Spekulatius

-

Posts

19,034 -

Joined

-

Last visited

-

Days Won

39

Content Type

Profiles

Forums

Events

Everything posted by Spekulatius

-

What are you listening to ? (Music thread)

Spekulatius replied to Spekulatius's topic in General Discussion

I liste mostly to rock music, I sometimes I like the fine arts: -

Europe may not be investable, but at least it can automate ports without politics interfering: http://www.hafen-hamburg.de/de/presse/news/neue-containerbruecken-fuer-den-container-terminal-burchardkai/

-

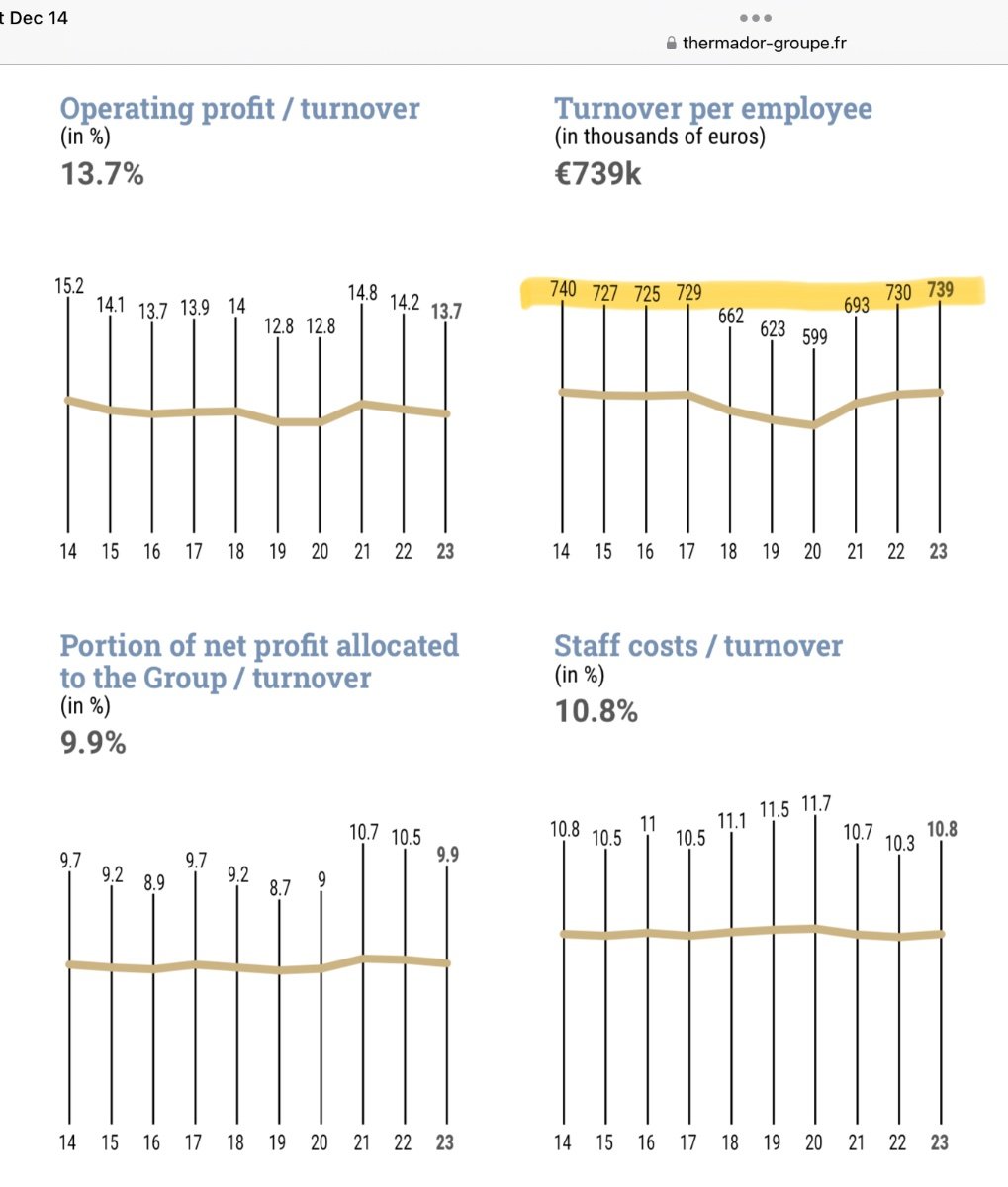

To @Dalal.Holdings point, some metrics in annual reports are really awful. For example, I look at Thermador - a French building distributor and not a bad business at all. However, they clearly have a productivity issue.

-

Just my guess, but they do as they are told. They probably have a Russian commander who doesn’t give a damn and spends them as he sees fit. He probably got the message from above that he has more supplies for the meatgrinder coming if the current batch is gone.

-

Imagine getting red 10 times in row at the roulette wheel. Is it bad luck or is the wheel rigged?

-

High Line Trail (if you are into walking with a lot of stops at restaurants, coffee shops along the way) Do a mini cruise around Manhattan (starts at the Hudson River - a couple locations there) Koreatown (great and cheap food) NYC Diamond district. Bryant Park (between Korea town and Diamond district) 9/11 Memorial

-

North Korean attack. Reminds me of WW2 footage from the eastern front: No vehicles , no artillery support (as far as I can tell), no camouflage even, open field…

-

@John Hjorth …and that’s how DOGE will go (imo).

-

Fighting two wars is getting expensive: https://www.reuters.com/world/middle-east/israel-budget-deficit-dips-79gdp-oct-despite-higher-war-expenses-2024-11-11/#:~:text=The ministry said that despite,first 10 months of 2024.

-

For comparison, Germany‘s stock Market valuation is ~2.6T if my math is correct.

-

So $DOW, a company which makes a lot off stuff that everyone uses is worth $29B or EV/S~1 while Broadcom tacks on $250B in market cap because they announced they make AI chips. $DOW chart looks like this and $AVGO looks like that. What to make of it, I have no idea, but it doesn’t look right.

-

Thx, it’s good to hear accounts like this. I see the Doctors who volunteer their time often under perilous circumstance as modern day saints as well. I actually had concerns about DwB last year, due the the same thinking that @Dinar explained and especially because pushed the aid in Palestine so hard in their Fundraising, but then thought better of it. The world is not a black and white place and while it’s true that some of those victims that get help may not be our friend or maybe even enemies there generally a whole lot more victims and participants in any war. What DwB does simply to enable Doctors who volunteer their time to fulfill the Hippocrates oath in situations where people need it most and that’s good enough for me.

-

I wonder about the math to 9% FCF with CP in 2028, way above consensus. Raising prices above inflation won’t work forever either. I think self driving trucks will be a thing and quite deflationary on Transportation costs and that will affect RR’s too. FCF yield for most RR’s seems to be below 4% which seems rich.

-

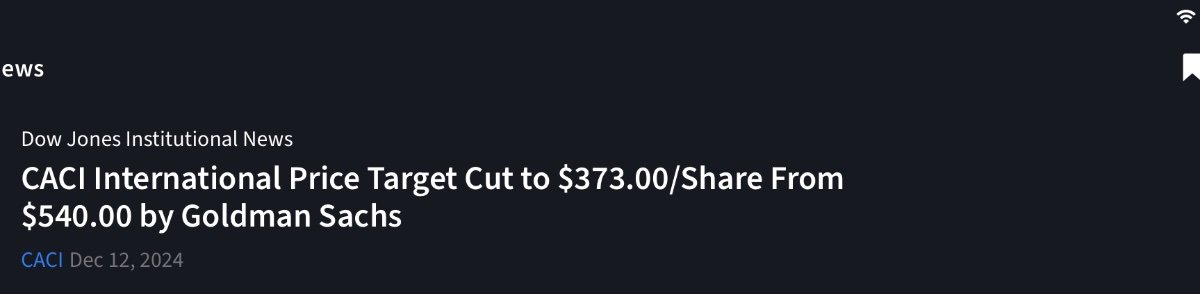

Always curious how these downgrades work. Seems to be based more based on pure momentum than anything else. This time $CACI:

-

Will be fun to get a margins call at 3AM in the morning. Or will they just liquidate? Imagine, you go to bed with a margined portfolio and wake up with some margin debt due to overnite trading gyrations.

-

I have been donating to Doctors Without Borders for years and continue to do so. I think you get a lot of bang for the buck because most Doctors volunteer their time there. They tend to go where it’s most needed. I also agree going local. I used to donate to the (then local to me food bank) because I knew someone working there but I moved around a lot. So ai no longer have that connection. I think going either far (Doctor without Borders) or going local makes the most sense.

-

Thats relevant for MSGS, not MSGE though, isn’t it?

-

Quantum computer are really good at solving a few mathematical problems. They are awful at general computing. The google quantum computer solved a problem with no real application, just to show off theoretical capabilities. Any real application is at least 10 years out.

-

Health insurers look very juicy to me . I just added a bit more ELV today.

-

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

Spekulatius replied to tnathan's topic in General Discussion

Just a year or two ago, they were stating they were making acquisition at 10-11x and that was before synergies, I think. However that applied to smaller acquisition than this monster here. I do think the BRO edge was their ability to make many plankton size acquisition at lower multiples, similar to what CSU does in software. Eventually as the whale becomes bigger, living off plankton becomes harder and AJG at least starts to go bigger in the food chain. -

Ashtead moving their listing to the US: https://finance.yahoo.com/news/ashtead-move-primary-listing-us-075934041.html I think we will see the day when BP moves to the US as well. Will be quite the day when British Petroleum becomes US Petroleum. They can toss the energy transition crap at the same time. Get rid of corporate deadwood by not making them a good offer to move. Very convenient.

-

What is interesting is how quickly these regimes disintegrate once the dominos start to fall. Syria is no exception - there was Alysia under Ghadaffi , Ceausescu in Romania, the Sha in Iran. Same could happen with Putin and Russia. There are only handful people at the top and once the head of the snake is severed, the rest just disintegrates.

-

I Need a Laugh. Tell me a Joke. Keep em PC.

Spekulatius replied to doughishere's topic in General Discussion

-

Turkey backs the rebels though. I think it’s in the West and Turkey‘s interests to kick the Russians out there. It‘s also in the rebels interests to kick the Russians out there and prevent them from getting foothold hold again, if I were in their shoes. Who knows who is going to gain power and what their interests are and decisions will be.

-

Why do you think Russia will keep their naval base?