glider3834

-

Posts

1,082 -

Joined

-

Last visited

-

Days Won

5

Content Type

Profiles

Forums

Events

Everything posted by glider3834

-

Yes agree - also as Fairfax repurchases its common stock (via SIB & NCIB), existing holders will effectively end up owning a bigger percentage of Fairfax India via Fairfax's stake. Fairfax is repurchasing its common stock at up to 80% of BV & in that BV Fairfax India's shares are being carried at close 0.5x BV or around $10 per share. So assuming Fairfax repurchases at 0.8x BV multiple (and we feel that Fairfax's BV is at a minimum being carried appropriately - its fair value is higher IMO ) then we can say that Fairfax are effectively buying Fairfax India shares at 0.4xBV or approx $8 per share.

-

Looking the most recent Ki share allocation/capital injection, both Fairfax (via Brit) and Blackstone appear to be contributing on a 20/80 split, so I suspect that out of the $500 mil capital commitment - $100 mil is going to be funded from Fairfax via Brit & $400 mil via Blackstone. Not sure whether Fairfax can at any point have the option to contribute a higher percentage - we just don't know what the terms of the $500 mil commitment are. Also the wording of the $500 mil commitment are its coming from Fairfax & Blackstone, why not write Brit & Blackstone (or does Fairfax potentially have option to put money in from its own pockets ??) Yes would be nice for Fairfax to own a greater share of Ki, but at the same time we can look at it in the context of what the world was like in Sep-20 - we had no vaccine & Blackstone would have been spoilt for choice in terms of investments. Why would they commit to invest in a promising tech start up with no revenues? They would need a decent % of the equity to compensate them for that risk. For Fairfax & Brit, getting this new tech start up off the ground & scaling up quickly (with other competitors out there) would have been important. Plus Fairfax tipped in around $520 mil into Brit during 2020 to support their underwriting capital & they had to pull down on their credit facility to do this. Putting a further $400 mil into KI as well was probably a bridge too far & again in the context of Sep-20, Fairfax would have been prioritising its own capital position plus would have been spoilt for choice on investment side. Anyway thats my take - but as SJ said this is just speculation because we need to get it from the source.

-

Ok according to May-21 update for Ki Financial Ltd - it looks like Blackstone has around 79% of the ownership, Brit 20% (so Fairfax via Brit 17.2%) & less than 1% held by company officers. Brit have majority voting rights of 51%. https://find-and-update.company-information.service.gov.uk/company/12594708/filing-history On 23 September 2020 and 24 November 2020, Brit Limited invested US$15m and US$16m respectively into Ki Financial Limited. The Group holds 20.0% of the share capital of Ki Financial Limited and 51.0% of the voting rights. The entity is consolidated in full by the Group. https://www.annualreports.com/HostedData/AnnualReports/PDF/LSE_BRE_2020.pdf

-

article on Ki & its potential to be IPO'd at some point (Interesting they note that Ki's premiums could potentially double in 2022!) https://www.insuranceinsider.com/article/29ee5pw6no1rnvrtsvfgg/the-typtap-playbook-lessons-for-hiscox-brit-and-canopius Brit launched Ki in November 2020 with $500mn in backing from Fairfax and Blackstone’s Tactical Opportunities fund, while its technology was developed in collaboration with Google Cloud. The business stands out as having the fastest year-one start of any tech-enabled underwriting enterprise, and is on course to write $400mn of premiums this year. By way of comparison, Lemonade was launched in 2015 and had premiums in force of $347mn at the end of Q3. Ki has approval from Lloyd’s to double during 2022, pointing towards potential for $800mn of top line next year. But as it is scaled the early benefits of being umbrella’d by Brit will lessen, and there would be scope for Brit and Fairfax to look to crystallise value through an IPO. Indeed, this path could also make sense as a liquidity event given Blackstone’s involvement, or as a means of raising additional capital to support surging growth. Also worth noting, Ki won the Digital Insurance Award at the National Insurance Awards 2021, held in London in July. https://www.britinsurance.com/news/ki-wins-digital-insurance-award

-

Tidefall have posted some quotes from the CIBC report below

-

https://www.forbes.com/sites/billybambrough/2021/12/03/300-billion-bitcoin-and-crypto-price-crash-after-stark-fed-warning-ethereum-bnb-solana-cardano-and-xrp-in-free-fall/?sh=e05be3522fd5 I don't believe that Bitcoin or Ethereum are worthless like JD suggested - IMO they have a value - I am not sure what that value is. I won't go into the positives & negatives of crypto but crypto does seek to address some of the problems inherent in national currencies & that has some value. However, unlike stocks, crypto are not tied down by this pesky metric of discounted cash flows. So this then opens the gates for people to espouse these unbelievable forecasts around what what BTC or other crypto should trade at - you can basically throw any number out there just throw in a lot of zeros at the end! Often you see prominent people like Tim Cook interviewed & they say I have dabbled in BTC - but what is rare to see is a prominent investor putting in a conviction trade on BTC which would actually get my attention (ie significant % of their personal wealth not a 1 or 2% trade). The reality is that most prominent investors don't want to do that, because they don't know what its actual value is - that 1 or 2% investment is just to hedge their bets because they are looking at a chart that seems to only ever be going in one direction at an exponential rate. And that goes to the heart of the matter for me - the reason I have avoided & will continue to avoid BTC etc - it is the biggest driver of these massive returns on one hand (no cash flows to tie down valuation, throw any number out there) & it is also the achilles heel of crypto IMO.

-

saw this today but I haven't read their report Fairfax Financial Holdings Ltd (FFH.TO): CIBC initiates coverage with "outperform" rating https://www.reuters.com/markets/stocks/tsx-futures-flat-omicron-dents-sentiment-propped-by-stronger-crude-2021-12-03/

-

Interesting insights thanks viking

-

viking I know you are following RFP closely - in terms of damage to transportation infrastructure (rail lines etc) - how that might impact their movement of lumber? If they can't move the lumber until Feb, could they lock in the current favourable pricing?

-

Looks like FFH (via HWIC Asia Fund) to me & then Fairfax India would hold its IIFL Finance shares through FIH Mauritius (see below) As of September 2021, HWIC Asia Fund held 7.48 per cent stake in IIFL Finance, FIH Mauritius Investments, a subsidiary of Fairfax, owned 22.32 per cent stake in the company https://www.business-standard.com/article/markets/prem-watsa-backed-fairfax-sells-3-2-stake-in-iifl-finance-for-rs-365-crore-121120101508_1.html

-

https://www.athina984.gr/en/2021/12/01/mitsotakis-theloyme-na-einai-i-chora-mas-kainotomos-kai-protathlitria-stin-anaptyxi/

-

https://www.businesstoday.in/latest/story/fairfax-sells-32-stake-in-iifl-finance-for-rs-365cr-314148-2021-12-01

-

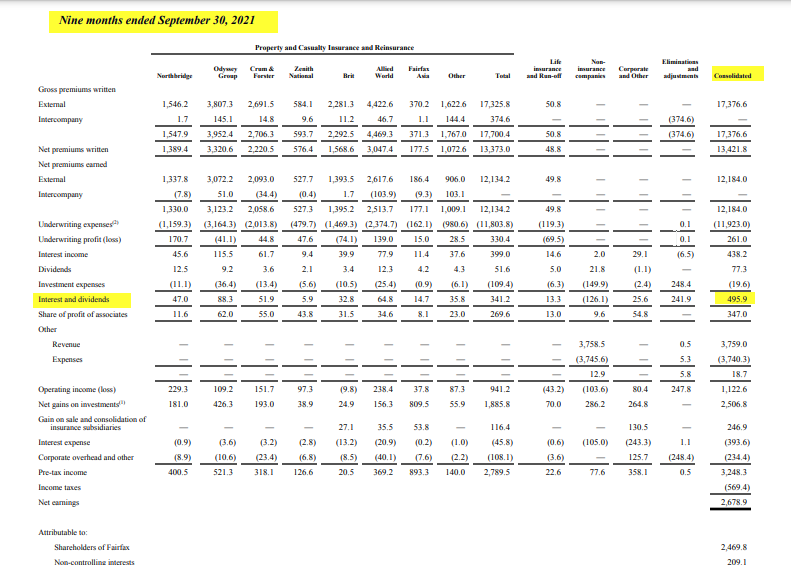

I just wanted to add a few thoughts here on my operating revenue estimates for 2022 Underwriting Profit - I think a 95-96 CR on 18 bil in net earned premium (10% increase on my 2021 estimated net premium of 16.5 bil) is reasonable which would put it at between 720 to 900 mil (what is really interesting here is every 1 CR point is equal to around 180 mil, so if we have a cat light year the underwriting profit could really blow out, but 95-96 CR would sit Fairfax in line with last 3 years CR in high 95s (excl covid losses) . Note: given the trend in their underlying CR is falling, as underwriting expenses ratio is lower on a higher net earned premium base, they could also surprise here assuming normal cat loss year. Interest & Dividend income - I am estimating 660 mil for 2021 (annualising based on 9mths to 30 Sep-21 of $495mil) & lets say 700 to 730mil for 2022 (expecting higher interest rates next year and potential lift in dividends) Profit from Associates - For all their associates, I think a number in the 500-600 mil area looks possible in 2022. I want to see the final Q4 results before drilling down on a more definite estimate/range. I am estimating around $457 mil in 2022 potentially to come from 5 key associates (Atlas,Eurobank, Resolute Forest, Quess, BIAL) which comprise 57% of $4.7 bil (mkt value) out of total of $8.2 bil of market value of Fairfax's associates (insurance & non-insurance) at 30 Sep-21. Broken down below (excluding Riverstone because any gains there will be MTM & come through as derivative gains on their repurchase option, if I understand it correctly) Atlas Corp 170 mil (use Atlas mgmt 2022 estimate 535mil less preferred dividends estimate 70mil) x 36.6% ownership (excl riverstone stake) Eurobank 167 mil (Eurobank mgmt. expect 10% ROE in 2022 – estimate 520 mil net income on 5.2 bil NTA) x 32.2% ownership Resolute Forest 80 mil (FFH 31% ownership (excl Riverstone) - 2022 Est net profit 260 mil or $3.25 per share - at lower end of analyst expectations ) Quess 10 mil (my estimate 10% ROE for 2022 (note mgmt. aim 20% ROE in 2023) - (10% x 2325 crore equity Sep-21 = USD 31 mil) x 31% ownership) BIAL 30 mil (use FFH share of BIAL profit in 2019 assuming international flights resuming by 1 Jan-22 - Omicron could be an issue??) Non-Insurance companies (pre-tax income)- this is a really interesting one - if you look at the Q3'21 report, the restaurants & retail segment had a pre-tax income of $56.8 mil but the overall result was only $35 mil pre-tax due to losses in Thomas Cook India & Other segment. The Q4 result for non-insurance segment will be a key one to see how restaurant & retail segment performs. Hopefully this Omicron variant won't throw a spanner in the works, but assuming most travel resumes in 2022 I think we can expect at least a breakeven result from Thomas Cook. Like Viking I don't think 100mil in 2022 looks unreasonable for this segment, but I think it could even be higher. Run-off & Life Insurance - run-off loss tends to be higher in Q4 & I believe this might be due to 4Q auditing of loss reserves. Would like to see how life insurance business performs in Q4. Will wait for Q4 result before forming estimate for 2022. Putting above together, I am estimating between $2 bil to $ 2.3 bil in operating revenues (excluding net investment gains) in 2022. Please note - with my estimates I am just looking at operating revenues & 1. ignoring run-off & life insurance for now which will be a sub $100 loss IMO 2. minority interests (eg Fairfax India) will claim a % of the above operating revenue number, but their net earnings share gets deducted at the bottom of the earnings statement.

-

all good klipbaai

-

thanks @Mick92 ok well if they can't fully complete the SIB, they will waste no time restarting the NCIB at these price levels at lower end of tender pricing IMO

-

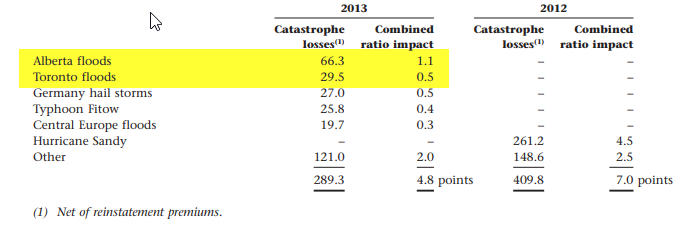

good insights SJ - expect the insured losses to be less than the actual losses - in Calgary 2013 insured losses appear to be around about 33% of the actual losses/damages https://www.theglobeandmail.com/business/article-bc-floods-will-be-canadas-most-expensive-natural-disaster-this-year/ I am going back to 2013, floods in Alberta & Toronto. https://www.reuters.com/world/americas/canadas-10-costliest-natural-disasters-by-insurance-claims-2021-11-17/ In 2013, Northbridge Insurance had 2.52% market share & looks like Fairfax incurred around 3.6% of the insured losses. Alberta C$1.7 bil (Fairfax loss 66.3 mil or 4%) Toronto C$0.94 bil (Fairfax loss 29.56 mil or 3%) In 2020, Northbridge had approx 3.2% market share so maybe we could expect 4-5% of the insured loss based on their market share? Of course just purely an estimate & their underwriting exposures would have likely changed, but I think their market share in terms of premium does provide some help in terms of measuring potential exposure. I haven't been able to find an insured losses estimate yet but anyone feel free to post if you have. Cheers

-

Can't Fairfax execute its normal course issuer bid at the same time as its substantial issuer bid? With their shares trading in the mid US$400s, why would they bother waiting for the auction tender which we know could be a challenge to fill anyway? Looking at the TSX today the volume today is over 140,000 shares when its avg volume is normally around 50,000 shares.

-

thanks viking - just on interest & dividend income - I think you might be looking at the interest & dividends for insurance business but not the consolidated number (ie including non-insurance subs, corporate etc) this number is higher Here is screenshot of 3Q Interim report which shows the breakdown of interest & dividends per operating segment - the total is $495 mil in interest & dividends for 9mths s to Sep-21.

-

https://nymag.com/intelligencer/2021/10/why-the-big-short-guys-think-bitcoin-is-a-bubble.html

-

well the lower Fairfax's share price (relative to pricing under this tender), the more attractive this buyback might look to tax advantaged funds/individuals to participate IMO Also volatility in the market would encourage funds to prioritise liquidity - another reason why funds might sell into this SIB. Finally, timing - we are coming to end of the calendar year - funds are mindful of their annual performance (particularly if markets are weak) & may have incentive to lock in gains at a fixed price under this tender. So a temporary period of volatility could work for Fairfax at least while this SIB is open - as long as we don't see the the economic recovery completely derailed (which I see as a low probability at this stage).

-

i meant to say asset side - higher loan quality

-

3Q results out from Eurobank - I haven't been able to find the 3Q call transcript but what has been reported in media https://www.kathimerini.gr/economy/561603262/eurobank-kategrapse-kerdi-298-ekat-eyro-sto-enneamino/ is - management expect double digit ROTE in 2022 - based on tangible book of 5.2 bil at 3Q - I believe that would be a NPAT in the area of 520 mil euro at 10% ROE (if mgmt can deliver then Fairfax's share or profit from this associate at 32.2% ownership would be in $167 mil area) - discussions with supervisory bodies starting in early 2022 to discuss the dividend - obviously this would be significant for Fairfax - other metrics look good - non-performing exposures down to 7.3%, deposits up 8% YTD (over 9mths) I noticed Eurobank's share price down 5% or so today which looks to be in line with many other European financials- I think people are more concerned about this new SA covid strain today anyway cheers

-

I posted under Eurobank thread - also posting here https://greekcitytimes.com/2021/11/25/surprisingly-growth-athens-property-prices/ Property prices in Athens soared by nearly ten per cent in the third quarter of the year, according to the latest batch of data, as Greece’s real estate sector proves to be one of the strongest in Europe. this bodes well for Eurobank's banking ops - on revenue side (more potential lending growth) on liability side (ie increases collateral values on their lending book) It is also a tailwind for Eurobank's 1.36 billion euro property investment portfolio https://www.ekathimerini.com/economy/1171079/athens-the-2022-commercial-property-capital-of-europe/ Athens looks forward next year to being the commercial property capital of Europe, based on the projected course of prices and rental rates for 2022. The latest annual survey by PwC and the Urban Land Institute on the European property market shows that the Greek capital will lead the ranks in future capital gains and rental hikes among 31 cities. Notably, the Athens market gained the highest marks regarding the future course of both rental rates and sale prices.

-

@SafetyinNumbers from SEC filing On November 16, 2021, the Company executed a binding agreement to sell a 9.99% minority stake in Odyssey to the Odyssey Investors for consideration of US$900,000,000. https://www.sec.gov/Archives/edgar/data/915191/000110465921140897/tm2132409d1_sc13e4f.htm I read that as an equity sale (via new issue) for a 9.99% stake(rather than a bond issuance) If it was a mandatory convertible - it must be converted by some future date into an equity interest - but in this case the 9.99% minority stake appears to vest immediately with the purchasers (and then Fairfax has option to repurchase at some future date) I would never say never but thats just my reading based on the wording

-

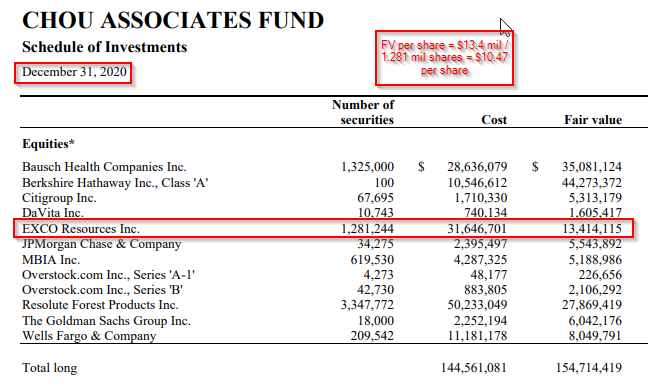

@Maxwave28Exco Resources Chou Associates Fund are also shareholders in Exco & it appears they have increased the fair value of their Exco investment by 29% YTD to 31 Aug-21. All of this fair value increase has happened since 30 June. This fair value increase in Exco is probably what might be expected given the big jump in natural gas prices in 2021. Fair value = US$10.47 per share at 31 Dec-20 Fair value per share = $13.51 at 31 Aug-21 (assuming they held same number of shares as at 30 Jun-21) Assuming Fairfax are using similar valuation approach to Chou Funds, then we could expect approx 29% increase YTD in fair (market) value of Fairfax's stake in Exco. At 31 Dec-20, Fairfax had a fair vale of $238 mil on their Exco holding(same as carrying value). A 29% increase would be $69 mil increase in fair value on this position over carrying value. Looking at the Q3 Interim report from Fairfax, it looks like they have increased the fair value of of All other - non-insurance associates (which would include Exco) between Q2 & Q3 by $67 mil - so its possible that this Exco fair value increase has already been taken up by Fairfax - we will have to wait for the 2021 Annual report to know for sure!