glider3834

-

Posts

1,082 -

Joined

-

Last visited

-

Days Won

5

Content Type

Profiles

Forums

Events

Everything posted by glider3834

-

Here is a presso today from Blackberry - I thought Blackberry Ivy insights were interesting & some pieces from transcript below https://wsw.com/webcast/jeff195/bb/1520040 Charles Eagan So there's quite a bit of future potential being achieved by Ivy. And, and the potential for applications being developed on Ivy is almost endless. I think of imagine when we first were awful offered Google play and Android, and we asked people, what, what would the useful apps be on, on your, on your phone? I don't think we could have said, we're all going to have 50 apps on our phone, and we couldn't even name what they are today. So this invention is being enabled by this platform. But recently we announced for, for example, recently we announced the development of an app through a partner called car IQ that, that enables in vehicle payment. Obviously we want our car to, to be able to help us you know, acquire services. So this leverage is to have IVs key differentiators. The first is that Ivy has direct access to sensor data in the car. It uses this data to create a digital fingerprint of the car allowing for the highly secure payment authentication. It can also do a highly secure authentication of the user by looking at the patterns that it user like you are, what you do and what you do in the car can be determined by ID to give identity management. So and rely on pulling data from the cloud is nowhere near as secure as having direct access to these sensors. And then secondly, IVY pro provides edge compute analysis of the data is performed on a real-time basis in the car. Joe Gallo Switching gears you talked about it briefly, but just what's the value add of the partnership with AWS as it relates to IVY? Charles Eagan Yeah, so, but I think we compliment each other very well. So AWS is obviously a extremely large game changer in the cloud space, but there's lots of cloud technologies, but the ability to take that and combine the down into the automotive platform, the automotive platform access is equally strategic. So, together, we call it car to cloud. That stack is really unique. AWS has quite a lot of success bringing plat traffic into the AWS platform. Without this kind of partnership, obviously we're co-developing it. So we have a group of engineers working with Amazon engineers and doing this very unique. co-development. So basically we're trusted by the OEMs and tier ones. AWS has I don't know, 150 features that are available in the AWS cloud that now become applicable in, into the, into the connected vehicle via Blackberry Ivy. So, so this means app developers who are already well equipped at working within AWS cloud and AWS developer tools are now automotive developers. So as the vehicle becomes you know, rich in software features, we're opening up development potential to all of these cloud developers which is extremely strategic, the volume of developers that now have access to the vehicle in the future, compared to the automotive OEM software developers, it's orders of magnitude, more feature driving positive. So, the other thing I want to mention too, just from a IVY ecosystem evolution into the future that we designed IVY, Amazon and Blackberry to be OS agnostic and cloud agnostic. So, that means you don't have to be running QNX in your vehicle to run IVY. Although we think, we'd like it, if you would, let's say. It's also cloud agnostic. So it doesn't have to be an AWS cloud. You could pick another big cloud provider or a small cloud provider, Azure or Google, or some other cloud. We really wanted IVY to be this ubiquitous platform for the vehicle data. So we wanted to make it as flexible as possible. So, this, this is a massive potential for what we're, we're stitching together here. And it's really, I like to say it's a one plus one equals 10. So, extremely excited. I was in the first AWS Blackberry strategy session years ago, and what we pitched there was exciting and it's still exciting to see it come into fruition.

-

interesting insights on Recipe's business/restaurant environment thanks guys - sounds like we will see improving results but will take time

-

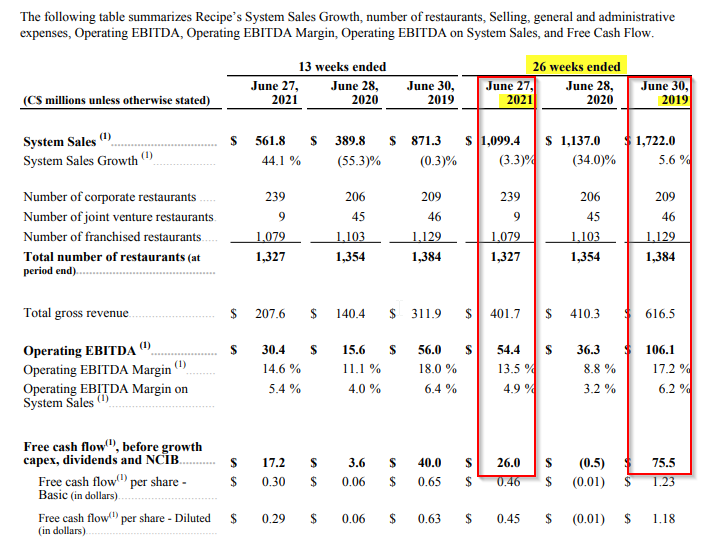

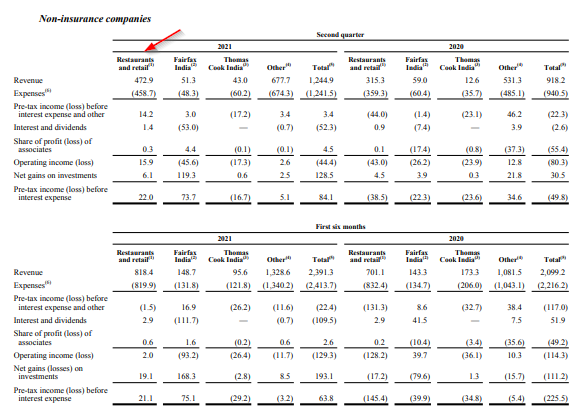

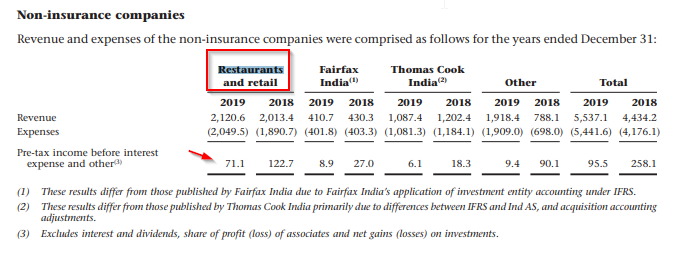

I don't live in Canada I am Sydney based - but has anyone visited any of the Recipe owned/franchised restaurants since the covid dining restrictions were eased in Jun-21 - would be interesting to get some feedback on how busy they are? Recipe is a significant non-insurance subsidiary for Fairfax & Prem mentioned on the Q2 2021 conference call he expected they could get back to 2019 sales levels Prem Watsa Yes, Jaeme. All of those things, including the restaurants, we think the revenues will be through 2019 levels once we back up. And unfortunately, lots of smaller restaurants have gone out of business. And so, if you want to go out dining, the big restaurant chains are where the action is going to be and our Recipe expects in the years to come to do well. (from Q2 2021 MD&A - Recipe) Looking at the Restaurants & Retail segment, I estimate around 40-45% of revenue is from Recipe and I expect Recipe to contribute most of the pre-tax income (before interest expense & other). In 2019, Restaurants & Retail generated around $71 mil in pre-tax income before interest & other (see below) versus the first 6 months of 2021 where it has only generated -$1.5mil (see above) while under the effects of Covid. Also worth mentioning that these revenue & income numbers are not pro-rata for Fairfax's share ie. non-controlling interests are subtracted out further down the Consolidated Earnings Statement.

-

thanks Twocities thats a nice summary & makes sense If we have a hypothetical situation where there is a large sudden increase (I wish:) in the price of Fairfax shares - could there be situation for example where hedge funds (who are short Fairfax via total return swaps) become buyers of common stock to offset their exposure OR where the counterparties that are writing OTM (over-the counter) call options start buying the underlying shares to also offset their risk. Could there be a feedback loop or squeeze type situation or would all these parties (hedge funds or option writers) again use derivatives to manage their exposures to effectively avoid buying the underlying shares where liquidity may be limited? Sorry if I am rambling but this TRS investment is unusual & I am trying to understand how it could impact the share price potentially ....:)

-

Looks like BIAL UDF fee rate increases will be postponed to start of March 2022 - would expect a negative impact on BIAL valuation - probably have to wait for Q3 to see. https://bangaloremirror.indiatimes.com/bangalore/others/from-april-2022-flying-to-become-a-tad-pricier/articleshow/85964418.cms At June 30, 2021 negotiations between BIAL and AERA in setting tariffs for the third control period were ongoing. In the event that these negotiations develop unfavourably, this may result in a negative impact to the fair value of the company's investment in BIAL.

-

just to put in context 1.96 mil shares - thats a CAD 1.1 billion position

-

Agree , although I would still probably continue to hold most of my position in shares due to the timing risk with options, I would also like to be able to buy OTM calls. I am super curious about how this total return swap on Fairfax shares has been structured. Its on around 1.96mil shares and there is no institution or fund that appears to own that many shares https://www.morningstar.ca/ca/report/stocks/ownership.aspx?t=0P00006821&lang=en-CA - if the payer (of this equity swap) wants to fully hedge their exposure, I assume they own the underlying share position in Fairfax?

-

no worries nwoodman yep I was the same I had to hunt around to find those quarterly reports today I think Prem at AGM said they don't want to IPO just yet & want to work toward a 10% market share in general non-life and are currently in 1.6-1.7% area - so I think they want to build it to a mature business at hopefully a bigger valuation. But I agree it would be a very attractive IPO given it is insurtech/high growth . There has been a muted reaction so far (buts lets see!) to revaluation of Digit which surprises me because if they were to IPO it , I suspect the Fairfax share price would probably jump with value recognition through IPO.

-

in terms of Digit valuation I have no unique insights but the last two fundraising rounds have both been at 3.5 bil level so we have had price discovery twice there now & if you look at Digit's current operating metrics (Jun21 Qtr) there doesn't appear to any let up in the pace or quality of growth (higher premiums & lower combined ratio).

-

Yep Viking honestly its a head-scratcher for me too given the sheer size relative to Fairfax's market cap but I think the market will come around eventually:) maybe the conclusion of the deal with regulatory approval & recognition in reported financials will help act as catalysts.

-

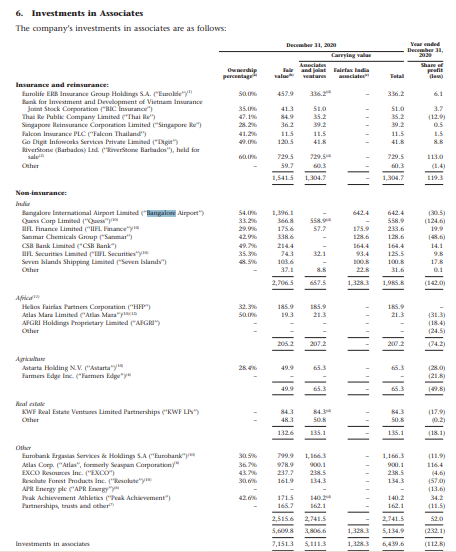

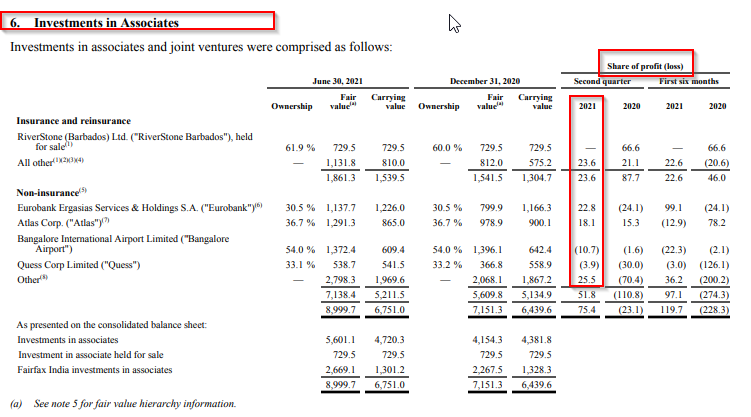

We are half way through 2021 but looking ahead to FY2022, I wanted to try & estimate potential income from Share of Profit of Associates. These estimates could change if Fairfax monetises positions (quite possible)and key risk includes any deterioration in economic recovery from Covid. Anyway here goes Two largest associates for Fairfax by carrying value are Eurobank & Atlas Corp Atlas Corp are forecasting $535 mil profit for Fy 2022 (see Q2 2021 presentation), I estimate Fairfax's shareholding (excluding Riverstone Europe) at around 44% based on 25 Aug-21 update (see SEC filing) - if Atlas Corp hit their forecast then Fairfax's profit share could be around $235 mil. Eurobank did 7.7% approx ROTE in most recent Jun-21 Qtr, lets assume they can do slightly improved 8.5% ROE on their tangible equity circa 5bil euro at 30 Jun21 as they emerge from Covid -their target is 10% ROE but lets be conservative. Lets assume EUR USD 1.2 & Fairfax ownership of 30.5%. Fairfax profit share would be $155mil. So lets say we have a potential contribution of around $390 mil to Share of Profit of Assoc from Eurobank & Atlas Corp in FY22 (compared to $104 mil from these holdings in FY20) Looking at 1HFY21 results from associates , if BIAL (international flights resuming from Sep-21) & Quess ((3) loss for 1H21 but covid still impacting demand for staffing & business process outsourcing) can move to break even in FY22, 'Other' category can contribute around 100mil in FY22 (was 25mil in Q221, & 36.2 mil in 1H21), $390 mil from Eurobank & Atlas (as above) & $10mil contrib from Insurance associates -we could get to $500 mil for Share of Profit from Associates (& I think the highest it previously reached was 221 mil in 2018) I am curious to hear other peoples' thoughts? Cheers

-

https://www.fairfaxindia.ca/news/press-releases/press-release-details/2021/Fairfax-India-Receives-All-Regulatory-Approvals-to-Complete-Sale-of-Minority-Position-of-Anchorage-Infrastructure/default.aspx

-

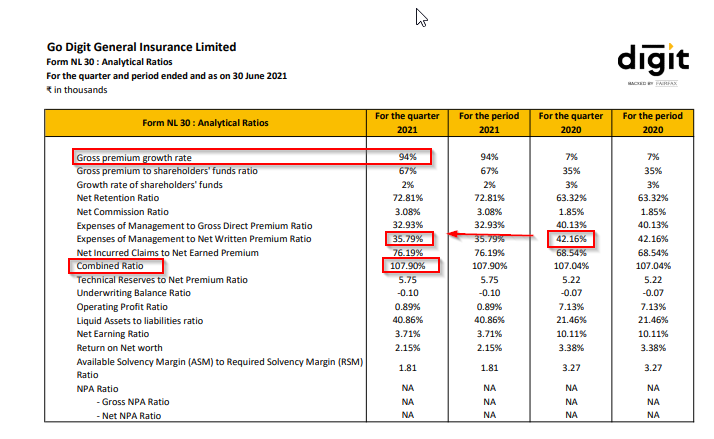

for Jun-21 Qtr - looks like around 76% increase in net premiums earned (vs Jun-20 Qtr) 94% growth in GWP (QoQ) & Expenses of Mgmt to Net premium written continue to fall nicely while net incurred claims to net earned premium are 76% (see table below avg 74% in FY 2021 & 75% in FY 2020) slightly on higher side not sure if one off factors or a trend or mgmt are content to target this mid 70% level but combined ratio is the key one below. Combined ratio (CR) now sitting around 107.9 up slightly QoQ, but improving on 2021 FY (CR109) & 2020 (CR117) - see below from Digit annual report.

-

article on Digit & podcast https://ajuniorvc.com/digit-insurance-lic-unicorn-india-startup-tech-general-acko/

-

thanks petec well if they can hit their 10% ROE target then there would probably be significant upside for Eurobank given current price/TBV level IMO- I noticed this ECB article which interestingly notes that banks with higher valuations also tended to have higher dividend payout ratios https://www.ecb.europa.eu/pub/financial-stability/fsr/focus/2020/html/ecb.fsrbox202005_05~d3679873d3.en.html I guess regulators will have to balance dividends with ensuring Eurobank continues to maintain its capital strength, but I suspect any dividend reinstatement would be a net positive for Eurobank shares.

-

thats interesting - how did you get to 15% for 'potential' dividend - that would be around 0.12 euro per share?

-

I agree petec I think Eurobank share price at 0.82 euro is at around 0.58 x TBV & looking at recent earnings report on nearly every metric from operating profitability through to capital strength they are showing great progress with a dividend potentially starting in 2022. I think provided economic recovery continues in Greece & Europe, then with a bit of multiple expansion, a 15% annualised return for next few years is possible for this investment for Fairfax. If Eurobank averages 7.5% ROTBV over next 3 years (it was 7.7% for 1H21) , then ignoring dividends TBV would move from 1.40 to 1.73 over 3 years. Then if shares trade at 1.24 or 0.71 x TBV (a pretty modest multiple) in 3 years, then that would give us that 15% compounded return.

-

I just checked I believe any fair value marks/gains on these warrants up to 30 June have already been taken up by Fairfax in their consolidated earnings - so any gains will be for this current quarter.

-

viking I believe if the warrants were exercised at 8.05 per warrant then that should lower the carrying value/cost per share.

-

Would make sense to exercise the original 25 mil warrants with exercise price of $8.05 - so cost around $201 mil and shares trading at around $15 so now worth $375 mil plus they will now be able to scoop up a $12.5 mil div approx on those shares.

-

Just saw this article https://www.investmentexecutive.com/newspaper_/focus-on-products/values-time-to-shine/ Within the past six months, Simpson bought shares in Fairfax Financial Holdings Ltd., a company with interests in insurance and investment management. Simpson said the company has a solid balance sheet, good execution capabilities and the potential for healthy growth. Further, its insurance business will benefit from higher prices.

-

https://www.fitchratings.com/research/insurance/hurricane-ida-not-capital-event-for-louisiana-re-insurance-market-30-08-2021

-

thanks bearprowler6 interesting insights - well if any country was to benefit from foreign investment shifts resulting from China's regulatory mis-steps it would be India & Fairfax is long India. https://economictimes.indiatimes.com/tech/startups/more-fuel-for-indian-startups-as-global-capital-shifts-from-china/articleshow/85547173.cms

-

My view is 1.1 to 1.2 x BV so taking the mid-point - I am sitting on a fair value of around 1.15 x BV (noting that Fairfax's median P/B over the last 5 years was around 1.09) My assumptions here are - Fairfax can achieve a double digit avg compounded return on book at least in the 10-15% range (mid-point 12.5%) over time & - Fairfax's book value per share understates fair value ( for example - market value of non-insurance investments exceed carrying value by around US$29 at 30 Jun-21) Now if interest rates were to increase in a measured way, allowing higher fixed income returns possibly Fairfax could trade at even higher price/book levels as it has done historically but I am not assuming this will happen - it would just be a bonus.

-

I agree spekulatius that complexity is playing its part, Prem & Co are working harder on that front through better communication (look at Ar 2020 breakdown on their portfolio) as well as monetising assets which are otherwise hidden on their balance sheet.