glider3834

-

Posts

1,019 -

Joined

-

Last visited

-

Days Won

4

Content Type

Profiles

Forums

Events

Everything posted by glider3834

-

strange - looks like CEO has left & replaced by COO- will have to wait & see the reasons - usually not a good sign but I don't think its related to their operating performance - posted record quarterly result in Dec-21 qtr in terms of revenues, EBITDA,PBT https://www.quesscorp.com/investor/dist/images/pdf/Announcements/Press-Release-Q3FY22.pdf

-

https://www.businessdaily.gr/agores/57633_eurobank-systasi-agoras-tis-metohis-apo-ti-13d-research-strategy actually I think they meant to say 2022 ROTE 10% - which is where Eurobank mgmt were guiding last quarter. as reported by HSBC, "the share price of Eurobank has doubled on an annual basis and has 0.59x P / TBV and is close to the highs of the last five years. However, the valuation still does not reflect the strong 10% increase in the 2022 ROTE and the possibility of starting a dividend in 2023 . Although the bank is very similar to its EU counterparts in terms of capital and profitability, its valuation still has a discount of about 20% on P / TBV and about 40% on a P / E basis."Eurobank's valuation premium against its Greek competitors has recently widened, but we believe it was worth it, given its superior profitability and the possibility of distributing dividends."

-

good summary Viking I estimate increase in fair/market value for Exco could be around 40% for 2021. Chou Associates Funds is carrying their Exco stake at $13.41 mil at 31 Dec-20 (actual reported) $17.3 mil at 31 Aug-21 (my estimate based on Exco position 8.7% & fund NAV 198.8 mil) $18.76 mil at 31 Dec-21 (my estimate based on Exco position 11.4% & fund NAV $164.6 mil) http://choufunds.com/pdf/Asso 2021 Q4 Holdings.pdf Assuming Chou Funds didn't change their shareholding during 2021, the increase in fair value is 40% Now its likely that Fairfax has already reflected most of this Exco increase in fair value in their 3Q 2021 report (Excess of FV over CV for non-insurance subs number). There was no breakdown for Exco in 3Q in there so its hard to be certain.

-

but is the valuation better?

-

I think Fairfax's focus is more about protecting the balance sheet, rather than 'timing' an increase in interest rates. But higher cash/ST investment weighting gives them optionality to take advantage of higher rates.

-

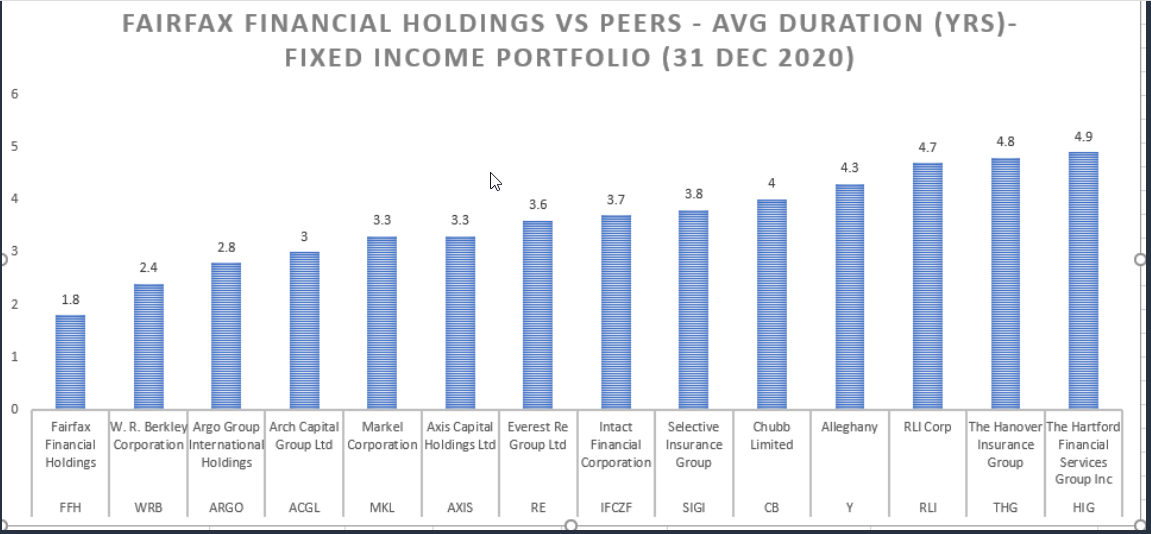

great summary Viking - not much to add Just on those equity swaps - their avg cost I believe is US$373 - so likely sitting on a US$215 mil gain Looking forward, I am curious if they made any additions with the recent market sell off. Fairfax is certainly better positioned than most of their peers to take advantage of higher interest rates, with shorter duration on their fixed income portfolio - I actually did a chart & posted on twitter but re-posting it below ( source Company Annual Reports 2020)

-

Another sub selldown and SIB would also likely increase existing TRS swap position value.

-

BB can't redeem converts before maturity - it does put BB in a stronger cash position but i think analyst expectation was closer to $1 bil rather than $600 mil - on the flipside they got deal done

-

Interesting for 4Q - WRB had Insurance CR 88.1 4Q (vs 89.9 2Q) and Reinsurance/Monoline excess CR 88.4 4Q (vs 88.6 2Q) That suggests to me that potentially Fairfax's underwriting profit could be closer to 2Q result which was a record & in the 94-95 area. I am just adding a proviso here that they are doing their annual reserve reviews so that could have an impact. But overall it does look positive for Fairfax IMO.

-

Probably the best interview I have seen with Kamesh CEO Digit (tip: you will need to turn the volume right up)

-

I think that tech to value rotation to defensive financials is also definitely benefiting FFH, BRK etc - investors now focusing on profit over hype - check out ARKK down a further 5% today

-

+1

-

10 year treasury continues march up to 1.76% today - i think we will be over 2% this year - another catalyst for Fairfax with 44% of Fairfax portfolio in cash and short term invest that they are waiting to deploy to higher yielding fixed income opportunities which could be not too far around the corner

-

I received positive result yesterday for my partner & I but we have had symptoms sore throat, headaches, fatigue for a few days now. Starting to improve a bit & we need to isolate for 6 more days. It feels like the flu. We have both had Pfizer vaccine (2 doses) but not the booster - we were actually due this week!

-

Yep Prem nailed it

-

We don't have all details here but why couldn't it be similar to Brit - issue a new class of common stock? With Brit, it looks like OMERS has the A shares & Fairfax has the B shares & the A shares have certain priority in respect of dividends On IFRS impact https://ifrscommunity.com/knowledge-base/ifrs-10-consolidated-financial-statements/ Changes in a parent’s ownership interest in a subsidiary that do not result in the parent losing control of the subsidiary are equity transactions So I think we could see a potential BV gain here (see my earlier post suggesting potential accounting impact) to reflect the excess of $900 mil cash proceeds over carrying cost of 9.99% interest in Odyssey Again this is just my hunch, could be wrong but we will find out for sure next month

-

https://www.fairfax.ca/news/press-releases/press-release-details/2022/Fairfax-Declares-Annual-Dividend/default.aspx

-

Yes agree viking - along with earnings/BV growth points 1-3, i think likely we will see a multiple re-rating in 2022 on Fairfax shares ie P/BV x 1 or higher. Fairfax remains my largest equity position.

-

https://m.timesofindia.com/business/india-business/digit-first-unicorn-of-2021-in-top-10-non-life-insurers/articleshow/88600245.cms

-

yes I think over US$1000 is achievable- if we use BV Sep-21 of US$562 - I think over 5 years a BV growth rate could be around 12% p.a & P/BV multiple could expand to 1.1x to 1.2x (mid-point 1.15x BV) - which would give a PT of US$1,139 in 5 years. This would be compounded share price return of just over 18% p.a, based on current share price of US$490.

-

What valuation is too high to buy a great compounder?

glider3834 replied to tnathan's topic in General Discussion

I think extremely low interest rates have fueled some very high PE multiples & I think we are moving to higher rates of 2% plus next year & so I think we all need to be careful. But I am generalising with above comments, if you find a company selling for 30x earnings & you have done your research & you are extremely confident it can continue powering away at 30% per annum earnings growth for the next 5 years then sure 30x earnings is reasonable. And if you can get the same company at 20-25x PE then you will do even better. -

What valuation is too high to buy a great compounder?

glider3834 replied to tnathan's topic in General Discussion

I think the trick is to pick up a great compounder at a reasonable multiple- MSFT, AAPL have all had periods where they sold at or below 15x earnings & so you get both multiple expansion plus earnings growth plus downside protection. When you pay 30-40x earnings then you can't afford for anything to go wrong - BABA is a classic example - it looked like a great compounder when the PE was in the 40s from 2016-2018 & now shares are trading well below avg 2018 levels, because you have had multiple compression! -

I'm not sure viking - maybe you could use Fairfax India buyback payment time as a reference - not sure if Xmas period might slow things down

-

+1

-

Yes could be true - also I think possibly there was an expectation that the SIB would be undersubscribed due to tax implications, and so the fact it was modestly oversubscribed took the market by surprise. Also maybe a signalling aspect that Fairfax is prepared to repurchase shares at a premium to current share price, indicating they see undervaluation. Would be great to see Fairfax have another go at this in 2022 if this discount is still there. Those swaps are looking good too.