Spekulatius

-

Posts

15,180 -

Joined

-

Last visited

-

Days Won

38

Content Type

Profiles

Forums

Events

Everything posted by Spekulatius

-

Russian NG was never that cheap in Europe, Europe had already to deal with higher energy costs for a while, that’s nothing new. Now Europe is going to pay spot and later contract prices for LNG to replace the natural gas. Those prices are higher than what they used to pay , but much lower than the prices that they are paying now. I don’t see a widespread de- industrialization but I think some industries that use a lot of Ng like basic chemicals and steel production are going to be challenged. I do think that the current situation in Europe will lead to even more renewables for energy but how to ensure grid reliability with all those fluctuations in production is going to be a challenge. I also think we are going to see a boom in defense spending for perhaps a decade pretty much everywhere (Europe, US, Asia, China).

-

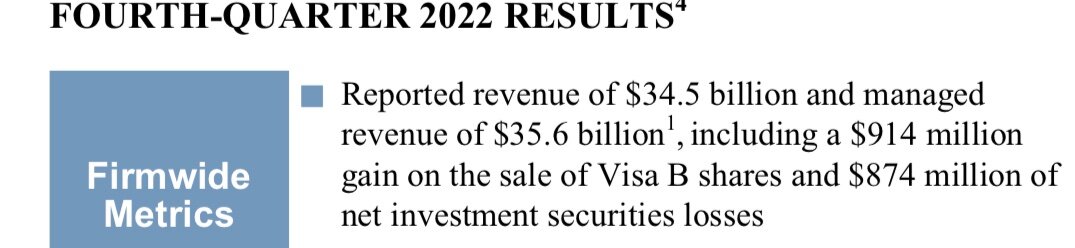

Can the Visa and Mastercard moat be bridged?

Spekulatius replied to Sweet's topic in General Discussion

Hm, I checked their release and it looks like they smashed the VISA piggy bank to compensate for other losses, At least it reads that way. VISA shares have held up pretty well (as did their business) so I see how it is enticing to sell those shares, especially if you expect an economic hurricane.

-

A cording to Ukrainian sources, the Russians are losing 500-600 soldiers on average/ day. That estimate of combat count casualties may be a tad optimistic, but I think Russia also loses people where Ukraine does see them (thickness, accidents, weather related and other attrition losses etc). If the losses are about correct, and we take a 550 average loss number per day, then Russia is going to lose 200k soldiers/ year and will need to new recruitment drive every year to keep this up. The 300k they raised in fall 2022 will be spent next fall. We probably need to give Ukraine more decisive weapons that allow for deceive wins in addition to the ability to strike these drone bases that continue to bash the Ukraine infrastructure. Europe is a relatively good shape. My brother is telling me that energy prices even for consumers are now rapidly dropping and the economy isn’t too bad. The meltdown from an energy crisis has been avoided for sure. Gas is at 64 Euros/MWH down from a peak of over 300 Euros, but still tripple the price from 2020. It’s won’t get all the way back to 2020, but I think it could go to 30-40 Euro pretty quickly. Storage in Germany is still 90.7% full and 83% in Europe overall. Further ore, the discounts on Russian crude keep increases as they have to dump this on fewer and fewer buyers apperntly.

-

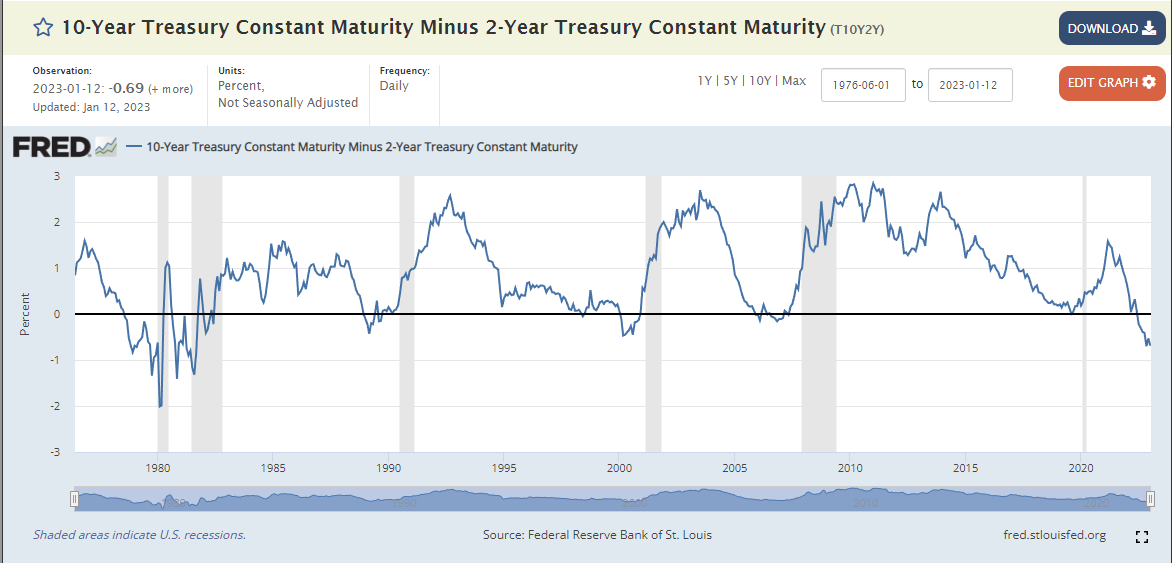

Where Does the Global Economy Go From Here?

Spekulatius replied to Viking's topic in General Discussion

Yield curve is deeply inverted now. So far, its 5/5 while I have been "watching" markets predicting recessions:

-

Why would a person in the US have a brokerage account with Schwab when Fidelity offers exactly the same thing, but gives you interest on your cash (currently ~3.7% in SPAXX) when Schwab pays you almost nothing (unless they changed this recently). Besides IBKR, Fidelity is about the only mainstream broker that gives you decent interest on cash balances / MM funds.

-

Reason 1) The labor market is about the only thing that the Fed has an influence on, by increasing interest rates to slow the broader economy . The Fed has no impact on crude, energy, food prices and many other things. Since the tight labor market presumably means persistent wage pressure, it is a number that the Fed is closely looking at, since it impacts core inflation. Reason 2). The Fed has dual mandate of facilitating price stability and maximum employment. Typically the two are contradicting each other - full employment means wage pressure which leads to inflation and that contradicts the primary mandate of price stability. Price stability is the most pertinent issue right now, so the fact that we do have basically full employment (which has in the past been defined as unemployment rate <5%) it means that the Fed should tighten to reduce inflation as long as the full employment mandate is not impacted.

-

The fact that the bond and equity market doesn't believe the Fed is one of the core issues for the Fed. The Fed needs to regain credibility and that is why I think higher interest rates for longer is a likely outcome. This will also prevent a whipsaw of inflation that we could see. It's very clear that CPI data is rapidly cooling for now, but it is less clear that core inflation is cooling to the extend that it allows for the 2% inflation benchmark. The labor market so far has not shown much indication of slowing (unemployment still at 3.5%) so that gives the Fed a lot of leeway. Same with the USD has been weakening, which also takes of systemic risk from USD shortage. Also, what happens if CPI data starts to re-accelerate because energy costs start to rebound, which is what many are expecting here? Just random musings of course.

-

I wish there were 9-10% wage increases. Not in my or my wife's circles that's for sure. They are just not happening.

-

Sold remainder of TMUS and LMT. Also sold HOPE (which i just bought) about flat. Didn't like the CFO leaving as well as earlier comments back and forth with the SEC regarding their filings. I don't like to be an hero.

-

Can the Visa and Mastercard moat be bridged?

Spekulatius replied to Sweet's topic in General Discussion

I don’t think we need to be worried about V and MA. The larger implication are for some of the Fintech that facilitate certain aspects of the payment process. Companies like Adyen or PayPal come to my mind or the owners of Zelle (large banks etc). Some might be able to take advantage of the new Infrastructure provided by FedNow and others may be disrupted. I think something like Adyen in particular could get disrupted, but I don’t know the inner working of payment well enough to be certain. I do know that Adyen facilities payments for large companies and that seems like something that Fednow can address, if not right away then later. I think it also makes competition easier for smaller financial institutions , as they get access to the Fednow infrastructure at the same terms than larger ones. So if you are a low cost tech savvy internet only bank, you may love Fednow, as you can now provide services to the customer better than before. -

Sold IAC today - 15% loss. That Meredith purchase looks like a turd to me. Maybe I am giving up and selling too soon, wouldn't be the first time.

-

Can the Visa and Mastercard moat be bridged?

Spekulatius replied to Sweet's topic in General Discussion

Looks like Fednow service is about to launch. I think this will be more disruptive to some Fintech than to VISA and Mastercard: https://www.frbservices.org/financial-services/fednow/about.html Hopefully, it will replace the painfully slow ACH transfer (for which some banks are still charging money). Fees look low: https://www.frbservices.org/resources/fees/fednow-2023 -

What do you think of Analyst Estimates and how useful are they?

Spekulatius replied to Luke's topic in General Discussion

The red (estimate) line seems to have some predictive power at turning points. -

What do you think of Analyst Estimates and how useful are they?

Spekulatius replied to Luke's topic in General Discussion

The short term estimates are useful to understand the market earning expectations. If they are missed the stock is likely going down. -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

Spekulatius replied to tnathan's topic in General Discussion

I think the insurance brokers were cheap when Spitzer was investigating them for these contingent fees. O don’t think they were 1*or 2* rated. I didn’t buy them because I didn’t understand the business model. There was concern that the absence of these fees would break the business model. I don’t think the brokers were really cheap since that episode about 10+ years ago, with the exception of a short period in 2015/16 (the mini recession) back then probably. Even great business get cheap once in a while, but it could be a once or twice decade event. Lot’s of patience required to acquire a position and then you need to sit on it, which is is even harder. -

Bought a bit of $HOPE today, the US-Korean focused bank brought up by @dealraker. I suppose it's down due to the CFO leaving. Paying about tangible book is a good bet here and it pays a decent dividend as well.

-

What is Putin’s snickers bar? https://www.wsj.com/articles/playing-risk-made-cold-war-kids-masters-of-an-unruly-globe-11673015444?mod=trending_now_news_4

-

Read the disclosures in the 10-Q or 10-K for same store revenues. You will be surprised. They do supply these details. I haven’t checked Realty Income recently but have checked on other NNN Reits and they typically are in they 2-3% range. Rent increases may have an inflation clause but they are capped. NNN is about the worst asset class you can own as Reit in times of high inflation. They are really much more a bond than real estate.

-

I bought my first house in 2002. The mortgage rate was 6.75 percent with BofA in spring 2002. So mortgage rate like we currently have currently certainly have are not exactly a new experience, thry were around exactly 20 years ago. I do think that once the Fed stops raising, mortgage rates will come down, because the margins that banks or mortgage lenders need will come down. That’s due to the convexity nature of MBS in a rapid rate rising cycle, I think. I do think the Fed already signaled that they won’t cut in 2023, but they may be about to be done rising for now. Maybe another 0.25% rise and we could be done.

-

The tripple net landlords will get destroyed when higher inflation persists. Their rent escalation is typically 2% annually which means you are buying a bond more so than real estate.

-

I bought some CPT (sunbelt MF) and ESS (West coast MF). I think Multifamily Reits have outperformed the SPY over the long run, but not lately (last few years). Lower interest rates have to do with it (not lately though) but I think pricing power and lack of terminal value risk and relative stability of rents are factors that make this a good asset class. Best asset class in Reits may be trailer park Reits like ELS and SUI but both still trade at pretty rich multiples.

-

The reason for the run doesn’t matter. They hold a bunch of securities , some HTM and some MTM that are have a fair value below the price they are held on thr balance sheet. If there is a run in the bank, they need to sell the securities and realize the losses and this will deplete their capital. I think SI is probably done here, I don’t think they will survive this. They also have liabilities from money laundering etc charges that are unknown and likely one of the causes of the run on the bank. FWIW, all these banks associated with crypto that have taken deposits have huge problems. Thats where regulators need to look to make sure that crypto does not impact the banking system. These banks like SI are on-ramps to crypto ecosystem and with crypto deflating there is ann impact on those FDIC insured banks.

-

Belgian beer St Bernardus :

-

Online Tool To Summarize SEC Form 4 Insider Stock Sales?

Spekulatius replied to persistentone3's topic in General Discussion

Openinsider.com: http://www.openinsider.com -

Movies and TV shows (general recommendation thread)

Spekulatius replied to Liberty's topic in General Discussion

“The Recruit” is definitely satire. think, “The Office” but with CIA instead of Dundee Mifflin paper company. It’s not the greatest show, but fairly entertaining.p for what it is.