glider3834

-

Posts

1,082 -

Joined

-

Last visited

-

Days Won

5

Content Type

Profiles

Forums

Events

Everything posted by glider3834

-

BIAL https://timesofindia.indiatimes.com/business/india-business/domestic-air-travel-in-april-only-5-lower-than-pre-covid-international-traffic-for-indian-carriers-surpasses-pre-covid-levels/articleshow/91459972.cms

-

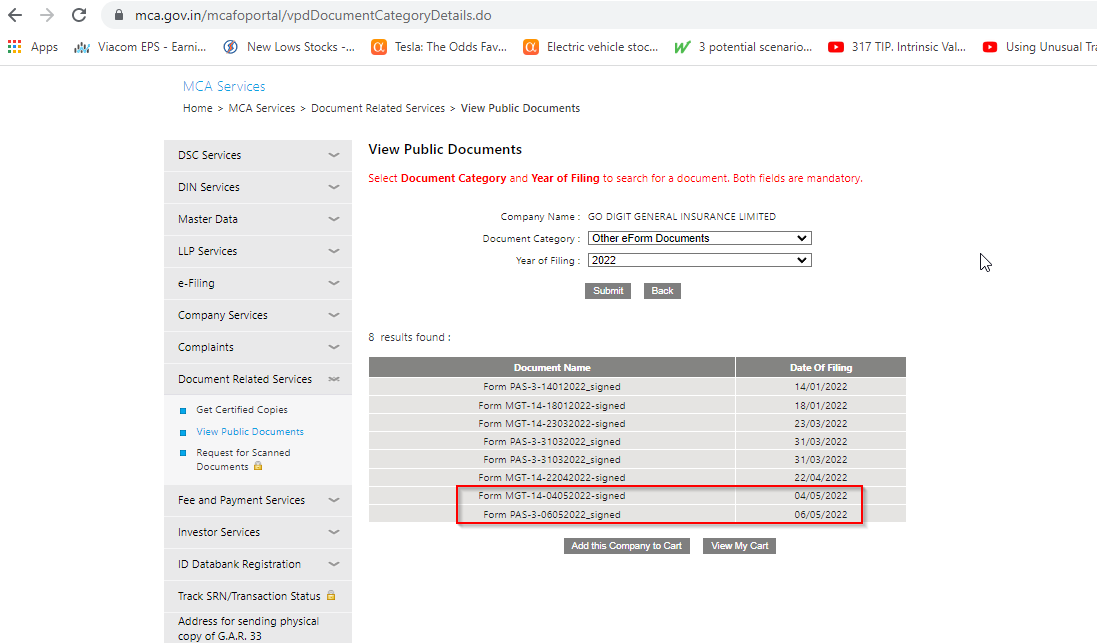

thanks! https://www.mca.gov.in/mcafoportal/vpdDocumentCategoryDetails.do You will need to register to login if you haven't already created one

-

Hey guys , is anyone based in India who can help - I wanted to check details of a potential equity issue for Digit (see PAS-3 form) - lodgement with MCA but you need to pay with Indian bank issued credit card & the cost is 100Rps - I am happy to reimburse the $1.50 or so. I am not based in India so its tricky! Can anyone help? Filings are below

-

yes that was interesting - another interview here I wonder if there would be any value in Fairfax India having a dual listing in India - has this ever been raised before? https://www.moneycontrol.com/news/interview/india-will-be-the-place-to-come-put-money-fairfax-founder-prem-watsa-8473471.html On Digit - looks like they have to wait 5 years before they can IPO - see below Will you be looking at raising more funds for Digit or will you prefer to go for an initial public offering (IPO)? Kamesh Goyal: Since we recently raised $200 million, we do not foresee any need for capital in this financial year. In the long term, we want the company to be listed. But as per IRDAI’s regulations, promoters cannot sell stake before completion of five years. That period will be completed for us in the latter half of 2022. Then we will be prepared, we will be happy to list because that is really the long term objective.

-

https://timesofindia.indiatimes.com/business/india-business/want-good-leadership-dont-care-about-sector/articleshow/91424333.cms

-

viking I just listened to a twitter space from 24/4 which is a good one - hosted by George Noble who used to work with Peter Lynch. Guest speaker Michael Howell (Cross Border Capital) gave an overview of global liquidity flows which he said are pointing to a less liquid environment - he suggested staying long US dollar, sticking to front end of yield curve. That is similar to Fairfax's recent fixed income moves - focusing on US treasuries, liquid & low risk & duration 1-2 yrs. He also said that corporate bond market is at risk as conditions tighten that spreads could push out & again that could be the reason Fairfax are not really pushing harder as yet into corporate bond space.

-

I just emailed Digit to verify this as 3rd party press release - sorry about big writing cant edit on phone

-

https://entrackr.com/2022/05/exclusive-digit-valuation-surpasses-4-bn-in-new-fund-infusion/

-

I think your question is around how industry capital could be impacted from rate rises - Oct-21 article from Fitch on US market might help The commercial insurance market is currently benefiting from profit improvement tied to higher commercial lines pricing, lower pandemic-related losses and outsized investment gains, but questions remain whether pricing and reserving can keep pace in an extended inflationary period. However, information system and financial reporting advances since past inflationary periods provide insurers with faster and more comprehensive information on loss costs that enhances capability to recognize and respond to shifting adverse trends. The industry balance sheet and capital position are also significantly stronger relative to past history. Investment risks are less prominent for P/C insurers versus life insurers as the industry has lower asset leverage (2.2x for p/c industry at YE20 vs. 9.0x for life industry), with less interest rate risk given a lower portfolio duration (estimated at 4.2 years versus over 7 years for the life industry). We estimate that a 300-bp parallel increase in interest rates would lead to a nearly 13% pre-tax decline in p/c bond portfolio market values. However, unrealized gains/losses from interest rate changes are amortized over time and eliminated to the extent that insurers hold bonds to maturity. At YE20, the market value of p/c industry fixed income portfolio was 107% of statutory carrying value tied to the previous extended period of declining interest rates. https://www.fitchratings.com/research/insurance/inflation-rising-rates-fuel-downside-risk-for-us-p-c-insurers-28-10-2021

-

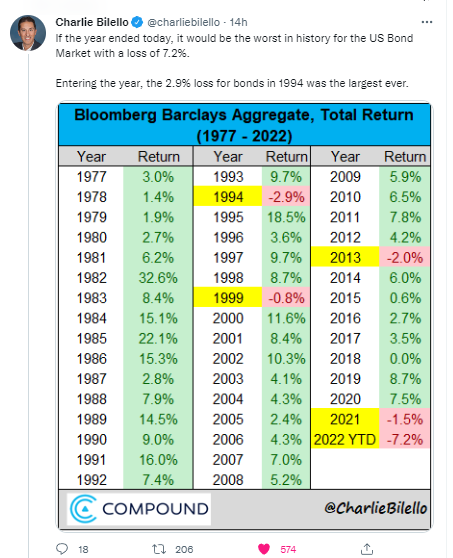

Yeh they made some critical moves in 2021, building up their cash, net sellers of bonds & equities, reducing long equity swap positions. I think the best part of Fairfax's strategy evolution, is that they have taken a leaf out of the Berkshire playbook, that the way to deal with an unattractive equity & bond investment environment is to build up your cash & ST investments rather than trying to hedge or short indexes or stocks. This is a critical shift in strategy IMHO. Just on Q1 results, if you look at other insurers eg Travelers, Chubb they have all had big hits to their book value in Q1 & potentially more come in Q2 given interest rate increases this quarter so far, but as I understand they are classing their bonds as held to maturity, so they are not reporting losses on bonds through their income statement. So the result is that it looks like they had great earnings, but in present value terms, the loss of value on those bonds is significant & is reflected in hit to book value. Whereas Fairfax are reporting their bonds as available for sale or trading, so MTM loss is being reported through their income statement (ie FVTPL), so its a better reflection of the economic impact of higher interest rates ie present value of their bonds is lower - even though Fairfax said on conference call they expect to hold these bonds to maturity, so these bond losses in Q1 should fully reverse in time - this is an important point to remember when we reflect on Fairfax Q1 result.

-

https://www.theguardian.com/world/2022/apr/24/all-omens-look-positive-greece-grateful-tourists-flock-back ‘All omens look positive’: Greece is grateful as the tourists flock back Not since the pre-Covid season, when 33 million holidaymakers visited, has business been as good

-

+1 - they have added a little over $1 bil of quarterly net earned premium in the last 12 months. I was thinking they might do around 18 bil in net earned premium this year & now with 4.77 bil in Q1, I am thinking potentially closer to 19-20bil area?? Below was a bit of a surprise - once off gain affecting result or is this reflecting underlying earnings potential going forward? Consolidated share of profit of associates of ...$38.0 million from EXCO Resources

-

No but they should keep webcast on their site - i was up from 11.30pm to 6am syd time watching both ffh and fih AGMs - they usually post the agm presentation

-

thanks viking 1) stood out for me - if they can get extra 100 bp on 7.5 bil thats extra $75 mil there 2) 'Although a substantial portion of EXCO’s oil & gas production is hedged for the year 2022, we believe that EXCO can fetch much higher prices as the hedges roll off.'https://www.gurufocus.com/news/1675983/francis-chous-chou-associates-fund-annual-2021-letter 9) they indicated Digit now has 2.4% market share - looks like a 50% increase in market share over last 12mths? Just on AGM question time, I think they should have given more time to online questions (JS said he still had a lot at the end).

-

Cheers!

-

I can't see the AGM presentation slide on the Fairfax website - was there an approx $7 bil investment in 1 & 2 year US Treasuries in Q1-22?

-

'In fact, Fairfax acquires the percentage of the British fund M&G, which according to the latest data reaches 51.1%. What has not been made known is whether the company's shares will be transferred directly to the Canadian group, or whether they will be distributed to its Greek holdings. Today the remaining 48.3% of Grivalia Hospitality is "shared" with Eurolife (26.7%), Eurobank (19.9%) and Grivalia Management (1.7%). ' https://www.moneyreview.gr/business-and-finance/business/74705/nea-epochi-gia-ti-grivalia-hospitality-perna-ston-pliri-elegcho-tis-fairfax/

-

Going all in on luxury hotels/tourism in Greece Acquisition of sole control by Fairfax Financial Holdings Limited over Grivalia Hospitality SA, which is currently jointly controlled by Fairfax and M&G Investment Management Limited. https://epant.gr/enimerosi/anakoinosi-sygkentroseon/item/2187-apoktisi-apokleistikoy-elegxou-apo-tin-fairfax-financial-holdings-limited-epi-tis-grivalia-hospitality-sa-i-opoia-epi-tou-parontos-telei-ypo-ton-koino-elegxo-tis-fairfax-kai-tis-m-g-investment-management-limited.html

-

would be curious to compare Recipe's multiples/valuation against peers

-

I think they would continue to consolidate if they went over 50% ownership

-

Prem Watsa, Chairman and CEO of Fairfax stated, “We are very happy to transition our investment in Altius to that of a supportive long-term shareholder. During the period that we held Preferred Securities we watched the Corporation’s progress closely and viewed the benefits of its disciplined, counter-cyclical and long-term strategies unfold. The Corporation’s business model of collecting royalties from a wide range of long-lived properties producing copper, gold, nickel, iron ore, potash and renewable energy generates considerable upside in an inflationary environment without having to make any additional capital investment. Royalty growth comes from production growth as well as price increases, not to mention meaningful optionality from existing royalty interests in projects which are likely to come onstream in the next few years.”

-

https://www.businesswire.com/news/home/20220413006065/en/Altius-Announces-Exercise-of-Warrants-Held-by-Fairfax-Surrendering-for-Cancellation-of-Preferred-Securities-and-Filing-of-Early-Warning-Report 'Following the completion of the Transaction, Fairfax will directly or indirectly own or control 6,670,000 Common Shares, which represents 13.94% of the issued and outstanding Common Shares as of April 14, 2022, on a non-diluted basis, and Altius will have no outstanding Warrants, Preferred Securities or resulting interest distribution obligations.'

-

no worries nwoodman - yes that was a potential question mark item, we can now strikethrough I think

-

thank you Brian Bradstreet & Co

-

yes viking i would agree