glider3834

-

Posts

1,019 -

Joined

-

Last visited

-

Days Won

4

Content Type

Profiles

Forums

Events

Everything posted by glider3834

-

https://www.business-standard.com/finance/personal-finance/digit-life-enters-insurance-space-with-maiden-product-group-term-plan-123062600546_1.html

-

National Stock Exchange of India (NSE) - unlisted market transactions are suggesting valuation around US$20B - on that basis Fairfax India 1% stake would be worth around US$200M - timing of IPO still unclear https://www.livemint.com/market/ipo/nse-ipo-creates-buzz-in-unlisted-market-shows-the-investor-interest-in-issue-11687254813352.html 'The current share price in the unlisted market values the bourse at around ₹1,65,825 crore.' “At this price, the PE Ratio of the bourse stands at roughly 22 times on historical basis versus BSE Ltd at 37 times and MCX at 50 times and international exchanges trading between 30x to 40x," the brokerage report said.

-

check out Lauren Templeton comments on Fairfax culture from 16 min 20 s mark

-

thanks - yes exciting news - can they scale rapidly? they have built Digit's brand recognition in India, they have built a partner ecosystem, already have API integrations (couldn't they use these to distribute life products on top of existing non-life?), they have also onboarded banks as minority shareholders/partners for distribution capability using bancassurance model, Kamesh Goyal has experience in life insurance with Allianz - nothing is certain of course but the ingredients look to be there IMHO this was interesting interview covering how they have used tech (AI,ML)/analytics to lower costs, scale quickly, reduce claim time/ improve customer experience 'Technology is the backbone of Digit and ever since our inception in 2017, we have developed multiple tech-enabled solutions that have accelerated our growth in a short span of time. The use of Big Data for business intelligence and data analytics has helped us close the gap between data, insights, and actionable solutions. This has also helped us in being more cost-efficient. We believe in a hybrid model of AI, analytics and human assessment to constantly improve the processes for our customers and partners. We have built ‘smartphone-enabled inspections’ for instant motor insurance pre-inspection using AI and ML. This has eliminated the need for inspection by physical surveyors and has made the process efficient by bringing down the turnaround time from a few days to a matter of 5-10 minutes. Our team is working constantly to make these solutions active for the entire userbase. We also have a system that helps us in detecting frauds through the use of image analytics, AI, and ML. Our integrated API solutions on the cloud help in triggering automatic claim notifications for travel insurance customers if their flight gets delayed beyond 90 minutes. Our tech solutions have also been built for our partner ecosystem to help serve the customers better. The reception of tech integrated solutions has been phenomenal and has helped Digit gain an edge over other players in a short span of time.' https://www.analyticsinsight.net/exclusive-interview-with-vishal-shah-head-of-data-science-at-digit-insurance/

-

yeh comparing health & liability numbers for April maybe there has been some re-categorisation but not sure - I guess we wait for May to see if there is some trend here

-

variant perception - how do you get yours?

glider3834 replied to glider3834's topic in General Discussion

Right so like looking from customer perspective - why are they buying the product or using the service? -

I am always thinking about how can I make my research process better? I am curious to ask if other members of cobf forum would like to share experiences of how they have gone about picking up different pieces of information to gain a unique perspective on stocks that may run counter to the existing narratives that are being pitched on different media outlets. Here is a quote from an interview with Ted Weschler at Berkshire https://kingswell.substack.com/p/ted-weschler-variant-perception-charity “I want to be able to look myself in the mirror and say that I’m reading enough weird stuff that nobody else is reading the same stuff that I am,” he says. “If you’re just reading the New York Times and the Wall Street Journal, there’s no way you’re going to beat other people.” Even so, Weschler makes a point to read as many newspapers and trade journals as possible. Newspapers, in particular, present readers with a random set of stories, curated by editors, that make for a well-rounded reader. It’s all about building up a critical mass of information and data that will help you connect the dots when examining a potential investment idea. “I read Furniture Today and Uranium Weekly,” Weschler laughs. “I’m not sure there’s a lot of people who subscribe to both of those, but you’re looking at one of them.” In the insurance space, some of the things I read https://www.reinsurancene.ws/ https://www.insidepandc.com/ https://www.theinsurer.com/ https://www.ajg.com/gallagherre/news-and-insights/ I also try & push my knowledge completely outside my comfort zone - I watched a Netflix series that was super interesting on understanding black holes & I don't want to spoil the show you might want to watch - but it underlines that to get the answer to a difficult problem, you may need to take a unique research approach that no-one else may have pursued.

-

Milk puts (like other agri product derivatives) i think would be related to insurance business eg protection sold to dairy farmers example below from Hudson crop insurance site 'Dairy Revenue Protection (DRP) is an insurance plan approved by the Federal Crop Insurance Corporation to allow dairy farmers to purchase risk management protection against declines in quarterly revenue from milk sales as a result of a decline in milk prices, a decline in milk production, or both.' https://hudsoncrop.com/products/drp/

-

no worries

-

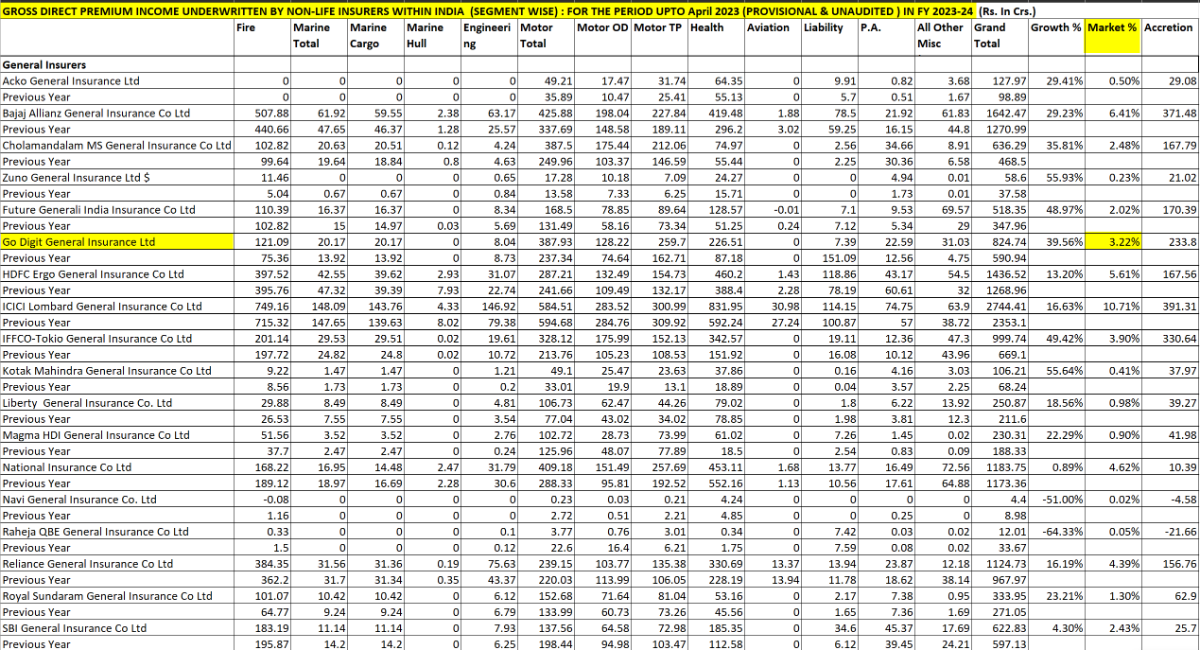

Digit market share up to 3.2% Apr-23 - YoY growth rate 39.6% https://www.gicouncil.in/statistics/industry-statistics/segment-wise-report-on-homepage/

-

happy to join in - I like the idea of maybe inviting a few special guests similar to the FFH pre-AGM dinner format

-

Worth considering loan mix (skew to residential multi-family/student housing) and completion guarantees in addition to the LTV All of the Loans are secured by real property located in the United States with an average loan-to-value ratio of approximately 51% and are supported by completion guarantees issued by the project equity sponsors. More than 70% of the Loans relate to multifamily or student housing development projects with the balance being a mix of industrial, hotel and life science office property development projects.

-

Just realised I didn't factor in estimate for minority interests share of pre-tax income in above table - so now factoring this in, results in my new estimate for CAGR for pre-tax income growth per common share at 14% over last 9 yrs

-

Rate the overall quality of the management team at Fairfax

glider3834 replied to Viking's topic in Fairfax Financial

Northbridge is also rated as a top insurance employer in 2022 https://www.insurancebusinessmag.com/ca/best-insurance/top-insurance-employers-2022-427797.aspx#winnersListSection

-

Rate the overall quality of the management team at Fairfax

glider3834 replied to Viking's topic in Fairfax Financial

@VikingI thought this was an interesting stat from C&F website which provides current employee perspective on management 'In 2022, 93% of C&F’s nearly 2,500 U.S. employees participating in the survey said the company is a great place to work - 36 percentage points higher than the average U.S. company.' https://www.cfins.com/ -

https://www.theglobeandmail.com/business/industry-news/energy-and-resources/article-canada-alberta-solar-farm-mytilineos/ 'One of Greece’s top industrial and power companies is launching a $1.7-billion solar-energy project in Alberta that it says will be the largest of its kind in Canada.' 'Mytilineos is backed by Toronto’s Fairfax Financial Holdings Ltd., led by Prem Watsa, which first bought into the Greek company in 2012 and has since increased its ownership to 4.7 per cent, making it the second-biggest shareholder, after Mr. Mytilineos, who owns 27 per cent. Fairfax has an option to take its ownership to 6.4 per cent.'

-

Just looking at this quote above from Morningstar. Based on my estimates, over last 9 years (2013-2022) - Operating Income has grown at 14% CAGR - Pre-tax operating income (before investment gains) per share has grown 15% CAGR Pre-tax Operating Income (excluding investment gains) as a percentage of Common Shareholder Equity (start of period) was 15% in 2022 (versus 7% in 2013). If we are looking at what sort of ROE or BVPS growth rate Fairfax can sustain going forward, IMHO I would look to pre-tax operating income (excluding investment gains) as a key driver. If you then consider over 50% of Fairfax's BVPS growth rate since inception has come from investment gains, it doesn't seem unreasonable to expect a positive number here when measured over longer periods. (Table below I put together from 2013 & 2022 Annual reports) Also please always do your own due diligence & don't just rely on my figures. Thanks!

-

sorry viking I am not sure what they mean by value is that the total build cost/gross asset value before factoring in debt etc?

-

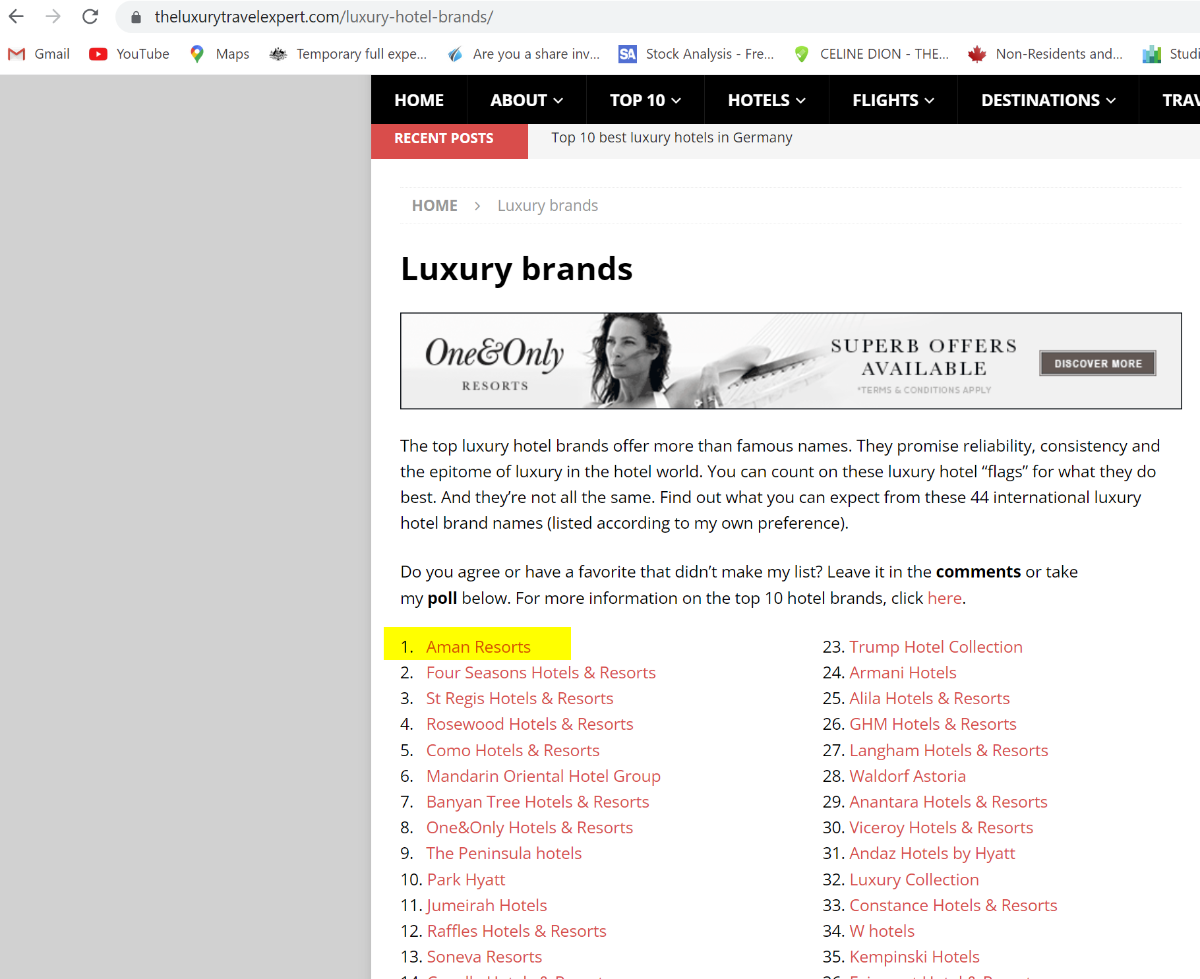

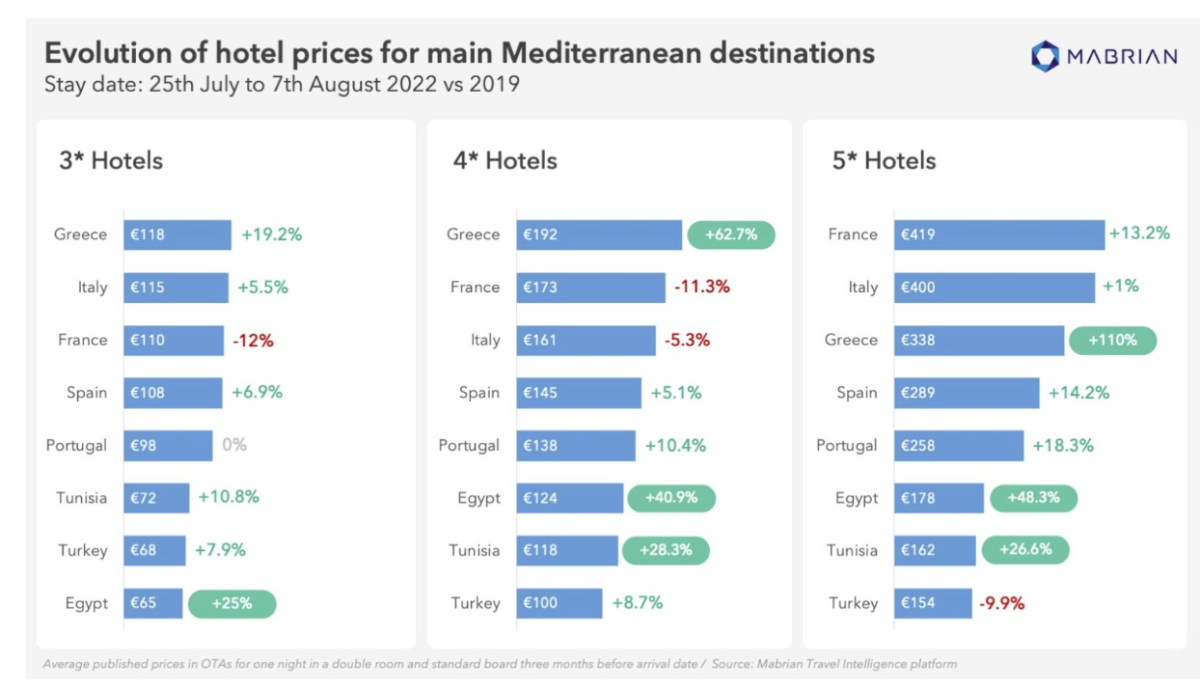

@Viking so this video below has terrible sound quality but from 27-32 min mark - George outlines their investment thesis on going after ultra luxury branded segment with Grivalia Hospitality - he talked about (in my words from memory not his) - Greece attractive tourist destination (natural beauty etc) - Greece has a shortage of genuine 5 star hotels (even though hotels might call themselves 5 star they are not genuine 5 star hotels by international standards) - a lot of hotels a family owned etc - lack of brand name luxury hotels in Greece like Aman, Mandarin etc - one of reasons you would build rather than buy hotel is that for luxury hotel guests need to have space etc - so existing hotels wouldn't be suitable in most cases - construction costs have gone up a lot but there is still attractive return even after factoring higher building costs https://www.youtube.com/watch?v=lRuZ2HXam-A Also I did some digging, according to this website https://theluxurytravelexpert.com/ the Aman Resorts are rated the number 1 luxury hotel brand in the world (if you are an ordinary person like you me you probably never heard of them! :)) The Amanzoe Resort owned by Grivalia is run by Aman Resorts & is rated (by same website) the best hotel in Greece https://theluxurytravelexpert.com/2020/10/12/best-hotels-greece/ & in Europe's top 10 https://theluxurytravelexpert.com/2021/07/08/top-10-best-beach-resorts-europe/ Now with Amanzoe, Grivalia didn't build it, they bought it in 2018 at a total EV (mostly consisting of debt) of 116M euro. https://markets.ft.com/data/announce/detail?dockey=1323-13740636-74QQ05NEK6U4F5D19IU8MDVHUB From what I can tell it cost the original owner over 100M euro to build it so it looks like they bought potentially close to its build price. Its unclear what its current EBITDA & valuation would be now & also what GH has spent on the property but given Greece 5 star hotel room prices are up 110% over 2019 to 2022 period, you would think that would be likely positive driver of Amanzoe's valuation & another factor maybe behind GH push in the 5 star space. https://greekreporter.com/2022/06/30/5-star-hotel-rooms-greece-rise/

-

Just having another look at this - AIG are paying a dividend out of Validus re prior to close so thats included in transaction value , but from M&A perspective this sale of Validus Re is priced at 1.4 x tangible BV & 1.1 x GPW of $2.7B in 2022 with 95 combined ratio 'Total consideration for the transaction is $2.985 billion, equal to 1.42x Validus' tangible equity of $2.1 billion to be delivered to RNR at closing, with any excess to be retained by AIG.' https://www.fitchratings.com/research/insurance/fitch-affirms-renaissanncere-ratings-following-validus-re-acquisition-announcement-outlook-stable-23-05-2023 The expected property GPW of the company will be approximately $900 million. For casualty and specialty, GPW is expected to be roughly $1.8 billion, with RenRe stating that the combined ratio will be in line with the existing portfolio, at around 95%. https://www.reinsurancene.ws/renres-gpw-poised-to-expand-by-30-to-12bn-following-validus-re-acquisition/ Worth noting too that Validus Re increased premiums by 40% in Q1'23 so that likely would be factored in too https://www.reinsurancene.ws/validus-re-premiums-up-40-significant-rate-increases-expected-in-june-aig-ceo-zaffino/ In addition, AIG will retain 95% of the development on Validus Re’s net reserves at closing, mitigating RenaissanceRe’s balance sheet risk. https://www.reinsurancene.ws/moodys-affirms-a-stable-outlook-for-renre-post-acquisition-of-aigs-validus-re/

-

I stand corrected thanks for the pick up!

-

BIAL passenger traffic 3.2M in Apr-23 vs 2.7M in 2019 (up 17%) domestic 2.86M vs 2.32M in 2019 (up 23%) international 0.35M vs 0.42M in 2019 (down 17%) https://www.aai.aero/sites/default/files/traffic-news/Apr2k23Annex3.pdf all-time record for BIAL in total passenger volume, but international still recovering post covid - running at 83% of 2019 levels international passengers are higher spending (on shopping/duty free etc) than domestic & they pay higher tariff rate, so if they can increase international passenger volume further with T2 up & running - this will be important from a margin perspective.

-

They recently announced looking to buy up to 10% of BIAL - so I think their strategy is to increase rather than reduce their BIAL ownership & then hopefully IPO at a more favourable valuation later on.

-

yes increases likelihood with a second round vote PM & ND will have an outright majority (courtesy of the bonus seats) to govern for another 4 year term and won't be forced to partner with a coalition partner that may not be on the same page. So I think that will be a positive from rating agencies viewpoint and for all investors in Greece . I am pleased for the Greek people too - they have an excellent PM who has done a lot for the country.

-

Grivalia Hospitality Grivalia appears to have had operating loss in Q1'23 but it looks like they are still in build out phase - they are aiming for completion on three projects According to Chryssikos, the third (three?) projects under construction will open as pilot operations very soon; Avantmar in June; the Glyfada project in early August; and the Voula Project in early 2024. but have additional ones planned, so I assume once they ramp up there would be revenue contribution there. https://www.ekathimerini.com/economy/1210801/aiming-for-wealthy-guests/ 'For the Grivalia CEO, there is a great market for 5- and 6-star resorts in Greece. Demand is high and, so far, supply is low. And the targeted cliented is high value: people with considerable disposable income who are going to spend large sums that will benefit the whole tourism ecosystem.'