glider3834

-

Posts

1,082 -

Joined

-

Last visited

-

Days Won

5

Content Type

Profiles

Forums

Events

Everything posted by glider3834

-

Pursuant to the terms of the Proposed Transaction, the Purchaser will acquire all of the Shares, other than those Shares owned by Fairfax or its affiliates and a maximum of 4,000,000 MVS owned by CHL, for a purchase price of $20.73 per Share, payable in cash. The Buying Group is comprised of certain affiliates of Fairfax. The Proposed Transaction would be financed by equity proceeds contributed by members of the Buying Group and debt financing, and would not be subject to any financing condition.

-

Atlas won't lose its neutrality IMHO as long as ONE is not the controlling shareholder & the charters that Atlas does with ONE are on similar commercial terms to other shipping liners. These charter rates are also being made publicly available, so they are visible to everyone.

-

These look like commitment limits - actual transaction value may be less

-

So these appear to be the equity financing commitment limits made to BidCo ( i only just saw link so need to read through) David Sokol $30 mil Washington Family $175mil ONE $1.4 Bbil https://www.sec.gov/Archives/edgar/data/0001794846/000119312522213659/0001193125-22-213659-index.htm @Viking

-

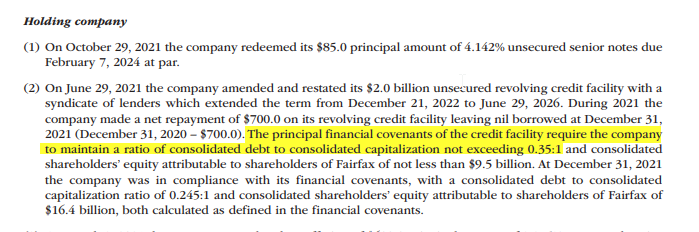

It will be interesting to see what structure this ATCO offer could take. I don't think that Fairfax can consolidate Atlas Corp - Why? because of the financial covenants on their revolving credit facility restrict their consolidated debt to consolidated capital to 35% & consolidating Atlas Corp will take this ratio to 36% (up from 28% at Jun-22) (my workings below but do your own dd) Fairfax Jun-22 total debt 7.7 total equity 19.7 total capital 27.4 Atlas Corp Mar-22 total debt 5.6 total equity 4.3 total cap 9.9 Consolidated total debt 13.3 total equity 24.1 total capital 37.4 Consolidated total debt/total capital = 36% (exceeds 35% limit)

-

I think for Fairfax there is strategic rationale here that Atlas with ONE as a co-shareholder raises the value of Atlas - ONE is largest customer 24% of vessels under lease - so this cements that customer relationship - logical for ONE to do more future charters via Atlas in which it has co-ownership - growth opportunity - ONE made 16.7 bil in 2021 - potentially provides atlas with deep pocketed partner if they want to go on acquisition path Still unclear what % ONE or other partners want to buy so offer vague here??

-

interview re BIAL - will be able to handle 60 mil passengers (T1 36 mil plus T2 25 mil )after T2 completed - not sure how quickly they will scale up to 60 mil after T2 opens- that part of the interview requires a subscription ...arghh https://airwaysmag.com/bangalore-kempegowda-airport/

-

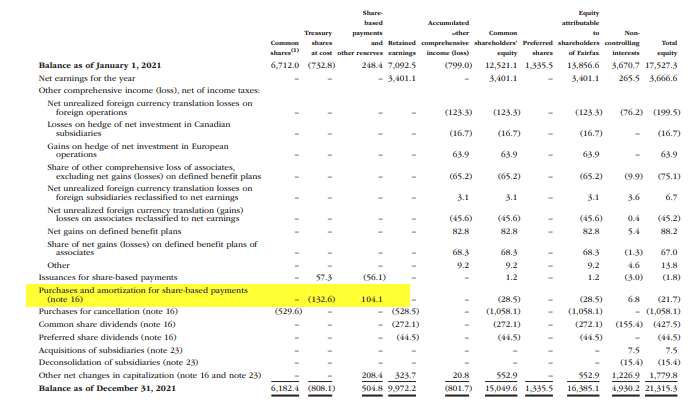

actually these restricted share-based payment awards (RSAs) were 567K at end of 2016, so increase for 2017 was 122k not 689k. Thinking holistically about the business, Fairfax needs to incentivise & retain management/staff & RSAs also help align management & shareholder interests over the long term. The financial results are really the litmus test on whether these types of remuneration arrangements are effective - so you have to evaluate against the financial performance (insurance & investment results) of the business over the last few years & ask the question has it been a win/win for Fairfax? Worth considering that these share based awards have long vesting periods of up to 15 years (in other companies it may typically be closer to 3-5 years) & these Fairfax awards are also subject to performance hurdles eg underwriting profit - here is one for Allied World https://www.sec.gov/Archives/edgar/data/915191/000094787122000815/ss1199327_ex9901.htm The amortisation of share-based compensation for Fairfax was 104 mil pre-tax in 2021. To offset the dilution on these share awards Fairfax has been repurchasing shares on an ongoing basis including in 2021 - this is a cash cost to Fairfax . Looking at the share-based comp expense in 2021, I estimate it might have reduced BVPS growth by approx $4-$4.50 or bit under 1% in 2021.

-

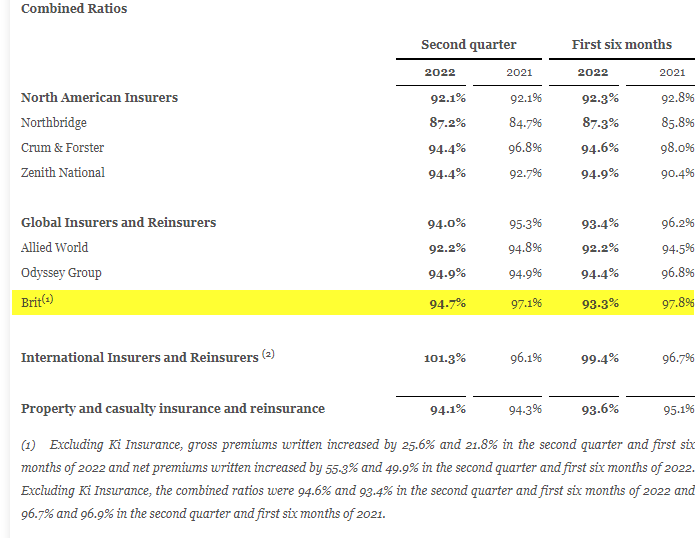

Just looking at 2Q & 1H'22 results & I don't want to speak too soon with business end of the year (ie hurricane season) upon us - but Brit results continue to improve with decent premium growth & better combined ratios Brit managed rate increases close to 12% in 1H driving premium growth Brit's (20% owned) Insurtech Ki continues to scale quickly with significant premium growth (Ki wrote close to 400 mil for 2021 calendar year) & its combined ratio has improved close to break even in 2Q & 1H'22.

-

-

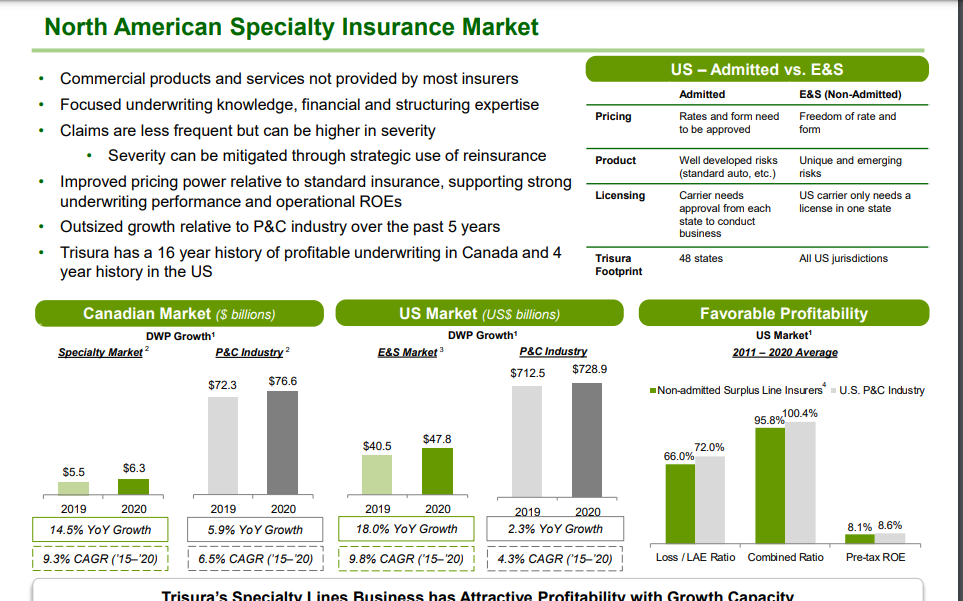

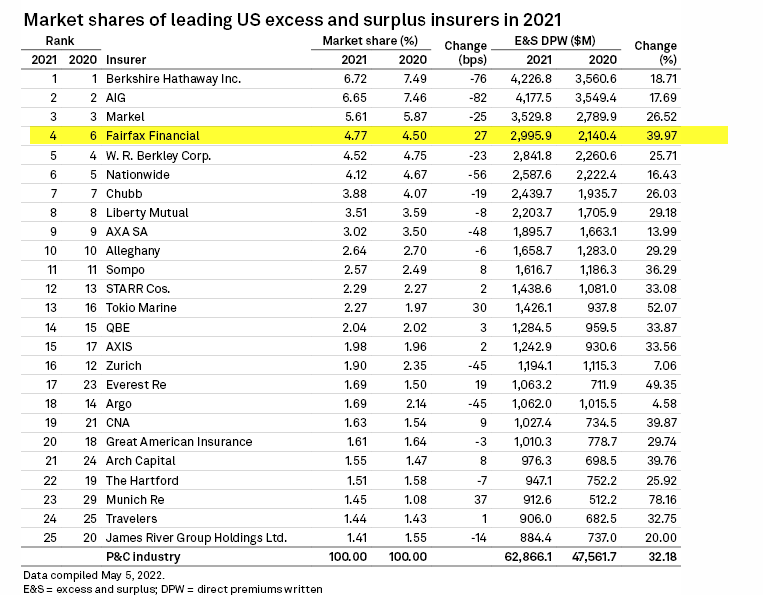

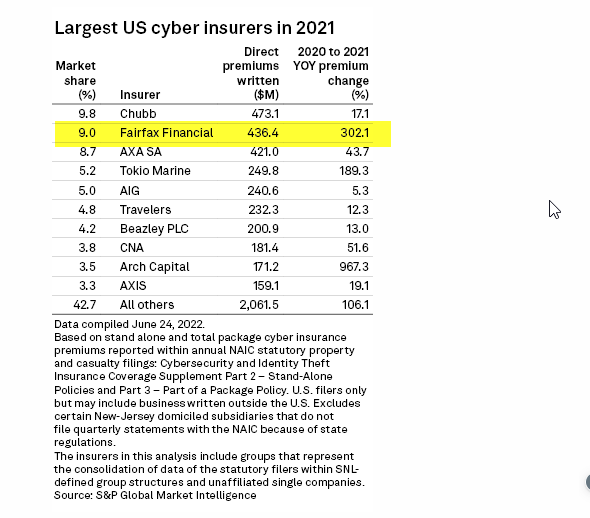

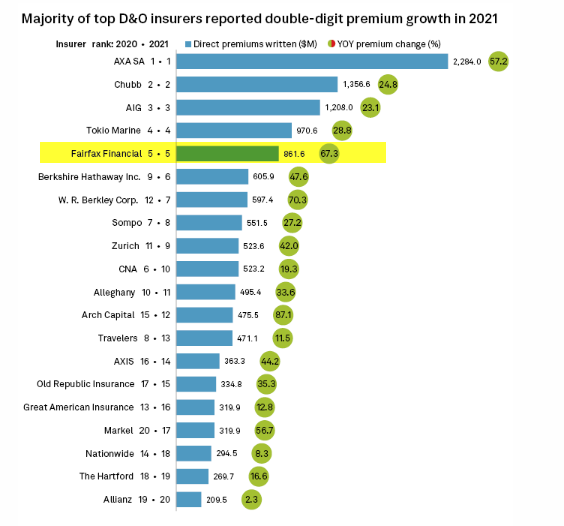

thanks viking - great summary - its interesting also where they are growing - one key area is specialty/E&S. E&S is harder to do so more specialised, less competitive & more profitable (lower CR) than standard lines. Trisura actually put up a nice summary comparing E&S(specialty market) to standard marketplace & why they are attracted to this space Fairfax has grown to be the #4 E&S (Specialty marketplace) writer in US One of the fastest sub-sector areas in insurance is cyber insurance & with rates hardening here a lot in high double digits, Fairfax has been putting emphasis on growth here - #2 US writer behind Chubb https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/insurers-revisit-cyber-coverage-as-demand-premiums-spike-70880071 #5 US writer in Directors & Officers Liability - again this market was supported by significant rate growth https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/d-o-premiums-grow-38-5-in-2021-loss-ratio-falls-to-multiyear-low-70106981

-

The investment environment & insurance cycle are inter-related because regulatory capital ultimately affect what business an insurer is permitted to write. I think hard market has also been affected by - low interest rates (were too low, depressed fixed income returns forced insurers to raise premiums) - higher inflation - social inflation (court judgement award amounts - trending up over time) & economic/financial inflation (impacts reserving/claim costs) - large natural catastrophe losses (elevated in last few years - climate change etc increasing in terms of size and severity - also factor in covid)

-

Just had a quick look at Eurobank results also released today - they are executing well - 2022 forecasts for loan growth, operating profit & EPS have been revised up - despite the challenging environment in Europe, Greece looks to be doing better with 4% GDP growth - tourism breaking records this year https://www.eurobankholdings.gr/-/media/holding/omilos/grafeio-tupou/etairikes-anakoinoseis/2022/2q-2022/2q2022-results-pr-en.pdf

-

still looking at Q2 result - heaps of moving parts but just tallying transactions coming up & MTM bonds (& not factoring in Stelco) after -tax impact estimate Pet insur/JAB 975 Bonds MTM reversal 805 estimate (965 pre-tax) (assuming bonds held to maturity) Digit gain 400 Resolute gain 150 (180 pre-tax) total $ 2.33 bil (just under $100 per share)

-

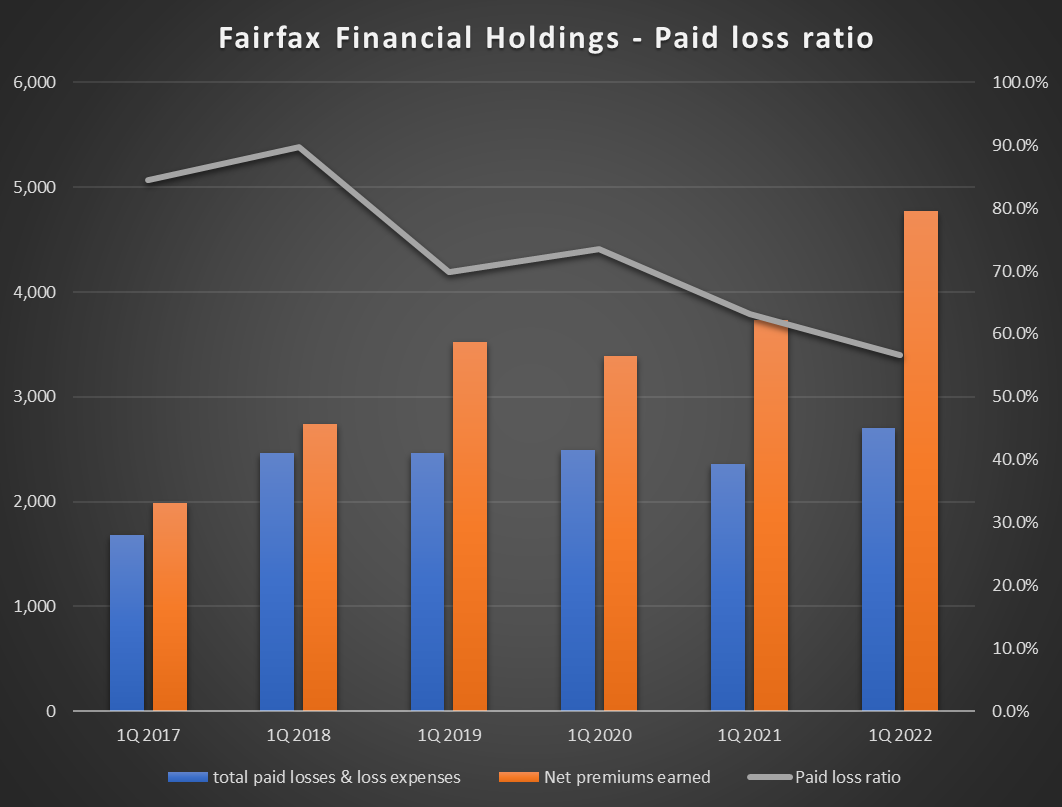

I was listening to WRB earnings call for Q2 - highly worth a listen - Rob Berkley highlighted how WRB's paid loss ratio (this is a hard number as its what an insurer has actually paid on claims) is in a falling trend - WRB are being cautious as there are still delays due to covid in court system, inflation trends etc, but it also is one data point that could suggest WRB is potentially giving themselves extra cushion on loss reserves that could potentially lead to redundancies later on if those loss picks prove too conservative - but again only time will tell! 'Loss ratio is the losses an insurer incurs due to paid claims as a percentage of premiums earned.' Investopedia One other piece on the loss ratio, and I think I shared this with all last quarter. And for us, it's just one of many data points that we pay attention to, and perhaps, it's of interest to you all and that's the paid loss ratio. From our perspective, it is an important data point. It's not the whole story, but an important data point. So here's a little bit of historical perspective for you again on Q2. And I'm going to give you what the paid loss ratio was going back to 2017 for Q2, that creates as much of an apples-to-apples basis as we can, at least using shorthand. So the paid loss ratio Q2 in '17 was a 55.9. In '18, it was a 58.3. In '19, it was a 53.8. In 2020, it was 52.9. In '21, it was a 44.3. And in '22, it was 41.9. So obviously, an attractive trend. Doesn't necessarily tell the whole story. But again, from our perspective, a meaningful data point and an encouraging indicator. I looked at the paid loss ratio for Fairfax looking at 1Q results over 2017 to 2022 and this is also in a falling trend (again try to avoid mistakes but please do your dd) - worth continuing to track this data point

-

this is interesting - it sounds like Fairfax are looking to create two new insurance company start ups in India raising their own capital. You have applied to the IRDAI for life insurance and reinsurance licences. What is the plan for those verticals? Right now the focus is to get through the licensing process. Life insurance and reinsurance will function as separate companies. Once we are successful in securing the licences, we will have talks on further plans. Both the new companies will have to raise funds separately, they will have their own management teams.

-

https://www.moneycontrol.com/news/business/startup/will-assess-timing-of-ipo-based-on-market-conditions-digit-insurance-chairman-kamesh-goyal-8881791.html

-

you can track here https://www.irdai.gov.in/ADMINCMS/cms/frmGeneral_List.aspx?DF=MBFN&mid=3.2.8 but it looks like data not loading - they might be having issues

-

good points Twocities I would just add point that was made at Fairfax's AGM that a lot of these infrastructure assets have been developed by govt over decades but are not well managed (my take - that would be reflected in the sale price).

-

-

Fairfax Financial Holdings Limited, a significant stockholder of Resolute, has entered into a voting and support agreement to vote its shares in favor of the transaction. As of July 5, 2022, Fairfax Financial Holdings held approximately 30,548,190 shares, or 40% of the outstanding shares as of that date.

-

Around 40%

-

Resolute Forest takeover https://www.bloomberg.com/news/articles/2022-07-06/paper-excellence-to-buy-resolute-forest-for-1-6-billion#xj4y7vzkg

-

Article on Kyle Shaw at ShawKwei https://theceomagazine.com/executive-interviews/finance-banking/kyle-shaw

-

viking I think they will separate out the pet insurance business as asset held for sale at its carrying amount in Q2 results. And the gain on sale would be reported when transaction is closed. Once we have the carrying amount, we can work out what the gain should look like. Cheers