Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

What Is Wrong with Fairfax’s Stock Price? The Lesson of Mr. Market After five years of near uninterrupted gains, Fairfax’s share price has hit some turbulence: Down 7.5% on Friday, May 2, 2026 Down 16% year-to-date Flat over the past year What is an investor to do? Panic? And sell? Or step back and think clearly? Start with the Right Framework This is not primarily an analytical problem. It is a behavioral one. The behavioral dimension of investing—how psychology, emotion, and bias influence decisions—often dominates real-world outcomes. Price volatility tests temperament, not intelligence. Few have explained this better than Warren Buffett, building on the teachings of Benjamin Graham. Two Questions That Actually Matter Before reacting to price, an investor should ask: 1. Do you understand the business? Fundamentals Capital allocation Management quality Long-term prospects Shareholder alignment On these measures, Fairfax has been exceptional. The past five years have been outstanding, and the next five look equally compelling. The company resembles a high-performing athlete entering its prime. 2. Are you an independent thinker? Do you rely on price to validate your view? Or do you anchor on intrinsic value? Because price and value are not the same thing. Mr. Market: The Key Insight Graham’s Mr. Market offers a simple but powerful lens: The market is there to serve you—not to guide you. Daily price quotes reflect emotion, not value. Sometimes they are useful. Often, they are not. The implication is critical: Price weakness does not necessarily mean business weakness. Reconciling that apparent contradiction is the essence of successful investing. It requires having the right temperament. What Fairfax Is Actually Doing Management is behaving consistently with this framework. They understand the business. They understand its value. And they are acting accordingly. 2025: repurchased and cancelled >1 million shares at ~$1,615 Q1 2026: repurchased 374,883 shares at ~$1,684 May 2, 2026 close: $1,598/share At the same time: 2025 was the best year in company history Intrinsic value has grown meaningfully over the past 15 months The signal is clear: management is treating price weakness as opportunity. If current conditions persist, continued aggressive buybacks in 2026 would represent a high-certainty, high-return use of capital. Putting It Together You are left with two facts: The business is performing at a high level The stock price is underperforming Most investors struggle here. They assume the second must reflect the first. It doesn’t have to. The Real Lesson Mr. Market is not teaching you about markets. He is teaching you about yourself. Can you separate price from value? Can you remain rational when others are not? Can you act when opportunities appear—and do nothing when they don’t? Because in investing: Behavior—not analysis—is often the decisive edge. Bottom Line Fairfax’s recent share price weakness is not, by itself, a signal. It is an invitation. Whether it becomes an opportunity—or a mistake—depends entirely on how you respond. =========== Quote from Warren Buffett – from Berkshire Hathaway’s 1987 Annual Report “Ben Graham, my friend and teacher, long ago described the mental attitude toward market fluctuations that I believe to be most conducive to investment success. He said that you should imagine market quotations as coming from a remarkably accommodating fellow named Mr. Market who is your partner in a private business. Without fail, Mr. Market appears daily and names a price at which he will either buy your interest or sell you his. “Even though the business that the two of you own may have economic characteristics that are stable, Mr. Market’s quotations will be anything but. For, sad to say, the poor fellow has incurable emotional problems. At times he feels euphoric and can see only the favorable factors affecting the business. When in that mood, he names a very high buy-sell price because he fears that you will snap up his interest and rob him of imminent gains. At other times he is depressed and can see nothing but trouble ahead for both the business and the world. On these occasions, he will name a very low price, since he is terrified that you will unload your interest on him. “Mr. Market has another endearing characteristic: He doesn’t mind being ignored. If his quotation is uninteresting to you today, he will be back with a new one tomorrow. Transactions are strictly at your option. Under these conditions, the more manic-depressive his behavior, the better for you. “But, like Cinderella at the ball, you must heed one warning or everything will turn into pumpkins and mice: Mr. Market is there to serve you, not to guide you. It is his pocketbook, not his wisdom, that you will find useful. If he shows up some day in a particularly foolish mood, you are free to either ignore him or to take advantage of him, but it will be disastrous if you fall under his influence. Indeed, if you aren’t certain that you understand and can value your business far better than Mr. Market, you don’t belong in the game. As they say in poker, “If you’ve been in the game 30 minutes and you don’t know who the patsy is, you’re the patsy.” “Ben’s Mr. Market allegory may seem out-of-date in today’s investment world, in which most professionals and academicians talk of efficient markets, dynamic hedging and betas. Their interest in such matters is understandable, since techniques shrouded in mystery clearly have value to the purveyor of investment advice. After all, what witch doctor has ever achieved fame and fortune by simply advising “Take two aspirins”? “The value of market esoterica to the consumer of investment advice is a different story. In my opinion, investment success will not be produced by arcane formulae, computer programs or signals flashed by the price behavior of stocks and markets. Rather an investor will succeed by coupling good business judgment with an ability to insulate his thoughts and behavior from the super-contagious emotions that swirl about the marketplace. In my own efforts to stay insulated, I have found it highly useful to keep Ben’s Mr. Market concept firmly in mind. “Following Ben’s teachings, Charlie and I let our marketable equities tell us by their operating results – not by their daily, or even yearly, price quotations – whether our investments are successful. The market may ignore business success for a while, but eventually will confirm it. As Ben said: “In the short run, the market is a voting machine but in the long run it is a weighing machine.” The speed at which a business’s success is recognized, furthermore, is not that important as long as the company’s intrinsic value is increasing at a satisfactory rate. In fact, delayed recognition can be an advantage: It may give us the chance to buy more of a good thing at a bargain price.” Berkshire Hathaway AR - 1987

-

Fairfax has consistently said the TRS is an investment. If Fairfax continues to hold the TRS, I think we can assume they view the shares as being undervalued. My guess is they also apply a nice margin of safety to their calculation of fair value. Meaning as long as they hold the TRS they view their shares as being very undervalued. This is supported by how aggressive they have been on the share buyback front over the past 5 years (since they put the position on). They were also VERY aggressive in Q1. Most importantly, Fairfax is an insider - they understand what Fairfax is worth. Much better than the rest of us. Yes, there are risks (it is leverage). The question is Fairfax being compensated appropriately? Do you trust management? I do, based on what I have seen from them the past 5 years. With shares trading at $1,600, I like this investment a lot. For those who think Fairfax should take the TRS off what do you think Fairfax is worth? I think that needs to be part of the analysis.

-

From my perspective, the most significant development in the first quarter for Fairfax and its results/valuation was the sale of ~50% of Poseidon and the massive increase in the market value of the asset. An asset that Fairfax was carrying on the books at $2B was revealed to be worth $3.7B. +$1.7B over CV +$1.1B over MV This sale will result in a massive investment gain in Q2. And provides us with a useful update of what the remaining stake is worth (and another big gain will likely be coming in the future). Many of the analysts call this source of earnings 'low quality', which of course is rubbish. (It is 'low quality' because it cannot be accurately forecasted in their models each quarter.) So they largely exclude it from their models, communication, valuation and evaluation of management/results. That, of course, is also nuts. Investment gains is one of Fairfax's most important sources of earnings. Look at their history. Pretending it isn't (or worse, that is shouldn't be) is stupid. Fairfax should be evaluated for what it is - not what an analyst thinks it should be. This is really important because Fairfax is sitting on an enormous amount of "hidden value". And it has been rapidly growing in size over the past 5 years. "Hidden value" is simply a code word for future earnings for Fairfax - most analysts just haven't figured it out yet (a few have). Poseidon is just the latest example. Many more will be coming in future years. Investment gains is quite predictable when viewed through a three year time horizon (rolling average). Tough for analysts. Easy for investors. The value creation from the sale of 50% of Poseidon - all by itself - made Fairfax's Q1 an outstanding quarter. Does it matter that the gain is not showing up until Q2? Really? The Poseidon sale provides a great demonstration of how misunderstood Fairfax continues to be. Especially when it comes to the investment gains bucket. In turn this often causes the stock to be undervalued. And this provides a wonderful opportunity for investors who are able to think for themselves and do basic math. I have followed Fairfax closely for 23 years. This is not something new.

-

The key questions: Has the value of the business increased over the past year? How much? What are the prospects for the business moving forward? How is management doing? One of the wild cards is multiple. I think we are all learning what the range for this will be for Fairfax moving forward (1.3 to 1.6 x BVPS?). Of course it could go both lower and higher when pessimism/optimism are at extremes.

-

FFH. Looks cheap. Anyone follow it?

-

@Crip1, I was lucky with my forecast for Q1. Having said that, my experience with forecasting (at Kraft and Saputo) was if you put enough thought into the key inputs, you normally ended up with a fairly accurate forecast (final number). Each of the inputs will be off - but some will be favourable and some with be unfavourable and the differences will often balance out in the end. If you go through my individual forecasts (the build), there was a lot of variability. Anyways, the exercise really helped me understand what Fairfax actually reported much better (than if I had done nothing). The fact the end number was close was icing on the cake.

-

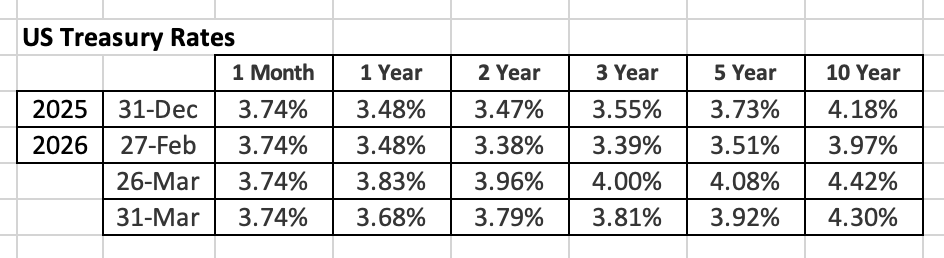

@Hoodlum, yes, Fairfax was active with bonds in the 3 to 5 year bucket. I am happy they have used the increase in interest rates as an opportunity to extend duration. The other important piece is how conservative they are positioned - 76% of the portfolio is government. Fairfax is positioned much more conservatively than most P/C insurance peers. From the press release: "The company's fixed income portfolio has an average term to maturity of 3 years and continues to be conservatively positioned with 76% of the fixed income portfolio invested in U.S. treasury and other government bonds, 13% in high quality corporate bonds, primarily short-dated, and 11% in first mortgage loans." From the Q1 quarterly report: "The increase in the company's holdings of bonds due after 3 years through 5 years was primarily due to net purchases of U.S. treasury bonds of $3,612.3, other government bonds of $824.4 and Canadian government bonds of $635.0." This is a good example of how Fairfax is opportunistic. And sometimes able to earn a little extra with its fixed income portfolio. Being short duration in a rising interest rate environment: Results in a lower investment loss. Allows for duration to be extended, locking in higher interest income for longer.

-

Fairfax delivered another quarter of solid results in Q1 Net earnings were $695.7M, or $31/diluted share. Solid. Insurance Top line growth (NPW) of 4.2% - demonstrate continued discipline with insurance CR of 94.1% - low cat losses and minimal PY reserve development Underwriting profit of $381.6M - getting paid handsomely to hold ~$38.5B float Investments Interest and dividend income of $662M - solid. Share of profit of associates of $371.5M - very good (increase driven by Waterous EFIII) Non-ins consol co operating income of $36.9M (one-time costs of AGT IPO was a drag) Investment gains (losses) were a loss of $385.9M - as expected Fixed income: loss of $363.9M (due to higher interest rates) Mark to market equities: loss of $81.8M (due to weakness in equity markets) Excess of FV over CV: increased to $3.9B, or $173/share pre-tax - driven by Poseidon sale Was $3.1B at Dec 31, 2025; increase in Q1 of $800M, or $36/share pre-tax ($29 after tax) This is not captured in BV. Represents future earnings. Fairfax grew shareholder value in Q1 by $31 (EPS) + $29 (FV over CV) = $60/share Capital allocation/shareholder return Paid annual dividend of $15/share, or $329.1M Bought back and retired 374,883 shares, for $631.3M, or $1,684/share Effective shares outstanding were 20.62M at Mar 31, 2026 (was $20.86M at Dec 31, 2025) BVPS: $1,250 (was $1,260 at Dec 31, 2025) Decline in BVPS was due to dividend, share repurchases (above BV) and currency movements Very strong set-up for Q2: Transactions expected to close in Q2: Poseidon sale: proceeds $1.9B, pre-tax gain of $837M Eurolife sale: proceeds $935M, pre-tax gain of $350M Total pre-tax gain: $1.2B, or ~$53/share Fairfax continues to hit the ball down the middle of the fairway. Not flashy. Wins championships.

-

Fairfax Q1 Earnings Preview (Guess) - Small edit My very rough guess is earnings will come in around $28/share when Fairfax reports Q1 results. Fairfax paid a US$15/share dividend in Q1. As a result, this would put book value at March 31, 2026, at about $1,270/share. Note, I am not doing this exercise to come up with a high conviction specific number (I know it will be wrong) for EPS or BVPS. Rather, I do it to help prepare me for Fairfax’s earnings release. Below is the logic I used to come up with my forecast (the thought process is what matters). What are other board members thinking? Please share your thoughts. Note: My annual estimates for 2026 and 2027 in thechart below were put together in February. I will likely update these estimates mid year. Details Underwriting profit: Net premiums of $6.91B x CR 94% = underwriting profit of $415M Questions: What is impact of war in middle east, especially GIG? Is it a near term risk and medium term opportunity? Interest income Q1-2026 of $640M Run rate in Q4 2025 was $646 Question: Did Fairfax take advantage of the increase in interest rates in March to increase average duration of their fixed income portfolio? Share of profit of associates Q1-2026 $150M ($225M-$75M hit from Sanmar) Tailwinds: Waterous Energy Fund III (Greenfire) was -$60M in Q1 2025. EXCO? Significant capex in 2026. Headwind: Sale of Sanmar by Fairfax India in March (not sure on timing here... Q1 or Q2). Markdown on sale ~$75M? (FV at Dec 31 of $101.6M - proceeds of $27M) The bigger picture: Sanmar is an example of Fairfax India dealing with a chronically underperforming equity holding. Good to see. This is one of the ways Fairfax has been optimizing their equity portfolio in recent years. Poseidon: When it closes in Q2, the sale of 50% of Poseidon will result in an annual hit of ~$150 million ($12.5M per month). The proceeds from the sale will be reinvested by Fairfax - which will benefit the company in some way. I’ll update my models for the Poseidon sale when I know what they are going to do with the proceeds. I know what to take down. I need to know what to take up. Consolidated companies Q1 2026 $75M My annual number is $450M. There appears to be some seasonality to the business, with Q1 being the slowest quarter of the year for the different businesses. Q1 2025 was -$41M Loss was driven by Boat Rocker impairment charge of $108.6M (as part of its reverse take-over by Blue Ant Media. Example of Fairfax (finally) dealing with a chronically underperforming holding. Investment gains (losses) Equities Q1-2026 Loss of ~$100M Estimated impact of mark to market equity holdings in my tracker will be $0. Digit's stock price was down about 8% in Q1. The excess of FV over CV was $3.1B at Dec 31, 2025. This will be down in Q1. Below is a summary of the big movers in the equity portfolio in the quarter. Bonds Interest rates were higher across the curve in Q1. The increase in interest rates will have two offsetting impacts on Fairfax. This will result in a decline in the value of the bond portfolio. My estimate is -$300M. This puts estimate for investment gains (losses) at -$400M in Q1. IRFS 17 Higher interest rates will increase the discount rate Fairfax uses to value its insurance liabilities (future cash flows). This will decrease the value of the insurance liabilities. My estimate is $+350M. How will the two net out? If Fairfax matched the average duration of its bonds and insurance liabilities, the impact of higher (or lower) interest rates would largely net out. But the average duration of Fairfax’s fixed income portfolio (< 2.5 years?) is lower than the average duration of its insurance liabilities (~4 years?). The net result is assets fall less than liabilities, which results in a benefit to earnings and an increase in book value. Please note, I am still learning about this topic. So take my summary above with a heavy dose of scepticism. (Actual results will likely be quite different.) Investment Gains - Q2 2026 Q2 is shaping up to be a big quarter for investment gains for Fairfax: Sale of Eurolife’s life insurance business: estimated gain $350M Sale of ~50% of Poseidon: estimated gain $860M Total is $1.1B, or ~$50/share (pre-tax) Interest expense Q1 2026 $220M Q4 2025 run rate was $211M New issuance in Q1 2026 was $475M (~4.8%) $23M in annual interest expense. Corporate expense Q1 2026 $120M FY2025 was $481M Estimate for 2026 is $490 Tax rate Estimate is 23% Minority interest Estimate is 10% Share count Fairfax was very aggressive buying back stock in Q1 (~+300,000?). Estimate of shares outstanding at March 31, 2026: Diluted shares outstanding at 22.3M (from 22.6M) Effective shares outstanding at 20.65M (from 20.86M)

-

When interest rates were at 1% in 2020 and 2021, an interest rate of 5% was unimaginable. Of course, we got higher than that in 2024. Today, rates along much of the curve are in the 4% range. What if something happens in the coming years to spike them to 6 or even 7%? That is not forecast. Rather, just a though exercise. With fixed income it is so easy to get anchored in an interest rate paradigm that is heavily influenced by recency bias. The lesson when trying to understand Fairfax: the key is to get compensated properly for the different risks you are taking on when owning a bond.

-

That is my speculation. Here is the org chart slide from the AGM presentation.

-

@Hamburg Investor, I have no special insight into exactly how the sausage gets made. One possible framework: interest rates move in very long cycles (multi decades). 2021 was likely end of a 40 year period of declining rates (continuously lower highs and lower lows). We are likely now in a period of higher rates - higher highs and higher lows). Why? In short, many of the trends that were driving interest rates lower for 40 years have now reversed. Fairfax also approaches fixed income through a value lens. They ask: "are we being compensated for a given risk". Like duration. Credit. Reinvestment. Etc. People think they are macro investors. I don't think this describes how they manage the fixed income portfolio. Bottom line, they have an outstanding long term track record with fixed income. As a result, I try not to second guess exactly what they are doing quarter to quarter. (I do like to understand what they are doing). Succession planning: Brian Bradstreet is handing the reins to Kleven Sava (Managing Director, Hamblin Watsa, fixed income / bond trading). This is also a critically important development. Q1 is interesting to me because interest rates were trending lower at the end of February. They then shot up close to 60 basis points in about 30 days. Fairfax got a great opportunity to extend duration if they wanted to.

-

I am sceptical. My understanding is a sovereign wealth fund is created to invest the surplus wealth being generated at the time so it is not squandered and can benefit future generations (like windfall profits from oil). Canada is borrowing $25B to seed the fund - at the same time it has a historically high deficit and spiking total debt levels (and growing interest costs). We are fiscally a mess. Management: It will likely invest primarily with a strong political lense. Quebec. Atlantic Canada. Return will be an after thought. IMHO, this is not a great set up from a return perspective. Bottom line, the governments role in the economy continues to expand. This is another brand new department that will need to be staffed... But it is an interesting idea. We still do not have the specifics... so I remain open minded

-

Fairfax Q1 Results — What to Watch For? A number of P/C insurers have now reported Q1-2026 results. The pattern is consistent—and instructive. What’s Working Underwriting income remains strong Interest income is solid What’s Lagging Book value per share (BVPS) growth is muted—and in some cases declining The divergence is the direct consequence of higher interest rates. Below are top-line details for Chubb: Reported net income was $2.32 billion. But this did not include much of the decline in the value of the fixed income portfolio. The Mechanics: Why BVPS Is Under Pressure Most P/C insurers structure their balance sheets by roughly matching the duration of assets and liabilities—typically in the 4–5 year range. When bond yields rise, two things happen: Balance Sheet Impact (Immediate) The market value of existing bond portfolios declines This flows through to book value (but not the income statement) Income Statement Impact (Delayed) Maturing bonds are reinvested at higher yields This drives future interest income higher (or maintains it at a high level) The key point: The negative impact to BVPS is immediate. The positive impact is earned over time. So yes—BVPS weakness matters. Not from a solvency standpoint, but from a capital and valuation perspective (the bonds ARE worth less). Average duration matters Shorter-duration portfolios → lower hit to book value, faster earn-through Longer-duration portfolios → larger hit to book value, slower, more gradual benefit Average duration of fixed income portfolio of P/C insurance company matters. (Credit quality also matters – but we are going to ignore this variable for now – as we do not want to add even more complexity to our analysis.) Where Fairfax Financial Holdings Is Different Fairfax is not positioned like a typical P/C insurer. Average fixed income duration: likely < 2.4 years at Dec 31, 2025 Versus industry norm: ~4–5 years This positioning likely impacts Q1 results in important ways. Importantly, the average duration came down in 2025. This can be seen in the change in Fairfax’s fixed income maturity profile over the past year. Implications for Fairfax 1) Smaller Mark-to-Market Hit Shorter duration = lower price sensitivity to rising yields BVPS should be less negatively impacted (all else equal) 2) Faster Earnings Uplift A larger portion of the portfolio turns over quickly Higher yields are captured sooner, not gradually over years 3) Greater Optionality Management can reprice the portfolio rapidly if rates move again IFRS 17: Two Offsetting Forces Fairfax reports under IFRS 17, which introduces an additional layer. Rising bond yields create two largely offsetting effects: Investment Side Decline in bond values → recorded as investment losses Insurance Side Higher discount rates → lower present value of liabilities Net effect: Often muted—but not perfectly offsetting. With a short-duration asset base, Fairfax may experience: Less downside on the asset side While still benefiting from liability revaluation That asymmetry is worth paying attention to. The Real Question: Did They Extend Duration? Given the sharp move in rates during March, the key question is tactical: Did Fairfax extend duration into higher yields? Over the past year, management has deliberately kept duration short. The rationale is straightforward: Inflation risk remains elevated Investors are not being adequately compensated for taking on duration risk This is value investing applied to fixed income. When yields moved high in March, did Fairfax: Lock in those yields by extending duration? Or maintain a defensive posture and stay short? Something worth paying attention to when Fairfax reports Q1 results.

-

@Maverick47, I appreciate the feedback. There are so many interesting storylines at Fairfax. What is especially interesting about the insurance side of things is how long term they think and operate. Lots of fantastic examples. That is a big competitive advantage.

-

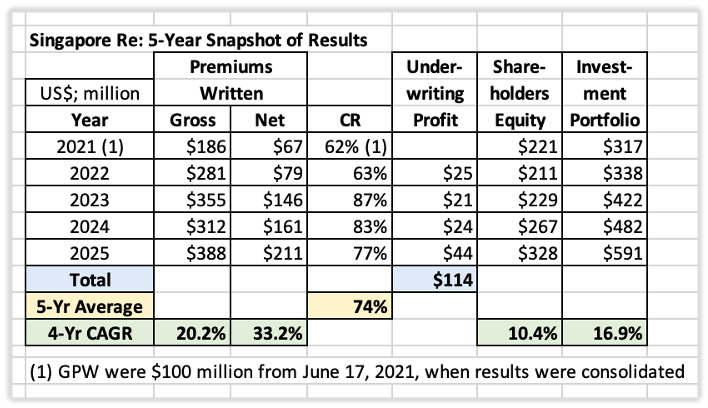

Singapore Re: A Case Study in How Fairfax Creates Value Introduction: A Small Asset, A Clear Signal What insurance operation delivered the lowest combined ratio at Fairfax in 2025? Singapore Re. Largely unknown, and easy to overlook. That is precisely why it matters. Singapore Re provides a clean, observable example of how Fairfax actually creates value—through a repeatable process built on long-term ownership, disciplined capital allocation, and high-quality operators. It is not a large asset. But it is an important one analytically. A 20-Year Investment: Ownership as a Process Fairfax’s involvement spans more than two decades: Initial investment: 1999 Increased to ~20% (associate): 2009 Acquired control: 2021 This was not a transaction. It was a progression. Fairfax did not “buy” Singapore Re in the conventional sense—it grew into ownership over 21 years. This reflects a core principle seen across Fairfax: Ownership is often the result of time, trust, and accumulated knowledge—not a single decision. People First: The Origin of the Investment The investment originated with Mr. Athappan, one of the key architects of Fairfax’s Asian insurance operations. His approach aligns directly with Fairfax’s operating philosophy: Long-term orientation Strong underwriting discipline Emphasis on relationships and trust Early identification of capable operators Singapore Re is not an isolated success. It is an outcome of this system. Fairfax institutionalized his legacy through the Athappan Cup—awarded annually to the top underwriting operation—reinforcing underwriting excellence as a cultural anchor. Patience: Strategic, Not Passive Fairfax did not seek immediate control. It waited. In 2021, circumstances changed. The CEO faced terminal illness and sought a permanent, stable owner. Fairfax—already a long-standing shareholder—was the natural acquirer. This is a recurring Fairfax pattern: Patience creates optionality. Relationships convert optionality into opportunity. Price Discipline: The Foundation of Returns When Fairfax acquired control: Paid: $103 million (to move from ~28% to ~96%) Implied valuation: $152 million Shareholders’ equity: $221 million Purchase price: ~0.69x book value This is a critical step. The investment works because it starts with a margin of safety. Everything that follows—growth, underwriting profits, investment income—compounds from a low entry point. This is not accidental. It is by design. Cycle Awareness: Scaling at the Right Time The acquisition closed just before the reinsurance hard market began in 2022. The outcome: Net premiums written: $67M → $211M (2021–2025) 4-year CAGR: 33.2% Investment portfolio: $317M → $591M 4-year CAGR: 16.9% Two things happened simultaneously: Underwriting expanded into a favourable pricing environment Investment income increased with both scale and higher interest rates This is Fairfax’s model working as intended: Capital is deployed ahead of improving conditions—and then allowed to scale. Quality: The Underwriting Engine Singapore Re is a high-quality operator: 5-year average combined ratio: 74% 2025 combined ratio: 77% (best within Fairfax) 4-year underwriting profit: $114 million In four years, underwriting profit alone exceeded the cost to acquire control. That is a defining characteristic of high-quality insurance businesses: The underwriting engine becomes self-funding—and then value-generative. Contribution: Small but Economically Meaningful In 2025: Underwriting profit: ~$44 million Represents the majority of Fairfax Asia’s underwriting income Singapore Re is not large in absolute terms. But it is highly productive capital. And at Fairfax, productivity—not size—is what matters. The Framework: How Fairfax Wins Singapore Re maps directly onto Fairfax’s operating model: People → Strong operators identified early Price → Acquired below intrinsic value Patience → Ownership built over decades Cycle → Scaled into a hard market Capital Allocation → Disciplined and opportunistic This is not a one-off success. It is a repeatable process. The Broader Lesson: Compounding Through Process Over time, Fairfax builds value through a portfolio of businesses that share three characteristics: Sound underwriting economics Disciplined capital allocation High-quality operators The outcome is not driven by any single investment. It emerges from the aggregation of many decisions made correctly over long periods of time. A collection of “singles”—executed well and consistently—drives compounding. Occasional “home runs” accelerate it. Bottom Line Singapore Re is a small piece of Fairfax. But it captures the essence of the model: Buy well Partner with strong operators Wait patiently Scale with the cycle Allocate capital intelligently And over time: Let compounding do the heavy lifting. Fairfax 2026AGM - Brian Young “Turning to the international side. We generated $220 million of underwriting profit, more than double what we generated in 2024. The standout performers – Colonnade, Bryte and Singapore Re – all generated record underwriting profits. Singapore Re, headed by Philippe Mallier, had not only the lowest combined ratio on the international side, they had the lowest combined ratio of all of our companies at 77%. Well done, Philippe.” Fairfax 2025AR Singapore Re, based in Singapore, underwrites general property and casualty reinsurance in the Asian region. In 2025, Singapore Re’s net premiums written were SGD 275.2 million (approximately US$211 million). At year-end, the company had shareholders’ equity of SGD 422.0 million (approximately US$328 million) and there were 87 employees. Prem: Fairfax Asia in 2025 produced a 90.3% combined ratio, and $49 million of underwriting profit. Singapore Re, led by Phillipe Mallier, is responsible for $44 million of the collective Fairfax Asia result. Gobi Athappan and his team oversee our companies in Malaysia, Hong Kong, Indonesia, Sri Lanka and Thailand. Brian Young has taken a hand in advising Gobi and helping Fairfax Asia realize its potential in this rapidly developing area. Fairfax 2024AR Singapore Re, based in Singapore, underwrites general property and casualty reinsurance in the Asian region. In 2024, Singapore Re’s net premiums written were SGD 215.0 million (approximately US$161 million). At year-end, the company had shareholders’ equity of SGD 364.4 million (approximately US$267 million) and there were 81 employees. Prem: Fairfax Asia increased its underwriting profit to $34 million, reducing its combined ratio to 92.1%. As noted, Gobi Athappan and Ravi Prabhakar are taking Fairfax Asia forward after the unfortunate passing of our beloved Mr. Athappan. Singapore Re, under Philippe Mallier, contributed $24 million to the 2024 result. Fairfax 2023AR Singapore Re, based in Singapore, underwrites general property and casualty reinsurance in the Asian region. In 2023, Singapore Re’s net premiums written were SGD 196.1 million (approximately US$146 million). At year-end, the company had shareholders’ equity of SGD 302.1 million (approximately US$229 million) and there were 72 employees. Prem: Our Fairfax Asia group reported a combined ratio of 93.9% and underwriting profit of $26 million. Amongst the various companies of Fairfax Asia, Singapore Re, under the able and energetic guidance of Phillipe Mallier, was the stand-out, contributing $21 million to the result. Overall direction of Fairfax Asia continues to be under Mr. Athappan, with assistance from his son, Gobi, and Ravi Prabhakar. Fairfax 2022AR Singapore Re, based in Singapore, underwrites general property and casualty reinsurance in the Asian region.In 2022, Singapore Re’s net premiums written were SGD 108.9 million (approximately US$79 million). At year-end, the company had shareholders’ equity of SGD 282.9 million (approximately US$211 million) and there were 68 employees. Prem: Fairfax Asia grew net premiums written 25% in 2022, while posting an underwriting profit of $34 million at a combined ratio of 89%. Results benefited from a full-year contribution from Singapore Re, which was responsible for $25 million of the division’s total underwriting profit. Credit to Philippe Mallier in his role as CEO of Singapore Re. And, of course, great credit to Mr. Athappan who continues to direct the overall operations of Fairfax Asia. Fairfax 2021AR Singapore Re, based in Singapore, underwrites general property and casualty reinsurance in the Asian region. In 2021, Singapore Re’s net premiums written were SGD 90.3 million (approximately US$67 million). At year-end, the company had shareholders’ equity of SGD 297.5 million (approximately US$221 million) and there were 71 employees. Prem: We were very pleased to purchase the remaining 72% of Singapore Re. Brought to us by Mr. Athappan, who is the Chairman, we first invested in Singapore Re in 2009, so we knew the company very well. It is with deep sadness that we announce that Theresa Wee, the CEO of Singapore Re, lost her health battle late in the year. Theresa had been with Singapore Re for more than three decades and her loyalty, hard work and leadership, built Singapore Re into the company it is today. Philippe Mallier is taking over as President and CEO – Philippe has been with Odyssey Group for 25 years and will remain CEO of its Latin America division. He will work closely with Mr. Athappan. We are very excited about this move as it will help link our North American operations with our Asian operations. Mr. Athappan, Brian Young and Andy Barnard have made this happen. Additional investment in Singapore Reinsurance Corporation Limited On June 17, 2021 the company increased its ownership interest in Singapore Reinsurance Corporation Limited (“Singapore Re”) from 28.2% to 94.0% for $102.9 (SGD 138.0) and subsequently increased its ownership interest to 100%. Singapore Re is a general property and casualty reinsurer that underwrites business primarily in southeast Asia. Fairfax 2009AR: Application of the Equity Method of Accounting The company began acquiring common shares of Singapore Reinsurance Corporation Limited (“Singapore Re”) in 1999 and until December 24, 2009 accounted for its investment in 17.5% of the common shares of Singapore Re as available for sale at fair value. On December 24, 2009, the company increased its interest in Singapore Re to 20.0% and determined that it had obtained significant influence and, accordingly, the company changed the accounting treatment of its investment in Singapore Re from available for sale to the equity method of accounting on a prospective basis.

-

P/C Insurance - Structural Strength Revealed - Insights From the 2026 AGM - Part 2 Transcript from Fairfax’s AGM – April 16, 2026 (lightly edited to make it more readable) Question from Jeff Stacey Prem and Peter, our first question is about the current insurance environment. The question is as follows. Fairfax had record underwriting profits in 2025 of $1.8 billion and achieved its objective of $1.5 billion. You commented, however, in your shareholder letter that insurance pricing is beginning to soften. I would appreciate hearing any additional comments you might have about the current insurance underwriting environment. And specifically, do you think that Fairfax can still achieve its $1.5 billion underwriting profit target in a soft insurance market? V. Watsa - Founder, Chairman & CEO Thank you, Jeff. Peter will usually answer this. But we do have Andy Barnard, Brian Young, Lou Iglesias and Silvy Wright here. So, we'll ask them instead. As Andy makes his way up to speak, let me just say… yesterday I had people ask me: “What is the biggest -- best -- acquisition you've ever made?” The best one is Markel Insurance - the first one (1985) - because otherwise, you're not in the P/C insurance game. And the second best was a small company called Skandia America Re (1996). And why? Because I had to get someone to run Skandia. I went to New York three times to get Andy Bernard. The first time he said, "You got to be kidding me.” Over dinner he said, “I'm not going to leave Transatlantic to come and join Skandia." That's how it began. After a second and third attempt, ultimately, we were fortunate to get him 30 years ago. He's had a huge impact on Fairfax. In 2011, all of the insurance companies began reporting to him. After he started in his new role – 15 years ago (2011) – he said that he hoped that the insurance business will have the same reputation of being fantastic like the investment business that we had at the time. And the investment business did a little less well, and the insurance business has done fabulously well. Andy, over to you. Come on in. Andrew Barnard - Chairman of Fairfax Insurance Group Thank you very much, Prem, for all of that. I'm going to let Brian and the others talk about our position, the market and our prospects. As Prem mentioned, I've been in this role now for 15 years, and I thought I'd just give a little brief broad perspective on how I look back on that. I divide that 15 years, which started in 2011, into two periods. First, 2011 up to 2019. Looking back with the benefit of hindsight – this was a period of preparation. During that period, we added Allied World and Brit – two very powerful new platforms with capabilities that really build out our suite of products. We had Crum & Forrester, bolstering its capabilities. We had a few small acquisitions. Earlier on in that time Northbridge finished its integration, which really positioned it as a much stronger company. And of course, during this time, Odyssey and Zenith flourished. (Yes, Zenith had a few tough years at the beginning.) And we built out the international operation during the latter part of that first period. As Peter mentioned, it has become a significant business that we think will serve us well in the future. This was really a period of preparation that brought us to 2020. At Fairfax, across our companies, we now had in place excellent leaders, leaders that are fully aligned with Fairfax’s culture, that embody the trust, the transparency, the talent that without which our decentralized system could not function. That's all in place as we roll into 2020. Of course, the big thing at the start of the year was the pandemic. A lot of companies heading to the hills, a lot of uncertainty. Plus, we had a very attractive hard market that had already been underway – and I think the pandemic just accelerated it. So, we were at that time in just a unique position because of our structure, our capability, our leadership to thrive. And thrive, we did. Over the subsequent years, we go into the second period, 2020 up to 2025. From 2020, we virtually doubled our premium volume, and almost all of that was organic with the one exception of GIG. The vast majority of that growth was organic, driven by our companies by their leaderships, by their management teams. And more importantly than that, our underwriting profit over that period more than quadrupled. This is where we really came into our heyday. Today, to 2026, we're recognized as an underwriting powerhouse in the industry by the marketplace, by the rating agencies. We had huge increases in our ratings over the last 1.5 years. Looking back on it all over the past 15 years – with the benefit of hindsight – we just positioned ourselves so favorably to really take off when the market conditions were supportive of that strategy. I believe that what we built is built to last. It is built to withstand the pressures of the market cycle. Those who follow the industry know that we're in a softening cycle where things become more challenging. But we're very confident about our capabilities – about our management abilities – to navigate through some more challenging times and to sustain superior performance as we go into the future from here. I've been in this industry now for close to 50 years. I've been at Fairfax for 30 years. I'm not going anywhere quite yet. However, my good friend and partner of the last 36 years, Brian Young, is taking on a larger and larger share of the oversight responsibilities in Fairfax. Those of you who have followed Odyssey will know Brian took the helm in 2011. It's very clear that Brian is someone that knows how to make money in this business. And so, I think our future is very, very bright as we move forward from here. So let me turn the microphone over to my friend, Brian Young. Brian Young - President of Fairfax Insurance Group Thank you, Andy. I learned some big news a few minutes ago. Andy told me that he is going to be a grandfather for the third time. So big hand to Andy. I will cover the AI question (from earlier), the current market environment and our ability to generate an underwriting profit in the current environment. But first I want to highlight, as Peter mentioned, $1.82 billion of underwriting profit in 2025, fractionally higher than $1.79 billion in 2024. Combined ratio of 93%. Embedded in that was 4.8 points of CAT loss or the $1.2 billion, the biggest being the California wildfires in Q1. Within the 93%, we benefited from 2.9 points of favorable reserve development. And it's important to note that Fairfax has had 19 consecutive years of favorable reserve development for the last 2 decades. Our reserves have been a store of value. As you all know, all of our companies are really focused on disciplined underwriting and strong reserving. Prudent reserving is really foundational to disciplined underwriting. We have more than 30 operating companies. Nearly all of them equalled or exceeded expectations from an underwriting perspective in 2025. The small number that didn't – we weren't expecting them to make underwriting profits given the market circumstances that they faced. So, there were no negative surprises in any of our companies. I'd like to highlight a few standout performers, focused first on the big companies. Let's start with the most recent recipient of the Athappan Award, Allied World. Our largest insurance company generating record underwriting profit of $546 million – a fantastic result. Congratulations, Lou and to the team. I'm going to let Lou come up and tell us what the secret sauce is that's made Allied World so successful. The second company I'd like to highlight is last year's recipient of the Athappan Award, Northbridge. Silvy and team delivered the lowest combined ratio, at 88.3%, of all our big companies. In the last 4 out of 5 years, Northbridge has delivered a combined ratio below 90%. And Silvy will come up after Lou and give us an update on Northbridge. Turning to the international side. We generated $220 million of underwriting profit, more than double what we generated in 2024. The standout performers – Colonnade, Bryte and Singapore Re – all generated record underwriting profits. Singapore Re, headed by Philippe Mallier, had not only the lowest combined ratio on the international side, they had the lowest combined ratio of all of our companies at 77%. Well done, Philippe. Our premiums were $33.3 billion. It is slowing down. The market is getting more challenging, no doubt. And we have to exercise more discipline. We have to be more selective in the risks that we take. We have to focus on our line size deployment. But we still think there's opportunity out there in the market. The sectors of the business that are under the most pressure are the ones that have generated the most profit. So yes, the margins are shrinking, but we still think the margins are ok. When the margins are not there - when there is not that margin of safety we need to take on the volatility of insurance – then we're going to scale back. There's no pressure on any of our companies to write for top line growth. And I've experienced that at Odyssey working there for 28 years, leading it for 14 years, never did I or any of our people have any pressure to write for top line. On the question of AI, it's important in our decentralized structure, innovation comes from the ground. It can't be forced from the top down. And we've got 30-plus wonderful businesses. Everyone is focused. AI may well be very transformative. We're not at the cutting edge, and we don't really want to be at the cutting edge. We're where we think we need to be in the pack with the rest of the insurance industry. To understand and take advantage of the innovative things that we're doing at the company level, we formed an AI working group, across the Fairfax organization. We have more than 75 people participating in the working group. We have developed more than 100 use cases. We have a SharePoint site. If we develop a use case in a company in a certain part of the world, we can share that with the other companies through the forum, through the SharePoint site. In terms of the AI use cases, most of them have really been focused on improving process, doing things faster and smarter – trying to underwrite more business efficiently through the use of AI. Using AI to inform our underwriting decisions. Marc Adee (President of Crum and Forster) has used the phrase, and I think it's great, does AI bang the cash register, does it lower your loss ratio, does it lower your expense ratio? I would say right now we're not banging the cash register yet. With AI, we are able to underwrite more business using the tool than previously. Lowering the loss ratio, lowering the expense ratio in terms of the AI tools that we're using, that's really the focus. And I think lastly, it's really important to say, and Prem has emphasized it ad nauseam that AI will not cost us any jobs. We don't believe in laying off employees. Period. And that includes AI. If AI allows us to operate more efficiently then maybe the rate of growth in our employee count will slow down, which will help the expense ratio. But it won't come at the expense of people. Thank you. Now I would like to turn it over to Lou. Louis Iglesias - President of Allied World Thank you, Brian. Great to see everybody. It's good to see so many of you, I only get to see once a year and talk about our businesses here at Fairfax and at Allied. And it's also not every day that I feel like Allied World has won the Stanley Cup. So we're really proud of that as well. Brian mentioned our underwriting profit. We did have a record year last year on underwriting profit. We also had a high watermark on our net income. And I just want to recognize the investment group at Fairfax, who does a tremendous job on our portfolio. Having that type of net income really helps our cash flow and everything else. So, it's really, really good to see. We grew our company to $7.4 billion last year. And Brian talked about the market a bit. It is softening some. I would say it's getting a little bit more price competitive. But for those of you who've been with our industry for a long time, it's not a traditional soft market. We're not bottoming out. Terms and conditions are holding pretty well. Combined ratios don't have so much pressure on them, still manage the profitability. There are opportunities around the world to be able to get some growth. So we're not giving up on that because I think there are certainly some opportunities. What I wanted to talk about just for a couple of minutes is what are some of the things that we do to help us manage the cycle. We feel like we've built a company that could perform in all segments of the cycle. And in order for that to happen, we have to execute on many strategies every single day. The company has to be structured in a way to give us that ability. There are a couple of things in there. The first thing to talk about is the structure of having a very flat organization. You see that elsewhere in Fairfax. We have a very flat organization at Allied. We don't have many layers. So strategies and communication moves quickly. This gives us the opportunity to move fast in different marketplaces around the world. So as the markets change, we can change strategies. We can execute on those strategies. Our underwriters are at the desk since there's not lots of layers. They don't have to get multiple sign-offs to do their job to able to make a decision. We run with the mantra of hire really great people. And give them the authority and accountability to be able to get the job done. Additionally, we have product diversity – over 40 products. We are in 29 offices around the world – 11 countries and 4 continents. We're expanding our presence around the world geographically. So, the earnings stream is very diverse. And when we have that type of diverse earnings stream it really limits earnings volatility. So when the market starts to get a little bit tougher, it's really helpful to have different earnings streams because you may have to slow some down. If you're not getting the marketplace that you like in a certain product or a certain country, you're going to have to slow that down, but maybe there's an opportunity someplace else. So the diverse earnings stream is really very helpful. And I think you see that throughout Fairfax as well. The third thing that I would touch on is underwriting discipline. Underwriting discipline helps in every marketplace, whether it's a hard market, soft market in the middle. It's extremely important. It runs through every Fairfax company. It's part of the culture of Fairfax. Now what does that mean really? Our underwriters understand rate adequacy, they understand when they're negotiating a deal, where that rate crosses the line to not being enough for the exposure that they're taking on. When we run into that situation, we have the ability to say no. We say no a lot more than we say yes. But what we really prefer to do is to say, "No, we don't like the deal that way, but we do like it this other way. And we'll put a proposal out that works for us, and we hope works for the client. And we've been able to do business like that and sell deals like that fairly often, even in this marketplace when things are getting just a little bit softer. So that's been very helpful. Now nothing works without great people. And every year, I come up here, and I think I talk about how great the people are at Allied. We've had people with us for a very long period of time. They've seen all different cycles, so they understand how to manage in and through the different cycles. And we have a very low attrition rate at the company. So our people are really the key to making all the strategies work. And so for us, we're going to continue to do the things that we're good at. As the markets soften some, we're going to limit our mistakes so that when the market does get to a better place, we can do all the things that Andy talked about that we did a couple of years ago and not have any distractions. Thank you very much, everybody. Have a great day. Silvy Wright - President of Northbridge Financial Good morning, everyone. First, I'll start with a little confession to Lou. Northbridge employees wanted to do a Rory McIlroy (repeat as winners of the Athappan Cup), but we are happy that Allied World won this year. First a little perspective on Canada. Northbridge represents the Canadian insurance operations for Fairfax. With $3.4 billion in revenue, we're the third largest commercial insurer in Canada. We have a very good position - maybe a smaller fish at Fairfax but a bigger fish in this country. What are market conditions? What happened in '25, as Lou said, the price competition really started to ramp up. And we're starting to see competitors trying to buy business. And sorry, I apologize for being a broken record, but once again, we are not pressured to write premium at a loss. And so, in 2025, our employees did the right thing. They remained disciplined, not only in underwriting but claims and expense management. But equally important, we doubled down on really focusing on customer loyalty, customer service and customer safety. So not only be there when things go wrong, but we're trying to help our customers have safer operations. As a result, we did not grow in 2025. However, we did have a record year, as Brian noted. In 2026, it looks like the price competition continues and we will manage accordingly. Along with just being disciplined, we're also looking at building areas where we can grow when it's the right time to grow. For instance, increasing our lines on renewable energy in Canada. So just manage the market and then be ready to go when it's time. And one more comment. We talked about the culture many times and the beautiful word of being empowered not just at the president level, but throughout the company. I just wanted to share with you that our employees are like you, they're shareholders. Over 70% of our employees at Northbridge are shareholders. So not only are they empowered but they're owners in doing the right thing. Thank you. V. Watsa - Founder, Chairman & CEO Thank you very much Silvy. Peter, anything to add, final words, on the insurance industry? Peter Clarke - President & COO Sure. Just two quick things, Prem. And I mentioned in my remarks that we write $33 billion of premium across the world and that grew by 2.3% this year. It's interesting when you look at the international operations and how we benefit from diversification and scale. Bryte in South Africa grew 20% this year, Colonnade 18%, Asia was up 15% and Polish Re was up 15%. And so even though North America rates are coming down, we're maybe not growing as much, we have all these opportunities around the world. Secondly, I just have to comment that we have 2 cups in Fairfax. One is the Mr. Athappan Cup. And we also have a hockey game between the Fairfax head office and the Allied World Group, and unfortunately, now Allied owns both cups for this year and I have to say it did come into the evaluation process a bit, but we left that aside.

-

P/C Insurance - Structural Strength Revealed - Insights From the 2026 AGM - Part 1 Introduction Property & casualty (P/C) insurance has historically been the foundational economic engine behind leading insurance conglomerates. At Berkshire Hathaway, it enabled decades of above-average compounding. At Fairfax, its importance is even greater. Fairfax is more leveraged to insurance float than Berkshire was at a comparable stage. As a result, understanding the quality, structure, and evolution of Fairfax’s insurance operations is essential to evaluating the company’s long-term earning power and intrinsic value. The April 16, 2026 AGM provided an unusually transparent window into that engine—not just through senior leadership, but through the operators running the business day to day. Why the 2026 AGM Matters Fairfax continues to distinguish itself through openness. Rather than tightly controlling messaging, the company brought forward leaders across the insurance platform—Andy Barnard, Brian Young, Lou Iglesias, and Silvy Wright—alongside Prem Watsa and Peter Clarke. This matters for three reasons: Depth of insight: Investors hear directly from operators, not just executives Organizational visibility: Reveals strength of bench and succession planning Cultural transparency: Demonstrates how decentralization actually functions Over time (multiple AGM’s), this approach compounds in value. Investors are not simply evaluating reported results—they are evaluating the system that produces those results. A Unifying Theme: Structure Over Cycle Across all speakers, one message was consistent: Fairfax’s insurance performance is structural, not cyclical. Current results are not simply a function of a favorable insurance market. They are the outcome of deliberate decisions made over decades—particularly around leadership, culture, and capital discipline. 1. Prem Watsa: People, Not Cycles, Drive Outcomes Prem’s opening remarks did not focus on the near-term insurance outlook. Instead, he reframed the discussion around what he views as the true foundation of Fairfax’s success: people and long-term decisions. Key Ideas Best acquisitions = foundational moves, Markel (1985): established Fairfax in the P/C insurance business Skandia America Re (1996): pivotal because it led to recruiting Andy Barnard People drive performance Significant effort to recruit Barnard His leadership has shaped Fairfax’s insurance operations over decades Long-term transformation of the insurance business In 2011, insurance leadership was consolidated under Barnard Goal: build an insurance franchise with a reputation equal to Fairfax’s investment arm Result: insurance is now a core strength of the company Interpretation Fairfax’s underwriting performance today reflects institutional capability—not cyclical tailwinds. The competitive advantage is embedded in people and culture. 2. Andy Barnard: From Preparation to Performance Barnard provided a clear framework for understanding Fairfax’s evolution over the past 15 years: Phase 1: Build (2011 – 2019) Expansion through acquisitions (Allied World, Brit) Strengthening leadership and structure Integration and cultural alignment Development of international operations Phase 2: Execute (2020 – 2025) Premiums nearly doubled (primarily organic) Underwriting profits more than quadrupled Full participation in a favorable market Interpretation The “hard market” did not create Fairfax’s results—it revealed them. Years of preparation positioned the company to capitalize when conditions turned favorable. 3. Brian Young: Discipline in a Softening Market Brian Young grounded the discussion in current performance and market conditions. 2025 Performance Snapshot Underwriting profit: $1.8B Combined ratio: 93% Cat losses: $1.2B (4.8 pts) Favorable reserve development: 19 consecutive years Operating Quality Broad-based execution across ~30 companies No negative surprises (all companies met or exceeded expectations) Reserves function as a long-term store of value Market Behavior Pricing is softening Increased underwriting selectivity No pressure to grow without margins AI Strategy Decentralized, bottom-up implementation ~75 participants, 100+ use cases Focus on efficiency (loss ratio, expense ratio) Importantly, not a job displacement strategy Interpretation Fairfax is behaving like a high-quality insurer late in the cycle: Protect margins. Preserve capital. Avoid undisciplined growth. 4. Allied World: A Platform Built for Cycles Lou Iglesias demonstrated how Fairfax executes at the operating level. Performance Record underwriting profit and net income ~$7.4B in premiums Continued global expansion Despite a softening market, conditions remain rational Pricing is more competitive, but not collapsing Terms and conditions are holding Margins remain acceptable Structural Advantages 1. Flat Organization Faster decision-making (minimal bureaucracy) Authority pushed to underwriters (point of action) 2. Diversification 40+ products 29 offices globally Multiple earnings streams reduce volatility 3. Underwriting Discipline Willingness to walk away Ability to restructure deals (rather than accept poor terms) Embedded cultural behavior Underlying Driver: People Experienced underwriters Low turnover Deep cycle knowledge Interpretation Allied World is not reacting to the cycle—it is structurally designed to manage it. The key in softer markets is limiting mistakes – preserving capacity for future opportunities when conditions turn favorable again. 5. Northbridge: Discipline Over Growth Silvy Wright provided a Canadian lens. Snapshot ~$3.4B revenue #3 commercial insurer in Canada Delivered strong results despite no growth in 2025 Strategic Positioning Rising price competition No compromise on underwriting standards – no pressure to write unprofitable business Focus on claims, expenses, and customer outcomes (service, safety, building loyalty) Long-Term Orientation Patience: growth deferred until economics justify it Targeted expansion for future growth (e.g., renewable energy) 70% employee own Fairfax stock → strong alignment with shareholders Interpretation No growth is not weakness—it is discipline. Northbridge is optimizing for long-term value, not short-term premium volume. 6. Peter Clarke: Scale and Global Optionality Clarke highlighted two structural advantages: 1. Global Diversification Strong growth outside North America: South Africa: +20% Colonnade: +18% Asia: +15% Polish Re: +15% This enables: Capital reallocation across markets Offset to regional pricing pressure Sustained overall performance 2. Scale ~$33B in premiums Broad global platform Scale improves: Risk diversification Data and underwriting insight Competitive positioning Interpretation Fairfax’s global footprint is a strategic asset. It allows the company to navigate local cycles while maintaining consolidated strength. Synthesis: What the AGM Reveals Across all perspectives, a coherent picture emerges: 1. The Insurance Business Is Now a Core Strength Not historically true—but now clearly established. 2. Results Are Structural, Not Cyclical Driven by leadership, culture, and discipline—not market conditions alone. 3. The Organization Is Built for Cycles Decentralized decision-making Embedded underwriting discipline Long-tenured operators 4. Capital Discipline Is Intact No pressure to grow at the expense of profitability. 5. Global Scale Provides Flexibility Geographic diversification allows dynamic capital allocation. Conclusion The 2026 AGM reinforced a critical conclusion: Fairfax’s P/C insurance platform has matured into a high-quality, structurally advantaged underwriting franchise. What investors are seeing today is not a peak—it is the visible output of a system built over decades. As the cycle softens, the real test begins. Based on the evidence presented, Fairfax appears positioned not just to withstand that transition—but to use it as the next stage in long-term value creation. Continue to next post to read transcript from AGM.

-

@Lazarus, yes, it makes perfect sense for Canada and the US to do a free trade deal. But economic theory and Trump's agenda are two completely different things. What if the deal trump wants to make is not in Canada's long term best interest? I am not talking about small issues like dairy. Why is it in the US's best interest to allow ANY manufactured products to come from Canada (auto's etc)? Or put another way, is your perspective that Carney should just sign the best deal he can get? I don't have a strong opinion because I am not in the meetings with the US people. And I like that Carney is not negotiating in the public (like Trudeau usually did). My guess is if Canadian's knew what the US wants in a new deal they would be shocked. I think Canadians are grossly underestimating (still) how much the world order is changing. Our views are much to anchored on the past. We still think we are in a Disney movie - waiting for the Disney ending - that is never coming. I am optimistic. But we will have a couple of tough years to get through. Adversity, after all, is what builds character.

-

@Lazarus, you are assuming Trump wants to do a deal with Canada. Why do you think that? My view is Trump has no interest in doing a deal with Canada. (Why would he?) I am not sure why everyone is so infatuated with Carney and China. And ignoring that he has done the same sort of thing with the EU, the middle east, India etc. Canada exports commodities. Carney is simply saying Canada is willing to do business with the world. This is a massive change from Trudeau - who lectured the US/China/India/Saudi Arabia etc on how they should run their countries. Canada's economy is sick. Carney understands that basic fact. He is pivoting the country and its basic economic/trade relationship with the rest of the world. Its basic framework is 'rational pragmatism'. Music to my ears.

-

@cubsfan, I am not a Trump hater (as a change agent). But he is so binary: great good or great bad. My assessment is over time, the bad is smothering the good. Of course, I am coming at it from the perspective of a Canadian - that matters. At the end of the day I am trying to understand what is going on so I can navigate me and my family through it as best as possible. This board has helped me a great deal. So thank you to those who post.

-

Perhaps a better way to explain the skit: this is Trump and Iran in negotiations today. Some of us see how ludicrous the situation is. Others try to explain how rational ("right") one of the participants is (depending on which team they are on). The longer the skit goes on the more they are convinced they are right (and the more vociferous they become in trying to explain why they are "right")... Sometimes the real world is better than fiction.

-

@Hoodlum, this makes sense. Fairfax has been slowly selling down their Blackberry position. Perhaps they took advantage of the recent spike in the share price to exit the position. This would do a couple of things: Free up some capital that can be reinvested into other above average opportunities that fit Psychological: exit a long term mistake (Was Blackberry their worst long term investment?) At the end of the day, I don't have an opinion on what I think Fairfax should do. BB is a small investment today. I trust Fairfax will make a good decision (keep or continue to sell). But it is interesting to speculate - BB continues to provide lots of entertainment value.

-

I have been trying to come up with a mental model to help me understand Trump and US policy today. I think I just found it - the Abbott and Costello skit: Who's on first? This is what Trump sounds like on most issues - the war in Iran just being the latest example. Now imagine trying to take sides: Which of the two people in the skit "is right?" Of course that is a ludicrous question. But it does help me understand some of the people who post in this section (who do their best to try explain the logic in what Trump/US is doing).

-

@LC and @JGBRK, I appreciate the comments. What has made Fairfax such an interesting investment over the past 5 years is it keeps morphing into something better. It has been a 5 years voyage of discovery. We all have been chronicling this amazing journey on this wonderful board. 2020: Turnaround play 2022: Value play 2024: Quality play This has important implications for investors: it requires an open mind and flexibility in both framework and thinking. The people on the board who have approached Fairfax this way have likely done very well with their investment over the past 5 years. 'To The Man With A Hammer, Every Problem Tends To Look Like A Nail' Charlie Munger Munger’s quote above describes how most people look at and value Fairfax. They have been in a straight jacket for the past 5 years and they don’t even know it. As a result they have likely missed out on one of the great investments. I think Fairfax is in the process of morphing again. This change is being driven by the soft market in insurance. What is happening? Fairfax is entering its “BRK 1980’s/1990’s” phase where capital allocation and compounding will be the primary driver of growth in economic/intrinsic value moving forward (not top line growth in the P/C insurance business). BRK delivered outstanding growth in economic/intrinsic value per share in soft insurance markets in the 1980’s and 1990’s and I suspect Fairfax will do the same in the coming years. There are a lot of parallels with Fairfax today and BRK in the 1980’s/1990’s. Yes, there are also important differences. One being Fairfax is much more levered to float. Another being how it does capital allocation (different does not mean worse). Another being Fairfax is international. But to capture the opportunity with Fairfax moving forward, investors will need to once again update their investment framework. This will allow them to better understand what is coming (fundamentals, earnings and growth in economic/intrinsic value per share). Most will not (like what has been happening the past 5 years). Actions have consequences. Each set of investors will earn their just reward.