Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

All three of my kids played rep sports. I managed lots of teams and bought lots of team apparel over the years. Under Armour was the brand of choice for the coaches and kids. There was a lot of brand value there. Not sure about today. It is exceedingly hard to turn around a public company - much easier if it is private. Perhaps that is the endgame with partners. There might also be an interesting angle with Peak Achievement and Under Armour. IF the business can get righted it will be a multi bagger. Bottom line, UA is a tiny position.

-

@73 Reds, this is a great question and one that I have thought about quite a bit. Proponents of the ‘old’ investment framework likely didn’t think they had a problem. The shift to the new investment framework took time (years). It probably wasn’t a ‘switch.’ Success is a powerful tonic. Too much trust/loyalty: this is a weakness in a decentralized company. Fair and friendly: Fairfax wants to be viewed as a good partner. Not one that runs at the first sign of trouble. We have incomplete information, especially the private investments. As a result, our understanding is going to inaccurate. Bottom line, I am not sure. But i am very happy with where the company is today. I do think they are moving quicker on problems today (both insurance and investments). I think there has also been a culture shift - expectations are higher (in terms of performance). Poorly managed/performing units likely really stand out today within the company (and not in a good way). And to be clear, Fairfax will have some clunker type investments moving forward. That is the normal way of things.

-

My math says UA is less than a $200 million position. Fairfax’s investment portfolio is about $75 billion, with equities about $26 billion. $200 million is a tiny position - not even a 1% position (or big enough to crack the top 25 largest equity holdings). For context, Fairfax was paid $200 million in dividends by Eurobank in 2025.

-

Fairfax has had many poor performing equity holdings over the past 5 years - mostly the shitty stuff they bought from 2014-2017. I have written extensively in the past about this group of stocks (Fairfax Africa, APR Energy, Farmers Edge, Boat Rocker etc). I view what has happened over the past 5 years with this group of underperforming stocks as a good news story... every one is an example of Fairfax cutting its weeds. Yes, there have been big write downs over the years. And it has taken years. But it appears the holdings have largely been 'fixed.' Regardless, the gains of the top 10 equity 'winners' dwarf the losses from the 'losers.' My goal with putting together the top 10 list was to provide perspective. The gains have been massive. The losses modest. The net result partly explains why Fairfax has been able to deliver such exceptional performance over the past 5 years. 'Winning big' is a super important part of the emerging Fairfax story that is not understood by most investors today.

-

@dartmonkey, Blackberry is a great example of Fairfax cutting its weeds over the past 5 years - of a significant amount of capital being shifted to better opportunities (first the $500M debenture and more recently common stock). My math says Fairfax's investment in BlackBerry was down about $122M over the 5 years from Dec 31, 2020 to Dec 31, 2025. That deserves to be on the top 10 list of the most impactful equity holdings (total return delivered) of the last 5 years? A loss of $122 million is a rounding error compared to a $10.1 billion gain. ---------- Blackberry was a big investment for Fairfax at Dec 31, 2020. But largely because of the debenture of $330M (reduced from $500M to $330M Sept 2020). Importantly, Fairfax did not lose any money on the debenture. In fact it delivered a small return (interest payments). In Nov 2023 it was reduced to $150 million and in February 2024 it was fully repaid. ---------- BlackBerry common stock has not performed well over the past 5 years. But the total loss of $122 million is a small amount. And Fairfax has been selling the common in Q2 and Q3 2025.

-

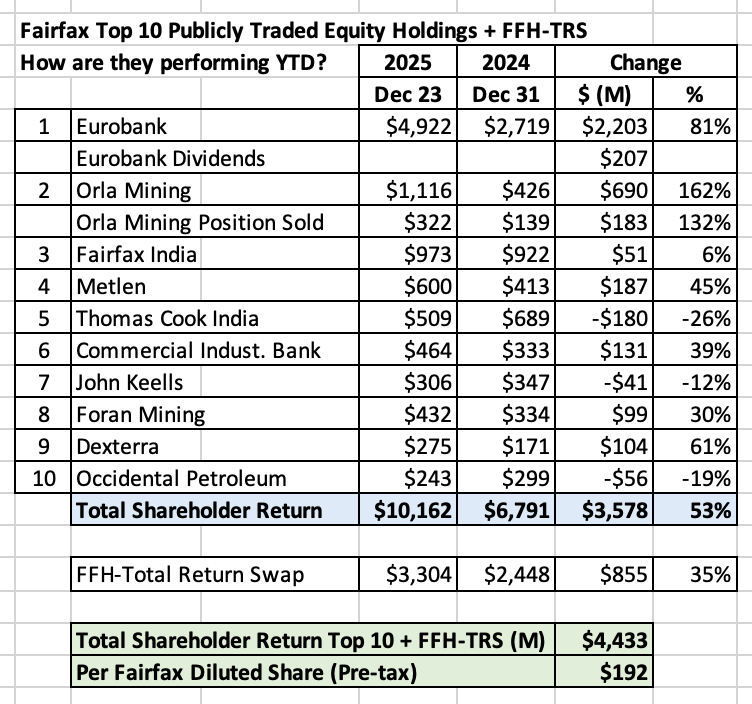

2025 Top 10 List: Fairfax – The Compounding Machine (Part 2 of 2) Equities At December 31, 2025, Fairfax’s Fairfax equity portfolio was valued at approximately $26 billion, split roughly 60% public and 40% private. Fairfax runs a concentrated portfolio. Focusing on the 10 largest publicly traded holdings provides a fact-based view of what is happening across a significant portion of the equity book. 4. Publicly Traded Equities Top 10 Holdings – 1-Year Return Total shareholder return: $4.3 billion (47%) No, that is not a typo. Yes, that is outstanding performance. For context, Fairfax’s common shareholder’s equity was $23 billion at 2024 YE. Generating ~$4.3 billion (pre-tax) in gains from just 10 holdings is a big deal. Notes: The top 10 holdings are ~50% of the equity portfolio This data is not cherry picked - we didn't just include the good stuff The performance is broad based: 7 of 10 holdings are up +30% The group is not expensive: the strong performance is not due to 'euphoria' Much of the gain is not yet captured in the accounting results Importantly, each of the holdings (as a whole) are well managed, not expensive with solid prospects. You are probably thinking this is just a one-year wonder. It isn’t. Top 10 Holdings: 5-Year Return Total Shareholder return: $10.1 billion (242%) 5-year CAGR ~30.6% Again, not a typo. Are you surprised? For context, Fairfax’s common shareholders’ equity at 2020YE was $12.5 billion. Generating $10.1 billion (pre-tax) in gains from 10 equity holdings is a big deal. (Of course, this is just one part of what has been happening ‘under the hood’ at Fairfax in recent years.) Details: Two holdings were sold at peak valuations: Stelco (steel consolidation mania late in 2024) and Resolute Forest Products (top of the lumber cycle in 2022). Two positions were initiated at very low valuations: Orla Mining (2022 to 2024), a gold producer, and Foran Mining (2021 to 2025), a copper start-up. Other positions were opportunistically added to: Fairfax India (2022), Thomas Cook India (2022) and Metlen (2022 and 2025). Fairfax has been patient with other positions: Eurobank, FFH-TRS and CIB. Over the past 5 years, Fairfax has been very busy with its total equity portfolio - watering its flowers and pulling its weeds (fixing/exiting poorly performing legacy holdings). It has also been very opportunistic, exploiting volatility - buying low and selling high. Fairfax is partnering with outstanding CEO’s/entrepreneurs. Fairfax has been quietly putting on a clinic on how to do active management well – with the performance of the equity portfolio being just one example. Built over the past 40 years, Fairfax has skills sets (and relationships) that appear to be the perfect match for the current economic/macro environment. For 5 years they have been feasting. And they are licking their chops right now… patiently waiting for Mr. Market to serve up more wonderful investment opportunities that fall into their circle of competence. Narrative The narrative is Fairfax are not very good equity investors. Yes, this is complete crap. The next time you talk to an investment professional about Fairfax - and they say they do not like their equity portfolio - ask them how the top holdings have actually performed over 1- and 5-year periods. My guess is they will have no idea. But when it comes to Fairfax knowing nothing and having a strong opinion usually go hand-in-hand. Crazy but true. 5. Non-Insurance Consolidated Companies (NICC) Let’s pivot and look at some of Fairfax’s private holdings. NICC includes Recipe, Sleep Country, Peak Achievement, Grivalia Hospitality, AFT Food Ingredients, Meadow Foods and Dexterra. Fairfax has 5 income streams that flow through to earnings. NICC is the smallest. But that is changing. Fairfax has been investing heavily in recent years in NICC and the income stream is inflecting higher. Pre-Tax Income* 2020 to 2023 average per year: $12M 2024: $212M 2025E: $360M 2026E: $450M Fairfax has created a new, meaningful fifth income stream: Not correlated with P/C insurance With significant reinvestment opportunities Rapidly scaling * Pre-tax income (loss) before interest expense; excludes interest and dividends, share of profit (loss) of associates and net gains (losses) on investments. Capital allocation Capital allocation is a competitive advantage of Fairfax’s business model. 6. Investments P/C Insurance Investments Fairfax continued to invest to grow its insurance business: Albingia SA (33%): $216 million (closed in May) Gulf Insurance Group: $165 million (payment 2 of 4). Eurobank Cypress (45%): $69 (expected to close in Q1 2026) Buyouts of minority partners at Allied World (16.6%) and Odyssey (9.9%) remain future catalysts. Equity Investments Watering Flowers: Buying More of What it Already Owns Metlen: $119M (March) - 2.75M shares at €40 per share Increased ownership from 9.2 to 11.95M shares. Recipe (three transactions): $157M (Q1): took out minority partner (16%); now own 100%. $75M (May): take private Keg Royalty Income Fund. Now control Keg banner. Purchased rights to Olive Garden Canada + 8 locations (July) Foran Mining: $53M (May) – 25M shares at C$3 Ownership increased from 96.9 to 121.9M shares. John Keells - $18M (Sept); 230M shares at Rs 23.20/share Ownership increased from 4,282 to 4,512M shares. Kennedy Wilson: take private offer (Nov) at $10.25/share (38% premium) Awaiting response from KW special committee (timing: 2026) Pulling Weeds Blue Ant reverse takeover of Boat Rocker Boat Rocker impairment charge of $108.6M over first 6 months. Another example of Fairfax dealing with a poorly performing legacy holding. Solution: merge with a stronger player (and take the impairment charge). Over the past 7 years, Fairfax has dedicated significant resources (time and money) to deal with a number of poorly performing legacy holdings (purchased 2014-2017). It looks like they might be done. The equity portfolio has been significantly upgraded. New Investment Blizzard Vacatia: $835 million (Jan) Partner with entrepreneur Caroline Shin. Boosted interest income by $86M 7. Asset Sales Asset sales have always been an important part of Fairfax’s capital allocation framework. Sigma (March) - $327M proceeds; 178.7M realized gain. Orla (December) - $316M proceeds; ~$216M gain vs. original cost (estimate). Praktiker - (July) - Greek home improvement retailer. No details disclosed. Eurolife’s life insurance business: $945M proceeds; expected to close in Q1 2026 and result in ~$250M pre-tax gain. 8. Share buybacks Fairfax remained aggressive in 2025. 2025 (estimate) Shares repurchased: ~670,000 Cost: ~$1.1B (at ~$1,625 per share) Shares outstanding at year end: ~21M Five-Year Impact Shares reduced: 20% Cost: $4.3B Average price: $833 per share At 2025 YE, shares closed at $1,908. At September 30, 2024, book value was $1,204. Over the past five years, a significant number of shares were repurchased at very attractive prices – delivering enormous value to long-term shareholders (and reinforcing that Fairfax is being run for owners). 9. Final Observations Ratings Agency Upgrades In 2025, Fairfax and its P/C insurance subsidiaries were upgraded by both AM Best and S&P Global for the second time in three years – the result of strong performance and improving overall financial strength. Currency Tailwind Given Fairfax’s significant international exposure (insurance and investments), currency has been a headwind in recent years (strong US$). In 2025, currency flipped to a tailwind (weak US$). This gain should be reflected in OCI and book value (net of any hedging done by Fairfax). Book value is losing its relevance for investors Buffett banished BV Berkshire Hathaway in his shareholder letter in the 2018AR. Fairfax is not there yet, but it is moving in that direction. Fairfax’s economic results have exceeded accounting results for years and the gap in 2025 is especially wide. A key reason: more than 50% of the equity portfolio consists of associate and consolidated holdings. Carrying value for many of these holdings is much lower than their market value. This hidden value will get surfaced in the coming years (boosting accounting results like EPS, BV and ROE). Fairfax is helping investors. They publish the excess of FV over CV for non-insurance associate and consolidated holdings with their accounting results. Eurobank alone represents ~$100 per share of hidden value. This helps explain why Fairfax has continued being very aggressive with buybacks at 1.5 x BV. And why they continue to hold the FFH-TRS position. Management knows book value is understated – and the stock is even cheaper than it appears. 10. Personnel Changes Fairfax is very good at succession planning. A slow and thoughtful transition to the next generation of leadership has been happening in recent years at all parts of the organization: insurance, investments and capital allocation. The old guard is moving into mentorship and stewardship roles while the next generation takes on operating leadership/greater responsibilities. Appointments: Andy Barnard - Chairman - Fairfax Insurance Group (was President) Brian Young - President - Fairfax Insurance Group (was CEO Odyssey) Carl Overy - CEO – Odyssey Jennifer Allen - Chief Business Officer (was CFO) Amy Sherk – CFO Christine Magee - Fairfax Board Mr. Amitabh Kant - Senior Advisor

-

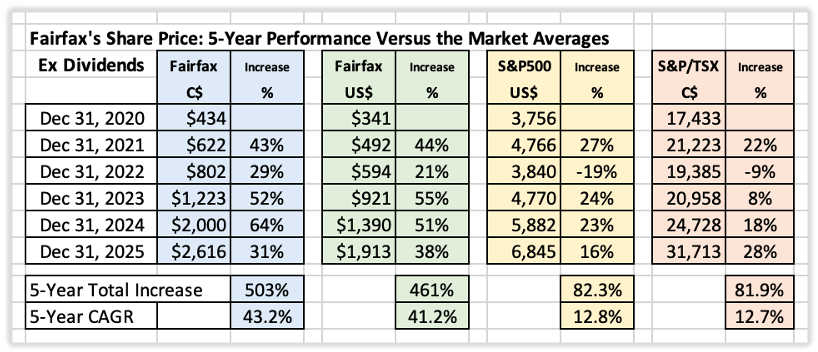

2025 Top 10 List: Fairfax – The Compounding Machine (Part 1 of 2) Below is our annual review of major developments at Fairfax. What is missing from the list? Please share your thoughts. In 2025, Fairfax quietly delivered another exceptional year. That makes five in a row, and that matters. Fairfax is delivering consistent, very strong performance. What happened? This is where the story gets interesting. No one thing. It was everything: insurance, investments and capital allocation. It was Fairfax’s people (culture) and their business model. What we learned in 2025 is Fairfax doesn’t have to do anything spectacular to deliver spectacular results. That is what an exceptional business looks like. Fairfax has re-emerged as a compounding machine. Importantly, this version of Fairfax is much better than past versions: earnings streams are more balanced and higher quality, and the company is more experienced and mature. It’s like Fairfax has grown up right in front of us - after 40 years of refinement, Fairfax has figured out how to best exploit the model pioneered by Buffett at Berkshire Hathaway – with P/C insurance at its core. Fairfax today looks like a star athlete entering their prime - performing to their full potential. It has become fun to own and follow. That is the definition of a high-quality business. Financial Performance Snapshot Earnings, Book Value and ROE Fairfax is on pace to deliver record earnings in 2025. Earning Accounting EPS estimate: ~ $200 per diluted share (my guess today) Economic EPS estimate: ~$240 per diluted share (conservatively calculated) Book Value Per Share 2024 YE: $1,060 2025E: $1,255 (current) Increase: $195 per share Return on Equity Accounting ROE (rough): ~17.3% Economic ROE: ~20%+ The accounting change in BVPS and ROE does not include an additional ~$40 per share of economic earnings. Fairfax’s book value is materially understated. Share Price Performance In 2025, Fairfax’s share price increased: +31% (C$) +38% (US$) For comparison: S&P 500: +16% S&P/TSX: +28% Five-Year Performance Fairfax: +503% (C$) | +461% (US$) S&P 500: +82% S&P/TSX: +82% Fairfax has outperformed market averages every year over this period. Dividend Fairfax paid a dividend of $15 per share in 2025. Valuation Versus Peers Relative to a group of high-quality P/C insurance peers, Fairfax: Has dramatically outperformed on total shareholder return and BVPS growth over the past six years Trades at the lowest valuation, on both P/BV* and P/E The best performer remains available at the cheapest price. * Important caveat: Fairfax’s BV is understated. Its economic P/BV is materially lower than the reported ~1.59x. The Fairfax Business Model: What’s Driving Results? To understand 2025, it helps to break Fairfax into its core engines: Insurance operations (net premiums written and underwriting profit) Investments (fixed income and equities) Capital allocation (reinvesting, harvesting, and buybacks) Final observations (ratings agencies, currency, book value) Personnel changes (succession and bench strength) Insurance Operations 1. The Top Line: Net Premiums Written The hard market that began in late 2019 is moderating, and top-line growth is slowing. 2025 Estimate Net premiums written (NPW): $26.6B (+5%) Six-Year Growth (since the start of the hard market) Total growth: $13.3B (+100%) CAGR: 12.3% These are solid numbers – but total dollars are not what matter most to shareholders. Per-share results do. Per-Share Metrics 2025 NPW per share (estimate): $1,265 (+9%) Six-year per-share growth: $770 (+156%) Per-share CAGR: 16.9% Measured per share, Fairfax’s insurance business has been growing like a weed. Over the past six years, it has effectively been a growth company. Early in the hard market (2021–2022), top-line growth was strongest. In later years, growth has slowed—but aggressive buybacks materially accelerated per-share results. Fairfax has delivered a textbook example of how to manage the hard-market phase of the insurance cycle. 2. The Bottom Line: Underwriting Profit Underwriting performance determines the value of an insurance business. 2025 Estimate Combined ratio: ~93.5% Underwriting profit: ~$1.7B Underwriting profit per share: ~$80 Six-Year Growth Underwriting profit per share: +443% Drivers: Strong NPW growth (16.9% per-share CAGR) Structural improvement in combined ratio Aggressive share buybacks (~20% reduction in shares) Fairfax operates a high-quality, consistently profitable P/C insurance franchise – and that franchise is very valuable. An underwriting profit means Fairfax is being paid to hold float—estimated at $37B at YE 2025—which it can then invest for its own benefit. Investments After strong years in 2023 and 2024, Fairfax is having a blowout investment year in 2025. 2025 Investment Snapshot Average investments: ~$72B Estimated total return: ~$7.56B (~10.5%) Breakdown by Asset Class Fixed income: ~$2.92B (5.1% yield + gains) Equities & other: ~$4.64B (20.1% return) This estimate includes the annual change in excess of fair value over carrying value for non-insurance associate and consolidated holdings, which is not captured in accounting earnings. Even so, the 10.5% return figure remains conservative. 3. Fixed income – Interest Income Interest income (2025E): $2.46B (record) Average yield: ~5.1% Drivers Growth in the fixed-income portfolio from ~$46.5 (2024) to ~$50 billion (2025) First-mortgage partnership with Kennedy Wilson increased by $800M (9 months) Portfolio grew from $4.8B to $5.6B (Sept. 30, 2025) Blizzard Vacatia investment ($835 million). Five-Year Growth Interest income per share: +393% Drivers: Larger portfolio. Much higher interest rates Aggressive share buybacks (+20% reduction in shares) Interest income has become Fairfax’s largest income stream – and it’s a high quality source of earnings. Part 2 follows below in this thread.

-

Here is how Buffett frames float for Berkshire Hathaway shareholders in the 1998AR: “With the acquisition of General Re — and with GEICO’s business mushrooming — it becomes more important than ever that you understand how to evaluate an insurance company. The key determinants are: the amount of float that the business generates; its cost; and most important of all, the long-term outlook for both of these factors.” Warren Buffett – Berkshire Hathaway 1998AR ————— This is very important for Fairfax shareholders today. Why? Fairfax has been aggressively growing its insurance business over the past 10 years. First with acquisitions. And more recently by capitalizing on the hard market. As a result, the amount of float has spiked higher. Companywide underwriting has structurally improved (lower cost). And the long-term outlook for both is positive. The core engine for Fairfax has never been stronger or better positioned than it is today.

-

2025 = 20.9%. Very happy with that result. Context: I am shifting towards a wealth preservation mindset (direction of travel). “Why risk what you need for what you don’t need.” This impacted my return in 2025. And it will impact future returns. Our best accounts (TFSA, non-registered and kids accounts) were up about 30%. Our ‘worst’ accounts (RRSP’s, LIF’s) were up about 15%. We are trying to wind down the RESP account as we only have one kid still in university; return was 5%. 5 years ago 100% of investments were in our ‘worst’ accounts (plus RESP). Today it is almost a 50-50 split between ‘best’ and ‘worst’. My plan is to continue to use our ‘worst’ accounts to fund expenses (and pay the taxes) and let our best accounts run higher. Bottom line, our total investment portfolio is now split nicely among the different accounts and this will give us a lot of optionality moving forward (in terms of what accounts to use to fund living expenses). The restaurant menu is now full of options! ————— To clarify, Canada has a large number of tax-advantaged investing accounts and they are all good and amazing generators of wealth - FHSA, TFSA, RRSP, RRIF, RESP. And each of them have different strengths and weaknesses. A weakness of RRSP and RIF accounts is they can get too big - and yes, that is an awesome problem to have.

-

My very rough estimate is the average cost on the common shares is about C$5.30/share. I use C$5.50/share (to be a little more conservative). 56.8 million common shares: total cost = $228 million Convertible Bonds: total cost = $150 million Total amount invested by Fairfax to date = $378 million Proceeds from the sale of 25M shares Dec 5 = $316 million This drops the total amount invested by Fairfax to $62 million. The market value of 76.9 million shares = $1.05B The convertible bonds can be converted to 27.2 million shares (C$7.90 or $5.51/share). The warrants can be exercised into 17.9 million shares (C$11.50 or $8.03/share) Cost to exercise the warrants = additional $144 million. This would bring Fairfax's investment in Orla to $206 million (cost basis) Fairfax is getting paid a 4.5% coupon on the convertible bonds = $6.75 million per year. This lowers the cost basis a little. Bottom line, Orla has turned into a fantastic investment. Very high return. Very short timeframe (the convertible bonds/warrant deal was struck 14 months ago). Fairfax is getting paid a coupon on the convertibles (they are getting paid to wait). And the warrants give Fairfax exposure to the upside at a very low upfront cost. The structure of the deal is amazing.

-

Orla Mining (gold producer) is a recent investment for Fairfax. They are partnered with Pierre Lassonde. How did it perform in 2025? It delivered a gain of about $747M. Outstanding performance. The big dogs at Fairfax have been feasting in 2025. The bigger story: exceptional capital allocation In 2022 Fairfax sold Resolute Forest Products at the top of the lumber cycle ($626 million). They started buying Orla in Q3 2022 (open market purchases) and continued until Q3 2024. My guess is a chunk of capital from RFP was recycled into Orla. On December 5th, Fairfax sold 25% of their position in Orla (taking advantage of the bull market in gold). Proceeds from the Orla sale will now be recycled into a new investment. Orla was a very unconventional investment when it was made. Today? Gold has gone mainstream - Gundlach recently recommended investors have a 25% weighting to gold in their portfolios. Fairfax has been putting on a capital allocation clinic over the past 5 years. There are so many examples of exceptional decisions - Orla is just one in a long list. What Fairfax is doing is a skill - it is repeatable. And they are demonstrably good at it. Yet, from a valuation perspective, Fairfax trades at the low end when compared to peers. Fairfax shares continue to climb the 'wall of worry.'

-

What is Fairfax’s best performing equity investment? Eurobank. Up $2.3B in 2025 and $4.4B over the last 5 years. The 5-year gain from Eurobank and FFH-TRS (see previous post in this thread) has been about $7.3 billion ($4.4 + $2.9). To put this number into perspective, common shareholders equity at Fairfax at Dec 31, 2020 was $12.5 billion. That is nuts. (Actually the crazy part is the returns from Eurobank and FFH-TRS is just scratching the surface of what has been happening under the hood at Fairfax over the past 5 years. The value creation has been enormous... and that is not hyperbole.) Eurobank is very well managed. Still cheap. Bright future. (Sound familiar?) My summary below is broken into two parts: Current position (1,178 million shares): the change in market value + dividends paid The position Fairfax sold in January 2025 (80 million shares). Greek regulators do not allow foreign ownership of a bank to exceed 33% (Fairfax was a little over). Yes, my current position (1,178 million shares) is not accurate given Eurobank is buying back stock and Fairfax is selling on a pro-rated basis (to keep their ownership below 33%). I will update my share count when Fairfax releases their 2025AR. The goal with my analysis is to get the big picture/themes right (not to be precise - when it is not possible). PS: Eurobank is equity accounted - so much of gain in MV has not been captured in accounting results (EPS, BV and ROE).

-

Fairfax has been building additional resiliency into its business model in recent years. One example is the build out of the non-insurance consolidated group of holdings. This is now a significant group of companies (number and size). This is a fifth income stream for Fairfax that is starting to break out (my estimate is $450 million in 2026) - that is not correlated with P/C insurance and will not be affected by stock market volatility. Holdings could also an important source of liquidity should Fairfax need some cash. My guess is this bucket of holdings will continue to grow in size in the coming years.

-

Fairfax has made many very good investments in recent years. Like its purchase in late 2020/early 2021 of total return swaps giving it exposure to 1.96 million Fairfax shares at an average cost of $373/share. Position is up $900M in 2025 and $2.9B over the past 5 years (not including dividend or carrying cost). Unconventional and brilliant. For perspective, common shareholders’ equity was $12.5 billion at Dec 31, 2020. A $2.9 billion return over a 5 years period from one investment is material. Will this become Fairfax’s best ever single investment? (Capital required to put position on. Risk profile. Timeframe involved. Etc)

-

We have a houseful. I am multitasking (something I don’t normally do). Cheers Sanjeev

-

@Redskin212, not nit picking. I appreciate you pointing out my error (my previous post has been updated).

-

Yes, Merry Christmas everyone. My wife and I both pinch ourselves every morning at our good fortune. This message board has been a very important piece in the puzzle. Thank you.

-

Great point - and I agree. “If it does not show up in accounting results it did not happen.” Investors/analysts on Fairfax results This sounds like something Warren Buffett would say (yes, that was my attempt at humour). I think Fairfax has been building a significant amount of ‘hidden value’ in recent years. Excess of FV over CV is one good example ($2.5B at Sept 30, 2025). But there is much more happening ‘under the hood’. And because of the size and quality of Fairfax’s equity holdings (most of which are not mark to market) it will keep growing - likely materially - in the coming years. And as you say, Fairfax will surface this value over time. When they do it will be material to earnings. Sigma in Q1 is a good example of what will happen in future years. Except Sigma was small. Some big investment gains are coming. BIAL IPO (via Achorage). Eurobank will be massive (billions). There are more. We already have our first example for 2026: the sale of Eurolife’s life insurance business for $945 million will result in a gain of about $300 million when it closes in Q1. This is an example that was not an anyones radar (not in the excess of FV over CV bucket). When these gains happen, investors will be surprised. “Who could have known?” they will say. To your point, economic value getting realized into accounting results will simply drive a higher ROE in the future. It is such an interesting part of the Fairfax story. Investors/analysts are willfully ignoring something that has already happened and is very important/material. It’s like when a child covers their eyes to hide - they think they are invisible. (It’s probably not the behaviour you want to see from an investment advisor/professional. But that is effectively what they are doing.)

-

The narrative is Fairfax are not very good equity investors. It can be useful to look at facts (sorry detractors). How have the top 10 publicly traded holdings performed YTD 2025? They delivered a total shareholder return of $3.6B, or 53%. If we add FFH-Total Return Swap: They delivered a total shareholder return of $4.4B, or $192 per diluted share (pre-tax). Yes, that is outstanding performance. Fairfax is firing on all cylinders. Notes: The top 10 holdings capture about 40% of Fairfax's $25B (at the end of 2025) equity portfolio. This data is not cherry picked - we didn't just include the good stuff. The performance is broad based: 7 of 10 holdings are having positive years. 6 of 10 holdings are having stellar years, with the lowest performer at 30%. The stocks, as a group, are not expensive: the stellar year is not due to 'euphoria' Many of the companies on the list are undervalued. Fairfax India is materially undervalued (BIAL is a jewel). Currency is shifting from a headwind (strong US$) to a tailwind (weak US$). Economic value creation is much higher than what is being reflected in accounting results: Much of the value gain at Eurobank is not showing up in reported (accounting) results. Can we estimate the return being generated of Fairfax's total equity portfolio? Fairfax's equity portfolio finished 2024 with a total value of about $19B. On their own, the top 10 holdings + FFH-TRS have delivered a return of 23% to the total equity portfolio YTD in 2025. Of course the other 60% of holdings are also performing well. When we put the two together, Fairfax has likely generated a return on its total equity portfolio well in excess of 30% in 2025. Fairfax's equity holdings are having an even better year than the outstanding numbers presented here suggest. Is this a one-year wonder? This is not a one year phenomenon. If I ran this same report for the past 5 years investors would be shocked at how good the results have been. What explains the outstanding performance? What we are seeing are benefits of the significant work Fairfax has been doing with its equity portfolio since 2018: Fixed investment framework (equities): focus on jockey, balance sheet and profitability. Dealt with poorly performing legacy holdings (purchased pre-2018) New purchases since 2018 have been performing exceptionally well (as a group). Concentration - new capital goes to the best ideas. The power of Fairfax's business model The big benefit of equities over bonds is equities have unlimited upside. The results Fairfax is delivering in 2025 (and the last 5 years) is proof (+30% on $19B equity portfolio). Despite its incredible run the past 5 years, Fairfax's equity portfolio is still cheap (as a group). And it is high quality (management, balance sheet, profitability). This is a great set-up for shareholders. The fantastic news with equities is just one part of the good news story called Fairfax. The company is firing on all cylinders - insurance, investments and capital allocation. Welcome to new Fairfax - a compounding machine! Below is the math Please let me know if you see any errors (I have made one other two over the years).

-

With Fairfax’s equity holdings I think we are benefitting from a couple of things: Jockeys: Fairfax is partnering with outstanding CEO’s/founders/entrepreneurs - they have picked the right ones. Concentration: Fairfax continues to concentrate its portfolio around its best ideas/jockeys and has been for the past +5 years (buybacks should be included). Together, this one-two strategy is really juicing the returns of the investment portfolio. What they are doing makes sense… they have a $27 billion equity portfolio (valuing FFH-TRS at notional). And it is quickly growing in size. Fairfax has a small corporate office. Fairfax is executing exceptionally well these days. They are getting exceptional leverage from how they are investing in equities (the people factor and the unlimited upside factor). Very powerful when it is done well.

-

Here is some holiday cheer for Fairfax shareholders. With a week to go in Q4, Fairfax's equity portfolio is up about $900m (intraday Dec 23), with most of the gains in the MTM bucket ($25/share pre-tax). Fairfax's equity portfolio is having an outstanding 2025. Fairfax is firing on all cylinders - all aspects of the company are performing at a high level. Insurance. Investments. Capital allocation. Total shareholder return in 2025 is about 30%. This is after two back-to-back years of +50% returns. And the stock's valuation is still the cheapest among peers. Nuts!

-

The increase in Eurobank’s share price in 2025 has been the #1 single driver of value for Fairfax shareholders this year. It has been quite the move. And there have also been two dividend payments.

-

@glider3834 , it would be nice to see Fairfax's ownership position in Digit get simplified - lots of benefits moving forward. Thanks for sharing.

-

Yes, with hindsight, the equity hedge was the biggest issue. But Jan 1, 2017, Fairfax still had big problems. It was still shorting in a bog way. And its equity portfolio was littered with dogs. Here is how I think about it: Fairfax had three problems: 1.) Equity hedges 2.) Shorts 3.) Investment framework used for equities 1.) Equity hedges - 'fixed' end of 2016 (when it was removed) 2.) Shorts - 'fixed' end of 2020 (when last short was removed and Fairfax promising it would not happen again) 3.) Investment framework used for equities - 'fixed' around 2018 The first 2 were clean (all Fairfax had to do was exit the positions). The third has taken the company 8 years to 'fix'. The reverse takeover of Boat Rocker by Blue Ant this year was (hopefully) the final act (with a $109 million write-down in 2025). The dogs are gone. The queens/keepers (in the old portfolio) are rocking. New purchases (since 2018) are rocking. What Fairfax owns today (as a group) are a bunch of holdings that are very well managed, strong balance sheets, profitable with solid prospects. I have followed Fairfax since 2003. The equity portfolio (as a group) is higher quality (based on the 4 metrics I mentioned) than I have ever seen before. I think that is (primarily) by design not happenstance. Yes, other factors have had an impact - but that was the case 10 years ago too (and will be the case 10 years into the future). Other factors will always be a factor. I think the performance of Fairfax's equity portfolio in recent years is primarily because of the decisions/efforts of the management team over the past 8 years. As a result, I expect future results to continue to be strong (over time, with some volatility) - irrespective of the economic backdrop.

-

@TwoCitiesCapital , difference of opinion is what makes a market. Thanks for taking the time to share your thoughts. That is the value of this board.