glider3834

-

Posts

1,082 -

Joined

-

Last visited

-

Days Won

5

Content Type

Profiles

Forums

Events

Everything posted by glider3834

-

just on cat risk exposure - yes higher than Markel but I think Fairfax have been taking pro-active steps here worth talking about Cat losses were $1.3B In 2017 & that was 12.3% of net premium (adjusted to include a full year of premium from AWH) whereas in 2022, we had $1.3B in cat losses & it was 6.2% of net premium & they generated a $1.1B underwriting profit. To me that suggests while they have more than doubled their net premium earned, they are not growing their cat exposure. They also said they are keeping their cat exposure constant on a conference call, but its also good to see it reflected in the reported figures. Also Brit recently reported they are reducing their cat risk exposure & Brit was responsible for 50% of the Ian loss that drove 50% of cat loss in 2022. This hopefully will have a flow on impact for 2023 & going forward so maybe potentially cat loss to net premium earned could fall further. Also I wouldn't want FFH to completely do a u-turn on reinsurance business given the very hard market in 2023 & much more attractive reward on risk economics there now than in last 5 yrs. MKL looks like they have scaled back their property reinsurance business appetite too.

-

Good point luca investment income only includes dividends received - i havent looked at look through earnings for MKL or FFH but would be an interesting exercise for both

-

Just reviewing some of the earnings power components of Markel & Fairfax for 2022. MKL NPW $8.2B Underwriting Profit $626M Investment income $446M Markel Ventures Operating income $325M Fairfax NPW $22.2B Underwriting profit $1.1B (mgmt conservative projection $1B in 2023) Investment income $961M (mgmt expect $1.5B in 2023) Share of Profit of Associates $1B (mgmt conservative projection $0.5B in 2023) FFH has more non-controlling interests than Markel, just under 6% of net earnings in Q4 & so the above pre-tax figures need to be adjusted down for this. FFH's interest repayments are around 452M vs 196M for MKL It looks like FFH's income pre-tax (adjusting for interest exp & non-controlling interests) is approximately 84% higher than MKL . MKL mkt cap is $17.9B and FFH mkt cap is $16B With all my posts, I try to get the numbers right but please always double check my math (ie do your own due diligence) Cheers! (note also that FFH has more RSUs than MKL - I have ignored here as they are long-term & FFH is buying back in - but there is still a buyback cost here for FFH you might want to factor in)

-

I agree Viking - put another way FFH is on a forward 15% after tax yield - see Prem's comment Q4 call - name one other insurer globally thats trading that cheaply? I agree with @Parsad that all of us want FFH to continue to improve the quality of its equity investments/operating businesses & raise credit rating & cash at holdco. I think with holdco they are in full growth mode with the insurance ops while we are in a hard market & the insurance subs as hard market starts to ease, will be receiving this 1.5B in interest/div income etc - they will be in a stronger position with excess capital & they can dividend back to the holdco - holdco's cash will increase & holdco will be in position to buyback shares or add to equity/bond holdings or buy operating businesses. So its coming, we have to be patient but as a shareholder you want them to be expanding, taking advantage of this hard market while pricing is good. On quality of the underlying operating businesses - I don't mind if they own fractional shareholdings or wholly own subs - but agree we don;t want to see them allocating money to speculative start ups (like Farmers Edge) we want them to be investing in mature, cash generative operating businesses. Now I would argue the last 3 years supports the idea that they recognise this - if you look at their larger equity purchases they are well established, cash generative businesses and examples of recent additions Mytilineos, Kennedy Wilson, Atlas, Bank of America, Micron Technology, Grivalia Hospitality, Recipe - none of these are speculative, start ups. Also I think there has been organic improvement with quality of underlying operations eg two examples Eurobank & Stelco - if you go back 3-5 years & compare to now - quality of underlying business has been raised a lot due to management.

-

I would be curious if anyone has crunched the numbers on Berkshire's actual underwriting record since inception? I found this in 2021 annual report

-

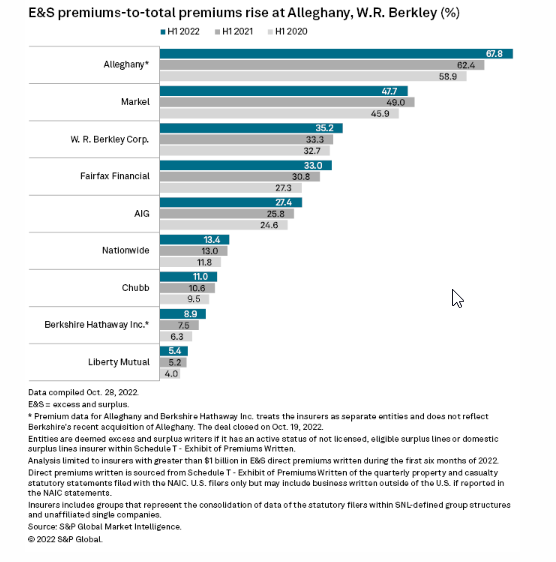

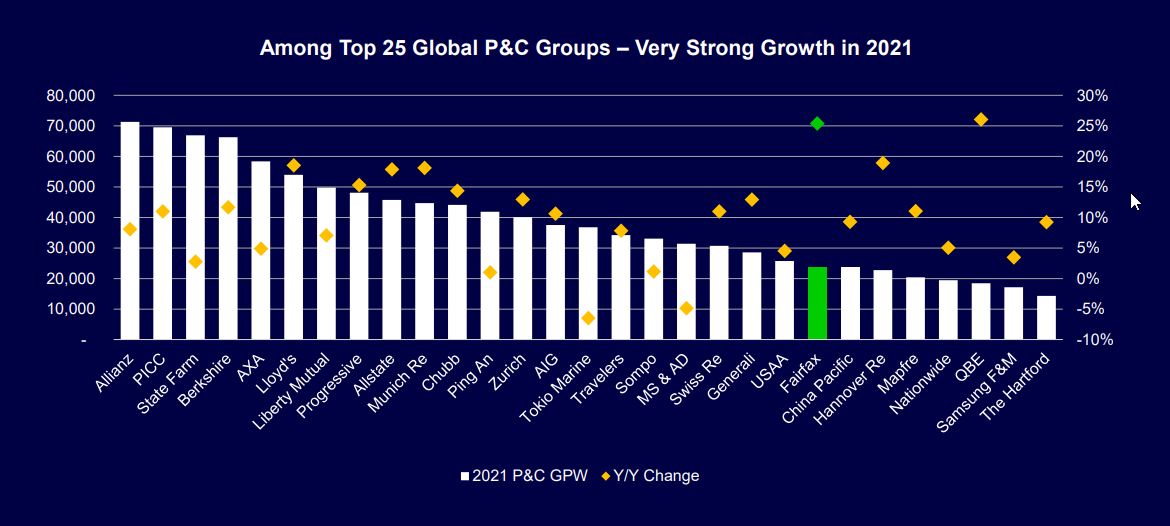

If you look at Berkshire's insurance business versus Fairfax I think there are some big differences - by product line & by growth profile- with geography (this is a little harder to determine so feel free to chime in)- but overall not a straight apples/apples comparison. Looking at Berkshire 2021 premium written Reinsurance - global - 29% Insurance - private passenger auto (US)/Geico - primary- 54% & - Commercial (primary & specialty) - 17% So I would say the rate/growth dynamics in the US private passenger auto insurance markets in US and the reinsurance markets globally are significant drivers for Berkshire's underwriting results. For Fairfax, the GPW split is around 76% insurance and 24% reinsurance. So Fairfax's reinsurance business appears smaller as a percentage of Fairfax's total written premium versus Berkshires. Also Fairfax has grown significantly in E&S/specialty - according to S&P, around 31-33% of Fairfax's total direct premiums written is E&S versus 7.5% to 9% for Berkshire before taking into account Alleghany acquisition which will lift this percentage. Then you have the premium growth profile - Berkshire is a lot larger, more mature - its growing GPW at a slower rate than Fairfax - the underwriting profit growth is a function of both combined ratio & the rate of net earned premium growth.

-

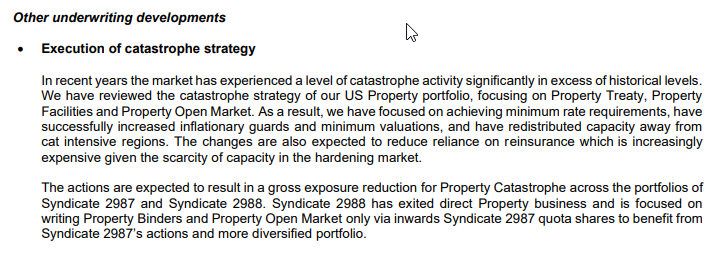

Brit are reducing their exposure to cat intensive areas of US property - around 50% of Fairfax's cat losses from hurricanes Ian (2022) and Ida (2021) were at Brit - so I view this as a positive move.

-

cheers!

-

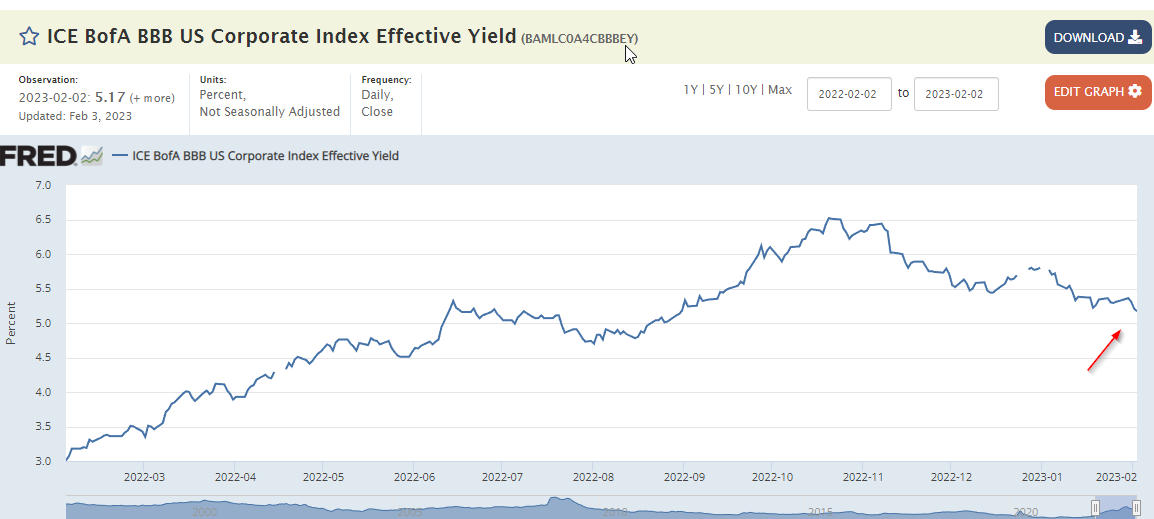

Just on this fixed income debate regarding whether Fairfax should push out duration to lock in extra yield. My view is they are focused on total return which includes capital gains plus yield. If economy deteriorates or for some other reason, and Fed forced to cut rates - rates (US1y,2y etc)would drop and treasury prices would increase -depending on size of these rate cuts, potentially Fairfax could go from an unrealised loss to unrealised capital gain position? Also I am not a bond expert so please someone correct me if I am wrong! But wouldn't the shorter end treasuries see the larger price (& capital gain) increases over longer end treasuries? So they could potentially sell their treasuries & realise capital gains, like they did in 2008 From 2008 AR Also, as the yield on long (30-year) U.S. Treasuries began to drop below 3%, we sold almost all our U.S. Treasuries (at year-end we had only $985 million left, compared to $6.4 billion on December 31, 2007), having realized net gains of $583 million in 2008 on sales of U.S. Treasuries....Our U.S. Treasury bond position was to a large extent replaced by $4.1 billion in U.S. state, municipal and other tax-exempt bonds (of which $3.6 billion carry a Berkshire Hathaway guarantee) with an average yield (at purchase) of approximately 5.79% per annum. The interest income may not necessarily then be lost if they re-deploy those treasury proceeds into higher yielding parts of the credit market plus they realise capital gains - again like they did in 2008. So I am just speculating here, no-one knows for sure what will transpire. Prem indicated on Q4 call they are currently pushing duration now closer to 2 years. My view is they are looking to capture some extra duration, but they want to stay nimble - corporate bonds are a big question mark for me at the moment - credit spreads look low yet a lot of refinancing still to come, already signs of problems in commercial real estate bonds https://finance.yahoo.com/news/commercial-property-market-freezes-bond-180729652.html https://www.afr.com/property/commercial/investors-seek-to-pull-20b-from-core-real-estate-funds-20230201-p5ch5f One other important point is IFRS 17, this impacts how they manage the fixed income side - I am hoping in the AR they will lay out some more details of the impact - but I also need to re-listen to Q4 call where they went into some details.

-

I just wanted to post an update on the contingent value rights (CVR) that Fairfax potentially will have(subject to Ambridge/Resolute deals closing) - these may be worth something or nothing, but they are not potentially inconsequential either. I am not sure what the state of the CVR is for the Riverstone Barbados transaction, because I can't see any update on that. Here is my list Fairfax - Contingent value rights Riverstone – up to $235.7 mil (Riverstone Barbados sale - based on performance targets) ‘On closing the company expects to receive proceeds of approximately $730 for its 60.0% joint venture interest in RiverStone Barbados and a contingent value instrument for potential future proceeds of up to $235.7’ (AR 2020) Davos Brands - up to $36 mil (based on brand performance of Aviation Gin over next 10 yrs) In 2016 we invested $50 million into Davos Brands (a spirit company) for a 36% interest alongside David Sokol. In September 2020 the company was sold to Diageo: our cash proceeds were $59 million and we are eligible to receive additional consideration of up to $36 million, contingent on the brand performance over the next ten years. (AR 2020) Ambridge - up to $100 mil (Ambridge Group sale - based on performance targets) On January 7, 2023 Brit entered into an agreement to sell Ambridge Group, its Managing General Underwriter operations, to Amynta Group. The company will receive approximately $400 million on closing, comprised principally of cash of $275 million and a promissory note of approximately $125 million. An additional $100 million may be receivable based on 2023 performance targets of Ambridge. Resolute Forest Products – up to $200M (potential refund of total lumber duty deposits – calc US$500M x 40% Fairfax stake = $200M The transaction will be carried out by way of a merger between Resolute and a newly created subsidiary of Domtar, providing for conversion of each share of Resolute common stock into the right to receive US$20.50 per share, together with one CVR, entitling the holder to a share of future softwood lumber duty deposit refunds. Under the CVR, stockholders will receive any refunds on approximately US$500 million of deposits on estimated softwood lumber duties paid by Resolute through June 30, 2022, including any interest thereon, net of certain expenses and of applicable tax and withholding.

-

article on the Keg https://www.richmond-news.com/hospitality-marketing-tourism/dine-out-vancouvers-business-bump-helps-wary-restaurant-owners-6500823 'Fairfax Financial fully owns the Keg restaurant chain thanks to it buying Recipe Unlimited Corp. in a deal that closed in October. "These days you're inundated with cautious news," Aisenstat said. "There's inflation, interest rates – all that stuff. If you're looking for something to be nervous about, in the restaurant business it's pretty easy to find it, but so far nothing [bad] has materialized, really. Fall was great. January is better than we would have expected." Aisenstat said things are also going very well at other restaurants, where he has ownership stakes.'

-

So if Q4 report shows more of the same - basically continuing a high quality bond/credit allocation but still pushing duration out more - US & CAN treasuries at 2 yrs etc - that won't surprise me. They have been doing some high yield deals too https://www.lse.co.uk/news/duke-royalty-upgrades-credit-facility-to-gbp100-million-until-2028-qdy9ut7qebkhk5b.html

-

SJ good points. My thought in 2023 was with a recession, they could start to transition from a short duration Treasury position to investing more in corporates at higher spreads, but its interesting corp spread over treasuries has been tightening over last 4 mths https://www.barrons.com/articles/high-quality-bonds-defaults-junk-51674769295

-

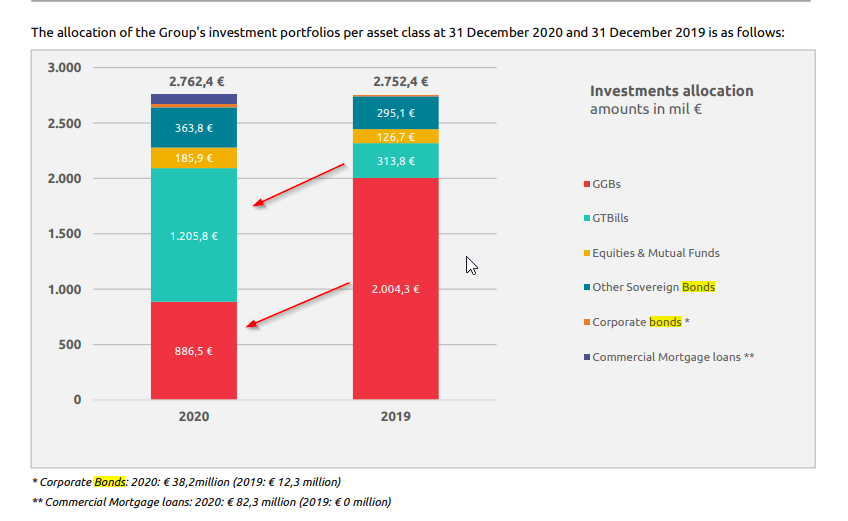

SJ I would agree in terms of being conservative as an investor & thinking about BV impact, assume they hold to maturity & those unrealised losses will reverse. At same time, we know HWIC are very active, value, bond managers who focus on total return ie investment gains not just yield eg When Greek bond yields went from 8% to 1%, they realised gains over 300mil euro over 2019-2021 - selling Greek Govt bonds & re-distributing into Greek T Bills etc. That one investment move has probably driven a big chunk their return on Eurolife FFH investment. IMHO I think there is 'alpha' in Fairfax's fixed income investment team that should be factored into their P/B multiple. Hamblin Watsa's 5,10 & 15 years record versus benchmark was last published in 2017 (see below) , so I am hoping there might be an update in the 2022 annual return.

-

Fairfax recently raised its position in Mytilineos - MYTIL.AT - on fully converted basis they will have around 9.2M shares = approx $230M position https://www.mytilineos.gr/news/company-news/fairfax-becomes-the-2nd-largest-shareholder-in-mytilineos/ And their reported results look decent https://www.ekathimerini.com/economy/1190127/mytilineos-sees-net-profit-turnover-more-than-double/

-

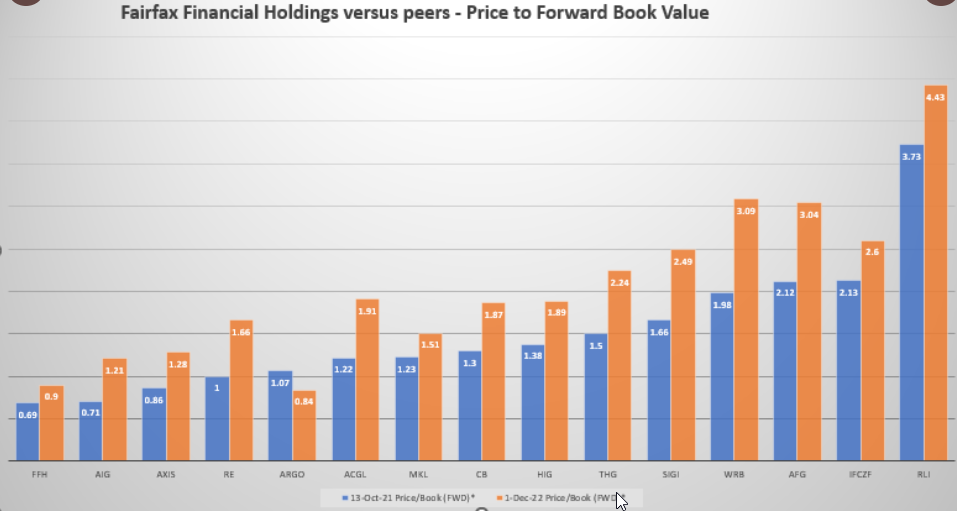

I did this chart benchmarking FFH against peers using seekingalpha data but please do your own due diligence - it was done 1 Dec-22 so bit outdated but it shows how P/B multiples have expanded likely due to interest rates - FFH's peer group median P/B was 1.8x. FFH's P/B was 0.9x at the time but probably closer to 1.0x now. BRK's p/b looks to be around 1.5x. I think the challenge for BRK in terms of forward ROE is just BRK's sheer size. A 1% increase in BVPS for Fairfax is 155M & for Berkshire its around 4.6B. Berkshire size means fewer investment options to pick from that can move the needle which impacts ROE potential.

-

that makes sense cheers!

-

thanks @SafetyinNumbers thats interesting - so potentially there is a broker &/or counterparties out there with 1.96M shares of FFH. I looked at substantial shareholder filings - I couldn't see any disclosure for this quantity of shares - I wonder if they need to disclose if the beneficial interest in the TRS effectively lies with FFH not with the broker. Another thought, a risk with a TRS would be that if there is an increase in interest rates, the receiver (Fairfax) of the swap has to pay much higher interest payments to the total return payer. But when you think about it, higher interest rates benefit insurers through higher interest income & even more so insurers (like Fairfax) that are short duration on their fixed income portfolio. And higher interest income also increases probability of higher share price so TRS appreciates. So Fairfax's strategy of short duration fixed income portfolio to benefit from higher rates plus the TRS swap are actually working hand in hand - Fairfax essentially was minimising interest rate risk on this TRS & in fact seeking to capitalise on higher rates. And if interest rates had stayed really low, Fairfax would have had to pay little to hold the TRS.

-

yes @SafetyinNumbers if you could layout how these things are usually structured that would be great because details from Fairfax are limited - Peter Clarke said they have renewed for a few years, it sounds like there are renewal clauses built in - but what if the counterparty effectively short wants to exit - would the IB then just look for other investors who are interested in replacing them? Another related question is if there are 1.96M shares sitting somewhere as part of this swap, can Fairfax in closing swap make some sort of repurchase agreement with counterparty perhaps for a partial buyback equal to their gains on the swap? or is the whole thing synthetic with no shares involved? Apologies if my questions sound stupid.

-

-

Yes agree I think the role has shifted from Investment focus to Insurance business focus & I would say the optimisation of Fairfax's insurance businesses has been a focus over the last 12 mths given Ambridge & C&F pet sales as examples - I think Peter Clarke has actuarial background & is go to person on conference calls on any questions relating to insurance business. So I think the role has a central focus being Strategy for Insurance business but also with a 'seat' at the Investment Committee as every decision in Fairfax needs to be considered first & foremost looking at its impact on the insurance business. Peter Clarke looks to be bridging both the investment team & the insurance operations. These profit centres also facilitate transparency when Andy Barnard and Peter Clarke monitor the insurance operations. We now have a small investment committee consisting of Roger Lace, Brian Bradstreet, Wade Burton, Lawrence Chin, Chandran Ratnaswami, Quinn McLean, Peter Clarke and me that reviews large investments, asset mix, regulatory requirements and performance

-

https://www.reinsurancene.ws/storm-elliott-to-have-limited-impact-on-lloyds-syndicates-argenta/

-

cheers good pick up Ambridge Partners LLC, our New York based MGA, generated $420.8m of premium for Brit (2020: Ambridge and BGSU combined: $317.5m). This reflects the increase in corporate transactional activity which was impacted in 2020 COVID-19 and other factors such as Brexit uncertainty. The remodelled BGSU portfolio, now rebranded Ambridge Specialty Casualty and Ambridge Re

-

Looks like they bought original 50% stake for $28.6M - so $75.2M original cost On December 9, 2015 Brit completed the acquisition of a 50% ownership interest in Ambridge Partners for $28.6.

-

Fairfax Top 10 Events of the Year - Driving Shareholder Value

glider3834 replied to Viking's topic in Fairfax Financial

Cheers viking - you too! Yes i was surprised it was $2B as well - i think that strategic shift to protect their Bal Sheet by adopting a high cash/ST invest weighting strategy ala Berkshire really set them up in 2022 and hopefully in 2023 to play offense.