasting damage to oil/energy markets would be enormous. LNG and refining facilities take years to rebuild. "Choose wisely..." PS: I just thought of a big flaw in my reasoning: the US is located on a different continent, is 'energy independent' and doesn't appear to give a shit about pretty much anyone else... so why would they care what the consequences of their actions are to Gulf countries and the ROW?

-

@Maverick47, I agree. The US just lifted sanctions on the country it is at war with - and one that is killing Americans. This should tell people how desperate and untenable the current situation is getting. My fear is this ‘problem’ (massive energy shortage) is just getting started. In some important respects, it reminds me of Covid. We could see it coming - we had months of warnings, especially in North America. But we chose to ignore it - including financial markets. Of course, a bucket of cold water got poured on our heads in February and March of 2020 - because reality at some point matters. Again, my base case is we find a way to muddle our way through. But IMHO the tail risks are getting larger with each passing week.

-

This war isn’t going to have a Disney ending? Here is what Iran wants to end the war: (Does it sound like the two sides are close to an agreement?) “Demands voiced by Iranian leaders in recent days as conditions for ending the war include massive reparations from the U.S. and its allies and the expulsion of American military forces from the region. They have also called for transforming the Strait of Hormuz—an international waterway where free navigation is guaranteed under international law—into an Iranian toll booth controlling one-third of the world’s shipborne crude oil. “Iran is planning to enshrine a “new status” for the Strait of Hormuz to require every passing ship to pay fees to Tehran for the privilege, Expediency Council member Mohammad Mokhber, an adviser to the supreme leader on economic affairs, told the country’s Mehr news agency. “Iran will turn its position from a sanctioned country to an enhanced power in the region and the world,” he said. “We will sanction those domination-seeking arrogant powers.” https://www.wsj.com/world/middle-east/iran-war-negotiations-demands-85555522?mod=WSJ_home_mediumtopper_pos_1

-

I have no idea how the war in Iran plays out. I am trying to be open minded. Here is another perspective. It doesn’t suggest the two sides (US/Israel and Iran) are close to resolving their dispute… ————— Iran Believes It’s Winning—and Wants a Steep Price to End the War Tehran sees an opportunity to control the Mideast’s energy as it bets on outlasting Trump’s will—a risky gamble DUBAI—Three weeks into the war, the Iranian regime is signaling that it believes it is winning and has the power to impose a settlement on Washington that entrenches Tehran’s dominance of Middle East energy resources for decades to come. This attitude may prove to be a dangerous misreading of President Trump’sdetermination, or of Israel’s capacity to inflict strategic blows on the Islamic Republic’s surviving leadership and military capabilities. Trump and Israeli Prime Minister Benjamin Netanyahu have given mixed signals on how long the war would go on, as they try to talk markets down and keep Tehran guessing. Netanyahu said Thursday that the war would end “a lot faster than people think.” Trump said this week the U.S. would wrap up the conflict in the “near future” even as the Pentagon dispatched thousands of additional Marines to the Middle East. The problem is, Iran also has a say in when the guns fall silent—and, for now, it seems to think time works to its benefit. Despite optimistic U.S. and Israeli pronouncements about destroying launchers and missile stocks, Iran has retained the ability to fire dozens of ballistic missiles, and many more drones, every day across the Middle East. Instead of declining, the rate of fire actually picked up in recent days compared with 10 days ago. Iranian strikes inflicted catastrophic damage this week on key energy installations in Qatar, Saudi Arabia, Kuwait, Bahrain and the United Arab Emirates—while Iran’s own oil exports kept booming. Shipping through the Strait of Hormuz, the Persian Gulf’s chokepoint, remains only possible with Iranian permission. Surging oil and gas prices, meanwhile, are exacting growing pain on economies worldwide—and putting pressure on Trump to end the war that he began in expectation of swift victory on Feb. 28. https://www.wsj.com/world/middle-east/iran-war-negotiations-demands-85555522?mod=WSJ_home_mediumtopper_pos_1

-

@John Hjorth, your post brings up an important point. The world uses about 100 million barrels of oil per day. About 20 million of the total are shipped through the Straight of Hormuz. Well it used to be - it hasn’t for three weeks now. Yes, some is being re-routed via pipeline. And there is are global SPR releases. Sanction has been removed from Russian and Iranian oil (if you don’t think we are in deep shit think about this - the US just removed sanctions from the countries ‘we’ are at war with). This is providing some ST relief. But there is, of course, much more to the story. We don’t consume oil. We consume the refined products - jet fuel, propane, gas etc. The supply chain for refined products is getting completely messed up. The impact of what is happening in the Persian Gulf is just starting. Of course, it will impact those closest first (reliant on oil/refined products/fertilizer). But like a tidal wave, it will in time wash over the rest of the world. What is happening right now is Americans/Canadians (those not reliant on oil/refined products/fertilizer from the gulf) are like tourists standing on the shore watching in amazement as the water gets sucked out into the ocean. Not realizing that a tsunami is coming - and they should be heading for higher ground. My point is if this war continues for another month or two in its current form it will affect everyone in the world in a very adverse way. There is a reason no previous US president attacked Iran (took out their supreme leader/leadership). And it wasn’t because they wen’t able to drop a bomb on the supreme leader. Or because they were chickens. It was because of the risk the Straight of Hormuz would get closed for an extended period - and if that happened the impact on the global economy would be severe. Well, it has happened. And the impact has been severe. If it stays closed the effect will be catastrophic. But like the tourist standing on the beach watching the water go out and wondering why - we just don’t get it yet.

-

Two thoughts: Yes, the truth hurts (for some anyways). And, yes, it is what it is… NY Times opinion piece: Trump Is Hiding the Truth About the War in Iran https://www.nytimes.com/2026/03/21/opinion/iran-war-trump-lying.html From his first announcement of the attack on Iran on Feb. 28, President Trump has issued a stream of falsehoods about the war. He has said Iran wants to engage in negotiations, though its government shows no sign of it. He has claimed that the United States “destroyed 100% of Iran’s Military capability” when Tehran continues to inflict damage throughout the region. He has said the war is almost complete even as he calls in reinforcements from around the globe. Lying is standard behavior for Mr. Trump, of course. His political career began with a lie about Barack Obama’s birthplace, and he has lied about his business, his wealth, his inauguration crowd size, his defeat in the 2020 election and so much more. A CNN tally of Mr. Trump’s falsehoods during one part of his first term found that he averaged eight false claims per day. Many people are so accustomed to his lies that they hardly notice them anymore. Yet lying about war is uniquely corrosive. When a president signals that the truth does not matter in wartime, he encourages his cabinet and his generals to mislead the country and one another about how the war is going. He creates a culture in which deadly mistakes and even war crimes can become more common. He makes it harder to win by hiding the realities of conflict and by making allies wary of joining the fight. Ultimately, he undermines American values and interests… Summary: Starting a war is the most serious action that a political leader can take. It ends lives and can change history. The decisions that guide war must be based in reality, and presidents owe American service members and their families the truth about why they are being asked to fight. Whatever short-term gain Mr. Trump thinks he is getting by lying about the war in Iran is far exceeded by the cost, for him, the country and the world.

-

Niall Ferguson has some interesting things to say at the end of a recent podcast. He questions if the US paid enough attention to the global geopolitical situation with the war in Iran. He says the US is giving the Chinese leader a path to take Taiwan without firing a shot. He says we are in Cold War 2. Interesting perspective. From a geopolitical perspective, the US needs the war with Iran to end quickly… they grow weaker by the week. Russia and China? They are growing stronger. What is priced in to financial markets? That is where the story gets even more interesting. For the China angle and summary, go to the 49:30 minute mark.