Spekulatius

-

Posts

19,023 -

Joined

-

Last visited

-

Days Won

39

Content Type

Profiles

Forums

Events

Everything posted by Spekulatius

-

Let rename Intel US semiconductor: TSMC is going to be next. The government will get a stake in their US fabs. I mentioned Francois Mitterrand nationalizations in the early 80’s here before, but there was one big difference. France paid for the business they acquired a fair price (decided by a court), the US paid nothing, but retroactively changed the rules and gets equity stakes for formerly given grants. I guess to beat China, we have to become China.

-

$INTC Win win: Who is next?

-

Putin does not want to sit down with Zelensky and negotiate. It is not going to happen.

-

Odet is probably next because the float is so small. Bollore is in the process of eliminating Cambodge, Artois and Moncey and they all went for a premium, but not fair value. If you own this on a tax deferred account , you just cash out and buy into a surviving entity (Odet, Bollore) and rinse and repeat. Bollore has the largest float even though that went from 37% to ~30% too over the years as there were tender offer and buybacks. I think eventually the Bollore family will own it all, but it will be a while.

-

Newsom getting better at trolling too:

-

So What Exactly Is The "Short Homebuilders" Thesis At This Point

Spekulatius replied to Gregmal's topic in General Discussion

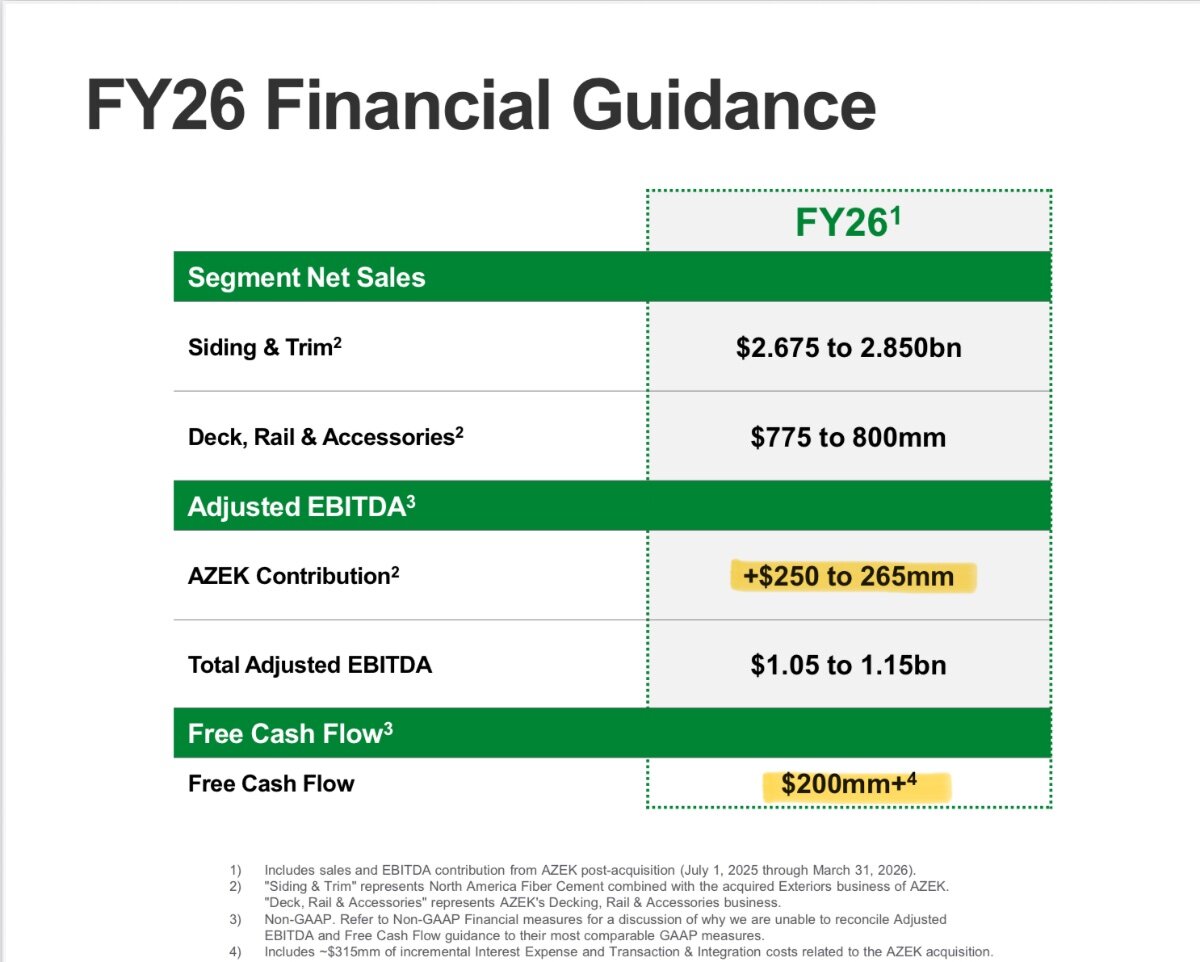

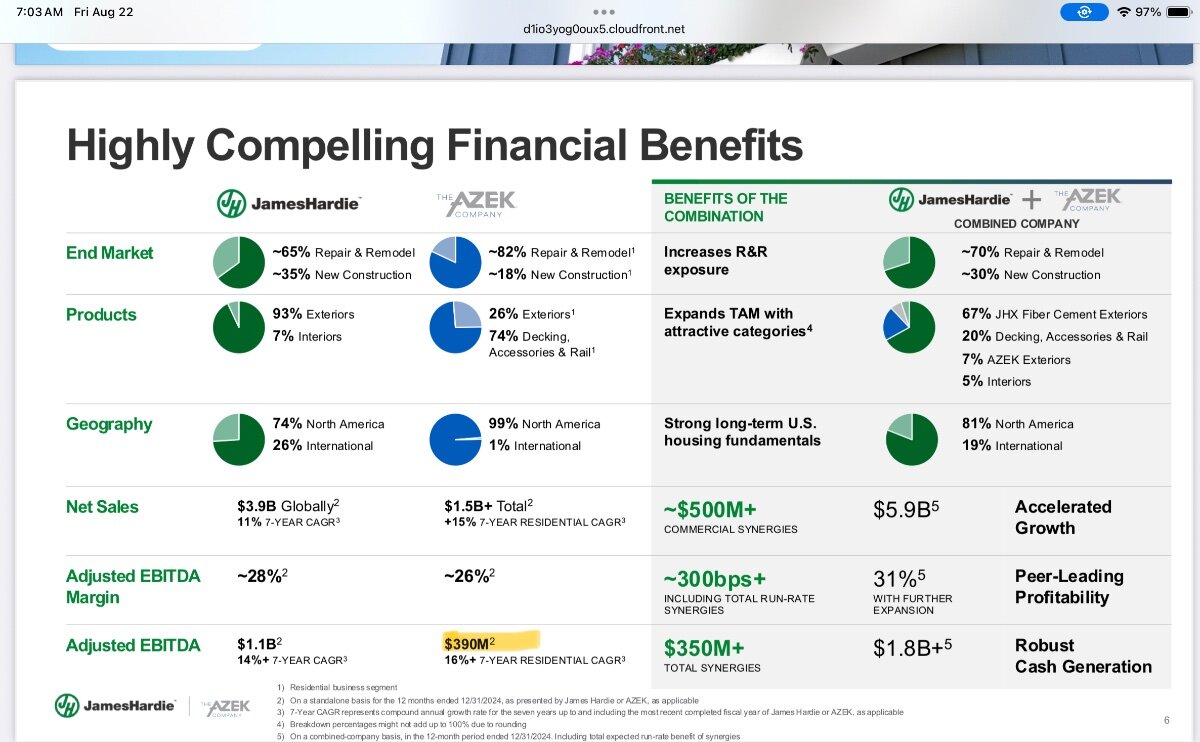

JHX - I went through the presentations and some of the filing and the numbers are insane. JHX acquired AZEK which makes deck related products and while that seems a great business also, they paid 21x adjusted EBITDA EBITDA. AZEK made $390M at $1.5B in revenue at a 26- EBITDA margins - not bad. They claimed to hieve ~500M in commercial synergies down the road, which would be 1/3 of Szek revenue base. How is this even remotely possible. Then 3 month later AZEK EBITDA now went to $250-$265M per Q1 2026. How is such a deterioration in such a short period of time possible? Besides that JHX cement board siding business has similar problems with rapidly shrinking re neues. looks to me like both AZEK and JHX were stuffing channels last and now have inventory coming out their ears. It’s really quite something. The most interring thing I learned is that the cement board business is insanely profitable, hence the former high valuation. Their EBIT margins were exceeding 32% in NA for cement board siding which is a product that has been around forever. They also disclose the margin for similar European business (gypsum is used in Europe, but otherwise similar ) and their EBIT margins were barely scratching 10%, which is what you expect in a competitive business. How can a commodity profit command 32% margins in one market and <10% in another. It’s not like cement where transportation costs dominate. While they play a role, the transportation costs are not that high. My guess is that this is one of those market where capitalism is broken and the industry managed to avoid competing with each other. I think it would be an interesting job for antitrust and FTC to find out how this happens, because you can tell by the results that there is something fishy going on. Its one of those things that makes building homes more expensive than it should so every homeowner, home renovators and by extension renter pays these guys a tribute in some way. I am sure there is an investment angle to all this but not sure why it is at this point . It’s not shorting homebuilders for sure. I put JHX on a watchlist but it’s not actionable at this point. LOX may be an interring one to watch as they transform from a lumber business into a siding business.

-

I have. Moctezuma - extremely illiquid. It’s essentially controlled by Buzzi, so I decided to buy some Buzzi instead. Bolsa Mexicans . earning have not done much for many years now. The reason is that the Mexican stock market is a backwater with terrible liquidity and also has not performed well. Nola’s is an old fashioned exchange that generates revenue from trading and more than half the revenue is custodian revenue, which depends on total market capitalization. Also, that business has shrinking margins. It’s more like custodian bank like BK than a modern exchange like CME, LSEG which are infrastructure business that sell a lot of adjacent services. I think Sheinbaum really should reform the Mexican stock market which seems to have outdated modus operanti but that may include introducing competition, which would not be great for Bolsa Mexicana.

-

Brand ambassador Lutnick bumbled this one- NVDA needs to negotiate better deal with a lower take rate than 15%: https://www.engadget.com/ai/china-reportedly-discouraged-purchase-of-nvidia-ai-chips-due-to-insulting-lutnick-statements-123055120.html

-

The Donbas looks the same than cities destroyed in WW2. Putin is just one notch above Hitler and Stalin. Both had an ideology they claimed to fight for, Putin doesn’t even have that.

-

You can read up the soft here. It’s a shame they never got the recognition they deserved until much later. https://www.nationalww2museum.org/war/articles/african-american-333rd-field-artillery-battle-of-bulge I guess as movie material, this was too controversial and Saving Private Ryan was better for the box office,

-

Europe, Japan, South America, Mexico is what know and like best. If I had access to, I would also look into Korea

-

Added WDAY AH

-

Yes, IBKR is great for Japan as @Paarslaars has noted.

-

Some interewting stats on a Russian energy exports: https://energyandcleanair.org/july-2025-monthly-analysis-of-russian-fossil-fuel-exports-and-sanctions/

-

Lichtenstein is the most successful warrior nation there is. They went to war to help out the Swiss a couple hundred years ago (I think in the 17 century ) with 12 men and came back with 13. Or so I have been told.

-

1 FC Kaiserslautern went to the second league a long time ago, but still found fans even in North Carolina:

-

I don’t care about Mexico in particular but I like to invest where I where I find interesting business trading at attractive valuations. Mexico is interesting because valuations were actually sky high before the GFC and even after and have moved continuously down since. At some point interesting opportunities get created in these circumstances,. I also think it’s a great time to diversify out of the US markets where I think governance has gotten worse while valuations are still sky high. I can live with iffy governance but I don’t like to pay up for it.

-

This is correct. Biden didn’t want to go down that route, Trump won’t and the European don’t push for it either. It’s a way to win against Putin and that was the question. A credible threat to act like it might work but Putin most likely will call the card and then the only way forward is to do what you said you are going to do. Trump already has done quite a few useless ultimatums (50 day, secondary sanctions, even threatened to bomb Moscow) that are all expired with zero consequences, so here we are. Putin has nobody to answer to, so he escalates as he see fits. As for who drops them bombs, I am guessing that Ukrainian pilots could do the job with some training. However, nobody want to hand over F-35 either, The F-16 are 30 year old tech and while they serve a purpose, they can’t take out the Russian air defense without risking to get shot down either. Ukraine would need many of those If we go down that route.

-

3836 Avant Group. Very encouraging results. https://data.swcms.net/file/avantgroup-corp/dam/jcr:4038374d-491e-45b9-a86b-c3dec7bd183c/140120250805530352.pdf If they make their 2028 targets, the stock would be a double without multiple expansion.

-

Anyone still following Femsa (FMX). I bought a few shares yesterday. This company has transformed by shedding the beer business (a good decision) and expanding convenience retail (acquisition of the European Valora business). What caught my attention was the expansion of the OXXO stores in Columbia and Brazil which seems to going well, albeit only a small base. Both market are significant compared to Mexican markets. They still own ~47% of KOF (Coke bottler) which had been doing alright. I have owned this in the past it alway tended to sell due to volatility and macro issues Mexico but it looks to me that the story has and continues to change for the better. That said, the macro issues in Mexico are still and issue (see that last quarterly report ) but FMX has a strong balance sheet and the business are fairly resilient. I think it’s one of the cheapest way to get in the convenience store space.

-

Negotiation is always preferable but Trump should put the threat on the table. If negotiations go nowhere follow through. You need a big stick to rule the unruly.

-

Ensure Ukraines air superiority. Everything else will follow if you can bomb the enemy at will from the air. It might require stealth fighters and bombers to take down the air defense systems initially , once those are done regular jets will do. If you can create a 50 mile deep no fly zone where no air defense exists and Russian fighter can around the front line, you can crate huge losses to the enemy with little losses to Ukraine and prevent any attack from even forming much less succeeding. I think if you win air superiority in this type of stale mate WW1 war can be won.

-

So What Exactly Is The "Short Homebuilders" Thesis At This Point

Spekulatius replied to Gregmal's topic in General Discussion

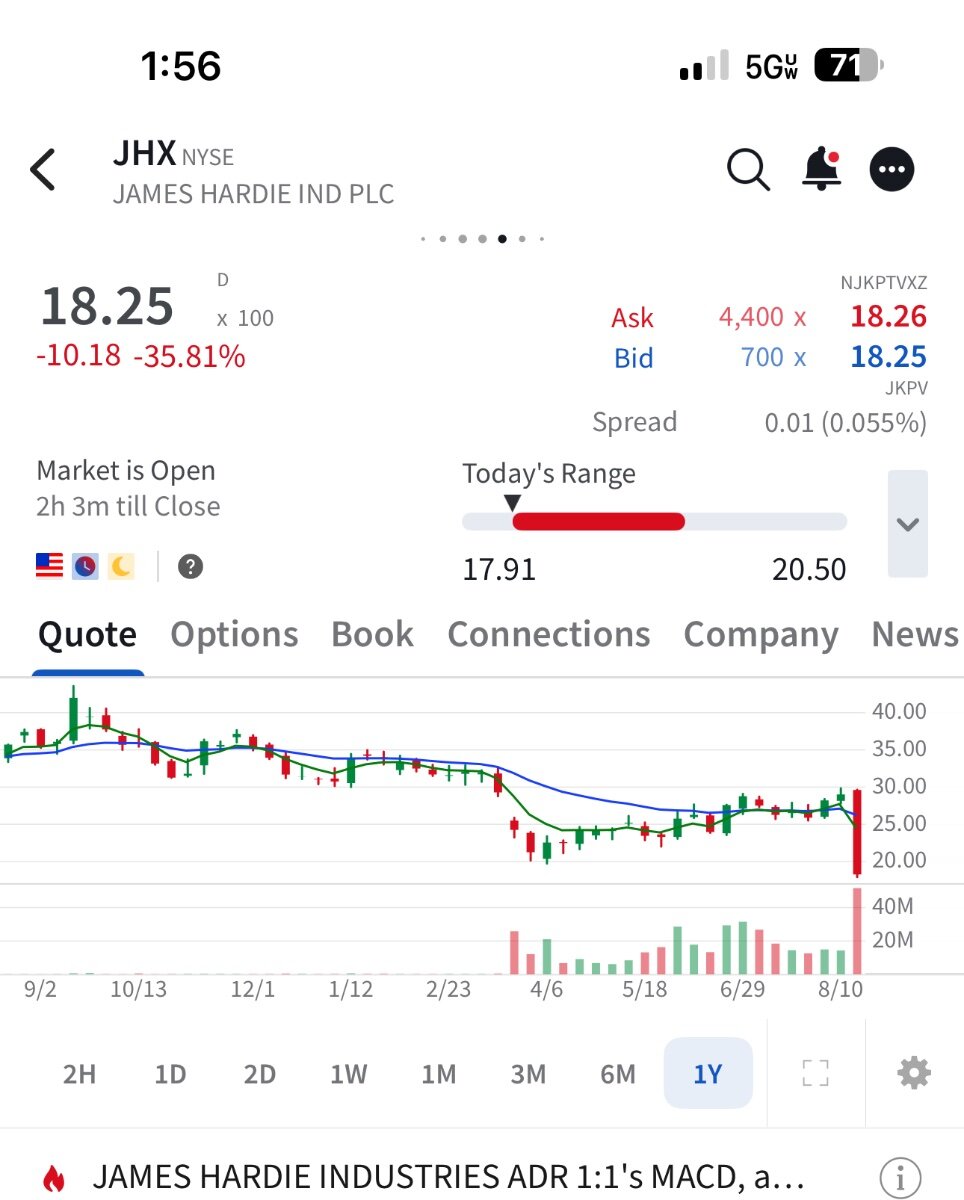

I had to laugh when I looked at JHX valuation (4.4x EV/revenues, 30x earnings) and their 35% drop today. What were people thinking paying up for this cement board siding business? Maybe I am missing something too but for sure the longs who owned this yesterday did.

-

This is going to be fun to watch: https://www.reuters.com/business/media-telecom/us-examines-equity-stake-chip-makers-chips-act-cash-grants-sources-say-2025-08-20/ Every company who can afford to do so will pay back the grants pronto. I think Europe and Japan in particular can really exploit this if they play this smartly.

-

Magas yard stick is broken. Countries like Denmark have chipped in and yet get criticized as bad allies and then there is this Greenland thing.