glider3834

-

Posts

1,082 -

Joined

-

Last visited

-

Days Won

5

Content Type

Profiles

Forums

Events

Everything posted by glider3834

-

Bangalore International Airport - May-22 passenger traffic now at 85% of May-19 levels https://www.aai.aero/en/business-opportunities/aai-traffic-news

-

Odyssey paid $900 mil div to Holdco in 2021 after the 10% sale transaction, but only had a $362 mil div capacity at end of 2020 - so I think that div capacity number potentially can change

-

no worries SJ these business units sit inside C&F's Accident & Health (A&H) division. FFH owns 100% of C&F. The full details of transaction are not available yet but assuming proceeds went to C&F then I guess subject to meeting regs around divs & capital requirements, potentially they could dividend to holdco.

-

this is interesting - looks like Fairfax is selling its pet insurance business for $1.4 bil WASHINGTON and TORONTO, June 20, 2022 (GLOBE NEWSWIRE) -- JAB Holding Company (“JAB”) and Fairfax Financial Holdings Limited (“Fairfax”) (TSX: FFH and FFH.U) today announced a transformational strategic partnership, in which JAB’s pet insurance business has agreed to acquire all of Fairfax’s interests in the Crum & Forster Pet Insurance Group™ (“C&F Pet”) and Pethealth Inc., including all of their worldwide operations. As part of the transaction, Fairfax will also make a $200 million1 investment in JCP V, JAB’s latest consumer fund. As a result of the transaction, in which Fairfax will receive $1.4 billion in the form of $1.15 billion cash and $250 million in seller notes, JAB’s combined global pet insurance and ecosystem platform will be estimated to have gross written premiums and pet health services revenues of well over $1.2 billion by 2023, insuring more than 2.1 million pets. https://www.kulr8.com/news/money/jab-s-pet-insurance-business-to-acquire-global-pet-insurance-operations-of-fairfax-financial/article_1a5ce79b-9f63-598e-bc0a-16401efb451c.html I can't get behind the Bloomberg paywall but here is another article https://www.bloomberg.com/news/articles/2022-06-20/jab-is-said-to-buy-fairfax-stakes-in-pethealth-crum-forster

-

https://www.hindustantimes.com/cities/bengaluru-news/bengaluru-airport-recognised-as-best-in-india-south-asia-101655461485551.html

-

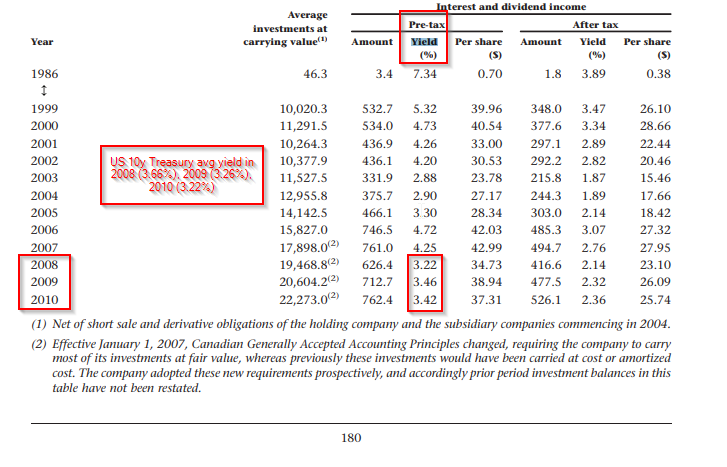

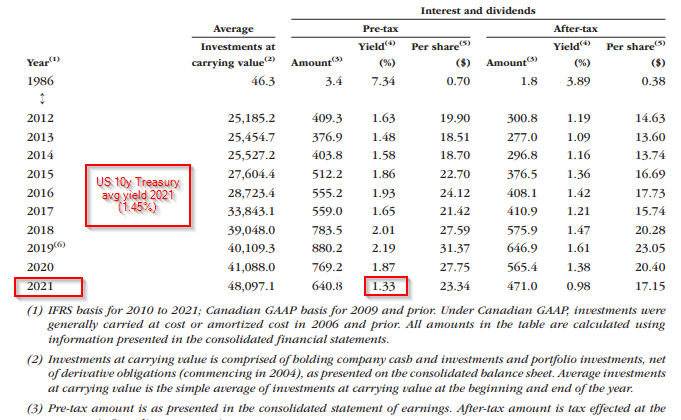

guys I decided to delete my post re interest & dividend income (pre-tax yield) forecast to wait for more clarity on how Fairfax develop their fixed income portfolio positioning. From a pre-tax yield perspective - twin drivers of higher treasury rates and higher credit spreads are both positive drivers going forward. But to model what the new pre-tax yield will look like, we need to see in particular how their fixed income positioning develops - in particular end of 2021 they had roughly 50% cash & ST maturities and 20% bonds mix. So if we assume corp bonds, mortgages etc become more attractive & they move to a 25% cash & ST maturities & 45% bond mix for example, that could have a big positive impact on pre-tax yield.

-

https://www.newindianexpress.com/cities/bengaluru/2022/jun/16/wait-is-over-modi-to-inauguratekempegowda-international-airport-terminal-2-in-october-2466118.html date to be confirmed but looks like October opening for T2 aka the 'garden terminal'

-

Yes really good point - US BBB Corporate effective yields have increased around 300bp from low 2% area in 2021 to low 5% area today- Fairfax in 2008 & 2009 had a 40-50% ish allocation to bonds & currently they are sitting around half of that level. QT has just started & there is potential for this to pressure credit spreads further.

-

Twocities yes agree they have been investing at shorter end of the curve - i just picked the US10y to show how it has tended to sit close to ffh pre-tax yield over time

-

Yes how high will interest rates go is the big question - at what point do rates start to cause problems in economy the big assumption with the above we have treasury rates (10y) sitting in 3% area - but is that sustainable, will the Fed be forced to reverse course at some point & could it come back down in a recession ???

-

@Viking yes agree - credit risk already starting to spike - should create more investment opportunities in corporates down the track https://chicagotoday.news/world-nation/us-credit-risk-spikes-to-may-2020-high/ Here is a sobering quote from this article Monetary policy tightening has been largely responsible for a nearly 14% total return loss for the Bloomberg US Investment Grade Index this year. 14% total return loss in US investment grade - unbelievable!

-

thanks @ourkid8 for finding this - a small buyback under the NCIB https://www.sedi.ca/sedi/SVTItdOneLineDetailDerivRemarkIss?locale=en_CA

-

viking I just wonder if FIH would be able to spin off its publicly listed holdings into an actively managed exchange traded fund (ETF) - which should trade closer to NAV - units could be issued to current FIH shareholders - & then retain the private/unlisted investments in FIH as a separate company? One issue could be debt - they may not be able to leverage their investments - but then is the leverage actually worth the cost in terms of the current deep discount to BV.

-

two interesting comments from PW - privatisation of railway stations & possible logistics opportunities with Fedex Read more at: https://economictimes.indiatimes.com/news/india/modi-has-made-india-business-friendly-prem-watsa-chairman-fairfax-financial-holdings/articleshow/92027160.cms?utm_source=contentofinterest&utm_medium=text&utm_campaign=cppst

-

thanks Viking one positive potentially could be Exco Resources - natural gas prices have doubled YTD to over $8MMBtu & their hedges roll off this year.

-

https://www.thehindubusinessline.com/money-and-banking/prem-watsas-fairfax-shows-interest-in-idbi-bank/article65496966.ece

-

Lets hope they manage their assets through shipping cycle effectively, take advantage of market conditions & don't fall into the position of having to scrap vessels - they are currently selling older 2nd hand vessels with charters attached - lets see how they go

-

also saw this https://news.ambest.com/presscontent.aspx?refnum=32073&altsrc=2

-

icumd just on the question of passenger volumes, I am curious what BIAL's actual passenger numbers could look like. What I mean is that BIAL's designed capacity historically speaking has been exceeded by actual passenger numbers. Again I am not making a prediction whether this can happen in the future, but lets consider some historical data. Existing Terminal 1 was designed to handle to around 20 mil passengers p.a, but using digital technology BIAL made improvements within the existing Terminal 1 to increase its capacity up to around 36 mil passengers p.a (for example they handled 32 mil PAX in 2018 & 34 mil PAX in 2019). Thanks to numerous technology measures adopted, the passenger handling capacity of Terminal 1 (T1) has zoomed. “It was initially built to handle 20 million passenger per annum (MPPA), and it is now capable of handling 36 MPPA and 90 air transport movements (ATMs) per hour. Credit goes to smart digital like Digi Yatra, Smart Security System and Contactless Self-Baggage Drop,” the spokesperson said. This would take care of growth in traffic for the next 12 months, she added. https://www.newindianexpress.com/cities/bengaluru/2022/apr/27/kia-terminal-2-will-open-byyear-end-bial-2446897.html#:~:text=March 2021 was pushed to,well as shortage of manpower. On Terminal 2 1st phase expected to increase annual capacity by 25 mil (expected completion date October 2022?) 2nd phase expected to increase annual capacity by 20 mil (expected completion date fiscal year 2029) 'The combined capacity of the existing terminal and Terminal 2 will be approximately 73 million passengers per annum.' (Fairfax India 2021 AR) This comment from Fairfax India's annual report implies that Terminal 1 has capacity of 28 mil, but in actual fact it can handle up to 36 mil ( see above). Does this mean that Fairfax is planning to reduce services in Terminal 1 after they complete 1st phase of Terminal 2, to effectively reduce its capacity back to 28 mil? Or is it possible that Fairfax's planned capacity number for the end of 2022 of around 53 mil (for Terminal 1 & Terminal 2 - 1st phase) will actually understate the actual passenger numbers they will be able to handle, perhaps using digital technology? On this front, BIAL recently announced a joint undertaking with AWS to continue this digital tech push https://economictimes.indiatimes.com/tech/technology/bangalore-international-airport-aws-to-open-joint-innovation-center/articleshow/90684488.cms Again not making predictions here, but historically speaking BIAL has been able to use digital tech to increase actual passenger traffic numbers beyond the terminal's designed capacity. So then the question is can BIAL exceed the planned airport capacity in future years? Any thoughts?

-

https://www.traveldailymedia.com/india-travel-business-back-to-2019-levels/ From booking.com The portal’s India business is back at 2019 levels, and is already “moving in the right direction towards normalcy. the company’s April 2022 bookings are already better than April 2019 levels, Commercial Director for APAC, China & Oceania, Ritu Mehrotra said. According to Mehrotra, “India is already a percentage point higher”, with domestic travel picking up and international travel starting to pick up. Business travel, incidentally, is also “creeping back”.

-

I put this chart together - sourced data from Airports Authority of India BIAL passenger numbers continue to recover - running at 82% of 2019 level in April (versus 41% of 2019 level in January)

-

it usually takes time to get approvals in India, Generali recently received regulatory approval to increase its stake to 74% in its Indian non-life insurance JV 06 MAY 2022 - 17:49 Milan - Generali completed the acquisition from Future Enterprises Limited of 25% of the shares of Future Generali India Insurance (FGII) and will now hold a stake of around 74% in FGII. Generali received the approval from the relevant regulatory and competition authorities. https://www.generali.com/media/press-releases/all/2022/Generali-completes-the-transaction-to-become-the-majority-shareholder-in-its-Indian-P-and-C-insurance-joint-venture

-

https://www.reuters.com/markets/stocks/eurobank-grows-first-quarter-profit-lower-bad-debt-provisions-2022-05-25 Eurobank core income (net interest plus fees & commissions)exceeded estimates - they are sticking with their goal of 10% ROE this year & dividend distribution from 2022 profit. https://www.eurobankholdings.gr/-/media/holding/omilos/grafeio-tupou/etairikes-anakoinoseis/2022/1q-2022/1q2022-results-pr-en.pdf

-

it looks like article from Reuters & they didn't receive any comment from Digit or Fairfax - if they did their DD & cross checked Fairfax's filings, then they would have realised 30% number is not correct. I guess we need to wait to Sep to see what happens but I think it would be great if they can execute an IPO although I think they should wait until markets settle a bit more.

-

Francis Chou recently talking about Wintaai & his portfolio moves - worth having a listen