Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

@dartmonkey, I am not following you. Fairfax’s carrying value captures all the accounting pieces. Fair value captures the change in the share price. The difference is excess of FV over CV… That pre-tax number is not captured in EPS, ROE or BVPS. How is it double counting? I think there are two ways to think about hidden value: Incorporate it into past results. Incorporate it into future results. As @SafetyinNumbers has pointed out, what approach you take will impact ROE (past or future). I prefer to incorporate it into future results (will allow Fairfax to generate a higher future ROE). My guess is most people ignore it. This approach seems bizarre to me. (Ignoring facts in ones analysis.) —————- 5.25 years ago, excess of FV over CV was a minus $660 million. Fairfax was starting in a big hole. Over the past 5.25 years, the accounting returns they have generated on their investments has been stellar. Fast forward to today. Excess of FV over CV has blown out to $3.9 billion, a swing of $4.56 billion. This is a new source of future earnings for Fairfax - in addition to the usual sources.

-

@gfp, thanks for brining this forward. Two things come to mind for me: Fairfax is not going to nail every one of their investments. Having said that, their ‘hit’ rate over the past 6 years has been outstanding. Especially with the large investments (Eurobank, Poseidon, FFH-TRS, BIAL, Orla, Stelco etc). Bottom line shareholders have been spoiled. To evaluate management on a sale, we need to know what the proceeds were used for. If the proceeds were used to buy back stock below book value or to invest in Orla… that matters. I do not expect Fairfax to continue to do as well with their investments over the next 5 years as they have over the past 5. I think they will do better than average moving forward, so I am not concerned. Rather, I am trying to keep my expectations reasonable.

-

@Maverick47, if I am understanding you correctly… I think you are referencing another source of hidden value: Fairfax’s fair value marks for their non-market traded consolidated holdings. For these holdings it is the same as their carrying value. This is another bucket of holdings that have increased materially in size over the past 5 years. Fairfax India is another one. It is included in excess of FV over CV. But the FV is comically low (Fairfax India’s share price). We know economic/intrinsic value of this holding is much higher than its share price (with BIAL being the primary reason). Bottom line, hidden value is growing in all sorts of places. Importantly, it compounds over time.

-

Hidden Value Fairfax has been transformed over the past five years. The accounting results clearly show it: record EPS, high-teen ROE, and best-in-class growth in BVPS among P/C insurance peers. But the accounting results tell only part of the story. Much more has been happening under the hood at Fairfax that has not been captured in reported earnings or book value. As a result, the increase in Fairfax’s economic/intrinsic value over the past five years has been far greater than the accounting results suggest. We refer to this growing gap between economic value and accounting value as hidden value. That is the focus of this post. Hidden Value Hidden value exists throughout Fairfax — across both its insurance operations and investment holdings. This leads to two important questions: How big is it? What is the trend? Is it growing? The answers help investors better understand Fairfax’s past performance, current positioning, and future prospects. The challenge is that hidden value is a broad and complicated topic. Some sources are relatively easy to identify and measure; others are much more nuanced. So, it makes sense to break the analysis into smaller pieces and begin with the easier ones. Today, we will focus on one important component of hidden value: Excess of FV over CV Fairfax provides investors with valuable disclosure regarding one of its most important sources of hidden value: the excess of fair value (FV) over carrying value (CV) for non-insurance associates and market-traded consolidated holdings. Associate Holdings These are investments where Fairfax typically owns 20%–50% and exercises significant influence, but not control. Examples include: Eurobank Poseidon (Atlas/Seaspan) EXCO Resources Waterous Energy Fund III Market Traded Consolidated Holdings These are holdings where Fairfax owns more than 50% and controls the business. Examples include: Fairfax India Thomas Cook India Dexterra AGT Food & Ingredients How the Accounting Works Associate Holdings Associate investments are generally accounted for using the equity method under IFRS (IAS 28). This differs significantly from ordinary public equity holdings. At acquisition — or when ownership rises above 20% — the investment is initially recorded at purchase price. After that, carrying value changes based on: Share of earnings → increases carrying value Dividends received → reduce carrying value OCI adjustments → FX, pensions, etc. Impairments → permanent write-downs Importantly, associates are not marked to market each quarter. As a result, carrying value largely reflects: Original cost Plus retained earnings over time Minus dividends This differs sharply from ordinary public equities, where balance sheet values are regularly adjusted to current market prices. For public equities: Fair value ≈ carrying value For associates: Fair value can become materially higher than carrying value Especially when: Earnings quality improves Valuation multiples expand Businesses compound over long periods of time This is one reason companies like Fairfax Financial Holdings and Berkshire Hathaway can develop substantial hidden value over time. Market-Traded Consolidated Holdings Market-traded consolidated holdings create similar economic dynamics, although the accounting treatment differs. When Fairfax controls a business, it consolidates 100% of the subsidiary’s assets, liabilities, revenue, and expenses onto its financial statements. At acquisition: Assets and liabilities are recorded at fair value Excess purchase price becomes goodwill Over time, carrying value changes through: Retained earnings Dividends OCI adjustments FX movements Impairments Like associates, these businesses are not marked to market each quarter simply because they are publicly traded. As a result: Accounting values remain largely historical Internally generated intangible value is often not recognized Goodwill generally remains static unless impaired Over time, market value can diverge materially from carrying value. Calculating Hidden Value For associate and market-traded consolidated holdings, hidden value can be estimated by comparing fair value to carrying value. Importantly, Fairfax does this work for investors each quarter. Excess of FV over CV: Size and Growth At March 31, 2026, Fairfax’s associate and market-traded consolidated holdings had a fair value of approximately $12.8 billion. This represented about 45% of Fairfax’s total equity portfolio of ~$29 billion — a very significant portion of the company’s equity investments. Here is where the story gets interesting. The carrying value of these holdings was only $8.9 billion — the amount reflected in shareholders’ equity. The difference was approximately: $3.9 billion Or about $176 per diluted share (pre-tax) That is hidden value. Growth This bucket of holdings has grown dramatically over the past 5.25 years. Carrying value increased 79% Fair value increased 197% As a result, the excess of FV over CV surged: From negative $663 million at December 31, 2020 To positive $3.9 billion at March 31, 2026 That is an increase of approximately $4.6 billion, or an average of $873 million per year. This represents a significant amount of value creation that has not been captured in reported EPS, ROE, or BVPS. The key takeaway: Fairfax’s economic performance over the past five years has been materially better than the accounting results indicate. Book value today understates economic value by a meaningful amount. Summary Excess of FV over CV for associate and market-traded consolidated holdings is an important and rapidly growing source of hidden value at Fairfax. How big is it? Approximately $3.9 billion What is the trend? Growing at roughly $873 million per year over the past 5.25 years Fairfax itself highlights the importance of this metric. From the company’s quarterly disclosure: “Excess (deficiency) of fair value over carrying value – These pre-tax amounts, while not included in the calculation of book value per basic share, are regularly reviewed by management as an indicator of investment performance for the company's non-insurance associates and market traded consolidated non-insurance subsidiaries that are considered to be portfolio investments…” Fairfax effectively provides investors with a roadmap. The message is clear: book value and reported earnings alone are no longer sufficient to fully understand Fairfax’s economic performance. And this is only one example of hidden value. Additional sources remain embedded throughout Fairfax’s insurance operations, investment holdings, and capital allocation activities. Investors who ignore them risk materially understating the company’s intrinsic value. Future topics to explore include: What is driving the rapid growth in hidden value? Will this value eventually be realized? Or will it remain hidden? How should investors think about hidden value when valuing Fairfax?

-

@gfp, this is an important topic for Fairfax shareholders/investors. As you have laid out above, conservative reserving practices is another example of hidden value. Fairfax’s insurance business is also much larger today than it was 10 years ago. As the reserves are released in the coming years it will likely be a large and important tailwind to underwriting profit and earnings. My guess is Mr Market will not factor conservative reserving practices into their valuation models. It does provide shareholders with an additional margin of safety. I am still thinking about how to incorporate all the different (and substantial) sources of hidden value into how I model/understand and value Fairfax. Currently, I like to think of them primarily as ‘locked and loaded’ future income streams (in addition to all the regular ones). Some, like conservative reserving, will boost underwriting profit. Others, like excess of FV over CV will boost investment gains. The amount and the timing can be estimated - using a two or three year rolling average. Which shouldn’t be a problem for an investor. Lots of analysts will struggle (as it will be impossible to estimate the exact amount each quarter or year). What has happened with hidden value (the sources and amounts/growth) - both in insurance and investments - is another really good example of how much Fairfax has been transformed over the past 5 years. BVPS is losing its relevance as a valuation and performance measure.

-

@djokovic1, I agree - time frame is key. I also use a 5 year time frame when I look at Fairfax. Through that lens there is lots to like about the stock price/valuation today. But I do think investors will get tested (even from the low current valuation level). When the next bear market hits my guess is Fairfax will get hit (and likely harder than the market averages). At some point, +$100 oil is going to matter to financial markets - so the next bear market might be right around the next corner. Of course, exploiting volatility is one of Fairfax's superpowers. Investors won't care (if history is any guide). In fact, it will be the opposite (most investors view volatility as a terrible thing - especially for Fairfax). Fairfax is such an interesting investment because the gap between perception (narrative) and reality (fundamentals/actual business model) is so large. During times of market weakness (when fear grips markets) the gap widens. This has been largely true for Fairfax through most of the company's history. The reality is Fairfax makes many of their great (needle moving) investments in bear markets. My guess is that will continue... and most "investors" won't care. It is so counterintuitive.

-

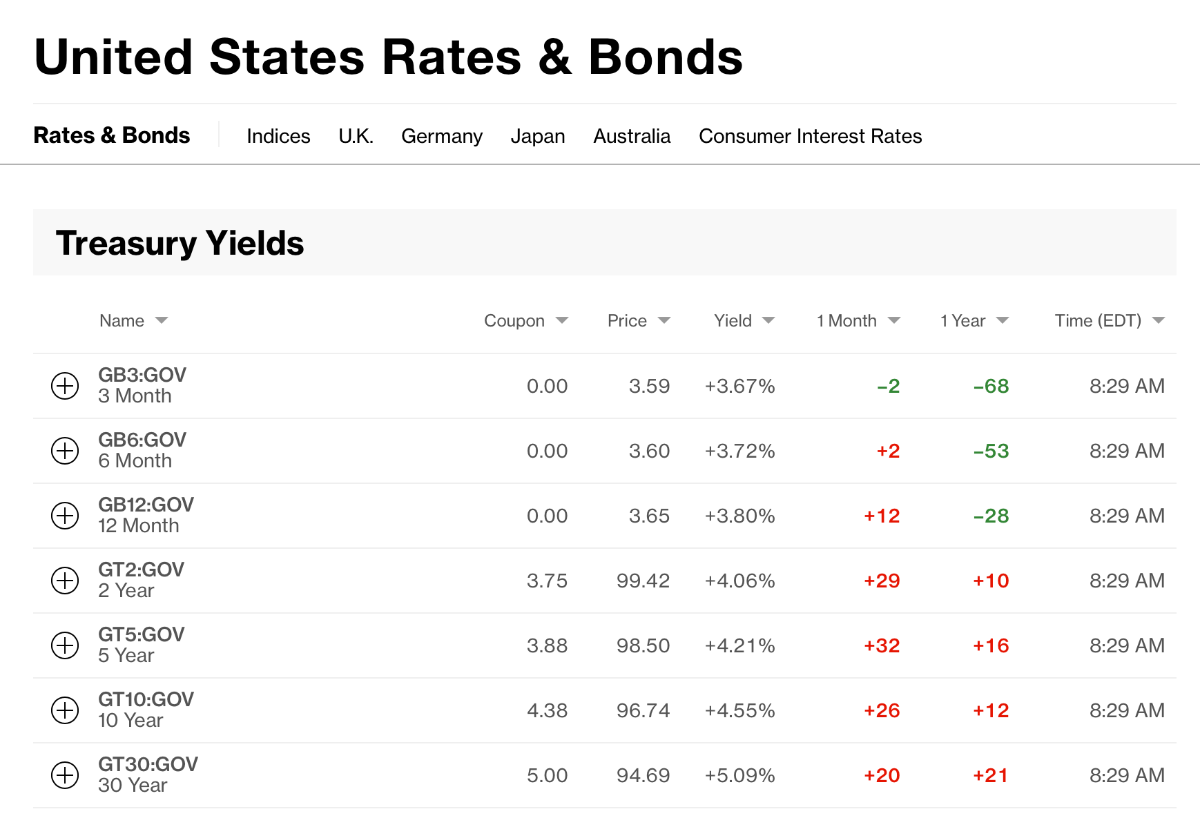

Nine short months ago, many people were very concerned about lower interest rates and how much it would impact interest income at Fairfax in the coming years. Fast forward to today... the 2 year treasury is back above 4% (4.06%) and the 10 year is back above 4.55%. What is the lesson? Trying to predict short term movements in interest rates is a tough game. It makes me wonder what Mr. Market is worried about today... (and what we will think about it in another 12 months...)

-

@NnnnotSoSmart, I appreciate your post. It appears Fairfax continues to put a premium on quality management. I love that. I also like that it appears management is highly focussed on making money - not empire building (with the combination being another step in the process). Very encouraging. It is super interesting to understand the key players in the gold mining space and how everyone knows each other very well. After 30 or 40 years in the business things like character and fit become pretty easy to see and match (one would think).

-

@NnnnotSoSmart, the interesting part of the merger to me is the size aspect (and understanding why big is better in mining). I think it is a similar logic with Foran’s purchase by Eldorado.

-

Really? I think gold stocks have been weak in general the past few days...

-

Fairfax first invested in Orla Mining in 2022 and continued to build its position until 2024. Fairfax sold ~25% of its position in late 2025 for a big gain. Orla has been an exceptional investment for Fairfax. With a market value of about $1.1 billion, Orla Mining is Fairfax’s 4th largest equity holding. On May 13, 2026, Orla and Equinox Gold announced a combination of the two companies. They hosted a conference call with analysts to discuss the proposed combination of the two companies. Link to presentation: https://wp-orlamining-2024.s3.ca-central-1.amazonaws.com/media/2026/05/Equinox-and-Orla-Announcement-20260513.pdf Link to call: https://event.choruscall.com/mediaframe/webcast.html?webcastid=KqhsPRKx ---------- The comments below from Ross Beaty, Chair of Equinox Gold, summarizes nicely the benefits to both companies from the combination: scale matters in mining - for whole bunch of important reasons. “Well, this is a momentous day for Equinox Gold, and it's a momentous day for me personally. Just over eight years ago, we began our journey to build Equinox Gold. From the beginning, we had one big goal - to build a great new gold company at scale. "Why have we focused on scale? "Because it creates better resilience and diversification against risk, better valuation multiples, better liquidity, a stronger financial condition, and, most importantly, greater leverage to gold. "Since we began in 2018 I've been bullish on the gold price, and I've been right. Gold has had a glorious run. But I'm just as bullish today, given the macro environment, particularly for the US dollar. "Gold is money. It's been money for 5000 years. And it's been used as money as much today as ever. The bigger our company is in gold production and gold reserves and resources, the better we will deliver value to our shareholders as the gold price rises. "To build scale, Equinox has - since 2018 - combined with four companies, including today's deal with Orla. We've built mines. We've sold mines that were non core. And we've spun out three companies, each with over $1 billion in market value today. It's been a busy time, and I thank our whole management team and Board for their hard work in making all this happen. "The Orla deal will add icing on the Equinox cake. Darren Hall and Jason Simpson will add details about today's announcement. I only want to say how exciting this combination is for me. "It's truly synergistic. Both companies have mines in Mexico, the United States and Canada with a total of 1.1 million ounces of gold production. And our three mines in Canada will make us the second largest Canadian gold producer at 700,000 ounces of production. "We also have exceptional organic growth prospects that give us the clear path to about 1.9 million ounces of gold production per year in a few years - all self funded from a robust free cash flow. "I'm very pumped about this transaction, and I know it will create terrific shareholder value…”

-

@roundball100, I agree. Part of me loves the fact that Fairfax is so misunderstood. It really is the Rodney Dangerfield of P/C insurance companies (and, yes, I also love Rodney Dangerfield).

-

Ok. Let’s use a 40 year time horizon (I don’t). Their stock price compounded at better than 19% per year (US$, dividends included). And for the first 25 years of this time period they had some pretty crappy insurance businesses. Their stellar results were driven primarily by their investment decisions - which you characterize as ‘mediocre.’ Please square that circle… PS: Fairfax is a contradiction. What people think about the company. And what the company actually did. There is, IMHO, a massive disconnect.

-

@tnathan, when you say that Fairfax / Prem are mediocre investors, what timeframe are you using? Personally, i use a 5 year time frame. I think that length of time provides a solid body of work. Longer than that just isn’t relevant to the company as it exists today. When I look at Fairfax’s execution over the past 5 years their capital allocation / investment decisions have been outstanding. Easily best class when it comes to P/C insurance companies. So please educate me

-

Poor past investment decisions (mostly pre-2018) is one reason Fairfax is cheap. But I think there are more reasons it is cheap. How Fairfax invests is frowned upon by most investors: The industries and types of companies. Their creativity (FFH-TRS being a great recent example). Being opportunistic - exploiting market dislocations The fact they sell companies/positions (not buy and hold forever). The turnover of the portfolio (in general). As a result, the key question an investor needs to come to grips with to invest in Fairfax is “do you trust management.” I think this is very important for Fairfax (more important than for most companies). And of course, most investors don’t trust management - so it is rational they don’t invest in Fairfax. (Note: I am not saying it is rational to not trust management.)

-

I think using a younger Berkshire Hathaway as a comparable for Fairfax today is useful, but only if done at a very high level. Key components of business model: Use P/C insurance as the core engine. For the float (leverage) it provides. Decentralized operations (insurance and investments) Centralized capital allocation, succession planning Invest in equities (public & private) Controlling shareholder Long term focus How each company does each of the key components is very different. Expected rates of return And, of course, when it comes to picking equities, Buffett is the GOAT. No one is going to compound at the rates he did at Berkshire Hathaway over their first 40 years. However, the model (and the management team at Fairfax is good enough) that Fairfax should be able to compound shareholders’ capital at above average rates of return over the next 5 or 10 years (as far as my crystal ball looks out). Summary Comparing Berkshire Hathaway and Fairfax is a very nuanced exercise.

-

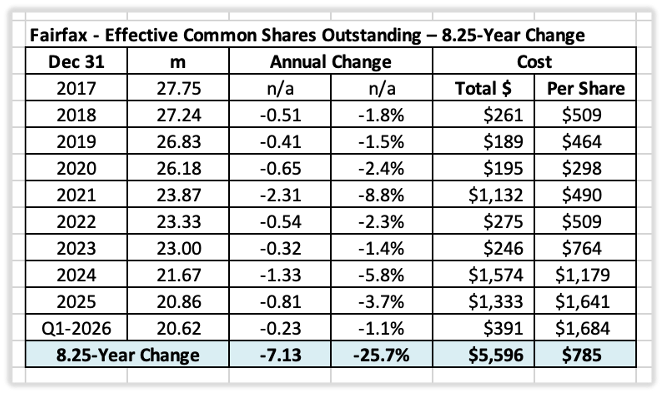

What were the key take-aways from Fairfax's Q1 earnings report? One KTA was they continue to be very aggressive buying back their stock and reducing the number of shares outstanding. Let's explore this more. Share Buybacks – Theory (Warren Buffett) – A Real World Example (Fairfax) The Big Picture Over the long term, three factors drive stock returns: Earnings Valuation multiple Shares outstanding The first two get most of the attention. The third — shares outstanding — is often overlooked, even though it can be a powerful driver of per-share value creation. Capital Allocation Matters Capital allocation is management’s most important job, and share buybacks are one of the most effective tools available. When executed properly — at attractive prices and over long periods of time — buybacks can create enormous value for shareholders. Among all capital allocation options, buybacks offer one of the highest levels of certainty. High certainty generally means lower risk. As Warren Buffett wrote in Berkshire Hathaway’s 1984 Annual Report: “When companies with outstanding businesses and comfortable financial positions find their shares selling far below intrinsic value in the marketplace, no alternative action can benefit shareholders as surely as repurchases.” Warren Buffett – Berkshire Hathaway 1984AR Shareholder Friendly Management It is counterintuitive, but for long-term shareholders a low stock price can actually be a gift — if the company is aggressively repurchasing shares. This is especially true when the discount persists for years. Buffett highlighted two major benefits. 1. Higher Per-Share Intrinsic Value This is straightforward arithmetic. When a company repurchases undervalued shares, the ownership stake of remaining shareholders increases. Intrinsic value per share rises immediately. 2. A Signal of Shareholder-Friendly Management This second benefit is more subtle — and often underappreciated. When management consistently repurchases stock below intrinsic value, it signals disciplined, shareholder-oriented capital allocation rather than empire building. Over time, investors reward this behavior with a higher valuation multiple. Buffett explained it this way in Berkshire Hathaway’s 1984 Annual Report: “The companies in which we have our largest investments have all engaged in significant stock repurchases at times when wide discrepancies existed between price and value. As shareholders, we find this encouraging and rewarding for two important reasons - one that is obvious, and one that is subtle and not always understood. The obvious point involves basic arithmetic: major repurchases at prices well below per-share intrinsic business value immediately increase, in a highly significant way, that value. When companies purchase their own stock, they often find it easy to get $2 of present value for $1. Corporate acquisition programs almost never do as well and, in a discouragingly large number of cases, fail to get anything close to $1 of value for each $1 expended. “The other benefit of repurchases is less subject to precise measurement but can be fully as important over time. By making repurchases when a company’s market value is well below its business value, management clearly demonstrates that it is given to actions that enhance the wealth of shareholders, rather than to actions that expand management’s domain but that do nothing for (or even harm) shareholders. Seeing this, shareholders and potential shareholders increase their estimates of future returns from the business. “This upward revision, in turn, produces market prices more in line with intrinsic business value. These prices are entirely rational. Investors should pay more for a business that is lodged in the hands of a manager with demonstrated pro-shareholder leanings than for one in the hands of a self-interested manager marching to a different drummer...” Warren Buffett – Berkshire Hathaway 1984AR Fairfax’s Buyback Philosophy Prem Watsa laid out Fairfax’s long-term buyback strategy in the company’s 2018 Annual Report: “…we are focused on buying back our shares over the next ten years as and when we get the opportunity to do so at attractive prices. Henry Singleton from Teledyne was our hero as he reduced shares outstanding from approximately 88 million to 12 million over about 15 years.” Prem Watsa – Fairfax 2018AR Fairfax approaches buybacks exactly like a value investor: Buy shares when they are cheap “Back up the truck” when they are really cheap What Has Fairfax Actually Done? 2015–2017: Aggressive Expansion of P/C Insurance Fairfax issued shares to fund the rapid expansion of its international P/C insurance operations. Effective shares outstanding increased by 6.57 million shares Average issuance price: approximately $462 per share Effective shares outstanding peaked at 27.75 million in 2017 2018–2026: Aggressive Buybacks Beginning in 2018, Fairfax pivoted to large-scale share repurchases and has bought back stock every year since. Over the past 8.25 years: Effective shares outstanding declined by 7.13 million shares Total reduction: 25.7% Average repurchase price: approximately $785 per share Effective shares outstanding (March 31, 2026): 20.62 million Fairfax spent approximately $5.6 billion repurchasing stock during this period — its single largest investment. As a result, the share count has fallen to levels last seen in 2010. Did Fairfax Get Good Value? Absolutely. Current metrics: Book value per share: $1,250 (March 31, 2025) Share price: $1,625 (May 4, 2026) Intrinsic value is well above book value Fairfax reduced its share count by 25.7% at an average repurchase price of approximately $785 per share — a substantial discount to book value. Importantly, the company repurchased shares aggressively while simultaneously expanding its core insurance business. Net Premiums Written (NPW) 2017: $10.0 billion ($353 per share) 2025: $26.3 billion ($1,261 per share) Growth from 2017 to 2025: Total NPW growth: 163% Per-share NPW growth: 257% Fairfax walked and chewed gum at the same time. Buybacks materially amplified per-share growth. This is elite capital allocation. Is Fairfax Done Buying Back Shares? Current valuation: Share price: approximately $1,628 (May 4, 2026) Book value: approximately $1,250 (March 31, 2026) P/BV: approximately 1.30 ROE: averaging in the high teens in recent years Despite Fairfax’s strong operating performance, the stock still appears very cheap. Importantly, book value excludes a meaningful amount of hidden value that has accumulated over the past five years. One obvious example is the excess of fair value over carrying value of non-insurance associate and consolidated holdings: Excess of FV over CV: $3.9 billion (at March 31, 2026) Per share: approximately $189 before tax And this is only one source of hidden value on Fairfax’s balance sheet. As a result, Fairfax is cheaper than it appears based solely on book value. I also expect the stock to remain undervalued for some time. Fairfax is still underfollowed, misunderstood, and largely ignored by many investors and analysts. Most still do not fully appreciate how much the company’s business model and earnings power have changed over the past five years. Or how well the company is executing. That likely changes over time. Fairfax has now delivered outstanding results for five consecutive years. If it continues compounding capital at above-average rates over the next five years, it will build a full decade-long track record. That will resonate much more strongly with investors and likely lead to a more appropriate valuation. In the meantime, a persistently undervalued stock is a tremendous advantage for long-term shareholders. It allows Fairfax to continue repurchasing shares at attractive prices. That is an excellent setup for long-term owners. Bottom Line Over the past 8.25 years, Fairfax Financial Holdings has executed a textbook, Henry Singleton-style — Buffett-approved — buyback strategy: Repurchased aggressively when deeply undervalued Created enormous per-share value Continued growing the core insurance business at the same time This is what exceptional capital allocation looks like. It is also a clear signal that Fairfax is being managed with a strong shareholder orientation. One More Thing: Fairfax’s Total Return Swaps Fairfax also holds total return swaps (TRS) on its own stock. The position was established in late 2020/early 2021 at an average cost of approximately $373 per share. The initial position was 1.96 million shares and currently stands at 1.76 million shares. (The position was reduced by approximately 200,000 shares in Q4 2024 when Fairfax purchased and retired shares from the counterparty.) Over the past 5.33 years, the TRS-FFH position has increased in value by roughly $2.4 billion before carrying costs. It has become one of the most successful investments Fairfax has ever made. Some investors view the TRS position as a form of synthetic buyback. Including the impact of the TRS position: Effective shares retired (8.25 years): 32.0% Average price: approximately $704 per share Yes — that is absurdly good capital allocation.

-

Personally, I don’t have a problem with what Lauren did. One of the reasons Buffett did not do stock buybacks was because Berkshire Hathaway had a big information advantage over shareholders - so buying them out when the shares were undervalued was kind of immoral behaviour in Buffett’s mind (taking advantage of BRK shareholders). Pivot to Fairfax today. Fairfax has been buying back extraordinary amounts of stock over the past 8.25 years (~25% of effective shares outstanding). Fairfax has been telling investors (and shareholders) for years at pretty much every chance they get that they think their stock is undervalued. This continues to be the case today. My guess is Lauren’s topic/presentation was vetted through senior management at Fairfax and they were ok with it (most of what she presented was material that was covered at the recent AGM). What she presented was very high level - it was primarily educational and a framework - a way for investors (and shareholders) to think about and better understand the company and the opportunity that exists today. To help them better value the company. My view is Fairfax continues to be misunderstood, under-appreciated and miss valued as a company. (I am not complaining… this has proven to be a big benefit to the company and long term shareholders.) I applaud the efforts of management and those associated with Fairfax of continuing to educate investors (and shareholders) to help them better understand the company as it exists today. And nobody is paying attention anyways - this is Fairfax after all.

-

I am very interested to see what impact history has on investors perception of Fairfax in the coming years. Yes, 2010 to 2020 was largely a lost decade for shareholders. However, the past 5 years have been stellar. My guess is Fairfax will be able to compound BVPS at 15% (or more) each of the next 5 years (on average). Once we get to a 10 year track record that is outstanding does that impact the multiple that investors think the company is worth? As I have said in the past, I am an idiot when it comes to understanding how the market values Fairfax (the multiple at a given point in time).

-

Back in the 1990's I understood many of Buffett's / Berkshire Hathaway's strengths. What I did not understand was the power of time and compounding. I think this is the same challenge most investors/analysts have with Fairfax today. They are so focussed on trying to predict the next quarter or year that they are missing the bigger picture (what time and compounding will do). For a company with Fairfax's business model (capital allocation), trying to predict what happens the next quarter or even the next year is like a dog chasing its tail... (it is fun to guess...). In terms of rate of return, I am pretty confident Fairfax will be able to compound at an above average rate of return. Over a decade that would deliver an exceptional result. Now if they do even better (which certainly is possible given their exceptional track record over the past 7 years), well... that would be icing on the cake. The best part? Where the stock is priced today, investors expect Fairfax to compound at below average rates of return moving forward. As a result, there is a big margin of safety built into the stock price (at $1,622).

-

Fairfax Financial: The Ugly Duckling of the Insurance Industry Introduction Hans Christian Andersen’s The Ugly Duckling is not really a story about transformation. The swan was never ugly — it was simply misunderstood. Placed among ducks, the swan looked awkward and out of place. The other animals judged it using the wrong framework. Because it did not behave like a duck, they assumed it was inferior. For decades, many investors have viewed Fairfax Financial the same way. The market has largely analyzed Fairfax as a traditional property & casualty insurer — focusing heavily on underwriting results, combined ratios, and conventional insurance valuation metrics. But Fairfax has never been a conventional P/C insurer. At its core, Fairfax is something different: a long-term capital compounder built on insurance float, decentralized operations, equity investing, and disciplined capital allocation. Because the market has often viewed Fairfax through the wrong lens, the company has frequently been misunderstood, underappreciated, and misvalued. And yet, as Fairfax continues to execute and deliver above-average returns, investors are increasingly being forced to reconsider what the company actually is. The “ugly duckling” may finally be recognized for what it truly is: a swan. The Market’s Core Mistake The market’s misunderstanding begins with a flawed assumption — that Fairfax is primarily an insurance company. Insurance is the foundation of the business. Float provides the fuel. But Fairfax’s long-term economics are driven by something much broader. Fairfax is better understood as a long-term capital compounder built on three interconnected components: A decentralized P/C insurance operation A large and flexible investment portfolio Disciplined capital allocation These components reinforce one another. Insurance operations generate float. Float provides investable capital. Investments and capital allocation determine how effectively that capital compounds over time. Traditional insurers primarily monetize underwriting. Fairfax monetizes capital allocation. That is a fundamentally different business model. Today, Fairfax manages an investment portfolio of roughly $76 billion, including approximately $50 billion in fixed income and $26 billion in equities and equity-related investments. This is where leverage becomes critically important. Insurance float allows Fairfax to control an investment portfolio far larger than shareholders’ equity alone would support. One of the best ways to understand this dynamic is to compare total investments to shareholders’ equity. For a well-run insurer, float functions as low-cost leverage. When combined with sound underwriting, equity investing, and disciplined capital allocation, the compounding effect can become extremely powerful. Importantly, Fairfax allocates meaningful capital to equities and equity-like investments — asset classes that historically have generated higher long-term returns than fixed income securities. Combined with insurance leverage, this creates the potential for above-average long-term returns. Capital Allocation Is the Key Variable The critical question is not simply how much float Fairfax has. The real question is: how effectively can management allocate that capital over long periods of time? That is the straw that stirs the total return drink. This is also where Fairfax increasingly distinguishes itself from traditional P/C insurers. Since roughly 2018, Fairfax’s capital allocation has arguably been best in class among its peer group. Management has more than doubled the size of its insurance business, improved underwriting profitability, benefited from rising interest rates, monetized and optimized the equity portfolio, repurchased undervalued shares, and built significant recurring investment income — all while maintaining substantial flexibility. The company’s earnings power today is dramatically stronger than it was five years ago. Importantly, this transformation was not accidental. It was the direct result of capital allocation decisions. Past performance is never perfect. But in capital allocation businesses, past performance matters enormously because it provides evidence of management skill, discipline, and decision-making ability across different environments. In many ways, Fairfax today resembles a younger Berkshire Hathaway. During the 1980s and 1990s, Berkshire compounded capital at exceptional rates despite prolonged soft insurance markets. Insurance provided the float — low-cost leverage that Buffett could allocate opportunistically across equities, acquisitions, and wholly owned businesses. The key insight is that Berkshire’s long-term returns were never driven solely by underwriting conditions. They were driven by capital allocation. Fairfax increasingly appears to operate from the same playbook. An important distinction needs to be made. Buffett is the GOAT. Fairfax is not Berkshire Hathaway, and it would be unrealistic to expect Fairfax to replicate Buffett’s stock-picking record from the 1980s and 1990s. However, Fairfax has proven to be a very capable capital allocator and equity investor. Importantly, Fairfax today also has materially more leverage to float than Berkshire had during that earlier period. The lesson is straightforward: a soft insurance market does not automatically prevent exceptional shareholder returns. It hurts traditional P/C insurers because underwriting margins compress. But for a company with a powerful investment engine and strong capital allocation, insurance still provides the leverage while investments drive the compounding. The Swan Emerges The most important development at Fairfax over the past five years has been the transformation in earnings power. Historically, Fairfax was often viewed as a company that under-earned relative to its asset base and intrinsic potential. That has now changed materially. Stronger underwriting results, higher investment income and disciplined capital allocation have combined to materially increase normalized earnings power. With roughly $50 billion invested in fixed income securities and a relatively short-duration bond portfolio, Fairfax has also benefited significantly from reinvesting at higher interest rates. At the same time, Fairfax’s equity and non-insurance investments continue to provide additional upside and embedded value that is often not fully reflected in reported earnings. In The Ugly Duckling, the swan does not suddenly become beautiful. Others simply begin to recognize what it was all along. Fairfax may now be approaching a similar moment. The company increasingly combines: A high-quality insurance platform Massive investable float Rising recurring investment income Strong equity exposure Disciplined capital allocation Opportunistic share repurchases Multiple long-term compounding engines These are not the characteristics of a traditional insurer. They are the characteristics of a long-term capital compounding machine. That is the swan. As Fairfax continues to execute, compound intrinsic value, and demonstrate its transformed earnings power, investors may eventually stop viewing the company as an awkward insurance stock and begin recognizing it for what it really is: A decentralized, long-duration capital compounding machine built on insurance float and disciplined capital allocation. Not an ugly duckling. A swan. ----------- How to Think About Fairfax and Its Transformation in Recent Years - The Ugly Duckling The Ugly Duckling by Hans Christian Andersen is a classic fairy tale about rejection, identity, resilience, and transformation. First published in 1843, the story follows a young bird born in a farmyard who looks different from the other ducklings around him. Larger, awkward, and unattractive in appearance, he is mocked and bullied by the other animals almost immediately after birth. Even his own family struggles to accept him. Everywhere he goes, he is treated as an outsider. Unable to endure the constant ridicule, the ugly duckling leaves the farmyard and wanders alone through the countryside searching for acceptance and belonging. Along the way he encounters harsh conditions, loneliness, hunger, danger, and repeated rejection. The seasons change as he survives a difficult autumn and a brutal winter. Despite his suffering, he continues moving forward. During his journey, the duckling occasionally sees beautiful swans flying overhead. He admires them deeply but believes he could never belong among such graceful creatures. They represent everything he is not — elegant, admired, and confident. When spring finally arrives, the duckling approaches the swans, expecting to be rejected once again. Instead, as he looks into the water, he discovers that he himself has transformed into a magnificent swan. He had never been an ugly duckling at all; he was simply a swan born into the wrong environment. The other swans welcome him warmly, and for the first time in his life he experiences acceptance and happiness. The story’s central message is that people who appear different, misunderstood, or undervalued may possess hidden beauty and potential that only become visible with time and maturity. It is also a story about perseverance, self-discovery, and ultimately finding one’s true identity and place in the world. The story of the Ugly Duckling explains Fairfax’s journey (and that of its investors) of the past 40 years. Importantly, for Fairfax (and its investors), spring has arrived. ----------- The Incredible Power of Berkshire Hathaway’s Business Model Berkshire Hathaway’s stock increased from ~$2,800 in 1987 to over $48,000 in 1997. Insurance markets were soft for many of these years.

-

@kab60, it looks to me like you evaluate Fairfax (and insurance companies in general) primarily through the lens of underwriting profit and interest income. Please correct me if I am wrong. If true, is this how you would have evaluated BRK back in the 1980's and 1990's? My view is to understand and value traditional P/C insurance companies, the two keys are underwriting profit and interest income. My view is Fairfax is a very different animal. The key to understanding and valuing Fairfax is capital allocation. The insurance cycle matters, but much less than for a traditional P/C insurance company - and that is because Fairfax has many ways to grow earnings / economic value beyond just underwriting profit and interest income. I think the best way to think about Fairfax today is not to compare them to P/C insurance peers. Rather, it is to compare them to BRK back in the 1980's and 1990's. Insurance markets were soft and yet BRK was still able to compound capital at excellent rates of return. Why? Capital allocation decisions. Of course, Buffett is the GOAT. I do not expect Fairfax to compound capital at the rates BRK did in the 1980's and 1990's. However, given what I have seen from management over the past 8 years or so, I think Fairfax can continue to compound capital at above average rates of return. This will allow them to compound shareholders' equity at above average rates of return in the coming years - even as the P/C insurance market softens. Do you disagree with my basic thesis? I do appreciate the opportunity to discuss/debate.

-

I agree we need to be open minded about how we analyze and value Fairfax. Interest rates are a great example. Yes, there is a good chance they could go lower from here. That was the big worry with Fairfax 6 months ago. And what has happened? Interest rates have moved much higher. Where do interest rates go from here? We have to options: Lower Higher My view is both possible outcomes need to be incorporated into models for Fairfax. What I find many investors (and analysts) do is think about headwinds. And ignore tailwinds. From my perspective that is not a balanced approach.

-

@kab60 underwriting income represents only about 22% of Fairfax's various earnings streams. This is much less than traditional P/C insurers (who are closer to 45% or more I think). Does this split matter in your analysis? PS: Moving forward investment gains will be a larger source of earnings for Fairfax than underwriting income. And we now have $3.9B in excess of FV over CV... this is a leading indicator of how strong investment gains will be in the coming years (with Q2 being a good example). Traditional P/C insurance companies do not have this income stream at all (let alone $3.9B sitting there waiting to be harvested). Of course, there are other examples of hidden value not captured in the $3.9B, with BIAL being a good example. This is a massive asset that is growing in value each year. Traditional P/C insurance companies do not have these assets as well.

-

Fairfax’s share price closed at about $1,700 at March 31, 2026. So that is the price of the TRS that is baked into Fairfax’s book value of $1,250 (at March 31, 2026). The TRS is a significant investment for Fairfax (its third largest, based on exposure after Eurobank and Poseidon). My view is Fairfax is undervalued at $1,700. One example of how book value at $1,250 looks conservative.