Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

I agree. Higher earning + higher multiple + much lower share count = outstanding investment This is the story that has been playing out with Fairfax for 5 straight years. My guess is it continues for the next 5 (that is a far out as my crystal ball looks). The stock trades today at about 1.4 x YE BV. Cheap. And you get $3 or $4 billion in hidden value for free (excess of FV over CV, BIAL, Poseidon etc). Meaning it is much cheaper than it looks. Like the past 5 years, the key is patience. ---------- A low share price just means Fairfax will be able to continue to vacuum up shares - giving us visibility into the 'much lower share count' part of the equation. Love it!

-

Commercial International Bank – Great bank. Tough country. (Egypt) 2025 was a fantastic year for Fairfax's equity holdings - the top 10 public holdings delivered a total return of ~47%. Amazing. The performance was broad based - 7 of 10 holdings each delivered a return of better than 30%. One of the holdings, CIB, had a very strong 2025, up 40%. And so far in 2026 it is up another 19%. The strong performance in 2025 has carried over to 2026. Let's review CIB in a little more detail. Commercial International Bank (CIB) is Egypt’s leading private-sector bank and one of the country’s most respected publicly traded companies. Fairfax first invested in CIB in August 2014, committing approximately $330 million. Today, Fairfax owns roughly 6.26% of the company. At current prices: Market value of Fairfax’s stake: ~$553 million Share of Fairfax’s equity portfolio: ~2% of ~$27 billion Recent Performance CIB’s performance over the past year has been exceptional: Market value (Dec 31, 2024): ~$331 million Market value (Jan 15, 2026): ~$553 million Increase: +$222 million (+67%) CIB also pays a dividend, though I have not quantified the cumulative payout over the years. However, this recent strength masks a long period of disappointment. From 2014 to 2024, CIB was a poor investment for Fairfax in USD terms. Returns were likely limited to dividends. Therefore, the opportunity cost of holding the position was substantial. So, What’s Problem? CIB itself is not the problem. It is: Well managed Operationally strong Consistently profitable The issue is location. Egypt—like much of Africa—is politically and economically unstable. Chronic currency depreciation has repeatedly wiped out the benefits of CIB’s strong operating performance for foreign investors. Local-currency success has failed to translate into meaningful USD returns. This is a classic case of a great business trapped in a difficult macro environment. Bottom Line It will be interesting to see how CIB performs moving forward – does business quality (finally) win over country risk? CIB Investor Relations Company web site: https://www.cibeg.com/en/investor-relations Q3-2025 Corporate Presentation: https://www.cibeg.com/-/media/project/downloads/investor-relations/ir-library/ir-and-esg-presentations/2025/3q25-ir-ppt.pdf Comments from Prem about Commercial International Bank from Fairfax’s 2024AR. “Commercial International Bank (CIB) led by Hishan Ezz Al-Arab had very strong results in 2024 with an ROE of 50%, net interest margin of 9.5%, earnings growth of 86% and loan-loss provision coverage ratio of 351%. There is significant hidden value in the build-up of provisions on the balance sheet which, if adjusted for, reduces the price-to-book ratio to 1.2x. Since 2014, the bank has continued to compound book value per share and EPS by nearly 20% per annum. The key driver of value to Fairfax and other foreign investors in CIB is the stability of the Egyptian pound and the development of new businesses within the bank. CIB is close to launching a new tech- enabled business line which caters to retail banking and lower-income markets. CIB’s shares are trading at very attractive levels at 4x earnings. The Egyptian government asset disposal program is well underway with $35 billion committed by the Abu Dhabi Investment Authority to develop the Egyptian North Coast. Many other infrastructure assets including the country’s largest airports will also be sold to address the country’s high sovereign debt. While there is much work to do, opportunity awaits given the relatively low asset prices and size of the market with over 100 million people. Since our purchase of CIB shares, they have increased 664%, compounding at 21% per year in local currency (including dividends). Unfortunately, due to depreciation in the Egyptian pound, our return in US dollars is just 7% or 1% per year.” Prem Watsa – Fairfax 2024AR

-

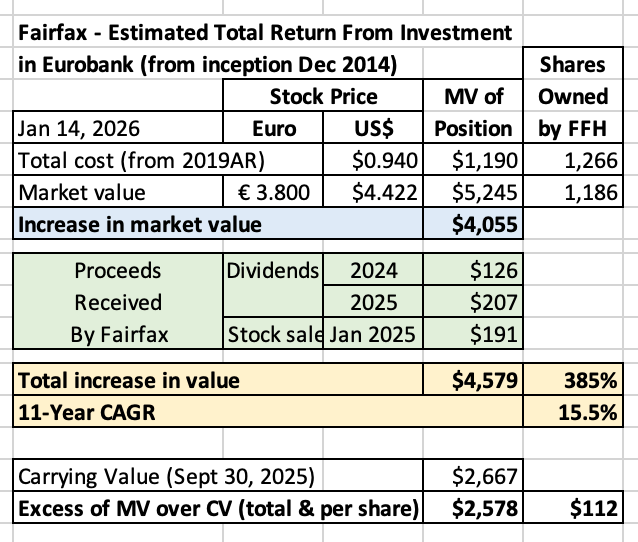

Eurobank – EUROB.AT – Fairfax’s ‘Greek Freak’ - Part 2 Eurobank – Excess of FV over CV – Fairfax’s Hidden Earnings Engine One of the most misunderstood—and increasingly important—sources of value creation at Fairfax is what I call “hidden earnings.” These are not theoretical or speculative. This is economic value that already exists—value that Fairfax has already created for shareholders. The problem? Accounting conventions do not allow it to be recognized—yet. If this were immaterial, it would not matter. But it is not immaterial. It is large. And it is growing rapidly. The best example is Eurobank. Eurobank: The Poster Child for Hidden Value As of today: Market value: $5.2 billion (Jan 14, 2026) Carrying value: $2.7 billion (Sept 30, 2025) Excess of fair value over carrying value: ~$2.6 billion (this is overstated a little, as CV has increased) ~$112 per diluted Fairfax share That gap widened dramatically over the past year alone: Increase in last 12 months: ~$1 billion This is real economic value that has been created. It simply does not appear in Fairfax’s reported earnings or book value. How Did This Happen? Eurobank became an associate holding on December 19, 2019—the day Greek regulators removed restrictions on Fairfax’s voting rights. Critically: The share price was severely depressed at that time That locked in a very low carrying value for Fairfax Everything that followed—operational improvements, earnings growth, multiple expansion—accrued to economic value, not accounting value In other words, the starting point was artificially low. The value creation since then has been extraordinary. Why Accounting Masks the Value Because Eurobank is classified as an associate, it must be equity accounted. That means: Income Statement Fairfax reports its share of Eurobank’s earnings Change in the share price doesn’t matter: no mark-to-market gains are recorded Balance Sheet Carrying value increases only by: Fairfax’s share of Eurobanks earnings Less dividends received from Eurobank (substantial the past 2 years) Market price is irrelevant under current accounting So even though Eurobank’s share price has soared, Fairfax’s carrying value barely moves. This creates a growing disconnect between: What Fairfax owns (economic reality) What accounting reports (book value) How Will This Be Resolved? The accounting distortion disappears the moment Fairfax sells (ownership drops below 20%). At that time, the position becomes mark to market. That would trigger: ~$2.6 billion pre-tax investment gain ~$112 per diluted Fairfax share In one stroke. Will Fairfax Sell? Probably not anytime soon. Eurobank: Is well managed Has strong fundamentals Has solid long-term prospects Remains cheap, even after a massive five-year run Fairfax has no reason to rush. If anything, the most likely outcome is: the excess of fair value over carrying value continues to grow. Which means: More hidden value More future “surprise” earnings More economic value creation not yet recognized Why This Matters Eurobank is the biggest (and best) example of how Fairfax’s reported earnings materially understate true economic performance. This is not aggressive accounting. This is conservative accounting. But investors who only look at: GAAP earnings Book value Reported ROE Miss a large and growing pool of value. Hidden earnings are real. They are measurable. And eventually, they will be recognized.

-

Eurobank – EUROB.AT – Fairfax’s ‘Greek Freak’ - Part 1 Giannis Antetokounmpo is a global NBA superstar and two-time MVP (2018–2019, 2019–2020). Born in Greece, he is affectionately known as “the Greek Freak.” Fairfax has several star performers in its equity portfolio. But one holding stands above all others: Eurobank. Over the past five years, Eurobank has been Fairfax’s top-performing equity investment by a wide margin. It is now Fairfax’s largest equity holding and has been its “MVP” multiple times. Headquartered in Greece, Eurobank has earned its nickname: Fairfax’s Greek Freak. Today, Eurobank is Fairfax’s largest equity investment, with an estimated market value of approximately $5.25 billion. Fairfax owns roughly 32.4% of the bank. A Transformational Investment Fairfax’s investment in Eurobank began in December 2014—at the depth of the Greek depression. The early years were very painful. But patience has been spectacularly rewarded. Total Return Since Inception Eurobank has delivered Fairfax a total return of approximately $4.6 billion, making it Fairfax’s best equity investment ever (measured by total return). Cost basis: ~$1.19 billion (As disclosed in Fairfax’s 2019 Annual Report – including $444 million effectively lost in the initial 2014 investment) Components of total return: Increase in market value Market value (Jan 14, 2026): $5.25B Increase vs. cost: ~$4.05B Dividends received 2024: $126M 2025: $207M Mandatory share sale (Jan 2025) Proceeds: $191M Importantly, virtually all of the $4.6 billion return occurred over the past 5 years. From 2014–2020, Eurobank was a poor investment. From 2021–2025, it has been extraordinary. Why the Turnaround Happened Four factors drove Eurobank’s resurgence: 1. Exceptional Management (Most Important) Eurobank’s leadership—under CEO Fokion Karavias—has executed at an elite level over the past 8 years. Their most recent masterstroke: acquiring Hellenic Bank at just 4x earnings (a textbook example of disciplined, patient capital allocation). 2. Greek Economic Recovery Greece exited a decade-long depression. Two consecutive elections delivered a pro-business government (rare for Greece). Tourism is booming. Real estate is surging. Animal spirits have returned. 3. Higher Interest Rates The disastrous era of global zero-interest rates ended. Net interest margins expanded dramatically—supercharging bank profitability. 4. A Patient Controlling Shareholder (Fairfax) Eurobank was given time to work through their issues. This also allowed them to think strategically and manage the business for the long-term. Comments from Prem about Eurobank from Fairfax’s 2024AR. Eurobank and its superb management team led by Fokion Karavias, had another fantastic year in 2024. Against a backdrop of declining interest rates in Europe, Eurobank grew EPS by 26% and tangible book value per share by 16% (adjusted for the 2024 dividend). Importantly, risk metrics continue to improve – non-performing loans reduced further from 3.5% to 2.9% (with increased provisions). Core Tier 1 capital remains at very healthy levels. This allowed the bank to accelerate the reduction of deferred tax credits – acquired during the Greek crisis – thus increasing the quality of its capital base. Having started to acquire shares in the number two bank in Cyprus – Hellenic Bank – in 2021, Eurobank finalized an agreement in November to take their shareholding to over 93%. Once completed, management will have acquired the company at a valuation of 4x earnings. A terrific demonstration of patience and value investing! Not only did this give Eurobank a strong presence in Cyprus, but it is likely to see 2025 become the first year that profits from international operations exceed those in Greece. Due to the strong underlying value creation, and despite a 39% increase in the share price in 2024, Eurobank remains attractively valued at 1x tangible book value and 6x earnings. After paying its first dividend since 2008 last year, the payout ratio will ramp up to 50% and equates to a 7%+ yield on the current share price. Interestingly, this equates to an 18% yield on Fairfax’s net cost – patience and value investing at the Fairfax level! Prem Watsa – Fairfax 2024AR Part 2 follows in the next post (continue reading).

-

A number of Fairfax's equity holdings are ripping higher 14 days into 2026: Eurobank, Foran, CIB etc. This is after a massive increase in 2025. Resource stocks are smoking. Gold. Copper. Fairfax did monetize 25% of Orla in December. It would be interesting if we got a big sell off in the market averages at resource stocks kept going higher. Fairfax would get a great opportunity to sell high and buy low.

-

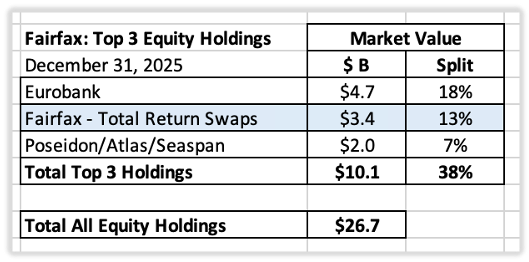

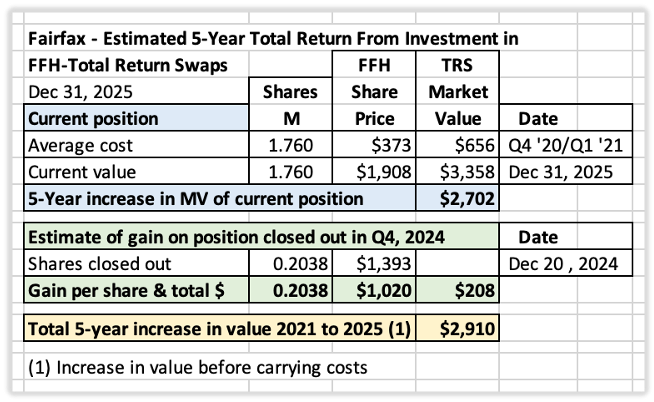

Fairfax Total Return Swaps – A Stealth Buyback of 1.96 million Shares? Fairfax’s second-largest equity holding is its total return swap (TRS) position, which provides exposure to 1.76 million Fairfax shares. At December 31, 2025, the notional value of this position was ~$3.4 billion, representing 13% of Fairfax’s total equity portfolio of $26.7 billion. This position was originally established in late 2020 and early 2021, when Fairfax shares were trading at an absurdly depressed valuation. The initial exposure was 1.96 million shares, making it one of the most aggressive capital allocation decisions in the company’s history. In Q4 2024, Fairfax reduced the position by 203,800 shares, lowering exposure to 1.76 million shares. It is possible they reduced it further in Q4 2025; confirmation will come when year-end results are released in February. From day one, management understood what they were doing. As Prem Watsa wrote in the 2020 Annual Report: “We think this will be a great investment for Fairfax, perhaps our best yet!” Prem Watsa 2020AR Performance: An Extraordinary Result Since inception, the FFH-TRS has generated approximately $2.9 billion in total return (before carrying costs). That is an exceptional outcome by any standard. The return breaks down as follows: $2.7 billion – increase in market value of the current position $208 million – gains realized on the portion exited in Q4 2024 As management foreshadowed in 2020, this has indeed become one of Fairfax’s best investments ever. This single decision exemplifies the quality of capital allocation Fairfax has demonstrated over the past seven to eight years. The cumulative value creation has been enormous. This is not hyperbole — it is fact. Yet this investment has been largely ignored by investors and analysts. Why? Because a total return swap is a non-traditional investment for a P&C insurer. It is far more common at hedge funds. As a result, most analysts never fully incorporated it into their earnings models — one reason estimates for Fairfax have consistently been too low. Given its importance, this position deserves deeper analysis. Margin of Safety Fairfax entered the TRS at an average price of $373/share. At December 31, 2020: Book value: $478.33/share Entry valuation: 0.78x P/B This was an enormous margin of safety. Management was buying its own business at a massive discount to intrinsic value. Circle of Competence Was Fairfax operating inside its circle of competence? Of course. No one understood Fairfax’s intrinsic value better than… Fairfax itself. Management knew the stock was being criminally undervalued. In June 2020, Prem Watsa personally purchased $150 million of stock at roughly $311/share, stating: “I have never seen Fairfax shares sell at a bigger discount to their intrinsic value… I believe that this will be an excellent long-term investment.” — Fairfax News Release, June 15, 2020 This was a high-certainty investment — and therefore a low-risk one. Position Sizing: Backing Up the Truck What should an investor do when: They deeply understand an investment It trades at a historically cheap valuation Conviction is extremely high? They should back up the truck. Fairfax did exactly that. They established exposure to 1.96 million shares, representing: 7.5% of effective shares outstanding at the time (26.2 million) One of the largest single positions in the equity portfolio With this investment, Fairfax got out their elephant-gun. How Did Fairfax Pay? The cost to buy 1.96 million shares outright would have been approximately $731 million (at $373 per share). But in late 2020: The hard market was accelerating. Fairfax needed capital to grow its P/C insurance business. The company had just absorbed a $529 million loss closing its final short position They did not want to drain liquidity. So, they got creative. Instead of buying shares outright, Fairfax used a total return swap, achieving: Full economic exposure Minimal capital outlay Limited impact on balance-sheet A Masterclass in Capital Allocation The FFH-TRS checks every box: Large margin of safety Deep in circle of competence Concentrated position Creative structure (TRS vs. cash purchase) This was rational, opportunistic, creative and unconventional – Fairfax pulled a brand new tool out of their capital allocation toolbox. Just like Henry Singleton used to do when he ran Teledyne. Outlook: Still Attractive Three powerful forces are now working in Fairfax’s favor: Growing earnings – underwriting and investment income Multiple expansion – narrative improving Falling share count – aggressive buybacks The outlook for this investment remains very strong Despite the massive rally, Fairfax’s stock still trades at a discount to peers. Exit Strategy: The Stealth Buyback At the end of the day, the FFH-TRS position is an investment for Fairfax. Like all investments, they have an exit strategy. In Q4 2024, Fairfax reduced the TRS by 203,800 shares (from 1.96 to 1.76 million shares). But here’s the twist: Those shares were purchased and cancelled by Fairfax from the counterparty. So, the TRS reduction was executed as a share buyback. Details: Buyback cost: ~$284M (average price: ~$1,393/share) Total TRS gain in 2024: ~$922M The buyback was funded entirely from a part of the gains on the TRS. This reveals the brilliance of the structure: The TRS may ultimately function as a self-funded buyback program for ~1.9 million shares. That is exceptional capital allocation. Buybacks + TRS = Magic for an Undervalued Stock Fairfax has been very aggressive buying back its stock over the past 5 years. This is a tailwind for the share price. Every $100 increase in Fairfax’s share price creates: $175 million pre-tax gain on the TRS This makes buybacks even more compelling. Shareholders benefit twice: Numerator – TRS boosts earnings Denominator – buybacks shrink share count Higher earnings and lower share count boosts EPS.

-

@dartmonkey, good question. The MV's are as of Dec 31, 2025 (Eurobank = Eu 3.425). Eurobank is up about $500 million (11.1%) in 2026. A bunch of Fairfax's holdings are up solidly to start the new year. Nuts.

-

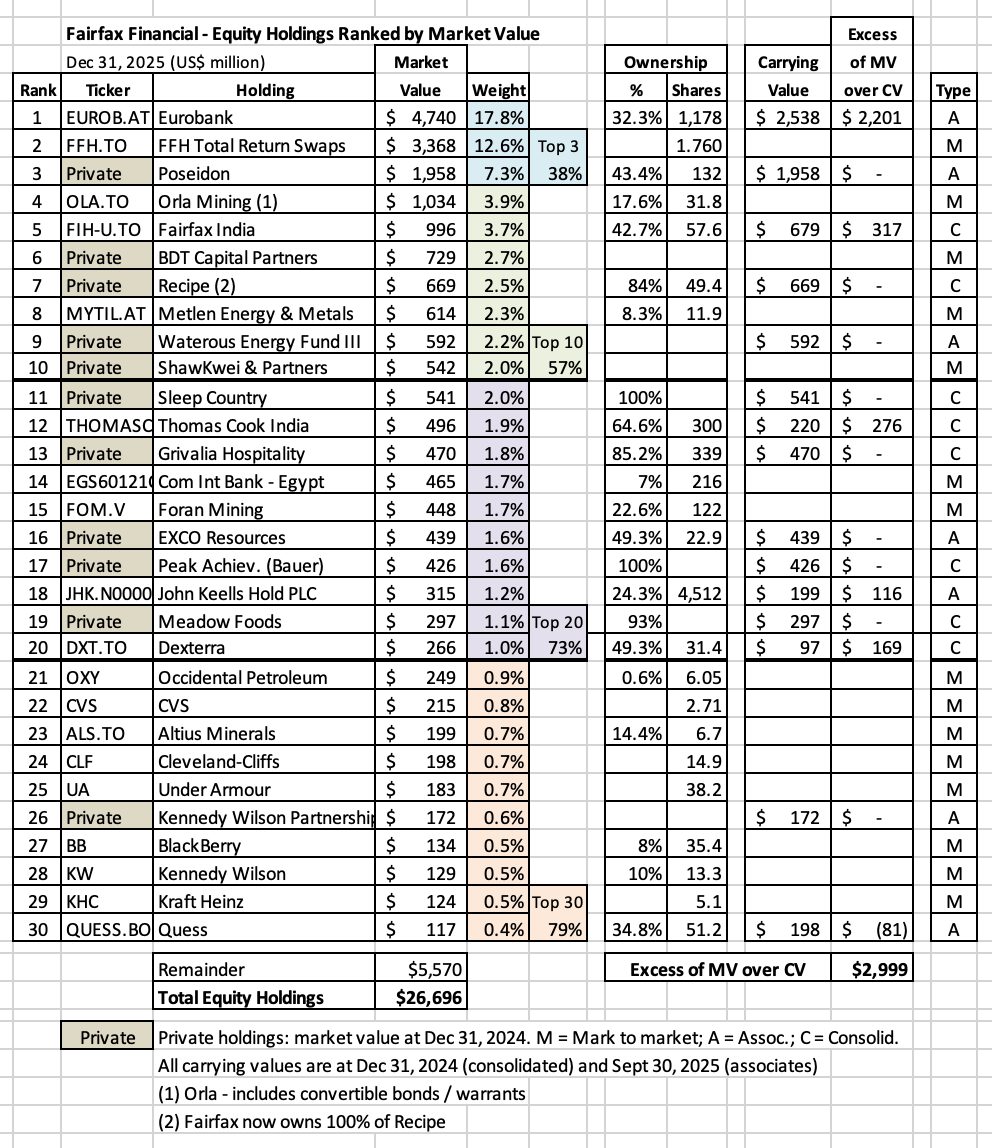

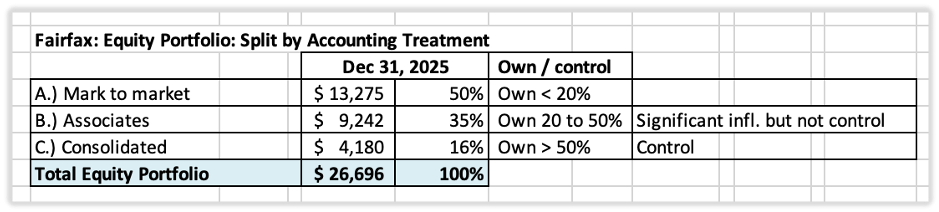

Size Rankings: Top 30 (December 2025) This analysis ranks Fairfax’s 30 largest equity holdings at December 31, 2025. Key Takeaways 1.) A Highly Concentrated Portfolio Top 3 holdings = 38% Top 10 holdings = 57% This is intentional. Concentration reflects conviction, not carelessness. 2.) Comfortably Contrarian At first glance, many holdings look… unconventional: A Greek bank? Total return swaps on its own shares? Heavy exposure to India and Greece? Resource producers? Classic Fairfax. Being different is in their DNA. 3) Structural Shift Toward Private & Associate Holdings A slow evolution: 15 of top 20 holdings are now private or associate investments (where Fairfax has control or exerts significant influence) Over the past 7–8 years, Fairfax has steadily allocated more capital to private and associate investments. Implications: Lower volatility Less mark-to-market exposure → smoother reported results. Growing Gap Between Accounting and Economic Results At Sept-30-2025: Excess of fair value over carrying value = $2.5B $108 per diluted share (pre-tax) This value creation is real–but not (yet) captured in accounting results (EPS, BV and ROE). Investors need to keep this in mind in their analysis of the company. Conclusion: The Shift to Quality When you look at Fairfax’s largest equity holdings today, they all have a number of things in common: Very well managed Solid balance sheets Growing earnings Strong fundamentals Solid long-term prospects In short, Fairfax’s equity holdings (as a group) are high quality. (That was not the case 8 years ago.) This bodes well for future returns the company will be able to deliver. This “shift to quality” aspect is not well understood. This is partly because the individual holdings are not followed. The high quality of the total portfolio becomes even more apparent when we examine performance, which we will do in our next post. (Sneak peek: the top 10 public holdings were up 47% in 2025).

-

I think it is more nuanced than that. When it comes to insurance, Fairfax’s core engine, was the first 20 years better than the last 20 years? What Fairfax has done with their insurance business the past 10 years has been epic: Aggressive growth by acquisitions in the soft market Strong organic growth in the hard market Structural improvement in underwriting What I am most focussed on with Fairfax is today. I really like how the company is positioned. A big reason for that is how well they have performed over the past 5 years (both insurance, investments and capital allocation). Mid-teens ROE looks like a conservative baseline. Monetizing the growing hidden value will be a tailwind to ROE. And yes, there will be some volatility.

-

I agree. Most publicly traded P/C insurance companies can’t accept short term volatility. So equities are off the table as investments. Despite the fact they can deliver a much higher return over the long term. This gives Fairfax a structural return advantage. Time and compounding magnifies this advantage.

-

“Why do you think the business is exceptional?” @Marco Van Basten, Fairfax’s stock has compounded at 19% for 40 years (dividend reinvested, US$). That is an exceptional business. And I don’t think it is debatable. William Thorndike in his book The Outsiders, said judge management by their performance. And the best way to measure performance is the change in the share price over the long term. Simple. Powerful. Yes, insurance is a commodity. And it can be a wonderful business. Fairfax is just one of many examples. There are many ingredients in Fairfax’s secret sauce: Founder/CEO Ownership structure - allowing long term focus Company structure (centralized capital allocation, decentralized operations) Investment management (fixed income and equities). Company culture Shareholder friendly ---------- From Fairfax's AGM presentation (April 2025):

-

I thought Kyle did a very good job with his historical overview of Fairfax - not an easy thing to do (it is easy to get distracted). Bottom line, the company has been able to compound at 19% per year for 40 years (stock, US$). Yes, I think we can say Fairfax is an exceptional business/company.

-

My guess is he will get a nice bump But I don't know... the increase in the share price was only +30% in 2025. The increase was materially below each of the prior two years when it was +50%. Looks like he is slipping...

-

@Munger_Disciple, thanks for catching my error. I meant to say owned/controlled. My post was not meant as a slight to the CEO of Berkshire. For a company of that size, $25 million per year is likely a very good deal for shareholders. And I agree, Buffett's salary at $100,000 per year was a crazy good deal for BRK shareholders. But my guess is that is well understood. Prem at C$600,000? My guess is that is not well understood. Hence why I thought it was worth bringing up. And it also aligns with the 'shareholder friendly' theme - another strength of Fairfax that is not generally understood or recognized.

-

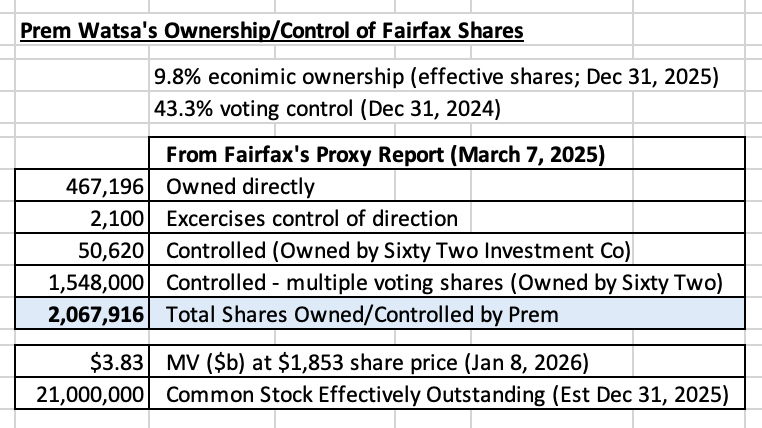

I got lazy in my prior post; I meant 'owned/controlled'. I used what was reported in Fairfax's Proxy Report. Below are updated numbers/estimates. My guess is effective shares outstanding will be around 21 million at YE.

-

CEO compensation is in the news. Berkshire Hathaway (Greg Abel) = $25 million Markel (Tom Gaynor) = $9.7 million Fairfax (Prem Watsa) = C$600,000 cash (no stock options or awards) Fairfax shareholders are getting an unbelievable deal. Especially when you factor in performance. Dramatically underpaying your CEO boosts bottom line results. Doing so for decades boosts the intrinsic value of the company. Of the three CEO's listed above, which one owns the most of their respective company? Prem, who owns 9.2% of Fairfax. His interests are firmly aligned with those of long term shareholders. Fairfax is a very shareholder friendly company. Another under-appreciated strength.

-

Fairfax is doing their part. They already report excess of FV over CV for non-insurance associate and consolidated holdings. We know BIAL is materially undervalued. Analysts and investors (mostly) chose to ignore it. They justify ignoring it by saying they are simply being conservative. Which is completely non-sensical. It is not rational. It’s like when a kid covers their eyes and then thinks they are invisible. Does doing that really make them invisible. Or are they really just fooling themselves?

-

I think you are conflating price and value. Volatility is the short term change in price. Buffett teaches us this is an investors friend. This certainly has been Fairfax’s great friend over the past 5 years. Volatility allowed them to make many of their great investments. Eurobank, as an example, is going up so much because the fundamentals have improved greatly, Greece has emerged from a depression, and a pro-business government is in power. Fairfax is carrying Eurobank on their books at an egregiously low carrying value. Eurobank is not an expensive stock today. Yes, the stock will fluctuate. As long as the company continues to execute well (and they have been putting on a clinic the past 5 years), the intrinsic value of Eurobank should continue to increase. That (not short term price volatility) is what matters. It sounds like you are saying a 10% rate of return with low volatility is better than a 15% rate of return with modest volatility.

-

@djokovic1, my guess is about $60, similar to you. That would be about $215 for the year. Add another $40 for hidden value (one year change in excess of FV over CV) and economic EPS = $255 (conservatively calculated). Who had that as their estimate a year ago? No one (I certainly didn’t). Outstanding performance. (Yes, it is being driven by investment gains… which will be lumpy.) What is the learning? We all continue to underestimate Fairfax and its earnings power. That, IMHO, continues to be the biggest risk for investors. It’s like we don’t really understand its business model. Continue to underestimate management. Don’t get reinvestment. Or how compounding works. The emerging story is all the hidden value that is building. As it gets realized in the coming years it will be a tailwind to reported (accounting) earnings (boosting ROE). This tailwind is not built into analysts estimates. Or the multiple of the stock. Investors today get it for free. ————- Fairfax has been delivering record results in a very low volatility environment. Guess what happens when volatility spikes? That is opportunity for Fairfax. And should boost future returns.

-

@vinod1, I appreciate the comment. Thank you. Fairfax is a complicated company. And it has been changing in important ways every year for 5 years. This combination makes it even more difficult for investors to understand/analyze/value. The company keeps morphing each year into a better version of itself. Now I don't expect that this will keep happening every year. My guess is the investors who have been most successful with Fairfax (as an investment) over the past 5 years are the ones who have been the most inquisitive and open minded about what is happening and focussed on where the Fairfax puck is going.

-

@djokovic1, thank you for the comment. To state the obvious, it is very difficult to calculate a total annuall return for Fairfax's equity portfolio - using a bottom up analysis (i.e. by each holding). With a value of $26.7B, it is of a significant size. There are a large number of holdings. There are both public and private holdings (with limited disclosure). There are outright sales (100% of a position is sold). And there are also brand new purchases. Fairfax often adds to positions. And also does partial sales. Some holdings pay dividends. This can be determined/calculated for public holdings but not for private holdings. Fairfax has material international holdings - currency movements also needs to be included in the analysis (currency changes in 2025 have been significant). And if all that wasn't enough, how should derivative type positions like FFH-TRS be included? What cost base should be used for this investment? And what level of expenses? Needless to say, calculating a one year total return is very difficult. What about a 5 year? That is much more difficult - the one year actually looks easy in comparison. Because it is difficult - does this mean we do nothing? The key question is this - is this an important part of Fairfax's business model? The answer is an obvious yes. It is critically important. What can we do to better understand the performance of the equity portfolio? The answer is easy. You break it into smaller pieces. And that is what I have tried to do over the years. I have developed a number of tools that help us understand what is going on at Fairfax's equity portfolio. Each tool is incomplete on its own. But when they are used together they provide a pretty good picture of what is going on. Recently, I came up with a a couple of new tools. I think they are helpful. Like all new tools, I am learning how to use/explain them properly. I appreciate the feedback from other board members - and my learnings will find their way into future updates. ----------- The 'narrative' is Fairfax is not very good at equity investing. I don't agree. In fact, it looks to me like Fairfax is very good. My view is informed by what my tools tell me.

-

Here are the summary pages of Fairfax's equity holdings at Dec 31, 2025. I was not able to load them on the summary above. My Excel workbook is attached below. Fairfax Dec 2025.xlsx

-

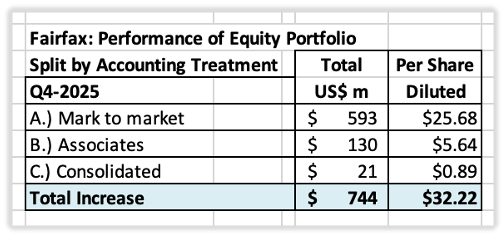

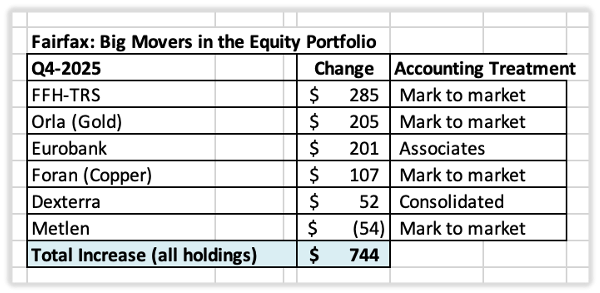

Estimate of Change in Market Value of Fairfax’s Equity Portfolio – Q4-2025 A necessary warning When looking at Fairfax’s equity holdings, what ultimately matters to investors is the underlying business performance of those holdings over time – not the quarter-to- quarter change in market value. Short term (quarterly) changes in market value are inherently volatile and should therefore be viewed with an appropriate degree of skepticism. So why track quarterly changes at all? Because they are interesting and because they can provide early insight into one of Fairfax’s largest income streams—investment gains (and losses)—ahead of reported earnings. Importantly, over time (like a couple of years), the change in the market value of Fairfax’s equity holdings should roughly match the change in their intrinsic business value. Q4-2025 summary In Q4-2025, Fairfax’s equity portfolio increased in market value by approximately $744 million (pre-tax), or 2.9%. At December 31, 2025, Fairfax’s total equity portfolio was valued at approximately $26.7 billion. Fairfax’s equity portfolio has performed exceptionally well in 2025. Key assumptions and limitations Estimates incorporate information from interim earnings releases and 13F filings. The FFH-TRS investment is included in the mark-to-market bucket at its notional value. Convertible bonds, warrants, and debentures are included in the mark-to-market category. The tracker does not include Digit, Fairfax’s publicly traded insurance company in India. A portion of Fairfax’s ownership in Digit is mark-to-market; the shares were flat in Q4. Currency: U.S. dollar weakness was a tailwind for Fairfax in 2025. Where this benefit appears in reported results (net income vs. OCI, net of hedging) is complex. The “tracker portfolio” is not an exact replica of Fairfax’s actual holdings. It is intended solely as a tool to estimate the direction and magnitude of changes in value—not precision. Portfolio composition by accounting treatment Approximately 50% of Fairfax’s equity holdings are mark-to-market and therefore fluctuate each quarter with equity markets. The remaining 50% consist of associate and consolidated holdings. Q4-2025 gains by accounting treatment Total estimated increase: $744 million, or $32 per diluted share (pre-tax) Mark-to-market component: $593 million, or $26 per diluted share (pre-tax) Major movers in Q4-2025 Several holdings continued their strong performance throughout 2025: FFH-TRS, Orla, and Eurobank again delivered exceptional results. Additional strong contributors in Q4 included Foran Mining (copper start-up) and Dexterra (facilities management). The largest laggard was Metlen, which gave back a portion of its substantial Q3 gain. Excess of fair value over carrying value (FV – CV) The excess of fair value over carrying value for non-insurance associate and consolidated holdings is now estimated at approximately: $2.8 billion, or $120 per diluted share (pre-tax) For context, this figure was approximately $1.5 billion at December 31, 2024. FV – CV has increased materially in recent years. It represents economic value created by Fairfax that is not captured in reported earnings or book value—one clear illustration of how traditional accounting metrics understate Fairfax’s true economic performance. Note: The carrying values used for associate and consolidated holdings are as of September 30, 2025 and December 31, 2024, which likely causes this excess to be slightly overstated. Breakdown of FV – CV Associate holdings: $2.0 billion = $86 per share Consolidated holdings: $0.8 billion = $34 per share

-

@vinod1, I think if you look at specific investments it becomes relatively easy to see the changes that Fairfax has made in their approach. I see three things they changed: The importance of management/CEO/partners when making a large investment The financial condition of the company - strength of the balance sheet. Profitability. Prior to 2018, Fairfax was littered with company's that scored low on all three metrics. Today, most of Fairfax's large positions score well on all three metrics. I don't think that is happenstance (luck). I think it is by design - i.e. Fairfax changed their internal framework. New purchases have been much better. And 'keeper' holdings have been forced to get with the new program - be run by strong management teams, have a solid balance sheet and be profitable. Fairfax is operating at a completely different level today. And this new framework is becoming embedded in their culture. I could be completely wrong. I don't think so - the evidence looks too compelling (to me anyways).

-

@dartmonkey, I appreciate the opportunity to discuss this. I think we are solving for two different problems. My focus was: 1.) only publicly traded holdings - not private. 2.) the holdings that have had the largest impact on Fairfax's business performance (impact on earnings) over the past 5 years. I could have included Season/Atlas up to the point it was taken private. I thought about Blackberry, but decided to not include it given its minor impact on earnings and the fact Fairfax exited the debenture (which represented the majority of the investment). Bottom line, there are many different ways to look at Fairfax's equity holdings. What I put together was an analysis that I found helpful. Of course, there is no 'right way.' Also, lots of my stuff is directional in nature - it is not meant to be precise (although I do try). My goal is to be directionally right rather than precisely wrong.