glider3834

-

Posts

1,082 -

Joined

-

Last visited

-

Days Won

5

Content Type

Profiles

Forums

Events

Everything posted by glider3834

-

We don't have all details here but why couldn't it be similar to Brit - issue a new class of common stock? With Brit, it looks like OMERS has the A shares & Fairfax has the B shares & the A shares have certain priority in respect of dividends On IFRS impact https://ifrscommunity.com/knowledge-base/ifrs-10-consolidated-financial-statements/ Changes in a parent’s ownership interest in a subsidiary that do not result in the parent losing control of the subsidiary are equity transactions So I think we could see a potential BV gain here (see my earlier post suggesting potential accounting impact) to reflect the excess of $900 mil cash proceeds over carrying cost of 9.99% interest in Odyssey Again this is just my hunch, could be wrong but we will find out for sure next month

-

https://www.fairfax.ca/news/press-releases/press-release-details/2022/Fairfax-Declares-Annual-Dividend/default.aspx

-

Yes agree viking - along with earnings/BV growth points 1-3, i think likely we will see a multiple re-rating in 2022 on Fairfax shares ie P/BV x 1 or higher. Fairfax remains my largest equity position.

-

https://m.timesofindia.com/business/india-business/digit-first-unicorn-of-2021-in-top-10-non-life-insurers/articleshow/88600245.cms

-

yes I think over US$1000 is achievable- if we use BV Sep-21 of US$562 - I think over 5 years a BV growth rate could be around 12% p.a & P/BV multiple could expand to 1.1x to 1.2x (mid-point 1.15x BV) - which would give a PT of US$1,139 in 5 years. This would be compounded share price return of just over 18% p.a, based on current share price of US$490.

-

What valuation is too high to buy a great compounder?

glider3834 replied to tnathan's topic in General Discussion

I think extremely low interest rates have fueled some very high PE multiples & I think we are moving to higher rates of 2% plus next year & so I think we all need to be careful. But I am generalising with above comments, if you find a company selling for 30x earnings & you have done your research & you are extremely confident it can continue powering away at 30% per annum earnings growth for the next 5 years then sure 30x earnings is reasonable. And if you can get the same company at 20-25x PE then you will do even better. -

What valuation is too high to buy a great compounder?

glider3834 replied to tnathan's topic in General Discussion

I think the trick is to pick up a great compounder at a reasonable multiple- MSFT, AAPL have all had periods where they sold at or below 15x earnings & so you get both multiple expansion plus earnings growth plus downside protection. When you pay 30-40x earnings then you can't afford for anything to go wrong - BABA is a classic example - it looked like a great compounder when the PE was in the 40s from 2016-2018 & now shares are trading well below avg 2018 levels, because you have had multiple compression! -

I'm not sure viking - maybe you could use Fairfax India buyback payment time as a reference - not sure if Xmas period might slow things down

-

+1

-

Yes could be true - also I think possibly there was an expectation that the SIB would be undersubscribed due to tax implications, and so the fact it was modestly oversubscribed took the market by surprise. Also maybe a signalling aspect that Fairfax is prepared to repurchase shares at a premium to current share price, indicating they see undervaluation. Would be great to see Fairfax have another go at this in 2022 if this discount is still there. Those swaps are looking good too.

-

if (?) they have structured it as a preferred, then I agree I think that is more realistic than 9 or 10% but I am still not sure what the structure is. https://am.jpmorgan.com/content/dam/jpm-am-aem/global/en/insights/market-insights/guide-to-the-markets/mi-guide-to-the-markets-us.pdf

-

if (?) they have structured it as a preferred, then I agree I think that is more realistic than 9 or 10% but I am still not sure what the structure is.

-

Amazing - it was oversubscribed! Happy with the result.

-

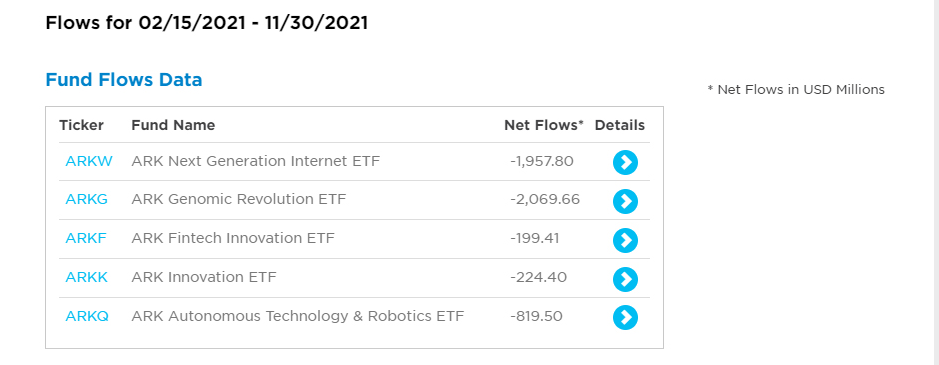

The fund flows picture doesn't look great up to November https://www.etf.com/sections/features-and-news/ark-funds-leaking-assets I checked & over the last month the same ETFs are down between 14-22%. What will net fund flows look like for December?

-

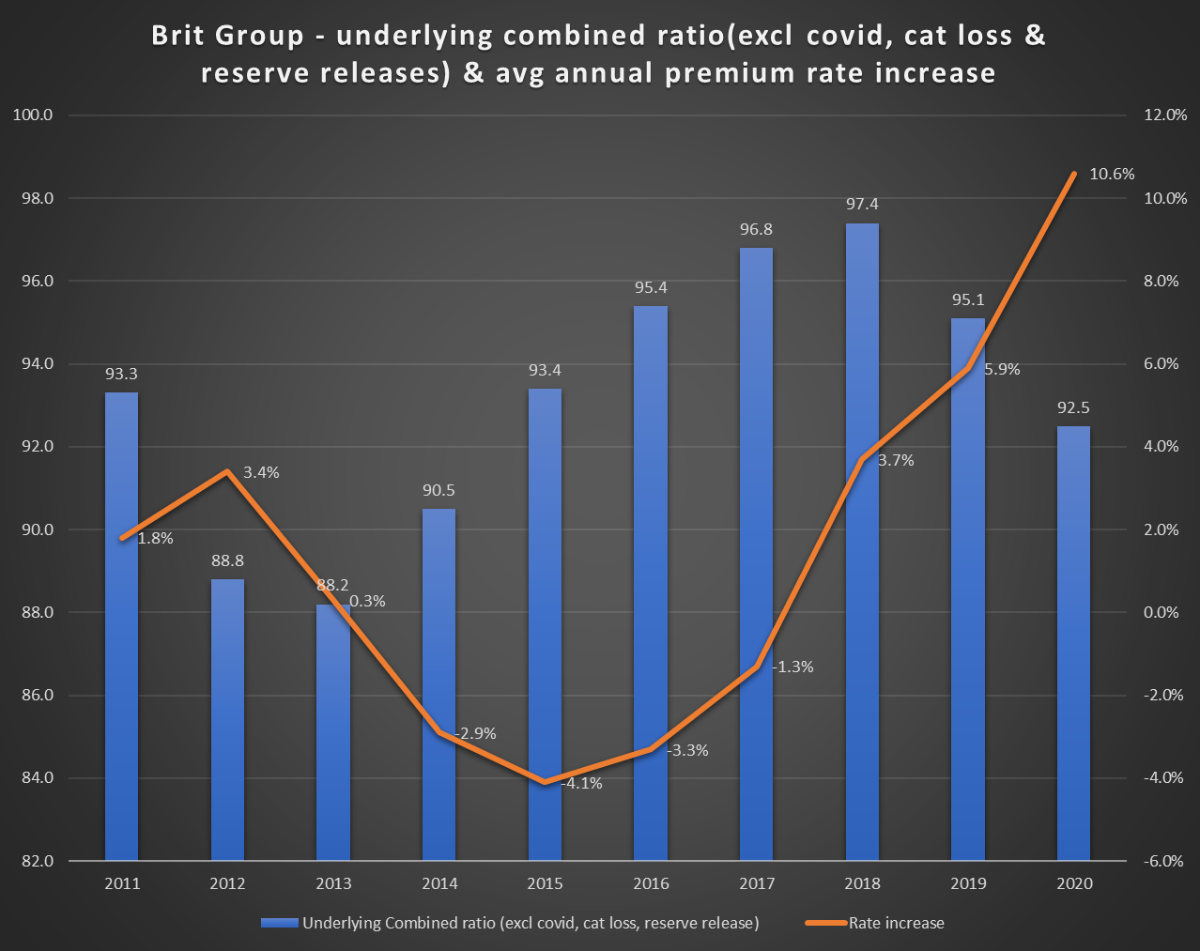

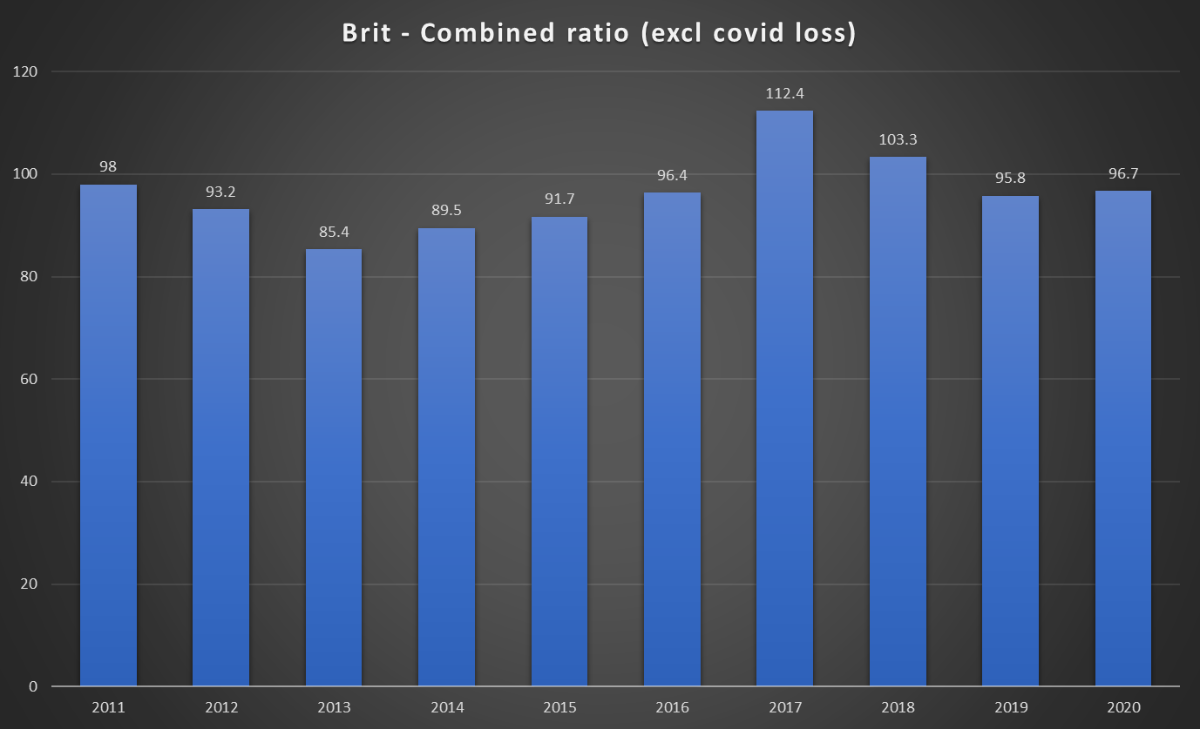

I have done a little work on Brit - I have scooped the data from Brit's reported financials (again try to be careful but always double check my numbers ;)) It looks to me like premium rate increases (due to hard market) have improved Brit's underlying combined ratio (excluding covid loss, cat loss & reserve releases) over last 3 years. You can see that successive price decreases from 2014 to 2017 (as market suffered from over-capacity & excessive competition) resulted in higher underlying combined ratios. Then from 2018 to 2020, successive price increases have helped reduce Brit's underlying combined ratio from 97.4 to 92.5. A further, 10% increase in first 6mths of 2021, took the total aggregate price increases since 2018 to 30%. The overall combined ratio (excluding covid losses) looks to have improved over 2018-2020 as a result of these rate increases. Now lets turn to Q3 result which appeared to be disappointing. Brit's combined ratio increased from 94.6 in 6mths to Jun-21 to 105.3 for 9mths to Sep-21 (103.1 excluding start up Ki) due largely to losses from Hurricane Ida of $169 mil. This appears to combination of Brit having a material exposure to North Atlantic hurricane risks and also proportionally more exposure to Louisiana in their open market property book. To manage this exposure, it looks like Brit also uses excess reinsurance & on Q3 call Peter Clarke said their aggregate cat losses for year are close to their retention level so Q4 result should be better. And lastly at Brit, they didn't get any benefit from their cat reinsurance program. So basically as of now, their aggregate cat losses for the year are just coming up to their the retention of their cover. So the good news is any further, any further development or losses in the fourth quarter will be minimal for Brit. My take is that I think Brit is showing improvement on underwriting front as rate increases reduce their underlying combined ratio. Key to them achieving a consistent sub 100 combined ratio will be their ability to also effectively manage their cat loss risk exposure.

-

still too early to say but initial estimates are a single digit billion dollar event https://www.artemis.bm/news/weekend-tornado-storm-losses-to-run-into-billions-of-dollars/ https://www.insuranceinsider.com/article/29g01n5bkms47pokxasjk/fatal-tornadoes-a-manageable-loss-but-outsized-disruption-for-reinsurers looks like Fairfax had approx 1.1% of loss from Ida (340 mil loss on 30 bil or so event) So if we are looking at single digit billion dollar event, then I would guess loss for Fairfax is likely less than $100 mil

-

https://bfsi.eletsonline.com/our-aim-is-to-empower-humans-with-technology-and-not-replacing-them-vijay-kumar-ceo-and-principal-officer-go-digit-general-insurance/

-

thanks SJ for posting - here is another article too https://www.theglobeandmail.com/canada/british-columbia/article-preliminary-insurance-cost-estimates-for-bc-floods-point-to-a-massive/ Widespread flooding across southern British Columbia in November is now estimated to have caused $450-million in insured damages, making it the most costly severe weather event in the province’s history, new figures from the Insurance Bureau of Canada show. But that figure reflects only a small portion of the total price tag, in part because many residents affected were in high-risk flood areas and floodplains where insurance coverage is not available.

-

Thrifty its good you have raised this, its something we have to factor in with ATCO - I think for Fairfax there is a hedge to this risk with Fairfax's high cash/ST invest allocation. I guess the big question if Fed moves, how much to get to neutral & also how quickly will they move rates? (I haven't read Vanguard report) It looks like ATCO are forecasting avg LIBOR rate (figures from Q2'21 earnings presentation) at 0.48% for 2022 0.96% for 2023 1.3% for 2024 ATCO have $3.4 bil of variable rate credit facilities at 30 Sep-21 with fixed rate swaps on around $1 bil (rounded) of that amount. So lets say $2.4 bil of variable rate debt at risk to higher interest rates. Then I would guess that if LIBOR is 1% higher than Atlas Corp's projections above(assuming it approximates Fed rate) - it would approximate to an increase in interest exp of $24 mil (using Sep-21 balance). However, with new builds & deliveries, that variable debt balance would I think be higher - Thrifty you or someone else might know? Does anyone know what ATCO projecting for their variable debt balance for 2022,2023,2024 in modelling their profit forecasts? Cheers

-

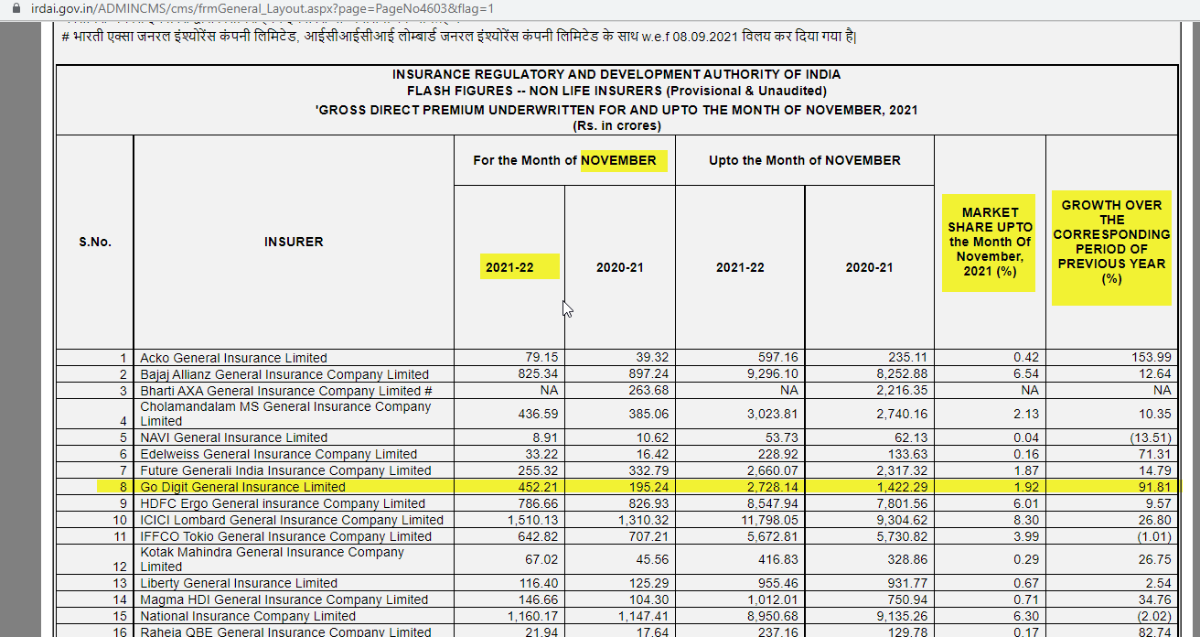

closing in on 2% market share

-

could be they are raising liquidity due to their share buyback at holdco level or to make another portfolio purchase - may be different reasons

-

+1

-

https://www.livewiremarkets.com/wires/what-you-need-to-know-about-india-s-structural-growth-story We maintain a very positive view on India’s long-term structural growth prospects. This is because the country has strong demographics — its 1.4 billion population is not only behind China, but younger (with a median age of 28 years) and growing more rapidly. India is expected to add 200 million people to its workforce between 2020 and 2050. As these extra hands join the workforce, they will contribute to GDP growth as well as add to the country’s consumer base. Also, India has one of the lowest penetration of goods and services such as automobiles, white goods, electronic devices and services such as mortgages, credit cards and online travel.

-

Just a quick comment on Greece with Fairfax having significant investments there (Eurobank, Eurolife etc) Greece was the second fastest growing economy in the Eurozone in 9mths YTD & fastest growing in the 3rd Quarter. Greece also recorded their highest GDP in the last decade over the Sep-21 Qtr https://www.fortunegreece.com/article/staikouras-protathlitria-anaptixis-stin-evrozoni-to-trito-trimino-i-ellada/ Greece has been a long & painful road for Fairfax, but the steady flow of data now coming out in terms of GDP growth, property prices growing, increased foreign investment (Amazon. Pfizer, Microsoft to name a few), lower unemployment etc all further supports the view that things are well & truely improving for Greece and thats good news for Fairfax's banking, insurance & property businesses there. Also the Greek PM & government are really doing a great job (I have to pinch myself now because I am complimenting politicians!) but they have had a difficult task & have really made a lot of progress - they are making it much easier for foreign companies to invest in Greece & its now paying off as well as lowering taxes & other policies to encourage Greeks to return to Greece or foreign workers to move to Greece - I have now watched a few interviews with the PM & came away very impressed - & the results are starting to show in higher GDP growth etc. Eurobank are also expecting Greece to have the busiest year in tourism in 20 years in 2022 based on bookings to date (provided covid doesn't flare up again!). Also GDP growth over time will become less dependant on tourism (obviously big hit from covid) as Greece is seeking to expand its economy in other sectors - nearly 23% of foreign investment in Greece in 2000 was in software & IT. https://greekreporter.com/2021/07/14/foreign-investments-greece-soar-77-percent-2020/

-

looks like a subscription required :(