glider3834

-

Posts

1,082 -

Joined

-

Last visited

-

Days Won

5

Content Type

Profiles

Forums

Events

Everything posted by glider3834

-

https://cyprus-mail.com/2022/12/30/greek-eurobank-further-increases-its-stake-in-hellenic-bank/ Assuming regulatory approvals given, Eurobank stake will be 29.2%, if it decides to move to 30% or above it could launch a takeover of Hellenic.

-

Fairfax Top 10 Events of the Year - Driving Shareholder Value

glider3834 replied to Viking's topic in Fairfax Financial

thanks viking - you have done an awesome job putting this together! Happy New Years! -

+1 Blackberry i think we can pop in the bottom drawer - i do think Ivy is very interesting and worth following developments there - check out this Moodys podcast from 14min mark which explains how OEMs could threaten incumbent auto insurers or end up as distribution partners with their access to vehicle data and customers https://www.moodys.com/web/en/us/about/insights/podcasts/moodys-talks-focus-on-finance.html Another related article https://www.carriermanagement.com/news/2022/03/10/233728.htm

-

thanks viking you have made this point but it is something I wanted to just comment on I think that analysts place more emphasis on Operating income (underwriting profit & interest/dividend income & non-insurance income) than they do on Investment gains (realised or unrealised) because operating income is seen as a more predictable. So to the extent Operating income becomes a bigger component of Fairfax's earnings - we could say the earnings become more predictable/consistent or higher quality & so based on this factor (all else being equal) it would make sense to put higher P/B multiple or P/E multiple on those earnings (compared to earnings are coming principally from investment gains) IMHO earnings power of the business has transitioned meaningfully - we have gone from a business that I thought could do 12% ROE (that gets me to P/B of 1.1 to 1.2) 12 mths ago, to a business that could do ROE for 2023 closer to 15% with a significant Operating Income component in that Net income number , which IMHO takes the target P/B higher. (Aside: I am curious if we view Fairfax's fixed income management as significantly better than their peers who have lost 20-30% or more of their BV this year, should we ascribe some further premium to the P/B multiple - I believe we should) For 2023, I see the most significant opportunity in 2023 is reinsurance which could see record UWP assuming normalised cat activity & the biggest risk in 2023 I see is inflation impacting reserving - Fairfax's commercial, non-admitted business gives it flexibility to price ahead of inflation/cost trends but nevertheless remains a risk Again above comments just my opinion, please always do your own due diligence ...

-

Have a great Christmas and New Years

-

fun fact - the new 'Glass Onion' release in Netflix was filmed at Amanzoe resort owned by Grivalia https://www.housebeautiful.com/lifestyle/entertainment/a42268845/glass-onion-knives-out-2-filming-locations/ https://www.aman.com/resorts/amanzoe/accommodation/villas/villa-20

-

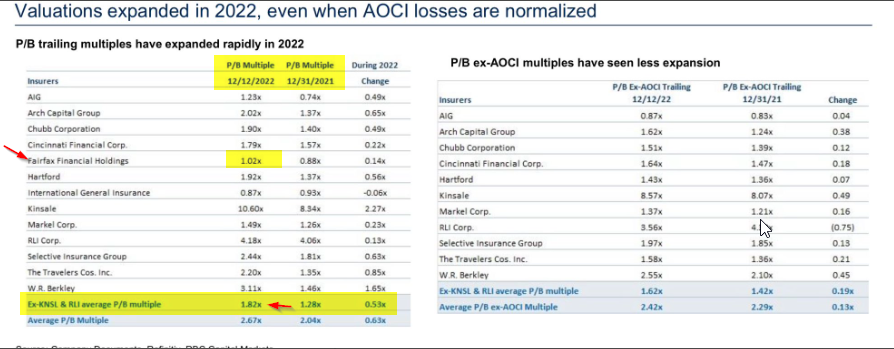

But can we make the argument that the baseline has moved up over the last 12 mths peer group avg P/B multiple has expanded from 1.2 to 1.8x (adj to remove RLI & KNSL) (however, less expansion with ex AOCI multiple to 1.6x)

-

S+B: How does the future look? MYTILINEOS: We completed 2021 with record-high profitability and used it to prepare for the transition to higher levels of financial performance and value creation for our shareholders in the following years. In a year full of significant challenges, we demonstrated our capability to adapt in difficult conditions, with good planning and hard work, and will continue to do so in the years to come. I think 2022 and 2023 are going to be record years for us. Our Renewables and Storage business unit is doing well, and prevailing trends are in its favor. In the metallurgy sector, we have enjoyed bumper years, and that’s part of a ten-year cycle. And in power and gas, we are establishing ourselves as the number one private utility in Greece, as our major investments in power and renewables are now maturing and starting to pay back. Considering all of this makes me very hopeful for the next two years. https://www.strategy-business.com/article/Powering-the-net-zero-transition-at-Greeces-Mytilineos

-

https://www.mytilineos.gr/news/company-news/fairfax-becomes-the-2nd-largest-shareholder-in-mytilineos/ MYTILINEOS: MYTILINEOS S.A. is a leading Greek industry active in Metallurgy, Power & Gas, Renewables & Storage and Sustainable Engineering Solutions. Established in Greece in 1990, the company is listed on the Athens Exchange, has a consolidated turnover of €4.5 billion (9M 2022) and employs directly or indirectly more than 4,820 people in Greece and abroad.

-

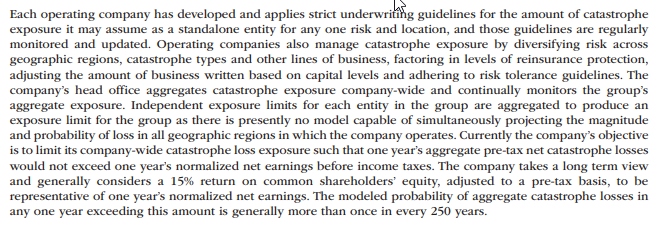

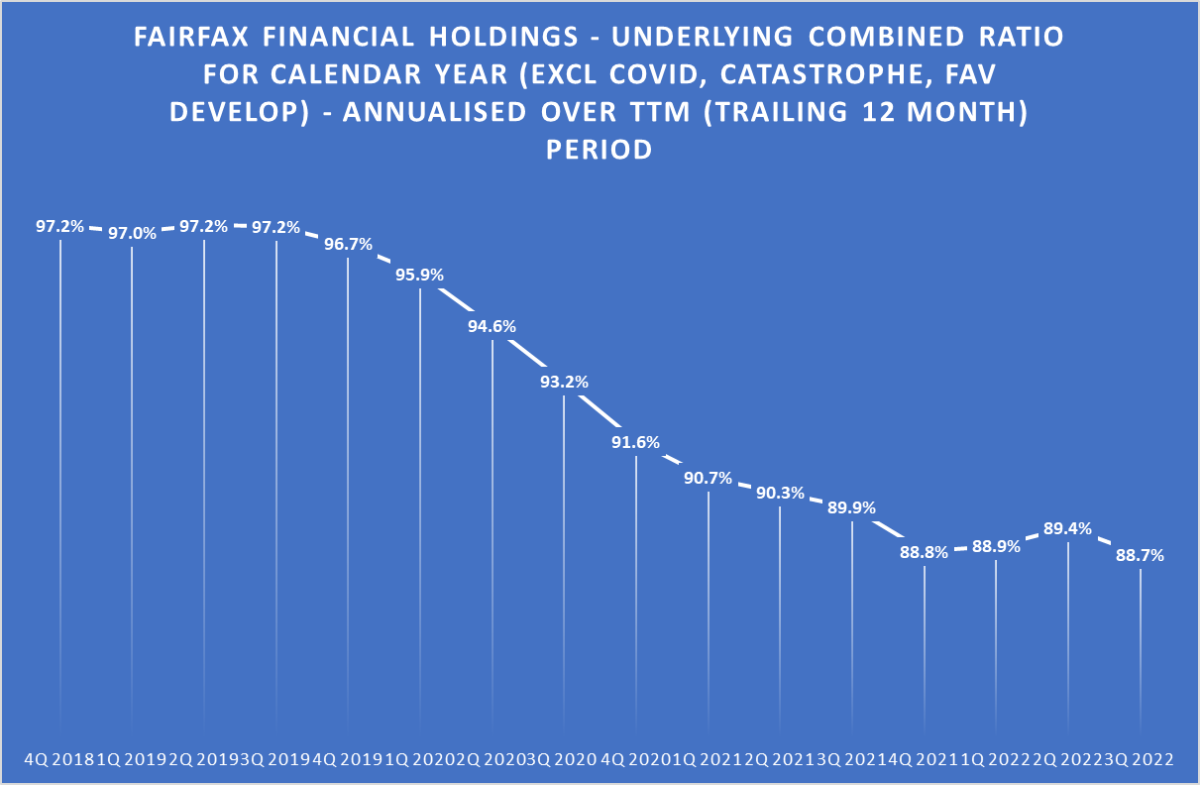

I think this section from AR 2021 report is relevant to this discussion - Fairfax have limits on amount of cat exposure risk by entity & for the group with the aim of limiting company wide cat loss exposure to not exceed one-year's pre tax normalised earnings One risk management tool Fairfax use to limit exposure is retrocessional cover - after Ida in 2021, Brit was very close to triggering group protection under its multi-year retrocessional cover ( reinsurance for reinsurers). Despite the significant impacts of catastrophes, Clarke said that, “At Brit, they didn’t get any benefit from their cat reinsurance program,” during the third-quarter. But Brit’s aggregate reinsurance protection is now close to coming into play, after impacts from events throughout 2021. Clarke explained, “Basically, as of now, their aggregate cat losses for the year are just coming up to the retention of their cover. “So the good news is any further, any further development or losses in the fourth quarter will be minimal for Brit.” https://www.artemis.bm/news/no-reinsurance-recoveries-for-brit-but-aggregate-deductible-almost-eroded/ Another point, with Fairfax's underlying CR around 89, assuming no favourable development, they could sustain around $2.2B In cat losses in one year & still break even on underwriting. Just a final thought, as we move into 2023 reinsurance and retro markets https://www.artemis.bm/news/retrocession-quoting-scarce-with-60-100-rate-increases-demanded/ are already undergoing a significant spiking in rates & tightening in terms, all bets could be off if we got some sort of Ian size cat event or larger!

-

https://www.ekathimerini.com/economy/1199226/eurobank-to-buy-additional-13-4-stake-in-cypriot-hellenic-bank/

-

By my calc - based on 30 Sep positioning unrealised TRS gain (since inception) = 1.964 x (573 - 373) = $393M unrealised TRS gain for 4Q = 1.964 x (573 - 457) = $227M At September 30, 2022 the company continued to hold equity total return swaps on 1,964,155 Fairfax subordinate voting shares with an original notional amount of $732.5 million (Cdn$935.0 million) or approximately $372.96 (Cdn$476.03) per share

-

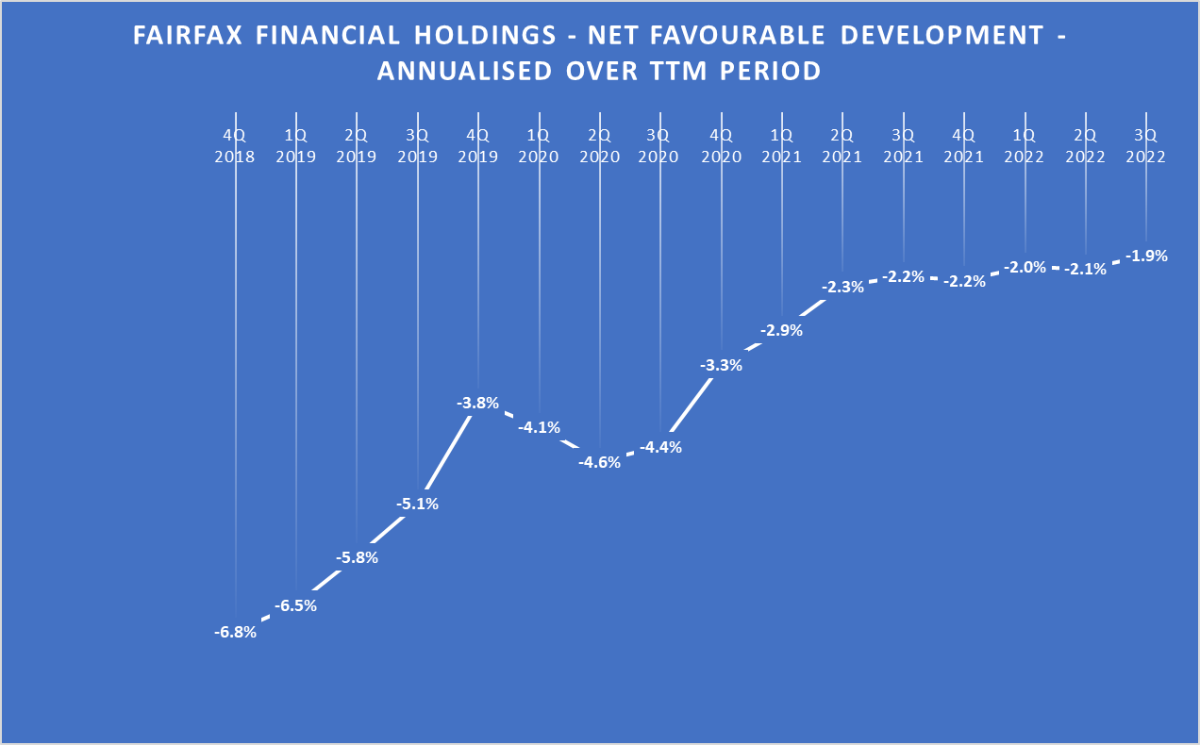

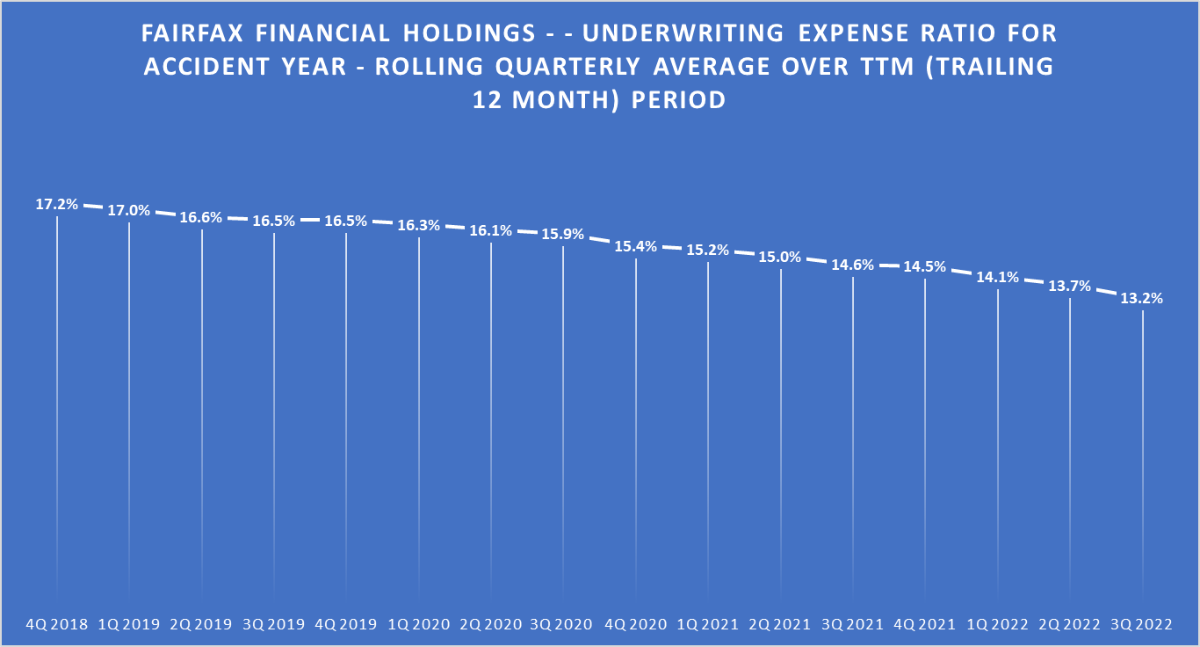

viking I have been doing some stats on the underwriting - my question is around the 95CR estimate - what factors could affect this? Fairfax's underlying combined ratio is sitting at around 89 annualised Higher net earned premiums have reduced the underwriting expense ratio (component of combined ratio) which is now sitting at 13.2% annualised (4Q21 adjusted for loss portfolio transfers). Fairfax has reduced reserves releases to -1.9% annualised Over the last 4 years, catastrophes have averaged 5.5 CR points - lets round it up to 6 CR points Putting the above together, if we assume no favourable reserve development in 2023 & underlying combined ratio holds then a combined ratio = 89 + 6 = 95 looks reasonable A conservative -1% in favourable reserve development could drop that to 94. The two elephants in the room are inflation & higher reinsurance rates. How will these impact the combined ratio? With reinsurance rate increases expected in 2023 plus tighter terms for reinsurers - Fairfax has the potential , provided we get a normalised cat year, to write more reinsurance more profitably (lower combined ratio) in 2023. Fitch expects reinsurer CRs to drop by 4CR points from 98 to 94 in 2023. I am not sure the overall impact of higher reinsurer pricing impacts combined ratio for insurance business - if they can pass on the rate increases then impact can be mitigated. How the mix of inflation combined with higher premium rates impacts reserves releases remains to be seen - we will have to wait & see.

-

Forex depn & are divs being subtracted too maybe ?

-

-

BRK is carrying its $134B or so position in Apple as a common stock, so counts toward tangible book, even though on a look through basis Apple mkt cap is approx 47x book value courtesy of its phenomenal earnings power. So most of Apple's mkt cap is goodwill. Similar observations could be made about Coke, Moodys etc Tangible book is useful yardstick but it has its limitations - I would also focus on earnings power & float

-

works out as a US$33M or so dividend for Fairfax https://investors.stelco.com/news/news-details/2022/Stelco-Holdings-Inc.-Reports-Third-Quarter-2022-Results-and-Announces-a-3-per-Share-Special-Dividend-and-a-40-Increase-of-its-Regular-Quarterly-Dividend-to-0.42-per-Share/default.aspx

-

they haven't converted them, the strike is $6 , matures Nov-23 https://www.globenewswire.com/news-release/2020/09/02/2087633/0/en/Fairfax-Announces-Acquisition-of-1-75-Convertible-Debentures-of-BlackBerry-Limited-After-Redemption-of-Existing-Convertible-Debentures.html

-

great article on drivers behind very hard market in reinsurance https://www.insurancejournal.com/app/uploads/2022/11/Schroders-market-correx-article.pdf Along with tighter terms, significant reinsurance rate increases are being suggested "Hurricane Ian affected the entire industry," Hagedorn said, adding that reinsurers were estimating global property reinsurance rate rises of 15%-40% next year. https://www.reuters.com/business/finance/reinsurance-hedge-fund-tangency-capital-raises-200-mln-2022-11-11/ https://www.wsj.com/articles/insurers-are-facing-a-steep-rise-in-reinsurance-rates-11667858056 In the run-up to the key 1 January reinsurance renewal date, Cox cited speculation that reinsurance rates could increase “from the mid-20s to the 50s and higher” and include a “significant change in attachment points”. https://www.insuranceinsider.com/article/2aveq15rr2b5bo0dv4glc/london-market-section/properly-priced-reinsurance-positive-for-insurance-industry-beazleys-cox

-

https://m.economictimes.com/news/india/watch-inside-visuals-of-bengalurus-newly-inaugurated-airport-terminal-2/videoshow/95475394.cms They expect T2 will be operating in 1 to 1.5 mths - they are up to 16.8M to Oct-22 with T1 - so i think that puts them on trajectory of 28-29M just with T1 - then we add 3 mths of T2 passengers ???- although i think they will ramp up slowly. Both terminals can do up to 60M. Looks amazing - they are really pushing in terms of tech, sustainability

-

thanks viking

-

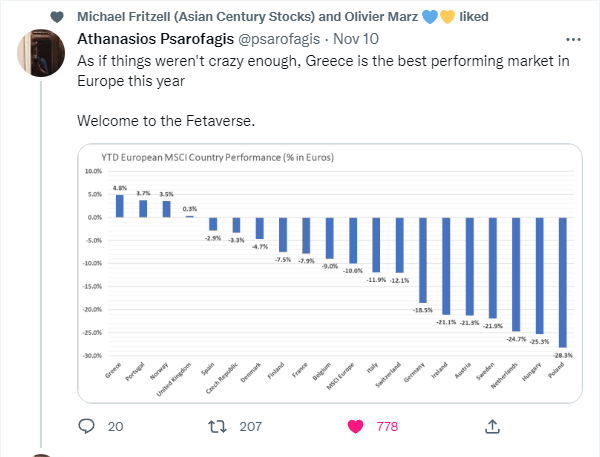

just on Greece saw this

-

Yep looks like they are guiding normalised EPS €0.17 on €1.09 share price - 15% yield - thats decent

-

-

I think you are using 8.8% as a sort of worst case scenario but it is really skewed by the hedges If you take out period they were 100% equity hedged, CAGR% in in book value per share is higher 2002-2010 (9 yrs) 13.9% 2011-2016 - 100% equities hedged 2017-2021 (5yrs) 13.1% (including dividends) Plus also factor in pre-tax investment yield (Interest & dividends) was 3.6% in 2002-2010 period but fell to 1.8% in 2017-2021. That impacted BVPS growth. We are now back to 3.2% - hopefully they can continue to move yield & duration higher.