giulio

-

Posts

298 -

Joined

-

Last visited

-

Days Won

2

Content Type

Profiles

Forums

Events

Everything posted by giulio

-

I am not sure about USD vs CAD conversion, still crazy to me.

-

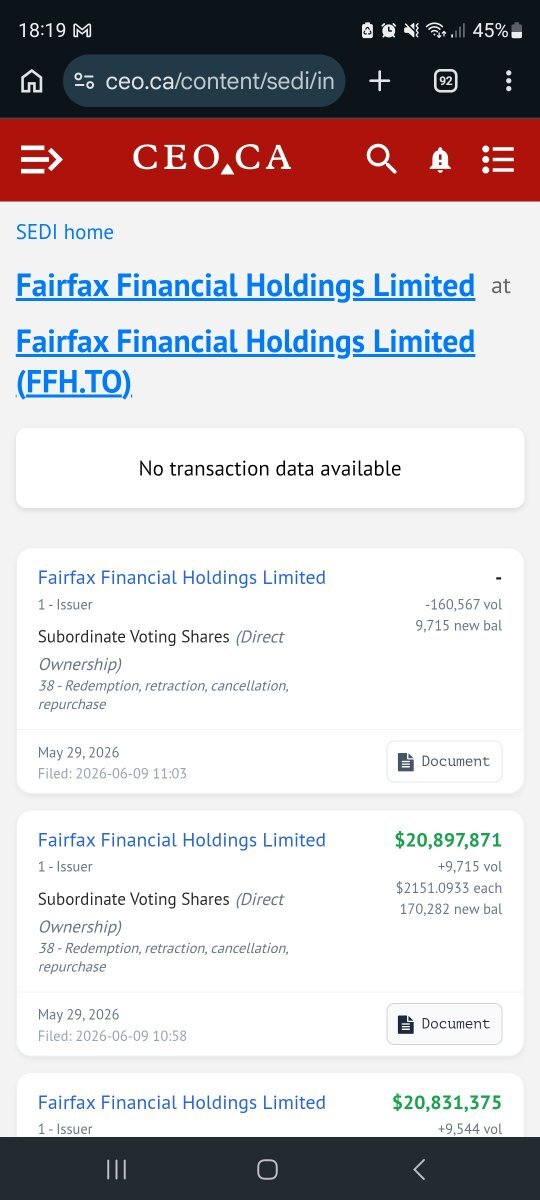

https://ceo.ca/content/sedi/issuers/2458 FFH did a 1B tender offer in 2022, financed by selling 10% of Odyssey. Another 1B bought back in 1 day in 2026 under their NCIB. Crazy.

-

I bought Panthera Resources (PAT - LSE), <1% position, essentially a lottery ticket on the results of their litigation process against India. $70M mkt cap, litigation claim is $1.6B but it will updated since gold price is ~25% higher now than when they filed initially. From what I read, they should have a strong legal basis. They are backed and fully funded by LCM (litigation capital management) who are highly selective in the cases they agree to support and have a good track record. Final hearing in Jan 2027, expected outcome announced by end of 2027. Wish me luck!

-

170k bought back, 160k cancelled

-

If you write an email to Watsa to complain about the Micron sale, don't forget to cc Li Lu!

-

You were absolutely spot on. I used fih 30.4% stake and 15crore (after tax as reported in the article I linked). 43.6% is held by Anchorage, I assumed they got the rest. I am looking forward to know how they financed the increased stake in IIFL capital...

-

https://economictimes.indiatimes.com/industry/transportation/airlines-/-aviation/bengaluru-airport-operator-bial-hands-over-rs-16-crore-dividend-to-karnataka-govt-arm/articleshow/131309196.cms?from=mdr BIAL paid a dividend of Rs3 per share. FIH share should be $3.6M.

-

https://www.hindustantimes.com/india-news/centre-looks-to-revive-stalled-idbi-bank-sale-process-report-101779091726437-amp.html Efforts are underway to make a deal feasible, including setting a price that captures the bank’s intrinsic value and lowers the reliance on its share price, the people said

-

Small adds to stvn, tdg and fih

-

I hope the image is readable. Just wanted to highlight that CR for FFH has been in very good shape since at least 2013 (I don't track earlier years), with the exception of 2017 (big acquisition). What many cite is that since 2020 BOTH underwriting profits and investment gains have been performing pretty well. @Viking maybe rates stay around where they are? + or - 50bps? It's also a possibility...ECB is about to raise rate apparently!

-

2.5% position in TDG, starter, hoping results tomorrow don't move the price too much on the upside (TDG pre announce in april)

-

Director Lauren Templeton speaking at Guy Spier's events during Brk weekend. starts at 5.05.00

-

As far as I am concerned, all your points are valid and well articulated. I am sure other posters find them useful as well: this is a discussion forum and if we all agreed with each other it wouldn't be fun and the learning opportunities would be far less. If FIH is a big position for you, you should definitely attend the AGM and voice your concerns, just don't go there with the expectation to hear the answers YOU want. I understand your frustration but there's not much the COBF can do, just sell it and be "psychologically short" a la Ackman. FWIW, I sized the position taking into account positives and the negatives and I am not in love with the stock: if the upside materializes great (I might trim it, keep it at 5% and redeploy proceeds elsewhere), if not I'll just sell and move on without losing money and a second of sleep. 3 years ago I bought VW and Porsche Holding thinking there was 4x upside, limited downside thanks big cash balances and a family willing to surface value through buybacks, spinoffs, costs cuts and dividends. I lost 50% but the position was sized appropriately and didn't impact returns too much. I took the loss, learned my lessons and bought other stuff. I encourage you to keep posting your analysis and discuss ideas. Just keep a joyful and playful attitude, we are blessed to be able to do this! Best, G

-

FIH put $300M in Sanmar in 2016 through bonds at 13%. they were redeemed for 434M in 2019. FIH then reinvested 217M and finally sold their stake for 27M. The loss is ~60M overall. Terrible investment, big opportunity costs but less bad than it might seem. My guess is Sanmar would have required additional liquidity (as reported in AR 2025) and equity injections due to their debt level. Their raw materials costs possibly spiked up given the Iran war and higher oil prices. IMO, FIH did well in taking the L and moving on. You can't get them all right!

-

https://www.fairfaxindia.ca/press-releases/fairfax-india-announces-sale-of-equity-interest-in-sanmar-chemical-enterprises-limited-2026-04-09/

-

I have written my thoughts in a previous post and on twitter If they double pax, I see a path to $1B in EBITDA. That should happen by 2029. They aim to 90M pax capacity by 2033. Shouldn't this be worth 15-20B? I don't know what will happen to the INR relative to the $ though

-

I can only speculate on why is down this much, all reasons have nothing to do with business performance -> 1) some investors think Bollore will sell down a big block if french court forces him to buy vivendi, 2) UMG shelved its us listing plans, possibly leading to investors selling as there's "no near term catalyst", 3) AI fears, 4) UMG did not announce a buyback, some think mgmt is bad at capital allocation. Here is a recent letter by the CEO of Warner Music which describes the opportunity better than me! https://www.wmg.com/news/a-letter-to-our-shareholders Based on their CMD guidance, I think UMG can grow revenue at 8% (9-10% including M&A) and EBITDA at 12-13% over the next 5 years. So far you had only subscribers growth. Starting from this year, thanks to new contracts with DSPs, you'll see the benefit of price increases (irrespective of whether DSPs decide to raise prices) on top of subs growth. There are many additional nuances, but that's the thesis in a nutshell!

-

I keep adding to stvn around 15 and umg below 18.

-

I am halfway through this and find the discussion interesting and relevant to ffh (now and in the future). Not the usual Gayner interview, the questions are more specific and tackle all the insurance aspects many of us discuss on here. Best, G

-

adding to UMG and STVN

-

around march 7th iirc

-

@Marco Van Basten @Hamburg Investor look-through earnings exclude investment gains from equities, bonds and derivatives. these are not recurring and dependable, they are at mgmt discretion. The way I take into account the TRS is through a lower share count. the trs position will fluctuate with the share price and at some point get closed, so it should not be included in your estimate of earning power. taking into account ffh's share of its investees earnings (very easy for associates) takes care of the investment gains part. I'll update my calculations when the ar is published. I just wanted to point out that last year, on a look-through basis, eps were already close to ~200$ and while downsides are known, investors should also consider "positive surprises" as mitigants. I think 200$ is conservative given the numerous moving parts. I'll be happy to be wrong if the avg is higher over the next 5 years!

-

Interesting that most are discussing future returns expectations but only a few here are focusing on what actually matters, i.e. the per share earning power of the business and relative IV. I certainly have no idea where interest rates will be in the future or what returns to expect from ffh equity portfolio, or investment gains. What helps me in having a better/complete view is calculating look-through earnings. Last year they were ~190USD per share. These excludes gains from investments and derivates such as TRS. Is this a reasonable expectation going forward? YES. On average, over the next 5 years I expect ffh to earn ~200USD per share. The possible downsides are pretty clear to all: higher CR, slower growth or reduced NPW, lower yield on FI, lower returns from equities. Here are the factors that may help mitigate these risks: less premiums ceded, minorities buyback, longer FI duration, shift from gov to corporate bonds, higher income from consolidated companies, reinvestment of earnings, lower shares count. Not everything that matters can be counted and not everything that can be counted matters. Still, starting from last year 190, I am pretty sure that 1) buying back minorities can add 20USD per share, 2) consolidated operations might add another 20, 3) s/o will be lower, closer to 18M if I have to guess. What's a fair multiple? Certainly not 8x. 13x or 15x? That means today IV is 2600-3000USD. You can then triangulate this estimate with other methodologies, P/B, float + equity? Hard for me to see a value lower than 3000. You cannot know exactly what bonds will yield or what realized gains will be. You know the company culture, investment framework and horizon. Make your bets accordingly. Best, G

-

there's inpractise in the UK. https://inpractise.com/. I did not consult with them but I know the platform and applied for a job. they do transcript as well, everything is anonymous.