glider3834

-

Posts

1,082 -

Joined

-

Last visited

-

Days Won

5

Content Type

Profiles

Forums

Events

Everything posted by glider3834

-

Digit is a high growth digital insurer with a sustainable business model (profitable on IFRS basis in year 3) - I wouldn't put Lemonade or Root in that category IMO - they are are losing bucketloads of money ,operating in very competitive, mature markets & have narrow product offerings. Look with Digit on valuation - gut instinct probably bit lower but not a drawdown of the size you have indicated. We may never find out for certain because Digit have indicated they don't need to raise capital now & also that they are better capitalised than a lot of their insurer competitors (which actually gives them a competitive advantage). Its worth noting too that Digit have increased their market share by around 25% from 1.6% (mar-21) to 2% (Jan-22) of non-life market so the underlying IV has grown since the time of July capital raise to current IMO I think this article probably makes some good points on your question https://www.insurancebusinessmag.com/us/news/technology/ceo-turns-back-to-private-markets-after-reverse-merger-derailment-324535.aspx “Now that the public markets are depressed, it’s causing valuations in the private market to be a little bit lower, but not quite as extreme, right?” In other words, the private markets continue to have an appetite for private technology investments, though they’re slightly more sober about it. “There’s still a lot of [venture capital] appetite,” Harper said.

-

looking at the 13F - no major changes among Fairfax's largest equity positions in Q4 from what I can see https://www.dataroma.com/m/holdings.php?m=FFH

-

Just on Ukraine - if Russia does invade there is real risk of asset seizures (which happened in Crimea) & this would impact Fairfax but not in a material way from what I can see. I genuinely hope the situation can get resolved peacefully obviously it would be terrible for the Ukrainian people. For Fairfax I see these assets at risk - Astarta - has large Ukrainian agri-industrial business - 28% ownership - Fairfax carrying value $65 mil Fairfax Ukraine - 70% ownership - shareholder equity 2020 $90 mil (GWP $144 mil) In terms of insurance liability exposure I would expect they would have the standard war exclusion clauses so not expecting issues on liability side but more the assets at risk - I don't know what assets Fairfax Ukraine has & whether they can be moved to friendlier territories. I am sure Fairfax has been making contingency plans either way.

-

correction - its US$160 so would be 30% of current share price

-

Talking about the narrative on Fairfax changing... WATSA’S STILL GOT IT Prem Watsa’s investing acumen powered Fairfax Financial in its latest quarter. While profit almost doubled in the company’s core property and casualty insurance and reinsurance operations, it was the US$938-million gain on investments that accounted for the lion’s share of earnings in the fourth quarter. For the year, investing gains surged to US$3.45 billion. We’ll keep an ear on what Watsa tells analysts in a conference call this morning. https://www.bnnbloomberg.ca/the-daily-chase-blockade-hammers-auto-sector-prem-watsa-flexes-investing-smarts-1.1721969 Also SA fixed the earnings release revenue number

-

Without looking at their numbers, Kamesh Goyal was interviewed recently & said they became profitable on an IFRS basis by the end of their 3rd year in operation.

-

It starts to get nuts when you start putting valuation on the remaining 90% interest If 10% sale resulted in $429 mil realised capital gain - a sale of remaining 90% (9 x $425 mil) could yield a further realised gain (over book value) of $3.825 bil - divide that by 23.9 mil shares & you get $160 per share which is 25% of Fairfax's market cap that is not reflected in Fairfax's book value. Even if you take a conservative view & dial that number down - or because its OMERS or whatever - it is still going to be significant number & that is just Odyssey - what about the other insurers that Fairfax owns?? If you do a valuation of Fairfax based on float per common share you start to get a snapshot of that value (maybe theres a chart worth doing there Odyssey had 28% NWP growth for 2021 & had 49.8% NWP growth in Q4! Its growing very fast & it has a very long, stable record of underwriting profitability. That really counts too!

-

yes good point SJ - I just wanted to strip it out so we could compare 2021 & 2020 to see any improvement in underlying CR - but to go back to your point which Prem just made on the conference call they believe their reserving is conservative - so their reported combined ratio probably understates how profitable the underwriting actually is & that is likely to manifest itself in fav develop in future years.

-

2020 CR 97.8 exclude catastrophe loss 4.7 (-) exclude covid loss 4.8 (-) add back net fav develop 3.3 (+) Underlying CR (excl catastrophe, excl covid, excl net fav develop) 91.6 2021 CR 95.0 exclude catastrophe loss 7.2 (-) exclude covid loss 0.3 (-) add back net fav develop 2.2 (+) Underlying CR (excl catastrophe, excl covid, excl net fav develop) 89.7 If we try & estimate 2022 CR Lets assume they continue the trend & reduce underlying CR down to 88.0 from 89.7. Lets assume 0.1 CR covid loss (reduced from 0.3 in 2021), 6.5 CR catastrophe loss (at higher end of range from 4.7(2020) to 7.2 (2021)), net fav development 1.0 (reduced from 2.2 in 2021 to 1.0 in 2022) Then you get estimate CR 93.6 for 2022 & would estimate underwriting profit for 2022 = $1.15 billion (est 18 bil net earned premium x (100-93.6)%) so I would agree with you guys @Parsad & @Viking - I think 93-94 range for CR looks about right for 2022

-

'At December 31, 2021 the company's insurance and reinsurance companies held $24.9 billion in cash and short-dated investments representing 50.3% of portfolio investments' I think they might have reduced their fixed income portfolio duration even more in Q4 39% at 31 Dec-20 44% at 30 Sep-21 50% at 31 Dec-21

-

strange - looks like CEO has left & replaced by COO- will have to wait & see the reasons - usually not a good sign but I don't think its related to their operating performance - posted record quarterly result in Dec-21 qtr in terms of revenues, EBITDA,PBT https://www.quesscorp.com/investor/dist/images/pdf/Announcements/Press-Release-Q3FY22.pdf

-

https://www.businessdaily.gr/agores/57633_eurobank-systasi-agoras-tis-metohis-apo-ti-13d-research-strategy actually I think they meant to say 2022 ROTE 10% - which is where Eurobank mgmt were guiding last quarter. as reported by HSBC, "the share price of Eurobank has doubled on an annual basis and has 0.59x P / TBV and is close to the highs of the last five years. However, the valuation still does not reflect the strong 10% increase in the 2022 ROTE and the possibility of starting a dividend in 2023 . Although the bank is very similar to its EU counterparts in terms of capital and profitability, its valuation still has a discount of about 20% on P / TBV and about 40% on a P / E basis."Eurobank's valuation premium against its Greek competitors has recently widened, but we believe it was worth it, given its superior profitability and the possibility of distributing dividends."

-

good summary Viking I estimate increase in fair/market value for Exco could be around 40% for 2021. Chou Associates Funds is carrying their Exco stake at $13.41 mil at 31 Dec-20 (actual reported) $17.3 mil at 31 Aug-21 (my estimate based on Exco position 8.7% & fund NAV 198.8 mil) $18.76 mil at 31 Dec-21 (my estimate based on Exco position 11.4% & fund NAV $164.6 mil) http://choufunds.com/pdf/Asso 2021 Q4 Holdings.pdf Assuming Chou Funds didn't change their shareholding during 2021, the increase in fair value is 40% Now its likely that Fairfax has already reflected most of this Exco increase in fair value in their 3Q 2021 report (Excess of FV over CV for non-insurance subs number). There was no breakdown for Exco in 3Q in there so its hard to be certain.

-

but is the valuation better?

-

I think Fairfax's focus is more about protecting the balance sheet, rather than 'timing' an increase in interest rates. But higher cash/ST investment weighting gives them optionality to take advantage of higher rates.

-

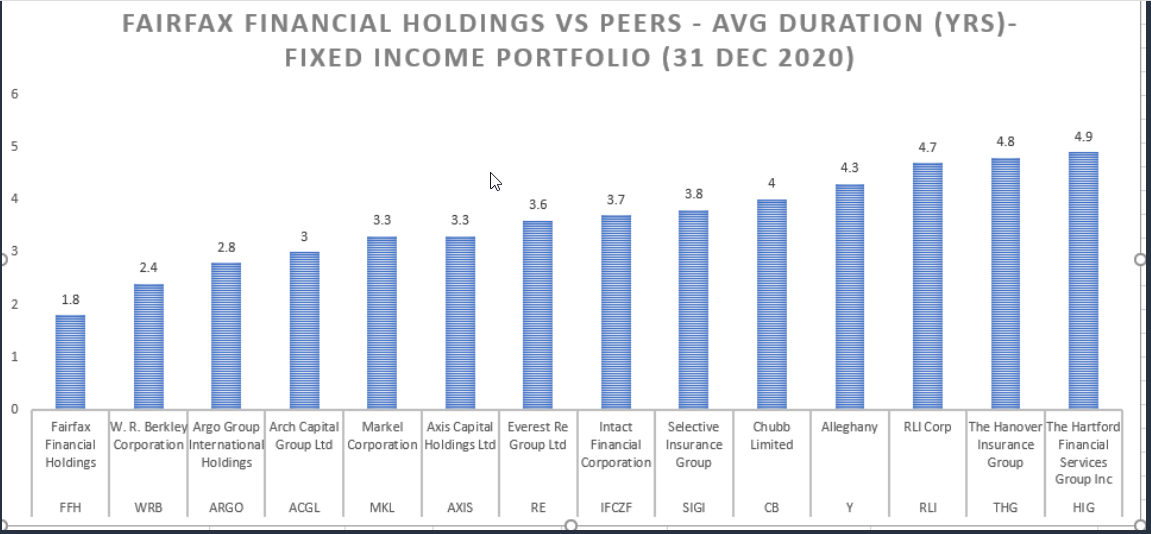

great summary Viking - not much to add Just on those equity swaps - their avg cost I believe is US$373 - so likely sitting on a US$215 mil gain Looking forward, I am curious if they made any additions with the recent market sell off. Fairfax is certainly better positioned than most of their peers to take advantage of higher interest rates, with shorter duration on their fixed income portfolio - I actually did a chart & posted on twitter but re-posting it below ( source Company Annual Reports 2020)

-

Another sub selldown and SIB would also likely increase existing TRS swap position value.

-

BB can't redeem converts before maturity - it does put BB in a stronger cash position but i think analyst expectation was closer to $1 bil rather than $600 mil - on the flipside they got deal done

-

Interesting for 4Q - WRB had Insurance CR 88.1 4Q (vs 89.9 2Q) and Reinsurance/Monoline excess CR 88.4 4Q (vs 88.6 2Q) That suggests to me that potentially Fairfax's underwriting profit could be closer to 2Q result which was a record & in the 94-95 area. I am just adding a proviso here that they are doing their annual reserve reviews so that could have an impact. But overall it does look positive for Fairfax IMO.

-

Probably the best interview I have seen with Kamesh CEO Digit (tip: you will need to turn the volume right up)

-

I think that tech to value rotation to defensive financials is also definitely benefiting FFH, BRK etc - investors now focusing on profit over hype - check out ARKK down a further 5% today

-

+1

-

10 year treasury continues march up to 1.76% today - i think we will be over 2% this year - another catalyst for Fairfax with 44% of Fairfax portfolio in cash and short term invest that they are waiting to deploy to higher yielding fixed income opportunities which could be not too far around the corner

-

I received positive result yesterday for my partner & I but we have had symptoms sore throat, headaches, fatigue for a few days now. Starting to improve a bit & we need to isolate for 6 more days. It feels like the flu. We have both had Pfizer vaccine (2 doses) but not the booster - we were actually due this week!

-

Yep Prem nailed it