Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

Do it! I find writing helps organize my thoughts. And improves my understanding. (If I can’t write it so it is understandable I probably don’t understand it…) And the discussion on the board then takes it even further.

-

@Buffett_Groupie, good point. Earlier in January I did updates for all the public equity holdings (using Dec 31, 2025 stock prices). When Fairfax releases their annual report I plan on doing the same for the private holdings (like Poseidon/Atlas/Seaspan). When I post i tend to over-emphasize the other things I have been working on at the time (and other important things tend to get under-emphasized). Needless to say, this is the first ‘version’ of this post - so it is a little clunky and missing things. This is where comments/input/critique from other board members becomes quite valuable/helpful - so please keep it coming.

-

I am bringing this post forward as it is the sister post to the one above.

-

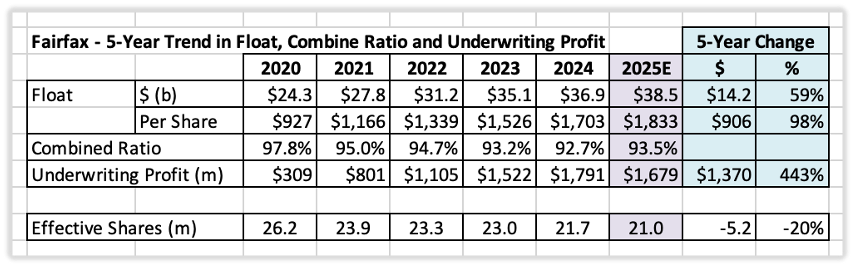

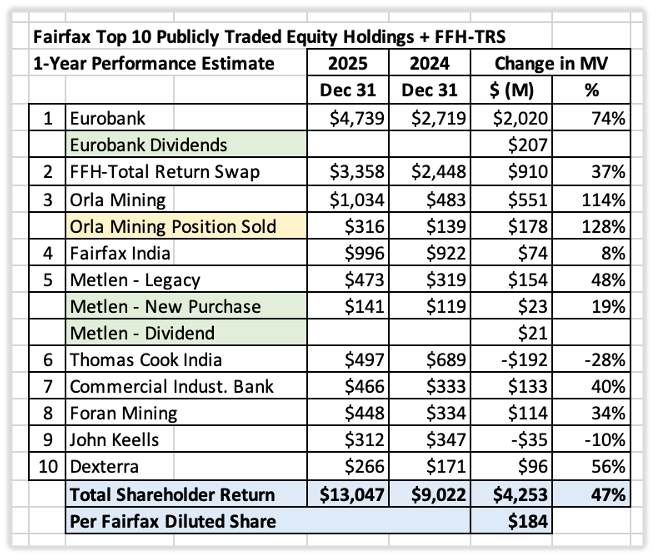

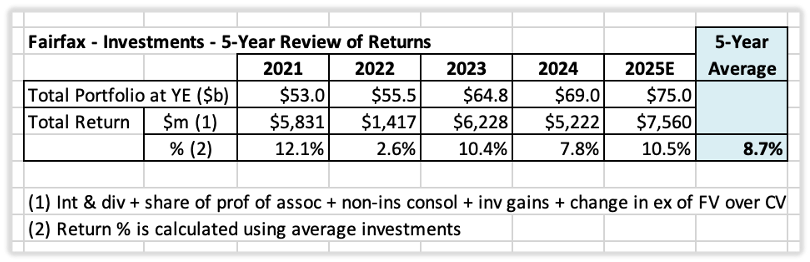

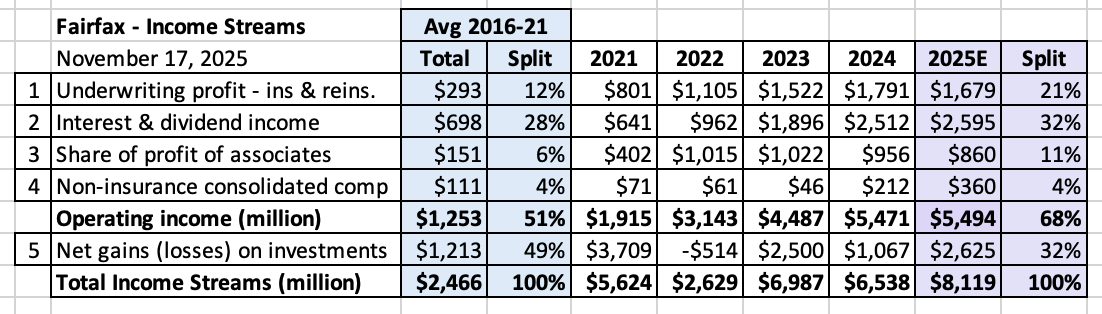

Fairfax Financial’s Business Model A Long-Term Capital Compounding Machine Built on Insurance Float, Decentralized Operations, and Disciplined Capital Allocation Why Focus on the Business Model? My recent work has focussed on Fairfax’s business model for a simple reason: most investors—and many analysts—do not understand Fairfax particularly well. I include myself in that group; there is still plenty to learn. The confusion is understandable: Fairfax is underfollowed It is complex and does not fit neatly into standard industry boxes models It has evolved meaningfully over four decades. It has been transformed again over the past 5 years. As a result, the company is frequently misunderstood and underappreciated – and undervalued. Too often, Fairfax is analyzed as if it were a conventional P/C insurance company. It is not. That framing overemphasizes underwriting results and materially underestimates the importance of the investment portfolio and, especially, capital allocation. Using the wrong model does not lead to better understanding, better decisions, or better outcomes. (Keep that in mind the next time you read an analyst report – or hear pundits discuss Fairfax on social media.) So, what is Fairfax? That is the question this post aims to answer. Overview: What Fairfax Actually Is Fairfax is not a conventional P/C insurance company. It is best understood as a capital-compounding system organized around three complementary business engines: Insurance operations that generate large, durable, growing amounts of low-cost (often negative-cost) float A flexible investment portfolio, spanning fixed income and public and private equities A growing collection of wholly owned operating companies across industries and geographies At the center of this system sits Prem Watsa and Fairfax’s senior leadership team, including Hamblin Watsa, acting as central capital allocators. Crucially, Fairfax’s business model is not designed to maximizing near-term reported results. It is designed to compounding capital at above-average rates and to optimize per-share value creation over the long term – very much in the spirit of William Thorndike’s The Outsiders. Management states this objective clearly: “We expect to compound our mark‑to‑market book value per share over the long term by 15% annually by running Fairfax and its subsidiaries for the long term benefit of customers, employees, shareholders and the communities where we operate – at the expense of short term profits if necessary.” Fairfax corporate website This philosophy is not marketing. It is embedded in how Fairfax is structured, capitalized, and run. If this sounds familiar, it should. Fairfax clearly drew inspiration from Berkshire Hathaway’s model of the 1980s and 1990s—while adapting that framework to its own temperament, opportunity set, and history. Conglomerate-Light Structure: The Organizational Advantage Fairfax operates what can best be described as a conglomerate‑light structure—capturing most of the benefits of conglomerates while avoiding many of their traditional drawbacks. Core Characteristics Small head office Highly decentralized operating businesses (attractive to founder-owners and entrepreneurial managers) Centralized capital allocation, with capital flowing to the best available opportunity Benefits Optimize cash generation from operating units (insurance and investments) Efficient capital deployment – capital is not trapped in silos (for example, excess insurance capital in a soft market) Meaningful diversification across businesses, industries and geographies Greater financial strength and resilience A long term orientation that allows capital to be patient and opportunistic Insurance: discipline through soft markets Investments: ability to exploit volatility and pursue higher-return opportunities Avoided Pitfalls Excessive bureaucracy and organizational bloat Difficulty identifying and fixing underperforming units Unchecked empire-building Keeping it small, size does not become an impediment This organizational design is a foundational reason Fairfax’s model works. Engine 1: Insurance Float – The Structural Foundation Insurance is the backbone of Fairfax’s entire business model. How Float Creates the Core Advantage Insurance float represents premiums collected today that will be paid out in the future as claims. When underwriting is disciplined and profitable (combined ratio < 100), float becomes free capital—and in many years, better than free, because Fairfax generates underwriting profits while holding it. Fairfax is able to invest the float and keep the return that it generates. Why Float Is Superior Leverage Insurance float is a form of leverage that is structurally superior to almost any alternative source of capital: Large and growing No fixed maturity (as long as underwriting remains disciplined) No contractual interest cost; often negative cost Extremely stable due to the scale and diversification of the insurance business Non-callable This is low-risk leverage that cannot be replicated by most conglomerates, asset managers, or private equity firms. Fairfax’s Major Insurance Platforms Odyssey Group Allied World Brit Crum & Forster Northbridge Gulf Insurance Group These operations are diversified by geography and line of business, reducing volatility and enhancing the durability of float. Recent Performance Snapshot (Past Five Years) Total float has increased 59% Float per share has increased 98% (driven by aggressive share buybacks) Estimated underwriting profit in 2025: ~$1.7 billion Put simply: The insurance business provides a $38.5B pile of capital (2025E) The pile is growing rapidly per share Fairfax is being paid handsomely to hold it And Fairfax keeps everything it earns on it Yes—underwriting profit matters. But the much more important outcome is the large, durable, and growing float that Fairfax can invest for its own benefit. Which brings us to Engine 2. Engine 2: Investments – Compounding Float The Investment Portfolio (~$77 billion) Fairfax’s investment portfolio represents the combined deployment of: Shareholders’ equity (~$26.2B) Insurance float (~$38.5B) Holding-company debt (~$7.7B, excluding non-insurance companies) This capital is invested with a long-term, largely unconstrained mandate – a critical structural advantage. Fixed income (~$50 billion) Strengths: Predictable income, lower volatility, senior claim on capital, balance sheet stability Weaknesses: Limited upside, inflation erosion, poor long-term real returns Bonds preserve capital and smooth results. Today, interest income has become one of Fairfax’s most important and reliable income streams. Equities (~$27 billion) Fairfax has historically allocated significant capital to public and private equities Strengths: Ownership in growth, inflation protection over time, unlimited upside, superior long-term compounding Weaknesses: High volatility, uncertain short-term outcomes, last claim in distress Stocks create wealth over the long term. Fairfax’s largest public equity holdings were up $4.3B (47%) in 2025 alone. Performance over the past 5 years has been outstanding. The Structural Return Advantage Unlike traditional P/C insurers—who invest almost exclusively in bonds—Fairfax invests meaningfully in equities. The result: Fairfax investment portfolio return: ~8.5% Typical P/C peers: ~5.5% That return gap compounds massively over time. It is one of the most underappreciated advantages in Fairfax’s business model. Engine 3: Non-Insurance Operating Companies – Small Today, But Growing Fast Fairfax owns a growing collection of non-insurance operating businesses: Recipe Unlimited & The Keg Sleep Country Peak Achievements Meadow Foods AGT Foods and Ingredients This engine is small today, and management has no stated ambition to become a full Berkshire-style operating conglomerate. So why treat it as a distinct engine? Because it is growing rapidly. Non-insurance consolidated companies are Fairfax’s fastest-growing income stream, and they are becoming increasingly important to overall earnings power. Strategic Benefits Greater diversification Another stable source of recurring cash flow Optional source of liquidity (assets can be sold) Increased resilience at the group level These businesses complement the more volatile investment portfolio. How Fairfax develops this engine over the next decade will be worth watching closely. The Control System: Capital Allocation Is the Multiplier Capital allocation is the most important responsibility of any management team. It determines long‑term performance, growth in book value, return on equity, and ultimately the multiple assigned by the market. When done well, capital allocation: Delivers strong returns Improves the quality of the business over time At Fairfax, capital allocation does not generate returns on its own. It amplifies the returns produced by the three engines and determines per-share outcomes over long periods. Unconstrained Capital Allocation Fairfax operates with an unusually unconstrained approach to capital allocation. Over 40 years, management has built deep internal capabilities and a broad network of external relationships. Importantly, Fairfax is still a small company (size is not a constraint). As a result, Fairfax can deploy capital across an unusually broad opportunity set, giving it a continuous flow of above average rate of return options. The Opportunity Set Fairfax can operate as: Fixed income investor Public equity investor Private equity investor Venture capital investor Venture debt / structured credit investor Incubator and platform builder Distressed and bankruptcy investor Turnaround investor Real estate investor Infrastructure investor Commodity and resource investor International and emerging markets investor Asset manager / permanent capital sponsor Cannibal / consolidation investor (buybacks, increased ownership) Few companies enjoy this level of flexibility. Best-In-Class Execution Over the past five years, Fairfax has put on a clinic. Below are some examples of the breadth/range of their capabilities: Insurance: net premiums written doubled to ~$26.6B (over six years) Acquisition of Gulf Insurance Group in 2023 Bonds: avoided the historic 2022 bond bear market (protected balance sheet) Equities: upgraded portfolio; delivering outstanding results, led by Eurobank FFH-TRS (2020/2021) provides exposure to 1.76 million shares at $373/share Digit IPO (2024) – insurance start-up in India (initial investment made in 2016) $2.1B PacWest real-estate construction loan purchase (2023), with Kennedy Wilson C$100M investment in Foran Mining (2021), exploration and development (copper) $150M convertible bond investment in gold producer Orla Mining (2024) Well timed asset sales – Pet Insurance, Resolute (2022), Stelco (2024), Orla (2025) Shares outstanding reduced 24.3% over eight years (at ~$734/share) The list only scratches the surface. The Results The outcomes speak for themselves: BVPS CAGR: 17.1% Share price CAGR: 27.2% This is best‑in‑class performance—and it is not close. Importantly, these results are not driven by the insurance cycle. Insurance cycles exist. Financial markets exist. Fairfax’s results are driven by capital allocation. That is the beauty of the model. Bottom Line Fairfax has spent four decades refining its business model. Roughly five years ago, the pieces finally aligned. Management learned how to fully exploit a framework inspired by Berkshire Hathaway—adapted to Fairfax’s own strengths. The model is simple in concept: Acquire capital cheaply Deploy it rationally Avoid permanent loss Let compounding do the heavy lifting With each passing year, the picture becomes clearer: Insurance: performing at a high level; never better positioned Investments: performing at a high level; never better positioned Capital allocation: best-in-class All parts of the company are working together. Earnings are larger, higher quality, and more resilient across cycles. Shareholder returns have been exceptional. The best part? This version of Fairfax is just getting started. The runway is long. It is an exciting time to be a Fairfax shareholder.

-

P/BV(YE) = 1.3 ($1,638/$1,255) looks pretty cheap to me. At the same time you get a couple of other things for free: Hidden value to YE2025 ($3.5B, conservatively calculated). This will show up as future earnings. Increase in equity holdings in Jan (~$1.9B) $250 million gain when Eurobank closes in Q1 (plus $900 million in cash, less the $ for Cypress P/C insurance) A company generating about $4.5 to $5B in earnings. And a management team that is best-in-class at capital allocation (and likely thinks their stock is cheap).

-

@gfp, I think this is spot on.

-

@Hektor, my core position in Fairfax stays the same. I am happy to build a flex position on weakness (and sell on strength). I am happy with a 6 to 8% return with my flex positions. I was able to do it a couple of times in 2025. I have been adding again.

-

@Parsad, I am getting deja vu with Fairfax! We are seeing a widening divergence in fundamentals and the company's stock valuation. The best example was 2007/2008 when they were sitting on billions in CDS gains and the stock price was not responding. It took a while for results to show up in the financials. and when they did... the stock did ok Perhaps a better comparison to today is back in late 2000 when their stock portfolio started ripping higher and the stock barely moved. And then Fairfax reported results and everyone else learned what we already knew - and even then the stock was slow to respond. Today, hidden value is blowing out. And we are getting crickets from analysts (and most investors). Of course, much more is going on at Fairfax. Super interesting. Funny however things don't change.

-

Do fundamentals matter? Fairfax’s largest equity investment, Eurobank, is up $1.2B YTD-2026 (~$50/share pre-tax). “Hidden value” is ~$3.1B, or $135/share pre-tax (adjusting excess of MV over CV of $3.3B for Q4 results and Jan). Fairfax is not a traditional P/C insurance company. Pretending it is means you have to ignore fundamentals/facts. Is that rational? No. But it is much easier. What we are seeing play out over the past week is very normal for Fairfax. Improving fundamentals and a much lower share price. The reason it doesn't bother me is because it will give Fairfax the opportunity to continue to buy back an enormous amount of shares at a cheap price. Let's hope the stock goes even lower - crazy cheap is even better! Most investors and analysts do not understand Fairfax's business model. As a result, the model they are using doesn't work. What is the solution? It's not complicated (in their eyes)... Fairfax needs to change and get with the program. ---------- "If all you have is a hammer, everything looks like a nail." When you only have one way to analyze companies in an industry - even when it is inappropriate.

-

@backtothebeach, yes, I noticed the forestry stocks are ripping…

-

Fairfax’s Business Model My next couple of posts are going to focus on Fairfax’s business model. Why? My thesis is most investors (and analysts) do not understand Fairfax’s business model. (I still have lots to learn.) Part of the reason is complexity – it is not a traditional P/C insurance company (despite some analysts’ best attempts to pretend otherwise). The other is it has changed in important ways over the past 40 years. To get us started, let’s explore how it has changed and where Fairfax is in their journey today. Where is my analysis off base? I look forward to hearing the feedback from other board members. Has Fairfax’s Business Model Changed Over the Years? Yes—dramatically. While Fairfax’s core philosophy has remained consistent for four decades, the expression of that philosophy has evolved meaningfully. The company has repeatedly adapted its insurance operations, investment framework, and capital allocation approach in response to hard-earned lessons, changing market conditions, and a steadily growing capital base. What follows is a clear, phase-by-phase overview of that evolution. Phase 1 (1985–2000): Scale Insurance + Value Investing Insurance: Scale and Learn Aggressive growth through acquisitions Primary objective: grow float and achieve scale Investments: Make Money with Investments Traditional Ben Graham-style value investing Investments were expected to be the primary profit driver Summary: This was Fairfax’s foundation-building phase. The focus was on rapid growth, learning the insurance business, and leveraging float through value investing. Scale came first; refinement would come later. Phase 2 (2001–2010): Digest Insurance + Value Investing Insurance: Digest and Learn Painful Lessons Worked through significant reserving problems Shifted from expansion to stabilization and repair Investments: (Still) Make Money—Spectacularly So Continued value-oriented investment approach Extraordinary success with CDS and equity hedges during the 2008 financial crisis Summary: This period was defined by humility on the insurance side and brilliance on the investment side. Fairfax learned—painfully—that insurance quality mattered far more than previously appreciated. At the same time, the success of CDS and hedges planted the seeds for a later big mistake. Phase 3 (2011–2020): Improve Insurance + Play Extreme Defense Insurance: Steady Quality Improvement + Acquisition-Driven Growth in a Soft Market Andy Barnard appointed to lead insurance operations in 2011 Underwriting profit becomes the central focus Quality improvement began with existing operations In a soft market, growth pursued primarily via acquisitions – with quality as a priority: Allied World, Brit, International, Zenith Global footprint expanded Strategic pivot in India (sale of ICICI Lombard; seeding of startup Digit) Investments: A Lost Decade Heavy use of equity hedges and shorts proved costly Equity investment framework deteriorated: Result was too many “chronically leaking boats” across the portfolio Summary: This period was defined by brilliance on the insurance side and humility on the investment side – the opposite of the prior period. While insurance quality steadily improved, defensive investment positioning overwhelmed results and masked the progress being made inside the insurance operations. Key inflection points: Equity hedge exited 2016 Final short position closed in 2020 Equity investment framework refined around 2018 Phase 4 (2021–Present): The Insurance-Float Compounding Machine This is where the transformation becomes unmistakable. Insurance: A High-Quality Business, Rapid Growth in a Hard Market Continued underwriting discipline under Andy Barnard and Brian Young Shift from acquisition-driven growth to organic growth, exploiting a hard market Insurance earnings are now larger, more consistent, and higher quality than ever Investments: A High Quality Business Delivering Exceptional Results Clear shift to high-quality equities: strong management teams, solid balance sheets, and sustained profitability Chronic underperformers addressed decisively: sold, merged, taken private, or wound down Equity holdings performing exceptionally well Eurobank stands out as a flagship success Capital Allocation: Best-in-Class Execution Fixed income: avoided the historic 2022 bond bear market (by being very short duration) Asset sales: pet insurance, Resolute Forest Products, Stelco, Orla Fairfax total return swap: opportunistic and unconventional Share buybacks: ~24% reduction in shares outstanding over eight years, executed at very low prices Summary: This period has been defined by brilliance on both the insurance and investing sides of the business. Capital allocation has been exceptional. All parts of the business model are working together (complementary/synergistically). As a result, earnings have been transformed – much larger, higher quality and more resilient across cycles. So—Is Fairfax’s Business Model Different Today? At its core: no. In practice: very much so. The foundational model remains: Insurance float Decentralized operating companies Centralized capital allocation But its modern expression reflects decades of learning. The Bigger Lesson – Resilience and Strength Fairfax made meaningful missteps over the years: Early on, with insurance quality and reserving Later, with equity hedges and short positions Yet despite those mistakes, Fairfax compounded its share price at approximately 19% annually over 40 years (US$, dividends reinvested). That is an exceptional record—and a powerful testament to the underlying strength of the business model. Today, for the first time in the company’s history: Insurance and investments are both high-quality businesses Capital allocation is operating at a best-in-class level This is a version of Fairfax we have never seen before—and it is the best version we have ever seen. Fairfax has become a true compounding machine.

-

A question for board members... How do you think about the significant (and growing) amount of "hidden value" that is residing in Fairfax's equity portfolio/balance sheet. Is there a "right way" to think about it? (academic and/or practical) For people on the board who have owned Berkshire Hathaway long term, my guess is this has been something you have had to grapple with. How did you do it? For Fairfax, some of the "hidden value" is pretty easy to calculate (excess of FV over CV for the publicly traded holdings like Eurobank). Some of it is less precise (like BIAL). I find it a fascinating topic. It is a fact - it is not theoretical. It is a big number: My guess is ~$4.5 billion = $155/diluted share, after tax It is growing by ~+$1 billion per year As we learned the past 2 days, some analysts ignore it completely in their analysis of the company. My guess is "hidden value" at Fairfax is going to continue to increase in size in the coming years. The equity portfolio is growing rapidly. A large and growing part of it is private holdings (with limited disclosures). As a result, how investors think about "hidden value" will be an increasingly important part of their analysis. Thanks in advance!

-

+1. This is very normal for Fairfax. As Graham (and Buffett) taught, price is to be exploited. Not to inform.

-

This type of analysis is totally to be expected. My guess is will we get more of the same from other analysts. It fits their narrative on Fairfax: low quality P/C insurance business, low quality investments, low quality capital allocation = ROE of 11 moving forward. Analysts struggle with Fairfax’s business model. And now with the onset of the soft market they have their excuse to throw in the towel (give up trying). I think Fairfax is going to able to continue to be very aggressive with share buybacks moving forward. That was why I did my long-form post on share buybacks today - to point out how a persistently low share price can be a good thing for a company like Fairfax (and for long term shareholders).

-

@anshulp, thanks for sharing. So Exco’s capex budget is going from $185 million in 2025 to $430 million in 2026. Looks like production is going much higher. And they hedge. Looks like a pretty good set-up for much higher earnings in 2026. This is also a perennial acquisition candidate. Another likely tailwind in Fairfax’s equity portfolio. My current estimate for Exco's contribution to share of profit of associates for 2026 is $75 million. That probably should be doubled to $150.

-

I agree the Toys R Us retail business was terrible. The fact they got rid of it is a positive in my book. But not knowing what the value of the real estate is… I give this transaction a grade of incomplete.

-

@LC, great question. I think it highlights what lots of investors are getting wrong when they look at Fairfax today. My view is the Fairfax that existed in late 2020/early 2021 is fundamentally different from the company that exists today. This is a theoretical thing for me. Because obviously it is the same company. Part of this is because some important things have changed. Interest rates are much higher - interest income is much higher - meaning float is much more valuable today than it was in 2021. This is just one example. Part of this is because we understand the company better today. For example, back in 2021 some of us suspected they were fixing their investment framework. Well, today we know they were (and have largely completed dealing with the long list of problem children). That means the company is worth much more (look at how well the equity portfolio is performing). Another example: Back in 2021, much of us thought Fairfax had an OK P/C insurance business - probably average. Today, I think we can say with confidence they have a better than average business. and it might even be better than this. This means the company is worth much more. Now stack all these things together - and you end up with a company that is worth much, much more (from a valuation perspective) than it was in 2021. Their P/C insurance business is much better. Their collection of equity holdings are much better. Their investment framework is much better. It is not the same company - it looks to me like Fairfax has cracked the code of how to best exploit the P/C insurance model (using Buffett's model - but adapted to fit how they are wired). Changes in the Income Streams Provide a Roadmap for Investors Since 2021, Fairfax keeps morphing in important ways. The best way to understand both what has been happening and the magnitude is to follow the income streams. You nailed it with your question. Underwriting: slow and steady improvement every year. growing NPW and lower CR. Share of profit: spiked in 2022. But the work was done years before. Interest income: spiked higher in 2023. Positioned perfectly. Growing nicely. Non-insurance consolidated companies: in the process of breaking out. Work was done years before. The other emerging income stream is "hidden value". I put it conservatively at $4.5 billion today. This is about how much it has grown over the past 5 years (meaning it was zero back then). This is not captured in my table below. But it is real value that has been created and will be dropping in to earnings in the coming years. This means investment gains are going to be much larger moving forward. But investment gains was already going to be bigger - and that is because the equities in Fairfax's portfolio are higher quality than they have ever been. So they are going to deliver above average returns moving forward. As "hidden value" gets realized, investment gains will be even higher - this will be additive. And on top of this, Fairfax will be generating about $4.5 billion (and growing) in earnings every year. This will get re-invested. Driving each of the income streams even higher. We just don't know exactly what Fairfax will do - so it is hard to know which income streams will increase the most (it will likely be spread out). Capital allocation The primary driver of earnings growth in the coming years will be capital allocation. And today, Fairfax is best-in-class. And it's not close. In my Excel spreadsheet I have a table that tracks all the capital allocation decisions for each year (it goes back to 2010). It is called 'Moves'. I built this model back in 2021 because I wanted to understand how good Fairfax was at capital allocation. (The file is attached below.) To try and predict what they are going to do is impossible. Go back a year. Look at what Fairfax did in 2025. Was it predictable? No. Was it good? Yes. Very. Do the same for 2024. Look at what they did. Was it predictable? No. Was it good? Yes. Very. Do the same for 2023.... and 2022. The mistake investors make is they want to know in advance what is going to happen. Of course that is not possible. But the insight is... you don't need to know. If you can wrap your head around that you will be on the right track. PS: Looking at income streams can be very helpful. But it is not enough. Why? It ignores share buybacks. And that has been a critically important part of the Fairfax story. And my guess is it will continue to be. Is Fairfax a better buy today than in 2021? It was cheaper in 2021. A better buy? The answer is not as obvious as many might think. Fairfax Jan 2026.xlsx

-

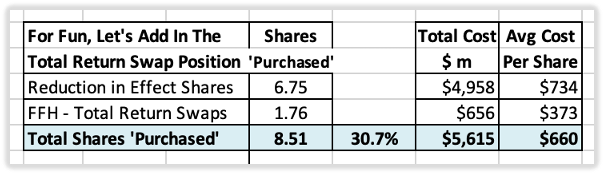

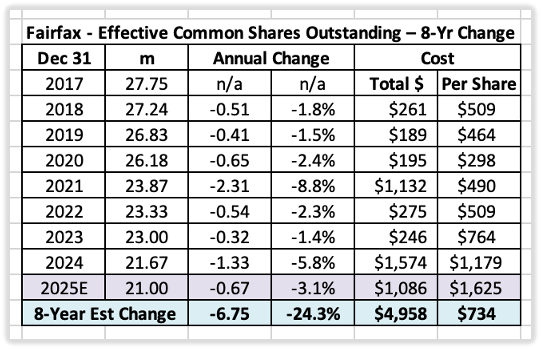

Capital Allocation & Share Buybacks – Warren Buffett (theory) – Fairfax (real world example) The Big Picture Three factors drive stock returns over the long term: Earnings Valuation multiple Shares outstanding The first two get most of the attention. The third – shares outstanding – is often ignored by investors, yet it can be a powerful driver of per-share value creation. Capital Allocation Matters Capital allocation is the most important function of a management team and stock buybacks are one of many options that are available to them. When executed properly — at attractive prices and over many years — buybacks can be extraordinarily beneficial for shareholders. Of all the capital allocation options available to management, share buybacks carry the highest degree of certainty. High certainty = low risk. “When companies with outstanding businesses and comfortable financial positions find their shares selling far below intrinsic value in the marketplace, no alternative action can benefit shareholders as surely as repurchases.” Warren Buffett – Berkshire Hathaway 1984AR Why Buybacks Are So Powerful It is counterintuitive, but for long-term shareholders a low stock price can be a gift - if the company is aggressively repurchasing shares. Especially if this persists for years. Buffett highlights two key benefits: 1. Higher Per-Share Intrinsic Value This is “basic arithmetic.” Repurchasing undervalued shares increases ownership for remaining shareholders and immediately boosts intrinsic value per share. 2. A Higher Valuation Multiple This benefit is more subtle – and often overlooked. When management repurchases shares well below intrinsic value, it sends a powerful signal. It demonstrates rational, shareholder-aligned capital allocation rather than empire building. Buffett explains: “The companies in which we have our largest investments have all engaged in significant stock repurchases at times when wide discrepancies existed between price and value. As shareholders, we find this encouraging and rewarding for two important reasons - one that is obvious, and one that is subtle and not always understood. The obvious point involves basic arithmetic: major repurchases at prices well below per-share intrinsic business value immediately increase, in a highly significant way, that value. When companies purchase their own stock, they often find it easy to get $2 of present value for $1. Corporate acquisition programs almost never do as well and, in a discouragingly large number of cases, fail to get anything close to $1 of value for each $1 expended. “The other benefit of repurchases is less subject to precise measurement but can be fully as important over time. By making repurchases when a company’s market value is well below its business value, management clearly demonstrates that it is given to actions that enhance the wealth of shareholders, rather than to actions that expand management’s domain but that do nothing for (or even harm) shareholders. Seeing this, shareholders and potential shareholders increase their estimates of future returns from the business. “This upward revision, in turn, produces market prices more in line with intrinsic business value. These prices are entirely rational. Investors should pay more for a business that is lodged in the hands of a manager with demonstrated pro-shareholder leanings than for one in the hands of a self-interested manager marching to a different drummer...” Warren Buffett – Berkshire Hathaway 1984AR Fairfax’s Buyback Philosophy Prem Watsa laid out Fairfax’s long-term strategy in the 2018 Annual Report: “I mentioned to you last year that we are focused on buying back our shares over the next ten years as and when we get the opportunity to do so at attractive prices. Henry Singleton from Teledyne was our hero as he reduced shares outstanding from approximately 88 million to 12 million over about 15 years.” Prem Watsa – Fairfax 2018AR Fairfax approaches buybacks exactly like a value investor: Buy shares when they are cheap “Back up the truck” when they are really cheap What Has Fairfax Actually Done? 2015–2017: Share Issuance Fairfax issued shares to fund aggressive international P/C insurance expansion. Effective shares outstanding peaked in 2017 at 27.75 million Fairfax issued 7.2 million shares from 2015–2017 Average issuance price: ~$462 per share 2017–2025: Aggressive Buybacks Once the expansion phase ended, Fairfax shifted to large-scale repurchases. Effective shares outstanding (Dec 31, 2025E): 21.0 million Shares retired since 2017: 6.75 million shares Total reduction: 24.3% Average repurchase price: ~$734 per share Over the past eight years, Fairfax spent $5.0 billion buying back stock – its single largest investment. The result: a massive reduction in share count. Did Fairfax Get Good Value? Absolutely. Book value per share: $1,255 (Dec 31, 2025E) Share price: $1,734 (January 20, 2026) Intrinsic value: well above book value Fairfax reduced shares outstanding by 24.3% at an average price of $734 per share. Repurchases were done at a significant discount to book value. And Fairfax “backed up the truck” – they took out a significant number of shares. Even more impressive: Fairfax aggressively grew its core P/C insurance business at the same time Net premiums written (NPW) 2017: $10B ($353 per share) 2025E: $26.6B ($1,265 per share) Total growth: 166% Per-share growth: 252% Fairfax walked and chewed gum at the same time. Thanks to buybacks, per-share growth massively outpaced total growth. This is elite capital allocation. Is Fairfax Done Buying Back Shares? Current valuation: Share price: $1,734 (Jan 20, 2026) Book value: $1,255 (Dec 31, 2025 estimate) P/BV: ~1.38 ROE: averaging high teens in recent years Fairfax is still cheap. And book value excludes a large amount of hidden value that has accumulated over the past five years. My conservative estimate: Hidden value: ~$4.5B Per share (after tax): ~$150 The hidden value is residing in Eurobank, Fairfax India, Poseidon and other holdings. I have discussed this at length in pervious posts so I won’t go into details again here. I also expect Fairfax to remain cheap — likely for years. The company is still misunderstood and unloved. Most investors and analysts do not understand their business model or grasp the quality of the business or management. That is wonderful for long-term shareholders. It allows Fairfax to continue reducing shares outstanding at very attractive prices. Bottom Line Over the past eight years, Fairfax has executed a textbook, Buffett-style buyback program: Repurchased aggressively when deeply undervalued Created enormous per-share value Maintained strong growth in its core business This is exactly what exceptional capital allocation looks like. Fairfax is putting on a clinic. It is also an important sign to investors that Fairfax is being run in a very shareholder friendly way. One More Thing: Fairfax’s Total Return Swaps Fairfax also holds total return swaps (TRS) on its own stock. Fairfax put on the position in late 2020/early 2021 at an average cost of $373 per share. The initial position was 1.96 million shares, and currently sits at 1.76 million. (Position was reduced by ~200,000 in Q4, 2024 – Fairfax purchased and retired shares from the counterparty.) Over the past 5 years, the TRS-FFH has increased in value by about $2.9 billion (before carrying costs). This has become one of Fairfax’s best investments ever. Some investors view this as a form of synthetic buyback. If we include TRS: Effective shares retired (8 years): 30.7% Average price: ~$660 per share Yes — that is absurdly good. Henry Singleton would approve.

-

Fairfax bought Toys “R” Us to be in the toy business? My understanding is it was bought for the real estate. When you say “ultimately selling it at a 60% loss” does this include the real estate?

-

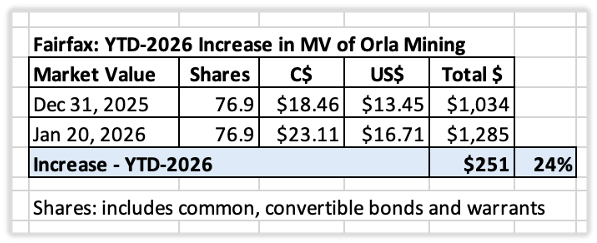

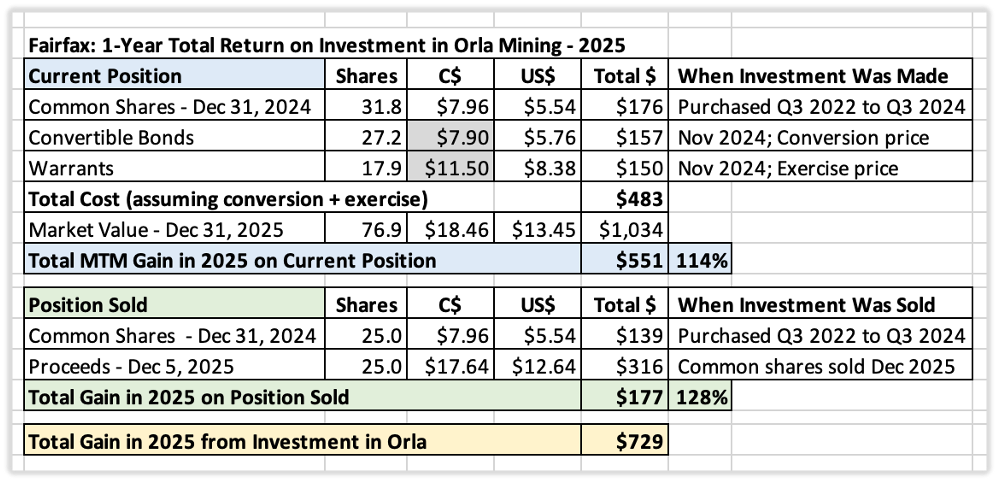

Orla Mining - OLA.TO – Prospecting for Discovering Gold January 20, 2026 Recent Developments Orla released a production update for Q4-2025. It was better than expected. Orla Mining Achieves Record Quarterly Production Propelling Company Above 300,000 Ounces for 2025, setting up a Catalyst-Rich 2026 https://www.newswire.ca/news-releases/orla-mining-achieves-record-quarterly-production-propelling-company-above-300-000-ounces-for-2025-setting-up-a-catalyst-rich-2026-821150642.html Shares are spiking higher. 20 days into 2026, Fairfax’s investment in Orla is up ~$250 million. This is after a $729 million gain in 2025. Yes, Orla has been an outstanding investment. December 31, 2025 Orla Mining Ltd. is a Vancouver-based mining company focused on acquiring, exploring, developing, and operating mineral properties to produce gold, silver, zinc, lead, and copper. Fairfax first invested in Orla between Q3-2022 and Q3-2024, accumulating 56.8 million shares through open-market purchases. In November 2024, Fairfax increased its exposure by investing $150 million in convertible bonds and warrants, bringing its total exposure to 101.9 million shares. On December 5, 2025, Fairfax reduced its position by approximately 25%, selling 25 million shares. Fairfax’s Investment Snapshot As of December 31, 2025: Market value of Fairfax’s stake: ~$1.0 billion Portfolio weight: ~3.8% of Fairfax’s ~$26.7 billion equity portfolio Portfolio rank: Orla is Fairfax’s 4th largest equity holding. Company Website: https://orlamining.com/investors/ Company Presentation: December 2025 https://wp-orlamining-2024.s3.ca-central-1.amazonaws.com/media/2025/12/Orla-Corporate-Presentation-12-2025.pdf Performance in 2025 With gold prices surging, 2025 performance was exceptional: Total return: +$729 million Continuing position: +$551 million Shares sold: +$177 million (128% return) Orla has quickly become one of Fairfax’s best investments in recent years. Return on Shares Sold in 2025 On December 5, 2025, Fairfax announced the sale of 25 million shares for $316 million (roughly 25% of its total position, including convertibles and warrants). Performance on shares sold: Cost: ~$98 million ($3.94 per share) Sale price: $316 million ($12.64 per share) Profit: $218 million (~$8.71 per share) Return: 221% Fairfax invested a total of $374 million in Orla ($224 million equity + $150 million convertibles). This partial sale returned a significant amount of its original investment. A Lesson in Capital Allocation In 2022, Fairfax sold Resolute Forest Products for a premium price at the top of the lumber cycle. Late in 2024, they sold Stelco to Cleveland Cliffs at a premium price, capitalizing on the acquisition mania in steel producers. And now they are selling 25% or Orla for another big gain. This is just the latest example of Fairfax’s management team executing at a very high level. Over the past five years, they have been putting on a master class in capital allocation. Why Is Orla Surging? Orla’s share price has been on fire over the past 18 months: June 30, 2024: $3.90 December 31, 2025: $13.45 Gain: +245% What is going on? Gold is widely viewed as a hedge against: Uncertainty Inflation Today, we have both. It should not surprise anyone that gold prices have been ripping higher — and that Orla’s share price has followed. Where Do We Go from Here? President Trump is still early in his second term. My guess is elevated uncertainty will persist for at least the next three years. Tariffs are central to Trump’s economic strategy. Tariffs are inflationary. My expectation is inflation remains elevated (around 3%?) for several more years. Bottom line: The current bull market in gold could continue for a few more years. If so, Fairfax’s investment in Orla may just be getting started. The Investment Thesis With its investment in Orla, Fairfax is effectively betting on: Gold prices staying higher for longer. Above-average management at Orla, capable of transforming the company from a two-asset producer into a multi-asset, intermediate-sized gold producer. A strong ownership group — Fairfax, Fidelity, Pierre Lassonde — which enables long-term thinking and rational, shareholder-friendly capital allocation. Fairfax planted another seed in its equity portfolio. In a short time, it has already turned into another home run. It will be fascinating to see whether gold’s improbable march higher continues. Partnering With Proven Winners Fairfax is not blindly speculating in commodities. They are consistently partnering with world-class operators and investors. Jurisdiction Matters The majority of Fairfax’s resource investments are located in North America — a far lower-risk jurisdiction than many global mining regions. This is no accident. All of Orla’s producing assets are in North America. Experience Matters Yes, Orla looks like a terrific investment for Fairfax. But there is a bigger lesson here. Fairfax has a deeply seasoned investment team — both at corporate and at Hamblin Watsa. Some team members were active investors in the 1970s and 1980s, the last sustained inflationary period. That experience likely contributed to Fairfax initiating this position back in 2022. In an environment of high uncertainty and persistent inflation, experience matters more than ever. Fairfax appears extremely well positioned not just to survive — but to thrive. Orla is a real-world example of that advantage. Comments about Orla Mining from Prem from Fairfax’s 2024AR. Orla Mining, run by Jason Simpson and his exceptional team, had a transformative 2024. In November, Orla announced the acquisition of the Musselwhite gold mine in Ontario from Newmont. Fairfax participated via a $150 million investment in convertible bonds (4.5% coupon, Cdn$7.90 conversion price and 0.66 of a warrant with a Cdn$11.50 per share exercise price). Musselwhite is a low-cost, long-life asset in one of the best mining jurisdictions in the world. The addition of Musselwhite will more than double Orla’s annual gold production to approximately 300,000 ounces a year. Orla’s Camino Rojo open pit mine in Mexico continues to perform extremely well, producing approximately 137,000 ounces of gold in 2024. Exploration activity at Camino is indicating the viability of an underground mine at the site with attractive economics. Lastly, progress continues to be made in permitting their South Railroad mine in Nevada.South Railroad is likely to be a low-cost mine with high free-cash flow. Orla generates attractive levels of free cash flow and has ample liquidity to fund its development and exploration activity. Orla is carried at its listed price of $5.47 per share (Cdn$7.87) or $311 million. Prem Watsa – Fairfax 2024AR

-

@Crip1, well said. Here are a couple of the learnings for me: Fairfax is very good at managing their fixed income portfolio. They have a very good long term track record. (It has been a big part of being able to compound at 19% for 40 years.) "In Brian (and team) we trust." Volatility is their friend. The more the better. It is counterintuitive. Volatility hits and investors want to run for the hills. It should be the opposite (when it comes to Fairfax).

-

A few months ago people were worried about treasury yields going way down and interest income imploding…. Now the risk is treasury yields going way higher and interest income spiking? Which is it?

-

I wonder if Fairfax has reduced their stake in CIB in 2025. We will find out when we get the 2025 annual report in March (and an updated share count for the big equity holdings). At year end 2024, Fairfax owned 215.5 million shares, or ~7%. In CIB's most recent corporate presentation (Q3-2025) they have Fairfax's ownership stake at 6.26%. Total share count at CIB is 3.07 billion, which puts Fairfax ownership at 192 million shares. So we will see. https://www.cibeg.com/-/media/project/downloads/investor-relations/ir-library/ir-and-esg-presentations/2025/3q25-ir-ppt.pdf

-

@Duke In Shadows, my view is Recipe was a terrible investment for minority shareholders. I think Fairfax took it out at a low price in 2022. The key, as @SafetyinNumbers suggests is what is the capital Fairfax put in (and it's not anywhere near $1.2B). And what is the return the investment is generating today. My guess is the return is solid. Recipe has been an active investment for Fairfax over the past year: Takeout of minority shareholder (16%) - funded by Recipe, I think Takeout of Keg Royalties Income Fund - getting control of Keg banner Purchase of rights to Olive Garden Canada (and 8 locations) Spin-off of Keg out of Recipe I would love to see Recipe do more spin-offs. Quick service. Full-service. Etc. Get entrepreneurs running smaller companies. Hopefully, what they appear to have done with the Keg is foreshadowing what they have planned. I think full service restaurants are having a very good year in Canada (Canadians not travelling to the US - eating out more). We will find out when Fairfax reports year-end results. ---------- PS: When we lived in Langley, BC, Olive Garden was one our favourite restaurants to have a family meal at. I think the banner might do ok. I am watching to see if the long term plan is to build/own or franchise. In the beginning build/own makes sense (to work out the kinks). Longer term, I am hoping they franchise.

-

Eurobank is up big to start 2026, ~+829 million. Fairfax is currently trading at 1.4 x YE BV. Cheap. Investors are also getting significant "hidden value" of about $4 to $5 billion for free (Eurobank is about $3 billion). The hidden value can be looked at in two ways: Apply it to current book value. This would add about $155, which would put YE 2025 BV at ~$1,400. This means Fairfax is trading at 'economc' P/BV = 1.25 Apply it to future earnings (via investment gains). This results in a higher ROE. Instead of mid-teens (base case, excluding 'hidden value') we now get high teens. Higher future ROE means Fairfax is worth a much higher multiple (than current 1.4x). The net result is "hidden value" can be and should be included in a valuation of Fairfax. The fact that most investors (and analysts) instead chose to ignore it is fascinating.